Automotive Torque Converter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 29.07 Billion |

| Market Size (2031) | USD 34.61 Billion |

| Growth Rate (2026 - 2031) | 3.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Torque Converter Market Analysis by Mordor Intelligence

The Automotive Torque Converter Market size was valued at USD 28.07 billion in 2025 and estimated to grow from USD 29.07 billion in 2026 to reach USD 34.61 billion by 2031, at a CAGR of 3.55% during the forecast period (2026-2031). The measured headline pace belies a deep transition as hybrid powertrains, multi-speed automatics, and rising commercial-vehicle production reshape demand patterns. Automatic-transmission adoption in emerging economies keeps baseline volumes rising, while developed regions channel investment toward hybrid-dedicated converter architectures that improve fuel economy and emissions performance. Supply-chain near-shoring in North America, continued light-commercial expansion after the pandemic, and OEM pressure for eight- and ten-speed gearboxes add further momentum. Conversely, pure battery-electric drivetrains and the growing popularity of DCT and CVT technologies temper long-term outlooks in some passenger-car segments. Raw-material cost swings in aluminum and copper inject additional uncertainty into component margins.

Key Report Takeaways

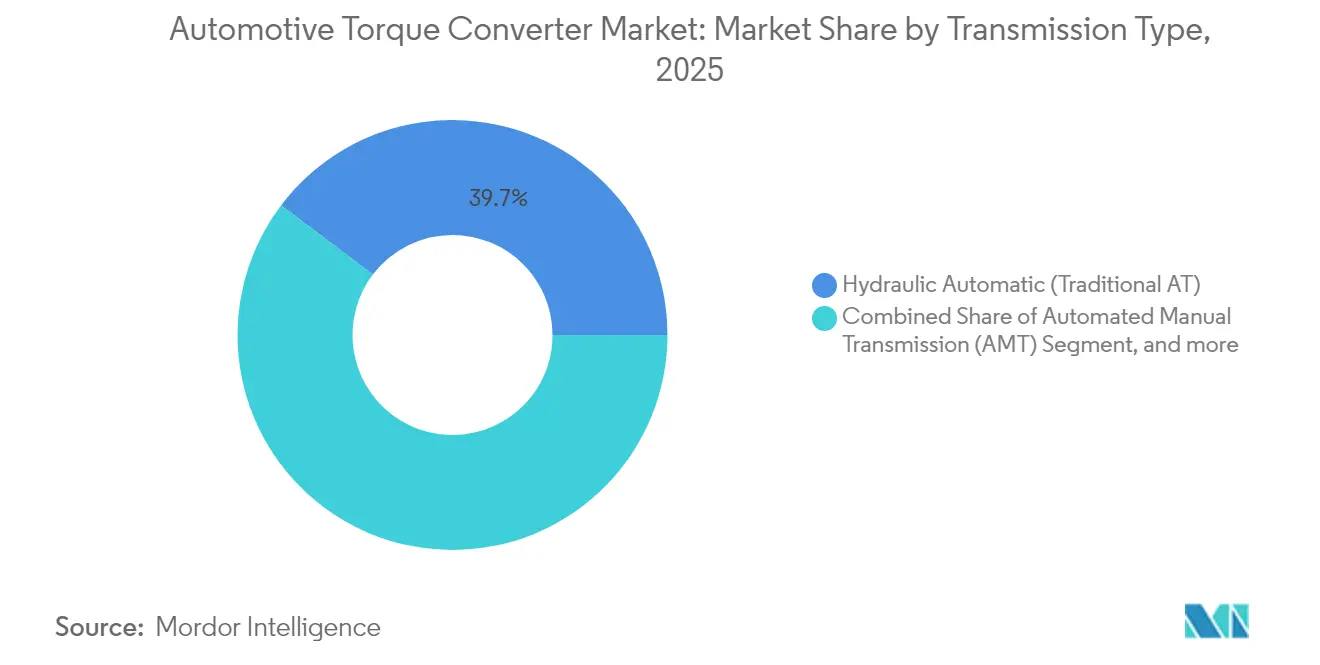

- By transmission type, hydraulic automatics retained 39.68% of the automotive torque converter market share in 2025, while hybrid-dedicated automatics are set to advance at a 10.35% CAGR through 2031.

- By vehicle type, passenger vehicles led with 63.12% of the automotive torque converter market revenue share in 2025; light commercial vehicles exhibit the fastest growth at an 8.05% CAGR to 2031.

- By component, pump assemblies accounted for 37.19% of the automotive torque converter market size in 2025, whereas lock-up clutch systems will expand at a 8.92% CAGR to 2031.

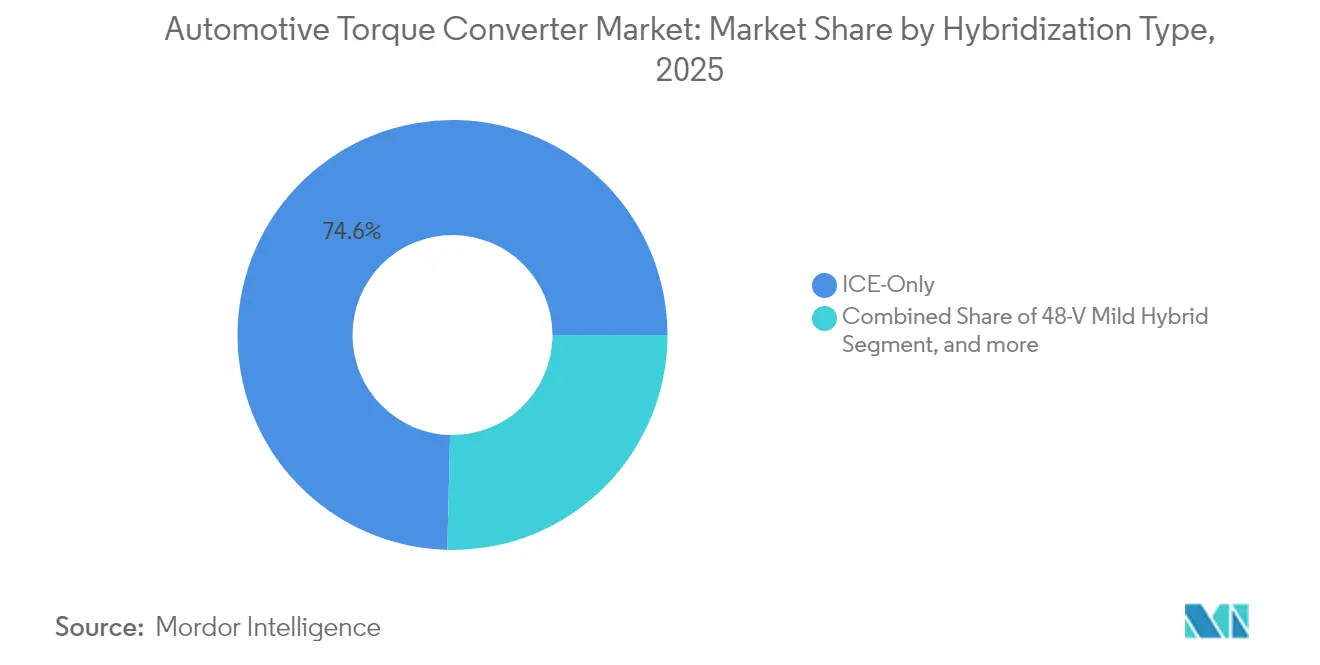

- By hybridization level, ICE-only applications held a 74.62% share of the automotive torque converter market in 2025; plug-in hybrids are forecast to post the highest 11.94% CAGR to 2031.

- By sales channel, OEM supply commanded 84.05% of the automotive torque converter market share in 2025, while the aftermarket is projected to grow at 7.12% CAGR as vehicle lifecycles lengthen.

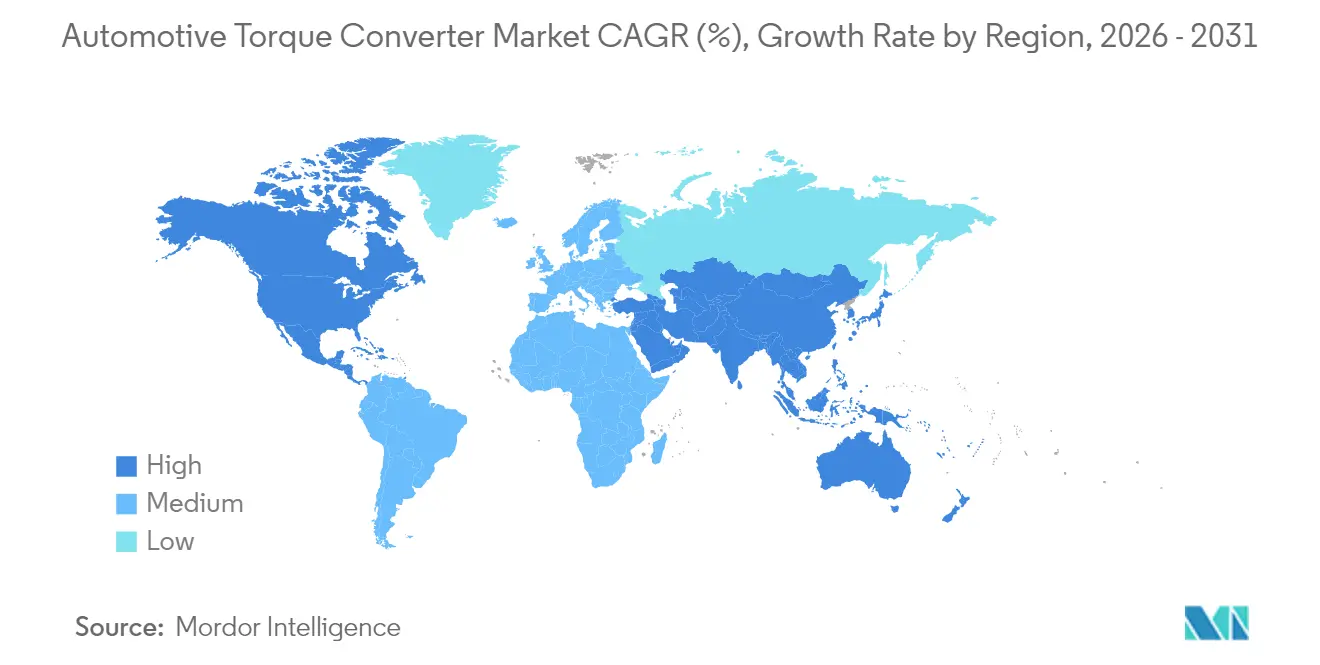

- By geography, Asia-Pacific captured 38.35% of the automotive torque converter market share in 2025 and is set to grow at 7.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Torque Converter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring Automatic-transmission Penetration In Emerging Markets | +1.2% | Asia-Pacific, Latin America | Medium term (2-4 years) |

| Hybrid And Mild-hybrid Boom Drives Lock-up Torque-converter Demand | +0.8% | Global, with concentration in Europe & China | Short term (≤ 2 years) |

| OEM Pressure For 8-/10-speed Fuel-efficiency Upgrades | +0.6% | North America, Europe | Medium term (2-4 years) |

| Recovery Of Global Light-commercial Production Post-covid | +0.4% | Global | Short term (≤ 2 years) |

| Next-gen High-temperature ATF Fluids Enable Higher Stall Torque | +0.3% | Global | Long term (≥ 4 years) |

| NVH Regulations Spur Advanced Multi-damping Converter Designs | +0.2% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring Automatic-Transmission Penetration in Emerging Markets

Escalating urban congestion and rising disposable incomes sharply increase automatic-transmission uptake in large developing nations. China’s automatic transmission is shifting millions of vehicles from manual to automatic transmission solutions. Similar momentum is visible in India, where Renault’s competitively priced Kiger CVT places a fully automatic option within sub-10-lakh budgets, eroding the long-standing manual bias.[1]“Renault’s CVT strategy reshapes India’s budget car market,”, Autocar Professional, autocarpro.inScale effects follow: as local volumes grow, unit costs fall, unlocking further penetration. Allison Transmission’s USD 100 million expansion in Chennai aims to double output by 2027, demonstrating supplier commitment to this demand wave. Regional champions such as Shaanxi Fast Auto Drive Group leverage entrenched manufacturing bases to capture incremental orders across commercial and passenger segments.

Hybrid & Mild-Hybrid Boom Drives Lock-up Torque-Converter Demand

Hybrid powertrains require converters with refined lock-up mechanisms that minimise slip during engine-off phases and enable seamless torque blending. Ford’s Ranger PHEV places an e-motor and separator clutch ahead of the converter, highlighting new integration layouts that increase lock-up duty cycles. ZF’s plug-in hybrid transmission for BMW’s X5 xDrive40e replaces conventional converters with integrated motors, yet still demonstrates how hydraulic coupling principles evolve in electrified systems, cutting fuel use by up to 70%. Stellantis already fields 30 European hybrid models, each deploying electrified dual-clutch transmissions that deliver a 20% CO₂ cut. As hybrids bridge the affordability gap to full BEVs, the automotive torque converter market benefits from sustained lock-up component innovation.

OEM Pressure for 8-/10-Speed Fuel-Efficiency Upgrades

More gear ratios demand compact, low-inertia converters and smarter hydraulic controls. Mercedes-Benz’s 9G-TRONIC reaches 92% hydraulic-circuit efficiency via advanced oil-supply architecture, claiming 54% of its drivetrain fuel-saving potential.[2]“Mercedes-Benz details efficiency gains of 9G-TRONIC,”, Green Car Congress, greencarcongress.com Mazda’s SKYACTIV-Drive raises lock-up engagement from 64% to 88% of operations, demonstrating the integral role of converters in multi-speed optimisations. PACCAR’s TX-8 shows parallel advances on the commercial side, offering first-gear lock-up and 5% better fuel economy. As OEMs chase official cycle targets and real-world savings alike, converter suppliers must deliver precision manufacturability and control-software compatibility to secure program awards

Recovery of Global Light-Commercial Production Post-COVID

E-commerce growth keeps last-mile fleets expanding, and driver shortages raise demand for automatic transmissions that reduce fatigue. Allison’s new 4440 series, standard on Hino Profia FS snow-removal trucks, showcases tailored torque converters that simplify seasonal heavy-duty tasks.[3] “Allison unveils 4440 series for Japan’s snow-removal trucks,” , AT Press, atpress.ne.jp Similar logic underpins Allison’s deal with Lingong Heavy Machinery, where converters deliver high-torque starts for 136 t mining dump trucks under extreme load. Regulatory pushes for cleaner logistics add urgency: operators view automatic gearboxes paired with hybrid or alternative-fuel powertrains as the quickest route to compliance without sacrificing uptime.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEV Drivetrains Eliminate Torque Converters | -0.9% | Global, concentrated in Europe & China | Medium term (2-4 years) |

| Rising DCT/CVT Share In Compact Cars | -0.5% | Asia-Pacific, Europe | Short term (≤ 2 years) |

| Volatile Aluminum & Copper Prices Inflate BOM Cost | -0.3% | Global | Short term (≤ 2 years) |

| E-clutch Modules Replacing Converters In Dedicated Hybrids | -0.2% | Europe, North America | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

BEV Drivetrains Eliminate Torque Converters

Pure electric vehicles use direct motor drive, sidelining traditional converters. BorgWarner’s pivot to electric torque-vectoring modules for Polestar SUVs illustrates incumbent diversification away from hydraulic components. However, infrastructure gaps and battery costs keep hybrids and ICEs prevalent in emerging markets, softening the restraining effect until after 2030.

Rising DCT/CVT Share in Compact Cars

Cost-efficient CVTs and fast-shifting DCTs erode converter automatics in fuel-economy sensitive B- and C-segment cars. JATCO’s Guangzhou plant alone ships 1 million CVT units a year, representing 20% of global CVT output and underscoring scale economics. Dana’s beltless VariGlide CVT and Punch Powertrain’s VT5 for crossovers raise durability while lowering weight, making them attractive alternatives. Mazda’s converter-less eight-speed automatic with multi-plate clutches matches manual shift feel, proving consumers will accept new architectures when performance aligns

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transmission Type: Hybrid Systems Drive Innovation

Hybrid-dedicated automatics are forecast to grow 10.35% annually, while hydraulic automatics still held 39.68% of the automotive torque converter market share in 2025. The dual structure means converters must span legacy ICE duty and new hybrid cycles, where frequent engine restarts test lock-up durability. OEMs such as ZF embed electric motors into eight-speed boxes, retaining a slimmed hydraulic coupling that smooths engine engagement and absorbs torsional spikes. Automated manuals linger in specialised heavy-duty fleets because fuel efficiency outweighs shift quality, whereas CVTs gain ground in cost-constrained small cars. Over the period, converters supporting integrated e-clutch modules will capture incremental value even as pure hydraulic units plateau because hybrids dominate mid-price electrification offerings.

Hybrid transmission growth compels suppliers to redesign pumps for lower parasitic drag and develop multi-mode lock-ups that engage under electrically assisted low-torque conditions. Converter casings migrate toward high-strength steels and clad aluminium to manage added heat from rapid clutch cycling. Software integration becomes critical as torque hand-off between motor and engine intensifies. Tier-ones that provide complete hydraulic controls alongside hardware retain pricing power, while stand-alone converter makers face margin pressure. The automotive torque converter market therefore rewards firms able to validate hybrid-ready designs quickly for global platforms.

By Vehicle Type: Commercial Segments Accelerate Adoption

Passenger cars dominated revenue with a 63.12% of the automotive torque converter market share in 2025, yet light commercial vehicles are growing fastest at an 8.05% CAGR. Urban freight, food delivery, and e-commerce logistics prioritise automatic gearboxes that cut driver fatigue in stop-start routes. Fleet managers focus on total cost of ownership, boosting demand for converters paired with eight-speed boxes that promise fuel savings without steep acquisition costs. In emerging markets, ride-hailing services also push for automatic transmissions that appeal to younger drivers unfamiliar with manuals. Conversely, premium European passenger-car buyers increasingly choose hybrids or BEVs where traditional converters may be absent, creating a nuanced demand balance.

Heavy commercial vehicles, though the smallest subgroup, require bespoke high-capacity converters that withstand extreme torque and high thermal loads. Due to range and power density constraints, applications such as mining haulage or municipal snow removal are resistant to full electrification. Allison’s latest series offers first-gear lock-up and twin torsional dampers, delivering smoother launches and reducing clutch wear. Such attributes encourage operators to shift from manuals despite higher upfront costs. The automotive torque converter market therefore benefits from commercial-segment resilience even as passenger-car electrification accelerates.

By Component: Lock-up Systems Lead Innovation

Pump assemblies controlled 37.19% of the automotive torque converter market revenue in 2025, yet lock-up clutches will expand at 8.92% CAGR as efficiency regulations tighten. Most future gains hinge on extending lock-up activation across broader speed maps, which lifts real-world consumption results without wholesale powertrain redesign. Mercedes-Benz’s 9G-TRONIC proves the concept, attributing more than half its savings to hydraulic-system refinements alone. Advanced friction materials and variable-damping designs now mitigate shudder during early engagement, a capability essential for hybrids where frequent engine restarts previously hampered comfort.

Electric auxiliary pumps emerge as a complementary growth pocket because they trim parasitic drag when mechanical demand is low. Meanwhile, turbine and stator blades see slower value growth as design maturity curbs differentiation. Converter suppliers increasingly bundle integrated temperature sensors, speed pickups, and control valves, linking mechanical parts to transmission ECUs for adaptive strategies. As hybrid adoption rises, components that manage thermal spikes and reverse torque flow during regenerative braking secure higher attachment rates. This shift realigns profit pools within the automotive torque converter market toward smart sub-assemblies rather than bulk castings.

By Hybridization Level: Plug-in Hybrids Surge

ICE-only drivelines held 74.62% of the automotive torque converter market size in 2025, but plug-in hybrids head the growth league at a 11.94% CAGR. This split reflects varied global charging infrastructure: emerging economies lean on mature internal combustion supply chains, whereas regulators in Europe, China, and parts of North America incentivise plug-ins as a bridge to full electrics. The converter’s role differs by architecture. Mild-hybrid 48-V systems largely preserve conventional units, yet software extends lock-up operation and adds idle-stop features. Full and plug-in hybrids sometimes replace converters with e-clutches; however, many OEMs still rely on compact hydrodynamic couplings for smooth engine re-engagement, especially in larger vehicles.

Converter makers adapt housings for axial-flux motors or incorporate separator clutches near the impeller to secure access to upcoming model cycles. Thermal management is important because electric-only periods cool the fluid, and engine restarts generate rapid temperature changes. Integrating heat exchangers or active fluid heaters into converter casings becomes a differentiator. Even if BEVs erode share beyond 2031, the intervening decade of hybrid growth anchors a sizeable opportunity set inside the automotive torque converter market.

By Sales Channel: Aftermarket Complexity Increases

OEM channels controlled 84.05% of the automotive torque converter market share in 2025, but the replacement market will grow at 7.12% CAGR as vehicles stay on the road longer. Sophisticated converters with integrated electronics reach end-of-life later and require specialised tools for service, tilting business toward authorised networks. Independent rebuilders respond by forming alliances with tier-one suppliers to secure parts and diagnostic data. Hybrid models entering the maintenance cycle need lock-up assemblies capable of higher engagement counts, shifting the aftermarket demand mix toward premium components.

Software pairing between the transmission ECU and the replacement converter adds complexity. Some OEMs lock calibrations, steering customers back to franchised workshops. Nonetheless, value-oriented fleets in Latin America and Southeast Asia maintain an appetite for remanufactured units when downtime trumps perfect shift quality. The evolving channel balance ensures continued volume diversity within the automotive torque converter market, but suppliers must offer service data packages and training to capture post-sale revenues.

Geography Analysis

Asia-Pacific held 38.35% of the automotive torque converter market revenue in 2025 and should grow 7.08% per year to 2031, supported by China’s ascent as the top vehicle exporter and sustained commercial-vehicle demand. Local champions such as Shaanxi Fast Auto Drive Group broaden converter portfolios for hybrid trucks, while Japan supplies cutting-edge CVT output via JATCO’s one million-unit Guangzhou plant. India’s accelerating automatic-transmission uptake, highlighted by Allison’s Chennai capacity doubling, further cements the region’s central role. Cost-competitive manufacturing and deep supply chains make APAC the nexus of global sourcing for mature hydraulic and new hybrid converter designs.

North America presents a mixed landscape: high baseline automatic penetration keeps unit volumes solid, yet electrification pushes converters into more specialised niches. Commercial-vehicle segments remain robust as urban freight fleets seek reliability upgrades over manual gearboxes, and OEMs such as PACCAR integrate fuel-saving lock-up features across eight-speed boxes. Europe’s stringent CO₂ rules quicken the pivot toward hybrids and BEVs. ZF’s plug-in hybrid units for BMW models exemplify the region’s leadership in integrating electric motors inside transmissions, sustaining converter demand in progressively evolved forms. Both markets illustrate how regulation simultaneously restrains and reshapes the automotive torque converter market rather than eliminating it outright.

South America, the Middle East, and Africa trail on automatic-transmission penetration yet promise catch-up demand as urbanisation deepens. Local assembly to bypass import tariffs gains momentum, with tier-ones scouting joint ventures for cost-sensitive offerings. Fleet operators in Brazil and the Gulf increasingly choose automatic gearboxes for driver retention and uptime, even where road-fuel subsidies persist. Although small today, these regions complement mainstream revenue centres and diversify geographic risk for converter suppliers.

Competitive Landscape

Market concentration remains moderate as established firms defend their share with technology breadth while regional specialists chip away at cost tiers. ZF Friedrichshafen posted EUR 41.4 billion sales in 2024 despite an 11% dip, yet its integrated powertrain strategy that couples converters with control electronics underpins stickiness among premium OEMs.[4]“ZF Group Annual Report 2024,”, ZF, press.zf.com BorgWarner’s evolution toward electric torque-vectoring modules for Polestar BEVs shows incumbents pivoting to adjacent technologies to hedge converter volume risk. Aisin Corporation delivered CNY 4,909.5 billion FY2024 revenue, up on strong take-rates for hybrid transmissions and electric drive units that reuse converter manufacturing know-how, macrotrends.

M&A tightens competitive fields. Schaeffler’s acquisition of Vitesco Technologies targets EUR 600 million annual synergies by 2029, combining e-motor, inverter, and hybrid geartrain competence into one house. Vertical integration offers scale economies in precision machining and friction-material development vital for next-generation lock-up clutches. Niche champions, meanwhile, chase rugged off-highway opportunities: Allison Transmission pairs converters with control logic tuned for 136-ton mining trucks and snow-removal fleets, where electrification pressures are muted. Regional manufacturers in China leverage low-cost casting capacity to win on price, particularly for legacy four- and six-speed boxes still prevalent in export-focused production runs.

Success hinges on balancing incremental efficiency improvements with long-term electrification bets. Players investing in thermally optimised casings, active fluid management, and software-defined shift strategies preserve relevance even if pure hydraulic volumes flatten. Conversely, firms tied solely to commodity cast components risk erosion as OEMs demand integrated mechatronics. The automotive torque converter market, therefore, rewards R&D agility, diversified product roadmaps, and proximity to growing APAC assembly hubs.

Automotive Torque Converter Industry Leaders

Aisin Corporation

ZF Friedrichshafen AG

BorgWarner Inc.

Jatco Ltd.

Schaeffler AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Mahindra Automotive Australia has unveiled the XUV 3XO SUV, offering it in two variants: the AX5L and AX7L. This SUV boasts a TCMPFi turbo-gasoline engine, producing 82 kW of power and 200 Nm of torque. It's mated to a 6-speed Aisin torque converter automatic transmission. Notably, the engine comes with enhanced vehicle management software and advanced intelligent turbocharging.

- June 2025: Toyota unveiled its latest Land Cruiser Hybrid 48V in Europe. The Hybrid 48V system seamlessly integrates the Land Cruiser's 2.8-litre engine and 8-speed automatic gearbox with an electric motor, power converter, and a 48V lithium-ion hybrid battery.

- October 2024: Allison Transmission has made a significant investment of over USD 100 million to enhance its Chennai facility, a move that will effectively double its global capacity for automatic transmissions. This ambitious expansion is set to reach full operational capacity by 2027, positioning the company to meet increasing demand and reinforce its leadership in the automotive industry.

Global Automotive Torque Converter Market Report Scope

A torque converter is a type of fluid coupling that transfers rotating power from a prime mover, like an internal combustion engine, to a rotating driven load. In a vehicle with an automatic transmission, the torque converter connects the power source to the load. It is usually located between the engine's flex plate and the transmission. The equivalent location in a manual transmission would be the mechanical clutch.

The Automotive Torque Converter Market is segmented by Transmission Type. Vehicle Type and Geography. By Transmission type, the market is segmented into AMT, DCT, CVT, and Others. By Vehicle Type, the market is segmented into Passenger Vehicles and Commercial Vehicles, and By Geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle-east and Africa. For each segment, market sizing and forecast have been done on the basis of a value (in USD billion).

| Automated Manual Transmission (AMT) |

| Dual-Clutch Transmission (DCT) |

| Continuously Variable Transmission (CVT) |

| Hydraulic Automatic (Traditional AT) |

| Hybrid Dedicated AT (e-Torque Converter) |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Pump |

| Turbine |

| Stator |

| Lock-up Clutch |

| ICE-Only |

| 48-V Mild Hybrid |

| Full/Strong Hybrid |

| Plug-in Hybrid |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Transmission Type | Automated Manual Transmission (AMT) | |

| Dual-Clutch Transmission (DCT) | ||

| Continuously Variable Transmission (CVT) | ||

| Hydraulic Automatic (Traditional AT) | ||

| Hybrid Dedicated AT (e-Torque Converter) | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| By Component | Pump | |

| Turbine | ||

| Stator | ||

| Lock-up Clutch | ||

| By Hybridization Level | ICE-Only | |

| 48-V Mild Hybrid | ||

| Full/Strong Hybrid | ||

| Plug-in Hybrid | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive torque converter market?

The market stands at USD 29.07 billion in 2026 and is projected to reach USD 34.61 billion by 2031.

Which region leads the automotive torque converter market?

Asia-Pacific dominates with 38.35% revenue share in 2025 and a 7.08% CAGR outlook through 2031.

Why are lock-up clutches attracting investment?

They expand converter efficiency by engaging over a wider speed range, driving a 8.92% CAGR and meeting stricter fuel-economy rules.

What role does the aftermarket play?

Although OEM channels hold 84.05% share, the aftermarket grows 7.12% annually as longer vehicle life and hybrid complexity boost replacement part requirements.

Page last updated on: