Automotive Interior Ambient Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

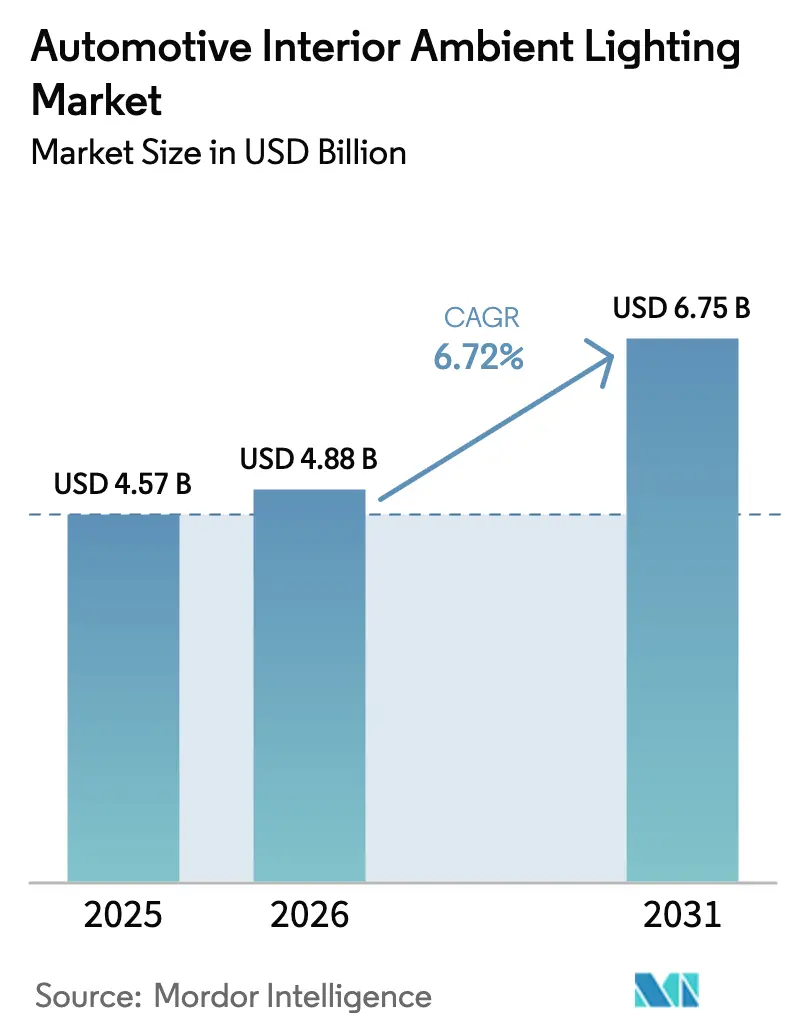

| Market Size (2026) | USD 4.88 Billion |

| Market Size (2031) | USD 6.75 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

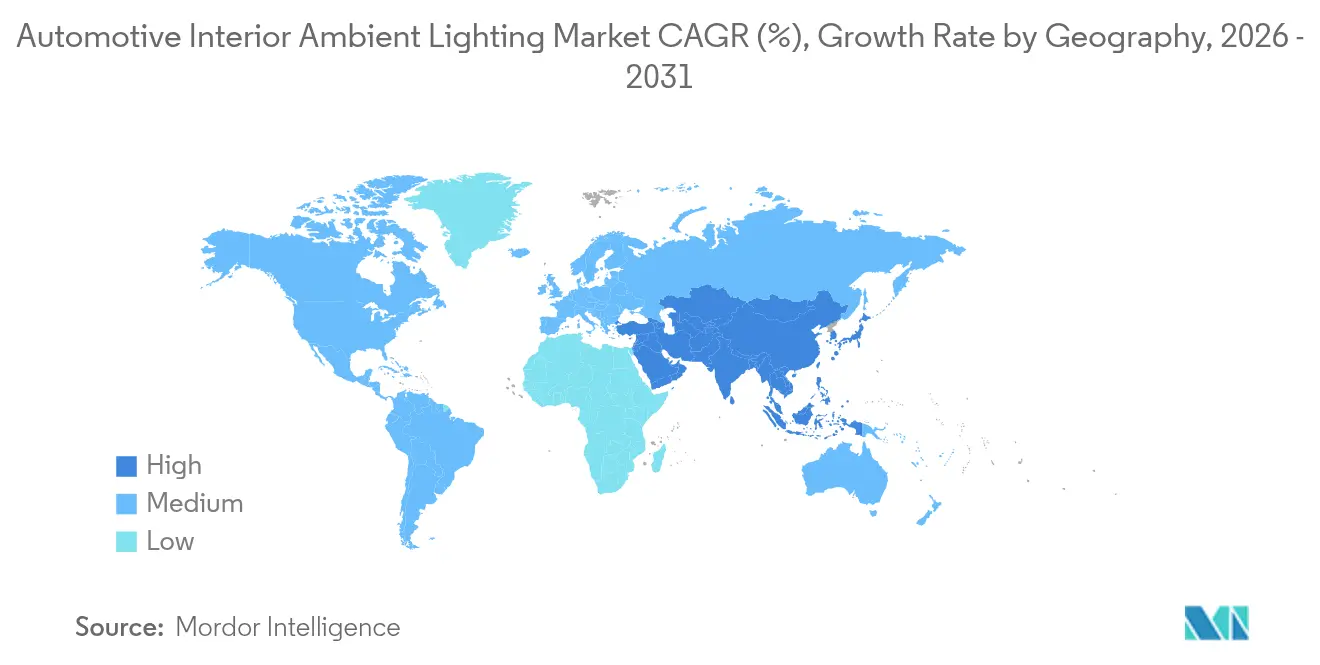

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Interior Ambient Lighting Market Analysis by Mordor Intelligence

The automotive interior ambient lighting market size in 2026 is estimated at USD 4.88 billion, growing from 2025 value of USD 4.57 billion with 2031 projections showing USD 6.75 billion, growing at 6.72% CAGR over 2026-2031. Sustained demand for customizable cabin experiences, regulatory attention to interior safety cues and rapid progress in LED and OLED technologies are widening adoption across vehicle classes. Automakers are embedding dynamic multi-color signatures that serve both branding and driver-assistance purposes, while cost reductions from vertically integrated Tier-1 suppliers are pushing advanced light modules into mainstream segments. The continued rise of battery electric vehicles (BEVs), ride-hailing fleets and large digital cockpit displays is further amplifying the role of ambient lighting as a core differentiator within connected cabins. Competition is intensifying as semiconductor and electronics firms enter a field historically led by traditional lighting companies.

Key Report Takeaways

- By product type, Ambient Light Modules led with 45.40% of the automotive interior ambient lighting market share in 2025, while Head-Up Display Light Engines are set to expand at a 9.07% CAGR through 2031.

- By technology, LED dominated with a 91.10% revenue share in 2025; OLED is projected to grow fastest at a 11.78% CAGR to 2031.

- By application position, door panels held 28.10% of the automotive interior ambient lighting market size in 2025; headliner and roof uses are advancing at an 11.52% CAGR.

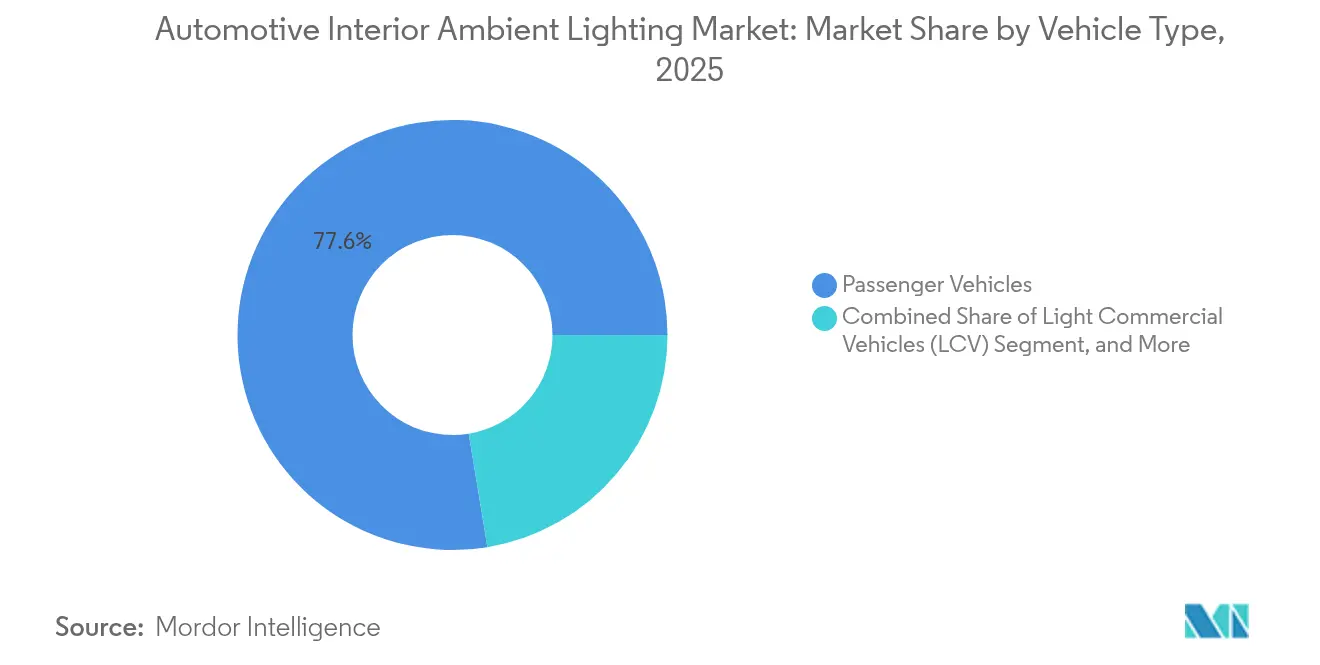

- By vehicle type, passenger cars accounted for 77.60% of revenue in 2025, whereas light commercial vehicles record the highest projected CAGR at 8.98% to 2031.

- By vehicle class, mid-range models captured 41.10% share in 2025, but luxury and ultra-luxury cars are growing at a 10.02% CAGR.

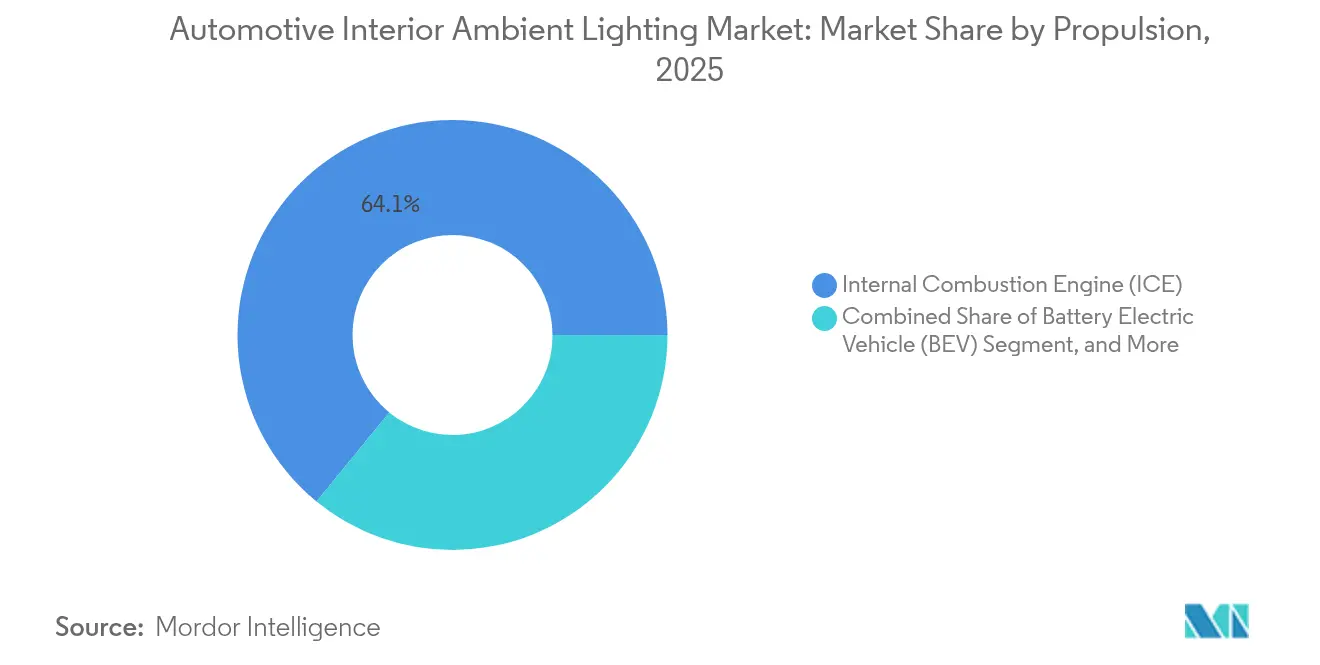

- By propulsion, ICE vehicles retained 64.10% share in 2025, yet BEVs post a 9.56% CAGR over the forecast horizon.

- By sales channel, OEM-fitted systems dominated with an 88.50% share in 2025; the aftermarket rises at an 8.78% CAGR as owners retrofit existing cabins.

- By geography, Asia Pacific led with 37.20% revenue in 2025, while the Middle East & Africa region is the fastest climber at 7.48% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Interior Ambient Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing OEM demand for multi-color dynamic light signatures | +1.8% | Global, with early adoption in Europe and China | Medium term (2-4 years) |

| Integration of Human-Machine-Interface (HMI) lighting in premium EVs | +1.5% | North America, Europe | Medium term (2-4 years) |

| Regulatory push toward interior‐light assisted ADAS alerts (UNECE R-48) | +1.2% | Europe, with global spillover | Long term (≥ 4 years) |

| Tier-1 supplier vertical integration lowering unit cost of flexible OLED strips | +0.9% | Global | Short term (≤ 2 years) |

| Ride-sharing fleet refurbishments adopting ambient lighting for brand differentiation | +0.7% | Asia, with expansion to North America | Medium term (2-4 years) |

| Accelerated adoption of addressable RGB LED controllers by Chinese NEV start-ups | +0.6% | Asia Pacific, with technology transfer to global markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing OEM Demand for Multi-color Dynamic Light Signatures

Manufacturers now treat animated cabin lighting as a signature brand element, moving beyond static hues to sequences that react to drive modes, external light and occupant profiles. The registered OSIRE RGB family enables single-controller orchestration of dozens of addressable nodes, allowing flowing welcome effects and synchronized pulses that emphasize audio beats.[1]ams OSRAM, “Automotive & Mobility – Ambient Lighting,” ams-osram.comEuropean premium models first normalized such features; cost-optimized controllers from Chinese suppliers are accelerating diffusion to mid-range crossovers sold in Southeast Asia and South America. Cabin personalization packages that once commanded high premiums are increasingly bundled as standard thanks to reduced LED-per-meter prices. Automakers also discover incremental revenue in software updates that unlock additional color palettes over the vehicle life cycle.

Integration of Human-Machine-Interface Lighting in Premium EVs

Electric vehicles adopt ambient strips that double as contextual displays for range status, charge progress or route alerts. FORVIA’s latest cockpit demonstrators combine overhead light guides with seat-belt buckles that flash coded colors to prompt driver action during automated-to-manual transitions.[2]FORVIA, “AutoShanghai 2025 Press Kit,” forvia.com At night, subdued cyan gradients around central screens minimize glare while preserving vital instrument readability. The seamless blend of visual cues and voice feedback is elevating perceived sophistication, and the model year 2025 launches from leading North American brands showcase how lighting is now intertwined with holistic HMI orchestration rather than isolated accent decor.

Regulatory Push Toward Interior-Light-Assisted ADAS Alerts

UNECE R-48 revisions mandate that interior alerts linked to driver-assist functions be both unmistakable and non-distracting.[3]United Nations Economic Commission for Europe, “Draft UN Regulation on Driver Control Assistance Systems,” unece.org Sector leaders respond with circumferential lightbars embedded in door trims that glow amber when lane keep assist senses unintended drift and flash red when imminent collision warnings trigger. Harmonizing animation length, brightness ramps and color semantics across markets is becoming a design imperative, prompting suppliers to share software libraries certified under automotive functional safety standards. The regulatory impetus is expected to solidify a common design language that strengthens supplier value propositions built around system-level compliance expertise

Tier-1 Supplier Vertical Integration Lowering Unit Cost of Flexible OLED Strips

Integrated players now fabricate substrates, encapsulate diodes and assemble wiring harnesses under one roof, eliminating multi-tier mark-ups and accelerating design cycles. Average per-vehicle cost for wide, seamlessly lit door cards has dropped by around 20% since 2023, encouraging A-segment urban cars in India and Indonesia to offer single-color light guides as showroom differentiators. Consolidated engineering capabilities also foster rapid experimental iterations, for example combining printed sensors directly onto OLED films so that a gentle swipe on the armrest simultaneously changes music track and cabin hue, enhancing perceived innovation without inflating part count.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EMC compliance challenges for multi-channel LED drivers | -0.8% | Global, with higher impact in regions with stringent regulations | Medium term (2-4 years) |

| Persistent thermal-management issues with high-density LED arrays in headliners | -0.7% | Global | Short term (≤ 2 years) |

| Limited aftermarket standardisation across regional in-car lighting regulations | -0.6% | Global, with particular impact in North America and Europe | Long term (≥ 4 years) |

| Cost-sensitive A-segment ICE cars delaying adoption in LATAM & Africa | -0.5% | Latin America, Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EMC Compliance Challenges for Multi-channel LED Drivers

As cabin schemes approach 48 zones or more, fast-switching drivers can radiate interference that impacts critical networks such as CAN-FD and ultrasound parking sensors.[4]Melexis, “MLX81116 Multichannel RGB-LED Driver Brings Smart Interior Lighting to Life,” melexis.com Achieving consistent color under varying battery voltages while meeting CISPR 25 limits demands costly filtering components and extended test schedules. Smaller tier-2 providers lacking in-house electromagnetic chambers rely on external labs, extending program timelines and eroding margins. The enhanced MLX81116 series mitigates part of the issue with spread-spectrum modulation yet complexity remains when dozens of units operate in close proximity.

Persistent Thermal-Management Issues with High-Density LED Arrays in Headliners

Star-field headliners and panoramic halo rings pack hundreds of emitters into confined foam substrates where convection is minimal. Junction temperatures that exceed 125 °C lead to luminous flux decay and discoloration of translucent films. Novel graphite heat spreaders and micro-perforated backplanes are showing promise, but production scalability and material cost currently restrain full-roof implementations outside top-tier luxury sedans. Development teams balance brightness, energy draw and lifetime, sometimes sacrificing pixel density to avert warranty risks, which delays broader proliferation of cinematic headliner effects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Head-Up Display Engines Accelerate Growth

Head-Up Display Light Engines recorded the fastest 9.07% CAGR outlook from 2026 to 2031 as automakers merge information projection with mood lighting to create layered depth cues. Ambient Light Modules nevertheless commanded 45.40% of the automotive interior ambient lighting market size in 2025 due to their ubiquitous fitment in door sills, footwells and decorative trims. The segment benefits from simplified harnesses and controller standardization that permit linear light guides to be trimmed to length on the assembly line, reducing part proliferation. Suppliers embed touch-sensitive patches directly onto light modules, enabling door unlock gestures or seat memory recalls using illuminated icons. Over the forecast window, convergence between projection engines, cluster displays and accent lighting is anticipated, forming cohesive visual ecosystems that reduce driver cognitive load.

Product developers also push further miniaturization of light engines that combine optic, phosphor conversion and driver logic into coin-sized packages. Such modules support augmented reality windshields by projecting traffic alerts while simultaneously illuminating the A-pillar trim to direct gaze toward merging lanes. As OLED strips gain bend radius flexibility below 10 mm, center console and seat-back pockets may receive curved lighting shapes previously impossible with rigid LED boards. This fusion of functional guidance and ambience is poised to embed advanced modules deeper into the mid-size SUV mainstream, propelling continued value growth within the automotive interior ambient lighting market.

By Technology: OLED Disrupts LED Dominance

LED technology retained a 91.10% slice of revenue in 2025, upheld by high efficacy, established supply chains and a constantly falling cost curve. Yet the 11.78% CAGR forecast for OLED signifies mounting preference for paper-thin, uniformly glowing surfaces that follow complex interior geometries. Designers exploit OLED sheets to deliver seamless light carpets over instrument panels without visible hotspots, a feat difficult for conventional LEDs even with advanced diffusers. The automotive interior ambient lighting market share of OLED is therefore expected to climb steadily alongside increases in yield and durability of automotive-grade organic emitters.

Hybrid strategies are spreading wherein OLED forms the primary diffuse plane while micro-optic LEDs inject targeted accents for chaser effects. Laser and fiber-optic solutions exist in niche use cases such as ultra-thin air-vent edging and backlit logos that require millimeter-scale apertures. Research into inorganic microLED tiles hints at future possibilities of high-resolution light matrices that display dynamic patterns across seat fabrics. For now, LED remains the volume driver, but accelerated investment by display panel giants is set to shift the cost parity threshold in favor of flexible OLED before the end of the decade, adding fresh momentum to the automotive interior ambient lighting market.

By Application Position: Headliners Illuminate Future Growth

Door panel installations ruled with 28.10% of 2025 revenue, reflecting their prominent placement at eye level and relative ease of packaging. Headliner and roof placements, however, show an 11.52% CAGR trajectory as panoramic glass roofs and cross-vehicle light arcs become hallmark features of premium crossovers. The automotive interior ambient lighting market size for these overhead elements expands in tandem with consumer appetite for immersive, lounge-like cabins. Full-width roof lightbars adjust from cool daylight tones during commutes to warm glows for evening drives, synchronizing with circadian lighting preferences.

Dashboard and instrument cluster surrounds remain critical both for visual cohesion and glare mitigation. Thin cross sections permit integration alongside curved displays, forming floating island themes popular in 2025 model-year EVs. Footwell illumination continues to enhance perceived spaciousness; programmable brightness now adapts to entrance detection, dimming once occupants settle. Console and cup-holder rings are increasingly interactive, pulsing during voice assistant feedback or navigation prompts. Collectively, these positions underpin differentiated UX narratives in an increasingly digital cockpit age, driving value growth across the automotive interior ambient lighting market.

By Vehicle Type: Light Commercial Vehicles Gain Momentum

Passenger cars continued to dominate the automotive interior ambient lighting market with 77.60% share in 2025, yet light commercial vehicles chart the quickest 8.98% CAGR path. Ride-sharing operators specify multicolor cabin kits that align with app branding, enhancing rider trust and driver ratings. Delivery fleets adopt red-shift night modes that maintain driver alertness without disturbing residential neighborhoods during late runs. The highest-end coaches and minibuses adopt waterfall ceiling patterns to elevate comfort on inter-city journeys, an area previously exclusive to aviation.

Automakers tailor lighting strategies to vehicle mission profiles. Family-oriented SUVs emphasize playful color themes selectable by rear passengers, while workhorse vans integrate white flood illumination for cargo checks. Modular plug-and-play harnesses simplify upfit conversions, a crucial factor for fleet downtime cost control. These trends collectively widen addressable volumes for suppliers and inject fresh demand into the automotive interior ambient lighting market

By Vehicle Class: Luxury Segment Drives Innovation

Mid-range cars held a 41.10% slice in 2025, underscoring how ambient lighting has become an expected comfort within USD 25,000-40,000 vehicles. Luxury and ultra-luxury models nonetheless remain the innovation spearhead, clocking a 10.02% CAGR that shapes consumer expectations for the broader automotive interior ambient lighting market. Flagship sedans deploy welcome-home choreographies that blend exterior pixel headlamps with interior wave effects, providing theater-style first impressions. Scent diffusers, 3D sound zones and massage seats now synchronize with light color transitions, creating multisensory mood suites selectable through a single menu tile.

Economy cars still lean on simpler single-color strips around the console, yet manufacturing cost compression is shortening the trickle-down cycle. Five-year product plans from volume OEMs reveal intentions to standardize at least footwell and door pocket LED elements on all trims, further enlarging penetration. Tier-1 suppliers craft scalable product families where optic designs and controller firmware remain consistent across classes, unlocking economies yet leaving room for feature scaling that preserves perceived hierarchy.

By Propulsion: BEVs Illuminate the Electrified Future

ICE vehicles retained 64.10% of 2025 sales; however, BEVs seize attention with a 9.56% CAGR as brands leverage ambient lighting to underline clean propulsion narratives. Charge status light pulses in dashboards and exterior charge ports now mirror interior halo colors, reinforcing intuitive feedback loops. Software updates push new visualization schemes that celebrate carbon-free miles reached or eco-driving scores, cultivating owner loyalty. PHEVs occupy a bridging role, with lighting that toggles between blue electric modes and green hybrid modes, educating drivers on power-train transitions.

Chinese new-energy vehicle (NEV) startups highlight addressable RGB controllers that play synchronized light-sound-screen shows during pre-trip inspections. Such advanced routines position lighting as an integral element of the digital service layer rather than a static component. The propulsion shift therefore serves as a catalyst for feature experimentation, boosting the overall automotive interior ambient lighting market.

By Sales Channel: Aftermarket Customization Expands

OEM installation accounted for 88.50% of shipments in 2025, reflecting deeper design integration, rigorous safety validation and maturing platform strategies. Yet an 8.78% CAGR signals vibrant aftermarket growth as tech-savvy owners retrofit door pocket strakes or roof starlights using plug-in harness kits that preserve warranty integrity. Online configurators let customers preview color themes against their vehicle trim, spurring impulse purchases. Authorized dealer accessory lines bundle BLE-enabled controllers that sync with smartphone apps, bridging the gap between factory options and DIY kits.

Standardization challenges persist due to regional wiring norms and varying in-car network protocols. Collaborative programs between OEMs and accessory giants are emerging to issue certified upgrade paths that safeguard EMC harmony. Transparent upgrade ecosystems stimulate brand engagement throughout the vehicle life cycle, injecting incremental revenue to the automotive interior ambient lighting market well beyond initial sales.

Geography Analysis

Asia Pacific commanded 37.20% of global revenue in 2025 as Chinese, Korean and Japanese OEMs push aggressive refresh cycles featuring large digital cockpits framed by sweeping lightbars. Local NEV startups integrate full-width dashboard ribbons and waterfall door strips as signature UX elements, driving supplier investment in regional capacity. Governments across South Korea and China prioritize vehicle electronics clusters, bolstering local component ecosystems that shorten lead times and foster cost advantages, thereby strengthening Asia Pacific’s anchor position in the automotive interior ambient lighting market.

Europe retains leadership in regulatory-driven innovation. UNECE directives accelerate cross-functional lighting-ADAS integration, prompting German and Swedish marques to pioneer safety-oriented color semantics that then migrate globally. High premium-vehicle density sustains value per car far above the world average. Supplier clusters in Germany, France and Italy specialize in precision optics, thin-film phosphors and specialty polymers, enabling differentiation even as cost pressure mounts.

North America embraces large-format pickups and SUVs whose spacious cabins invite extensive ambient schemes in pillars, roof rails and seat backs. The region’s strong customization culture propels the aftermarket, supporting a network of certified installers and e-commerce kit brands. The Middle East & Africa, though smaller, posts a 7.48% CAGR as luxury-SUV demand rises with household incomes, and as desert climates favor cooler interior color temperatures programmable through ambient controls. Latin America remains more price sensitive, yet flagship trims introduced by global OEMs now include footwell or console lighting, marking gradual diffusion into mass segments.

Competitive Landscape

The automotive interior ambient lighting market is moderately consolidated, anchored by integrated Tier-1 majors such as FORVIA (HELLA), Valeo and Koito. These leaders leverage combined optics, electronics and HMI design know-how to deliver turnkey solutions tightly aligned with OEM platform timelines. FORVIA’s acquisition of HELLA exemplifies a strategy that unites cockpit modules, smart surfaces and advanced illumination within one portfolio, allowing cost synergies and cohesive styling themes. Valeo, with a 16% global lighting systems share, channels OLED surface expertise into dynamic interior panels that double as soft displays, reinforcing its technology leadership.

Semiconductor specialists, notably ams OSRAM and Melexis, insert themselves deeper into system architecture by offering addressable drivers and intelligent LEDs that simplify wiring and enable over-the-air animation updates. Display titans explore cross-domain collaborations that merge instrument clusters with contiguous light zones, blurring category boundaries. Strategic alliances trump costly acquisitions in many cases, enabling rapid access to complementary patents while preserving organizational agility. Regional challengers in India and China carve niches by adhering to local sourcing quotas and offering tailored software stacks compatible with domestic infotainment operating systems.

White-space opportunities persist in health-oriented lighting that modulates circadian rhythms and stress levels using spectrum-controlled sequences. Suppliers that can integrate biometric sensors with software-defined lighting stand to secure design wins in upcoming autonomous shuttles. The drive toward low-power solutions also spurs R&D in higher-efficiency red and blue emitters, supporting OEM sustainability metrics. The next competitive frontier thus lies in holistic cabin ecosystems where ambient lighting, haptics and AI-driven interaction coalesce to yield differentiated brand identities

Automotive Interior Ambient Lighting Industry Leaders

Tenneco Inc.

Koito Manufacturing Co., Ltd

Akzo Nobel N.V.

OSRAM GmbH

General Electric

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Buick launched the 2025 Envision including selectable static ambient colors for user personalization.

- April 2025: Grupo Antolin introduced a lightweight headliner with high-density LEDs and advanced thermal control.

- April 2025: FORVIA showcased its Saphir Masterpiece at AutoShanghai 2025, featuring a holistic cabin HMI with multimodal interfaces and dynamic lighting solutions.

- March 2025: LG Innotek broadened its automotive LED line with components optimized for ambient lighting consistency.

- March 2025: Visteon Corporation expanded its digital cockpit suite, blending ambient lighting with displays to heighten immersion.

- January 2025: Continental AG rolled out an ambient lighting controller simplifying in-vehicle network integration

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the automotive interior ambient lighting market as the value generated by factory-installed and aftermarket systems that emit low-intensity colored or white light inside passenger and light commercial vehicle cabins, covering LED, OLED, fiber-optic, and laser modules integrated into doors, dashboards, footwells, headliners, and center consoles. Sensors, drivers, wiring harnesses, and dedicated control software that ship with these luminaires are also counted within revenue.

Scope exclusion: exterior accent, dashboard backlighting for instrument clusters, and non-automotive mood-lighting kits are outside this assessment.

Segmentation Overview

- By Product Type

- Dashboard Lights

- Ambient Light Modules (Roof, Door, Footwell)

- Head-Up Display Light Engines

- Center Console and Cup-holder Lights

- Others (Glove-box, Trunk, Seat-bolster)

- By Technology

- LED

- OLED

- Laser

- Fiber-optic

- By Application Position

- Door Panels

- Dashboard and Instrument Panel

- Footwell

- Headliner and Roof

- Center Console

- By Vehicle Type

- Passenger Vehicles

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV and Coaches)

- By Vehicle Class

- Economy

- Mid-range

- Luxury and Ultra-luxury

- By Propulsion

- Internal Combustion Engine (ICE)

- Battery Electric Vehicle (BEV)

- Plug-in Hybrid (PHEV)

- By Sales Channel

- OEM-fitted

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- South East Asia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed lighting-module engineers across Asia, the EU, and North America, design heads at mid-segment OEMs, and distributors serving the retrofit channel. These conversations validated average selling prices, color-customization take-rates, and the share of ambient packages bundled into ADAS upgrade trims, thereby filling gaps left by public statistics.

Desk Research

We collated production and trade tables from UN Comtrade, OICA vehicle build data, and ACEA new-registration releases, then blended them with patent trends on flexible light guides from Questel and LED ASP series available on UNCTAD. Regulatory briefs, such as UNECE R-48 interior-signal amendments, plus safety studies from NHTSA and Euro NCAP, anchored technology adoption assumptions. Company 10-Ks, investor decks, and automotive tier-one press releases supplied pricing and content-per-vehicle clues. Proprietary snapshots from D&B Hoovers and Dow Jones Factiva helped verify supplier revenue splits. The sources cited illustrate inputs; many additional open datasets underpinned corroboration.

Market-Sizing & Forecasting

A top-down build starts with regional vehicle production, adjusted for seating rows and trim-mix penetration, which is then cross-checked against sampled supplier revenue roll-ups for plausibility. Key levers include average light points per car, ASP erosion from LED commoditization, OEM option-package attachment rates, electric-vehicle share, regulation-driven color zoning, and aftermarket retrofit cycles. Forecasts employ multivariate regression that links ambient-package penetration to EV stock, premium-vehicle share, and median disposable income, before scenario analysis fine-tunes outlier regions. Where supplier disclosures are partial, inferred volumes are gap-filled through channel checks and capacity-utilization norms.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer analyst scrutiny, and final practice-lead sign-off. Variances above 5% versus fresh shipment trackers trigger source re-contact. Studies refresh annually, with mid-cycle revisions when regulatory or macro shocks materially affect the baseline.

Why Mordor's Automotive Interior Ambient Lighting Baseline Earns Trust

Published estimates often diverge because firms set differing cut-off years, exclude retrofit kits, or assume uniform ASP slides.

Key gap drivers here include whether light-engine software is bundled, if light points in commercial vans are tallied, and the speed at which analysts fold EV cockpit redesigns into penetration curves. Mordor's scope captures full hardware-plus-driver value and applies country-specific trim-mix data refreshed each year, whereas other publishers may rely on single-region averages or static price decks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.57 B (2025) | Mordor Intelligence | - |

| USD 1.70 B (2024) | Global Consultancy A | Counts only OEM fitment and omits light commercial vehicles plus aftermarket sales |

| USD 1.64 B (2023) | Trade Journal B | Uses constant ASP and excludes control electronics, leading to lower value recognition |

In summary, by anchoring volumes to verifiable production data, layering region-specific penetration insights, and reviewing outputs through multi-step validation, Mordor Intelligence delivers a balanced baseline that decision-makers can repeatedly trace and audit with confidence.

Key Questions Answered in the Report

What is the projected value of the automotive interior ambient lighting market by 2031?

It is forecast to reach USD 6.75 billion by 2031, expanding at a 6.72% CAGR over 2026-2031.

Which region currently leads demand for interior ambient lighting in vehicles?

Asia Pacific held 37.20% of global revenue in 2025 thanks to high vehicle output and fast feature adoption by Chinese manufacturers.

Why are headliner applications growing faster than other positions?

Panoramic roofs and immersive cabin concepts are driving an 11.52% CAGR for headliner and roof lighting, outpacing door-panel growth.

How quickly is OLED gaining share against LED inside vehicle cabins?

OLED technology is advancing at a 11.78% CAGR, eroding LED’s dominance as thinner, flexible panels enable seamless illuminated surfaces.

What challenges restrict broader rollout of sophisticated lighting effects?

EMC compliance for multi-channel drivers and thermal management in dense headliner arrays add cost and complexity, tempering adoption rates.

Are light commercial vehicles adopting ambient lighting features?

Yes, the segment shows a 8.98% CAGR as ride-sharing and delivery fleets use lighting for brand differentiation and driver comfort.

Page last updated on: