Automotive Inertial Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.43 Billion |

| Market Size (2031) | USD 5.61 Billion |

| Growth Rate (2026 - 2031) | 10.31% CAGR |

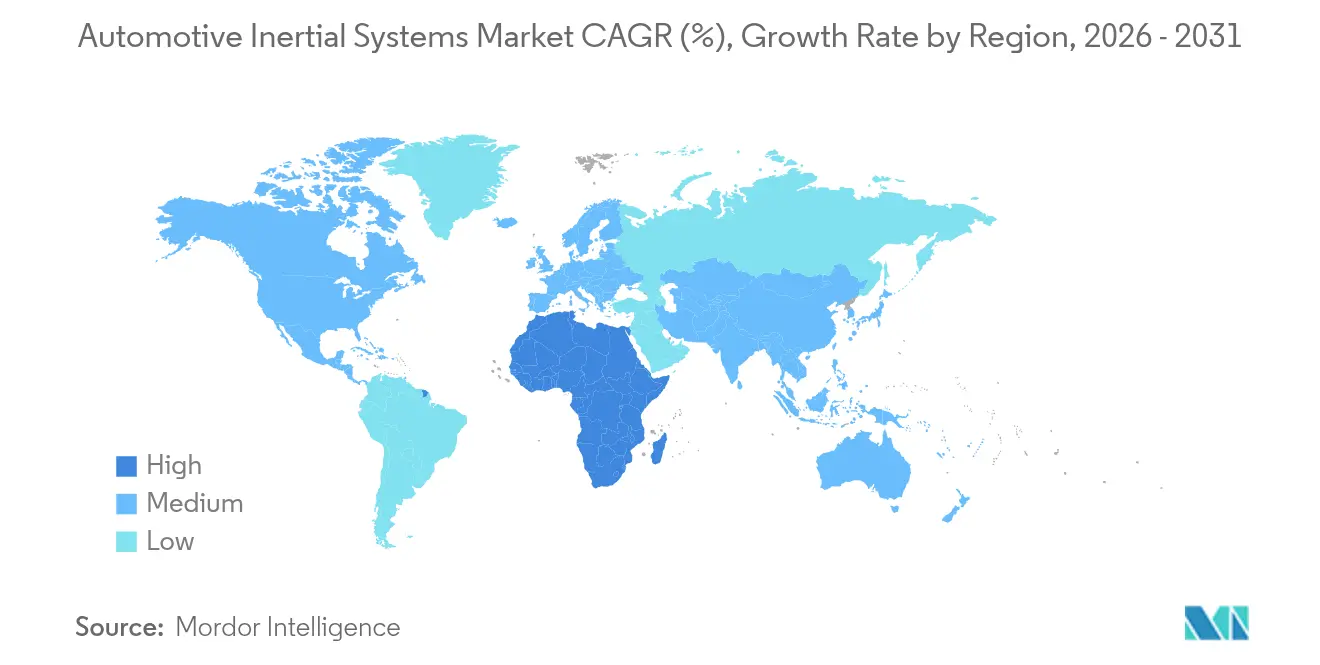

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Inertial Systems Market Analysis by Mordor Intelligence

The Automotive Inertial Systems market size is expected to grow from USD 3.11 billion in 2025 to USD 3.43 billion in 2026 and is forecast to reach USD 5.61 billion by 2031 at 10.31% CAGR over 2026-2031. Mandatory electronic stability control (ESC) laws on every major continent, the mainstreaming of Level 2+ driver-assistance functions, and wafer-size migration in MEMS fabrication collectively expand yearly unit volumes and compress cost curves. Automakers are replacing single-axis sensors with six-axis inertial measurement units (IMUs) to simplify board layouts and lower calibration budgets, while chipmakers’ move from 8-inch to 12-inch silicon boosts throughput and halves die-level bias variation. Asia-Pacific contributes the largest revenue slice, supported by China’s GB 21670 and India’s Bharat New Vehicle Safety Assessment Program, whereas Africa registers the fastest pace on the back of South Africa’s Automotive Production and Development Programme incentives. Competitive risk centers around two foundry partners, Taiwan Semiconductor Manufacturing Company and GlobalFoundries, which raises single-point-of-failure exposure for MEMS supply chains.

Key Report Takeaways

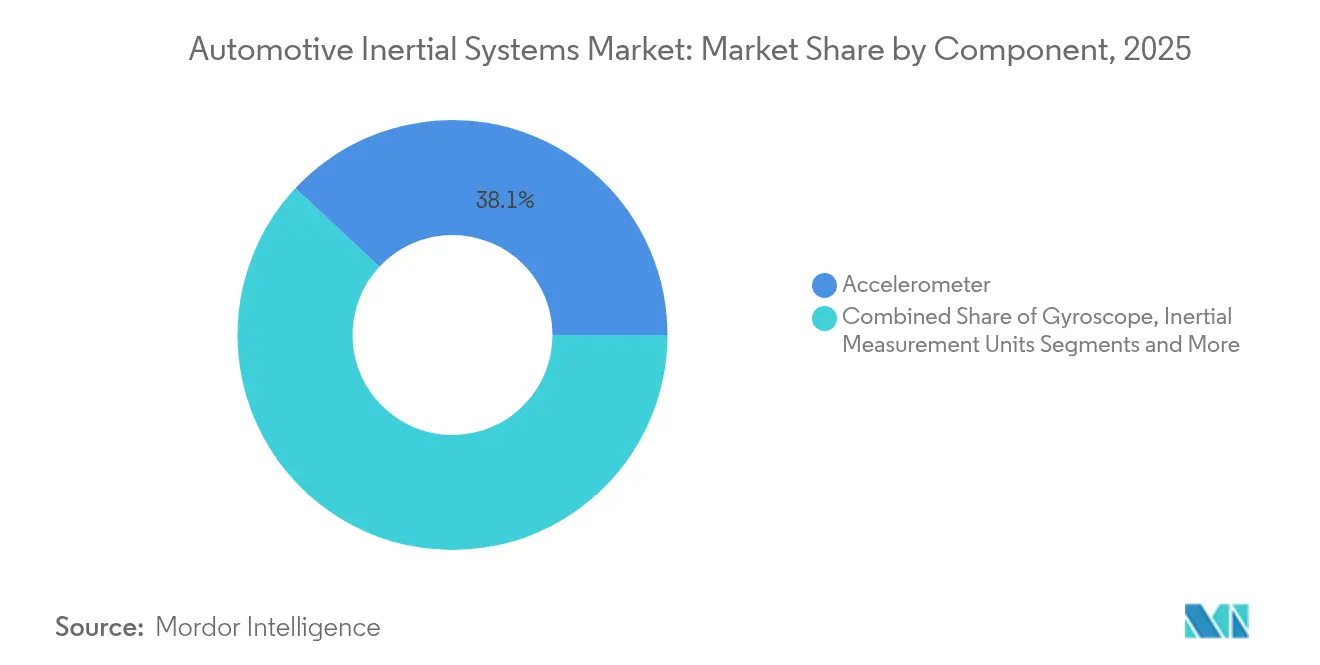

- By component, accelerometers led with 38.05% of the automotive inertial systems market share in 2025, while inertial measurement units are forecast to post the quickest 12.34% CAGR to 2031.

- By vehicle type, passenger cars retained 54.60% of the automotive inertial systems market share in 2025, whereas off-highway machinery is expected to surge at an 11.10% CAGR through 2031.

- By technology, MEMS devices accounted for 64.25% of the automotive inertial systems market share in 2025 and are on track for an 11.63% CAGR over the outlook period.

- By application, electronic stability control captured 40.55% of the automotive inertial systems market share in 2025, yet advanced driver assistance systems are projected to expand at an 11.05% CAGR to 2031.

- By sales channel, OEM-fitted systems dominated with 78.90% of the automotive inertial systems market share in 2025, but the aftermarket is poised for a 11.92% CAGR owing to insurance-driven retrofits.

- By geography, Asia Pacific captured 43.20% of the automotive inertial systems market share in 2025, whereas Africa is expected to witness at an 10.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Inertial Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in MEMS Manufacturing Processes | +2.3% | Global (foundry hubs in Taiwan and Japan) | Medium term (2-4 years) |

| Rising Adoption of Inertial Measurement Units in ADAS | +2.8% | North America, Europe, China | Short term (≤ 2 years) |

| Increasing Vehicle Autonomy Levels Across Passenger Cars | +1.9% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Growing Demand for Precision Farming Machinery | +1.2% | North America, Europe, Brazil, Australia | Medium term (2-4 years) |

| Stringent Safety Mandates on ESC | +2.1% | Global with rapid uptake in India, Middle East and Africa | Short term (≤ 2 years) |

| Emergence of Low-Cost Solid-State IMUs for Two-Wheelers | +0.8% | Asia-Pacific, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advancements In MEMS Manufacturing Processes

Wafer-level packaging combined with through-silicon vias trims MEMS gyroscope footprints by 40% versus 2024 devices, letting Tier 1 suppliers place redundant IMUs inside compact ADAS domain controllers without redesigning multilayer boards.[1]STMicroelectronics press office, “LSM6DSV32X Six-Axis IMU Launch,” STMicroelectronics, st.com Transitioning to 12-inch silicon at Taiwanese fabs reduces per-unit cost by 28% while doubling wafer starts, a key enabler for the sub-USD 10 billion bill-of-materials target many automakers stipulate for entry-segment vehicles. Bosch’s ThELMA co-integration of MEMS and CMOS eliminates bond-wire parasitics and increases bandwidth tenfold to 10 kHz, unlocking active-suspension use cases that previously required bulky discrete electronics. Yield, however, remains hostage to deep-etch defect density; if faults exceed 0.1 cm-², automotive qualification turns uneconomical. Continued capex in vacuum wafer-level packaging is forecast to reduce cavity pressure below 1 Pa, thereby stabilizing the quality factor and bias over high-G crash profiles.

Rising Adoption Of Inertial Measurement Units In ADAS

Driver-assistance features such as automatic emergency braking and lane-keeping support now blend six-axis IMU data with vision and radar streams at 400 Hz for precise ego-motion estimates. Euro NCAP’s 2025 protocol awards full points only when lateral accelerations remain under 0.3 g during emergency maneuvers, a threshold that is viable solely with closed-loop IMU feedback. Integrating discrete accelerometers and gyroscopes into unified IMUs reduces USD 8-12 from the bill of materials and eliminates two separate calibration stages, thereby accelerating adoption, even in cost-sensitive compact cars. China’s GB/T 38186 data-logging rule requires Level 2+ vehicles to record IMU signals at a minimum of 100 Hz, effectively establishing a baseline performance tier that favors solution providers shipping fully characterized modules.

Increasing Vehicle Autonomy Levels Across Passenger Cars

Level 3 rollouts from Mercedes-Benz and BMW in 2024 hinge on redundant IMU arrays meeting ISO 26262 ASIL-D fail-operational rules. Tactical-grade devices, such as Honeywell’s HG4930, offer 0.5 °/h bias stability, keeping dead-reckoning errors under 50 m after 10 minutes of GNSS outage, a critical threshold in dense urban canyons. SAE’s J3216 performance classes set a 1 °/h maximum bias for Level 3, guiding procurement specifications and prompting chipmakers to target sub-USD 100 price points at that performance level. Waymo’s sixth-generation robo-taxi platform demonstrates how coupling high-stability IMUs with lidar point clouds cuts localization drift below 10 cm per kilometer. Cost pressure persists because existing tactical-grade parts exceed USD 500, stimulating R&D into silicon-carbide resonators and wafer-level vacuum encapsulation to narrow the price-performance gap.

Stringent Safety Mandates On Electronic Stability Control

India, Turkey, and the United Nations Economic Commission for Europe all enacted new ESC directives in 2024, covering heavy trucks, buses, and even high-speed tractors. The NHTSA broadened Federal Motor Vehicle Safety Standard 136 to include Class 8 trucks, requiring fleets to retrofit IMU-equipped ESCs by the 2025 model year. Entry-level cost has fallen to under USD 150 for an integrated modulator and six-axis sensor assembly, allowing OEMs to list ESC as standard rather than optional content. The regulatory wave particularly benefits suppliers offering pre-calibrated modules because fleet retrofits often occur outside factory environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Calibration Costs for Safety-Critical Applications | −1.4% | Global, heavier burden for low-volume OEMs | Short term (≤ 2 years) |

| Sensor Signal Drift Limiting Long-Term Navigation Accuracy | −1.1% | Global, particularly acute in GNSS-denied urban corridors | Medium term (2-4 years) |

| Supply Chain Concentration in Few MEMS Foundries | −0.7% | Global exposure to Taiwan and Japan geopolitical risks | Long term (≥ 4 years) |

| Price Pressure from Commodity Accelerometers | -0.3% | Global, strong OEM bargaining power, long-term sourcing contracts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Calibration Costs For Safety-Critical Applications

Automotive-grade IMUs intended for ASIL-D functions must undergo 18-24 hours of multi-axis temperature cycling from −40 °C to +125 °C with 0.1 °C chamber precision, adding USD 12-18 per unit at the factory gate.[2]Analog Devices engineering team, “IMU Calibration for Automotive Applications,” Analog Devices, analog.com ISO 26262 traceability requires the annual recertification of calibration rigs, which can cost over USD 30,000, a non-trivial expense for small Tier 2 suppliers. Polynomial temperature-bias corrections stored in non-volatile memory increase firmware complexity and validation cycles by six to nine months. Machine-learning calibration, promising a two-hour throughput, is still awaiting automotive qualification, delaying near-term relief.

Sensor Signal Drift Limiting Long-Term Navigation Accuracy

MEMS gyroscope bias instability of 5-20 °/h causes dead-reckoning errors that balloon quadratically with time, reaching 200-500 m after a 15-minute GNSS blackout in parking structures. Kalman filtering with zero-velocity updates halves this error but requires the vehicle to stop for several seconds, an impractical constraint in highway tunnels. Continental found that even 0.5 °/h tactical devices drift 150 m after 20 min, forcing OEMs to double up on lidar or camera redundancy. Temperature-gradient spikes of 50-100 °/h during cold starts degrade parking-assist precision when drivers most expect flawless automation. Dual-IMU architectures mitigate the problem but double the sensor cost, while wheel-speed fusion introduces sensitivity to tire pressure and surface friction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Integrated IMUs Consolidate Board Real Estate

Accelerometers held 38.05% of the automotive inertial systems market share in 2025, underpinning airbag triggers, rollover detection, and cost-sensitive ESC. In contrast, integrated IMUs will post a 12.34% CAGR as automakers merge accelerometer and gyroscope channels inside six-axis monolithic packages to shrink printed-circuit footprints. Bosch’s BHI360 couples a MEMS stack with an Arm Cortex-M0 processor that executes sensor-fusion algorithms locally, offloading 30% of the electronic control unit's load.

Standalone gyroscopes now serve niche yaw-rate loops in steer-by-wire applications, while premium inertial navigation systems, costing above USD 1,000, remain confined to high-end autonomy pilots. The migration from discrete accelerometers to IMUs reflects broader semiconductor trends toward co-packaging, which can eliminate two ADC channels, one voltage regulator, and several passive components per board, resulting in a 15-20% reduction in system cost. Integrated IMUs, therefore, command growing design wins despite accelerometers’ numeric supremacy within the automotive inertial systems market.

By Vehicle Type: Off-Highway Equipment Accelerates Sensor Uptake

Passenger cars accounted for a significant 54.60% of total revenue in 2025. However, it's the precision-guided earthmoving and farming equipment that's witnessing the most rapid growth. Off-highway machinery is projected to expand at an impressive 11.10% CAGR. Caterpillar's innovative Grade Control system, utilizing dual IMUs and GNSS receivers, ensures blade height precision within 1 cm, effectively shortening duty cycles 25%.

Meanwhile, John Deere's Machine Sync technology harnesses IMU data on pitch and roll, allowing grain carts to stay within 5 cm of combines during transfers. This precision helps in reducing harvest losses by 3-5%. Komatsu, on the other hand, integrates IMUs into bucket-control loops, achieving trench accuracy of 2 cm and cutting down operator fatigue by a notable 40%. Such advanced applications demand high update rates and robust designs, leading to the quicker adoption of sensors, which outpace their already established use in the passenger car sector.

By Technology: MEMS Retains Dominance Through Cost And Integration

MEMS devices accounted for a commanding 64.25% share of the automotive inertial systems market revenue in 2025. With unit prices hovering below USD 10 and compact form factors under 5 mm³, MEMS devices are set to expand at an impressive 11.63% CAGR. Meanwhile, silicon-carbide resonators in the LSM6DSV32X are pushing the noise density envelope to 0.004 °/s/√Hz, closing the performance gap with pricier fiber-optic gyros.

While fiber-optic and ring-laser gyroscopes are favored in autonomous shuttles and defense applications for their impressive bias stabilities of below 0.01 °/h, their steep price tag, exceeding USD 5,000, and power draw of over 10 W make them a luxury. However, advancements like wafer-level vacuum packaging and atomic-layer deposition of piezoelectric films are bolstering MEMS' dominance. These innovations pave the way for passive energy harvesting, potentially eliminating the need for dedicated power rails. As a result, MEMS technology is firmly established as the gold standard in the automotive inertial systems market.

By Application: ADAS Surpasses ESC As Growth Catalyst

Electronic stability control accounted for 40.55% of total sales in 2025. However, advanced driver assistance systems (ADAS) are on track to grow at an impressive 11.05% CAGR, positioning them to surpass ESC revenue by 2028. Highlighting the advancements, Continental’s MK C2 brake-by-wire boasts a six-axis IMU integrated into its hydraulic block, achieving a swift 100-ms stop time during automatic emergency braking.

Navigation and dead-reckoning modules play a crucial role in maintaining localization within a 50 m radius, even after a 10-minute GNSS dropout, a feature essential for automated parking garages. Furthermore, high-bandwidth inertial measurement units (IMUs) operating at 400 Hz facilitate adaptive damping, effectively reducing body roll by 30% during sudden lane changes. In energy management, Bosch’s eBooster pre-spin electric superchargers utilize pitch-angle forecasts to eliminate lag during hill climbs.

By Sales Channel: Insurance Incentives Propel Aftermarket Retrofits

OEM-installed systems dominated the market, securing a substantial 78.90% share in 2025. This dominance underscores the importance of factory-level calibration and the warranty commitments that accompany these systems. Meanwhile, the aftermarket is poised for robust growth, projected at a 11.92% CAGR. This surge is largely attributed to fleet insurers in North America and Europe, who are slashing premiums by 10-15% for trucks equipped with retrofitted ESC modules.

Bosch has introduced a game-changing drop-in retrofit kit, designed for legacy trucks. This kit, which can be installed in just eight hours at a workshop, comes pre-calibrated, streamlining the process for smaller depots. Further incentivizing the shift, the European Union's General Safety Regulation 2 offers credits of up to EUR 500 (USD 565) per vehicle, alleviating initial financial burdens. However, challenges remain. Installers face calibration issues, requiring scan tools priced between USD 5,000 and USD 10,000 to adjust mounting-angle offsets. Yet, the investment pays off, with savings on insurance leading to a full return within three years.

Geography Analysis

Asia-Pacific commanded 43.20% of 2025 revenue as China built 30 million light vehicles and India rose to the world’s third-largest market at 5 million units. China’s ESC test spec requires yaw-rate tracking within 5% during sine-with-dwell maneuvers, favoring six-axis IMUs with 400 Hz update rates. Japan subsidizes 30% of ADAS retrofit bills for commercial fleets, boosting demand for aftermarket modules, while South Korea’s Sejong testbed mandates dual-redundant sensors for Level 4 pilots.

Africa is the fastest-growing region, with a 10.72% CAGR, driven by South Africa’s Automotive Production and Development Programme and Egypt’s tariff reduction on sensor imports from 40% to 10%. South Africa produced 631,000 vehicles in 2024, and OEMs have begun equipping entry-level trims with ESC to meet the harmonized rules of the Southern African Development Community. Egypt attracted USD 200 million of sensor-module investment clustered around the 10th of Ramadan industrial zone, positioning Cairo as a regional supply hub. North America and Europe focus on ADAS upgrades in otherwise saturated ESC environments. NHTSA’s pending rule for automatic emergency braking on heavy trucks will obligate IMU-based rollover detection on 400,000 U.S. Class 7-8 units annually. The European Union manufactured 13.2 million vehicles in 2024, and ties 2025 Euro NCAP star ratings to lateral-control metrics that require real-time inertial feedback. Middle East markets, which imported 1.8 million vehicles in 2024, align with Gulf Cooperation Council standards that enforce ESC for light commercial vehicles. South America lags on ADAS but will phase Mercosur Regulation 140 for commercial-vehicle ESC by 2027, opening retrofit opportunities in Brazil’s 2.1 million-unit industry.

Competitive Landscape

Bosch, Continental, and STMicroelectronics hold significant share of the automotive inertial systems market through vertical ownership of MEMS designs, ASICs, and ADAS electronic control units. Bosch’s SMI230 meets ASIL-D with 0.007 °/s/√Hz noise, anchoring Level 3 autonomy bids across multiple OEMs.[5]Bosch press office, “SMI230 IMU ASIL-D Qualification,” Bosch, bosch.com Continental complements proprietary sensors with a camera-radar fusion stack for one-stop ADAS sourcing. STMicroelectronics is expanding its Italian 12-inch MEMS capacity to lift annual output to 200 million units by 2027, ensuring supply resiliency.

Challengers include Analog Devices, now equipped with Inertial Labs’ 0.1 °/h tactical designs, and Infineon, which combines environmental and inertial sensing in a unified XENSIV package to reduce board real estate. Aceinna and VectorNav court smaller automakers by offering open-source algorithms that reduce integration time from 18 months to six. Dependence on TSMC and GlobalFoundries remains the primary systemic risk; the Kumamoto earthquake halted Sony’s accelerometer output for six weeks in 2024, resulting in delayed Tier 1 shipments of up to 16 weeks.

Product roadmaps center on bias-stability gains and system-level integration. Analog Devices’ ADIS16507 offers 0.5 °/h bias via temperature-compensated resonators. Infineon’s XENSIV adds barometric, humidity, and temperature channels inside a 3 mm × 3 mm footprint to speed chassis-control deployment. ISO 26262 certification costs USD 0.5-1 million per design, preserving the incumbents’ lead over start-ups.

Automotive Inertial Systems Industry Leaders

Robert Bosch GmbH

Continental AG

Honeywell International Inc.

STMicroelectronics N.V.

Murata Manufacturing Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: iNGage, a fabless company specializing in high-performance, multi-axis inertial MEMS navigation sensors for autonomous systems, has secured USD 7 million in its inaugural funding round. This capital infusion aims to expedite the commercial rollout of its cutting-edge technology. Reliable positioning is crucial for automotive applications and survey mapping. However, current capacitive MEMS sensors exhibit rapid drift, and while fibre-optic gyroscopes (FOGs) offer precision, they, along with other bulky inertial systems, often come with prohibitive costs or impracticalities.

- July 2025: ST Acquires NXP’s MEMS Unit, Zeroing in on Automotive Ambitions. The MEMS automotive market is expanding, driven by enhanced functionalities that enhance safety, facilitate electrification, automate processes, and improve connectivity in vehicles.

- June 2025: Trimble and InvenSense, a subsidiary of TDK, have partnered to develop a cutting-edge navigation solution. This solution integrates Trimble's ProPoint Go engine and RTX correction service with TDK's SmartAutomotive Inertial Measurement Units (IMUs) from InvenSense. As a result, customers can witness enhanced accuracy and reliability in positioning and navigation, benefiting a range of automotive and IoT applications.

- June 2025: TDK Corporation has rolled out the InvenSense SmartAutomotive IAM-20680HV, a premium 6-axis IMU, for global distribution. This IMU caters to diverse in-cabin applications, ensuring resilience in extreme conditions, enduring temperatures up to +125 °C, and guaranteeing performance at +105 °C. Leveraging TDK's robust technology and design, this component has established a quality benchmark in the automotive market, particularly for non-safety-related applications.

Global Automotive Inertial Systems Market Report Scope

Automotive inertial systems utilize Inertial Measurement Units (IMUs), which comprise gyroscopes (rotation sensors) and accelerometers (motion sensors), to monitor a vehicle's position, velocity, and orientation (roll, pitch, and yaw). By gauging shifts from a known starting point, these technologies play a crucial role in autonomous driving and safety systems, particularly in areas where GPS is unavailable. They deliver consistent and precise data for functions such as lane keeping, stability control, and accurate localization. These systems can operate autonomously or in conjunction with GPS/GNSS, ensuring enhanced navigation reliability and accuracy.

The Automotive Inertial Systems Market Report is Segmented by Component (Accelerometer, Gyroscope, Inertial Measurement Units, Inertial Navigation Systems, and Other Components), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, and Off-Highway Vehicles), Technology (MEMS, Fiber-Optic Gyro, Ring-Laser Gyro, and Others), Application (Electronic Stability Control, Advanced Driver Assistance Systems, Navigation and Dead-Reckoning, and Suspension and Chassis Control), Sales Channel (OEM-Fitted, and Aftermarket), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Accelerometer |

| Gyroscope |

| Inertial Measurement Units (IMU) |

| Inertial Navigation Systems (INS) |

| Other Components |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Off-Highway Vehicles |

| MEMS |

| Fiber-Optic Gyro |

| Ring-Laser Gyro |

| Others |

| Electronic Stability Control |

| Advanced Driver Assistance Systems |

| Navigation and Dead-Reckoning |

| Suspension and Chassis Control |

| OEM-Fitted |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Accelerometer | ||

| Gyroscope | |||

| Inertial Measurement Units (IMU) | |||

| Inertial Navigation Systems (INS) | |||

| Other Components | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Heavy Commercial Vehicles | |||

| Off-Highway Vehicles | |||

| By Technology | MEMS | ||

| Fiber-Optic Gyro | |||

| Ring-Laser Gyro | |||

| Others | |||

| By Application | Electronic Stability Control | ||

| Advanced Driver Assistance Systems | |||

| Navigation and Dead-Reckoning | |||

| Suspension and Chassis Control | |||

| By Sales Channel | OEM-Fitted | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the automotive inertial systems market in 2026?

The automotive inertial systems market size is USD 3.43 billion in 2026, with a forecast CAGR of 10.31% over 2026-2031.

Which component is growing the fastest?

Integrated six-axis inertial measurement units are forecast to grow at 12.34% CAGR as automakers consolidate discrete sensors.

Why are MEMS sensors dominant over fiber-optic gyros?

MEMS devices cost under USD 10, occupy less than 5 mm³, and integrate easily with automotive ASICs, meeting most performance targets at a fraction of the price.

Which region is expanding quickest?

Africa leads regional growth at a 10.72% CAGR owing to production incentives in South Africa and tariff cuts in Egypt.

What is the main supply-chain risk?

Concentration of MEMS wafer output in two foundries exposes the market to geopolitical and natural-disaster disruptions.

How does aftermarket retrofitting benefit fleets?

Installing ESC retrofit kits can cut commercial-vehicle insurance premiums by 10-15%, delivering payback inside three years.

Page last updated on: