Automotive Aluminium Extrusion Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

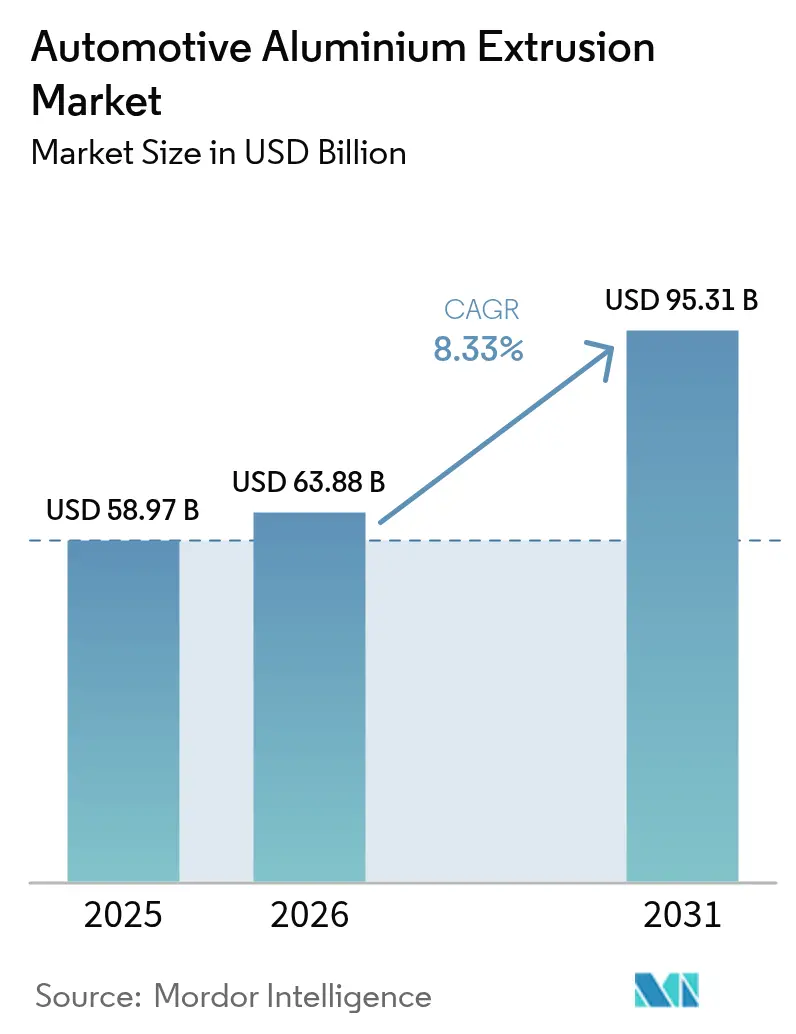

| Market Size (2026) | USD 63.88 Billion |

| Market Size (2031) | USD 95.31 Billion |

| Growth Rate (2026 - 2031) | 8.33% CAGR |

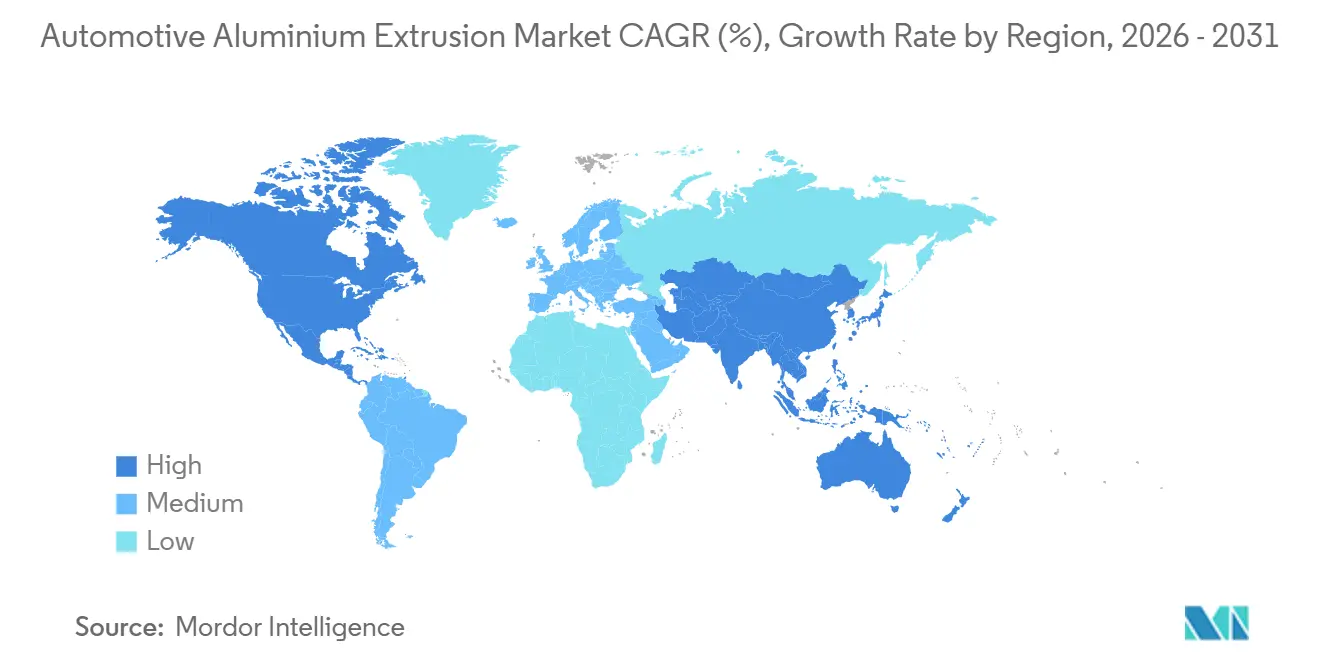

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Aluminium Extrusion Market Analysis by Mordor Intelligence

The Automotive Aluminum Extrusion market size is expected to grow from USD 58.97 billion in 2025 to USD 63.88 billion in 2026 and is forecast to reach USD 95.31 billion by 2031 at an 8.33% CAGR over 2026-2031. Persistent vehicle‐lightweighting targets, stricter fleet-average CO₂ ceilings, and the rapid scale-up of battery-electric architectures keep extrusion demand on an upward curve. Automakers view one-piece hollow profiles as a path to cut fasteners, welds, and assembly hours while retaining crash strength. Extruders respond by investing in larger presses and closed-loop recycling systems that lower embodied carbon and stabilize billet costs. Supply-chain localization in North America and Europe reinforces regional resilience as trade rules now reward aluminum sourced within the final-assembly bloc.

Key Report Takeaways

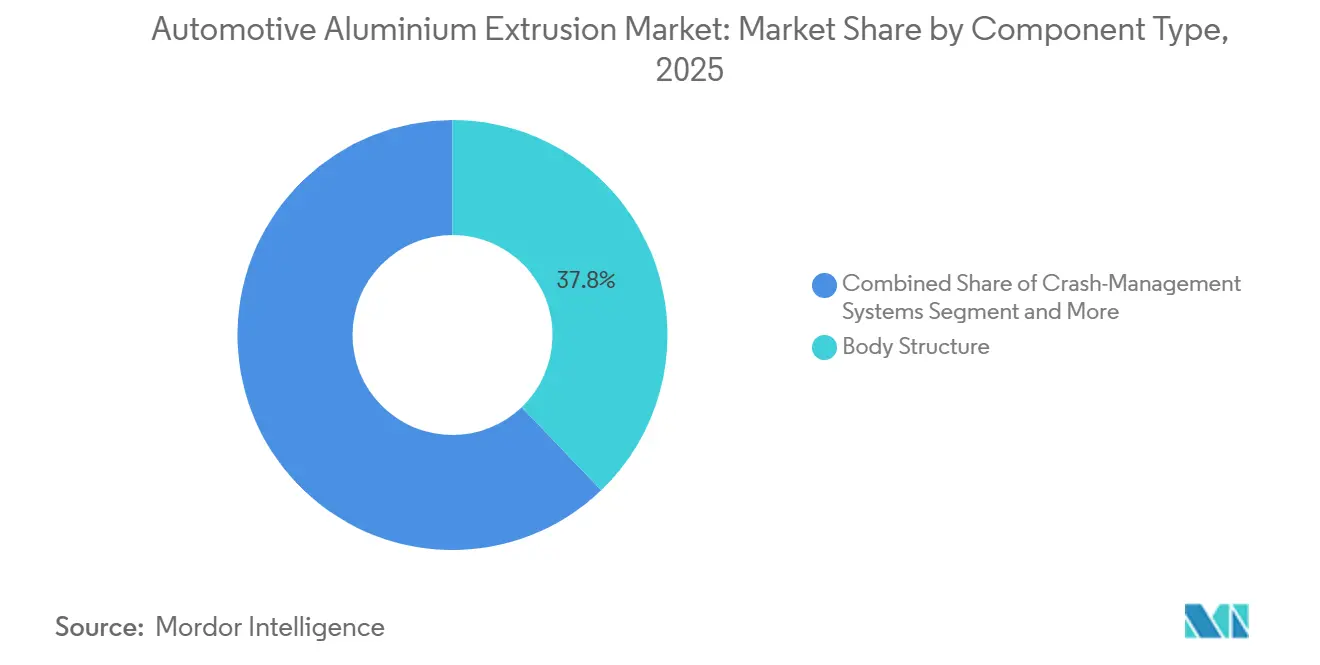

- By component, body structure components captured 37.83% of the automotive aluminum extrusion market share in 2025, whereas battery enclosures and thermal modules are expanding at a 9.87% CAGR through 2031.

- By vehicle type, passenger cars led with 52.38% revenue share in 2025 and are anticipated to record the highest projected CAGR at 9.88% to 2031.

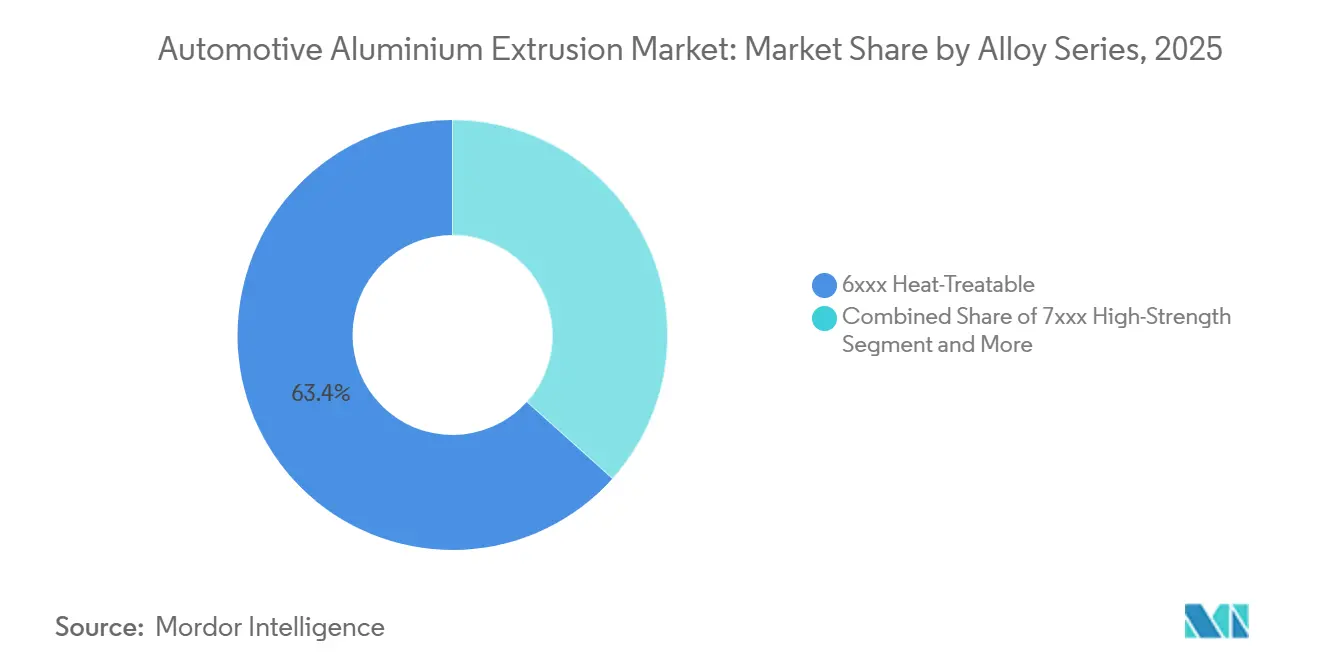

- By alloy series, the 6xxx grades accounted for 63.37% of the automotive aluminum extrusion market in 2025, while 7xxx high-strength alloys are forecast to rise at a 9.95% CAGR.

- By press capacity, 16 to 25 MN lines held the largest 37.81% share of the 2025 market, but presses above 35 MN are set to grow fastest at a 9.93% CAGR to 2031.

- By geography, Asia-Pacific dominated with a 39.92% share in 2025 and is poised to grow at a 9.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Aluminium Extrusion Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight Body-In-White Adoption | +2.1% | Global, with early concentration in China, EU, and California ZEV states | Medium term (2-4 years) |

| Fleet CO2 and Fuel-Economy Mandates | +1.8% | North America, EU-27, China (national); spillover to ASEAN via technology transfer | Short term (≤ 2 years) |

| Require Complex Hollow Extrusion Requirements | +1.5% | Global, led by Asia-Pacific cell manufacturing hubs and North American battery-belt investments | Medium term (2-4 years) |

| Tier-1 Extrusion Capacity | +1.2% | North America (USMCA), EU-27 (CBAM compliance); secondary impact in Mexico and Turkey | Long term (≥ 4 years) |

| Gigacasting-Extrusion Architectures | +0.9% | North America and EU premium segments; pilot adoption in China luxury brands | Long term (≥ 4 years) |

| Cost-Out & Scrap-Recycling | +0.7% | Global, with leading implementations in North America (Novelis) and EU (Norsk Hydro) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising EV Penetration Accelerates Lightweight Body-In-White Adoption

Electric-vehicle drivetrains add hundreds of kilograms in battery mass, so automakers redesign structures with hollow aluminum extrusions that merge crash rails and mounting bosses. Demonstrations from leading Asian-Pacific brands show 20-plus percent weight cuts at constant safety ratings. The Aluminum Association projects per-vehicle aluminum content reaching up to 550 PPV by 2030, with extrusions accounting for most of that growth. Mainstream hatchbacks now mirror premium SUVs in specifying extruded rocker and roof rails, spreading tooling amortization across millions of units. Range anxiety, raw-material costs, and warranty exposure jointly motivate this high-volume shift.

Fleet CO₂ and Fuel-Economy Mandates in the United States, European Union, and China

The European Union lowered its passenger-car fleet cap to 93.6 g/km in 2025 and will almost halve it by 2030; each excess gram triggers a hefty per-vehicle fine. Similar step-downs appear in United States CAFE updates that require 40.4 mpg United States fleet averages by 2026[1]"Draft Supplemental EIS for Safer Affordable Fuel-Efficient (SAFE) Vehicles Rule III for Model Years 2022 to 2031 Passenger Cars and Light Trucks", NHTSA, nhtsa.gov. China’s dual-credit program mirrors these goals by rewarding lightweight materials and levying penalties for non-compliance. Extruded aluminum lets manufacturers trim vehicle mass, offset battery weight, and avoid fines that can reach several thousand USD per car. Clear regulatory roadmaps also give suppliers the confidence to invest in new tooling and capacity. Mature crash data, proven recyclability, and scalable production further tilt the balance toward aluminum extrusions over magnesium or carbon fiber.

Battery Thermal-Management Enclosures Require Complex Hollow Extrusions

Lithium-ion packs operate reliably only when cell temperatures stay within a tight comfort zone, which makes effective thermal control a design priority. Engineers have shifted from heavier brazed assemblies to liquid coolers carved out of multi-port aluminum extrusions because the one-piece approach removes weld seams that can leak under vibration. The AA6xxx alloy family supplies the right mix of conductivity, formability and post-extrusion strength, letting the same profile carry structural loads while channeling coolant next to the battery. Producing such long, hollow shapes still calls for very large presses, and only a select group of plants owns equipment with the tonnage to push the metal in one pass. That scarcity keeps capacity constrained and grants premium pricing power to extruders that invested early in oversized machinery.

Near-Shoring of Tier-1 Extrusion Capacity (USMCA, EU-CBAM)

North American trade rules tie duty-free vehicle status to a high share of locally sourced aluminum, nudging automakers to procure billet and finished aluminum products within the region. Recent mill additions in the United States Southeast and northern Mexico mean stamping and assembly plants can receive metal in days rather than weeks, trimming inventory risk and freight emissions. On the other side of the Atlantic, Europe’s carbon-border policy penalizes aluminum made with fossil-heavy electricity, so OEMs increasingly favor billet from hydro-powered smelters within the customs union. Together, these measures encourage geographically compact supply webs that are less vulnerable to shipping delays or geopolitical flare-ups.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Volatility & Supply-Chain Speculation | -0.8% | Global, with acute exposure in spot-indexed contracts and regions lacking long-term offtake agreements | Short term (≤ 2 years) |

| Scarcity of More than 35 MN Press Lines | -0.6% | Global, concentrated in North America and EU where gigacasting adoption outpaces press investment | Medium term (2-4 years) |

| Carbon-Tax Pass-Through Risk | -0.4% | EU-27 primary impact; secondary effects in UK, Turkey, and MENA exporters to Europe | Medium term (2-4 years) |

| Plastics & CFRP Alternatives | -0.3% | Premium segments in North America and EU; limited penetration in mass-market Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

LME Aluminum Price Volatility & Supply-Chain Speculation

Aluminum base case price on the London Metal Exchange climbed close to USD 2,500 per ton in Q4-2024, the loftiest level since 2021, after Chinese smelters curtailed output and energy costs surged. Automakers locked into annual or longer vehicle-pricing cycles could not pass through those jumps quickly enough, eroding gross margins on battery-electric models that already carry higher bill-of-materials costs. Warehouse stocks are now dominated by Russian metal, so any sudden sanctions or export quotas could strip several million tonnes from accessible supply and trigger another spike. Hedging offers partial relief, yet the basis risk between cash metal and value-added billet still leaves extruders exposed when premiums widen. Smaller original-equipment manufacturers that rely on spot contracts remain the most vulnerable because they lack the scale to negotiate fixed-price offtake agreements with vertically integrated billet producers.

Scarcity of More than 35 MN Press Lines for Large EV Profiles

Battery-tray perimeters for midsize and larger electric vehicles exceed two meters in length and need presses above 35 meganewtons. Fewer than a dozen such lines operate worldwide, and each new installation requires capital outlays of nearly USD 150 million, plus a two-year lead time for foundations, auxiliaries, and dies. This bottleneck forces many programs toward multi-piece trays that add welds, gaskets, and mass, or toward gigacastings that remove extrusions outright. Because large-tonnage capacity is so concentrated, owners can charge premiums of 15%-25% over standard extrusion rates, raising vehicle cost and complicating price-parity efforts versus steel. The queue for development trials can stretch months, delaying model launches and pushing some automakers to redesign around what equipment is actually available rather than around the theoretically best solution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Battery Enclosures, Drive Application Evolution

Body structures accounted for 37.83% of the 2025 automotive aluminum extrusion market, underscoring the sector’s rapid shift toward lightweight vehicle designs. Carmakers replace conventional steel members with extruded aluminum to boost rigidity while reducing weight, improving fuel economy, and meeting tighter emissions regulations. These components also absorb crash energy effectively, enhancing passenger safety. The rise of multi-material body-in-white designs cements aluminum’s role as the preferred structural material. Consequently, body structures remain the cornerstone of extrusion demand in modern vehicles.

Battery enclosures and thermal modules form the fastest-growing component class, expanding at a 9.87% CAGR through 2031 as electric-vehicle adoption accelerates. The corrosion resistance and dimensional precision of aluminum extrusions make them ideal for safeguarding sensitive battery packs. As automakers shift to higher-density batteries and modular EV platforms, the need for advanced thermal-management housings continues to rise. Lightweight enclosures also extend driving range, a key performance metric for buyers—this growth trajectory positions battery systems at the center of future aluminum extrusion demand.

By Vehicle Type: Passenger Cars Lead Electrification Adoption

Passenger Cars commanded 52.38% of the Automotive Aluminum Extrusion market in 2025 and mirror the overall market’s 9.88% CAGR as BEV penetration climbs. Light commercial vehicles follow as parcel fleets electrify for last-mile delivery, prioritizing range and payload. Medium & heavy-duty trucks adopt extruded cab frames more cautiously, constrained by up-front costs. Buses and coaches present a steady replacement market, with fleet operators weighing long life cycles against lightweight benefits.

The automotive aluminum extrusion market for passenger cars is growing because platform economies of scale spread tooling costs across high unit volumes. Delivery vans, though cost-sensitive, increasingly favor extruded roof bows to offset the weight of battery packs under the floor. Drayage tractors and regional haul trucks investigate aluminum day-cab structures to recoup lost payload, yet frame rails often stay steel for torsional reasons. Transit buses are already alloy-intensive, so incremental adoption centers on next-generation alloys with higher recycled content.

By Alloy Series: 7xxx High-Strength Alloys Gain Momentum

The 6xxx heat-treatable series captured 63.37% of the 2025 market due to its mix of strength, corrosion resistance, and formability. These alloys serve body-in-white panels, crash-management parts, and chassis components. Automakers favor them because they achieve strong mechanical properties after heat treatment while remaining easy to extrude. Their flexibility suits the complex geometries found in modern vehicle designs. As lightweighting becomes standard practice, the 6xxx family retains its commanding lead.

The 7xxx high-strength series is the fastest-growing group, with a 9.95% CAGR, driven by its superior strength-to-weight ratio. Carmakers deploy these alloys in high-load structures, performance vehicles, and battery-protection frames. Their elevated mechanical performance allows thinner sections without compromising integrity, advancing deeper lightweighting goals. More rigid global crash rules further raise demand for stronger, chemically stable alloys. Next-generation EV and advanced chassis programs continue to fuel 7xxx adoption.

By Press Capacity: Large-Format Demand Outpaces Supply

Presses rated between 16 MN and 25 MN, led by a 37.81% share in 2025, met industry needs for versatile equipment capable of producing complex profiles at steady throughput. Tier-1 suppliers prefer this range for body structures, trim, and powertrain parts because it delivers medium- to large-section parts with uniform strength. The balance between cost efficiency and production flexibility has made these presses the backbone of automotive extrusion. Their capability matches the majority of current vehicle requirements. This segment, therefore, anchors overall market capacity.

Presses exceeding 35 MN are expanding the fastest at 9.93% CAGR, driven by demand for larger, stronger profiles used in EV battery housings and heavy-duty structures. High-tonnage equipment can extrude thicker, wider, and more intricate shapes needed for modern electric platforms and performance chassis. Leading aluminum producers are adding such presses to win next-generation vehicle programs. Structural integration and platform consolidation increase the value of single-piece extrusions. This trend positions the 35 MN+ class as a key driver of future manufacturing capability.

Geography Analysis

Asia-Pacific held 39.92% of the Automotive Aluminum Extrusion market share in 2025 and is set to grow at a 9.91% CAGR to 2031. China’s dual-credit regime rewards high new-energy-vehicle output, while India’s extrusion utilization hovers near 40%, leaving headroom for local suppliers as domestic EV production climbs PIB.GOV.IN. Japanese and South Korean value chains stretch into ASEAN, adding press lines in Thailand to serve regional assembly hubs. Tight primary-metal caps in China are pivoting the nation from a net exporter to balanced trade, influencing billet availability across the bloc.

North America benefits from USMCA regional-value rules that favor aluminum sourced and fabricated within the tri-nation zone. Recent capacity additions in the United States, Southeast, and northern Mexico shorten supply lanes to Detroit and Ontario plants. Canada supplies low-carbon primary aluminum via hydropower smelters, aligning with European decarbonization benchmarks and drawing interest from extruders seeking green-metal credentials.

Europe operates under the strictest fleet CO₂ ceilings and will implement the Carbon Border Adjustment Mechanism tariff in 2026[2]"First Biennial Transparency Report of Luxembourg under the Paris Agreement", UNFCCC, unfccc.int . Local billet stemming from hydropower smelters in Norway and Iceland helps automakers sidestep these charges. Germany, France, and Spain anchor demand, yet subsidy reductions in late 2025 slowed BEV uptake, challenging extruders to balance capacity. Neighboring Turkey positions itself as a near-shore alternative but must invest in low-carbon smelting or face the same CBAM levy.

Regulatory Landscape

Regulation shaping automotive aluminium extrusion demand is driven by fleet CO2 targets, circularity requirements, and trade and carbon-border measures. In the European Union, passenger-car fleet targets tightened to 93.6 g/km in 2025, and the CO2 standards framework remains under active revision in 2026, with industry proposals that explicitly link compliance pathways to low-carbon materials, including aluminium. Circularity rules are also moving from voluntary to mandated: the EU End-of-Life Vehicles (ELV) file reached a provisional agreement in February 2026, with follow-on delegated acts planned to define mandatory recycled-content targets, which will affect alloy selection, scrap qualification, and documentation needs for extruded body and battery structures.

On the supply side, extruders and OEMs manage evolving trade and product-compliance constraints. The EU Carbon Border Adjustment Mechanism is entering its 2026 implementation phase, and discussion is underway around potential downstream scope expansion to cover more aluminium products, raising the value of verified emissions data for billet and extrusion inputs. In North America, Section 232 aluminium tariffs remain a key procurement variable, with a scheduled review in July 2026 that supports business cases for regionalized billet and extrusion capacity under USMCA rules. Materials standards also continue to update: NS-EN 573-3:2026 (published April 2026) refreshes chemical composition specifications for wrought aluminium alloys, while ISO 6362-7:2022 remains a core reference for extruded rods, bars, tubes, and profiles used in automotive qualification.

Value Chain Analysis

The automotive aluminium extrusion value chain starts with upstream alumina, primary aluminium production, and recycling, then moves into billet casting (primary and secondary), followed by extrusion pressing and downstream value-add such as stretching, heat treatment, machining, surface finishing, and joining (including friction-stir welding for assemblies). Automotive programs typically lock in alloy and profile designs early, with qualification cycles that extend well beyond a year for crash and battery-structure applications, and with hardened steel tooling for hollow profiles often driving meaningful lead times. The main manufacturing bottlenecks are at qualified press sites for complex hollow and large-format profiles, especially where EV battery-tray perimeters and thermal-management multiport channels require higher tonnage, tight dimensional control, and robust die design.

Downstream, Tier-1 suppliers and OEM body shops convert extrusions into structural modules through cutting, machining, bonding, and welding, then integrate them into body-in-white, crash-management, and battery enclosure systems. Competitive differentiation increasingly depends on integrated circular supply, including closed-loop scrap return from stamping and fabrication back into billet, along with metallurgy and process control that manage impurities as recycled content rises. Technology upgrades at extrusion plants, such as Norsk Hydro commissioning a HybrEx press at Gainesville, Georgia in February 2026, show the shift toward lower-energy, higher-productivity extrusion. OEM projects that specify recycled aluminium grades, such as Hydro CIRCAL supplied into a Mercedes-Benz Trucks circular manufacturing project in April 2026, also illustrate how recycled feedstock is moving into defined material streams that influence sourcing, casting, and extrusion operations.

Competitive Landscape

Five global groups: Constellium SE, Novelis Inc., Norsk Hydro ASA, Kaiser Aluminum Corp., and UACJ Corp. control the majority of the worldwide automotive extrusion market, giving the sector a moderate concentration. These leaders combine captive billet casting with large-tonnage presses, allowing them to quote turnkey body-structure or battery-enclosure programs at less volatile cost. Mid-tier regional firms stay relevant by offering rapid die changes and shorter logistics lanes, yet their margins narrow when LME premiums spike because they purchase most billet on the open market.

Technology rivalry now centers on porthole dies that create multi-port hollows for liquid cooling, and on friction-stir welding that joins extruded panels without melting the interface, preserving the majority of the base-metal strength. Constellium’s press in Germany underscores the tonnage arms race; it can deliver battery-tray frames in one pass, a capability that competing plants struggle to match. Norsk Hydro, meanwhile, markets low-carbon billet from hydropower smelters, helping customers dodge Europe’s Carbon Border Adjustment Mechanism fees and improving cradle-to-gate footprints.

Disruption pressure comes from gigacasting vendors whose 6,000-tonne to 12,000-tonne die-casting machines enable OEMs to consolidate most rear-underbody parts into a single part. Extruders counter by designing hybrid architectures that bond cast nodes to hollow rails, reclaiming some volume while leveraging aluminum’s energy-absorption edge over castings in side-impact events. Closed-loop scrap programs add another competitive lever: suppliers that can melt stamping offcuts back into billet lock in customers eager to certify low-carbon supply chains under emerging Scope 3 mandates.

Automotive Aluminium Extrusion Industry Leaders

-

Novelis Inc.

-

Constellium SE

-

Norsk Hydro ASA

-

Kaiser Aluminum Corporation

-

UACJ Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace in automotive aluminium extrusion sits where lightweighting and verifiable low-carbon content overlap, since policy and OEM sourcing practices are tightening at the same time. In Europe, the February 2026 provisional agreement on the ELV regulation, along with the parallel 2026 discussion around revising EU CO2 rules, has elevated recycled-content traceability and low-carbon material declarations from procurement preferences into near-term design and supplier-qualification requirements. This supports opportunities for extruders that can supply documented recycled-content alloys, maintain stable chemistry windows for 6xxx and higher-strength series, and expand closed-loop scrap programs that help automakers meet circularity objectives without sacrificing structural performance for body rails, sills, and battery protection frames.

Capacity and process technology also shape the near-term opportunity set. Large-format, complex hollow profiles for battery enclosures and thermal modules remain constrained by limited availability of very large presses and by long die lead times, which increases the value of suppliers that can shorten industrialization cycles through co-design, simulation, and in-house tooling. Investment and localization signals are visible in North America, where capacity that pairs rolling and recycling with automotive-focused output is being built for body-in-white and closure material streams, including Novelis Bay Minette in Alabama, a USD 4.1 billion project targeting 600,000 tons of finished aluminium goods capacity with commissioning planned for the second half of 2026. On the extrusion side, plant upgrades such as Hydro's hybrid electric/hydraulic press start-up in Gainesville, Georgia in 2026 show how energy and CO2e-per-ton performance is becoming a differentiator in RFQs, alongside the ability to produce multiport cooling and crash-management profiles.

Recent Industry Developments

- June 2026: Novelis updated the market on its Bay Minette rolling and recycling facility in Alabama, highlighting a 600,000-ton capacity plan and commissioning targeted for the second half of 2026. The site is positioned to supply automotive sheet streams that complement extrusion-heavy body and battery architectures, strengthening localized aluminium supply options in the US Southeast. Bringing recycling and high-volume finishing closer to OEM and Tier-1 footprints supports shorter lead times and lower embodied-carbon sourcing strategies.

- February 2026: Norsk Hydro commissioned a HybrEx press at Gainesville, Georgia, marking a step toward lower-energy extrusion and higher productivity that enables advanced multiport cooling and crash-management profiles. This upgrade aligns with ongoing energy-efficiency and CO2 reduction efforts in hydrocarbon-free production lines and supports Hydro's strategy to expand high-volume, low-carbon aluminium tooling capabilities.

- July 2024: Constellium signed a long-term agreement with Lotte Infracell to supply battery foilstock and announced a EUR 30 million investment to increase capacity at its Singen, Germany facility. The move strengthens European battery-material supply chains and signals continued capital allocation into EV-related aluminium value streams. Incremental finishing capacity supports higher throughput and consistency for downstream converters and cell makers operating under increasingly stringent sustainability and traceability expectations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of aluminum extrusion products used in automotive applications, where extruded profiles are supplied for vehicle structures, safety parts, closures, and electrification-related modules.

Scope exclusions: We exclude aluminum castings, forgings, sheets and stampings, and non-automotive extrusion demand even when it uses similar alloy families.

Segmentation Overview

-

By Component Type

- Body Structure

- Crash-Management Systems

- Battery Enclosures and Thermal Modules

- Exterior Trim and Roof Rails

- Interior Modules

- Other Components

-

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy-Duty Trucks

- Buses and Coaches

-

By Alloy Series

- 6xxx Heat-Treatable

- 7xxx High-Strength

- 5xxx Non-Heat-Treatable

- Scandium & Novel Alloys

-

By Press Capacity

- Less than or equal to 15 MN

- 16 to 25 MN

- 26 to 35 MN

- More than 35 MN

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

-

Middle-East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- Egypt

- South Africa

- Rest of Middle-East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping what counts as an automotive extrusion, and how material moves from billet through extrusion presses to the finished profile, so we could test the demand side and the supply side within the same model. Public sources were used to anchor the big totals, such as vehicle production and registration series from agencies such as OICA, and trade and tariff-line statistics from sources such as UN Comtrade. To connect value to input drivers, we also referenced industrial and price indicators from sources such as the USGS and national statistics offices.

Next, we reviewed lightweighting and safety adoption signals that influence extrusion content per vehicle, using sources such as regulatory emissions standards publications, transport safety references, and peer reviewed materials engineering journals that discuss alloy series and joining trends. Company annual reports, investor decks, and press releases were then used to confirm capacity additions, plant footprints, and typical end uses for profiles like crash management parts and battery enclosures. In a few places, paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export records were used to fill gaps where public detail was limited. The desk sources listed above are illustrative only, and we used many other public references for cross-checks and clarification.

Primary Interviews and Surveys

Primary work focused on validating real purchasing behavior and how extrusion content is changing by platform, especially for EV battery trays, side rails, and structural modules. We spoke with a mix of extrusion producers, automotive component suppliers, OEM-aligned engineering teams, and distributors. The discussions were balanced across high volume manufacturing regions to confirm assumptions on demand mix and typical pricing movements. These inputs were then used to test desk assumptions, resolve unclear definitions, and confirm the practical boundary of what is booked as automotive extrusion revenue.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 16% | APAC: 39% |

| Mid tier: 44% | Functional/Unit leaders: 35% | EMEA: 34% |

| Smaller Players: 20% | Managers: 49% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where vehicle production by region was converted into an extrusion demand pool using extrusion content per vehicle, which was then valued using application-level average selling prices. Once the demand pool was established, we checked it against selective bottom-up approximations, where sampled supplier revenue splits, capacity utilization signals, and channel checks were used to confirm that totals were not drifting away from what the supply chain can deliver.

Key inputs in the model included regional passenger car and LCV production, EV share by region, the mix shift toward battery enclosures and crash management systems, alloy series preferences (especially 6xxx versus higher strength series), and press capacity deployment by major producing regions. Pricing was handled through a practical blend of aluminum price direction, conversion premium logic, and product mix changes, then stress-tested in interviews since contract timing can delay pass-through.

For forecasting, we used scenario analysis because adoption is driven by both regulations and platform redesign cycles, which do not move in a straight line every year. The base case followed expected build schedules and lightweighting targets shared by industry participants, and the upside and downside cases were used to reflect slower or faster EV and hybrid penetration. Where a clean bottom-up number was not available for a country or a small application, we handled gaps by applying peer-region intensity ranges and then reconciling back to production and trade signals.

Data Validation & Update Cycle

Validation was done by comparing the final market totals with independent signals such as aluminum consumption direction, vehicle build trends, and capacity announcements, and then reviewing any large variances region by region. When the model produced a jump that could not be explained by production, mix, or pricing drivers, we revisited the assumptions and triggered follow-up calls with the most relevant respondents.

Before sign-off, the work is reviewed in steps so definitions, math, and reasoning stay consistent across regions and years. Reports are refreshed annually, and interim updates are made when material events occur, such as major capacity starts, sudden vehicle build slowdowns, or policy changes affecting lightweight materials. Right before delivery, a final pass is completed so clients receive the most current view.

Mordor Intelligence's Automotive Aluminium Extrusion Market Size Compared With Other Published Estimates

Published market sizes for automotive aluminum extrusion often do not match, even when they appear to cover the same topic. The gaps usually come from how each study draws the line between automotive-only extrusions and adjacent aluminum products, and also from differences in the year used as the starting point.

By tracking press-capacity deployment, EV platform mix, and application-level pricing, Mordor Intelligence keeps the estimate tied to automotive end-use extrusions like crash systems and battery enclosures, rather than blending in wider aluminum extrusion revenue. Some estimates also apply aggressive price growth uniformly, or they convert currencies using a single point-in-time rate, which can move the number materially for regions with volatile exchange rates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 63.88 B (2026) | |

| Regional Consultancy A | USD 32.43 B (2024) | Uses an earlier base year and appears to apply a narrower demand pool tied to selected component types, which can undercount newer EV-driven extrusion applications and later-cycle platform rollouts. |

| Global Consultancy B | USD 98.30 B (2025) | The value level suggests a broader scope or higher ASP path, potentially folding in non-extrusion aluminum content or applying stronger price escalation before validating against vehicle production and application mix. |

The spread in the table mostly comes down to scope boundaries and how fast pricing and EV-related content are assumed to rise. When the model is built from vehicle output and extrusion content by application, and then checked back to supply-side signals, the result stays easier to trace and repeat year to year.

Key Questions Answered in the Report

What is the projected value of the Automotive Aluminum Extrusion market by 2031?

Forecasts indicate USD 95.31 billion by 2031, reflecting the segment’s sustained 8.33% CAGR.

Which component will grow fastest through 2031?

Battery Enclosures & Thermal Modules lead with a 9.87% CAGR as liquid-cooled battery packs scale.

Why are 7xxx alloys gaining share in automotive extrusions?

They offer yield strength above 400 MPa, enabling thinner crash rails without compromising safety.

How does closed-loop recycling benefit automakers?

It cuts billet cost volatility and shrinks embodied carbon, aiding compliance with corporate scope-3 targets.

Page last updated on: