Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.95 Billion |

| Market Size (2026) | USD 2.08 Billion |

| Market Size (2031) | USD 2.89 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Temperature Sensors Market Analysis by Mordor Intelligence

The US Temperature Sensors Market size is expected to grow from USD 1.95 billion in 2025 to USD 2.08 billion in 2026 and is forecast to reach USD 2.89 billion by 2031 at 6.78% CAGR over 2026-2031. Sub-degree accuracy demands, federal incentives that strengthen on-shore semiconductor production, and the diffusion of real-time monitoring across electric-vehicle (EV) value chains and data-center cooling systems keep the growth engine running. Liquidity in private semiconductor investments already past USD 400 billion has unlocked new fabs that rely on in-process thermal diagnostics, while autonomous factories and predictive maintenance programs drive continuous sensor retrofits. Distributed fiber-optic solutions, advanced infrared arrays, and AI-enabled edge devices are widening the competitive moat for suppliers able to pair measurement precision with integrated analytics. At the same time, tighter safety regulations in healthcare, energy storage, and petrochemical sites ensure that replacement cycles remain brisk even in legacy wired installations.

Key Report Takeaways

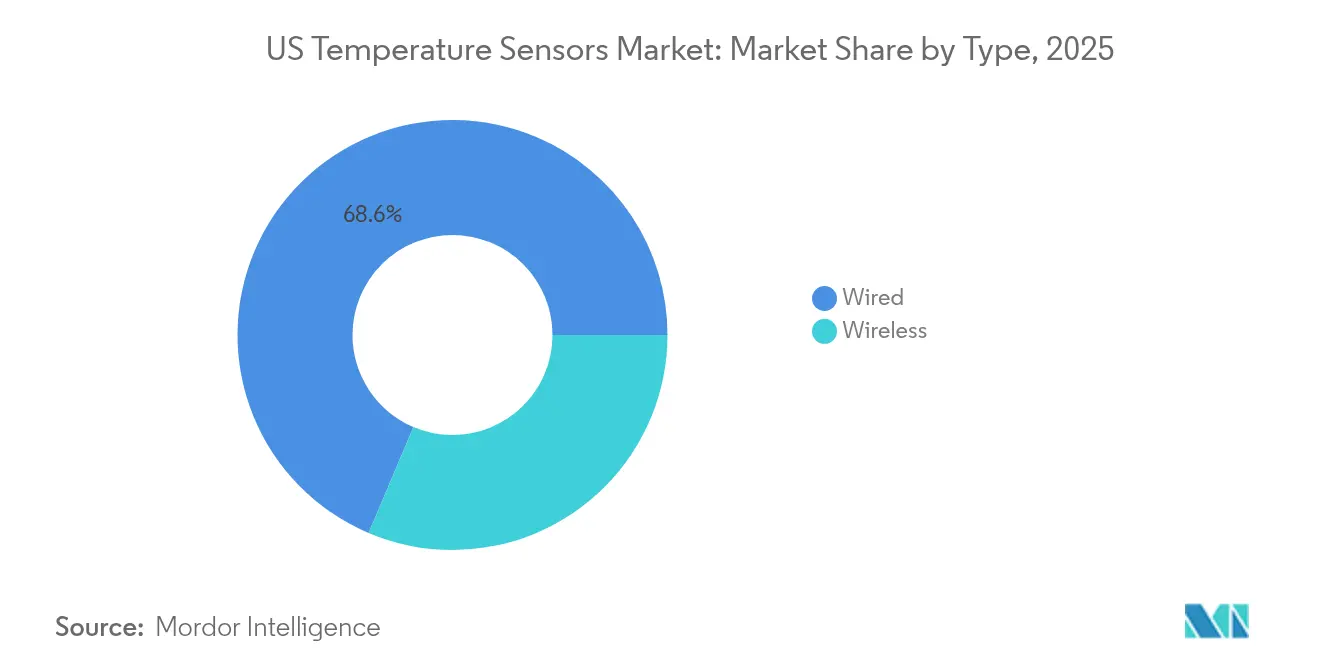

- By type, wired devices led with 68.62% of the US temperature sensors market share in 2025; wireless devices are projected to climb at 10.22% CAGR through 2031.

- By technology, thermocouples captured 31.95% of revenue in 2025, whereas fiber-optic distributed temperature sensing is forecast to expand 11.10% CAGR to 2031.

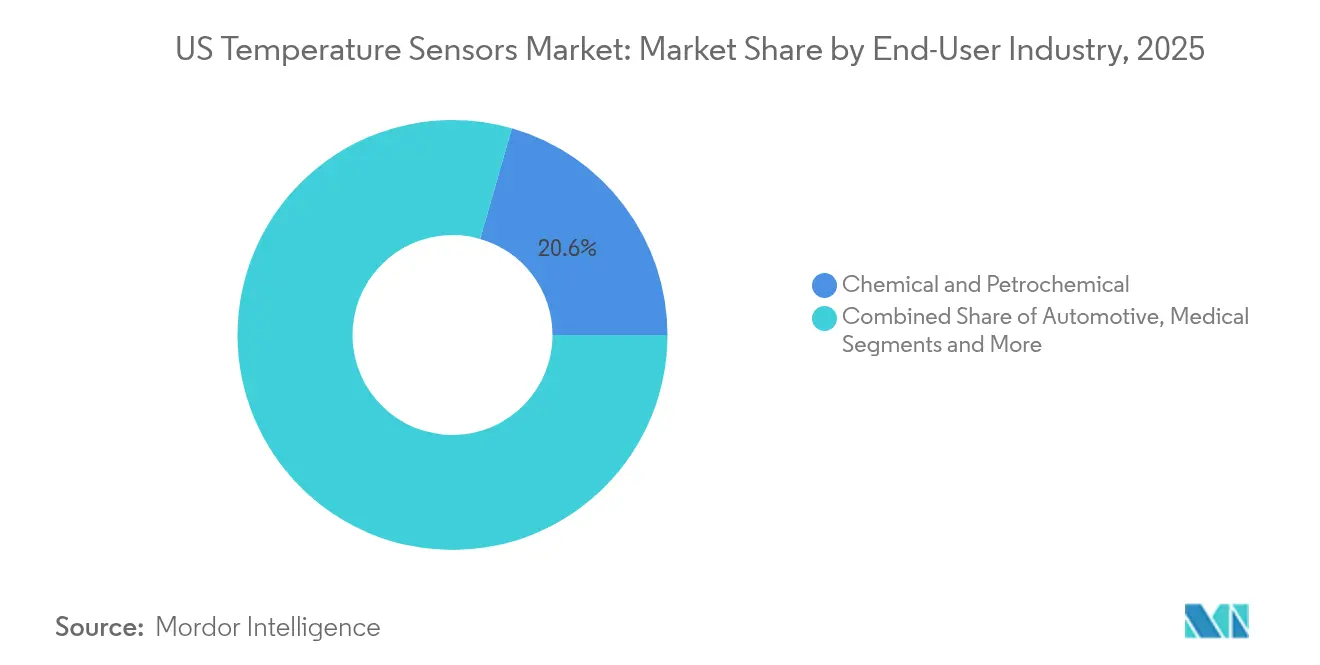

- By end-user industry, chemical and petrochemical facilities commanded 20.55% of 2025 sales, while medical applications are advancing at 10.63% CAGR to 2031.

- By connectivity, contact solutions maintained 85.10% share of the US temperature sensors market size in 2025; non-contact formats are pacing 10.05% CAGR to 2031.

- By application environment, industrial process monitoring accounted for 34.05% of revenue in 2025, with data-center cooling rising fastest at 9.35% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Temperature Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Industry 4.0 & smart-factory adoption | +1.8% | Nationwide; Midwest manufacturing belt | Medium term (2–4 years) |

| Growing demand for temperature sensing in wearable consumer electronics | +1.2% | West-Coast tech hubs; expanding nationally | Short term (≤2 years) |

| Rising automotive electronics & EV thermal-management requirements | +1.5% | South and West EV corridors | Long term (≥4 years) |

| Adoption of cold-chain IoT sensors for mRNA-vaccine logistics | +0.8% | Pharmaceutical clusters nationwide | Medium term (2–4 years) |

| Rapid growth of data-center liquid-cooling distributed sensing | +1.1% | West hyperscale & East financial hubs | Short term (≤2 years) |

| Federal on-shoring incentives boosting in-fab thermal-process sensors | +0.9% | Arizona, Texas, Ohio, New York | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expansion of Industry 4.0 and smart-factory adoption

Industrial digitalization reshapes factory floors by fusing AI, robotics, and connected instrumentation, and temperature sensing sits at the heart of that convergence. Predictive maintenance programs that once sampled a few key assets now blanket entire production lines with hundreds of nodes that flag thermal deviations hours before mechanical breakdowns.[1]Senseor, “AMS01 Solution – Switchgear Temperature and Partial Discharge Monitoring Solution,” senseor.com Edge AI chipsets embedded in new sensors from Texas Instruments crunch local data streams so millisecond-level alerts can trigger automated responses without cloud latency. Interoperable protocols such as FOUNDATION Fieldbus and PROFINET simplify system integration, while ruggedized housings and extended temperature ranges ensure reliable service in dusty, high-vibration zones. As a result, the US temperature sensors market keeps enjoying replacement sales into heritage PLC networks and fresh demand from green-field smart factories.

Growing demand for temperature sensing in wearable consumer electronics

Miniaturized, low-power die have brought clinical-grade temperature accuracy into everyday devices, letting consumers track core body temperature within ±0.1 °C for early illness detection.[2]Nishant Verma et al., “A Novel Wearable Device for Continuous Temperature Monitoring & Fever Detection,” IEEE Journal of Translational Engineering in Health and Medicine, ieee.org Stretchable substrates now conform to skin for days without irritation, and dual-sensor ear-canal designs deliver continuous readings that fit into telehealth workflows. Fifth-generation cellular links and edge computing chips send encrypted streams to healthcare dashboards so clinicians can intervene remotely, a capability valued by aging-in-place programs. For sensor makers, these design wins offer high-volume consumer channels plus technology leverage across industrial IoT where power budgets are equally tight. The resulting pull keeps the US temperature sensors market on a steep innovation curve.

Rising automotive electronics and EV thermal-management requirements

EV battery packs operate within narrow safety margins, turning temperature differentials of 0.1 °C into potential runaway events. New rotor sensors from Continental compress tolerance bands from 15 °C to 3 °C, helping motor designers reduce rare-earth magnet content while sustaining torque.[3]Austin Weber, “New Sensor Measures Heat in EV Motors,” ASSEMBLY Magazine, assemblymag.com Honeywell’s battery-safety electrolyte sensor warns up to 20 minutes ahead of thermal events, buying crucial reaction time during fast charging. Because next-gen 800 V architectures elevate switching frequencies, temperature nodes must survive stronger electromagnetic fields and meet top-tier ASIL D functional-safety goals. These stringent specs safeguard sensor margins and keep the US temperature sensors market closely tied to EV adoption curves.

Adoption of cold-chain IoT sensors for mRNA-vaccine logistics

Ultra-low-temperature storage has moved from niche biologics to mass immunization programs, forcing distributors to certify product integrity at every hand-off. IoT-enabled sensors now couple with blockchain ledgers to generate immutable temperature records, closing regulatory gaps and simplifying recalls. Satellite IoT connectivity addresses blind spots along rural routes, and multi-sensor units track dry-ice chambers and ambient holds simultaneously.[4]Wyld Networks, “How Satellite IoT Is Transforming Data Capture for Oil & Gas,” wyldnetworks.com As cell- and gene-therapy volumes climb, revenue prospects for real-time cold-chain sensing grow accordingly within the US temperature sensors market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in semiconductor & platinum-group metal prices | –0.9% | Nationwide via global supply chains | Short term (≤2 years) |

| Lengthy design-in cycles slow sensor replacement in regulated sectors | –0.6% | Aerospace & medical factories nationwide | Long term (≥4 years) |

| Cyber-security concerns over wireless sensors in critical infrastructure | –0.4% | Power and defense facilities nationwide | Medium term (2–4 years) |

| Shortage of fiber-optic installers curbs distributed sensing roll-out | –0.3% | Rural markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatility in semiconductor and platinum-group metal prices

Price swings in gallium, germanium, and platinum upset cost structures for RTDs and high-precision chip-based probes. China’s command of gallium and germanium refining keeps US buyers vulnerable to export restrictions, while platinum thin films face supply tightness amid intensified fuel-cell and catalytic-converter demand. Budget uncertainty can delay upgrade projects, trimming near-term volumes inside the US temperature sensors market.

Cyber-security concerns over wireless sensors in critical infrastructure

IoT devices extend attack surfaces for hackers targeting defense, power, and chemical assets. RF replay attacks and jamming episodes have prompted the Department of Defense to craft tougher authentication standards, adding cost and development time to wireless nodes. Until secure-by-design frameworks mature, some operators cling to wired systems, moderating the otherwise rapid wireless uptake across the US temperature sensors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Wireless Growth Accelerates Infrastructure Modernization

Wired devices retained 68.62% of 2025 revenue thanks to hard-wired reliability in safety-critical loops and existing DCS cabling, yet wireless nodes are scaling 10.22% CAGR on retrofit ease and lower installation costs. The US temperature sensors market size for wireless products is forecast to reach USD 1.09 billion by 2031, reflecting robust adoption in data centers and food plants. Self-powered harvesters developed at MIT remove battery maintenance barriers and widen use cases in pumps, kilns, and rotating equipment. In sprawling factories, LoRaWAN and 5G NB-IoT enable kilometer-scale reach with milliwatt power budgets, giving plant managers granular heat maps without trenching cable.

Reliability fears that once shadowed wireless have faded as frequency-hopping and AES-128 encryption become standard. Edge microcontrollers now pre-process readings to slash packet payloads, reducing congestion on factory backbones. Meanwhile, wired incumbency endures in nuclear, pharma, and aerospace lines where governance protocols require fixed cabling and analog outputs. Suppliers that bundle mixed-mode gateways bridging 4-20 mA loops with Wi-Fi or Sub-GHz radios capitalize on hybrid roll-outs and expand their stake in the US temperature sensors market.

By Technology: Fiber-Optic DTS Disrupts Traditional Sensing Paradigms

Thermocouples brought in 31.95% of 2025 turnover by covering extreme heat up to 2,300 °C, but distributed fiber-optic systems are rocketing at 11.10% CAGR as industries crave spatial resolution over point checks. The US temperature sensors market size for DTS is projected to exceed USD 525.4 million by 2031. Immune to EMI, fiber lines navigate high-voltage bays and induction furnaces where electronics fail. High-definition units from Luna Innovations achieve sub-millimeter granularity, mapping battery modules and cryogenic pipelines alike.

Resistance Temperature Detectors still dominate pharma cleanrooms and metrology labs that stipulate ±0.1 °C accuracy. Thermistors capture cost-sensitive appliances, while infrared arrays unlock thermal imaging for predictive maintenance. Hybrid transmitters delivering HART, Modbus, or Ethernet protocols simplify integration into digital twins. Vendors that supply full stacks sensing element, head-mount transmitter, and analytics firmware bolster recurring revenue and deepen their position inside the US temperature sensors market.

By End-User Industry: Medical Applications Drive Precision Innovation

Chemical and petrochemical complexes accounted for 20.55% of 2025 shipments as refineries monitor distillation column reflux and cracker furnace tubes. Yet medical deployments are surging 10.63% CAGR, outpacing overall US temperature sensors market growth. Demand stems from wearable patches, implantables, and portable dialysis machines seeking single-digit milliwatt budgets and biocompatible coatings. Sub-50 nW chips demonstrated in 2025 unlock months-long monitoring without battery swaps.

Elsewhere, EV battery plants, wind-turbine nacelles, and LNG export lines all raise unique accuracy, vibration, and corrosion hurdles. Cross-industry knowledge transfer means breakthroughs in one segment ripple quickly into another. Suppliers that master application engineering selecting sheath alloys, ingress ratings, and firmware filters win higher-margin custom orders, lifting overall returns in the US temperature sensors market.

By Connectivity: Non-Contact Sensing Gains Safety-Critical Applications

Contact probes held 85.10% revenue in 2025, underpinned by direct immersion RTDs and thermocouples embedded in process media. Non-contact infrared units, however, are expanding 10.05% CAGR as OSHA and NEC codes tighten safe-distance inspection norms. Robotic IR cameras patrolling data-center aisles spot hotspots behind door panels long before alarms trip.

Laser pyrometers now read molten-metal pours from several meters away, shielding operators from splash hazards. In electric substations, handheld infrared guns flag bushing failures without taking systems offline, while analytics overlays recommend load rebalancing. As predictive safety regimens proliferate, non-contact formats will steadily chip away at contact dominance inside the US temperature sensors market.

By Application Environment: Data Centers Drive Liquid-Cooling Innovation

Industrial process monitoring delivered 34.05% of receipts in 2025, but liquid-cooled data halls headline the growth charts with 9.35% CAGR. Hyperscale operators chasing AI inference throughput are pouring funds into cold-plate and immersion technologies, and every pump loop demands continuous inlet-outlet differential tracking. Fiber DTS strings measure hundreds of points along manifold runs, feeding machine-learning models that adjust flow rates in real time to cut PUE.

Healthcare wearables, EV powertrains, and building-automation HVAC segments add to demand diversity. A single gigafactory may host five distinct temperature-measurement ecosystems battery electrode drying ovens, coolant chillers, inverter stacks, ambient comfort loops, and energy-storage systems each calling for different accuracies, response times, and form factors. Such breadth keeps the US temperature sensors market both resilient and innovation-hungry.

Geography Analysis

The South dominates with 36.85% of 2025 sales, powered by Gulf-Coast petrochemical giants, EV assembly plants, and aggressive CHIPS Act fab construction. Tesla’s Texas expansions and new LNG terminals in Louisiana require high-temperature and cryogenic instrumentation, respectively. Local sourcing incentives drive procurement toward domestic sensor suppliers that can service sites within hours, keeping value capture inside US borders.

In contrast, the West is climbing 9.76% CAGR as Silicon-Valley data centers pivot to liquid cooling and California’s EV ecosystem scales. Renewable-energy mandates proliferate sensor points across solar farms, geothermal wells, and wind turbines. Intel’s foundry projects in Arizona deepen demand for Class 1 clean-room-certified probes, while wildfire-prone grids in California deploy non-contact infrared cameras for transmission-line monitoring.

Midwestern and Northeastern states embrace Industry 4.0 retrofits of legacy plants, rolling out wireless networks to counter skilled-labor shortages and raise OEE metrics. Harsh winter climates require sensors rated to -40 °C, whereas humid Gulf summers demand conformal coatings to fight condensation. Regional weather extremes therefore shape material choices and sealing techniques, giving full-suite suppliers an edge in the US temperature sensors market.

Competitive Landscape

Market structure is moderately concentrated. Heavyweights such as Texas Instruments, Honeywell, and TE Connectivity deploy end-to-end portfolios and fabs that secure silicon supply, shielding them from foundry bottlenecks. Their vertical integration lets them bundle transducers with ASIC signal chains and diagnostics software, deepening customer lock-in. Honeywell’s 2025 deal to automate LG Energy Solution’s Arizona battery plant underscores the shift from component sales to holistic thermal-management platforms.

Niche entrants pursue white spaces in quantum computing, nano-photonics, and extreme-environment sensing. University spin-outs tout integrated thermometry that maintains femto-kelvin stability for quantum bits, highlighting future demand beyond today’s industrial baseline. Cyber-secure firmware and AI-on-sensor chips differentiate mid-tier vendors aiming at critical-infrastructure tenders.

Strategic collaborations are trending: TI and Delta Electronics co-developed a 95%-efficient 11 kW onboard charger that embeds multiple high-speed temperature channels. Supply-chain hedging also gains attention; Polar Semiconductor’s Minnesota expansion insulates automotive sensor programs from Asia-Pacific geopolitics. Collectively, these moves reinforce the technology bar and sustain competitive churn within the US temperature sensors market.

US Temperature Sensors Industry Leaders

TEXAS INSTRUMENTS INC.

Honeywell International Inc.

ANALOG DEVICES INC.

Fluke Process Instruments

EMERSON ELECTRIC CO.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Texas Instruments rolled out TPS1685 48 V eFuse and GaN power stages topping 98% efficiency for data-center rails, improving thermal margins.

- January 2025: Texas Instruments debuted AWRL6844 60 GHz radar sensor with integrated edge AI for automotive cabins.

- January 2025: Honeywell launched Battery Safety Electrolyte Sensor and partnered with Titan Advanced Energy Solutions for ultrasound battery analytics.

- November 2024: Texas Instruments committed to 100% renewable electricity for manufacturing by 2030.

US Temperature Sensors Market Report Scope

The temperature sensors are devices to measure temperature readings through electrical signals. The sensor is made of two metals that generate electrical voltage or resistance once it notices a temperature change. The temperature sensors have various sensor types based on the technology type, such as Infrared, Thermocouple, Resistance Temperature Detectors (RTD), Thermistor, and others.

The report describes the type of sensors, such as wired and wireless, and also provides the study of output, which are analog and digital. The end-user industry is comprised of temperature sensor applications and majorly includes Chemical and Petrochemical, Oil and Gas, Metal and Mining, Power Generation, Food and Beverage, Automotive, Medical, Aerospace and Military, Consumer Electronics. The study is also being provided based on the COVID-19 impact.

By Type

| Wired |

| Wireless |

By Technology

| Infrared |

| Thermocouple |

| Resistance Temperature Detector (RTD) |

| Thermistor |

| Temperature Transmitter |

| Fiber Optic |

| Others |

By End-user Industry

| Chemical and Petrochemical |

| Oil and Gas |

| Metal and Mining |

| Power Generation |

| Food and Beverage |

| Automotive |

| Medical |

| Aerospace and Military |

| Consumer Electronics |

| Other End-user Industries |

By Connectivity

| Contact |

| Non-Contact |

By Application Environment

| Industrial Process Monitoring |

| HVAC and Building Automation |

| Healthcare and Wearables |

| Electric-Vehicle Battery Management |

| Data Centers and Telecom |

| By Type | Wired |

| Wireless | |

| By Technology | Infrared |

| Thermocouple | |

| Resistance Temperature Detector (RTD) | |

| Thermistor | |

| Temperature Transmitter | |

| Fiber Optic | |

| Others | |

| By End-user Industry | Chemical and Petrochemical |

| Oil and Gas | |

| Metal and Mining | |

| Power Generation | |

| Food and Beverage | |

| Automotive | |

| Medical | |

| Aerospace and Military | |

| Consumer Electronics | |

| Other End-user Industries | |

| By Connectivity | Contact |

| Non-Contact | |

| By Application Environment | Industrial Process Monitoring |

| HVAC and Building Automation | |

| Healthcare and Wearables | |

| Electric-Vehicle Battery Management | |

| Data Centers and Telecom |

Key Questions Answered in the Report

What is the current size of the US temperature sensors market?

The US temperature sensors market size reached USD 2.08 billion in 2026 and is forecast to climb to USD 2.89 billion by 2031.

Which segment is growing fastest within the US temperature sensors market?

Wireless sensors show the highest momentum, expanding at a projected 10.22% CAGR through 2031 on the back of retrofit flexibility and lower installation costs.

How are federal incentives affecting demand for temperature sensors?

The CHIPS Act’s 25% investment credit has spurred over USD 400 billion in fab construction, sharply increasing orders for high-precision in-process temperature probes.

Why is fiber-optic distributed temperature sensing gaining popularity?

Fiber DTS offers thousands of measurement points along a single cable, is immune to electromagnetic interference, and meets the fine-grained monitoring needs of data centers, battery packs, and high-voltage equipment.

Which US region generates the largest revenue for temperature sensors?

The South leads with 36.85% market share thanks to petrochemical clusters, EV assembly plants, and new semiconductor fabs that require extensive thermal monitoring.

What cybersecurity challenges face wireless temperature sensors?

IoT nodes in critical infrastructure must withstand RF replay and jamming attacks; adherence to emerging federal authentication standards is essential before widespread deployment.

Page last updated on: