Market Overview

| Study Period | 2020 - 2031 |

|---|---|

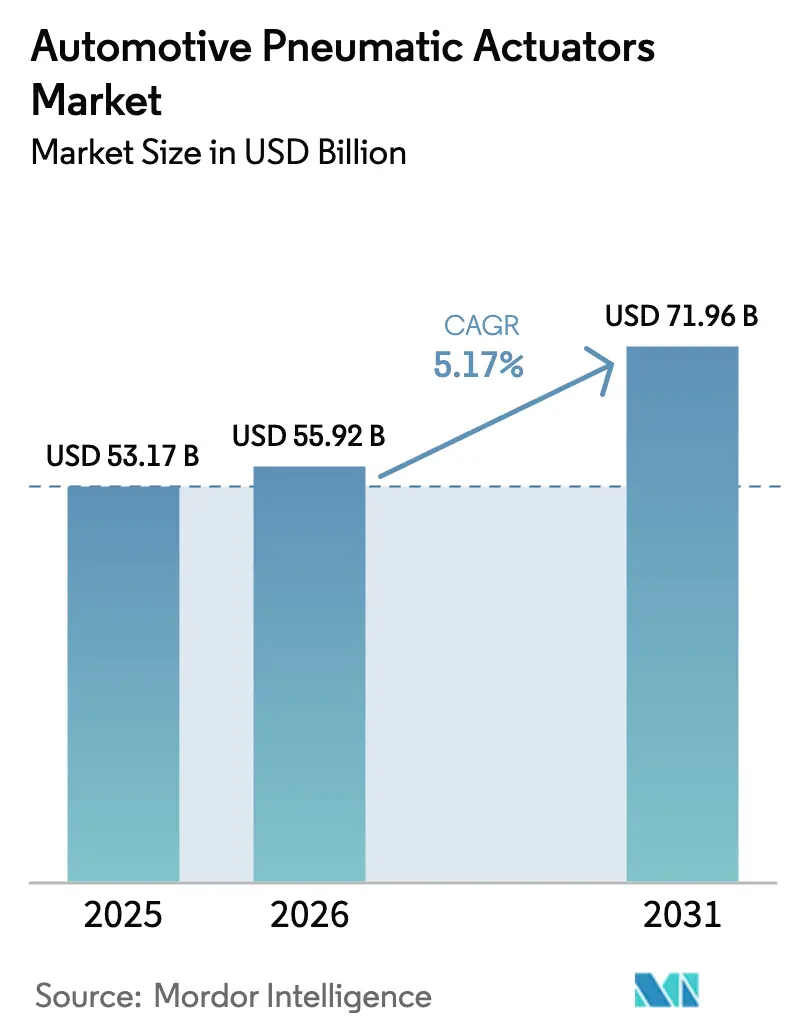

| Market Size (2026) | USD 55.92 Billion |

| Market Size (2031) | USD 71.96 Billion |

| Growth Rate (2026 - 2031) | 5.17% CAGR |

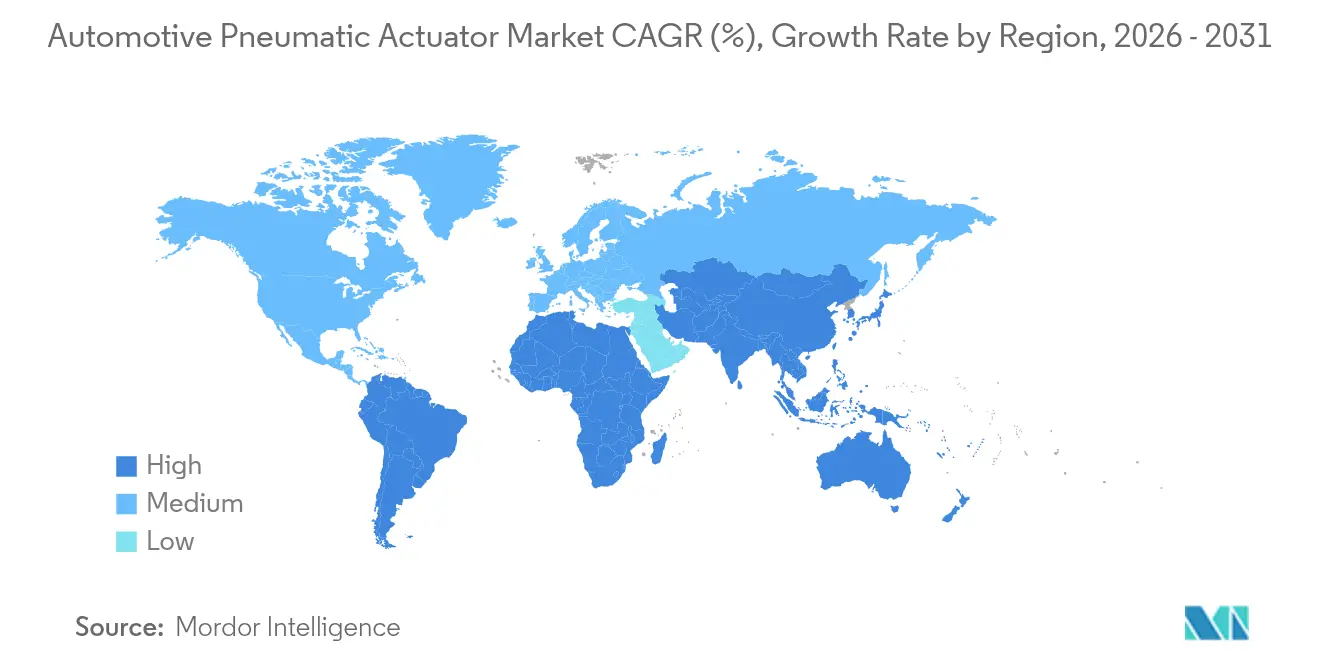

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

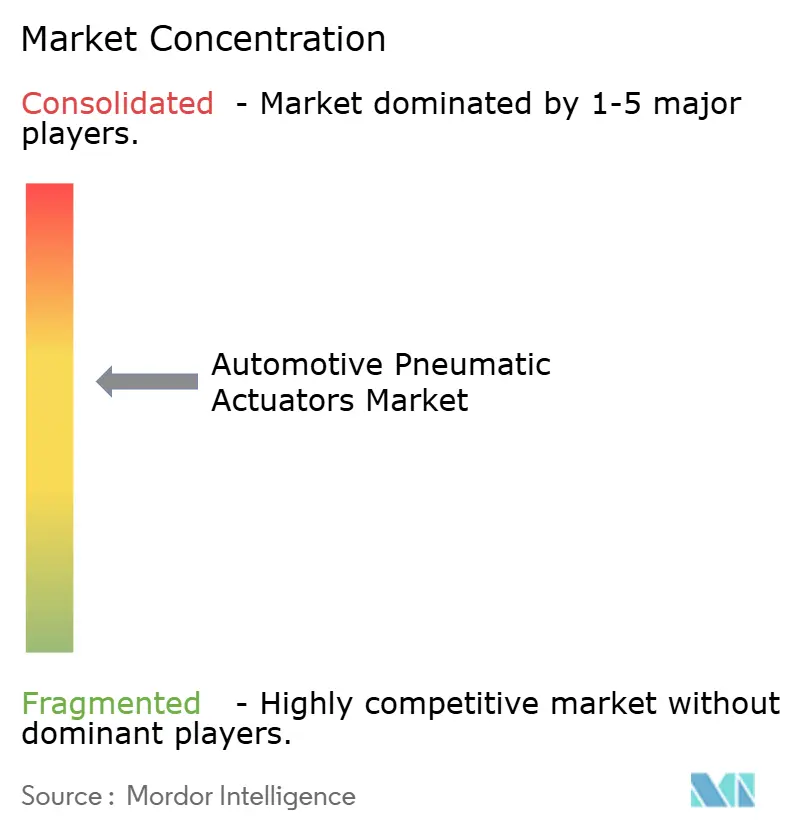

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Pneumatic Actuators Market Analysis by Mordor Intelligence

The Automotive Pneumatic Actuators Market size was valued at USD 53.17 billion in 2025 and estimated to grow from USD 55.92 billion in 2026 to reach USD 71.96 billion by 2031, at a CAGR of 5.17% during the forecast period (2026-2031). Despite competition from energy-efficient electric actuators, vehicle makers continue to rely on pneumatic devices for safety, powertrain, and chassis functions. Stricter emission regulations and the growing adoption of ADAS drive demand, with Asia-Pacific leading due to strong supply chains. At the same time, the Middle East and Africa, as well as South America, see rapid growth from expanding local assembly programs.

Key Report Takeaways

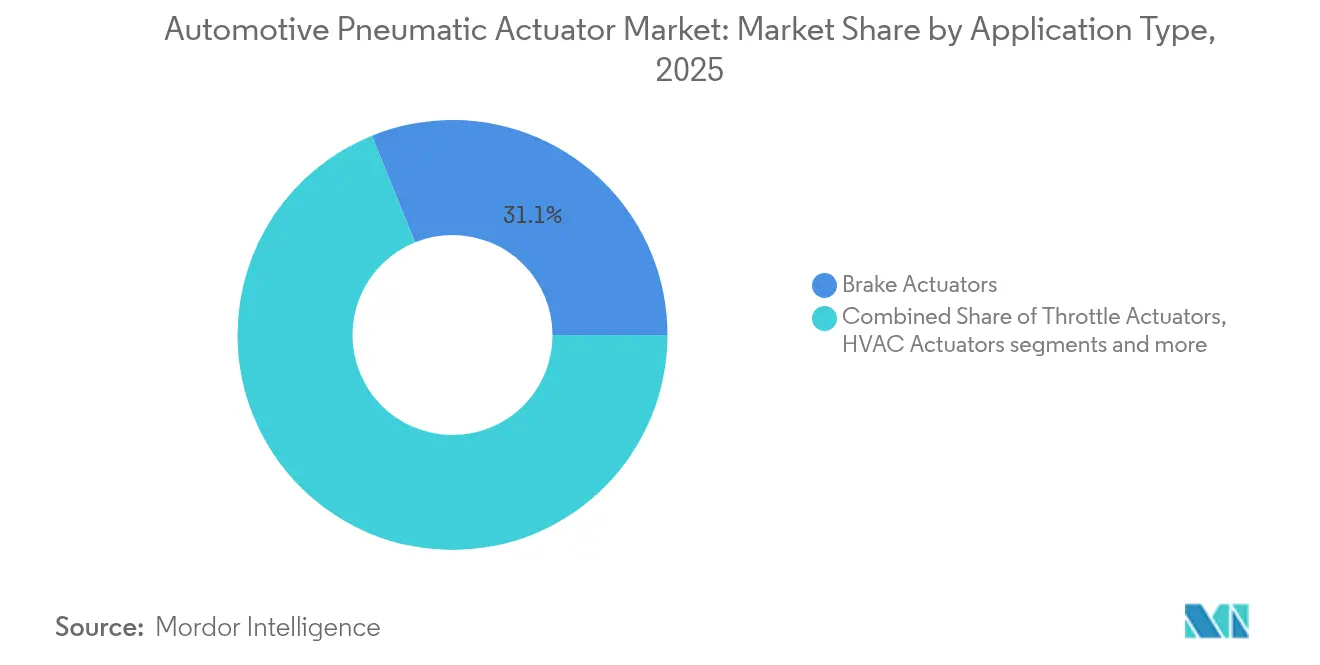

- By application type, brake actuators led with 31.12% automotive pneumatic actuators market share in 2025, while turbocharger wastegate actuators are projected to grow at a 6.43% CAGR through 2031.

- By vehicle type, passenger cars accounted for 56.05% of the automotive pneumatic actuators market size in 2025, yet heavy commercial vehicles are expected to register the fastest 5.63% CAGR to 2031.

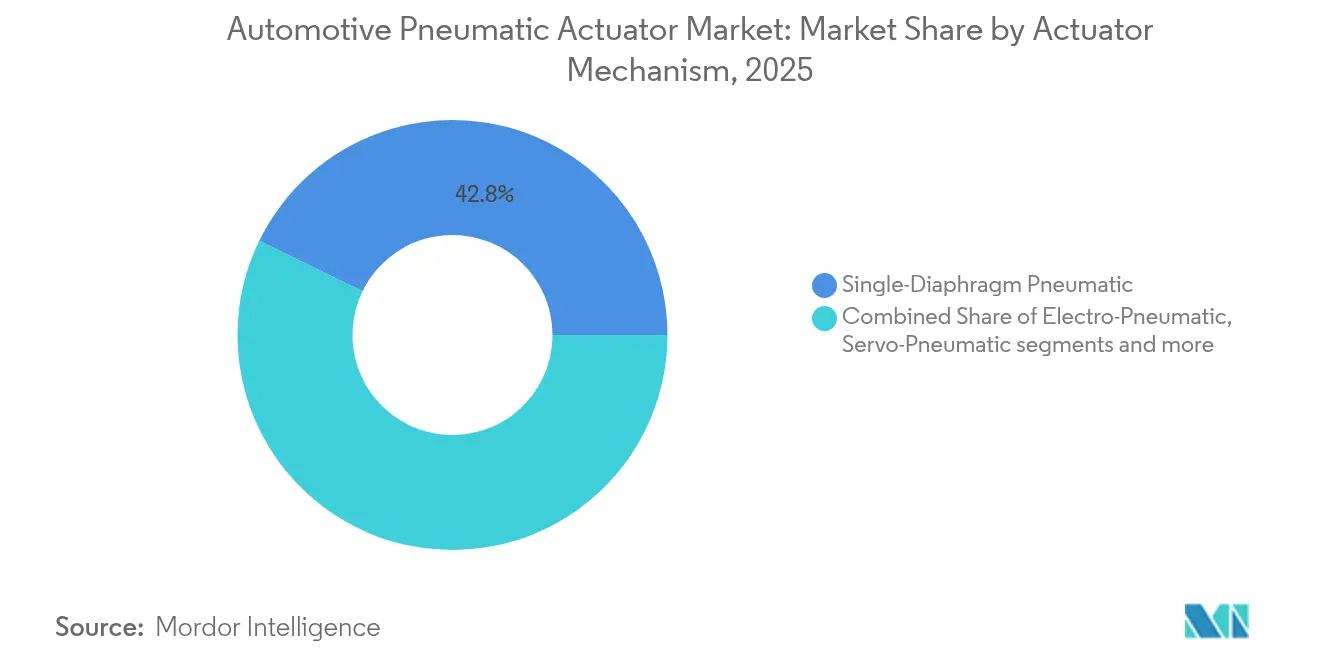

- By actuator mechanism, single-diaphragm designs held 42.78% of the automotive pneumatic actuators market share in 2025, whereas electro-pneumatic hybrids are forecast to post a 6.08% CAGR through 2031.

- By Sales Channel, OEM programs dominated distribution with 72.45% revenue share of the automotive pneumatic actuators market in 2025, whereas the aftermarket is projected to grow at a 5.05% CAGR through 2031

- By region, Asia Pacific captured 45.08% revenue share of the automotive pneumatic actuators market in 2025, while Middle East and Africa is advancing at an 7.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Pneumatic Actuators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter emission norms driving precise air-fuel control | +1.5% | Global, EU and North America leading | Short term (≤ 2 years) |

| Increasing global vehicle production | +1.2% | Global, with Asia-Pacific core concentration | Medium term (2-4 years) |

| ADAS proliferation demanding accurate actuation | +1.1% | Global, with premium segment focus | Medium term (2-4 years) |

| Lightweighting trend for fuel economy | +0.8% | North America and EU, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Hydrogen ICE valve-timing adoption | +0.3% | Japan, Germany, select Asia-Pacific markets | Long term (≥ 4 years) |

| OTA-enabled actuator software monetisation | +0.2% | North America and EU premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter emission norms driving precise air-fuel control

The US EPA’s Phase 3 heavy-duty standards enacted in 2024 tighten NOx thresholds, compelling diesel makers to refine EGR and dosing strategies that rely on high-resolution pneumatic valves.[1]United States Environmental Protection Agency, “Control of Air Pollution from New Motor Vehicles: Heavy-Duty Engine and Vehicle Standards,” epa.gov Similar Euro 7 drafts trigger demand peaks in Europe. Field-valid testing replaces laboratory cycles, forcing actuators to sustain precision under real-world vibration and temperature excursions. Suppliers with electro-pneumatic packages that close the digital feedback loop enjoy distinct bidding advantages. The regulatory timetable accelerates award decisions, locking in revenue visibility for the forecast period.

Increasing global vehicle production

Rising light-duty and heavy-duty volumes lift baseline demand across all pneumatic applications because every unit assembled carries multiple actuator points. The Japan Automobile Manufacturers Association confirmed that OEM schedules for 2025 still embed pneumatic solutions in brake, throttle, and EGR circuits to assure fuel efficiency and compliance.[2]Japan Automobile Manufacturers Association, “Motor Vehicle Statistics 2024,” jama.or.jp Platform sharing further magnifies volumes because a single actuator family can now be fitted across sibling models, raising economies of scale for suppliers. Western manufacturers are repositioning final-assembly footprints toward Southeast Asia, which encourages actuator makers to co-locate module lines. The production rebound therefore secures near-term growth in the automotive pneumatic actuators market even as electric rivals sharpen their cost proposition.

ADAS proliferation demanding accurate actuation

Higher-level driver-assistance features, from automated emergency braking to traffic-jam assist, need actuators capable of millisecond response to electronic control-unit commands. Hybrid electro-pneumatic devices handle the power density of air pressure while executing digital set-points from the vehicle network. Standard Motor Products broadened its electronic parking brake lineup in 2025 to support newest collision-avoidance algorithms.[3]“Standard Adds Electronic Parking Brake Actuators,” Standard Motor Products, smpcorp.com This integration imperative keeps the automotive pneumatic actuators market aligned with overarching software-defined-vehicle themes rather than sidelined by pure electrics.

Lightweighting trend for fuel economy

OEM fuel-efficiency roadmaps push actuator engineers toward composite housings and thin-wall metal stampings. Independent research on automotive composites confirms that substituting steel casings with carbon-fiber reinforced plastics can cut actuator weight by 35% without sacrificing strength. Lighter HVAC blend door modules and seat-adjust mechanisms directly translate into measurable consumption gains in homologation tests. The initiative also encourages function integration—merging two or more pneumatic roles into a single housing—which trims harness length and simplifies line installation, making cost-out and weight-out objectives mutually reinforcing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward energy-efficient electric actuators | -1.8% | Global, led by premium segments | Medium term (2-4 years) |

| Complexity & high maintenance cost of pneumatics | -0.9% | Global, particularly aftermarket | Short term (≤ 2 years) |

| Shortage of high-grade elastomers for seals | -0.6% | Global supply chain impact | Short term (≤ 2 years) |

| Tier-1 decarbonisation curbing pneumatic R&D | -0.4% | EU and North America focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift toward energy-efficient electric actuators

Electromechanical systems convert battery power into motion with up to 80% efficiency, dwarfing the 20% ceiling of air-driven counterparts. The delta becomes more pronounced in electric cars, where every watt saved extends range. Line-builders are also migrating their welding robots and material-handling arms to electric cylinders for tighter path accuracy. Yet pneumatics still dominates the highest-force nodes, such as heavy truck drum brakes, where compressed air is already integral to the vehicle platform. Consequently suppliers are channeling R&D toward mixed-technology actuators that preserve pressure-based force while embedding low-energy position control.

Complexity & high maintenance cost of pneumatics

Compressed-air architectures need dryers, reservoirs, and leak-proof couplings, all of which add to bill-of-material and service labor. Fleet operators report seal replacement intervals of 18–24 months on brake chambers, compared with 60-plus months for sealed electric alternatives. Reduced downtime expectations under predictive-maintenance programs place pneumatics at a cost disadvantage. The aftermarket channel takes the biggest margin impact because independent garages must carry a broader parts inventory and specialized leak-test equipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Type: Brake systems drive market leadership

Brake chambers and parking brake caliper units commanded 31.12% share of the automotive pneumatic actuators market in 2025. Their presence is mandated across every passenger and commercial vehicle variant, cementing baseline volume. Electromechanical parking brakes are penetrating luxury sedans, but heavy truck drum brakes still rely on air chambers that deliver high clamping force at low unit cost. Turbocharger wastegate actuators follow as the fastest riser, posting a 6.43% CAGR because downsized gasoline engines depend on accurate boost management to meet power and emission targets. Throttle valves, HVAC blend doors, and EGR butterflies retain mid-single-digit growth, each backed by regulatory or comfort imperatives.

Pneumatic fuel-injection rail regulators survive in certain flex-fuel layouts popular in Brazil, while door-lock plungers remain common in cost-sensitive hatchbacks. Across the board, suppliers experiment with smart pressure sensors embedded in actuator bodies to supply health data back to the vehicle control network. The enhancements prolong relevance of pneumatically powered devices even as direct electric motor drives tighten competitive gaps. Overall, the application mix underscores why the automotive pneumatic actuators market maintains double-digit billion-dollar revenues: it spans mandatory safety, emissions, and comfort functions that every vehicle must carry.

By Vehicle Type: Commercial segments accelerate growth

Passenger cars generated 56.05% of 2025 revenue, reflecting sheer production volume across global plants. Yet heavy commercial vehicles are projected to pace the automotive pneumatic actuators market size expansion with a 5.63% CAGR. Fleet operators prize the durability of air-brake and air-suspension circuits under intense duty cycles, while stricter CO₂ quotas push for optimized compressor management rather than wholesale technology swaps. Light commercial vans track e-commerce parcel demand and achieve a robust CAGR on the back of city-logistics growth. Construction and mining equipment are, chiefly for high-temperature exhaust-flap controllers and robust steering stabilizers.

Two-wheelers remain a micro-segment concentrated in select Asian economies, yet scooter OEMs are trialing low-pressure air servos for automatic clutch actuation. The diversity highlights a bifurcation: suburban passenger cars gravitate toward compact electric drives for NVH advantages, whereas high-payload vehicles sustain pneumatics for force density and proven maintainability. That divergence shapes future platform strategies of tier-1 suppliers, compelling them to produce modular families that scale from micro to heavy-duty ratings without rewriting qualification protocols.

By Actuator Mechanism: Electro-pneumatic hybrids lead innovation

Single-diaphragm designs still anchored 42.78% of 2025 volume because they deliver reliable linear throw at minimal parts count. Nevertheless, electro-pneumatic hybrids top the growth tables at 6.08% CAGR. In these units a small brushless motor operates a piloting valve, trimming pressure proportionally to digital commands while the diaphragm multiplies force on the output rod. The architecture reconciles the long-travel force of pneumatics with the closed-loop precision of electronics. Vacuum-boost varieties persist in gasoline platforms, though the shift to turbocharged or battery-electric powertrains shrinks the availability of manifold vacuum, driving incremental adoption of electrically driven compressors.

Servo-pneumatic and rack-and-pinion formats handle off-highway steering and loader-bucket articulation, environments that mandate explosion-safe operation around volatile dust clouds. Rotary-vane types occupy niche cabin-comfort tasks such as vent-door swing in premium HVAC modules. The richness of mechanisms means no single technology can claim ubiquity, and that diversity insulates the automotive pneumatic actuators market from sudden obsolescence, at least in mixed powertrain fleets projected for the next decade.

By Sales Channel: OEM integration complexity sustains dominance

Original-equipment contracts controlled 72.45% of global turnover in 2025 because braking and emission parts must clear stringent homologation tests before line-side delivery. Automakers favor long-term supply agreements tied to platform life cycles extending seven years or more, preserving predictable call-off schedules for vendors. The aftermarket grows at 5.05% CAGR, supported by global vehicle fleet age exceeding 11 years, yet faces structural drag where electric swap-out kits promise maintenance-free miles. Independent distributors invest in training to service air-systems diagnostics, but compressed-air leak repairs remain labor-intensive.

OEM pull is unlikely to dissipate given the functional safety classification of most pneumatic modules. Even when electric replacements surface, carmakers frequently dual-source to hedge technical risk, which prolongs lifecycle demand for incumbent air units. Suppliers therefore reinforce Tier-0.5 engineering programs—co-designing winter-test campaigns and cyber-security audits—to retain bench spots on future model launch bills.

Geography Analysis

Asia-Pacific generated 45.08% of global revenue in 2025, underpinned by China’s multi-brand passenger car output and Japan’s high-precision valve competence. The region is forecast to post a 6.84% CAGR as supply bases in Vietnam, Thailand, and India climb the value curve, making in-region sourcing attractive for global nameplates. Electro-pneumatic R&D centers in South Korea exploit the country’s advanced semiconductor ecosystem to integrate pressure MEMS sensors onto actuator PCBs, heightening competitive edge. Notwithstanding electric-vehicle penetration, cost-optimized sub-compact segments still install pneumatically driven HVAC and turbo wastegate units, securing volume for suppliers.

Middle East & Africa stands out as the fastest-growing cluster at a robust CAGR of 7.42%. Saudi Vision 2030 industrial policy lures CKD assembly lines, each demanding localized actuator content for commercial trucks that service construction booms. The UAE leverages free-zone logistics to re-export spare parts kits deeper into African markets. Turkey’s customs-union access to Europe boosts its component exports, compelling pneumatic suppliers to expand Izmir and Bursa facilities. These dynamics re-orient procurement away from trans-continental shipping toward near-market production, shortening lead times and cutting freight emissions.

In South America, flex-fuel engine architectures unique to the region stimulate EGR and fuel-rail actuator demand because ethanol blends alter combustion stoichiometry daily. Local content rules push multinational suppliers to site elastomer curing presses in Minas Gerais rather than import seal stacks. Argentine heavy-truck assembly rebounds after currency stabilization measures, adding lift for high-capacity brake chambers. Currency volatility and political risk temper the outlook, yet installed base inertia keeps the automotive pneumatic actuators market resilient in the hemisphere.

Competitive Landscape

The supplier arena shows moderate concentration. Continental, Bosch, and Denso leverage decades-deep brake and powertrain portfolios, plus tight integration at OEM program-management levels. Their established validation labs and geographic footprint allow quick pivoting when automakers add regional sourcing clauses. Continental’s 2024 re-organization placed actuator and motion-control activities into a dedicated division designed to accelerate decision making under volatile demand. Bosch anchors its competitive moat around high-volume machining and in-house elastomer compounding that cushions seal-shortage shocks.

Consolidation continues as suppliers chase scale and cross-portfolio synergies. The Schaeffler-Vitesco tie-up finalized in October 2024 created a EUR 600 million synergy roadmap by combining drivetrain electronics with mechanical actuation depth. Mid-tier companies focus on niche strengths: HEINZMANN specializes in heat-resistant EGR valves operating at 750 °C for diesel commercial engines, while small German and Japanese houses craft miniature servo-pneumatics for motorcycle ABS. New entrants from the industrial automation field attempt to transplant electric-cylinder know-how into vehicles, sparking technology cross-pollination.

Material innovation forms the next battleground. Suppliers investing in fluorine-rich elastomer chemistries secure superior ozone and biofuel resistance, a differentiator as E-fuel blends proliferate. Lightweight metal-matrix components that pair aluminum skins with polymer cores cut unit mass by double digits, aligning with OEM fuel-economy rules. Market share therefore hinges on how quickly incumbents can integrate electronics, software, and advanced materials into legacy air-powered architectures. Those unable to evolve risk ceding programs to agile electrification specialists over the five-year horizon.

Automotive Pneumatic Actuators Industry Leaders

Denso Corporation

Robert Bosch GmbH

Continental AG

Emerson

Hitachi Astemo Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Standard Motor Products expanded its Electronic Parking Brake Actuator program, adding coverage for late-model Ford, Jeep, Ram, Mercedes-Benz, and Subaru vehicles.

- October 2024: Schaeffler AG finalized the merger with Vitesco Technologies, targeting EUR 600 million annual synergies by 2029.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every factory-built device that converts compressed air into linear or rotary motion for on-vehicle duties such as braking, turbocharger waste-gate control, throttle actuation, HVAC flaps, and door locks. Revenues cover original-equipment supply plus first-fit replacements across passenger cars, commercial vehicles, two-wheelers, and off-highway equipment, expressed in constant 2024 US dollars.

Scope Exclusions: electric-only or hydraulic actuators, repair kits, and standalone valves are left out.

Segmentation Overview

- By Application Type

- Throttle Actuators

- Fuel Injection Actuators

- Brake Actuators

- Exhaust Gas Recirculation Actuators

- Turbocharger Wastegate Actuators

- HVAC Actuators

- Door Lock Actuators

- Others

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- Off-Highway Vehicles

- Two-Wheelers

- By Actuator Mechanism

- Single-Diaphragm Pneumatic

- Vacuum-Boost Pneumatic

- Electro-pneumatic (EP)

- Servo-pneumatic

- Rack-and-Pinion

- Rotary-Vane

- By Sales Channel

- OEM

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- Egypt

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with component makers, Tier-1 integrators, fleet workshops, and regional distributors across Asia-Pacific, Europe, and the Americas, clarifying average selling prices, warranty cycles, and regulation impacts before merging insights with desk findings.

Desk Research

We mined open data from OICA vehicle output tables, UN Comtrade HS-841231 trade flows, International Energy Agency EV stock outlooks, regional brake associations, and corporate filings, then verified news on Dow Jones Factiva. These sources anchored production, trade, and price baselines, and many other reputable portals were also consulted for cross-checks and clarifications.

Market-Sizing & Forecasting

A top-down build multiplies annual vehicle production, parc size, and actuator fitment per application by blended ASPs. Supplier roll-ups and channel checks adjust totals whenever variance exceeds five percent. Core variables include turbocharger penetration, ABS and ESC mandates, EV share, and replacement intervals. These feed a multivariate regression that extends forecasts through 2030.

Data Validation & Update Cycle

Outputs pass variance dashboards, peer review, and senior sign-off. We refresh each report every twelve months, with interim updates triggered by major recalls, policy shifts, or macro shocks, so clients always receive the latest view.

Why Mordor's Automotive Pneumatic Actuators Baseline Rings True

Published estimates diverge because publishers slice the market by different product baskets, vehicle sets, pricing years, and refresh rules. By aligning scope tightly with compressed-air motion points and by blending OE plus replacement volumes, Mordor Intelligence delivers a balanced baseline.

Key gap drivers are usually the exclusion of aftermarket units, lumping pneumatic with other actuation types, or stale price curves. Our wider geography coverage and annual refresh reduce drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 53.17 B (2025) | Mordor Intelligence | |

| USD 27.90 B (2024) | Regional Consultancy A | Counts OE light-vehicle sales only and omits aftermarket volumes |

| USD 20.25 B (2023) | Global Consultancy B | Bundles pneumatic within mixed actuator pool and uses a three-year update cycle |

These contrasts show that our disciplined variable selection and frequent validation give decision-makers figures they can trace back to clear levers and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the automotive pneumatic actuators market?

The market stands at USD 55.92 billion in 2026 and is projected to reach USD 71.96 billion by 2031.

Which application segment leads the market?

Brake actuators command the largest slice with 31.12% market share in 2025, reflecting their mandatory safety role.

Why do heavy commercial vehicles post faster growth than passenger cars?

Fleet operators emphasize durability and high clamp force, driving a 5.63% CAGR for heavy trucks versus lower growth in car segments that increasingly adopt electric actuation.

How significant is Asia-Pacific in this landscape?

Asia-Pacific holds 45.08% of global revenue, supported by dense assembly capacity and integrated supply chains, and is forecast to grow at a 6.84% CAGR.

What technology trend defines future product design?

Electro-pneumatic hybrids form the main innovation path, pairing pneumatic power with electronic precision to meet ADAS and emission-control requirements.

Which factor poses the greatest restraint?

The shift toward high-efficiency electric actuators subtracts 1.8 percentage points from the forecast CAGR due to energy-savings imperatives across premium segments.

Page last updated on: