Automotive Shielding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 24.17 Billion |

| Market Size (2031) | USD 29.84 Billion |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

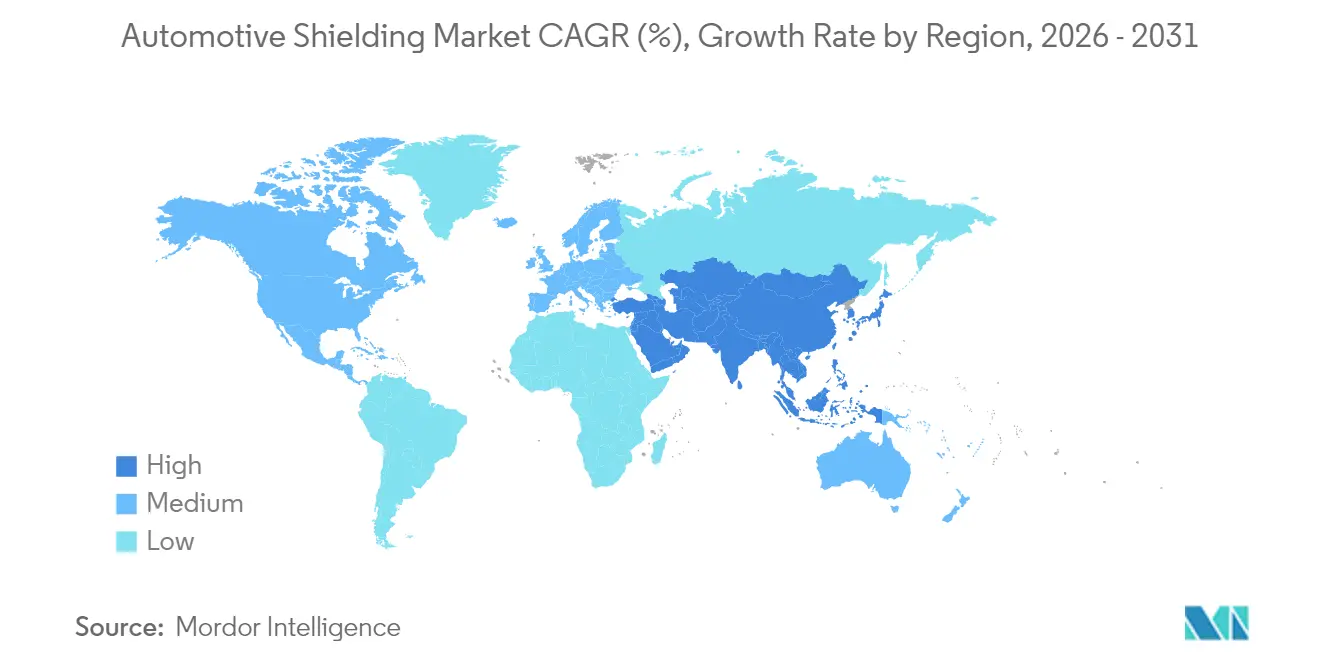

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

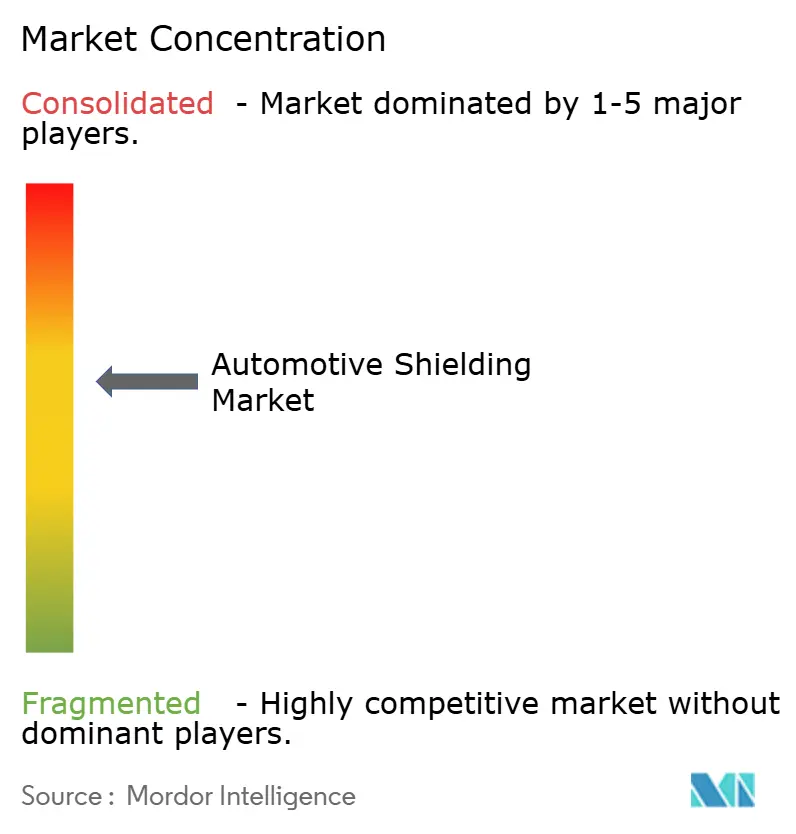

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Shielding Market Analysis by Mordor Intelligence

Automotive Shielding Market size in 2026 is estimated at USD 24.17 billion, growing from 2025 value of USD 23.17 billion with 2031 projections showing USD 29.84 billion, growing at 4.31% CAGR over 2026-2031. Continued electrification, tighter emissions rules, and the spread of advanced driver assistance systems push OEMs to adopt integrated electromagnetic interference and thermal solutions at the design stage. High-voltage 400 V and 800 V electric architectures, wider use of silicon-carbide inverters, and dense electronics packages raise both frequency and heat loads, making shielding a strategic rather than tactical purchase.

Key Report Takeaways

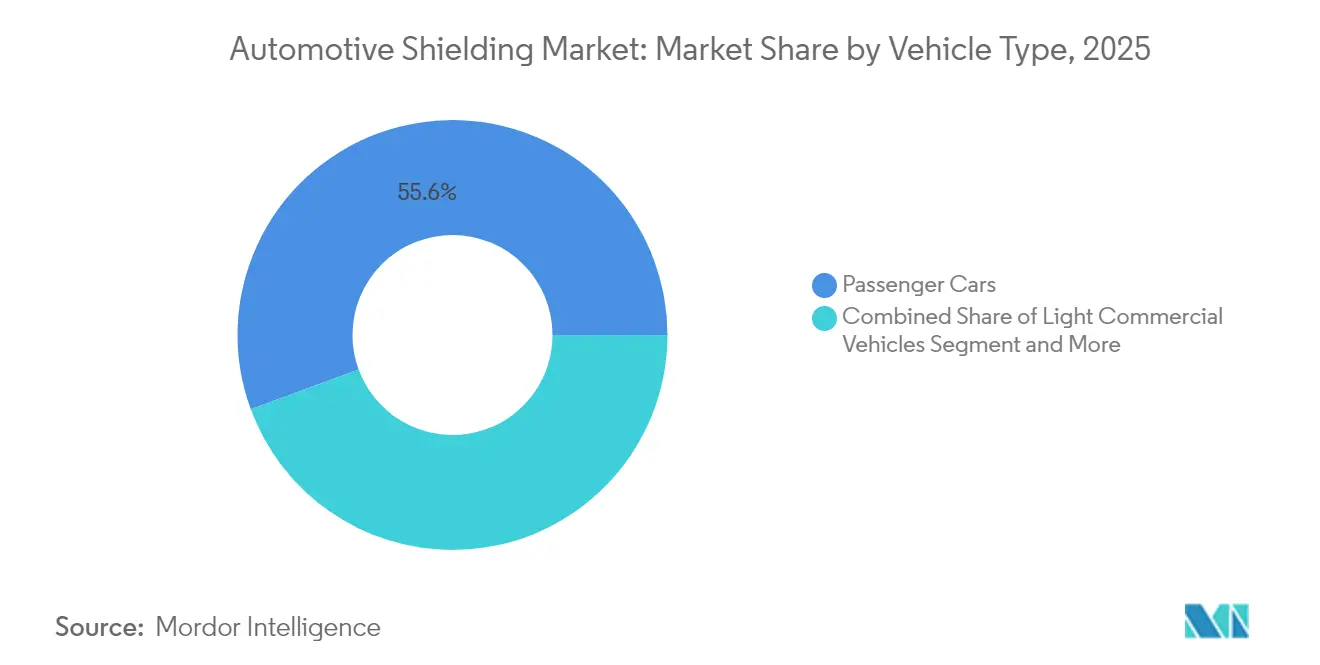

- By vehicle type, passenger cars led with 55.62% of automotive shielding market share in 2025, while the segment is set to expand at a 4.96% CAGR through 2031.

- By shielding type, heat solutions accounted for 60.58% revenue in 2025 in the automotive shielding market, while EMI products are forecast to record the fastest 4.72% CAGR through 2031.

- By propulsion technology, internal combustion engines held 55.12% share in 2025, whereas battery electric vehicles are projected to grow at 5.06% CAGR during the same period.

- By application, powertrain systems captured 48.21% of the automotive shielding market size in 2025; battery and high-voltage systems will advance at a 4.93% CAGR to 2031.

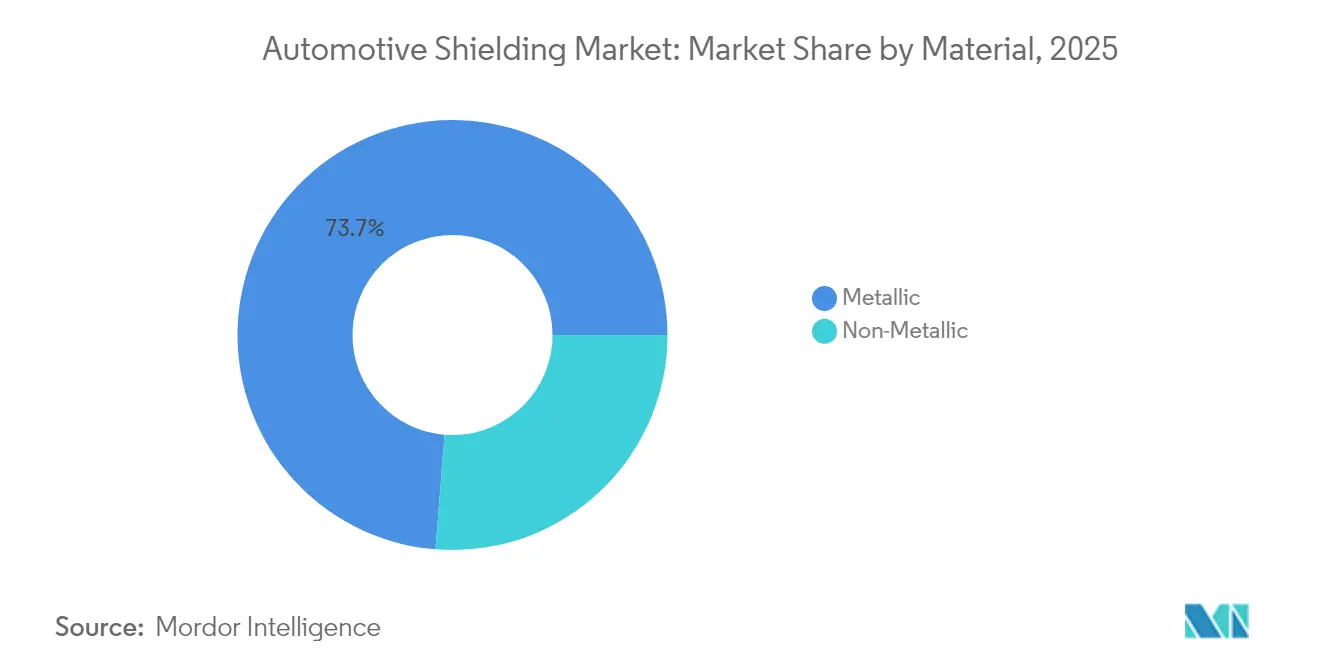

- By material, metallic formats commanded 73.74% share in 2025 in the automotive shielding market, while non-metallic composites constitute the fastest-rising class at a 4.21% CAGR.

- By sales channel, OEM programs represented 83.55% of revenue in 2025; the aftermarket is expected to post a 4.48% CAGR through 2031.

- By geography, Asia Pacific dominated the automotive shielding market with a 38.31% share in 2025 and is poised to record the highest 4.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Shielding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Proliferation | +1.2% | Global, with APAC leading adoption | Medium term (2-4 years) |

| Stricter Emission Norms | +0.8% | North America and EU regulatory focus | Short term (≤ 2 years) |

| ADAS Electronics Density | +0.7% | Global, premium segments first | Medium term (2-4 years) |

| SiC-Based High-Voltage Inverters | +0.6% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Turbo-Charged ICE Adoption | +0.5% | Global, with emerging markets acceleration | Short term (≤ 2 years) |

| Gigacasting Body Panels | +0.4% | North America and EU, Tesla-led adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV Proliferation Intensifies EMI & Battery Thermal Shielding Demand

Electric vehicles require roughly 30% more aluminum than comparable ICE models, which raises the need for large-area thermal barriers in the automotive shielding market that slow down thermal runaway between cells.[1]“NORYL™ NHP8000VT3 Resin Targets EV Battery Insulation,” SABIC, sabic.com High-voltage packs emit broad-band noise that can disturb GPS, cellular, and in-car entertainment systems. Material suppliers now market resin films, such as NORYL NHP8000VT3, that combine low flame spread with dielectric stability at elevated temperatures. As 800 V systems become common, exemplified by FORVIA HELLA’s 1200 V CoolSiC MOSFET-based DC-DC stage, attenuation targets extend well beyond the 1 MHz ceiling of legacy components. Because each EV needs more shielding content than an ICE vehicle, growth in EV sales magnifies unit revenue even when commodity prices remain under pressure.

Stricter Fuel-Efficiency / Emission Norms Drive Lightweight Heat Shields

The EPA’s multi-pollutant rule for model years 2027-2032 is pushing OEMs toward average fleet emissions of 85 g CO₂ per mile, accelerating innovation in the automotive shielding market. Compliance forces weight savings that ripple into heat management, prompting substitution of stamped steel shields with thin composite laminates. Research from the University of Birmingham shows aerogel-based blankets that cut thermal conductivity by a factor of ten and weigh a hundred times less than ceramic solutions.[2]“Ultralight Insulation Materials for Automotive Heat Management,” University of Birmingham, bham.ac.uk Ford’s use of composite C-braces trimmed more than half of mass relative to aluminum in the Bronco Raptor, illustrating real-world uptake. Because penalties escalate quickly, automakers demand validated materials in the next 24 months, creating a near-term pull for scaling lightweight shielding production.

ADAS Electronics Density Raises EMC Complexity

Modern radar at 77 GHz, camera processors running multi-gigabit links, and LiDAR optics all interact across wide frequency bands in the automotive shielding market. CISPR 25 testing has found infotainment boards to exceed limits by 2.51 dB in the 555-960 MHz range, an overage that requires conductive gaskets around stacked PCBs. Bourns responded with AEC-Q200-graded shielded inductors that radiate lower magnetic fields, mitigating cross-talk at the component level.[3]“AEC-Q200 Shielded Inductors for ADAS Power Lines,” Bourns Inc., bourns.com As OEMs combine several driver-assistance tasks on single ECUs, local heat densities rise, making simultaneous thermal and EMI protection essential. Demand therefore skews toward premium, space-saving foils that keep thin-wall enclosures below 40 °C surface temperature while providing at least 60 dB shielding effectiveness.

SiC-Based High-Voltage Inverters Spur Next-Gen EMI Materials

Silicon-carbide switches toggle up to 100 kHz, five times the speed of silicon IGBTs, generating high-frequency edges that leak through traditional copper sleeves in the automotive shielding market. Double-sided-cooled modules now reach stray inductance values as low as 4.7 nH, but system-level emissions remain a risk, propelling interest in novel MXene layers exhibiting conductivity near 35,000 S/cm. The samples already block over 80 dB at 18 GHz, pointing to future standard specifications for 800 V drivetrains. Suppliers that master hybrid foil-polymer stacks able to stay stable above 200 °C without delamination will gain early design wins in SiC-centric inverter platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Aluminum and Specialty Alloy Prices | -0.4% | Global, with Asia Pacific manufacturing concentration | Short term (≤ 2 years) |

| Rising Recyclability Compliance Costs | -0.3% | EU leading, North America following | Medium term (2-4 years) |

| Non-Uniform Global EMI Test Standards | -0.2% | Global, with regulatory fragmentation | Medium term (2-4 years) |

| ECU Consolidation in Software-Defined Vehicles | -0.2% | Global, premium segments first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Aluminum & Specialty Alloy Prices

Metallic inputs made up 74.36% of volume in 2024 in the automotive shielding market and remain exposed to swings that erode supplier margins. Primary aluminum is contested by aerospace, construction, and transportation sectors, producing price spikes that traditional hedging cannot fully offset. Recycled aluminum uses 95% less energy but has limited availability, as scrappage flows do not match surging demand from EV body structures. Specialty nickel alloys that withstand turbocharger exhaust gas at 900 °C, such as VDM C-264, trade at premiums that smaller suppliers struggle to absorb. Concentrated smelting capacity in Asia Pacific further amplifies susceptibility to policy changes, shipping logjams, or energy rationing events.

Rising Recyclability Compliance Costs

The European Union mandates 25% recycled plastic in new vehicles by 2030 and is reviewing a 30% baseline for steel, adding EUR 28 billion in first-year compliance outlays for small and medium enterprises in the automotive shielding market. Shielding makers must now set up closed-loop recovery for laminated foils and remove copper from recycled steel to automotive-grade thresholds. Extended Producer Responsibility rules shift disposal charges onto suppliers, raising long-term liabilities and making cash-intensive capital upgrades unavoidable. The patchwork nature of global rules forces manufacturers to redesign part tracking and documentation systems to satisfy multiple certification pathways, stretching engineering resources that could otherwise fund product innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Remain the Anchor of Market Demand

Passenger cars generated 55.62% of revenue in 2025, underscoring their sheer production volume and standardized electronics content. The segment’s 4.96% CAGR through 2031 benefits from mainstream rollout of level-2 ADAS, infotainment over-the-air updates, and efficient turbocharged engines that all require robust electromagnetic and heat protection. OEMs replace discrete brackets with large die-cast aluminum subframes, prompting integrated shield designs that reduce assembly steps and shave grams off mass budgets.

Growing electronic complexity in passenger vehicles offers stable margins because each model refresh triggers new validation programs. Suppliers that pre-qualify materials under OEM-specific standards gain lifetime contracts spanning 5–7 years, reinforcing revenue visibility in the automotive shielding market. Emerging low-cost brands in Southeast Asia also adopt similar EMI benchmarks to gain export clearance, extending the addressable base. The interplay of high build counts and rising per-car shield spend keeps this cornerstone segment instrumental to forecasts through 2030.

By Shielding Type: Heat Products Hold Majority, EMI Solutions Accelerate

Heat shields still capture 60.58% of revenue because downsized turbo engines and after-treatment systems operate above 1,000°C exhaust gas temperatures. Engine encapsulation to meet warm-up targets further expands under-hood blanket use. However EMI formats post the swiftest 4.72% CAGR as every new sensor or power module adds high-frequency interference.

Lightweight hybrid materials combining aluminum foil with polymer layers now replace multi-piece steel boxes, cutting up to 40% mass while meeting 60 dB attenuation at 1 GHz. Heat shielding nevertheless remains essential because ICE platforms still represent more than half of vehicle production in 2030.

By Propulsion Technology: ICE Leads While Battery EVs Capture Momentum

Internal combustion engines retained 55.12% market share in 2025 thanks to their large installed base and the ongoing popularity of turbocharged gasoline units in cost-sensitive markets. That dominance holds yet diminishes gradually as battery EV deliveries widen. Battery EVs, expanding at a 5.06% CAGR, shift shielding design from manifold wraps toward pack isolation mats, dielectric films, and inverter housings.

Hybrid electric vehicles straddle both needs, integrating under-hood heat protection with power-stage EMI shields, providing suppliers dual-revenue opportunities per unit. Fuel-cell vehicles, still niche, demand custom hydrogen tank blankets and stack diffusers, seeding small yet technically demanding orders. This propulsion mix sustains demand diversity and extends product life cycles for multi-functional materials.

By Application: Powertrain Tops Revenue, Battery Systems Drive Growth

Powertrain functions accounted for 48.21% of the automotive shielding market size in 2025, bundling exhaust after-treatment, turbo housings, e-motor end-shields, and gearbox cooling fins. Battery and high-voltage domains show the fastest 4.93% CAGR, helped by thermal-runaway risk mitigation that remains a headline safety metric.

Advanced driver assistance stacks also expand steadily, each radar module and LiDAR emitter requiring compartmental shielding that blocks cross-talk without adding glare or weight to the sensor housings. Infotainment units face intense cost scrutiny, yet the rise of 5G telematics introduces new RF bands, lifting basic shielding specifications. Multipurpose laminate inserts that satisfy both 24 GHz radar and 77 GHz packages give suppliers cross-application leverage, reducing part proliferation and tooling costs.

By Material: Metallics Dominate, Composites Gain Traction

Metal-based solutions delivered 73.74% revenue in 2025, with aluminum favored for its mix of conductivity and density. Stamped steel panels still appear near exhaust paths where peak temperatures exceed aluminum’s softening point. Non-metallic composites climb at 4.21% CAGR as thermoplastic EMI pellets and carbon-fiber cloth offer more than half of mass savings. Polymer matrices infused with conductive graphite now meet 50 dB attenuation across 1–10 GHz while remaining weldable to polyamide brackets, simplifying assembly.

The automotive shielding industry also pursues biomass fillers to reach recycled-content targets without sacrificing flame retardancy. Over the forecast period suppliers that perfect hybrid layups can tap both weight and sustainability priorities, capturing conversion business away from single-metal parts.

By Sales Channel: OEM Contracts Prevail, Aftermarket Builds Pace

OEM pipelines represented 83.55% revenue in 2025 due to rigorous validation, PPAP documentation, and life-cycle traceability. High integration of shields into structural castings locks in supply deals from vehicle concept stage through to mid-cycle facelift. The aftermarket’s 4.48% CAGR reflects a growing global fleet age that has surpassed a decade in several regions.

Higher electronic content per vehicle means more complex failures and replacement cycles. Independent repair networks now stock modular zone controllers whose shields can be swapped rather than scrapped, opening fresh volume for certified parts. Digitally tracked part numbers, QR-encoded on flexible foils, ensure compliance with tamper-proofing and recyclability codes, giving aftermarket players the confidence to handle advanced shielding units.

Geography Analysis

Asia Pacific held 38.31% of global revenue in 2025 and is poised for a 4.45% CAGR through 2031. China contributes the bulk of electric-vehicle demand, and with over 60% of world EV production, the country orders high-volume, high-specification battery pack shields that meet 800 V insulation levels. Japan’s leadership in auto-grade semiconductors keeps its domestic suppliers at the cutting edge of EMC materials, supporting premium contracts for radar and camera assemblies. South Korea’s battery cell innovation catalyzes local demand for thermal runaway barriers, while its exports propel cross-border content growth. Manufacturing density, cost-effective labor, and integrated metal smelters underpin the region’s price competitiveness, which in turn helps it secure new model programs from global OEMs.

North America commands a sizeable share anchored by stringent EPA and NHTSA mandates that raise shield performance thresholds. Domestic OEM investments in battery packs, such as the joint ventures launched in Tennessee and Ontario, create local pull for composite dielectric films and multi-layer foils. The region’s slower EV rollout relative to Asia is offset by high electronics penetration in pickup, SUV, and premium segments, each loaded with radar, camera, and infotainment hardware. Canada’s emergence as an integrated battery corridor strengthens regional supply resilience, encouraging suppliers to set up metallic heat-shield stamping and polymer compounding lines near new cell plants.

Europe benefits from ambitious sustainability frameworks that obligate recycled content percentages and detailed end-of-life reporting. German OEMs buy sophisticated EMI textiles and ceramic-matrix heat shields that align with luxury-vehicle brand positions. South America and Middle East & Africa remain smaller but ascending contributors. Brazil’s local content rules encourage stamping of aluminum heat shields for flex-fuel engines, while growing rooftop solar installations spill surplus conductive sheet capacity into the automotive chain. In the Gulf states, premium import volumes and large commercial fleets needing heavy-duty ventilation create demand for robust EMI meshes that tolerate sand-dust infiltration.

Competitive Landscape

The market is moderately fragmented with a cluster of long-standing materials specialists dominating high-volume orders. Tenneco integrates exhaust heat wraps and under-floor shields directly into its Clean Air modules, leveraging its OEM relationships to lock in multi-year contracts. Laird Performance Materials focuses on thin EMI foils and conductive elastomers, benefiting from cross-pollination with its consumer electronics division to shorten automotive product cycles. Henkel supplies thermally conductive adhesives that bond shield laminates to magnesium housings, enabling one-step foil attachment during assembly. Collectively these incumbents build protective moats around their portfolios through in-house validation labs and global application-engineering teams offered on retainer to automakers.

Strategic moves center on vertical integration and hybrid material R&D. Companies are acquiring foil producers, polymer compounders, and testing houses to secure supply and compress lead times. Electrospinning and vapor-deposition methods yield nanofiber layers that combine high surface area with low areal weight, letting the same part manage 200 °C radiant heat and 70 dB interference. Suppliers able to deliver such multifunctional solutions win platform awards that displace legacy metal stampings. Joint ventures linking shield makers with semiconductor packaging firms are emerging, recognizing that future architectures blur lines between chip carrier, thermal spreader, and EMI cage.

Disruptors come from academia and start-ups commercializing ultralight insulators with orders-of-magnitude advances in thermal resistance. Aegis Fibretech’s aerogel fabrics, spun out of university labs, claim conductivity 10× lower than current blanket technology and are moving into pilot production. Traditional suppliers answer by accelerating MXene and graphene composite programs. Despite fragmentation in lower-value sheet metal, the top five firms still command roughly near to half of global revenue, maintaining moderate concentration while leaving space for niche innovators to capture specialized subsegments.

Automotive Shielding Industry Leaders

Tenneco Inc.

Laird Performance Materials

3M Company

Dana Incorporated

Autoneum Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Tenneco secured a strategic investment from Apollo Fund X to accelerate Clean Air and Powertrain shielding projects aimed at EV platforms.

- January 2025: FORVIA HELLA chose Infineon’s CoolSiC Automotive MOSFET 1200 V for next-generation 800 V DC-DC converters, spotlighting the push for SiC components that demand high-frequency EMI covers.

- December 2024: NHTSA issued FMVSS 305a, tightening safety requirements for electric propulsion batteries, adding new performance tests for encapsulation and electrical isolation in crash events.

Global Automotive Shielding Market Report Scope

Automotive Shielding is used to protect the automotive equipment and parts from the heat generated and electromagnetic induction from several electric devices present in the system. The Automotive Shielding market report covers detailed study on latest trends and developments in metal casting which is segmented by Vehicle Type (Passenger car and Commercial Vehicle), by Shielding Type (Heat Shielding and Electromagnetic Induction Shielding), and Geography. Along with a detailed study on major players, their strategies, technological innovations and financials are also included in the report.

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Heavy Commercial Vehicles (HCV) |

| Heat Shielding |

| Electromagnetic Interference (EMI) Shielding |

| Internal Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) |

| Battery Electric Vehicle (BEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| Powertrain (Engine/Exhaust) |

| Battery & High-Voltage Systems |

| ADAS & Safety Electronics |

| Infotainment / Connectivity |

| Metallic (Aluminum, Stainless Steel, Copper) |

| Non-Metallic (Composites, Foils, Fabrics) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCV) | ||

| Heavy Commercial Vehicles (HCV) | ||

| By Shielding Type | Heat Shielding | |

| Electromagnetic Interference (EMI) Shielding | ||

| By Propulsion Technology | Internal Combustion Engine (ICE) | |

| Hybrid Electric Vehicle (HEV) | ||

| Battery Electric Vehicle (BEV) | ||

| Fuel-Cell Electric Vehicle (FCEV) | ||

| By Application | Powertrain (Engine/Exhaust) | |

| Battery & High-Voltage Systems | ||

| ADAS & Safety Electronics | ||

| Infotainment / Connectivity | ||

| By Material | Metallic (Aluminum, Stainless Steel, Copper) | |

| Non-Metallic (Composites, Foils, Fabrics) | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the automotive shielding market?

The automotive shielding market is worth USD 24.17 billion in 2026 and is expected to reach USD 29.84 billion by 2031.

Which region leads automotive shielding demand?

Asia Pacific holds 38.31% of global revenue in 2025 and shows the fastest 4.45% CAGR through 2031 due to high vehicle output and strong EV penetration.

Which shielding type is growing the fastest?

EMI products are the fastest-growing type, expanding at a 4.72% CAGR because rising electronics density elevates electromagnetic interference concerns.

How will battery electric vehicles affect shielding requirements?

Battery electric vehicles need more shielding per unit than ICE cars, especially around high-voltage packs and SiC inverters, driving above-average demand growth of 5.06% CAGR for related materials.

Why are lightweight materials important in automotive shielding?

Tighter fuel-efficiency and emissions rules force OEMs to cut mass, prompting the shift from steel to composites that provide equal or better heat and EMI performance at lower weight.

What is the main restraint on market growth?

Volatile aluminum and specialty alloy prices add cost uncertainty, while recyclability mandates raise compliance costs, jointly trimming the forecast CAGR by 0.7 percentage points.

Page last updated on: