Automotive Aluminum Parts High-Pressure Die Casting (HPDC) Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 22.24 Billion |

| Market Size (2031) | USD 28.80 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Aluminum Parts High-Pressure Die Casting (HPDC) Market Analysis by Mordor Intelligence

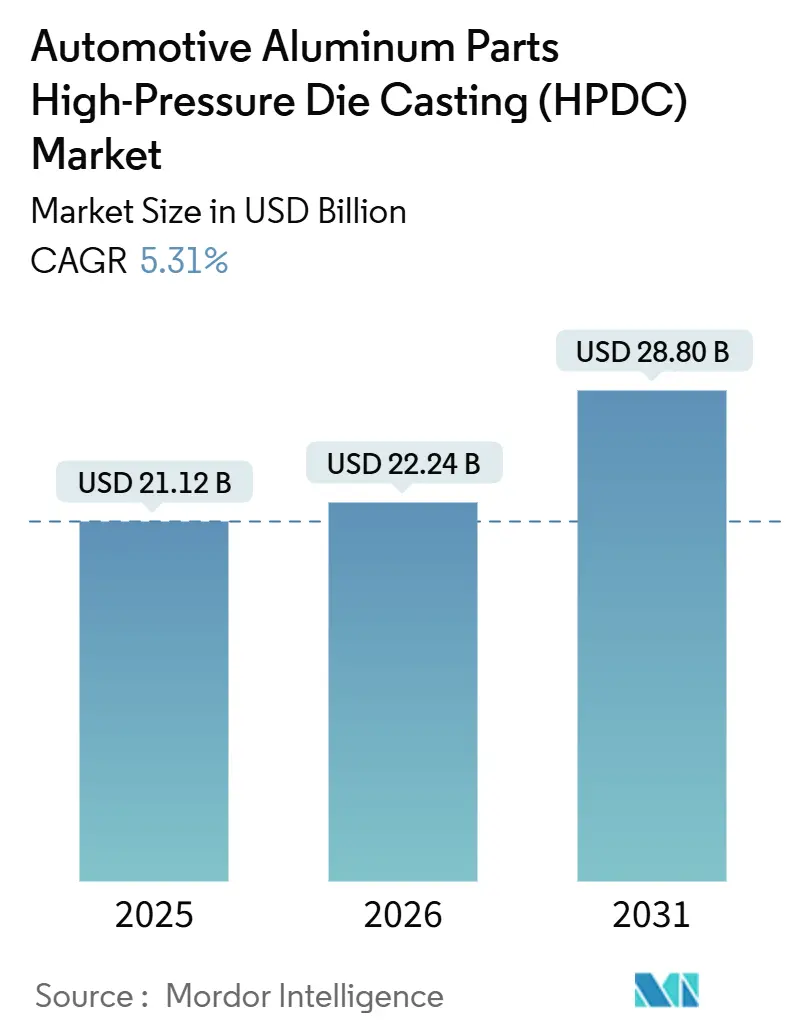

The Automotive aluminum parts High-Pressure Die Casting (HPDC) market size is expected to increase from USD 21.12 billion in 2025 to USD 22.24 billion in 2026 and reach USD 28.80 billion by 2031, progressing at a 5.31% CAGR. This outlook reflects tightening global fuel-economy rules, a surge in electric-vehicle (EV) production, and the rapid spread of gigacasting presses that convert dozens of welded steel stampings into single aluminum components. OEMs see immediate cost and weight advantages, while the availability of recycled metal eases supply-chain risk and improves sustainability metrics. Material substitution also aligns with national industrial-policy goals that encourage local smelting and near-shoring of lightweight components. These converging forces keep the Automotive aluminum parts High-Pressure Die Casting (HPDC) market on a multi-year growth trajectory even as legacy power-train demand plateaus.

Key Report Takeaways

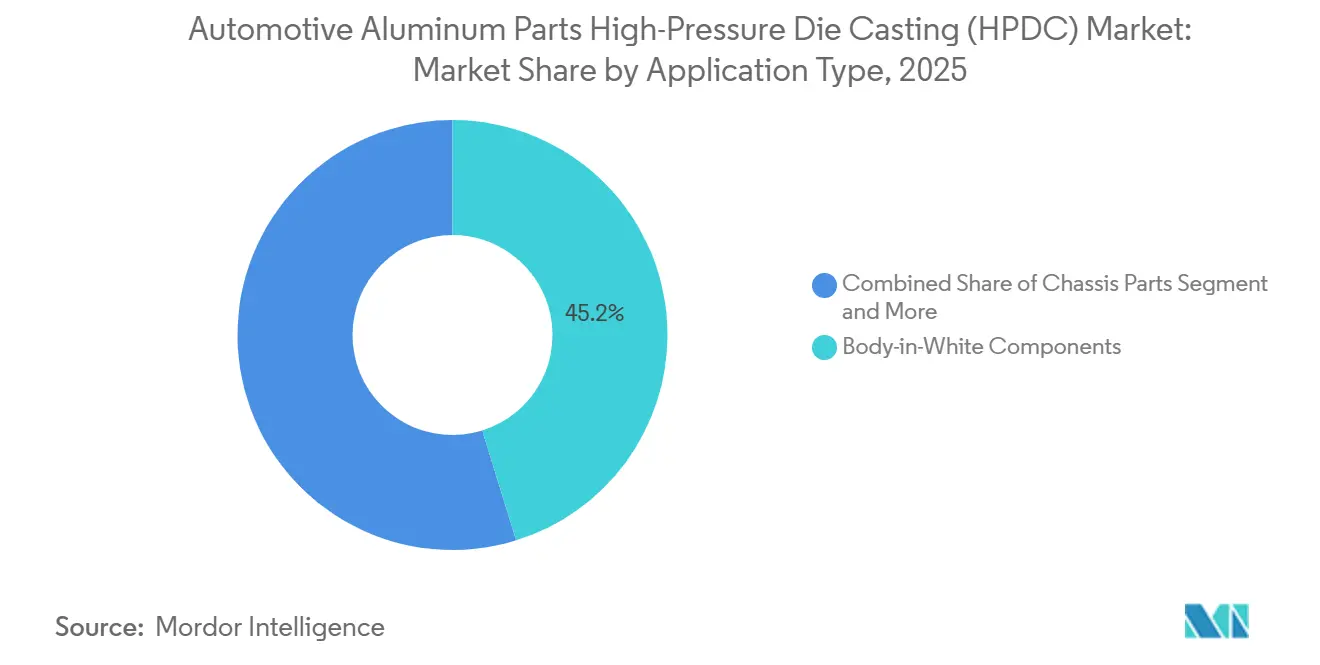

- By application type, body-in-white components captured 45.18% of the Automotive aluminum parts HPDC market share in 2025, and will post the fastest 6.12% CAGR through 2031.

- By vehicle type, passenger cars accounted for 75.03% of revenue share in 2025; light commercial vehicles are projected to grow at a 7.62% CAGR through 2031.

- By manufacturing process, die casting accounted for 78.13% of the Automotive aluminum parts HPDC market size in 2025, and is poised for a 6.54% CAGR through 2031.

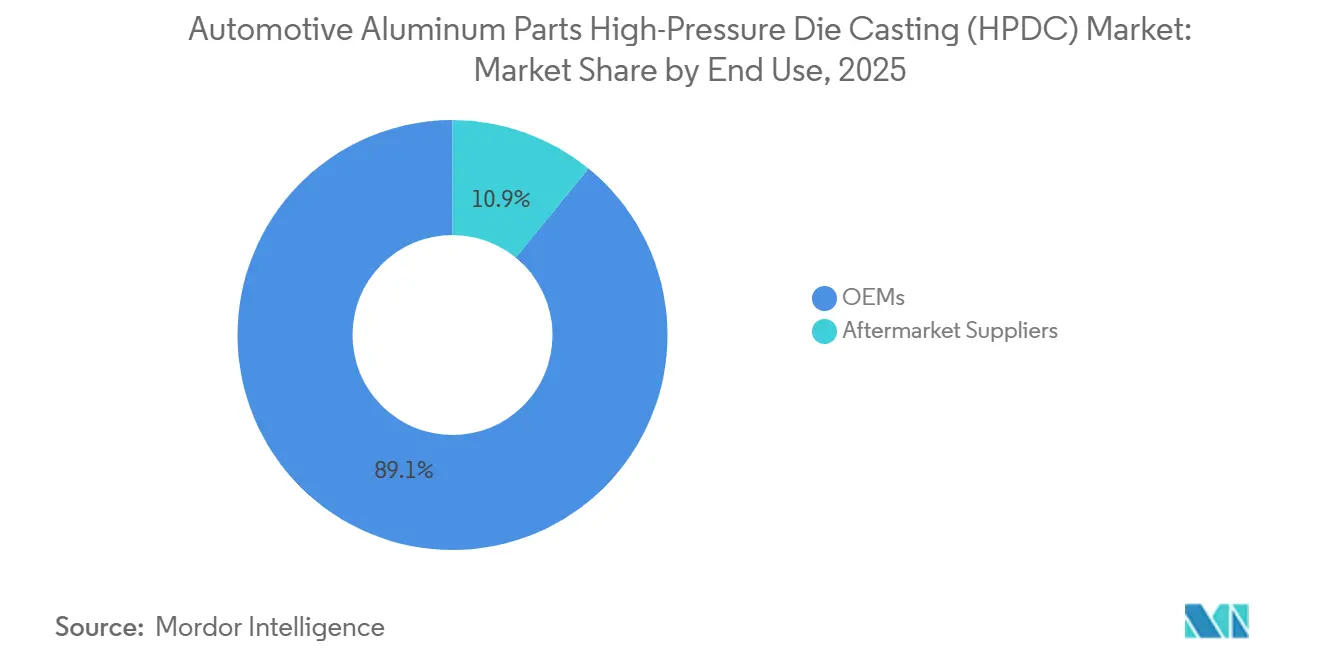

- By end use, OEM channels accounted for 89.12% of 2025 sales and will continue to expand at a 5.95% CAGR through 2031.

- By casting material, primary alloys accounted for 65.25% in 2025, but recycled alloys will accelerate at an 8.13% CAGR to 2031.

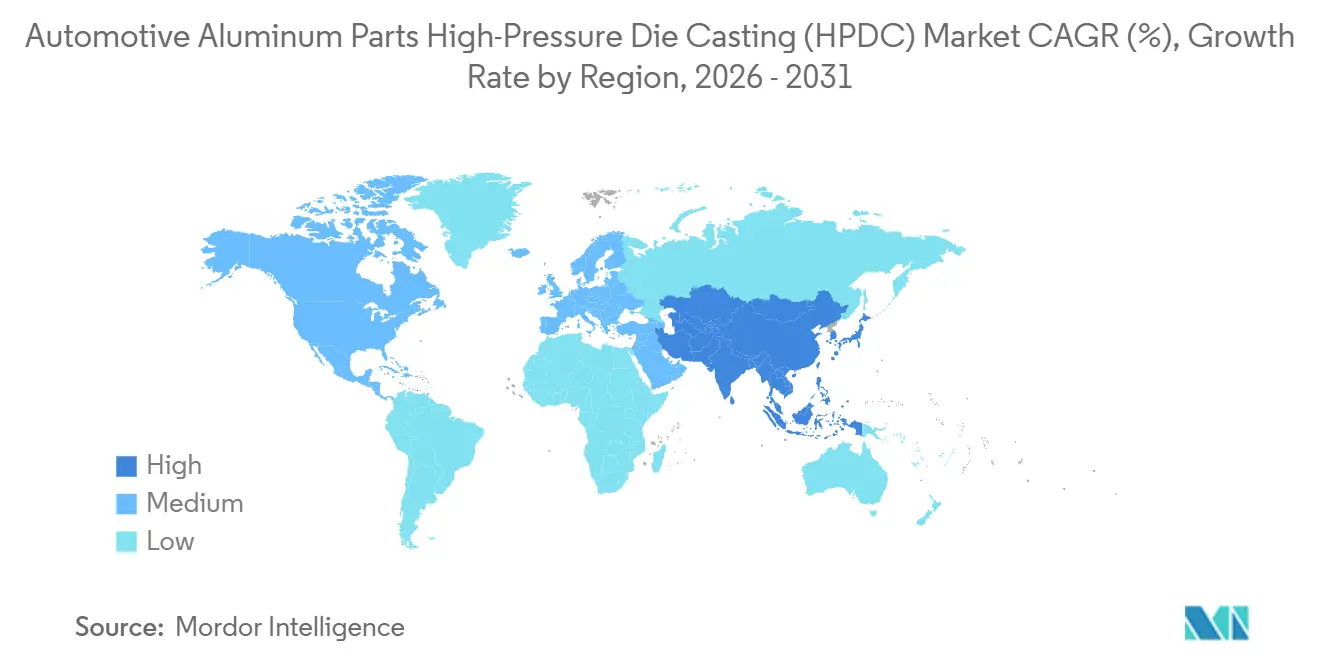

- By geography, Asia-Pacific led with a 57.04% share in 2025 and is forecast to post the strongest CAGR of 7.02% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Aluminum Parts High-Pressure Die Casting (HPDC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting and Emission Mandates | +1.8% | Global, early gains in the EU, China, and North America | Medium term (2–4 years) |

| EV Battery-Housing Demand | +1.5% | Global, spill-over from China to North America and the EU | Short term (≤ 2 years) |

| Gigacasting Enable Large Castings | +1.2% | Asia-Pacific core, spill-over to North America | Medium term (2–4 years) |

| Circular-Economy Push For Recycled Aluminum | +0.8% | EU and North America are primary, expanding to the Asia-Pacific | Long term (≥ 4 years) |

| Vacuum-Assisted HPDC | +0.7% | Global, early adoption in Germany, Japan | Medium term (2–4 years) |

| Rheo-HPDC Opens Opportunities | +0.5% | Asia-Pacific core, spill-over to North America and the EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OEM Lightweighting and Emission Mandates

Corporate Average Fuel Economy rules targeting 50.4 mpg in the United States by 2031 and the European Union’s EUR 95 (~USD 109) per gram CO₂/km fleet ceiling penalize excess emissions, forcing automakers to substitute steel for aluminum, which reduces mass per part by a significant amount [1]“Corporate Average Fuel Economy Standards,” U.S. Department of Transportation, nhtsa.gov. General Motors plans to lift average aluminum content, underscoring a long-term strategic shift. High-pressure die casting (HPDC) enables complex geometries, allowing battery trays and cross-members to emerge as single pieces that eliminate upwards of 60 welds. OEM purchasing executives accept aluminum’s material premium because weight savings avoid carbon fines and enable smaller traction-battery packs. As regulations tighten globally, the Automotive aluminum parts HPDC market gains recurring pull-through from every new vehicle platform.

EV Battery-Housing and E-Drive Demand Surge

EV sales exceeded 20 million units in 2025 and are tracking toward significant growth by 2031, intensifying the need for thermally conductive aluminum enclosures that shield cells and dissipate heat [2]“Global EV Outlook 2025,” International Energy Agency, iea.org. Tesla integrates 4680 cells directly into large structural castings, trimming vehicle mass while boosting torsional rigidity. Chinese leaders such as BYD replicate the concept, specifying 0.1 mm machining tolerances to secure cell-to-pack flatness. E-drive stator housings rely on silicon-rich A380 variants that deliver higher thermal conductivity, illustrating how alloy development and casting innovation advance in lockstep. Each of these developments widens the addressable market for HPDC Automotive aluminum parts.

Gigacasting Presses Enable Large Structural Castings

High-tonnage presses above 6,000 tons allow rear-underbody or side-frame modules to emerge in a single shot, eliminating significant stampings per vehicle while achieving notable tensile strength. Tesla’s 8,000-ton lines in Fremont cut unit cost compared with welded sub-assemblies, proving gigacasting’s economic case [3]“Battery Day Presentation,” Tesla, tesla.com. Asian suppliers such as Guangdong Hongtu deploy identical technology to serve domestic OEMs, leveraging labor-light automation that secures cost edges versus traditional lines. Vacuum-assisted injection further slashes porosity, unlocking structural applications once restricted to wrought grades. This manufacturing leap fuels steady share gains for the Automotive aluminum parts HPDC market.

Circular-Economy Push for Recycled Aluminum

The European Commission has proposed mandatory recycled aluminum content targets for vehicles. BMW intends to exceed the rule, aiming for 50% recycled content across structural castings. Recycling saves significant energy embedded in primary metal, equating to notable tons of CO₂ per ton avoided, a metric that appeals to OEM ESG scorecards. New spectroscopic sorting equipment lowers iron contamination, elevating secondary alloy mechanical integrity and pushing recycled metal into body-in-white roles. Sustained policy momentum ensures that recycled feedstock becomes a durable pillar of the Automotive aluminum parts HPDC industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminum and Energy Price Volatility | −0.9% | Global, acute in energy-intensive regions | Short term (≤ 2 years) |

| High-Strength Steel Alternatives | −0.6% | North America and the EU are primary, expanding globally | Medium term (2–4 years) |

| Giga-Cast Crash-Repair Complexity | −0.4% | Global, early impact in Tesla-dense markets | Medium term (2–4 years) |

| Corrosion Risks in Recycled Alloys | −0.3% | EU and North America are primary, expanding to the Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aluminum and Energy Price Volatility

LME cash prices fluctuated during 2025, compressing margins on six-month fixed-price supply contracts. Energy accounts for a significant share of primary aluminum costs, so the spike in European natural gas prices after geopolitical disruptions squeezed smelters, trimming regional supply. Die casters add more electricity per kilogram than steel stampers, exposing them to tariff shocks that erase notable EBIT margins. Hedging mitigates only limited exposure since forward curves extend merely 18 months, compelling many tier-ones to incorporate price-escalation clauses. Such volatility tempers near-term growth expectations for the Automotive aluminum parts HPDC market.

Advanced High-Strength-Steel Structural Alternatives

Third-generation AHSS grades exceed 1,500 MPa tensile strength at cost parity with legacy steels, offering weight savings that nibble at aluminum’s advantage while matching crash-energy absorption. Automakers like Ford use hot-formed boron steel in A-pillars to maintain stiffness without the galvanic isolation treatments required for mixed-material joints [4]“Advanced High-Strength Steel Applications,” American Iron and Steel Institute, steel.org. A-class stamping presses are already in place at most plants, sparing OEMs from eight-figure investments in casting presses. Although aluminum still wins in range-sensitive EVs, AHSS competes effectively in budget segments, slowing total addressable expansion for the Automotive aluminum parts HPDC market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Type: Body-in-White Components Anchor Structural Integration

Body-in-white parts accounted for 45.18% of 2025 demand, the largest slice of the Automotive aluminum parts HPDC market. Gigacasting trims assembly lines from 171 weld-intensive steel parts to two monolithic structures, raising torsional rigidity and curtailing takt time. Over the forecast horizon, this segment will expand at a 6.12% CAGR, as Mercedes-Benz and Toyota join Tesla in announcing structural cast programs. Chassis modules capture a modest share, propelled by suspension arms and sub-frames that benefit from aluminum’s stiffness-to-mass ratio.

Single-speed gearboxes in light trucks and multi-speed boxes in commercial EVs sustain transmission-housing demand even as internal-combustion engines decline. Smaller structural items—engine mounts, cross-members, and heat shields—capture incremental gains given aluminum’s vibration-damping benefits in low-NVH luxury models. These dynamics collectively fortify the Automotive aluminum parts HPDC market over the mid-term.

By Vehicle Type: Passenger Cars Remain Dominant While Commercial Segments Accelerate

Passenger cars accounted for 75.03% of 2025 shipments, forming the cornerstone of the Automotive aluminum parts HPDC market. High production volumes and rapid model-year changeovers keep tooling utilization high, encouraging further casting automation. Meanwhile, light commercial vehicles notch the fastest 7.62% CAGR as e-commerce hubs demand urban-delivery vans outfitted with substantial aluminum battery armor.

Medium-duty and heavy-duty trucks weigh ROI for aluminum against payload limits; fleet managers accept a higher up-front cost if it unlocks an extra pallet of freight. Regional divergence persists: European haulers pursue aluminum to satisfy carbon taxes, whereas some Asian fleets still favor low-cost steel. Nonetheless, electrification mandates will gradually tilt procurement toward lightweight materials, enhancing the long-range prospects of the Automotive aluminum parts HPDC market.

By Manufacturing Process: Die Casting Commands, but Innovation Re-Shapes Share

Die casting generated 78.13% of 2025 revenue, underscoring its centrality to the Automotive aluminum parts HPDC market size. The segment is also set to maintain its growth momentum with a 6.54% CAGR through 2031. Ongoing upgrades—vacuum-assist, real-time X-ray, servo-hydraulic injection, elevate density, and reduce cycle time. Designers increasingly rely on topology optimization software that minimizes wall thickness without compromising crash standards.

Surface-treatment steps such as T6 heat-treatment or anodizing hold a nominal share, reflecting durability concerns in EV applications subject to wide thermal swings. Digital-thread adoption links design files to press parameters, cutting prototype loops from weeks to days. Although rheo-HPDC remains niche, its ability to cast wrought-equivalent alloys positions it as the next inflection point for the Automotive aluminum parts HPDC market.

By End Use: OEMs Dominate While Aftermarket Widens Niches

OEM contracts accounted for 89.12% of 2025 sales, mirroring consolidated procurement in a handful of global automakers. Multi-year sourcing agreements provide volume certainty that justifies significant gigacasting cell installations, supported by the segment's growth trajectory at a 5.95% CAGR. As EV fleets mature, aftermarket suppliers will rise at a notable CAGR, addressing collision repairs where single-piece castings must be swapped wholesale.

Independent parts distributors in North America and Europe already build inventory for Model Y rear under-bodies, signaling new revenue lines. Stringent IATF 16949 quality rules thin the field of eligible vendors, keeping aftermarket concentration higher than in legacy steel stampings. Robust barrier-to-entry characteristics therefore sustain margin discipline within the Automotive aluminum parts HPDC industry.

By Casting Material: Primary Alloys Lead but Recycled Content Speeds Up

Primary aluminum delivered 65.25% of 2025 volume, supported by A380 and A383 grades that balance fluidity with corrosion resistance. Warranty-critical assemblies—front rails, crash boxes, sub-frames—continue to specify primary metal to guarantee mechanical consistency. Recycled input rides a 8.13% CAGR tailwind, driven by policy mandates and OEM ESG commitments that publicize recycled-content percentages on window stickers.

Laser-induced breakdown spectroscopy and X-ray transmission sorting segregate scrap streams at an industrial scale, narrowing compositional tolerances and enabling secondary metals to enter semi-structural nodes. With energy-adjusted cost below prime, recycled feedstock delivers tangible savings, making it a strategic hedge against commodity swings for the Automotive aluminum parts HPDC market.

Geography Analysis

Asia-Pacific commanded 57.04% of 2025 turnover, reflecting deep vertical integration from bauxite mines to final vehicle assembly. Chinese automakers spearhead gigacasting adoption, while Indian firms draw on Production-Linked Incentives that encourage local die-casting investments. Japanese and Korean suppliers co-develop rheo-HPDC lines and export the technology across the region. Urbanization, last-mile delivery demand, and tightening Euro 6-equivalent emission rules combine to yield a 7.02% CAGR, reinforcing Asia-Pacific’s leadership in the Automotive aluminum parts HPDC market.

North America will see a notable CAGR through 2031 as USMCA content rules reward regional sourcing. Nemak’s Michigan expansion and Linamar’s Tennessee line tap that policy tailwind, while Tesla’s Texas gigafactory demonstrates domestic scale. Federal infrastructure funding channels additional power-grid capacity toward lightweight-component corridors, lowering electricity costs for energy-intensive casting shops. Together, these drivers spell durable growth for the Automotive aluminum parts HPDC market in the Americas.

Europe contributed significantly to 2025 revenue, cemented by premium brands that demand top-tier cast integrity. Circular-economy directives force recycled content, spurring foundries to adopt closed-loop scrap collection. Advanced high-strength steel remains a formidable rival in certain structural nodes, yet battery-electric platforms lean toward aluminum. Supply-chain re-localization also gains favor as OEMs cut exposure to geopolitical risk, channeling new investment within the bloc and supporting the Automotive aluminum parts HPDC industry outlook.

Competitive Landscape

Market concentration is moderate, with the largest vendors holding a significant collective share. Nemak, Rheinmetall, and Linamar pursue vertical integration—running in-house tooling design, machining, and module assembly—to lock in margin on each kilogram poured. Capital-intensive gigacasting sidelines smaller rivals who cannot finance 6,000-ton presses, creating an equipment-based moat.

Chinese entrants leverage scale and automation to capture regional contracts at a cost advantage, pressuring incumbents to accelerate Industry 4.0 adoption. Predictive-maintenance sensors reduce downtime, and digital-thread traceability reassures OEMs on quality compliance. Active patent filings focus on vacuum infiltration and multi-shot die designs that collapse cycle times.

Strategic acquisitions heat up: two gigacasting specialists changed hands in 2024, giving buyers an instant foothold in structural battery packs. Environmental and quality certifications—ISO 14001 and IATF 16949—remain table stakes for sourcing committees, further limiting the challenger set. These dynamics preserve pricing power within the Automotive aluminum parts HPDC market while spurring relentless capability upgrades.

Automotive Aluminum Parts High-Pressure Die Casting (HPDC) Industry Leaders

Nemak, S.A.B. de C.V.

Ryobi Die Casting Inc.

Linamar Corporation

Endurance Technologies Limited

Rheinmetall AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Researchers from Fraunhofer ILT in Aachen, Germany, and MacLean-Fogg in Mundelein, Illinois, unveiled a scalable method for the additive manufacturing of sizable aluminum components. Highlighting its promise in the automotive realm, the team crafted a sophisticated die-casting tool inlay for the transmission housing of a Toyota Yaris Hybrid.

- February 2025: Nio introduced a self-hardening aluminum alloy optimized for HPDC and deployed it on ET9 and Onvo L60 body-in-white modules, anticipating broader structural-casting uptake.

Global Automotive Aluminum Parts High-Pressure Die Casting (HPDC) Market Report Scope

The scope includes segmentation by application type (body-in-white components, chassis parts, transmission components, and other structural parts), vehicle type (passenger cars, light commercial vehicles, and medium and heavy commercial vehicles), manufacturing process (design engineering, die casting, surface treatment, and assembly), and end use (OEMs and aftermarket suppliers), and casting material (primary aluminum alloys and recycled aluminum alloys). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. Market size and growth forecasts are presented by value in USD.

| Body-in-White Components |

| Chassis Parts |

| Transmission Components |

| Other Structural Parts |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Design Engineering |

| Die Casting |

| Surface Treatment |

| Assembly |

| OEMs |

| Aftermarket Suppliers |

| Primary Aluminum Alloys |

| Recycled Aluminum Alloys |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Application Type | Body-in-White Components | |

| Chassis Parts | ||

| Transmission Components | ||

| Other Structural Parts | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Manufacturing Process | Design Engineering | |

| Die Casting | ||

| Surface Treatment | ||

| Assembly | ||

| By End Use | OEMs | |

| Aftermarket Suppliers | ||

| By Casting Material | Primary Aluminum Alloys | |

| Recycled Aluminum Alloys | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Automotive aluminum parts HPDC segment in 2025, and what CAGR is expected to 2031?

The segment is valued at USD 21.12 billion in 2025 and is forecast to expand at a 5.31% CAGR to reach USD 28.80 billion by 2031.

Which geographic region contributes the most revenue today?

Asia-Pacific contributes 57.04% of 2025 sales and is set to grow at a 7.02% CAGR through 2031, keeping it in the lead.

What is the single biggest application for high-pressure die-cast aluminum parts?

Body-in-white components hold 45.18% share, driven by gigacasting that consolidates dozens of stampings into one structural module.

How fast is recycled aluminum adoption growing in automotive casting?

Recycled alloys are projected to register a 8.13% CAGR, outpacing primary metal as circular-economy mandates tighten.

Which vehicle class will add volume the quickest over the next five years?

Light commercial vehicles are on track for a 7.62% CAGR through 2031 as e-commerce fleets electrify and seek lightweight chassis parts.

Page last updated on: