Thermistor Temperature Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

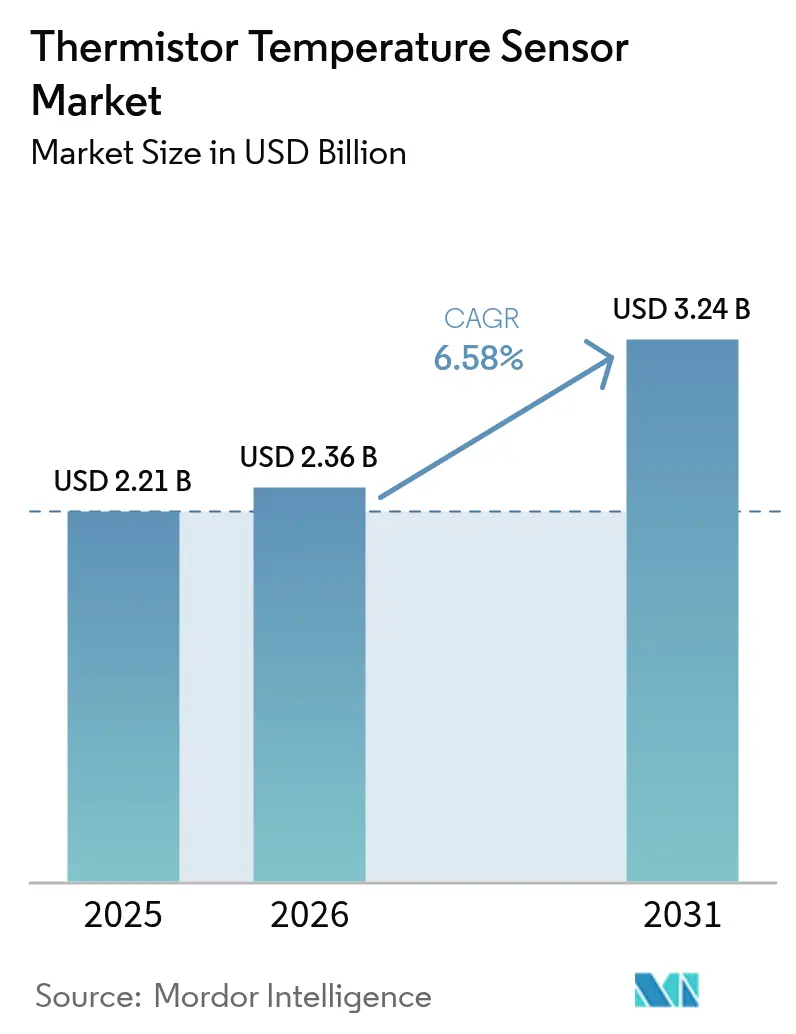

| Market Size (2026) | USD 2.36 Billion |

| Market Size (2031) | USD 3.24 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

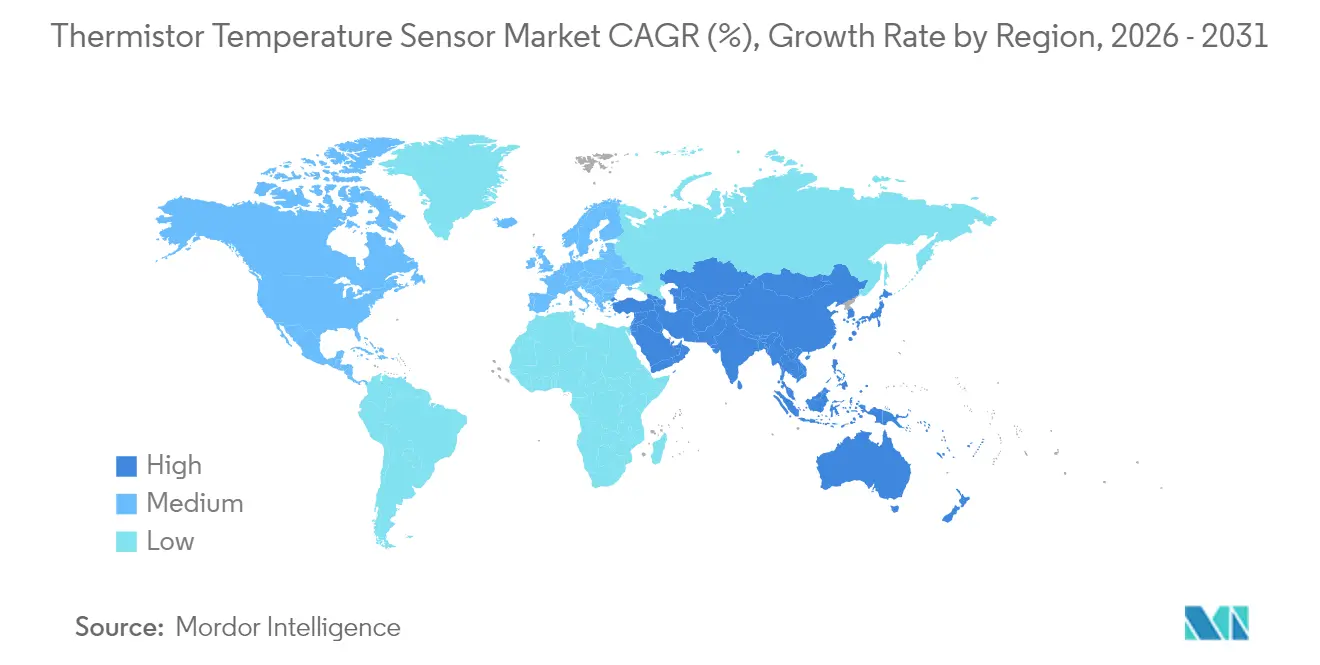

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermistor Temperature Sensor Market Analysis by Mordor Intelligence

The thermistor temperature sensor market size is expected to grow from USD 2.21 billion in 2025 to USD 2.36 billion in 2026 and is forecast to reach USD 3.24 billion by 2031 at 6.58% CAGR over 2026-2031. Demand accelerates as high-density battery packs, ultra-low-power IoT nodes, and smart consumer devices all require millisecond-level thermal feedback. Dense monitoring arrays inside electric-vehicle battery modules, large-scale sensor rollouts across industrial IoT lines, and regulatory mandates for food and pharmaceutical cold chains form the core volume drivers. Cost-effective NTC devices control 70% of global shipments, while PTC variants carve out niches where self-regulation adds value. Regionally, Asia-Pacific’s manufacturing depth anchors 46% of total 2024 revenue, yet the Middle East delivers the fastest regional upswing. Competitive positioning now hinges on the ability to bundle sensing elements with on-board signal processing and connectivity so that customers secure turnkey thermal-management subsystems rather than discrete components.

Key Report Takeaways

- By type, NTC devices led with 69.62% revenue share in 2025; PTCs are projected to expand at a 7.38% CAGR through 2031.

- By Temperature Range, Medium temperature deployments between -40 °C and 125 °C generated nearly three-quarters of 2025 shipments, with a market share of 64.92% and are advancing at a 7.07% CAGR to 2031.

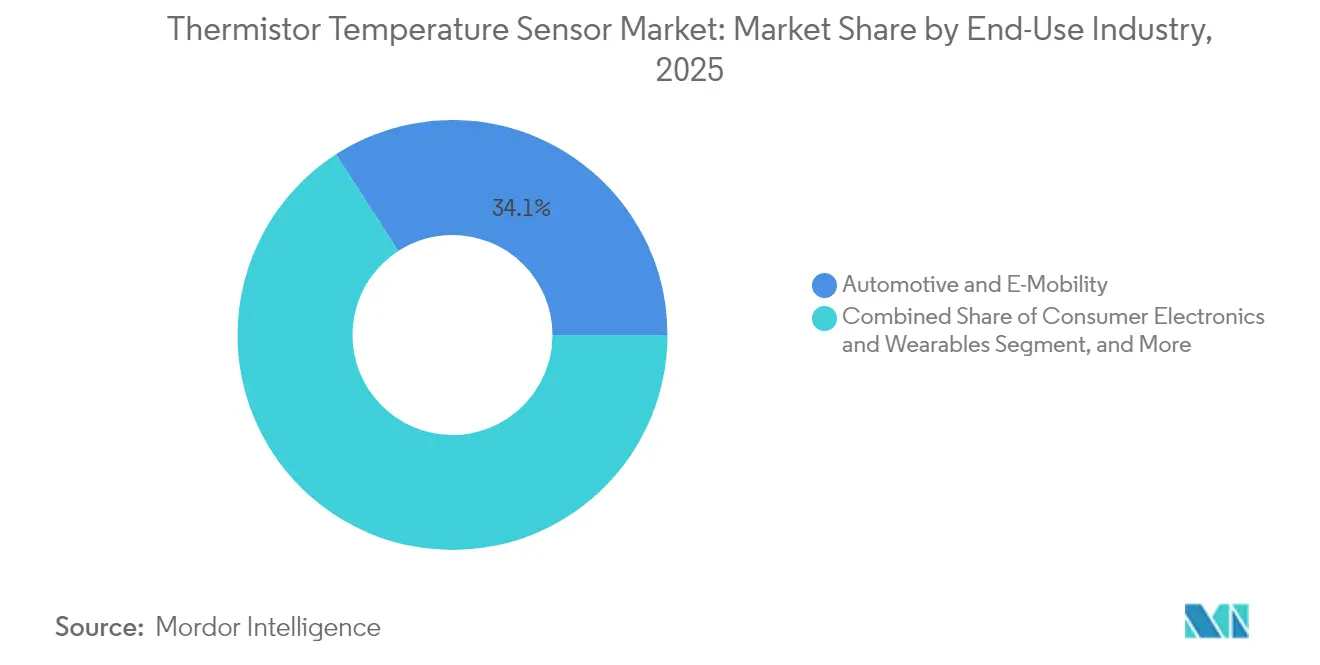

- By end-use industry, automotive and e-mobility accounted for 34.12% of the thermistor temperature sensor market share in 2025, while medical and life-sciences equipment is advancing at a 7.18% CAGR to 2031.

- By geography, Asia-Pacific held 46.08% of 2025 revenue; the Middle East region records the highest forecast growth at 6.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thermistor Temperature Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for cost-effective, high-accuracy sensors in consumer electronics | +1.2% | Global, with APAC core concentration | Medium term (2-4 years) |

| Rapid EV-battery deployment requiring dense thermal-runaway monitoring | +1.8% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Expansion of industrial IoT and smart factories | +1.5% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Regulatory mandates on food-safety and cold-chain traceability | +0.9% | North America and EU regulatory frameworks | Long term (≥ 4 years) |

| Solid-state battery early-warning chips integrating micro-NTC beads | +0.7% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Smart-textile wearables embedding flexible thermistor yarns | +0.5% | Global, with fashion-tech convergence centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for Cost-Effective, High-Accuracy Sensors in Consumer Electronics

Thermistors are winning socket share in smartphones, laptops, and wearables because chip-scale 0402 packages occupy minimal board real estate while still achieving ±0.5 °C accuracy.[1]TDK Corporation, “NTC Thermistors Product Catalog,” tdk.com Device makers now embed multi-point thermistor arrays across batteries and system-on-chip heat spreaders to trigger predictive throttling algorithms that lengthen component life and improve user safety. Continuous shrinkage of application processors lifts waste-heat density, so every new smartphone generation adds incremental thermal nodes. The result is a steady rise in the thermistor temperature sensor market as OEMs favor the low cost and mature supply chains of NTC parts over digital IC alternatives. Suppliers that combine ultra-small die with low-noise signal chains are carving out premium ASP positions despite the commodity reputation of discrete thermistors.

Rapid EV-Battery Deployment Requiring Dense Thermal-Runaway Monitoring

Modern battery packs mount hundreds of sensing beads per vehicle because a 5 °C cell-to-cell gradient can cascade into runaway failures. NTC materials deliver sub-100 millisecond response across -40 °C to 125 °C ranges, allowing battery-management units to isolate overheating modules before venting occurs. Second-generation chemistries such as high-nickel NMC require even tighter temperature envelopes, enlarging sensor counts per kilowatt-hour. Automakers have therefore become the largest volume buyers in the thermistor temperature sensor market. To meet stringent AEC-Q200 reliability tests, vendors are introducing epoxy-coated leads that resist vibration, humidity, and electromagnetic interference, ensuring long-term calibration stability over the vehicle’s service life.

Expansion of Industrial IoT and Smart Factories

Predictive-maintenance programs depend on thousands of low-power wireless nodes that sample temperature every few seconds yet operate multiple years on coin cells.[2]Power Motion Tech, “Future Sensor Growth Benefits New Applications,” powermotiontech.com Thermistors consume micro-watts and integrate easily with energy-harvesting modules, so plant operators deploy them on motors, gearboxes, and HVAC ducts without costly rewiring. Coupled with edge-AI microcontrollers, these sensors flag early deviations that let technicians swap parts during planned outages rather than after catastrophic failure. This momentum is translating into expanded order books for industrial-grade NTC probes with extended moisture and chemical resistance, further enlarging the thermistor temperature sensor market footprint inside smart-factory rollouts.

Regulatory Mandates on Food Safety and Cold-Chain Traceability

HACCP rules and updated FDA guidance require verifiable temperature logs throughout storage and shipping. Wireless data loggers fitted with thermistor strings now accompany meat, dairy, and biologics cargo so that logistics managers can audit every pallet on delivery. Because these deployments run into millions of containers each year, the sensor cost per node is critical. Thermistors deliver the necessary ±0.2 °C precision while keeping BOM costs well below digital IC alternatives, preserving profit margins for logistics providers even as compliance thresholds tighten. The cumulative demand from global cold-chain operators adds meaningful lift to the thermistor temperature sensor market through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited temperature span versus RTDs and IC sensors | -0.8% | Global, particularly high-temperature industrial applications | Medium term (2-4 years) |

| Volatility in manganese, cobalt, and nickel-oxide feedstock prices | -1.1% | Global supply chain impact | Short term (≤ 2 years) |

| Shift toward fully-digital temperature-sensor ICs in automotive ADAS | -0.9% | North America and EU automotive markets | Medium term (2-4 years) |

| Self-heating drift in ultra-low-power IoT nodes | -0.4% | Global IoT deployments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Temperature Span Versus RTDs and IC Sensors

Most NTC formulations top out near 125 °C, which rules them out for aerospace turbines, petrochemical reactors, and engine-exhaust systems that run beyond 200 °C.[3]IEEE Spectrum, “Temperature Sensors: Now You See Them, Now You Don’t,” ieee.org End users in these sectors prefer platinum RTDs or digital silicon ICs that remain stable at elevated ranges and provide linear outputs without analog conditioning. The resulting application ceiling trims the obtainable share of the thermistor temperature sensor market in extreme-temperature verticals. Component makers are pursuing high-temperature glass-encapsulated beads, but production yields remain low and costs high, limiting near-term adoption.

Volatility in Manganese, Cobalt, and Nickel-Oxide Feedstock Prices

NTC pastes rely on manganese, cobalt, and nickel oxides whose spot prices have fluctuated widely since 2024 due to battery-materials competition. Sudden spikes flow directly into wafer and thick-film substrate costs, compressing margins for manufacturers that locked in long-term pricing with OEMs.[4]L.N. Antrim, “Strategic Materials Technologies to Reduce U.S. Import Vulnerability,” ota.fas.org Some suppliers hedge with multi-sourcing strategies and synthetically engineered dopants, yet sourcing uncertainty still weighs on profit visibility and dampens near-term expansion plans inside the thermistor temperature sensor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: NTC Dominance Driven by Sensitivity Advantages

NTC devices captured 69.62% of the 2025 volume, establishing clear leadership in the thermistor temperature sensor market share thanks to exponential resistance-temperature slopes that resolve 0.01 °C changes in medical, battery, and industrial control loops. The thermistor temperature sensor market size contribution from NTC parts is forecast to grow from USD 1.54 billion in 2025 to USD 2.22 billion by 2031, reflecting the segment’s ability to scale into chip-scale, probe, and flexible-substrate formats. PTC products, while rising at a 7.38% CAGR, remain niche for inrush current limiting and self-heating heaters.

The evolution of perovskite-doped ceramics is amplifying beta coefficients above 4,400 K, further tightening accuracy without complex linearization. Vendors also deposit thin-film NTC layers on polyimide and PET, giving designers stretchable sensors for e-textile garments. This steady innovation cadence underpins long-term NTC dominance even as digital ICs nibble at legacy sockets, ensuring the thermistor temperature sensor market retains a robust core around high-sensitivity discrete components.

By Temperature Range: Medium-Range Applications Drive Volume Growth

Medium-range deployments between -40 °C and 125 °C generated nearly three-quarters of 2025 shipments. The thermistor temperature sensor market size for this bracket is projected to hit USD 2.47 billion by 2031, aided by aligned requirements across EV batteries, consumer gadgets, and HVAC compressors. Low-temperature niches below -40 °C, such as cryogenic freezers and arctic monitoring buoys, demand custom chemistries that push resistance values into mega-ohm territory. Manufacturers have answered with nanostructured semiconductor blends that keep response times below 100 milliseconds even at -55 °C, broadening addressable opportunities.

High-temperature ranges above 125 °C remain constrained because standard NTC paste sintering cannot deliver long-term drift stability. Glass-encapsulated beads help, but add cost and fragile lead terminations. Consequently, RTDs and silicon diodes dominate turbine and refinery loops, limiting upside for thermistors within that slice of the thermistor temperature sensor market. Research labs are addressing the gap with wide-bandgap semiconductors, though commercialization is not expected until after 2028.

By End-Use Industry: Automotive Leadership Amid Digital Competition

Automotive and e-mobility held 34.12% revenue in 2025, driven by battery-pack proliferation that installs hundreds of NTC probes per vehicle. Yet ADAS radar, lidar, and cockpit domains are migrating toward digital temperature ICs with integrated bus interfaces, creating competitive tension. The thermistor temperature sensor market nevertheless benefits as powertrain electrification expands across cars, buses, and two-wheelers.

Medical and life-sciences equipment rises at a 7.18% CAGR through 2031 as hospitals deploy continuous vital-sign patches and smart catheters with embedded micro-beads for in-situ temperature tracking. Consumer gadgets and wearables add steady unit volume since every lithium-ion device ships with at least one battery thermistor. Industrial automation sustains baseline demand as factories attach probes to motors and gearboxes for predictive maintenance. Together, these segments keep the thermistor temperature sensor industry diversified and resilient even as certain automotive zones turn fully digital.

Geography Analysis

Asia-Pacific’s 46.08% share in 2025 stems from its vertically integrated ceramic processing and surface-mount assembly hubs concentrated in China, Japan, and South Korea. Tier-one suppliers operate large-scale kilns near component plants, cutting logistics costs and shortening lead times. Government incentives for EV adoption amplify local demand, while regional giant battery makers source sensors from domestic vendors to comply with tight pack-level thermal budgets.

North America and Europe combine for roughly 34.75% of 2025 revenue. Their advantage lies in high-margin medical, aerospace, and ADAS markets that prize traceability and functional-safety certification. Automotive Tier-1s in Germany and the United States have begun qualifying combined temperature-voltage probes that simplify wiring inside 800-V battery architectures, a trend expected to lift average selling prices even if unit counts plateau.

The Middle East tops growth tables at 6.98% CAGR as giga-factories, smart-city programs, and energy-intensive desalination plants demand thousands of sensors per facility. Africa and South America remain nascent, but mining, agriculture, and renewables create early footholds. Export-oriented Asian vendors are partnering with local distributors to bridge support gaps and capture incremental share in these frontier regions, further broadening the thermistor temperature sensor market.

Regulatory Landscape

Regulation for thermistor temperature sensors is primarily driven by safety and component-compliance requirements tied to end equipment such as appliances, HVAC, and building automation. In May 2026, the International Electrotechnical Commission published IEC 60730-2-9:2026, setting requirements for temperature sensing controls used in automated control systems, which serves as a reference point for sensor selection, test evidence, and documentation by OEMs and module suppliers.

In Europe, alignment to harmonized standards and substance restrictions functions as a commercialization gate. CENELEC published EN IEC 60730-2-9:2026 in July 2026, enabling conformity routes for temperature-control functions across HVAC and appliance applications. Separately, the European Commission adopted Delegated Directives (EU) 2025/1802, 2025/2363, and 2025/2364 amending RoHS Annex III, with market application starting July 1, 2026, tightening how lead-related exemptions apply to electronics, including sensor assemblies that rely on specific solders or glass/ceramic components; this increases redesign and material-declaration workload for suppliers shipping into the EU.

Value Chain Analysis

The thermistor temperature sensor value chain starts with metal-oxide inputs (commonly manganese, nickel, cobalt, and copper oxides) and specialty binders, followed by ceramic formulation and powder processing, sintering, and component fabrication into beads, chips, or SMD parts. Manufacturing then moves through dicing, metallization/termination, encapsulation or probe assembly, and calibration and characterization (often using traceable temperature references), before final test, packing, and shipment to OEMs, contract manufacturers, and module integrators across automotive, industrial automation, medical devices, and consumer electronics.

Recent supply-side actions point to capacity and resilience being managed at the fabrication stage, which acts as a major bottleneck for high-volume NTC shipments. In May 2026, Murata Manufacturing announced construction of a new five-story, 18,010 m2 production building at its Yokaichi Plant in Shiga, Japan, dedicated to thermistor manufacturing with a 16.9 billion yen investment, indicating longer-cycle capacity additions aligned with EV, industrial automation, and energy use cases. Upstream volatility in oxide inputs and the need for tight process control heighten the value of multi-sourcing, quality assurance, and geographically diversified production footprints, particularly for automotive-grade parts that must meet stringent reliability requirements.

Competitive Landscape

Murata, TDK, and Texas Instruments anchor the market through proprietary ceramic formulations, MEMS integration lines, and global sales reach. Each invests heavily in automated screen-printing, laser-trimming, and statistical-process-control systems that push ppm defect rates ever lower. Medium-sized challengers focus on flexible substrates, glass-encapsulation, and extreme-temperature offerings where larger firms avoid low-volume complexity.

Strategic moves include Bourns’ 2025 launch of sub-millimeter NTC arrays for automotive battery modules and Ametherm’s dual-parameter ThermiVolt probe that fuses temperature and voltage sensing for renewable-energy inverters. Honeywell entered adjacent fluid monitoring by applying thermopile principles to infusion-pump flow sensors, illustrating convergence between thermal detection and broader sensing modalities.

Patent filings surged 12% in 2024 as vendors protected perovskite blends, coaxially shielded textile antennas, and AI-assisted self-calibration techniques. The competitive landscape, therefore, favors firms that couple materials science with digital circuitry and cloud analytics, ensuring their portfolios meet rising system-level integration requirements across the thermistor temperature sensor market.

Thermistor Temperature Sensor Industry Leaders

Murata Manufacturing Co. Ltd.

TDK Corporation (EPCOS)

TE Connectivity

Texas Instruments Inc.

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is the shift from discrete thermistors to bundled, application-ready temperature-sensing subsystems that reduce wiring, calibration effort, and qualification cycles for OEMs in automotive electrification, industrial automation, and energy equipment. This shows up in competitive positioning that emphasizes design-in support and integrated solutions alongside the sensing element, including moves to combine the sensing element with signal conditioning and digitally compatible interfaces so thermistors can plug into PLC/DCS sensor networks and connected maintenance platforms.

Supply expansion and higher-spec product roadmaps also create whitespace in segments that require reliability at tighter thermal limits and broader operating ranges. Murata Manufacturings May 2026 investment to build a new thermistor production building at its Yokaichi Plant (construction starting May 2026) provides tangible evidence of manufacturers committing capital to serve industrial automation, EVs, and renewable-energy applications. At the same time, automotive electronics demand is pulling toward miniaturized SMD formats and higher temperature capability (for example, up to 175 C class components in automotive environments), leaving room for suppliers that can deliver stable performance, robust packaging, and qualification support for harsh, vibration- and humidity-exposed deployments.

Recent Industry Developments

- May 2026: Murata Manufacturing announced an approximately 16.9 billion yen investment to build a new thermistor production building at its Yokaichi Plant in Shiga, Japan, and began construction in May 2026. The dedicated capacity build strengthens supply availability for high-volume end uses such as EVs, industrial automation, and renewable-energy power electronics, where qualification-ready continuity of supply is a purchasing criterion.

- June 2025: Bourns released a compact NTC thermistor series targeting high-precision automotive and industrial assemblies. The launch supports higher sensor density in constrained designs such as battery modules and industrial control equipment, where packaging and stability requirements increasingly drive preferred-supplier positioning.

- December 2024: Honeywell introduced a thermopile-based liquid-flow platform for medication delivery equipment. While adjacent to temperature sensing, the platform reflects broader medical-device sensing upgrades and can pull through demand for tighter thermal monitoring in integrated fluid and infusion systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as revenues earned from thermistor-based temperature sensors sold globally, covering NTC and PTC sensing elements used to measure and control temperature in devices and equipment across major end markets.

Scope exclusions: We exclude non-thermistor temperature sensing technologies (such as RTDs, thermocouples, and IC-based digital temperature sensors) and exclude downstream services and software bundled around temperature monitoring.

Segmentation Overview

- By Type

- Positive Temperature Coefficient (PTC)

- Negative Temperature Coefficient (NTC)

- By Temperature Range

- Low Temperature (Below -40 C)

- Medium Temperature (-40 C to 125 C)

- High Temperature (Above 125 C)

- By End-Use Industry

- Automotive and E-Mobility

- Consumer Electronics and Wearables

- Industrial Automation and IIoT

- Medical and Life-Sciences Equipment

- Energy and Power Generation

- Aerospace and Defense

- HVAC and Building Automation

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- Malaysia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by pinning down the demand pool and the technical scope, so the model does not drift into the wider temperature sensor market. We used public sources such as US Census trade statistics, UN Comtrade-style import-export series, OECD industrial indicators, and international energy and vehicle production statistics to sense-check end market direction.

To ground assumptions, we also reviewed standards and guidance publications from recognized bodies (for example, IEC and ISO references where accessible), peer-reviewed papers on thermistor performance and use cases, plus investor materials and annual filings from listed component manufacturers. For fill-in gaps, we leaned on paid subscriptions that provide company financials and market intelligence, plus patent database coverage to track where design activity is moving. These examples are not exhaustive, and many other public documents and datasets were also referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions on where thermistor temperature sensors are specified, how pricing behaves by temperature range, and how demand shifts across automotive, electronics, industrial, medical, energy, aerospace, and HVAC uses. We spoke with a mix of manufacturers, distributors, and engineering or procurement stakeholders, then re-checked the key assumptions across APAC, EMEA, and the Americas, so regional differences in product mix and adoption did not get averaged out.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 13% | APAC: 44% |

| Mid tier: 54% | Functional/Unit leaders: 32% | EMEA: 35% |

| Smaller Players: 17% | Managers: 55% | Americas: 21% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand reconstruction, where production and installed base signals from key end-use industries are translated into expected thermistor sensor consumption through penetration and content-per-unit assumptions. Once the demand pool is formed, it is converted to value using modeled average selling prices by type (NTC versus PTC) and by temperature range, then split by geography.

To keep the totals realistic, we also ran selective bottom-up checks, including sampled supplier revenue mapping, channel feedback on volume movement, and quick ASP x shipment approximations in the larger application pockets. The main inputs we track include EV and conventional vehicle output (because battery modules and thermal management drive sensor counts), consumer electronics shipments, industrial automation activity, HVAC equipment demand, and the mix shift toward higher temperature designs in tougher environments. For forecasting, we use scenario analysis, tuning the key levers (end market growth, adoption rates, and ASP progression) based on what experts expect over the next 12 to 24 months, followed by longer-term normalization.

Data Validation & Update Cycle

Before sign-off, the model outputs are triangulated against independent signals, and any large variance is investigated at the assumption level, not just corrected at the total. Checks include region-by-region growth sanity tests, price trend consistency by thermistor type, and whether end-use splits look plausible against observed application momentum.

A second analyst review is completed for calculation logic and consistency, and re-contacts are triggered if a key assumption moves or a new inconsistency appears during review. Reports are refreshed annually, and material events can prompt interim revisions, followed by a final pre-delivery pass so the latest public updates are reflected.

Mordor Intelligence's Global Thermistor Temperature Sensors Market Market Sizing Compared With Other Published Estimates

Published market sizes for thermistor temperature sensors often do not match because the scope line can shift, and then the pricing and end-use weights change the final value quickly. Differences also come from the chosen base year, the currency conversion timing, and whether the model is refreshed after a major end market swing.

Some sources appear to report a broader dollar pool by using higher assumed unit content in electronics and vehicles, then carrying that forward with aggressive price retention. In Mordor Intelligence's approach, value is counted only for thermistor-based temperature sensors (NTC and PTC) and is kept separate from non-thermistor temperature sensor technologies, and this narrower counting rule alone can pull totals down versus broader readings.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.21 B (2025) | |

| Industry Publisher A | USD 3.66 B (2025) | Uses a wider assumed demand pool and higher content-per-unit in major end uses, which increases the implied shipment base before pricing is applied, and this can inflate value even if the same thermistor types are referenced. |

| Industry Publisher B | USD 4.04 B (2024) | Uses a different base year and a longer forecast window, and the current-year figure is sensitive to how ASPs are trended and how quickly mix shifts (for example, automotive versus industrial) are assumed to occur. |

The spread is mainly explained by how strictly the product scope is kept to thermistor temperature sensors, plus how unit content and ASP change are treated in high-volume end uses. By tying the value build to visible demand indicators and then re-checking with supplier and channel feedback, the estimate stays traceable to repeatable steps instead of broad multipliers.

Key Questions Answered in the Report

How large is the thermistor temperature sensor market in 2026?

The thermistor temperature sensor market size is expected to reach USD 2.36 billion in 2026.

Which device type commands the highest share today?

NTC thermistors lead with 69.62% of 2025 revenue thanks to high sensitivity and scalable production.

Why does Asia-Pacific dominate shipments?

A dense semiconductor supply chain and booming electric-vehicle output give Asia-Pacific 46.08% of global revenue.

How will raw-material volatility affect pricing?

Fluctuations in manganese, cobalt and nickel oxides may squeeze margins, but diversified sourcing and synthetic dopants should limit sharp price swings.

Page last updated on: