Autosamplers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 2.24 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autosamplers Market Analysis by Mordor Intelligence

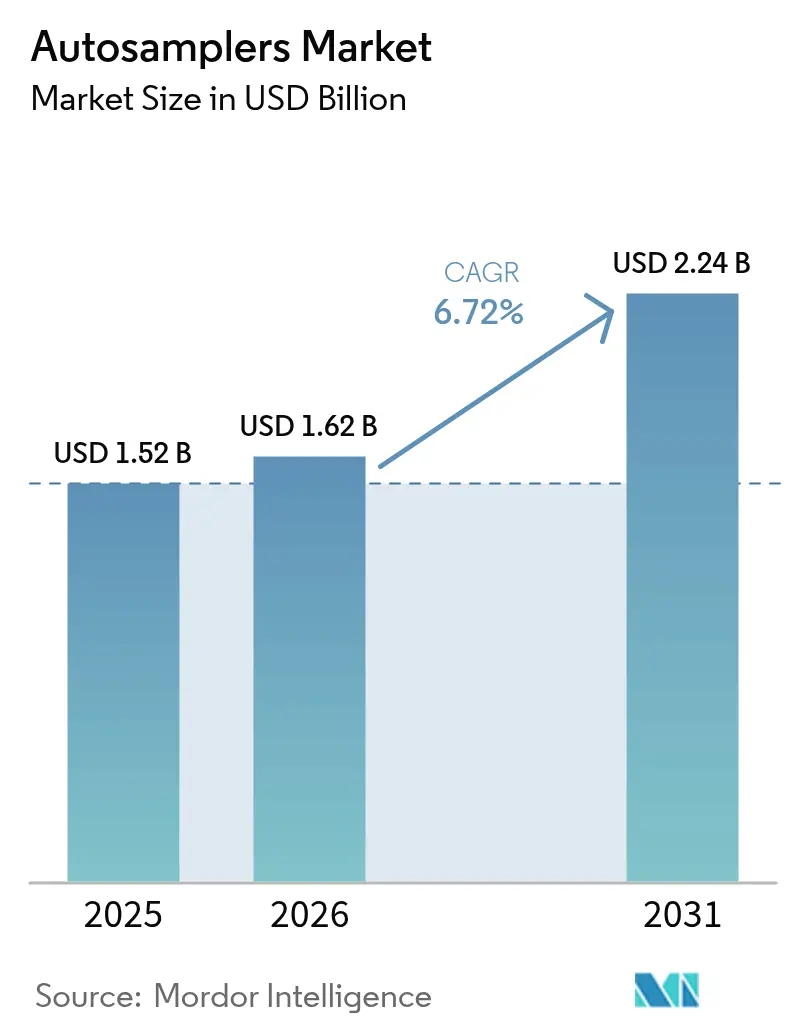

The Autosamplers market size is expected to grow from USD 1.52 billion in 2025 to USD 1.62 billion in 2026 and is forecast to reach USD 2.24 billion by 2031 at 6.72% CAGR over 2026-2031.

Strong replacement demand from pharmaceutical quality-control laboratories, together with growing environmental and food-safety testing volumes, sustains steady equipment revenues. Regulatory bodies such as the FDA now require detailed analytical method validation, prompting laboratories to adopt automated sample-injection platforms that eliminate operator variability and safeguard data integrity. Vendors also benefit from continuous upgrades toward AI-ready autosamplers that predict maintenance needs and reduce unplanned downtime. Heightened scrutiny of PFAS compounds in water supplies, pesticide residues in produce, and impurities in new chemical entities further widens the application base, pushing the autosamplers market toward higher throughput and improved sensitivity. Ongoing capital investment in Asia Pacific manufacturing sites positions developing nations as critical future volume drivers for high-capacity systems.

Key Report Takeaways

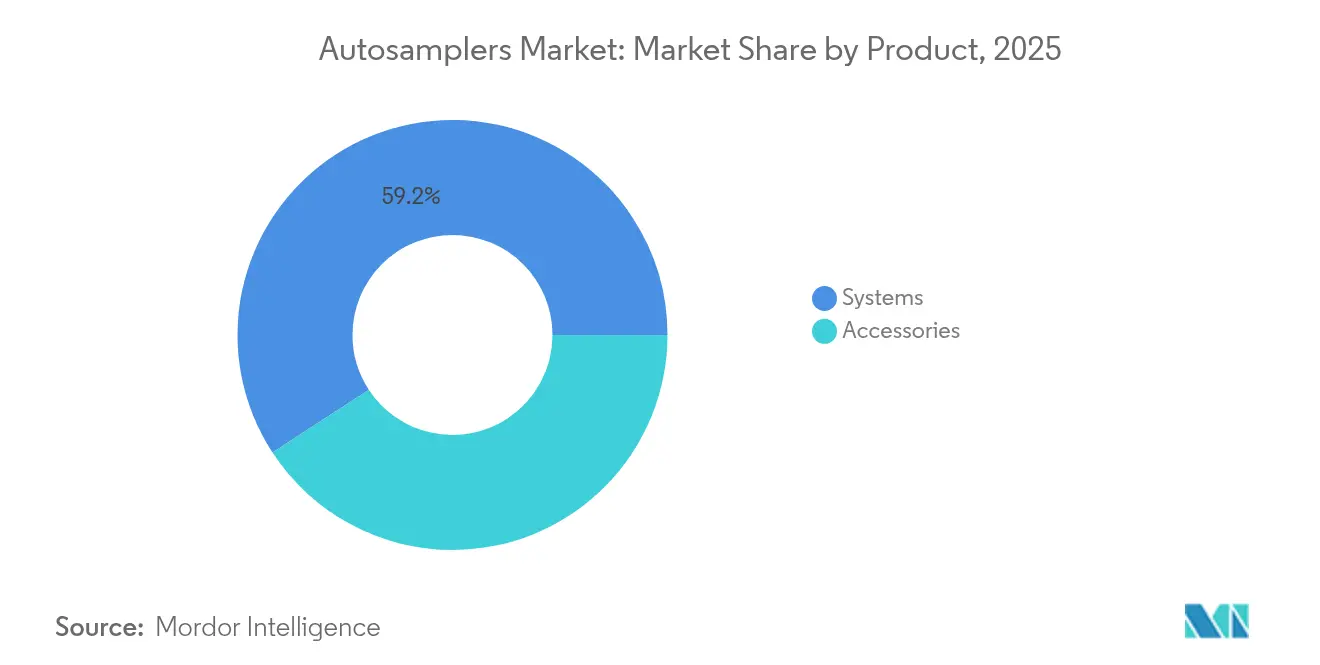

- By product category, systems held 59.21% of autosamplers market share in 2025; headspace and SPME autosamplers are forecast to expand at a 10.12% CAGR through 2031.

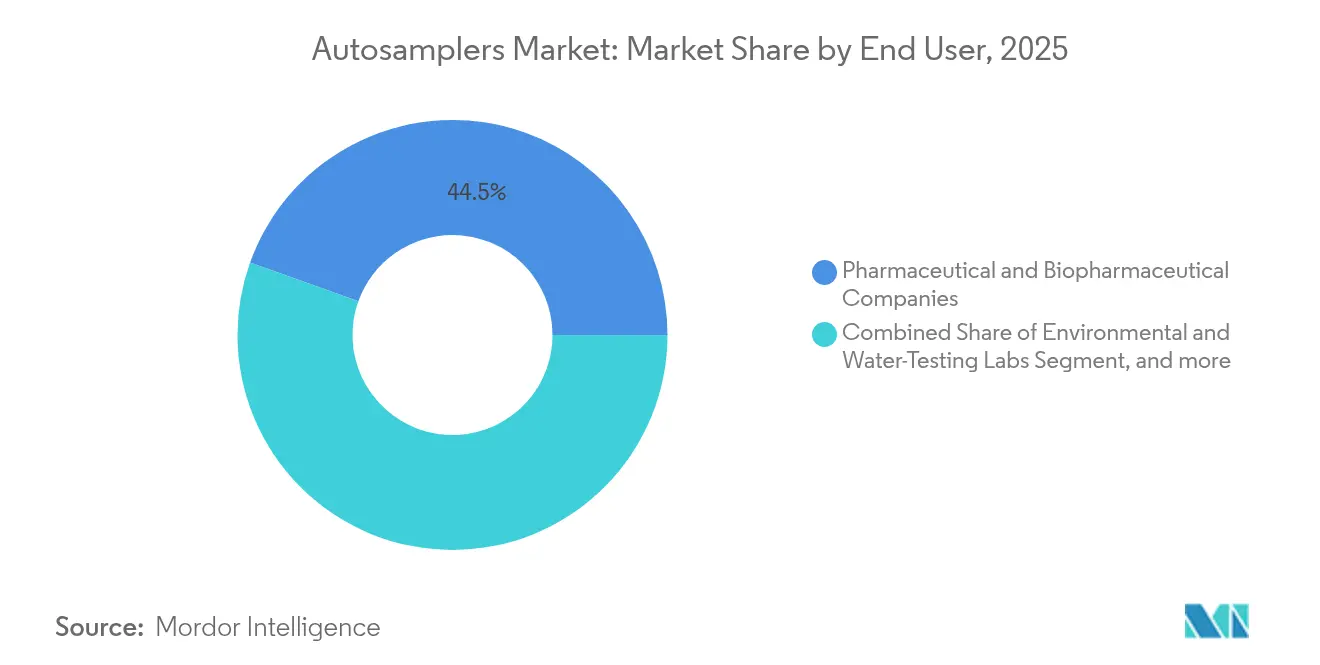

- By end user, pharmaceutical and biopharmaceutical companies captured 44.53% of the autosamplers market size in 2025, while academic and contract research laboratories will advance at an 11.05% CAGR between 2026 and 2031.

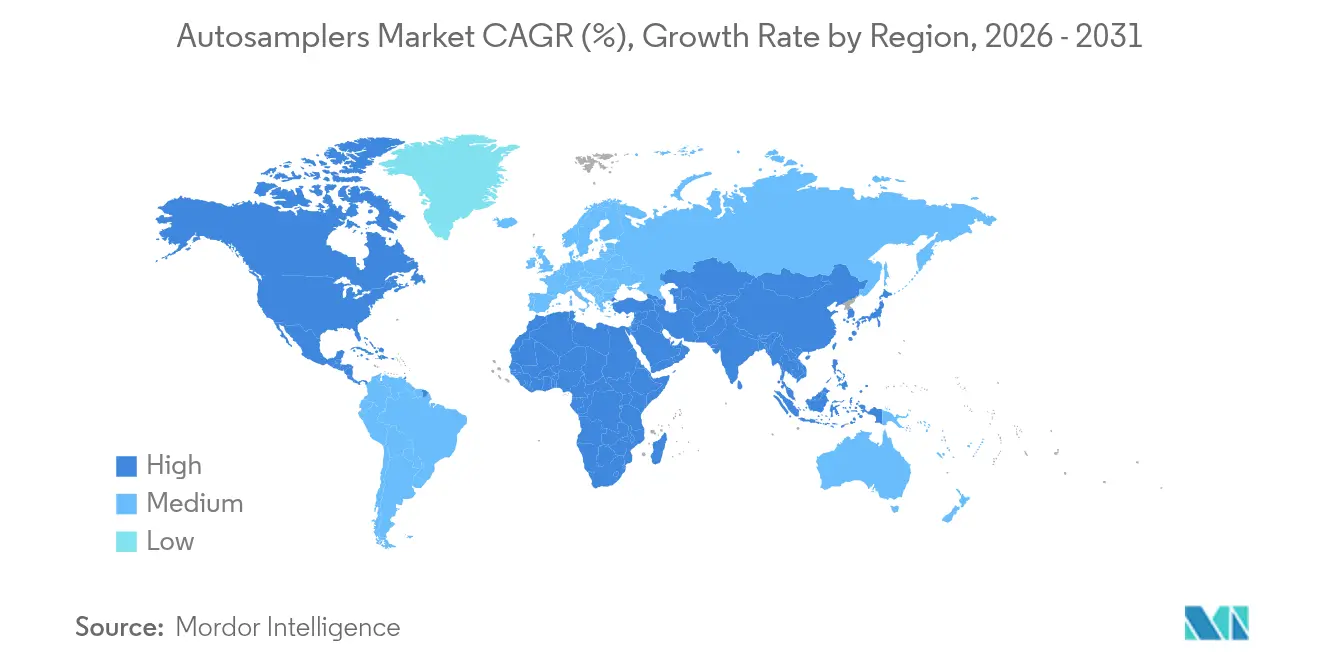

- By geography, North America accounted for 36.92% of the autosamplers market size in 2025; Asia Pacific records the fastest regional CAGR at 11.6% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Autosamplers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancing role of chromatography in drug approval workflows | +1.8% | North America & EU | Medium term (2–4 years) |

| Tighter global food-safety & environmental regulations | +1.2% | EU & North America | Short term (≤ 2 years) |

| Lab-automation push for higher analytical throughput | +1.5% | APAC core, spill-over to North America | Medium term (2–4 years) |

| Expansion of omics-driven clinical diagnostics | +0.9% | North America & EU expanding to APAC | Long term (≥ 4 years) |

| AI-enabled predictive-maintenance autosamplers | +0.7% | Developed markets | Long term (≥ 4 years) |

| Green-chemistry micro-volume injection designs | +0.6% | EU, followed by North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Advancing Role of Chromatography in Drug Approval Workflows

The FDA now mandates tighter controls on analytical method robustness, and that shift forces biopharma companies to automate sample handling to comply with data-integrity expectations.[1]“Analytical Procedures and Methods Validation,” FDA, fda.gov Automated autosamplers minimize human error, thereby ensuring reproducibility across global manufacturing networks. Centralized digital audit trails created by integrated sampling platforms accelerate dossier assembly for regulatory submissions. Complex biologic molecules demand multi-lane chromatography sequences, which are only practical with unattended autosampler operation. Biosimilar developers adopt identical strategies to prove comparability, extending demand across both novel and follow-on therapeutics. In consequence, the autosamplers market secures stable volumes from every late-stage development program moving through the pipeline.

Tighter Global Food-Safety & Environmental Regulations

EU Farm-to-Fork objectives and updated US drinking-water standards for PFAS impose lower detection limits that conventional manual injection cannot meet.[2]“High-Sensitivity Water Testing,” ELGA LabWater, elgalabwater.com Food and environmental laboratories therefore integrate autosamplers capable of processing dense sample batches while holding low carry-over. Contract testing organizations upgrade platforms to win regulatory tenders, driving replacement purchases every three to five years. Equipment vendors embed flexible racks that accept diverse container types, allowing a single unit to address both environmental and food matrices, which improves utilization. Multinational retailers, now subject to supplier-verification rules, demand certified laboratory partners, reinforcing capital cycles. These intertwined pressures add incremental growth to the autosamplers market across agriculture, water, and packaging industries.

Lab-Automation Push for Higher Analytical Throughput

Global supply-chain time pressures convert around-the-clock laboratory operation from aspiration into necessity. Modern autosamplers cut manual injection steps by as much as 60% and link directly with LIMS, enabling chain-of-custody assurance during overnight runs. CROs and contract manufacturers cite asset-utilization gains of 25% after installing robotic samplers, which boosts revenue without increasing headcount. Vendors now ship self-calibrating needle assemblies that reset after every batch and alert technicians only when deviation occurs. System scheduling software allocates urgent regulatory samples ahead of routine QC work, optimizing queue times. These tangible productivity benefits underpin continuous upgrades that support the autosamplers market across every high-volume analytical laboratory.

Expansion of Omics-Driven Clinical Diagnostics

Proteomics and metabolomics workflows hinge on nanogram-level precision that manual injection cannot deliver consistently. Clinical research groups therefore integrate autosamplers with ultra-high pressure liquid chromatography-mass spectrometry systems, gaining both throughput and traceability.[3]Waters Corporation, “UHPLC-MS Applications in Clinical Research,” waters.com Companion-diagnostic developers roll out identical setups across study sites to standardize biomarker readouts, lifting multinational demand. Liquid-biopsy testing expands sample types to plasma, saliva, and cerebrospinal fluid, necessitating versatile injection formats. Autosamplers fitted with disposable cartridges avoid cross-contamination in biohazardous matrices, a feature now specified in procurement tenders. Hospitals in Japan and South Korea already pilot such units, signifying broader Asia Pacific adoption during the forecast window. These clinical shifts feed a new vertical that enlarges the autosamplers market beyond traditional chemistry labs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of chromatography-skilled operators | -0.8% | APAC & emerging markets | Short term (≤ 2 years) |

| High capex & budget limits at SME labs | -1.1% | Cost-sensitive markets | Medium term (2–4 years) |

| Stringent validation & compliance timelines | -0.6% | North America & EU | Medium term (2–4 years) |

| Fragmented IP & patent-litigation risks | -0.4% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Chromatography-Skilled Operators

Many senior analysts retire faster than universities can train replacements, pushing laboratories to depend on fewer specialists. The skills gap complicates method-development projects that still require expert oversight even after automation. Small laboratories often postpone autosampler purchases because they cannot guarantee local support for troubleshooting. Equipment suppliers now bundle remote diagnostics and certified training to mitigate the talent deficit, yet onboarding still delays utilization by several months. Asia Pacific nations feel the shortage most acutely due to rapid laboratory expansion outstripping educational capacity. This workforce imbalance suppresses a portion of latent demand in the autosamplers market until operator pipelines stabilize.

High Capex & Budget Limits at SME Labs

Advanced autosampler platforms list between USD 50,000 and USD 500,000, a range that strains capital budgets in academic and small commercial laboratories. Total cost of ownership grows further with service contracts, consumables, and software licenses. Leasing reduces upfront cost but often locks laboratories into longer terms, raising lifecycle expenses. Budget constraints encourage second-hand acquisitions, yet older units may lack AI or green-chemistry features requested by regulators and sponsors. Funding agencies rarely cover full hardware upgrades, forcing investigators to split grants across competing priorities. These financial realities temper short-term expansion of the autosamplers market, particularly in developing economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Systems Dominate Through Platform Integration

Integrated autosampler systems secured 59.21% of autosamplers market share in 2025 as laboratories favored turnkey combinations that align mechanically and electronically with chromatography instruments. Liquid chromatography models lead volume shipments because HPLC and UHPLC remain the backbone of pharmaceutical release testing. Gas chromatography systems maintain relevance in petrochemical forensics and environmental VOC monitoring, while dual-mode designs support both techniques within one chassis. Continuous firmware updates now enable remote calibration that cuts maintenance calls by 20%, ensuring uptime for validated production lines. The complementary accessories subsegment vials, syringes, temperature-control blocks drives recurring sales that cushion vendors against equipment-cycle swings. Green-chemistry variants with micro-volume injection reduce solvent use by 40%, an attractive metric for sustainability-focused laboratory managers. Over the forecast horizon, headspace and SPME platforms expand fastest at a 10.12% CAGR through 2031, propelled by global rules on aromatic hydrocarbon and organophosphate residues in food and soil. These growth dynamics preserve top-line momentum and broaden the autosamplers market.

Consumables and modular upgrades also lift average selling prices across installed bases. High-capacity racks that hold 1,000 microtiter vials support cell-culture metabolite screening at biotech firms, replacing manual sample batching. AI-driven needle health diagnostics now predict seal wear, triggering just-in-time ordering of replacement parts and reducing unexpected downtime. Vendors actively cross-sell de-ionized water filtration units and in-line degassers, embedding themselves as single-source suppliers for entire analytical workcells. This bundling strategy reinforces customer retention and amplifies lifetime revenues per instrument. Sustained innovation across core systems and accessories therefore underpins a healthy autosamplers market size during the coming decade.

By End User: Pharmaceutical Leadership Faces Academic Challenge

Pharmaceutical and biopharmaceutical manufacturers commanded 44.53% of autosamplers market size in 2025 owing to strict FDA and EMA compliance rules that embed automation throughout drug-development lifecycles. These companies install multi-plate barcode readers and temperature-controlled carousels to support hygroscopic API testing. Batch-release timelines in continuous-manufacturing facilities tolerate no manual injection delays, further entrenching automation. Industry 4.0 initiatives integrate autosamplers with manufacturing execution systems so that analytical feedback loops adjust process parameters in real time. At the same time, in-house bioanalytical groups measure antibody drugs in serum, demanding low-volume, high-precision samplers equipped with anti-carry-over coatings.

Academic and contract research laboratories record the highest growth at an 11.05% CAGR to 2031 as grant agencies prioritize translational projects requiring pharmaceutical-grade analytics. Universities increasingly operate fee-for-service core facilities that mirror CRO workflows, thereby purchasing advanced autosamplers to attract external projects. Flexible financing arrangements, including pay-per-analysis models, lower the barrier to entry for smaller institutes. Environmental agencies and water-testing labs also invest steadily as PFAS limits tighten worldwide, feeding multisector utilization that enlarges the autosamplers market. Collectively, these user segments ensure broad demand diversity that shields vendors from cyclicality in any single industry.

Geography Analysis

North America retained 36.92% of autosamplers market size in 2025 because of deep pharmaceutical pipelines, NIH research grants, and active EPA enforcement of contaminant rules. US laboratories adopt AI-enhanced autosamplers early, citing productivity gains that justify premium pricing. Canadian biotech clusters in Toronto and Vancouver accelerate purchases for genomic medicine trials, while Mexican near-shore plants align analytical methods with US import regulations. Vendor service networks and same-day consumables delivery sustain high uptime across the region.

Asia Pacific posts a 11.6% CAGR through 2031, the fastest worldwide, as China and India expand formulation and active-ingredient manufacturing to capture global outsourcing contracts. Government subsidies in Shenzhen and Hyderabad offset up to 30% of automation capital costs, catalyzing multi-line deployments. Domestic instrument makers partner with leading brands to co-develop low-price variants, expanding reach into county-level environmental bureaus. South Korea and Japan emphasize clinical-diagnostic automation for precision-medicine initiatives, thereby diversifying regional demand. The combined momentum redefines the autosamplers market as a truly global arena rather than a legacy Western niche.

Europe records steady growth driven by REACH chemical regulations and the Farm-to-Fork strategy that mandates rigorous monitoring of pesticide residues. German chemical giants retrofit legacy QC labs with solvent-saving autosamplers to hit corporate carbon targets. The United Kingdom continues parallel compliance with EU analytical directives post-Brexit, preserving investment continuity. Eastern European CRO clusters in Poland and the Czech Republic leverage cost advantages to win bioequivalence studies, fueling additional equipment orders. Middle East & Africa and South America follow with gradual adoption, constrained by financing gaps and technical-skills shortages yet supported by expanding petrochemical and food-export sectors. Overall, geography trends collectively strengthen the autosamplers market trajectory toward diversified regional sales.

Regulatory Landscape

Regulation for autosamplers is largely determined by how and where the equipment is used. In pharmaceutical QC and other regulated analytical labs, adoption is shaped by FDA and EMA expectations for analytical method validation and data integrity. Where autosampler-enabled workflows are used in clinical diagnostics, the testing setup can fall under medical device controls when integrated into IVD or clinical test systems.

In the United States, the FDA issued a final rule on May 6, 2024 to phase out enforcement discretion for Laboratory Developed Tests (LDTs). Stage 2 begins May 6, 2026, and adds requirements tied to device registration, listing, and labeling for laboratories offering LDTs, which tightens compliance expectations around instrumented workflows that generate reportable clinical results. On quality and safety compliance, FDA’s Quality Management System Regulation (QMSR) incorporates ISO 13485:2016 by reference, aligning quality system expectations for manufacturers that supply autosampler-containing systems into regulated clinical settings. For electrical and operational safety of automatic and semi-automatic laboratory equipment, IEC 61010-2-081:2019 provides a common technical anchor used in conformity and procurement specifications, including requirements relevant to programmable functions, interlocks, and biohazard markings. Taken together, these frameworks push vendors and laboratories toward standardized documentation, traceable software and audit trails, and validated unattended sampling configurations, particularly when test results support regulatory submissions or clinical decision-making.

Competitive Landscape

The autosamplers market features moderate concentration, with Agilent Technologies, Thermo Fisher Scientific, Waters Corporation, and Shimadzu Corporation holding a dominant combined presence. These firms supply complete workflows that bundle samplers, chromatographs, and data-systems under consolidated validation packages, simplifying procurement for regulated laboratories. Recent product cycles introduce predictive-maintenance dashboards that alert users before seal failure, increasing perceived value and switching costs. Strategic alliances with AI software firms accelerate proprietary scheduling algorithms that cut cycle times.

Mid-tier specialists like CTC Analytics AG and GERSTEL GmbH carve out niches in headspace and thermal desorption applications, respectively. They emphasize modular retrofits compatible with legacy instruments, offering laboratories incremental automation paths. Patent filings reveal intensified activity in low-volume metering and microfluidic valve technology, indicating future differentiation via solvent economy and sample integrity. Larger incumbents frequently acquire these innovations; PerkinElmer’s 2024 purchase of an environmental sampler start-up exemplifies this tactic. Price competition remains subdued in the premium segment yet rises in entry-level models where Chinese manufacturers gain share through localized support.

Service contracts now represent up to 35% of lifecycle revenue for top vendors, highlighting the shift from one-time hardware margins to recurring analytics-as-a-service models. Remote-diagnostics portals reduce on-site visits by 40%, cutting costs for both supplier and customer. In emerging regions, distributors bundle financing with training, bridging skill gaps while cementing brand loyalty. This multilevel strategy allows established players to guard share while capturing incremental volume, ensuring sustained health for the autosamplers market.

Autosamplers Industry Leaders

Restek Corporation

Agilent Technologies, Inc.

Gilson Inc.

Bio-Rad Laboratories Inc.

PerkinElmer Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is emerging at the intersection of throughput expansion and unattended operation in regulated laboratories. Higher sample volumes from pharmaceutical QC, PFAS monitoring, and food-safety testing favor autosamplers that integrate closely with chromatography data systems and LIMS, while reducing operator touchpoints. Thermo Fisher’s Vanquish Duo UHPLC and associated Vanquish Sample Hub (May 2026) is one signal of this direction, pointing to parallelized analysis and extended walkaway capacity (additional well-plate handling). This reinforces demand for autosampler architectures that support high-capacity plate and vial formats, reliable temperature control, and low carry-over across long runs.

A second opportunity is to broaden accessible automation for emerging and cost-sensitive labs that still need traceability and repeatability. This demand shows up in Asia Pacific expansion programs and in CRO or university core facilities. Product activity such as Annuo’s AS-3016B multifunctional liquid autosampler (March 2026) underscores competitive space for modular, retrofit-friendly samplers with defined positional repeatability and standardized interfaces that can modernize legacy LC stacks without full system replacement. Over the regulatory cycle, the FDA’s LDT final rule milestones through 2026 and the EU’s move toward joint clinical assessments for high-risk technologies place additional weight on documentation, software transparency, and post-market discipline. That environment supports vendors that package validated workflows, cybersecurity-ready connectivity, and service models designed to keep systems compliant over multi-year instrument lifecycles.

Recent Industry Developments

- May 2026: Agilent Technologies launched the 8890B and 8860B gas chromatograph systems featuring GC Assist for automated monitoring, troubleshooting, and remote connectivity. The release supports the market shift toward intelligent instrumentation that reduces downtime and maintains consistent data quality across long, unattended analytical sequences, increasing pull-through for compatible autosampler configurations and service software.

- March 2026: Restek Corporation announced a supply relationship with BrightSpec to manufacture SpectrAline Cartridges, a new family of preconcentration columns for Molecular Rotational Resonance (MRR) spectroscopy, with ordering availability beginning in June 2026. The partnership expands specialized sample introduction and preparation options, reinforcing vendor focus on integrated front-end workflows where autosampling, preconcentration, and traceable handling determine analytical sensitivity and reproducibility.

- October 2024: Agilent Technologies announced the launch of its next-generation Infinity III LC autosampler with AI-powered predictive maintenance capabilities, supported by a USD 15 million R&D investment to reduce unplanned downtime. The launch sharpened competitive differentiation around software-enabled reliability and lifecycle serviceability, raising baseline expectations for validated laboratories that depend on high uptime and audit-ready automated injection.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers autosamplers used to automatically introduce liquid or gas samples into analytical instruments, mainly in chromatography and related lab workflows. The market is sized in revenue terms across common lab and industrial testing settings.

Scope exclusions: We exclude the core analytical instruments themselves (such as chromatographs or detectors), along with general lab automation robots that are not purpose-built autosamplers.

Segmentation Overview

- By Product

- Systems

- Liquid Chromatography Autosamplers

- Gas Chromatography Autosamplers

- Headspace & SPME Autosamplers

- Accessories

- Systems

- By End User

- Pharmaceutical & Biopharmaceutical Companies

- Environmental & Water-Testing Labs

- Academic & Contract Research Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundaries of what counts as an autosampler and to map the main demand pools that keep purchasing steady year to year. Public sources such as FDA and EPA lab testing guidance, NIH funding trends, USP and ISO testing standards, and customs or trade statistics for analytical instruments and accessories helped us align the model with real-world testing intensity.

We also reviewed manufacturer product catalogs, investor presentations, annual reports, and trusted press coverage to understand product positioning, replacement cycles, and typical attach rates with chromatography systems. In a few places, we referenced paid subscriptions for company financials and intelligence, plus patent databases, to validate technology direction and revenue mix signals. These sources are illustrative only, and many other public and proprietary references were used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with instrument channel partners, lab managers, and product and commercial leaders to confirm adoption patterns for autosamplers across pharma and biotech labs, environmental and water-testing labs, food testing, and other routine analytics users. We also used the inputs to tighten price bands, service and accessory attachment assumptions, and the timing of upgrade demand across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | APAC: 46% |

| Mid tier: 50% | Functional/Unit leaders: 32% | EMEA: 35% |

| Smaller Players: 15% | Managers: 54% | Americas: 19% |

Market-Sizing & Forecasting

Market sizing was built using a top-down approach where lab testing demand and instrument utilization signals are used to reconstruct the annual spend that typically flows into autosampling. To keep the logic practical, we anchor the demand pool using indicators such as chromatography installed base growth, regulated testing intensity in pharma quality control and environmental monitoring, lab automation adoption, and replacement and upgrade cycles that are common in routine analytical labs.

The total is then corroborated through selective bottom-up approximations, including sampled price by configuration (system versus accessory heavy bundles), channel checks on shipment direction, and a limited supplier roll-up for the most visible revenue blocks. Where direct volume clues were thin, gaps were handled through conservative attach-rate ranges that were cross-verified with interview inputs and then normalized by region.

Forecasting used scenario analysis supported by trend views from primary respondents, and it was tied to a small set of drivers that can be refreshed each year. The most used inputs include biopharma manufacturing expansion, outsourcing to contract labs, environmental and water-testing workloads, and expected ASP movement from features like higher throughput and better compliance support.

Data Validation & Update Cycle

Validation is done through multiple passes that check whether the final value aligns with independent market signals, including instrument demand trends, lab testing volumes, and directional revenue disclosures from key suppliers. When an outlier shows up at a region, product, or end-user level, the assumptions are re-tested, and experts are re-contacted if the variance is material.

Before sign-off, a separate analyst reviews the build for logic breaks, unit consistency, and currency conversion timing so the story matches the numbers. Reports are refreshed annually, and interim updates are triggered when major regulatory shifts, capacity expansions, or demand shocks change the likely path. Right before delivery, we do a final data pass so clients receive the latest updated view.

Mordor Intelligence's Autosamplers Market Size Measured Against Other Published Estimates

Published market sizes for autosamplers can look different even when they sound like they are covering the same product group, since the included revenue items and year choices are not always aligned. Differences also come from how firms treat accessories, service attachment, and the way regional splits are converted into a single USD total.

Installed-base direction for chromatography systems, routine lab testing workloads, and interview-backed ASP bands are the evidence points that keep Mordor Intelligence's USD 1.62 B (2026) estimate tied to autosamplers sold into active analytical workflows. In other estimates, the spread is often driven by a different base year, broader lab automation bundling, or a less explicit treatment of accessories versus standalone systems.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.62 B (2026) | |

| Global Consultancy A | USD 1.53 B (2025) | Uses a 2025 base and a longer forecast window, and the scope appears to be closer to end-user spend reporting, which can compress or expand totals depending on how accessories and service bundles are treated. |

| Industry Publisher B | USD 1.66 B (2025) | Anchors the model to 2024 to 2025 values with a lower growth path, and the segment breadth is broader, which can pull in adjacent automation functionality that is not always separated as autosamplers only. |

Across the three figures, the most visible drivers of difference are the base year used and how cleanly the scope separates autosamplers from nearby lab automation spending. By keeping assumptions tied to observable demand signals and by re-checking price and attachment logic with respondents, the final number stays traceable and repeatable when the model is refreshed.

Key Questions Answered in the Report

What is the current autosamplers market size?

The autosamplers market size equals USD 1.62 billion in 2026 and is projected to reach USD 2.24 billion by 2031.

Which region holds the largest share of the autosamplers market?

North America leads with 36.92% share in 2025 due to its mature pharmaceutical infrastructure and stringent regulatory standards.

Which product category is expanding fastest?

Headspace and SPME autosamplers register the highest growth at a 10.12% CAGR through 2031, propelled by volatile-compound testing in food and environmental labs.

Who are the key players in the autosamplers market?

Agilent Technologies, Thermo Fisher Scientific, Waters Corporation, and Shimadzu Corporation collectively dominate global revenues, supported by broad product portfolios and service networks.

What factors restrain adoption in smaller laboratories?

High capital costs, ongoing maintenance expenses, and a shortage of trained chromatography operators limit uptake among small and medium-sized laboratories.

How is AI influencing the autosamplers industry?

AI-enabled predictive maintenance and smart scheduling reduce downtime and increase throughput, delivering measurable productivity gains that encourage equipment upgrades.

Page last updated on: