Ambient Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 82.19 Billion |

| Market Size (2031) | USD 123.53 Billion |

| Growth Rate (2026 - 2031) | 8.49% CAGR |

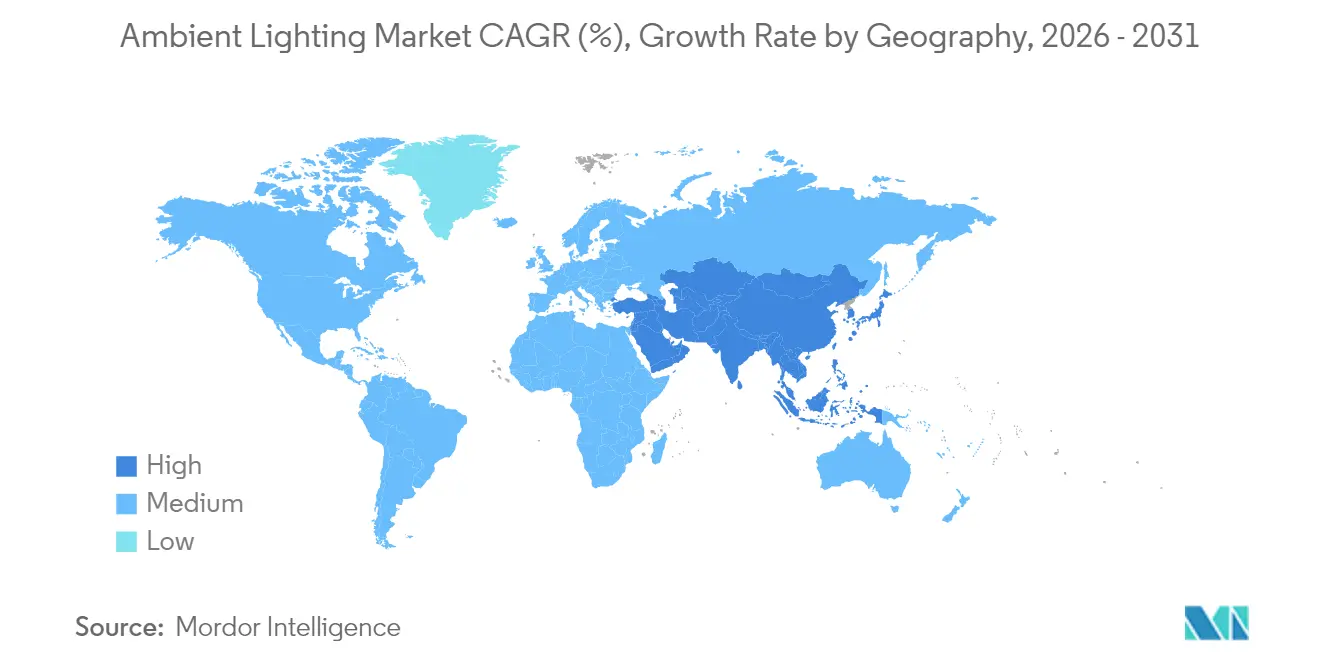

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

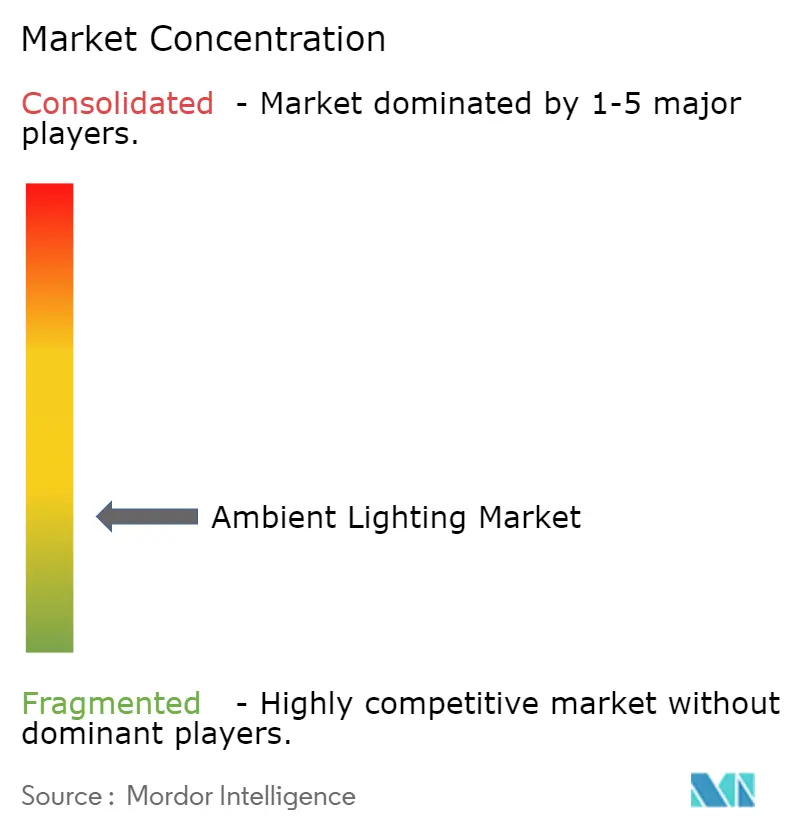

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ambient Lighting Market Analysis by Mordor Intelligence

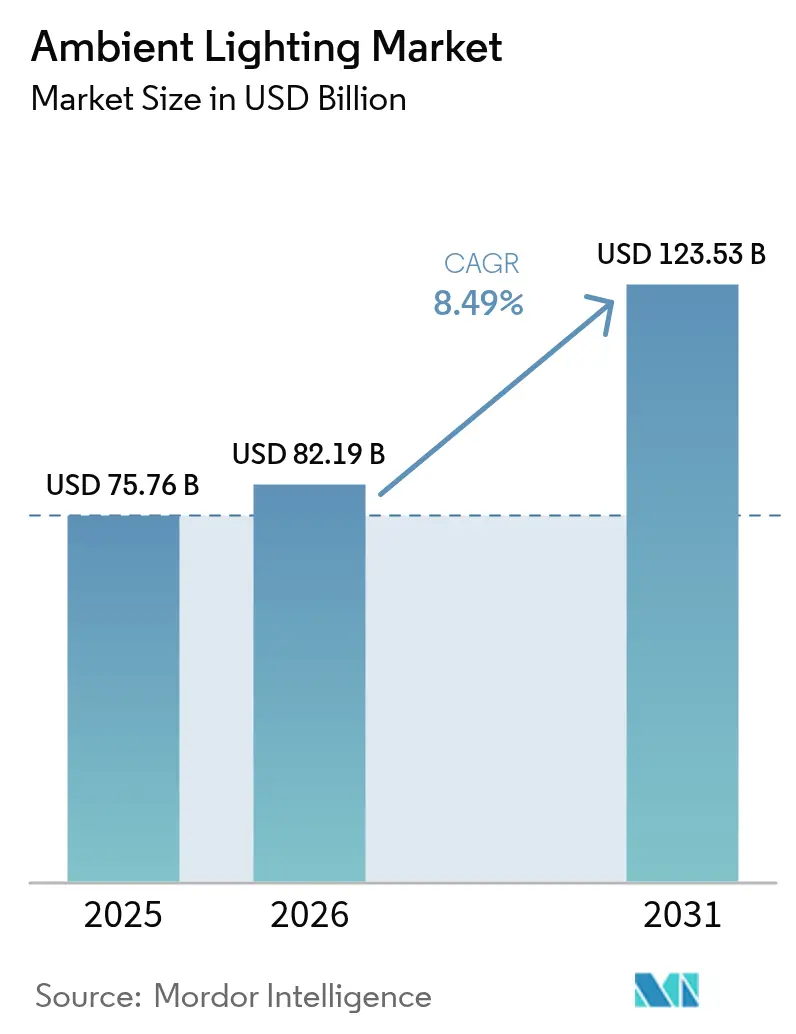

The ambient lighting market size is expected to grow from USD 75.76 billion in 2025 to USD 82.19 billion in 2026 and is forecast to reach USD 123.53 billion by 2031 at 8.49% CAGR over 2026-2031. Growth is anchored in global efficiency mandates, rapid LED penetration, and the widening appeal of connected systems that link lighting with broader smart-building platforms. LED-based products already account for 90% of total lighting sales, reshaping value chains toward software, sensors, and services. Asia Pacific owns nearly one-half of worldwide revenue and continues to expand at double-digit speed on the back of urbanization programs and state-funded smart-city rollouts. Product mix is shifting: lamps and luminaires still dominate, yet controls are now the strategic growth engine as end users seek energy savings, data, and human-centric functions that raise productivity.

Key Report Takeaways

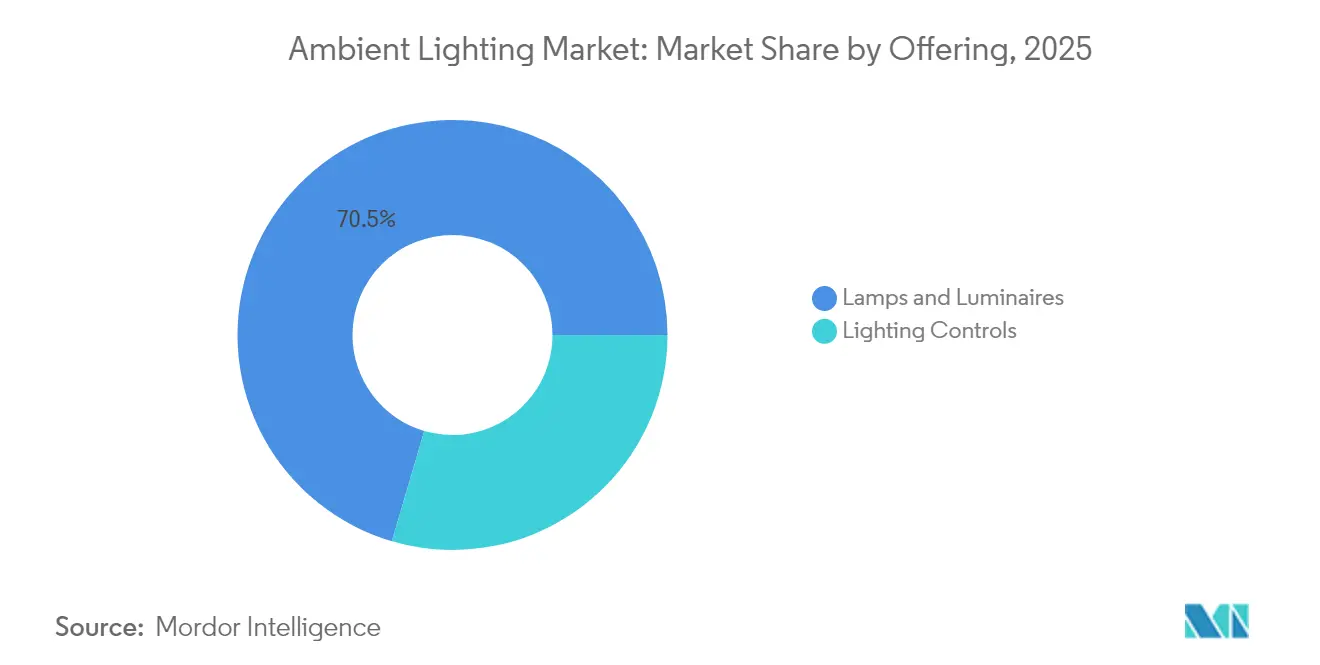

- By product category, lamps & luminaires led with 70.45% revenue share in 2025; lighting controls are projected to expand at a 9.02% CAGR to 2031.

- By installation phase, retrofit and renovation commanded 62.35% of the ambient lighting market share in 2025, while new-construction projects are set to grow at 8.74% CAGR through 2031.

- By type, surface-mounted fixtures held 27.55% revenue in 2025; strip lights are forecast to grow fastest at 11.04% CAGR.

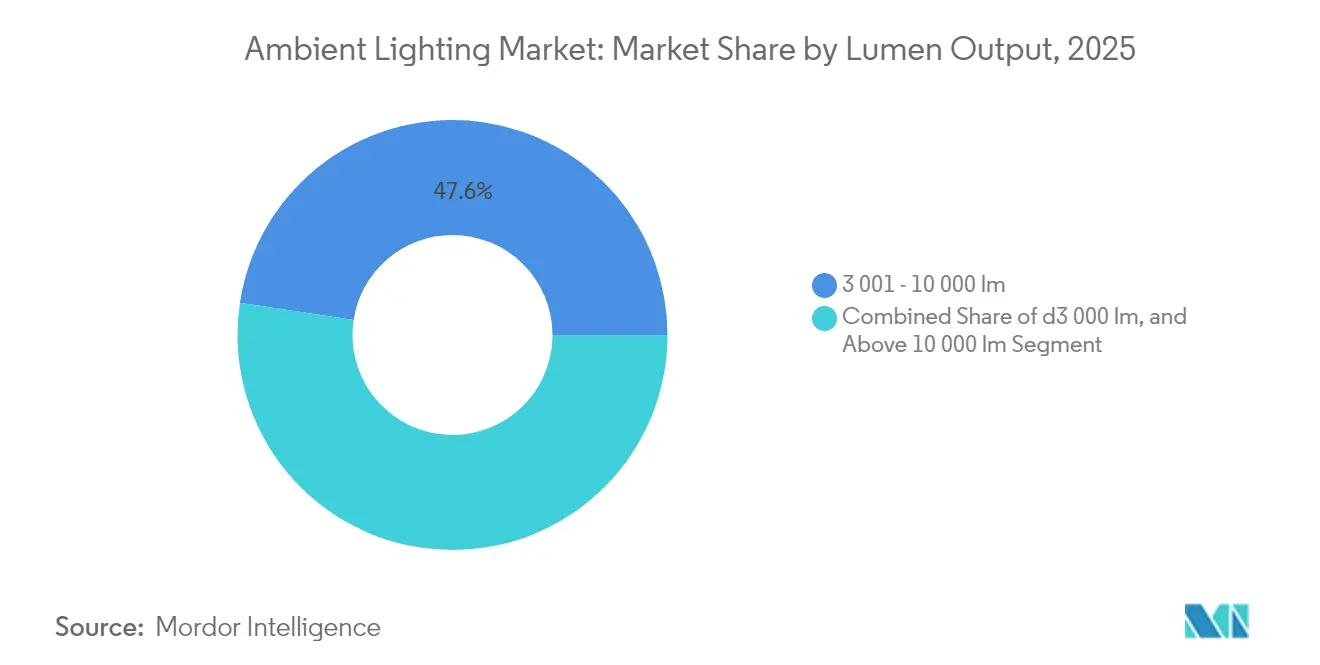

- By lumen output, the 3,001-10,000 lm commercial range accounted for 47.60% of the ambient lighting market size in 2025; the >10,000 lm class will post a 9.98% CAGR between 2026-2031.

- By connectivity, wired systems retained 71.30% of 2025 revenue; wireless platforms will record a 12.90% CAGR through 2031.

- By end user, residential applications captured 33.55% of 2025 revenue; automotive interiors will rise at 10.74% CAGR to 2031.

- By geography, Asia Pacific held 45.65% revenue in 2025 and will expand at 12.35% CAGR, the fastest globally.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ambient Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LED Retrofit Mandates Accelerating Commercial Up-grades in EU and Australia | +1.8% | Europe, Australia | Medium term (2-4 years) |

| Smart-city Investments Driving Connected Street-light Retrofits in Asia | +1.5% | Asia Pacific, with spillover to MEA | Medium term (2-4 years) |

| OEM-Triggered Ambient Packages in Mid-segment Autos (Asia and Europe) | +1.3% | Asia Pacific, Europe | Long term (≥ 4 years) |

| WELL and LEED v4 Standards Pushing Human-Centric Lighting in United States Offices | +1.2% | North America, with adoption in Europe | Long term (≥ 4 years) |

| Hospitality Re-brand Cycles Increasing Aesthetic Ambient Budgets (Gulf Cooperation Council Countries) | +0.9% | Middle East, with expansion to global hospitality chains | Medium term (2-4 years) |

| Rapid e-commerce Warehouse Build-outs Needing Low-glare Luminaires | +0.8% | Global, with concentration in North America and Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

LED retrofit mandates accelerating commercial upgrades in EU and Australia

Stringent policy frameworks such as the European Union Ecodesign Directive and Australia’s National Construction Code are forcing the phase-out of legacy lamps. Compliance rather than payback is now the tipping point, pushing building owners to adopt LED fixtures that satisfy minimum efficacy thresholds. The commercial segment alone is projected to jump from USD 17.07 billion in 2024 to USD 27.38 billion by 2030 as mandated upgrades converge with rising demand for connected controls. Suppliers are responding with quick-fit lamps, driverless tubes, and field-programmed retrofit kits that minimize downtime and labor costs.[1]Eric Rondolat, “Annual Report 2024,” Signify, signify.com

Smart-city investments driving connected street-light retrofits in Asia

National smart-city missions across China, India, and Japan place adaptive street lighting at the core of digital infrastructure. Municipalities are replacing conventional high-pressure sodium fixtures with networked LEDs that can host 5G small cells, air-quality sensors, and traffic cameras. Wireless protocols such as Zigbee and BLE Mesh offer scalability without trenching new cables, a decisive factor in dense urban cores. Hardware specialists that deliver open-API nodes are well-positioned as cities bundle lighting with broader IoT services.[2]LTECH Corporate News, “Li Fangfang of LTECH: Integration Trends in 2025,” LTECH, ltech.cn

OEM-triggered ambient packages in mid-segment autos

Automakers once reserved multi-color cabin light for luxury models; today, BMW, Toyota, and Hyundai supply customizable ambiance in mainstream vehicles. Interior LEDs now sync with drive modes, infotainment cues, and advanced driver-assistance warnings, enhancing both safety and brand appeal. Tier-1 suppliers are racing to miniaturize optics and add digital controls that withstand automotive temperature and vibration cycles while meeting new warranty requirements.[3]ams-OSRAM Product Group, “Automotive & Mobility – Ambient Lighting,” ams-osram.com

WELL and LEED v4 standards pushing human-centric lighting in US offices

Corporate real-estate teams pursue WELL and LEED credits that reward circadian-friendly lighting. Tunable-white luminaires that follow natural daylight cycles have shown 6% gains in worker productivity and 15% gains in creative output. Demand is spilling into the renovation wave of older office towers where occupant wellness now ranks alongside energy metrics in capital-planning decisions.[4]Alcon Lighting Editorial Team, “2025 Commercial Lighting Design Trends Move Beyond Basics,” Alcon Lighting, alconlighting.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Inrush-Current Failures in Large-scale LED Strip Deployments | -1.1% | Global, particularly in commercial and industrial applications | Short term (≤ 2 years) |

| Fragmented Wireless Protocols Elevating Control-System Integration Cost | -0.9% | Global, with higher impact in retrofit applications | Medium term (2-4 years) |

| Post-COVID Office Downsizing Reducing Retrofit Pipelines (NA and EU) | -0.7% | North America, Europe | Short term (≤ 2 years) |

| Tight Rare-earth Supply Chain Inflating Phosphor and Driver Prices | -0.6% | Global, with higher impact on cost-sensitive segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High inrush-current failures in large-scale LED strip deployments

Multi-string strip systems can draw damaging current spikes when thousands of drivers power up simultaneously, triggering breaker trips and warranty claims. Soft-start power supplies and sequential controllers mitigate risk but add cost. Reliability concerns may delay rollouts in logistics hubs where linear lighting often spans hundreds of meters.

Fragmented wireless protocols elevating control-system integration cost

Zigbee, BLE Mesh, Thread, and proprietary stacks each excel in specific use cases yet seldom interoperate. In retrofit projects the wrong choice can lock owners into vendor ecosystems or require costly gateways. Standards bodies are converging on DALI+ and Bluetooth LE specifications, but until true plug-and-play emerges, integrators must budget extra engineering hours.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Controls Drive Intelligence Revolution

Lamps and luminaires remain the revenue cornerstone, holding 70.45% in 2025 thanks to the mass conversion from fluorescent and halogen to LED. ENERGY STAR-rated fixtures consume 90% less power than incandescent alternatives and last 15 times longer, slashing maintenance budgets and carbon footprints. Replacement activity across offices, homes, and warehouses keeps demand stable even as unit prices fall.

Lighting controls are the market’s accelerant, forecast to grow 9.02% annually. Open DALI gateways, Bluetooth LE networks, and cloud dashboards embed data insights that extend beyond energy management. Signify reports that connected systems and services delivered 30% of company sales in 2024, confirming rising customer appetite for software-centric propositions. The ambient lighting market size for connected controls is set to widen as building codes mandate occupancy sensing and daylight harvesting.

By Installation Phase: Retrofit Dominance Drives Market

Retrofit and renovation projects generated 62.35% of 2025 revenue as owners upgraded vast stocks of outdated fixtures. The United States residential remodeling market surpassed USD 600 billion in 2022, with 34% of spend flowing into energy-related upgrades that include lighting. City carbon caps such as New York Local Law 97 amplify urgency, imposing fines starting in 2025 for inefficiency breaches. Guidance from the U.S. General Services Administration lists LED tubes, retrofit kits, or full luminaire swaps as approved pathways, fueling a deep replacement funnel.

New construction accounts for a smaller base but will outpace retrofits at 8.74% CAGR. Architects now program lighting early in design workflows to capture WELL and LEED credits, integrate sensors, and streamline commissioning. Smart commercial campuses specify network-ready fixtures as baseline, propelling ambient lighting market penetration in mixed-use towers, data centers, and healthcare facilities. Ambient lighting market size gains in new builds are also supported by economies of scale that allow bundled hardware-plus-software contracts.

By Type: Strip Lighting Leads Innovation Wave

Surface-mounted fixtures retained a 27.55% share in 2025, prized for straightforward installation across offices, classrooms, and corridors. Suspended linear bars and recessed cans complement the category, giving designers options for glare control and visual comfort.

LED strip lighting, however, will grow fastest at 11.04% CAGR as architects specify continuous “lines of light” that merge task and accent roles. Retail shelf illumination, cove accents in hotels, and under-cabinet task zones in kitchens exemplify its flexibility. Yet high inrush-current failures loom large. Vendors that deliver soft-start drivers and robust PCB thermal paths can capture outsized gains in this segment of the ambient lighting market.

By Lumen Output: Commercial Range Dominates Applications

The 3,001-10,000 lm class captured 47.60% revenue in 2025 because most offices, supermarkets, and learning facilities operate within this brightness band. Human-centric lighting pilots in open-plan spaces show tangible productivity lifts, encouraging corporate rollouts. Daylight sensors and occupancy analytics can trim lighting energy 25-80% while preserving comfort.

High-lumen (>10,000 lm) fixtures will register the quickest expansion at 9.98% CAGR as e-commerce warehouses, distribution centers, and smart-city highways demand glare-free but powerful illumination. Signify’s 2024 launch of UltraEfficient street luminaires underscores innovation aimed at halving energy draw versus earlier LED designs. Residential demand (≤3,000 lm) remains steady, spurred by voice-controlled smart bulbs and mood-tunable downlights.

By Connectivity: Wireless Revolution Accelerates

Wired networks such as DALI and KNX still dominate with 71.30% revenue in 2025 because of their robust reliability in mission-critical sites. DALI-2 and D4i drivers now expose energy reporting that facilities managers feed into building dashboards for carbon tracking.

Wireless links are the growth story, predicted to post a 12.90% CAGR. Bluetooth Mesh allows many-to-many messaging, making it fit for multi-tenant apartments and factory floors. Research in Sensors confirms its scalability when designers mitigate interference with channel planning. Wireless also triumphs in retrofits where tearing walls for new control cables is untenable. The ambient lighting market stands to benefit from hybrid architectures that blend wired backbones with wireless edge nodes, giving owners future-proof flexibility.

By End User: Automotive Applications Accelerate

Automotive interiors form the fastest-growing end-user niche at 10.74% CAGR. Cabin LEDs now pulse with driver-assist alerts, swing to warm tones for relaxation, and echo infotainment beats, turning light into a signature branding surface. Tier-1s supply thin lightguides and RGB controllers that withstand automotive temperature extremes. Signify’s 2025 debut of an EV lightstrip for Xiaomi illustrates how traditional lighting majors are carving footholds in mobility.

Residential spaces stay the largest slice at 33.55% thanks to smart-home adoption and wellness awareness. Tunable-white bulbs that align with circadian rhythms and voice-activated scenes elevate consumer demand. Hospitality chains in the Gulf Cooperation Council funnel renovation budgets into immersive ambience that shapes guest perception. Retail outlets deploy directional accent lights that lift merchandise appeal and increase dwell times. Across every vertical, the ambient lighting market pivots from pure illumination toward experiential value.

Geography Analysis

Asia Pacific controls 45.65% of 2025 revenue and will grow at 12.35% CAGR through 2031, driven by state subsidies for efficient lighting, sprawling residential construction, and global leadership in LED component production. China spearheads both manufacturing prowess and giant smart-city pilots that anchor connected street-light demand. India’s 100-city mission and Japan’s Society 5.0 vision reinforce the regional pipeline for controls, sensors, and platform integration.

North America is a mature but innovation-led arena. Signify’s 2024 data show that the United States contributed USD 2.20 billion, roughly one-third of its global sales. Residential remodels remain strong, yet office downsizing after COVID slows some retrofit schedules. WELL and LEED adoption maintains momentum for human-centric upgrades that justify premium fixtures and advanced controls.

Europe occupies a design-centric and regulation-heavy position. The Ecodesign Directive obliges LED transitions across commercial estates, and the region champions high color-rendering products that align with its emphasis on visual comfort. Automakers in Germany and France extend ambient packages downrange, spurring component suppliers to deliver cost-optimized RGB modules.

South America and the Middle East & Africa together contribute a smaller share but post healthy growth. GCC hospitality refurbishments prioritize dramatic ambience, while African infrastructure programs channel public funds into efficient street lighting that doubles as a smart-city gateway. The ambient lighting market gains long-term upside as governments apply green-building codes and attract foreign direct investment.

Regulatory Landscape

Global ambient lighting demand continues to be shaped by energy-efficiency rules and safety standards that affect lamps, luminaires, and separate control gear. In the United States, the Department of Energy amended energy conservation standards for general service lamps in April 2024, with compliance required on or after July 25, 2028. This reinforces the market shift toward higher-efficacy LED solutions and compliant drivers and controls.

On product safety and conformity, IEC 60598-1:2024 (Edition 10.0) updated general safety requirements for luminaires, including photobiological safety marking. ANSI/UL 1598 (5th Edition) was revised in January 2024 to harmonize luminaire requirements across the United States, Canada, and Mexico for non-hazardous locations. In February 2026, DOE issued a final determination to keep existing energy conservation standards for metal halide lamp fixtures under 10 CFR 431.326 unchanged, maintaining compliance continuity for high-bay and industrial fixture categories while manufacturers continue R&D on controls, connected systems, and higher-efficacy LED platforms aligned with EU Ecodesign and labeling frameworks.

Value Chain Analysis

The ambient lighting value chain spans LED chips and packages, optics and thermal materials, drivers and power electronics, sensors and controllers, luminaire assembly, software and platform integration, and channel distribution through electrical wholesalers, lighting agents, and project-based contractors. With LED-based products representing the majority of lighting sales, differentiation is increasingly shifting downstream to connected controls, commissioning tools, and software services that link lighting with broader smart-building platforms.

Component standardization and protocol-driven designs are also changing sourcing and lifecycle economics. In professional lighting, Zhaga Consortium specifications support modular, field-replaceable designs, and Zhaga Book 26 (March 2025) introduced a standardized electro-mechanical interface for linear socketable LED modules. This enables plug-and-play maintenance in commercial luminaires. In automotive interiors, the ecosystem increasingly depends on smart LED-driver silicon and network protocols (for example, LIN-based controllers such as Melexis MLX81124 and interior driver platforms such as Infineon LITIX Interior), alongside digital module approaches such as Microchip-supported ISELED, which enables daisy-chained RGB nodes and richer cabin effects while pulling more value toward electronics, firmware, and OEM-grade validation.

Competitive Landscape

Global majors such as Signify, ams-OSRAM, and Acuity Brands face margin compression in hardware but unlock new recurring revenue in software and services. Signify booked USD 6.45 billion in 2024 sales yet posted a -38.9% total shareholder return, highlighting transition strain. Still, R&D spend at 4.34% of revenue underscores commitment to generative-AI tooling for customer support and product development..

Regional specialists leverage proximity advantages. Asian manufacturers supply OEM white-label luminaires at scale and speed, while European firms carve premium niches in architectural and human-centric portfolios. M&A remains active: Acuity Brands acquired Arize horticulture lines to pursue controlled-environment agriculture, signalling cross-vertical convergence..

White-space competition now centers on system integration that links lighting with HVAC, occupancy analytics, and security layers. Vendors able to package hardware, cloud software, and managed services secure sticky contracts. The ambient lighting market thus rewards ecosystem breadth over component price alone, realigning success metrics around data insights and user experience.

Ambient Lighting Industry Leaders

Acuity Brands Inc.

OSRAM Licht AG

Koninklijke Philips NV

Samsung Electronics Co. Ltd

Eaton Corporation Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Controls-led retrofits remain a key whitespace because retrofit and renovation account for 62.35% of 2025 ambient lighting revenue, and many building owners still operate mixed fleets where energy savings depend on sensors, daylight harvesting, and standardized commissioning, not luminaire swaps alone. Interoperability and modularity also create a clearer upgrade path for large estates, supported by Zhaga Book 26 (March 2025). It supports socketable linear LED modules that simplify service and mid-life upgrades in professional installations, where maintainability and future-proofing are increasingly part of specifications.

Cross-ecosystem integration is creating additional pockets of demand in residential and consumer-adjacent ambient lighting, where unified control across brands reduces deployment friction. A concrete signal is the June 2024 Samsung Electronics collaboration with Signify to integrate LED ambient lighting into the Samsung SmartThings ecosystem, reinforcing the shift from standalone lighting products to platform-attached ambient experiences. In automotive, OEM ambient packages continue moving into mainstream vehicles, and supplier roadmaps increasingly align with software-defined vehicle architectures, lifting the opportunity for intelligent RGB modules, robust drivers, and validated in-cabin UX functions that connect ambient light with HMI cues and safety signaling.

Recent Industry Developments

- May 2026: ams OSRAM integrated its OSIRE E3731i intelligent RGB LED into the NIO ES9 SUV, featuring a multi-layer wraparound interior ambient lighting implementation. The deployment highlights rising OEM demand for higher-density, design-forward cabin lighting and reinforces the role of intelligent LED nodes in automotive interior differentiation.

- June 2025: Signify expanded Philips Hue with an immersive entertainment push and a new AI assistant, extending how consumers create ambient scenes tied to content and routines. This deepens ecosystem stickiness around connected controls and software, supporting higher attach rates for Hue-compatible ambient lighting products.

- May 2024: Samsung Electronics announced a strategic collaboration with Signify to integrate LED ambient lighting solutions into the Samsung SmartThings ecosystem. This integration targets multi-brand smart-home control under a single platform, reducing setup complexity and supporting broader adoption of connected ambient lighting across residential environments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the ambient lighting market covers revenue earned from lamps, luminaires, and lighting-control systems that deliver general, diffuse illumination as the base layer of light in a space. We treat demand across new installations and retrofit upgrades, and the market is captured in USD terms.

Scope exclusions: Specialized stage and show lighting, horticultural grow lights, and similar niche lighting built for narrow-use performance are not counted.

Segmentation Overview

- By Offering

- Lamps and Luminaires

- Incandescent Lamps

- Halogen Lamps

- Fluorescent Lamps

- Light-Emitting Diode (LED)

- Lighting Controls

- Lamps and Luminaires

- By Installation Phase

- New Construction

- Retrofit and Renovation

- By Type

- Surface-mounted Light

- Track Light

- Strip Light

- Suspended Light

- Recessed Light

- By Lumen Output

- Sub 3 000 lm (Residential)

- 3 001 - 10 000 lm (Commercial)

- Above10 000 lm (Industrial and Outdoor)

- By Connectivity

- Wired (DALI, KNX)

- Wireless (Zigbee, BLE Mesh, Thread)

- By End User

- Residential

- Automotive

- Hospitality and Retail

- Healthcare

- Industrial and Logistics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- South East Asia

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the starting structure for the model and to set realistic guardrails for demand, pricing, and adoption. We review public energy and buildings information such as U.S. DOE lighting and efficiency resources, IEA energy indicators, and national statistics offices that report construction activity and housing completions. References to standards and policy, including IES guidance and efficiency regulations published by regulators, are also used to identify when retrofits tend to accelerate.

On the supply side, we use sources such as company annual reports, investor presentations, earnings call transcripts, and press releases to map product focus, geographic exposure, and pricing direction. Import and export statistics, along with shipment-level trade databases, are used selectively to sanity check cross-border fixture flows where domestic production data is limited. These sources are not exhaustive, and other public references were also used during data collection, validation, and clarification steps.

Primary Interviews and Surveys

Primary work is used to pressure-test key assumptions that desk sources cannot consistently explain, especially around average selling price movement and retrofit timing. We speak with manufacturers, distributors, lighting designers, contractors, and large buyers, and we ensure the discussion covers residential and commercial demand patterns across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 15% | APAC: 48% |

| Mid tier: 53% | Functional/Unit leaders: 34% | EMEA: 30% |

| Smaller Players: 17% | Managers: 51% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable demand pool from construction and renovation activity, and then ties it to lighting intensity per building type and the share of projects specifying ambient fixtures. Results are checked using selective bottom-up approximations, such as sampled fixture ASP multiplied by shipment or install volumes discussed in channel conversations. This step helps adjust totals when a region shows pricing or mix shifts.

Practical inputs used in the model include new floor space additions, renovation and retrofit rates, LED penetration within general lighting, average fixture and control-system pricing, and commercial electricity-cost sensitivity that drives efficiency upgrades. Where primary inputs are not available for a niche end use, we use proxy ratios from similar building types, and then re-test those ratios with expert feedback. For forecasting, scenario analysis is applied around construction cycles and retrofit policies, and the final path is selected using consensus ranges from interviews so the outlook remains consistent year by year.

Data Validation & Update Cycle

Validation is done by comparing outputs against independent signals such as regional construction indicators, trade flows for lighting products, and stated growth direction from supply chain participants. Any large variance is investigated by rechecking the input chain, and then revisiting the assumption with at least one additional expert call when needed. Before sign-off, the model is reviewed in multiple steps so calculation logic, currency handling, and growth drivers stay consistent.

Reports are refreshed annually, and interim updates are added when major policy changes, sharp demand shifts, or notable technology transitions occur. Before delivery, a final pass is completed to ensure the latest public updates and interview learnings are reflected in the published numbers.

Mordor Intelligence's Ambient Lighting Market Estimate Compared With Other Published Estimates

Published market sizes for ambient lighting can look far apart even when studies cover similar products, because the scope and timing choices differ across publications. Differences usually come from what each study treats as ambient lighting versus adjacent categories, the year used as the starting point, and how pricing is carried forward during the forecast.

Some estimates fold in a wider lighting set, or they extend the definition to decorative and specialty applications that are purchased for effect more than base illumination. In Mordor Intelligence, ambient lighting is counted as lamps, luminaires, and lighting controls used for diffuse, general illumination, and specialized stage and horticultural lighting is left out. This narrower definition keeps the model tied to everyday building and interior usage.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 82.19 B (2026) | |

| Global Consultancy A | USD 81.15 B (2025) | Uses a different base year and a broader segmentation set that can capture a wider mix of ambient-adjacent lighting categories, so the starting value is not directly comparable to a 2026-only definition. |

| Industry Publisher B | USD 77.44 B (2024) | Back-casts to an earlier base year and provides limited clarity on inclusions and exclusions, which can change what gets counted as ambient lighting and how price and mix are carried into later years. |

The comparison shows that the spread is mainly explained by base-year choice and what each study groups under ambient lighting. By keeping scope rules explicit, and by linking demand to construction, renovation, and control adoption indicators that can be checked, our estimate stays traceable and repeatable for planning.

Key Questions Answered in the Report

What is the current size of the ambient lighting market?

The ambient lighting market stands at USD 82.19 billion in 2026 and is projected to hit USD 123.53 billion by 2031.

Which region contributes the largest revenue?

Asia Pacific leads with 45.65% of global revenue and is also the fastest-growing region at a 12.35% CAGR through 2031.

Why are lighting controls growing faster than fixtures?

Controls deliver energy savings, data analytics, and human-centric benefits that drive stronger value propositions, leading to a 9.02% CAGR versus slower fixture growth.

How will wireless protocols shape future installations?

Wireless platforms such as Bluetooth Mesh enable scalable retrofits without new cabling, supporting a 12.90% CAGR in wireless connectivity revenue.

What drives the surge in automotive ambient lighting?

OEMs install customizable RGB systems to enhance safety cues and brand identity, pushing automotive applications to an 10.74% CAGR.

How do WELL and LEED standards influence office lighting upgrades?

Both certifications reward circadian-aligned lighting, prompting companies to adopt tunable-white LEDs that have shown 6% productivity gains and 15% lifts in creative output.

Page last updated on: