Market Overview

| Study Period | 2025 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

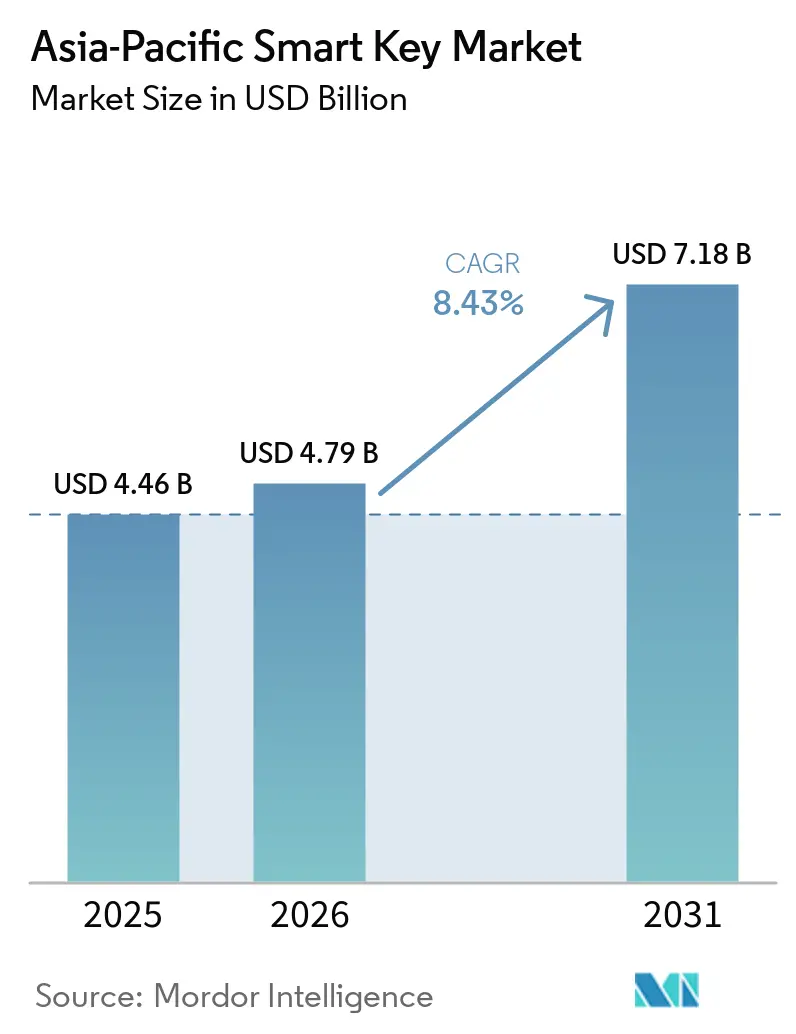

| Base Year Market Size (2025) | USD 4.46 Billion |

| Market Size (2026) | USD 4.79 Billion |

| Market Size (2031) | USD 7.18 Billion |

| Growth Rate (2026 - 2031) | 8.43% CAGR |

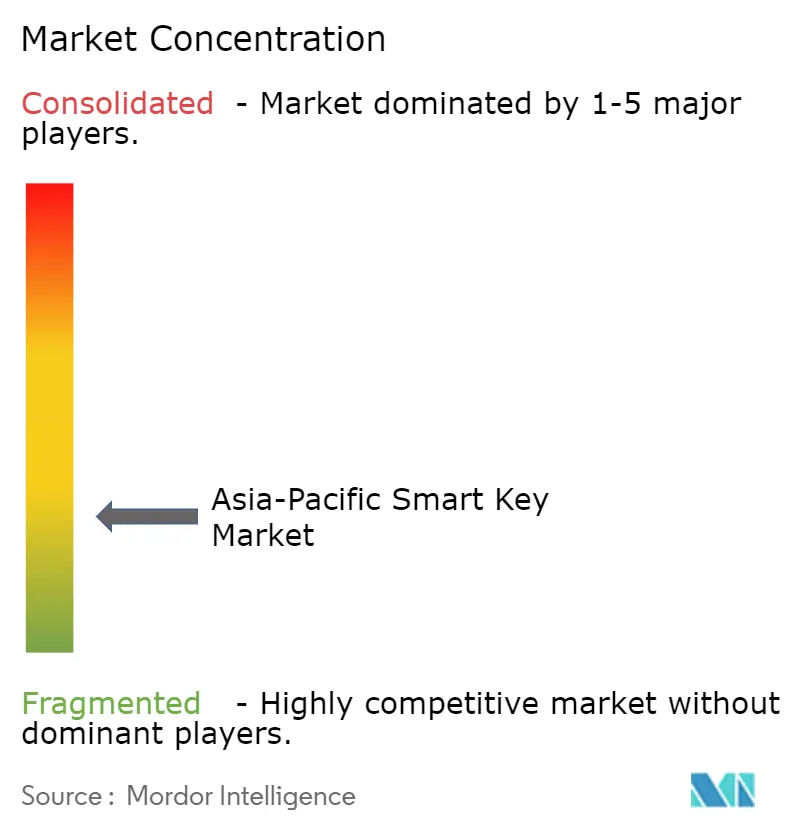

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Smart Key Market Analysis by Mordor Intelligence

The Asia-Pacific smart key market size is expected to grow from USD 4.46 billion in 2025 to USD 4.79 billion in 2026 and is forecast to reach USD 7.18 billion by 2031 at 8.43% CAGR over 2026-2031. The market is expanding as residential buildings, hotels, vehicles, and enterprise sites shift from mechanical access to digital credentials that can be managed, updated, and monitored. Demand is also being reinforced by rising urban density, broader smart city spending, more short-stay accommodation formats, and stronger enterprise interest in audit-ready access records. Revenue is shifting steadily from one-time hardware sales toward software, credential management, and service-led access layers, which is changing how vendors compete and where margins are built. Adoption is strongest where wallet-based entry, cloud management, and retrofit-friendly installation can work together without forcing a full replacement of legacy systems. The Asia-Pacific smart key market is therefore growing on both replacement and new-deployment demand, while competition is increasingly shaped by standards alignment, cybersecurity assurance, and the ability to serve multiple end-use settings from a single platform.

Key Report Takeaways

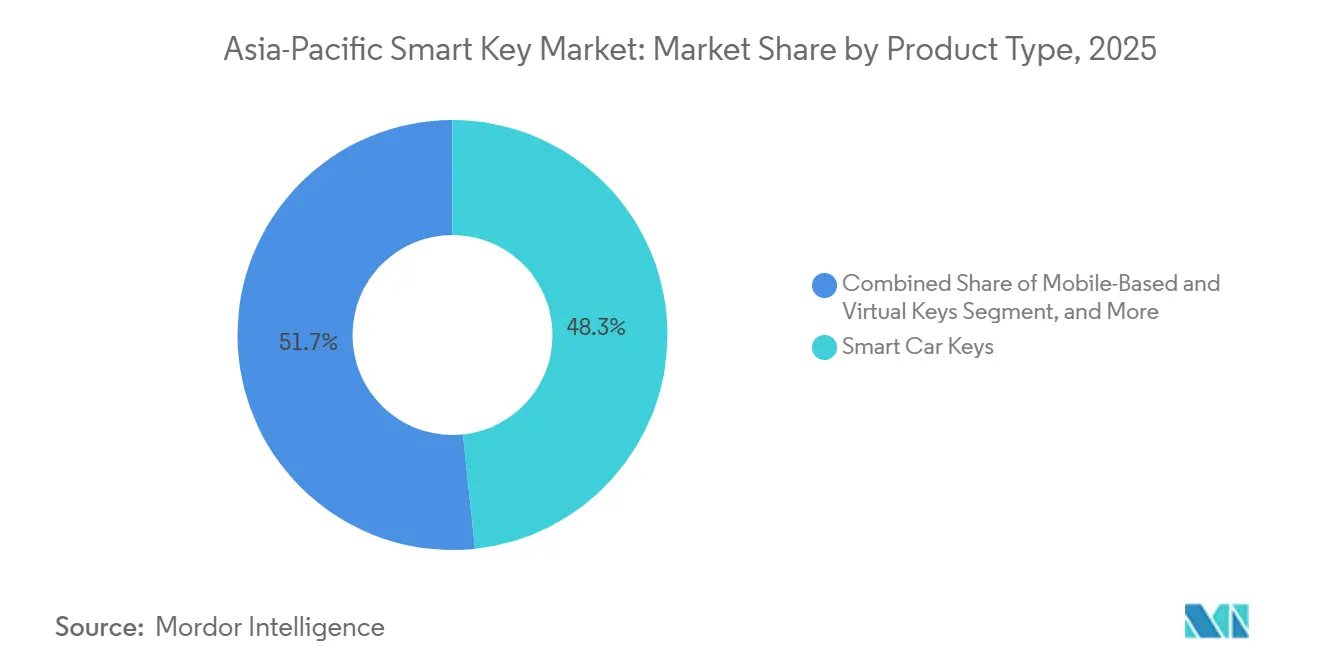

- By product type, Smart Car Keys held 48.33% share in 2025, while Mobile-Based and Virtual Keys are forecast to expand at a 9.03% CAGR through 2031.

- By technology, RFID held 34.87% share of the Asia-Pacific smart key market in 2025, while Bluetooth Low Energy is projected to record the highest CAGR at 9.43% through 2031.

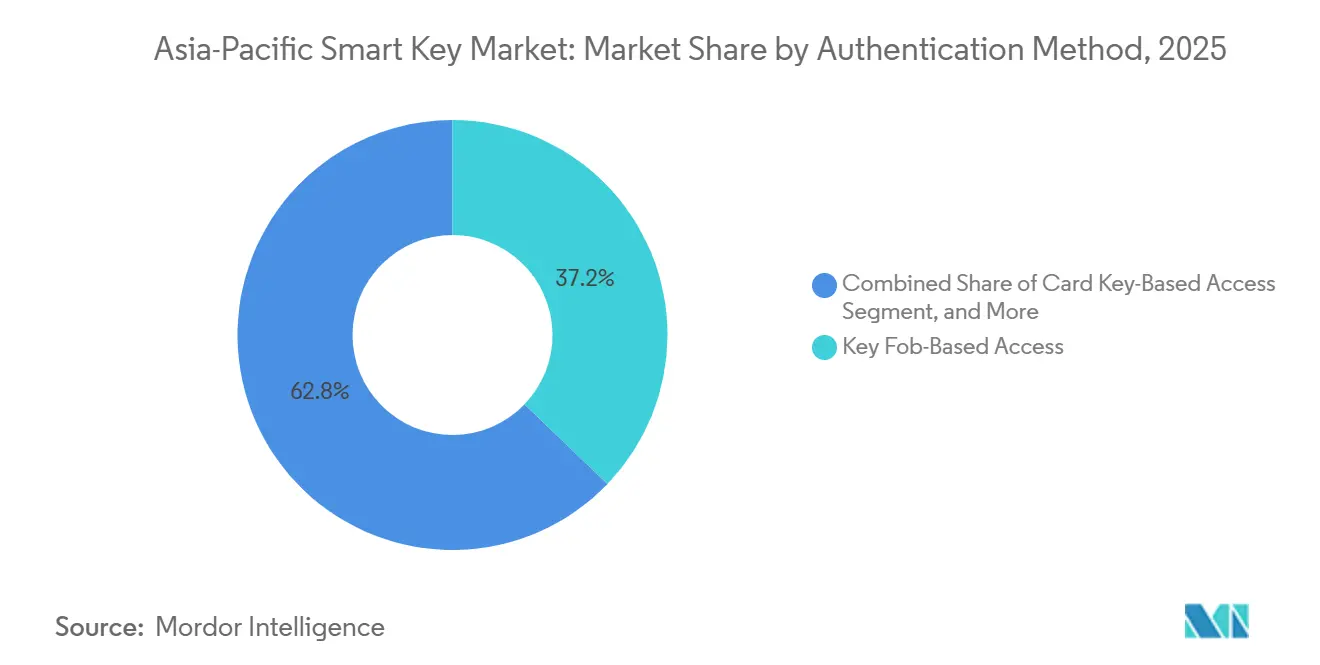

- By authentication method, key fob-based access accounted for 37.18% of the Asia-Pacific smart key market share in 2025, while smartphone-based access is expected to grow fastest at a 9.21% CAGR through 2031.

- By end-user industry, Enterprise and Commercial Buildings led with a 31.59% share in 2025, while Hospitality is forecast to advance at a 9.33% CAGR through 2031.

- By geography, China held 36.12% share in 2025, while India is projected to register the fastest growth at a 9.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Smart Key Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Smart Home Penetration in Urban Asia-Pacific Households | +2.1% | China, South Korea, Japan, Singapore | Short term (≤ 2 years) |

| Hospitality Shift Toward Contactless Guest Access and Mobile Keys | +1.6% | Japan, Australia, Thailand, Singapore, India, Vietnam | Short term (≤ 2 years) |

| Continued OEM Adoption of Connected Vehicle Digital Keys | +1.4% | China, South Korea, India, Southeast Asia | Medium term (2-4 years) |

| Enterprise Retrofit Demand for Cloud-Based Access Control | +1.2% | China tier-1 cities, Singapore, Japan, South Korea | Medium term (2-4 years) |

| Expansion of Co-Living, Short-Stay Rentals, and Unmanned Space Formats | +0.9% | Singapore, China, Japan, India, Southeast Asia | Short term (≤ 2 years) |

| Insurance and Compliance Push for Audit-Ready Access Logs | +0.4% | Regional, with stronger relevance in Singapore, Australia, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Smart Home Penetration In Urban Asia-Pacific Households

Rising smart home adoption in dense urban areas is expanding the addressable market for residential access systems across the region. The strongest demand is emerging where developers, landlords, and managed rental operators can bundle access into the broader digital home offer rather than sell it as a standalone device purchase. This speeds up replacement cycles in premium apartments and professionally managed properties, while new construction enables more direct installation during construction. It also raises the value of brands that can tie locks, credentials, user permissions, and resident support into a single service layer, rather than competing solely on hardware price. In the Asia-Pacific smart key market, residential demand is increasingly shaped by institutional buyers such as developers and property managers, shortening rollout timelines and shifting pricing power toward platform-led vendors. That change also favors suppliers that can support recurring credential management, remote provisioning, visitor access, and lifecycle service over the full occupancy period.

Hospitality Shift Toward Contactless Guest Access And Mobile Keys

Hospitality operators across the region are moving toward contactless access because it reduces reliance on the front desk and removes friction at guest arrival. Mitsui Fudosan introduced Room Key in Apple Wallet across its Mitsui Garden Hotels and sequence hotel brands in March 2026 using Vingcard's Vostio cloud-based access management system and MIFARE 2GO credentials. This kind of rollout shows that hotels are no longer evaluating locks in isolation, because the real decision now includes credential delivery, cloud orchestration, and property system compatibility. Wallet-based entry also matters because it lowers the user barrier that comes with proprietary app downloads and account setup, which can slow guest participation. In the Asia-Pacific smart key market, hotel adoption has become a visible proof point for mobile credentials and is helping normalize phone-based access across other settings such as serviced apartments and enterprise spaces. Vendors that can link door hardware, credential issuance, and hotel workflow software are therefore better placed to capture the next phase of hospitality spending.

Continued OEM Adoption of Connected Vehicle Digital Keys

Automotive digital keys are advancing because OEMs now have a clearer standards path and broader ecosystem support than they did a year earlier. The Car Connectivity Consortium reported that 115 vehicle and module products achieved CCC Digital Key certification in 2025, up from 2 in 2024.[1]Car Connectivity Consortium, “CCC Digital Key Certifications Surged in 2025, Reinforcing the Global Standard for Secure Vehicle Access,” Car Connectivity Consortium, carconnectivity.org That certification wave included first-time approvals for APAC OEMs such as NIO, XPENG, six Geely holding group brands, Hyundai, Genesis, and Mahindra. The 2025 expansion of the framework beyond NFC to BLE and UWB is important because it supports hands-free entry and wider multi-device use models. As consumers become more comfortable using phones and wallets as secure vehicle credentials, the learning curve for residential and hospitality access also becomes lower. This makes automotive adoption a direct product driver and an indirect familiarity driver for the Asia-Pacific smart key market.

Enterprise Retrofit Demand For Cloud-Based Access Control

Enterprise retrofit demand is rising because many building operators want centralized control, audit trails, and mobile credentials without replacing every legacy reader and controller in the field. A 30-story technology park in Shenzhen completed a 7-day smart access retrofit in April 2026 using a SaaS cloud-plus-edge-gateway architecture and reported a 70% reduction in O&M costs, a 98% improvement in card issuance efficiency, and a 50% reduction in security staffing without replacing existing readers or controllers. This kind of project matters because it shifts the retrofit discussion away from full hardware replacement and toward platform migration, which is far easier to justify operationally. Cloud access platforms such as Suprema's BioStar Air are built around centralized management and mobile credential support, which are well-suited to multi-site and hybrid enterprise deployments. Buyers in finance, technology, data center, and commercial office environments are also paying closer attention to security architecture, software control, and identity integration as part of the same procurement cycle. In the Asia-Pacific smart key market, enterprise growth is therefore being led less by standalone devices and more by the practical value of retrofit-friendly software layers that improve control without creating major site disruption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Retrofit and Integration Costs | -1.9% | Southeast Asia tier-2 cities, India tier-2 and tier-3, Indonesia, Philippines | Medium term (2-4 years) |

| Cybersecurity and Credential Spoofing Risks | -1.4% | Regional, with stronger relevance in China, India, Southeast Asia | Short term (≤ 2 years) |

| Fragmented Interoperability Across Property, Wallet, and Vehicle Ecosystems | -1.0% | APAC-wide, especially markets with mixed legacy hardware | Long term (≥ 4 years) |

| Installer and After-Sales Capability Gaps Outside Tier-1 Cities | -0.6% | India, Indonesia, Vietnam, Philippines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Retrofit And Integration Costs

High retrofit and integration costs continue to limit broader deployment, especially in older buildings and smaller property portfolios that lack a clear budget for connected access. The challenge is usually broader than the lock itself, because deployment may also require upgrades to doors, power, networking, credential-issuance workflows, and local service capabilities. This is a larger problem in tier-2 and tier-3 cities, where building stock is more varied, and installers may need to make more site-level modifications before a rollout can begin. Recurring software fees also matter, because portfolio operators have to evaluate not only the first installation cost but also the monthly expense of managing many doors across several sites. As a result, adoption tends to concentrate first in new construction, premium hospitality, enterprise campuses, and developer-led projects that can absorb the full software and service stack. In the Asia-Pacific smart key market, this cost profile narrows the practical retrofit base, even as user interest and technology readiness both improve.

Cybersecurity And Credential Spoofing Risks

Cybersecurity remains a meaningful restraint because buyers are increasingly aware that access credentials create both convenience and attack exposure. Researchers at UC San Diego disclosed 5 exploitable vulnerabilities in a commercial BLE smart lock at the USENIX WOOT 2025 conference, including replay attacks, persistent access profiles after revocation, and tampered audit logs.[2]Chengsong Diao, Danielle Dang, Sierra Lira, Angela Tsai, Miro Haller, and Nadia Heninger, “No Key, No Problem, Vulnerabilities in Master Lock Smart Locks,” USENIX WOOT 2025, usenix.org These findings show that security outcomes depend heavily on implementation quality, update discipline, and credential lifecycle design rather than on the protocol label alone. Enterprise and institutional buyers are therefore increasingly requesting third-party testing, stronger update controls, and greater auditability before approving large deployments. This lengthens procurement timelines in sectors such as commercial real estate, hospitality, and public infrastructure, where access failure can create both reputational and operational costs. The Asia-Pacific smart key market still benefits from the compliance moat this creates for audited vendors, but it also faces slower decision cycles whenever buyers need to validate software, hardware, and credential security together.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automotive Leadership Still Matters, But Software-Centric Credentials Are Gaining Ground

Smart Car Keys held 48.33% of the Asia-Pacific smart key market share in 2025, which made automotive the largest product segment by a clear margin. That lead reflects the long history of OEM investment in remote entry, immobilizer-linked systems, and increasingly phone-based digital access tools. By the end of 2025, CCC certification covered products from 16 automakers, and APAC brands were firmly represented in that base. This scale gave the automotive segment the deepest installed footprint and kept it central to supplier volume, standards participation, and ecosystem visibility. At the same time, automotive growth remains tied to vehicle launch cycles, supplier validation windows, and production schedules, so its maturity imposes natural limits on how quickly it can outpace other credential categories.

Mobile-Based and Virtual Keys are forecast to grow at a 9.03% CAGR through 2031, pointing to a stronger software- and wallet-led growth path within the broader category. Allegion stated in 2026 that Aliro 1.0 creates a standardized model for mobile credentials and reader communication across Apple, Google, and Samsung wallet environments. Smart Door Keys and lock-linked credentials remain important because residential and commercial buildings provide the widest non-automotive installed base, while Smart Key Fobs, Cards, and Wearables still fit institutional workflows where shared or temporary access is common. In the Asia-Pacific smart key market, this mix suggests that hardware volume will remain broad, but the commercial center of gravity is moving toward software control, credential portability, and recurring service value. The Asia-Pacific smart key industry is therefore being reshaped less by the presence of a new lock format and more by who controls the credential layer that sits above the device.

By Technology: RFID Keeps Its Installed Base, While BLE Gains From Experience-Led Upgrades

RFID accounted for 34.87% of the Asia-Pacific smart key market in 2025, reflecting its long-established role in hospitality locks, office access cards, and transit-linked credential environments. Its position remains strong because operators understand the workflow, staff know how to issue credentials, and many sites already have readers that are expensive to replace quickly. In practical terms, this gives RFID a durable role across mid-market hotels, corporate facilities, institutional sites, and mixed-use buildings where reliability matters more than feature novelty. The installed base is especially relevant in mature environments where card-centric access has become routine, and replacement cycles are long. That means a large part of the current technology transition is happening through hybrid stacks rather than through abrupt migration away from existing RFID-supported infrastructure.

Bluetooth Low Energy is forecast to grow at 9.43% CAGR through 2031 and is becoming the preferred layer for proximity-based and wallet-driven access experiences. The Car Connectivity Consortium expanded Digital Key certification to include BLE and UWB, which supports more seamless hands-free and cross-device use cases. NFC still plays a strong supporting role because tap-based access remains familiar and dependable, while Wi-Fi continues to matter for remote management, provisioning, and firmware updates rather than as the main credential channel. In the Asia-Pacific smart key market, technology competition is shifting from basic connectivity claims to a more practical test that centers on interoperability, reader compatibility, credential handoff, and the overall quality of the user journey. The Asia-Pacific smart key industry is therefore moving toward multi-protocol architectures in which the most successful vendors are likely to be those that simplify complexity for operators rather than those that promote a single wireless standard.

By Authentication Method: The Fob Still Leads, But Phone-Led Entry Is Lowering User Friction

Key fob-based access held 37.18% of the Asia-Pacific smart key market share in 2025, underscoring the size of the legacy installed base across enterprise campuses, commercial properties, and vehicles. Fobs continue to hold this position because they work offline, are easy to issue at scale, and fit the reader infrastructure already present in many buildings and fleets. Procurement teams often keep them longer than expected because migrating away from fobs may require reader updates, user retraining, and added integration work across access databases. This keeps fob-based systems commercially relevant even when operators already see the long-term logic of moving toward mobile credentials. It also favors vendors that can support both fobs and phone-based access during phased upgrades, rather than forcing a one-step migration.

Smartphone-based access is projected to expand at a 9.21% CAGR through 2031, as wallet integration eliminates the need for separate app downloads and makes credential use feel more immediate. In hospitality, wallet-based room access is moving from selective deployment to a branded rollout, as evidenced by Mitsui Fudosan's March 2026 implementation in Japan. Card key-based access, keypad access, and biometric methods still serve specific needs in guest turnover, temporary entry, and higher-security commercial environments, while cloud-native systems such as BioStar Air support biometric management across multiple sites. In the Asia-Pacific smart key market, the most durable authentication approach is increasingly one that lets operators support multiple credential types under a single policy layer rather than fully commit to a single method. That direction matters because access environments across the region are too varied for a one-size-fits-all model, which means flexible credential orchestration is becoming more valuable than any single device.

By End-User Industry: Enterprise Drives Current Scale, While Hospitality Drives The Fastest Shift In Use Model

Enterprise and Commercial Buildings accounted for 31.59% of the Asia-Pacific smart key market in 2025, making them the largest end-user segment. That leadership reflects the sheer number of doors, credentials, permission changes, and audit requirements handled each day across office towers, data centers, coworking facilities, campuses, and multi-tenant commercial sites. These environments place a premium on centralized administration, access history, visitor control, and policy consistency across large user groups. The Shenzhen technology park retrofit, completed in April 2026, demonstrates why operators prefer cloud migration, it enables them to retain existing readers and controllers while improving control and efficiency. Enterprise demand also tends to favor vendors that can combine devices, software, credential types, and ongoing support within a single managed platform.

Hospitality is projected to deliver the fastest growth at 9.33% CAGR through 2031, giving the Asia-Pacific smart key market size one of its clearest expansion paths by end user. Hotel groups are adopting mobile and wallet room keys to reduce front-desk dependence, speed up guest movement, and align room access with the broader digital stay experience, with Mitsui Fudosan offering a clear recent example in Japan. Residential demand is expanding through rental portfolios and developer-led projects, automotive remains critical through product scale, and industrial and public infrastructure are moving more selectively based on security needs and systems integration. In the Asia-Pacific smart key market, several adoption models are advancing simultaneously, keeping demand broad but also requiring vendors to tailor products and service models more carefully by site type. This is one reason the Asia-Pacific smart key market has a broader competitive landscape than many single-application access categories, even as software-led consolidation is gradually increasing.

Geography Analysis

China held a 36.12% share of the Asia-Pacific smart key market in 2025, driven by deep manufacturing, strong demand in residential and automotive applications, and a wide supplier base serving both domestic and export channels. It also leads vehicle credential standardization, with brands like NIO and XPENG achieving CCC Digital Key certification in 2025. This combination of supply scale and standards participation strengthens China's influence over product availability and credential ecosystems. India is projected to grow at a 9.29% CAGR through 2031, making it the fastest-growing market in the region.

Japan and South Korea remain the most technically mature markets, though their adoption drivers differ. In Japan, hospitality rollouts, such as Mitsui Fudosan's 2026 launch across its Mitsui Garden Hotels, are normalizing wallet-based room access, creating a consumer touchpoint for mobile credentials.[3]Mitsui Fudosan Co., Ltd., “Mitsui Garden Hotels/sequence Introduce Room Key in Apple Wallet for Guests,” Mitsui Fudosan Co., Ltd., mitsuifudosan.co.jp South Korea focuses on premium residential products, as seen with ASSA ABLOY's 2025 launch of the Yale GM900S, which features fire detection and emergency exit functionality to cater to high-spec security demand.

Southeast Asia, Australia, New Zealand, and Taiwan represent growth areas, supported by hotels, co-living spaces, and commercial properties seeking frictionless access tools. Singapore leads with its digital infrastructure agenda, accelerating the adoption of unified access control. Australia and New Zealand serve as test markets for new credential formats and deployment models, shaping vendor strategies on interoperability and user experience. These markets highlight a mix of mature high-spec countries and emerging demand centers driving the Asia-Pacific smart key market.

Competitive Landscape

The competitive landscape includes a small group of global access platform vendors and a broader field of regional specialists and domestic manufacturers. ASSA ABLOY, dormakaba, and Allegion dominate enterprise, hospitality, and commercial deployments, extending software and credential capabilities. ASSA ABLOY issued over 15 million mobile credentials globally in 2025, highlighting a shift toward software-linked access ecosystems.[4]ASSA ABLOY, “Annual Report 2025,” ASSA ABLOY, assaabloy.com Additionally, 27% of its Asia Pacific division sales in 2025 came from products launched within the previous three years, indicating active product renewal. In the Asia-Pacific smart key market, large incumbents leverage their installed base to expand software, services, and cross-vertical credentials.

Strategies now focus on standards alignment, multi-credential support, and reducing integration friction. Allegion’s 2026 launch of Aliro 1.0 created a shared framework for mobile credentials across Apple, Google, and Samsung wallet ecosystems, lowering switching costs for enterprise buyers. ZKTeco’s March 2026 launch of its Global Innovation Hub for Mechatronic Intelligent Control marked its shift from biometric hardware to AIoT ecosystem offerings for smart offices and communities. The Asia-Pacific smart key market rewards companies combining standards participation with strong regional channels, deployment support, and software-led account control.

Asia-Pacific native brands are gaining traction by addressing local installation norms, price sensitivity, and property management needs. igloohome reported its solutions were used across over 500,000 doors in 80+ countries in 2025, showing scalability beyond domestic markets. Dormakaba's Quantum Pixel+ hotel lock, which won the ICONIC AWARD 2025, and Allegion's Schlage Ascent launch in New Zealand highlight how vendors use design, certification, and targeted launches to strengthen their positioning. The Asia-Pacific smart key market remains fragmented at the platform and hardware levels, with differentiation driven by interoperability, ease of deployment, security assurance, and multi-market service capabilities.

Asia-Pacific Smart Key Industry Leaders

ASSA ABLOY AB

Allegion plc

Dormakaba Holding AG

SALTO Systems, S.L.

MIWA Lock Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: ZKTeco officially launched its Global Innovation Hub for Mechatronic Intelligent Control, signaling a strategic expansion beyond biometric hardware into integrated AIoT ecosystem solutions for smart offices and smart communities.

- March 2026: Mitsui Fudosan Co., Ltd. introduced "Room Key in Apple Wallet" across its Mitsui Garden Hotels and sequence hotel brands in Japan, using Vingcard's Vostio cloud-based access management system and MIFARE 2GO NFC credentials, marking one of Japan's first large-scale property group deployments of wallet-integrated hotel keys.

- February 2026: Allegion announced its support for the Aliro 1.0 specification, developed by the Connectivity Standards Alliance with Apple, Google, and Samsung as co-developers, establishing a unified mobile credential standard for smartphone- and wearable-based smart lock access, and Allegion committed its global electronic lock and reader portfolio to Aliro certification.

- January 2026: The Car Connectivity Consortium announced that 115 vehicle and module products achieved CCC Digital Key certification in 2025, including first APAC certifications from NIO, XPENG, Geely brands, Hyundai, Genesis, and Mahindra, representing an acceleration from 2 certifications in 2024 and cementing the NFC-BLE-UWB stack as the global OEM digital key standard.

Asia-Pacific Smart Key Market Report Scope

The Asia-Pacific Smart Key Market encompasses the development, production, distribution, and deployment of smart key systems that enable secure, keyless access and authentication across automotive, residential, commercial, hospitality, and industrial applications in the Asia-Pacific region. These systems leverage advanced technologies such as RFID, Bluetooth Low Energy (BLE), NFC, Wi-Fi, and biometric authentication to provide enhanced convenience, security, and connectivity compared to traditional mechanical key systems.

The Asia-Pacific Smart Key Market Report is Segmented by Product Type (Smart Car Keys, Smart Door Keys and Lock-Linked Credentials, Mobile-Based and Virtual Keys, and Smart Key Fobs, Cards, and Wearables), Technology (RFID, Bluetooth and BLE, NFC, Wi-Fi, and Biometric Authentication), Authentication Method (Smartphone-Based Access, Key Fob-Based Access, Card Key-Based Access, Keypad and PIN-Based Access, and Biometric-Based Access), End-User Industry (Automotive, Residential, Hospitality, Enterprise and Commercial Buildings, and Industrial and Public Infrastructure), and Geography (China, Japan, India, South Korea, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Smart Car Keys |

| Smart Door Keys and Lock-Linked Credentials |

| Mobile-Based and Virtual Keys |

| Smart Key Fobs, Cards, and Wearables |

By Technology

| RFID |

| Bluetooth and BLE |

| NFC |

| Wi-Fi |

| Biometric Authentication |

By Authentication Method

| Smartphone-Based Access |

| Key Fob-Based Access |

| Card Key-Based Access |

| Keypad and PIN-Based Access |

| Biometric-Based Access |

By End-User Industry

| Automotive |

| Residential |

| Hospitality |

| Enterprise and Commercial Buildings |

| Industrial and Public Infrastructure |

By Geography

| China |

| Japan |

| India |

| South Korea |

| Rest of Asia-Pacific |

| By Product Type | Smart Car Keys |

| Smart Door Keys and Lock-Linked Credentials | |

| Mobile-Based and Virtual Keys | |

| Smart Key Fobs, Cards, and Wearables | |

| By Technology | RFID |

| Bluetooth and BLE | |

| NFC | |

| Wi-Fi | |

| Biometric Authentication | |

| By Authentication Method | Smartphone-Based Access |

| Key Fob-Based Access | |

| Card Key-Based Access | |

| Keypad and PIN-Based Access | |

| Biometric-Based Access | |

| By End-User Industry | Automotive |

| Residential | |

| Hospitality | |

| Enterprise and Commercial Buildings | |

| Industrial and Public Infrastructure | |

| By Geography | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the size outlook for the Asia-Pacific smart key market?

The Asia-Pacific smart key market was valued at USD 4.46 billion in 2025, is estimated at USD 4.79 billion in 2026, and is forecast to reach USD 7.18 billion by 2031 at an 8.43% CAGR.

Which product category leads demand across Asia-Pacific smart key deployments?

Smart Car Keys led by product type with a 48.33% share in 2025, reflecting the scale of automotive access systems and the growing role of digital vehicle credentials.

Which technology is growing fastest in smart key adoption across Asia-Pacific?

Bluetooth Low Energy is projected to grow fastest at a 9.43% CAGR through 2031 because it supports proximity-based and wallet-enabled access experiences.

Why are hotels adopting mobile and wallet-based room access in Asia-Pacific?

Hotels are using mobile and wallet credentials to reduce front-desk friction, simplify guest arrival, and connect room entry with broader digital stay management.

Which end-user group is expanding fastest in the region?

Hospitality is expected to record the highest CAGR at 9.33% through 2031, while Enterprise and Commercial Buildings remained the largest end-user segment with a 31.59% share in 2025.

Which countries are most important in the regional outlook?

China held the largest country share at 36.12% in 2025, while India is projected to grow fastest at a 9.29% CAGR through 2031, with Japan and South Korea remaining important high-spec markets.

Page last updated on: