Automotive OEM Interior Coatings Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Growth Rate | 2.50% CAGR |

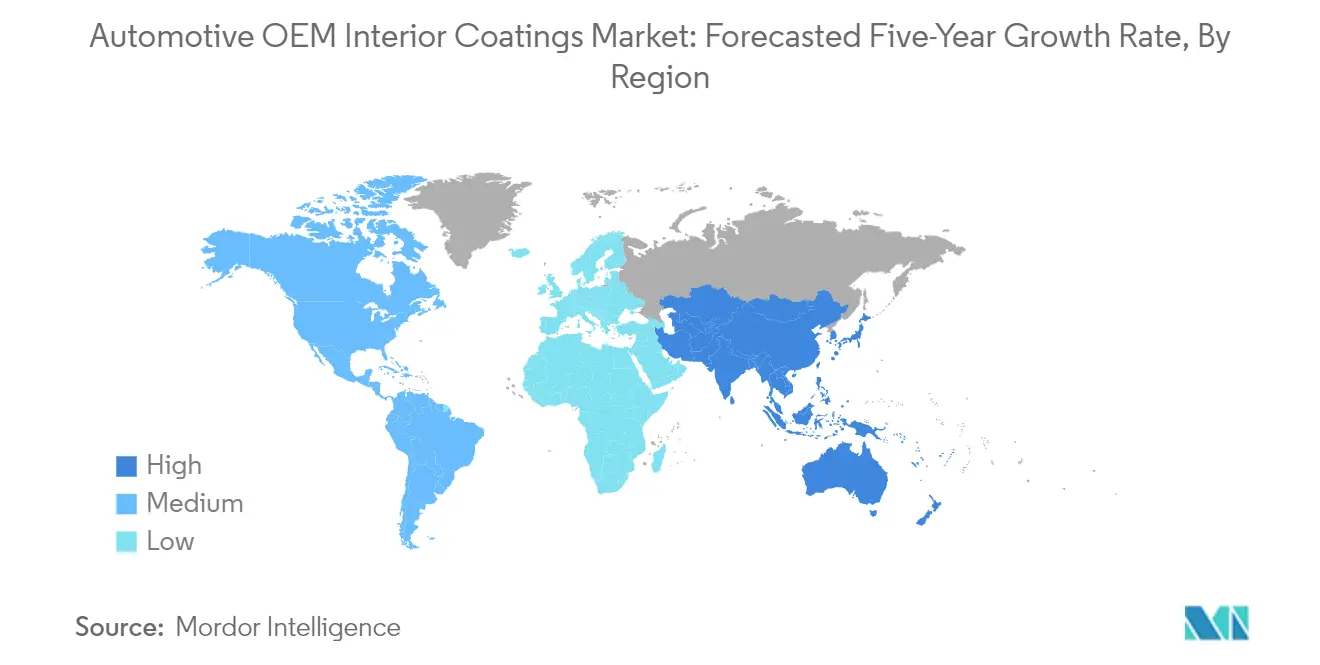

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive OEM Interior Coatings Market Analysis by Mordor Intelligence

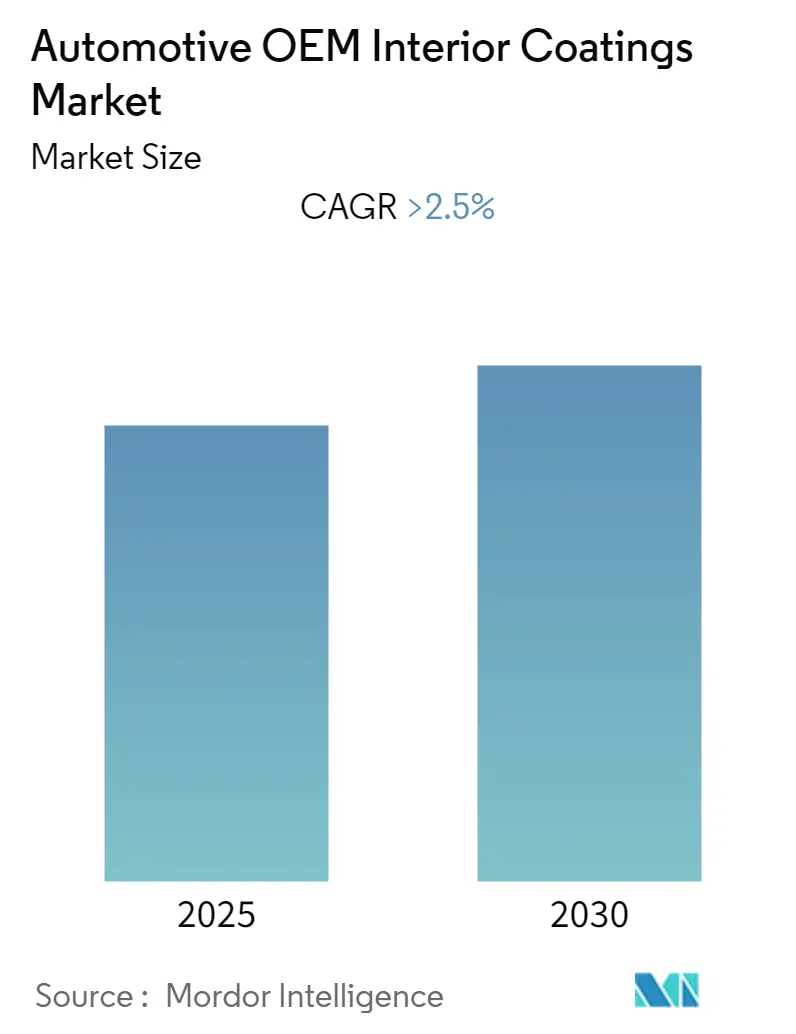

The Automotive OEM Interior Coatings Market is expected to register a CAGR of greater than 2.5% during the forecast period.

The global automotive industry is experiencing a significant transformation driven by shifting manufacturing patterns and regional investment flows. Major automotive manufacturers are strategically relocating their production facilities to emerging markets, particularly in Sub-Saharan Africa, where countries like Ghana, Ethiopia, Angola, and Nigeria are attracting substantial investments in manufacturing infrastructure. This redistribution of manufacturing capabilities is reshaping the automotive supply chain landscape and creating new opportunities for automotive OEM coatings suppliers in these regions.

The Middle East automotive sector is witnessing unprecedented growth and development, particularly in the Gulf region. Saudi Arabia's automotive market is projected to experience a robust 9% annual growth rate through 2025, driven by expanding consumer segments and government initiatives. The United Arab Emirates has emerged as a pioneer in sustainable mobility infrastructure, with Dubai already operating 200 charging stations and Abu Dhabi maintaining 20 stations, demonstrating the region's commitment to future mobility solutions.

The electric vehicle segment is experiencing remarkable expansion globally, with projections indicating that electric vehicles will constitute approximately 7% of the global vehicle fleet by 2030, representing around 140 million vehicles. This transition is particularly evident in markets like the UAE, which has set ambitious targets to deploy 42,000 electric vehicles on its roads in the coming years. The shift toward electric vehicles is driving innovations in automotive interior paint technologies, as manufacturers develop specialized solutions for EV-specific components and surfaces.

The automotive interior coatings industry is witnessing significant technological advancements, with manufacturers focusing on developing sustainable and high-performance coating solutions. The integration of bio-based materials and environmentally friendly coating technologies is gaining prominence, as evidenced by recent collaborations between coating manufacturers and automotive OEMs. For instance, the development of new coating solutions for engineering bioplastics demonstrates the industry's commitment to sustainability while maintaining high-quality surface finishes for interior applications. The automotive OEM coatings market is poised to benefit from these innovations as it adapts to evolving consumer preferences and regulatory standards.

Global Automotive OEM Interior Coatings Market Trends and Insights

MOBILITY PREFERENCE FOR PERSONAL TRANSPORT

The consumer preference for personal transport has witnessed significant growth in recent years, driven by multiple factors including better development of roads and infrastructure, innovations in the car rental industry, and increased accessibility of affordable vehicles for middle-class consumers. The car rental industry has gained substantial momentum globally, supported by the proliferation of online platforms, ease of booking systems, and the rising penetration of smartphones. According to industry analysis, the car rental market is projected to grow at a CAGR of 7.5% through 2025, indicating a strong shift towards flexible personal mobility solutions. Additionally, the introduction of economical cars in the market, combined with the easy availability of car loans and growing per capita income in developing countries, has made personal vehicle ownership more accessible to a broader consumer base.

The transformation in consumer behavior has been further reinforced by startup innovations in the car rental industry and the increasing preference for personal mobility solutions. Online tourist vehicle bookings have seen a notable uptick, particularly among users aged between 25 and 34 years who show a strong inclination towards digital booking platforms for vehicle rentals. This demographic shift, coupled with technological advancements, has made short-term personal vehicle rental through online booking platforms the preferred choice for many consumers. The trend is particularly evident in developing markets where rising disposable incomes and improved financing options have created a more conducive environment for personal vehicle acquisition, thereby driving the demand for new cars and their interior components.

GROWING DEMAND FOR BETTER INTERIORS IN VEHICLES

The automotive industry has witnessed a significant shift towards enhanced interior quality and aesthetics, driven by increasing consumer demands for high-performance cars and new aesthetic appearances. This trend has particularly impacted the demand for interior automotive OEM coatings used in various components such as dashboards, steering wheels, seat covers, and other plastic finishing elements in car interiors. The growing demand for customized cars, especially in the luxury segment, has created a substantial market for interior automotive OEM coatings, as customization often involves modifications to interior components to create distinctive appearances that differ from the original factory versions. The availability of economical customization options, coupled with updated technology, has further fueled the demand for interior automotive OEM coatings among car enthusiasts.

The intensifying competition among automotive manufacturers has led to substantial investments in providing high-performance features, visually appealing interiors, and sound-proofing finishes. Manufacturers are focusing on developing coatings that can provide multiple benefits including durability, aesthetic appeal, and functional properties. The application of these coatings extends to various interior components such as door trims, handles, airbags, center clusters, meter clusters, instrument panels, speaker grills, armrest bezels, and steering wheels. This comprehensive approach to interior enhancement has created a robust demand for specialized coating solutions that can meet both aesthetic and functional requirements while maintaining high quality and durability standards. The automotive OEM interior coatings market is poised for growth as these trends continue to evolve, with significant opportunities in the development of innovative automotive interior paint solutions.

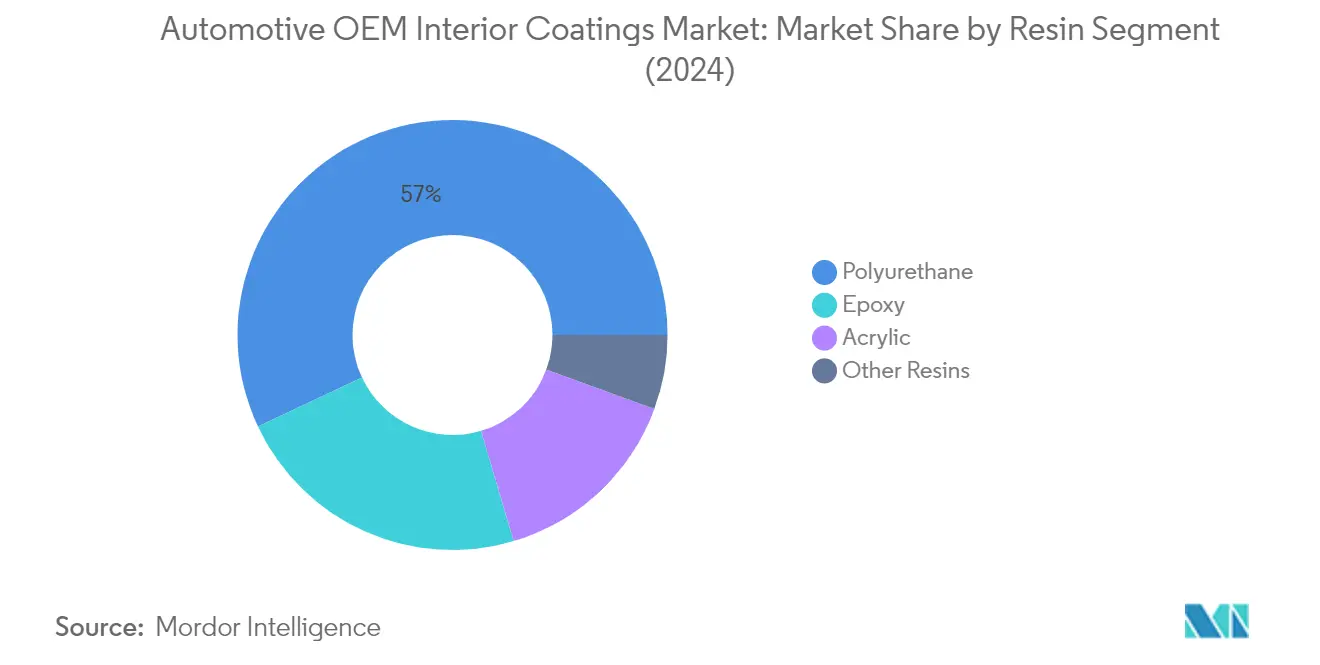

Segment Analysis: RESIN

Polyurethane Segment in Automotive OEM Interior Coatings Market

The polyurethane segment dominates the automotive OEM interior coatings market, commanding approximately 57% of the total market share in 2024. Polyurethane coatings are extensively used in automotive interior paint applications due to their superior properties, including high gloss, smooth finish, and excellent scratch resistance. These coatings are particularly suitable for a wide range of automotive interior plastic surfaces, including ABS, PC, PVC/vinyl, polyphenylene ether (PPE), and polyamide (PA) blends. Additionally, polyurethane coatings are utilized as coating materials for automotive interior wood surfaces in premium vehicles, and bio-based polyurethane coatings find applications in automotive leather treatments. The segment's growth is driven by the increasing use of plastics in interior parts and components, as well as the rising demand for high-quality interior finishes in modern vehicles.

Remaining Segments in Automotive OEM Interior Coatings Market

The automotive OEM interior coatings market encompasses several other significant resin segments, including epoxy, acrylic, and other specialty resins. Epoxy coatings play a crucial role in providing corrosion protection and ensuring adhesion of coatings on automobile OEM interiors, particularly for metal surfaces and parts such as door sills and handles. Acrylic coatings, available in both water-based and solvent-based formulations, are often used in combination with other coating types to provide additional protective layers on automotive interior parts. The other resins segment, which includes polyester and polypropylene-based coatings, serves specific applications such as providing finishes for automotive leather seats and specialized interior components, contributing to the overall diversity of coating solutions in the automotive interior market.

Segment Analysis: LAYER

Primer Segment in Automotive OEM Interior Coatings Market

The primer segment dominates the automotive OEM interior coatings market, commanding approximately 52% of the total market share in 2024. Primers serve as the crucial second functional layer in automotive interior coating applications, acting as an intermediate coat between e-coat and topcoats. These coatings are extensively used in automotive interiors where adhesion is required for other coats and in areas exposed to sunlight and weather conditions. The segment's dominance is attributed to its essential role in providing excellent stone chip protection and UV ray protection to the e-coat film. Major suppliers like Akzo Nobel, PPG, Kansai Nerolac, and KCC Coatings continue to innovate and develop advanced primer solutions for various automotive interior applications, particularly focusing on epoxy, polyurethane-modified polyesters, and acrylic-based formulations that offer superior protection and adhesion properties.

Base Coat Segment in Automotive OEM Interior Coatings Market

The base coat segment represents a significant portion of the automotive OEM coatings market, serving as the third coating layer and the final color-determining layer for vehicle components. Base coats are primarily formulated with polyurethane and polyacrylate resins, which enhance brilliance and elasticity while providing resistance against stone chipping. These coatings are available in various types, including solid base coats, metallic base coats, and pearlescent base coats, catering to different interior applications such as trunk interiors and interior framework components. The versatility of base coats in providing both functional and aesthetic properties makes them essential for automotive interior applications, particularly in areas requiring specific color matching and durability requirements.

Remaining Segments in Layer Segmentation

The clear coat segment completes the layer segmentation of the automotive OEM interior coatings market, serving as the final protective layer for interior components. Available in 1K, 2K, and powder systems, these coatings are primarily acrylic or polyurethane-based and are specifically designed for functional and decorative purposes in automobile interiors. While clear coats have limited application compared to primers and base coats in interior applications, they play a crucial role in providing protection against environmental factors, chemicals, scratches, and corrosion while offering UV resistance for specific interior components where high durability and aesthetic appeal are required.

Segment Analysis: VEHICLE TYPE

Passenger Cars Segment in Automotive OEM Interior Coatings Market

The passenger cars segment dominates the automotive OEM interior coatings market, commanding approximately 59% of the total market share in 2024. This segment's prominence is driven by the increasing consumer demand for high-quality interior finishes and aesthetic appeal in passenger vehicles. Various types of single and multi-component coatings, including both solvent-borne and waterborne varieties, are extensively used for coating different substrates like ABS and polycarbonate materials in passenger car interiors. These coatings find applications across multiple interior components, including center clusters, meter clusters, instrument panels, speaker grills, armrests and armrest bezels, steering wheels, door trim, and handles. The segment's growth is further bolstered by the rising preference for personal mobility solutions and the increasing focus on interior comfort and aesthetics in modern passenger vehicles. Additionally, the growing adoption of electric vehicles in the passenger car segment is creating new opportunities for specialized interior coating solutions.

Light Commercial Vehicles Segment in Automotive OEM Interior Coatings Market

The light commercial vehicles segment, which includes vans, mini trucks, delivery trucks, caravans, and small buses under 10 metric tons, represents a significant portion of the automotive OEM interior coatings market. This segment has shown resilient growth potential, particularly driven by the expanding e-commerce sector and last-mile delivery requirements. The demand for interior coatings in this segment is influenced by both functional and aesthetic requirements, as commercial vehicle manufacturers increasingly focus on driver comfort and interior durability. The segment's growth is supported by rising urbanization, growth in online retail, and the increasing need for small commercial vehicles in developing economies. Additionally, the introduction of new regulations regarding vehicle interior safety and comfort standards has led to increased attention to interior coating quality in light commercial vehicles.

Remaining Segments in Vehicle Type

The heavy commercial vehicles and other vehicle types segments complete the market landscape for automotive OEM interior coatings. The heavy commercial vehicles segment, encompassing heavy trucks, buses, and coaches, requires specialized interior coatings that focus primarily on durability and resistance to wear and tear. These coatings need to withstand more intensive use and harsher conditions compared to passenger vehicles. The other vehicle types segment, which includes agricultural vehicles like tractors and specialty vehicles, represents a niche market with specific requirements for interior coatings that must withstand unique operating conditions and environmental factors. Both segments contribute to the market's diversity by demanding specialized coating solutions that meet their particular operational requirements and regulatory standards.

Automotive OEM Interior Coatings Market Geography Segment Analysis

Automotive OEM Interior Coatings Market in Asia-Pacific

The Asia-Pacific region represents a dominant force in the automotive OEM interior coatings market, driven by its robust automotive manufacturing infrastructure and growing vehicle production capabilities. The region encompasses major automotive manufacturing hubs, including China, India, Japan, and South Korea, each contributing significantly to the market's dynamics. These countries have established themselves as key players in the global automotive supply chain, with extensive networks of OEM manufacturers and tier suppliers. The region's market is characterized by increasing investments in automotive production facilities, growing domestic demand for vehicles, and rising consumer preferences for quality interior finishes.

Automotive OEM Interior Coatings Market in China

China maintains its position as the largest market for automotive OEM interior coatings in the Asia-Pacific region, commanding approximately 52% of the regional market share. The country's dominance is supported by its massive automotive production capacity, extensive network of domestic and international automotive manufacturers, and robust supply chain infrastructure. China's market is characterized by strong domestic demand, technological advancement in coating applications, and an increasing focus on electric vehicle production. The country's automotive sector continues to evolve with significant investments in manufacturing capabilities and a growing emphasis on high-quality interior finishes.

Automotive OEM Interior Coatings Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 2% during 2024-2029. The country's automotive sector is experiencing rapid transformation driven by increasing domestic demand, a growing middle-class population, and expanding manufacturing capabilities. India's automotive OEM interior coatings market is benefiting from significant investments in automotive production facilities, rising consumer preferences for better interior finishes, and government initiatives supporting automotive manufacturing. The market is further strengthened by the presence of major global automotive manufacturers and their growing focus on localizing production.

Automotive OEM Interior Coatings Market in North America

The North American automotive OEM interior coatings market demonstrates a mature and technologically advanced landscape, encompassing the United States, Canada, and Mexico. The region's market is characterized by high standards of quality, stringent regulatory requirements, and continuous technological innovations in coating applications. The presence of major automotive manufacturers, established supply chains, and advanced manufacturing facilities contributes to the region's significant position in the global market.

Automotive OEM Interior Coatings Market in United States

The United States dominates the North American market, accounting for approximately 66% of the regional market share. As the region's largest automotive manufacturing hub, the country maintains its leadership through advanced manufacturing capabilities, strong research and development infrastructure, and high adoption of innovative coating technologies. The U.S. market is characterized by stringent quality standards, an increasing focus on sustainable coating solutions, and growing demand for premium interior finishes in vehicles.

Automotive OEM Interior Coatings Market Growth in United States

The United States also leads the region in terms of growth potential, with a projected growth rate of approximately 2% during 2024-2029. The market's growth is driven by increasing demand for electric vehicles, rising consumer preferences for high-quality interior finishes, and continuous technological advancements in coating applications. The country's strong focus on research and development, coupled with investments in sustainable coating solutions, positions it for sustained growth in the automotive OEM coatings market.

Automotive OEM Interior Coatings Market in Europe

The European automotive OEM interior coatings market represents a sophisticated and quality-driven landscape, with Germany, the United Kingdom, France, and Italy as key contributing nations. The region's market is characterized by its strong focus on technological innovation, environmental sustainability, and premium quality standards. European automotive manufacturers are known for their emphasis on superior interior finishes and sustainable coating solutions.

Automotive OEM Interior Coatings Market in Germany

Germany maintains its position as the largest market for automotive OEM interior coatings in Europe. The country's leadership is built on its robust automotive manufacturing sector, strong technological capabilities, and presence of major automotive manufacturers. German automotive producers are known for their high-quality standards and innovative approaches to interior coating applications, supported by extensive research and development activities.

Automotive OEM Interior Coatings Market in Italy

Italy emerges as the fastest-growing market within Europe for automotive OEM interior coatings. The country's growth is driven by its strong focus on luxury vehicle production, increasing investments in coating technologies, and a growing emphasis on sustainable solutions. Italian manufacturers are known for their expertise in premium coating applications and innovative approaches to interior finishing, particularly in the luxury vehicle segment.

Automotive OEM Interior Coatings Market in South America

The South American automotive OEM interior coatings market is characterized by its evolving nature and growing potential, with Brazil and Argentina as key markets. The region's market dynamics are influenced by changing automotive production patterns, economic conditions, and increasing investments in manufacturing capabilities. Brazil emerges as both the largest and fastest-growing market in the region, supported by its substantial automotive manufacturing base and growing domestic demand for vehicles.

Automotive OEM Interior Coatings Market in Middle East & Africa

The Middle East & Africa automotive OEM interior coatings market demonstrates growing potential, with Iran and South Africa as significant contributors. The region's market is characterized by increasing investments in automotive manufacturing capabilities and rising domestic demand for vehicles. Iran represents the largest market in the region, while South Africa shows promising growth potential, driven by its developing automotive manufacturing sector and government initiatives supporting industry growth.

Competitive Landscape

Top Companies in Automotive OEM Interior Coatings Market

The automotive OEM interior coatings market features prominent players like Axalta, AkzoNobel, BASF SE, PPG Industries, and The Sherwin-Williams Company leading the industry through continuous innovation and strategic expansion. These companies are focusing heavily on research and development to create advanced coating solutions that meet evolving automotive interior requirements while complying with environmental regulations. The industry witnesses regular product launches featuring improved scratch resistance, enhanced durability, and eco-friendly formulations. Companies are strengthening their global presence through strategic acquisitions of regional players and the establishment of new manufacturing facilities, particularly in emerging markets. Operational excellence is being achieved through backward integration of supply chains, investment in automated production technologies, and development of comprehensive distribution networks. Market leaders are also forming strategic partnerships with automotive manufacturers to develop customized coating solutions and ensure long-term supply agreements.

Consolidated Market with Strong Regional Players

The automotive OEM coatings market demonstrates a partially consolidated structure, with major global players holding significant market share while regional specialists maintain a strong local presence. These leading companies operate as diversified chemical conglomerates with dedicated automotive coating divisions, leveraging their extensive research capabilities and established relationships with automotive manufacturers. The market has witnessed increased consolidation through strategic acquisitions, particularly with global players acquiring regional coating manufacturers to expand their geographic footprint and technical capabilities. The competitive dynamics are characterized by a mix of multinational corporations and specialized coating manufacturers, each bringing unique strengths in terms of technology, customer relationships, and market understanding.

The industry landscape is shaped by ongoing merger and acquisition activities, with companies like PPG Industries actively pursuing strategic acquisitions to strengthen their market position and expand their product portfolio. Market participants are increasingly focusing on vertical integration to ensure supply chain stability and cost optimization. Regional players maintain their relevance through specialized product offerings and strong local customer relationships, while global players leverage their broad product portfolios and extensive distribution networks to serve multinational automotive manufacturers.

Innovation and Sustainability Drive Future Success

Success in the automotive OEM coatings market increasingly depends on companies' ability to innovate while meeting stringent environmental regulations and customer requirements. Market incumbents are focusing on developing eco-friendly coating solutions, investing in advanced manufacturing technologies, and strengthening their research and development capabilities to maintain their competitive edge. Companies are also emphasizing the development of customized solutions for specific customer needs, while building long-term partnerships with automotive manufacturers to secure their market position. The ability to provide comprehensive coating solutions, technical support, and global supply capabilities has become crucial for maintaining market leadership.

For contenders looking to gain market share, the focus needs to be on developing specialized coating solutions for specific applications or regional markets, while building strong technical capabilities and customer relationships. The industry's high barriers to entry, including stringent quality requirements and established customer relationships, necessitate strategic approaches for market penetration. Companies must also consider the increasing concentration of automotive manufacturers and their growing influence on coating specifications and supplier selection. The regulatory landscape, particularly regarding environmental standards and VOC emissions, continues to shape product development and manufacturing processes, making compliance capabilities a critical success factor.

Automotive OEM Interior Coatings Industry Leaders

Akzo Nobel N.V.

BASF SE

Axalta Coating Systems, LLC

Kansai Nerolac Paints Limited

PPG Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- In May 2021, PPG completed the acquisition of Wörwag, which is a global manufacturer of coatings for industrial and automotive applications.

- In February 2020, PPG Industries announced the acquisition of Industria Chimica Reggiana (ICR) SpA, a manufacturer of paints and coatings for the automotive refinish and light industrial coatings industries. ICR is based in Italy and manufactures automotive refinish products, including putties, primers, basecoats, and clear coats under the SPRINT brand.

- In July 2019, BASF SE expanded its automotive coatings production in North America with investments of nearly USD 40 million. The investments add capacity to the company's production plants in Greenville, Ohio, and Tultitlan, Mexico.

Global Automotive OEM Interior Coatings Market Report Scope

The automotive OEM paints and coatings can be classified as water-based or solvent-based, depending on the drying technique employed. Water-based coatings contain water as a volatile compound and solvent-based coatings contain volatile compounds like benzene. The market is segmented by resin, layers, vehicle type, and geography. By resin, the market is segmented into epoxy, polyurethane, acrylic, and other resins. By layer, the market is segmented into primer, base coat, and clear coat. By vehicle type, the market is segmented into, passenger cars, light commercial vehicles, heavy commercial vehicles, and other vehicle types. The report also covers the market size and forecasts for the automotive OEM interior coatings market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Epoxy |

| Polyurethane |

| Acrylic |

| Other Resins |

| Primer |

| Base Coat |

| Clear Coat |

| Passenger Car |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Other Vehicle Types |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Iran |

| South Africa | |

| Rest of Middle-East and Africa |

| Resin | Epoxy | |

| Polyurethane | ||

| Acrylic | ||

| Other Resins | ||

| Layer | Primer | |

| Base Coat | ||

| Clear Coat | ||

| Vehicle Type | Passenger Car | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| Other Vehicle Types | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Iran | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current Automotive OEM Interior Coatings Market size?

The Automotive OEM Interior Coatings Market is projected to register a CAGR of greater than 2.5% during the forecast period (2025-2030)

Who are the key players in Automotive OEM Interior Coatings Market?

Akzo Nobel N.V., BASF SE, Axalta Coating Systems, LLC, Kansai Nerolac Paints Limited and PPG Industries Inc. are the major companies operating in the Automotive OEM Interior Coatings Market.

Which is the fastest growing region in Automotive OEM Interior Coatings Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Automotive OEM Interior Coatings Market?

In 2025, the Asia Pacific accounts for the largest market share in Automotive OEM Interior Coatings Market.

What years does this Automotive OEM Interior Coatings Market cover?

The report covers the Automotive OEM Interior Coatings Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Automotive OEM Interior Coatings Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: