Automotive Temperature Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

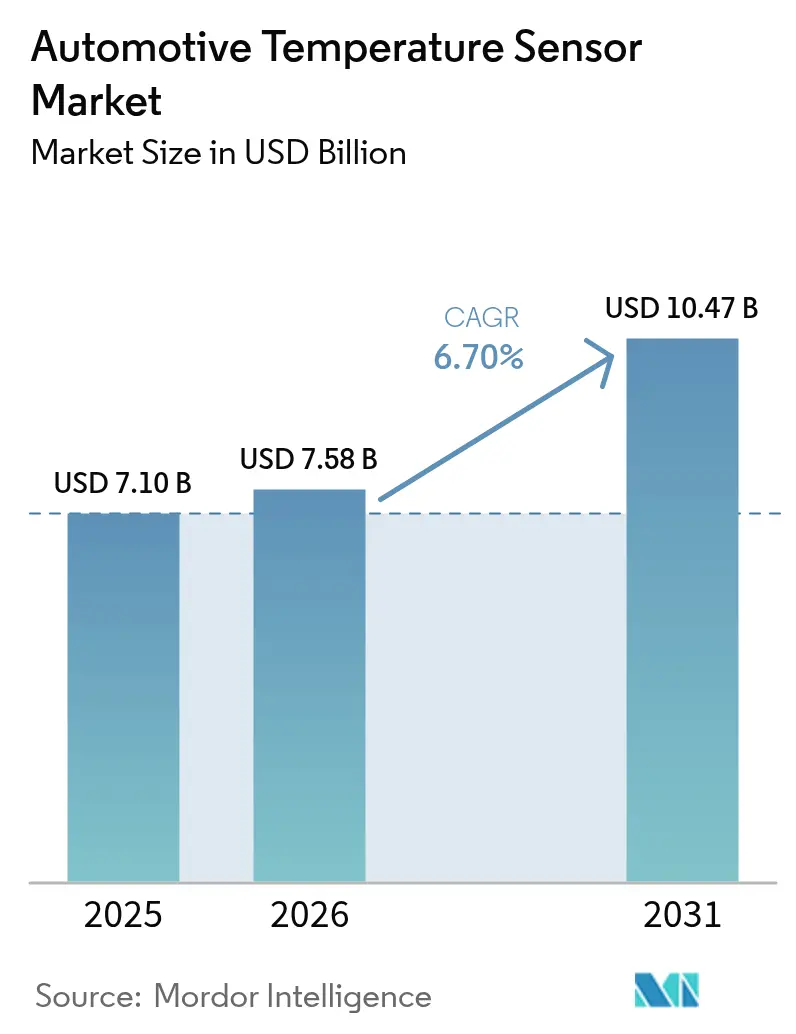

| Market Size (2026) | USD 7.58 Billion |

| Market Size (2031) | USD 10.47 Billion |

| Growth Rate (2026 - 2031) | 6.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Temperature Sensor Market Analysis by Mordor Intelligence

The automotive temperature sensor market size was valued at USD 7.1 billion in 2025 and estimated to grow from USD 7.58 billion in 2026 to reach USD 10.47 billion by 2031, at a CAGR of 6.70% during the forecast period (2026-2031). Growth is anchored by rapid electrification, with battery-electric vehicles (BEVs) installing close to 150 sensing points per car, nearly triple the requirement in combustion platforms. Zonal electronic architectures are compressing wiring looms and pushing demand for multi-point measurement nodes that can report through automotive Ethernet. High-voltage 800 V drivetrains built around silicon-carbide (SiC) inverters need precision sensors that remain stable above 600 °C, while EU7 and China VI-b regulations widen exhaust temperature monitoring windows as internal-combustion models sunset. Cabin health features in premium trims, solid-state battery pilots, and the migration to wafer-level sensor packaging are catalyzing additional volume in both OEM and service channels.

Key Report Takeaways

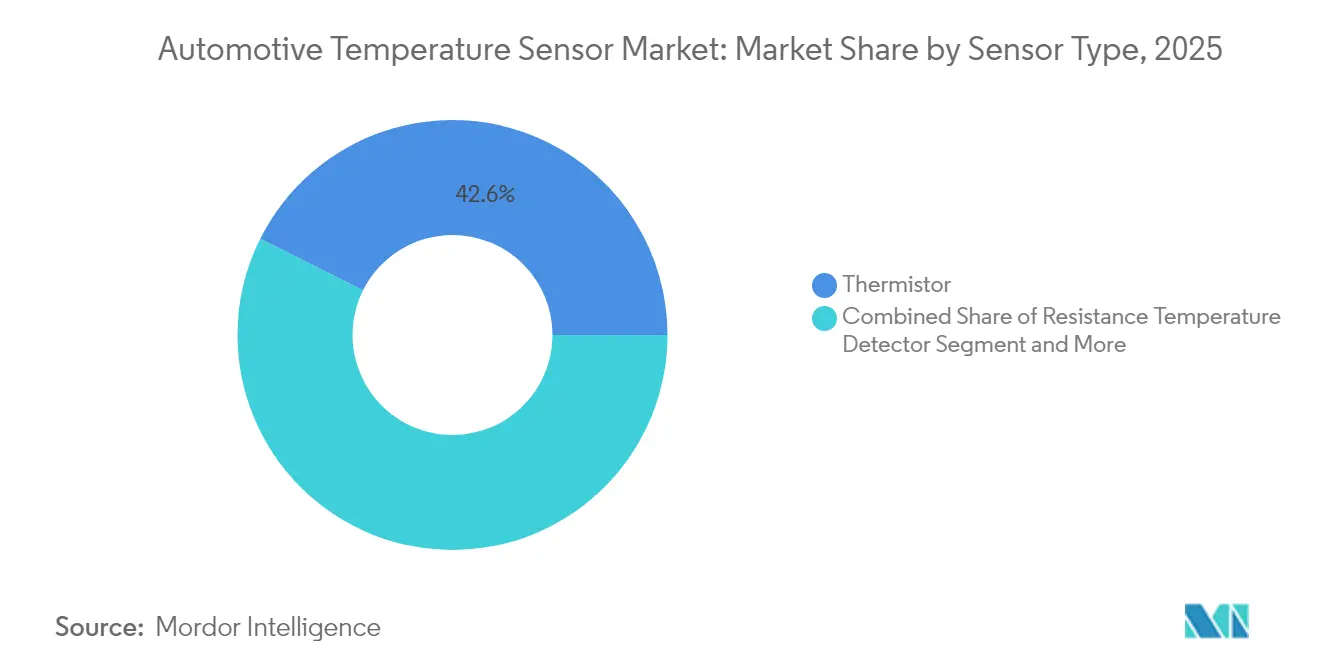

- By sensor type, thermistors led with 42.62% of automotive temperature sensor market share in 2025; semiconductor IC sensors are projected to expand at an 8.66% CAGR through 2031.

- By vehicle type, passenger cars captured 67.94% revenue share in 2025, while BEVs are forecast to grow at a 10.12% CAGR.

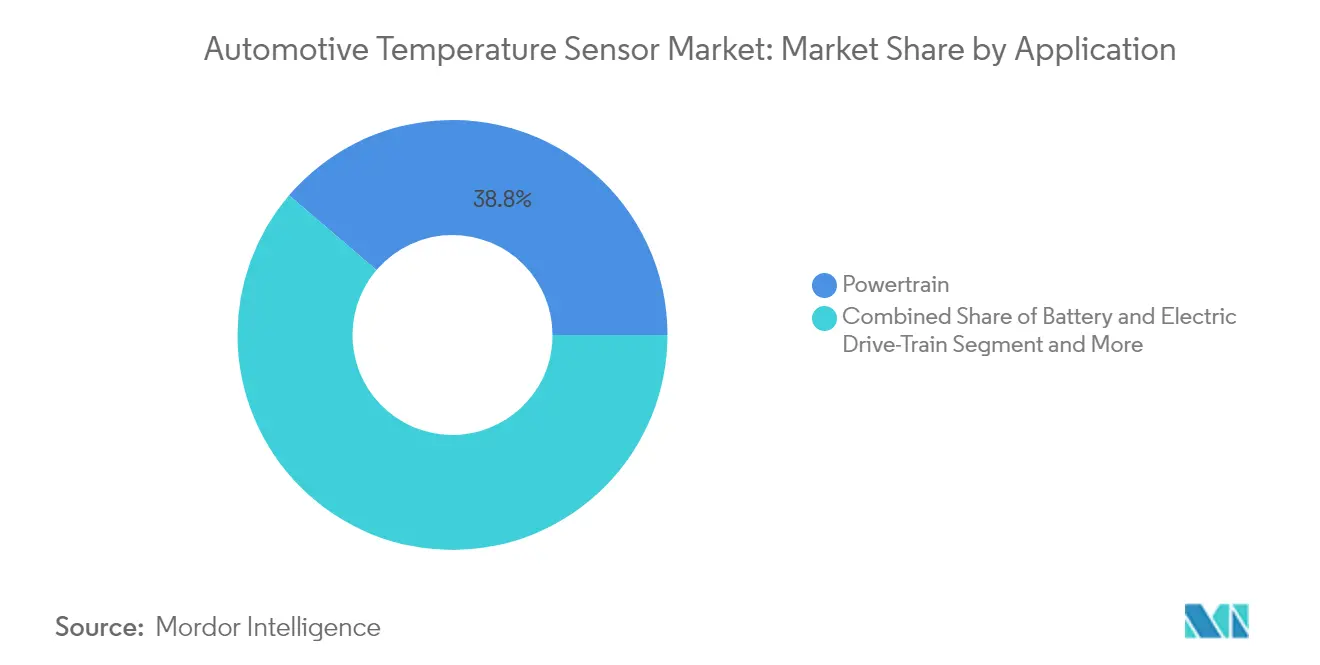

- By application, battery & electric drivetrain systems accounted for a 61.25% slice of automotive temperature sensor market size in 2025 and are set to advance at an 11.15% CAGR.

- By sales channel, OEM fitment held 90.92% share of the automotive temperature sensor market size in 2025, whereas the aftermarket is rising at a 5.98% CAGR.

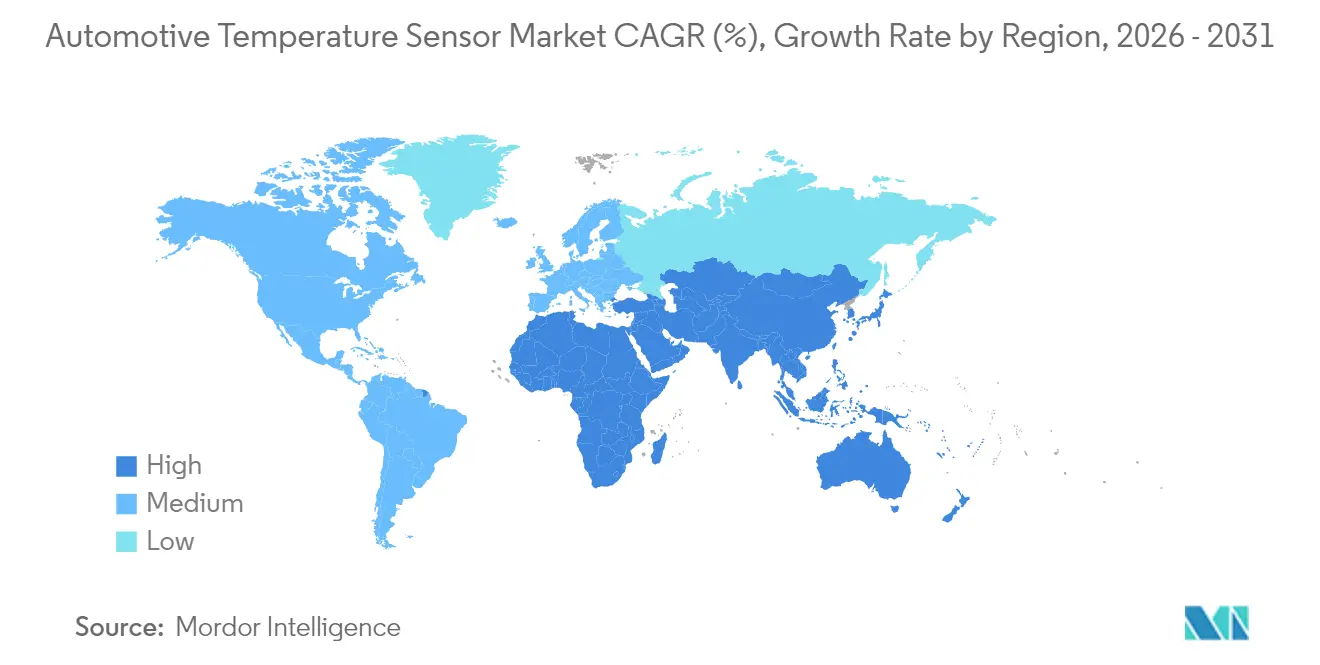

- By geography, Asia-Pacific dominated with 41.12% of automotive temperature sensor market share in 2025; the Middle East is on track to register a 9.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Temperature Sensor Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerating Adoption of SiC-based Power Electronics Intensifying Thermal Accuracy Requirements in EV Inverters | +1.9% | North America, Europe, China | Medium term (2-4 years) |

| Rapid Growth of Zonal‐Architecture ECUs Driving Multi-Point Temperature Monitoring | +1.5% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| EU7 & China VI-b Emission Norms Mandating Exhaust Gas Temperature Sensors with Wider Operating Range | +1.2% | Europe, China, with spillover to other regions | Short term (≤ 2 years) |

| Thermal Management Imperatives in Solid-State Battery Packs | +0.8% | Global, with concentration in Japan, South Korea, and North America | Long term (≥ 4 years) |

| Rising Demand for Cabin Health Sensors (HVAC Air Quality & Seat Comfort) in Premium Vehicles | +0.6% | Europe, North America, China | Medium term (2-4 years) |

| Semiconductor Packaging Shift to Automotive-Grade Wafer-Level Sensors | +0.4% | Global, with concentration in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of SiC-Based Power Electronics Intensifying Thermal Accuracy Requirements in EV Inverters

SiC switches enable drive modules to sustain junction temperatures near 600 °C while boosting conversion efficiency by 30% compared with silicon. Each SiC half-bridge therefore integrates two to three extra temperature sensing points to guard against thermal runaway and to optimise derating curves during 800 V fast charging. Foundry expansions at Onsemi and other suppliers underline how thermal data has become mission-critical for gate-drive calibration and extended inverter warranties.[1]Onsemi, “The Rise of Silicon Carbide in Power Electronics,” microchipusa.com

Rapid Growth of Zonal-Architecture ECUs Driving Multi-Point Temperature Monitoring

Vehicle networks built on zone controllers replace dozens of standalone ECUs, trimming wiring mass by 30% yet raising heat density inside sealed aluminium housings. Designers now distribute small digital sensors on local I3C links so that firmware can balance load, fan speed and redundancy in real time. Early deployments across premium European platforms are demonstrating field reliability that is convincing volume-segment OEMs to transition from 2026 onward.[2]Continental Automotive, “Zone Control Units,” continental-automotive.com

EU7 and China VI-b Emission Norms Mandating Exhaust Gas Sensors with Wider Range

Next-generation compliance hardware needs probes that withstand pulsating exhaust up to 950 °C and survive condensate shocks below -40 °C. Continuous data logging demanded by on-board monitoring systems relies on platinum RTDs, high nickel thermocouples, and increasingly SiC micro-hotplates that offer millisecond response.[3]Arrow Electronics, “Thermistors Boost the Development of New Energy Vehicles,” arrow.com This requirement is lengthening sensor replacement cycles and keeping combustion variants in the revenue mix during the decade’s first half.

Thermal Management Imperatives in Solid-State Battery Packs

Solid-electrolyte cells operate safely inside a tighter 20 °C bandwidth than liquid-ion designs, so modules embed dense strings of NTC beads, thin-film RTDs and quartz MEMS sensors. Laboratory results show phase-change composites paired with internal heaters can maintain pack temperatures for two hours at -15 °C, cutting winter range loss by 40%. As pilot lines scale after 2028, hybrid cooling plates with integrated thermoelectric coolers will receive direct feedback from these high-precision sensors.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Price-Erosion from Standardization of NTC Thermistors among Tier-1s | -0.7% | Global, with highest impact in Asia-Pacific | Short term (≤ 2 years) |

| Supply-Chain Volatility of High-Purity Nickel and Platinum Used in RTDs | -0.5% | Global, with concentration in Europe and North America | Medium term (2-4 years) |

| Slow Retrofit Rates in Commercial Vehicle Fleets | -0.3% | Global, with highest impact in emerging markets | Long term (≥ 4 years) |

| Cross-Sensitivity and Drift Issues in Low-Cost MEMS Sensors Limiting Aftermarket Adoption | -0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price-Erosion from Standardisation of NTC Thermistors among Tier-1s

Tier-1 harness builders have harmonised specifications around 1 kΩ to 100 kΩ curves, allowing large volume buys that drive annual price concessions of 3%-5%. Pure-play thermistor vendors are responding by shifting output to higher-value epoxy--coated beads for 250 °C zones or by moving up-market into digital ICs that embed calibration tables to secure margins.

Supply-Chain Volatility of High-Purity Nickel & Platinum Used in RTDs

Geopolitical tightening in ore extraction has seen spot prices swing by double digits. Research into electroless-plated nickel films on ceramic tubes demonstrates stable resistance up to 250 °C without precious metals, signalling a mid-term route to lower-cost exhaust gas sensing once corrosion challenges are resolved.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Thermistors Hold the Lead, ICs Gain Momentum

Thermistors retained a 42.62% share of the automotive temperature sensor market in 2025 owing to their low cost and proven reliability in coolant, HVAC and entry-level battery modules. Each BEV already deploys more than 100 NTC elements, and the automotive temperature sensor market size attributable to thermistors is on course to rise steadily even as unit prices drift lower. The firm grip of this legacy technology has forced higher-end vehicles to pair NTCs with linearisation algorithms inside zonal compute hubs to reconcile accuracy gaps.

Semiconductor-based IC sensors are advancing at an 8.66% CAGR through 2031. Their ±0.4 °C accuracy and direct I3C/I^2C output simplify harnessing in confined zones such as in-wheel power electronics, where every millimetre counts. As system designers phase out bulky compensation tables, the automotive temperature sensor market benefits from simultaneous gains in performance and bill-of-materials efficiency. RTDs continue serving precision exhaust feedback loops despite metal volatility, while thermocouples stay embedded in turbo housings that exceed 900 °C.

By Vehicle Type: Electric Propulsion Reshapes Demand Profiles

Passenger cars commanded 67.94% of 2025 revenue and remain the anchor for the automotive temperature sensor market. Sophisticated cabin comfort algorithms in premium trims exploit multiple sensing nodes to modulate micro-jets, seat heaters and zoned HVAC louvers. Continental’s factory trials reported a 15% uplift in overall equipment effectiveness after equipping production lines with additional thermal diagnostics — evidence that upstream manufacturing is also a consumption vector for sensors.

BEVs represent the fasting-growing cohort at a 10.12% CAGR. Every battery module clips thermistors to bus bars, embeds thin-film RTDs under cell tabs, and situates infrared die for non-contact monitoring—collectively doubling the automotive temperature sensor market size per vehicle relative to hybrids. Light commercial e-vans now integrate gas-generation detection sensors that relay early warning data to fleet dashboards, aligning thermal safety with asset-availability metrics. Two-wheelers in dense Asian cities add scale, leveraging compact, epoxy-sealed NTC beads resistant to vibration.

By Application: Electrification Pivots Spend Toward Battery Systems

Powertrain (ICE & hybrid) installations still represent 38.75% of total demand. Regulatory tightening around ammonia slip and particulate control necessitates dual-element exhaust probes that monitor both upstream and downstream of catalytic bricks. Hybrid architectures layer further complexity as control units balance oil, coolant and inverter temperature loops within millisecond windows.

Battery and electric drivetrain sensing is growing at an 11.15% CAGR, the quickest of any application. As solid-state cells arrive, algorithms will need an order of magnitude more spatial granularity, cementing this arena as the principal value generator for the automotive temperature sensor market. Chassis and safety electronics modestly expand with the rollout of brake-by-wire, while telematics modules integrate miniature die to oversee modem thermal throttling during 5G uploads.

By Sales Channel: OEM Fitment Dominates, Aftermarket Picks Up Pace

Factory-installed sensors commanded 90.92% of shipments in 2025 because integration inside powertrain controllers demands early design alignment. Software-defined cars intensify this preference: OTA updates in 2027 model years already tweak thermal maps for inverters and battery packs, necessitating firmware-grade component traceability that only OEM supply chains guarantee.

Aftermarket volume rises at a 5.98% CAGR as global vehicle age nears 13 years and home mechanics source replacement coolant probes online. Standard Motor Products’ acquisition of a European cooling specialist positions it to supply calibrated kits that plug into existing wiring while communicating revised offset values to diagnostic dongles. This dynamic ensures the automotive temperature sensor market can monetise parts sales even as fleet electrification gradually reduces mechanical wear items

Geography Analysis

Asia-Pacific held 41.12% of automotive temperature sensor market share in 2025, reflecting its status as the world’s largest vehicle production hub. Chinese assemblers are localising advanced electronic content from 15% to 60% by 2030, funnelling additional design‐win opportunities to domestic thermistor and IC fabs. Japan and South Korea continue to invest heavily in solid-state battery pilots, which embed denser sensing arrays and lift the region’s contribution to automotive temperature sensor market size through the decade.

Europe ranks second, propelled by stringent EU7 rules that require real-time exhaust gas analytics and by a strong premium vehicle pipeline that emphasises in-cabin climate refinement. German OEMs spearhead zonal architecture rollouts; each new controller cluster carries its own ambient, board-edge, and MOSFET backside die, spreading demand across multiple product families. Suppliers located near the Rhine valley are setting up nickel-film RTD lines to navigate platinum scarcity, reinforcing regional self-sufficiency.

North America maintains a robust position thanks to high uptake of SiC-based drive modules in pickup trucks and SUVs that favour 800 V propulsion for trailer towing. Legislative incentives for local battery manufacturing are steering sensor sourcing toward vertically integrated US facilities. The Middle East, although small today, is forecast to clock a 9.03% CAGR as purpose-built autonomous mobility zones in Riyadh and Dubai standardise L4 shuttles loaded with redundant thermal nodes to safeguard compute clusters against desert heat. South America’s incremental growth is linked to flex-fuel powertrains that still need exhaust gas sensors alongside emergent electric buses operating in Brazilian megacities.

Regulatory Landscape

Automotive temperature sensors used across ICE, hybrid, and BEV platforms fall under functional safety, environmental qualification, and vehicle compliance frameworks that increasingly bring thermal data into on-board monitoring. In Europe, the General Safety Regulation (EU) 2019/2144 supports broader electronics content and compliance obligations, while Commission Implementing Regulation (EU) 2025/1707 adds requirements for on-board monitoring of fuel and electric energy consumption, which raises the need for validated, traceable in-vehicle measurement chains that extend into thermal management for power electronics and HVAC.

China is also tightening product-level standardization for the component class through QC/T 821-2024 (Automotive temperature sensor), issued by MIIT on October 24, 2024 and implemented on May 1, 2025. This formalizes performance and test expectations for suppliers serving local OEMs. Internationally, ISO standards such as ISO 15500-23:2023 (CNG system temperature sensors) and ISO 20766-21:2023 (LPG pressure and temperature sensors) reinforce harmonized design and validation for specific fuel-system use cases. Trade and supply-chain policy is becoming a practical constraint as well, with a January 20, 2026 Federal Register proposal on semiconductor import actions and H.R. 2480 (Securing Semiconductor Supply Chains Act) signaling increased scrutiny on imported semiconductors. That shift can affect sourcing strategies for sensor ICs and packaging flows used in automotive-grade temperature sensing.

Value Chain Analysis

The value chain covers upstream raw materials, including ceramic powders and nickel and platinum inputs for RTDs, along with packaging materials. It then moves into semiconductor and ASIC fabrication for digital temperature ICs, and element manufacture for thermistors, RTDs, thermocouples, and infrared/MEMS components. Midstream, Tier-1 suppliers and sensor specialists assemble sensing elements, calibrate devices, and package them to automotive qualification targets, before integrating sensors into modules spanning battery packs, inverters, HVAC, exhaust aftertreatment, and zonal controllers.

Demand is anchored by OEM fitment, since powertrain and high-voltage EV systems require early co-design, firmware traceability, and validated thermal models. Distribution splits along that line, with OEM programs flowing through direct Tier-1 to OEM supply contracts and just-in-time logistics, while the aftermarket leans on cataloging, channel partners, and e-commerce, where price pressure is higher and standard NTC form factors are more common. Bottlenecks tend to cluster around automotive-grade semiconductor capacity and qualified packaging, which is amplifying strategies such as vertical integration for high-volume parts and selective outsourcing for specialty or lower-volume SKUs.

Competitive Landscape

The automotive temperature sensor market is moderately concentrated: the ten largest suppliers account for roughly 70% of revenue, balancing scale economies against pockets of niche expertise. Broadline semiconductor houses such as Texas Instruments, NXP and Onsemi leverage deep process technology to deliver highly integrated digital sensors that drop directly onto zonal controller PCBs. Meanwhile, specialists like Sensata and Amphenol focus on ruggedised inserts for exhaust manifolds and coolant jackets, safeguarding their franchise in high-temperature domains.

Strategic acquisitions illustrate the race for breadth. Spectris added Piezocryst to secure piezo-based probes suited for combustion optimisation, while Microchip absorbed VSI to marry networking SoCs with embedded sensing. MinebeaMitsumi’s tender for Shibaura expands its NTC footprint, reinforcing vertical integration from ceramic powders through finished beads. Packaging innovation is another battleground: Amkor’s optical ball-grid array with glass-on-sensor lids meets Grade 2 reliability while shrinking z-height for camera modules that also carry die to detect self-heating.

R&D spend is pivoting toward software-defined vehicles. Renesas collaborates with OEMs to embed thermal-aware schedulers inside zonal microcontrollers, dynamically allocating compute workloads away from hotspots. Littelfuse’s xEV portfolio targets inverter EMI with differential-pair sensor leads, guaranteeing signal fidelity during 400 A phase currents. As BEVs scale, collective bargaining for nickel film and ceramic substrates will intensify, but early movers with captive plating lines are positioned to shield margins.

Automotive Temperature Sensor Industry Leaders

Sensata Technologies Inc.

Robert Bosch GmbH

Continental AG

NXP Semiconductors N.V.

Amphenol Advanced Sensors

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Electrification is shifting the sensor mix toward higher-temperature, higher-accuracy, and more easily networked devices, as BEVs add close to 150 sensing points per vehicle and zonal architectures place multi-point nodes onto local digital buses. In 2026, product activity points to whitespace in non-contact and high-temperature sensing. In February 2026, Melexis introduced the MLX90637 miniature automotive infrared thermometer IC for critical EV monitoring, including inverters, motors, and HVAC, supporting galvanically isolated measurements where conventional contact sensors can be harder to place. Around the same period, TDK launched 175C automotive-grade NTC thermistors (February 2026) with terminations designed for conductive-glue mounting, aimed at improving reliability where solder joints are stressed in hotter zones, and expanding thermistor applicability deeper into EV thermal loops.

Regionalization of semiconductor and sensor-related capacity is also creating room for localized calibration, packaging, and second-sourcing strategies that reduce exposure to trade policy and long lead times. In China, new MEMS production lines reported 92% yield and supply contracts with Bosch and Continental (Suzhou MEMSensing Microelectronics and Wuxi CSMC Technologies, March 2026), indicating growing availability of automotive-grade sensor manufacturing clusters that can support Tier-1 programs. In the United States, Bosch began sample production at its first US silicon carbide semiconductor plant in Roseville, California (July 2026), after a USD 225 million CHIPS Act subsidy. As SiC inverters operate near 600 C junction temperatures, this localized scaling raises the importance of robust temperature sensing, interconnect materials, and packaging solutions that can maintain accuracy at elevated temperatures while fitting into zonal controller architectures.

Recent Industry Developments

- March 2026: Sensata Technologies launched the FaultBreak contactor, adding high-voltage switching and protection capability for electric vehicle power systems. The launch reinforces the push toward safety-critical, high-voltage architectures where temperature sensing is used alongside protection hardware to manage thermal stress and improve serviceability in xEV platforms.

- June 2025: Continental introduced its e-Motor Rotor Temperature Sensor (eRTS), designed to directly measure EV rotor temperature and reduce measurement tolerance from 15 C to 3 C. Rotor-level thermal visibility supports tighter control strategies for efficiency and durability, which increases demand for specialized sensing approaches beyond conventional stator or housing measurements.

- November 2024: Standard Motor Products completed the USD 390 million acquisition of Nissens Automotive, expanding its presence in aftermarket cooling-related components across North America and Europe. The deal strengthens channel reach for service parts where temperature sensing is bundled with cooling system maintenance and repair workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers temperature sensing devices designed for use in vehicles to measure and manage heat across key vehicle systems, where the output is used for monitoring, control, or safety functions in normal driving conditions.

Scope exclusions: We exclude temperature sensors used only in non-automotive end uses and general-purpose industrial probes that are not designed or qualified for vehicle integration.

Segmentation Overview

- By Sensor Type

- Thermistor (NTC/PTC)

- Resistance Temperature Detector (RTD)

- Thermocouple

- Semiconductor-Based IC Sensor

- MEMS and Infra-Red Sensor

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Two-Wheelers and Micro-Mobility

- By Application

- Powertrain (ICE, Hybrid)

- Battery and Electric Drive-Train

- Chassis and Safety Systems

- Body and Comfort Electronics

- Telematics and Connectivity Modules

- By Sales Channel

- OEM-Fitted

- Aftermarket

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Europe

- Germany

- France

- Italy

- Spain

- United Kingdom

- Nordics

- Rest of Europe

- Middle East

- Gulf Cooperation Council

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN-5

- Rest of Asia-Pacific

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the technical and demand context before we built the sizing model. We relied on public data series and reference material such as vehicle production releases from sources like OICA, emissions and compliance documentation from agencies such as the US EPA and the European Commission, and trade and tariff statistics from sources like UN Comtrade.

To translate demand signals into usable model inputs, we also reviewed sensor-related patents in a paid patent database, plus company filings, investor presentations, and reputable press coverage that discuss module-level sensing content. In parallel, customs and shipment patterns were sanity checked using a paid import-export shipment-level database for selected corridors where public trade codes were too broad. These examples are not exhaustive, and many other sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to verify how temperature sensing content changes by powertrain type and by application areas such as powertrain, thermal management, and cabin electronics. We spoke with a mix of component suppliers, module integrators, and downstream channel participants across APAC, EMEA, and the Americas, and then used the feedback to tighten ASP ranges, adoption timing, and replacement-rate assumptions where public data was thin.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 29% | EMEA: 31% |

| Smaller Players: 14% | Managers: 58% | Americas: 25% |

Market-Sizing & Forecasting

Our sizing starts from a top-down demand pool that is reconstructed using vehicle production by region and powertrain mix, and then filtered by installation rates for temperature sensing points across major vehicle systems. Once the demand pool is built, average selling price bands are applied by sensor technology and by use case, which is then adjusted for OEM versus service-channel weighting and typical price erosion over time.

To corroborate the totals, we ran selective bottom-up checks using sampled supplier revenue splits, channel checks on replacement volumes, and a few ASP x volume spot builds for high-usage applications such as battery thermal monitoring and exhaust temperature sensing. Where company disclosures were not cleanly attributable to temperature sensing, gaps were handled by applying conservative attribution factors that were validated through expert calls.

For forecasting, we used scenario analysis supported by input trends that experts were comfortable defending, rather than extending a single growth curve. Key inputs included global light-vehicle output, the share of electrified vehicles, expected sensor count per vehicle tied to thermal management complexity, regulatory pressure linked to exhaust and emissions monitoring, and expected shifts in technology mix between thermistors, RTDs, and infrared sensing in niche uses (illustrative, not exhaustive).

Data Validation & Update Cycle

Model outputs were cross-checked against independent signals like vehicle build trends, powertrain mix changes, and the pace of thermal management upgrades, and then reviewed for year-to-year jumps that did not match real-world adoption. If a variance looked large, we went back to the assumption level, and follow-up outreach was triggered to re-check the input ranges with industry participants.

Before sign-off, the work goes through multi-step analyst review so arithmetic, units, and currency timing are consistent across regions and years. Reports are refreshed annually, and interim updates are made when material events shift production outlooks or pricing expectations. Right before delivery, we do a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Automotive Temperature Sensors Market Sizing Compared With Other Published Estimates

Published market sizes for automotive temperature sensors can look far apart even when they are describing the same general space. Most of the spread comes from what each study chooses to count as an in-scope sensor, the year used for the base value, and how pricing is carried forward into the forecast window.

The table shows a clear split between estimates that stay close to automotive-qualified temperature sensing content and estimates that appear to bundle adjacent sensor categories or broader module electronics. The biggest drivers we saw were differences in whether multi-function temperature and humidity devices are rolled into the total, whether non-contact thermal cameras or wider thermal components are treated as sensors, and whether aggressive ASP uplift is assumed for advanced sensing technologies instead of a more typical erosion curve.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.10 B (2025) | |

| Global Consultancy A | USD 7.80 B (2025) | Uses a broader device set that appears to include multi-function temperature and humidity sensing and some higher-level thermal monitoring content, which lifts the 2025 total versus a temperature-only view. |

| Industry Publisher B | USD 18.35 B (2024) | The 2024 value suggests a much wider scope, likely bundling non-temperature sensor electronics or thermal modules, and it also uses a different base year, which makes direct comparisons difficult. |

The table points to scope as the main reason the numbers do not line up, and in Mordor Intelligence's model, only automotive temperature sensing devices are counted when they are used to measure temperatures in vehicle systems rather than broader thermal or mixed-sensor content. With the scope kept consistent year to year, the outcome stays traceable to vehicle output, sensor fitment, and realistic pricing movement, which makes the estimate easier to replicate and stress-test.

Key Questions Answered in the Report

What is driving growth in the automotive temperature sensor market?

Electrification, zonal electronic architectures and stricter emission rules are increasing the number and precision of sensors required per vehicle, propelling a 6.70% CAGR to 2031.

How many temperature sensors does a modern BEV use?

A typical battery-electric car now incorporates close to 150 sensing points, nearly three times the count installed in a conventional combustion model.

Which sensor technology is expanding fastest?

Semiconductor-based temperature ICs are growing at an 8.66% CAGR through 2031 thanks to their digital accuracy and simple system integration.

Which region leads demand today?

Asia-Pacific holds 41.12% of automotive temperature sensor market share, leveraging its dominant vehicle production base and aggressive EV rollout.

How will solid-state batteries influence sensor demand?

Solid-state packs operate within a narrower thermal window, requiring 40%–60% more sensors per module to maintain safety and performance, supporting long-term market growth.

What impact does SiC technology have on temperature sensing?

SiC inverters run at temperatures up to 600 °C, necessitating additional high-accuracy probes to protect power electronics and enabling faster 800 V charging architectures

Page last updated on: