Automotive Airbag Silicone Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 596.64 Million |

| Market Size (2030) | USD 983.82 Million |

| Growth Rate (2025 - 2030) | 10.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Airbag Silicone Market Analysis by Mordor Intelligence

The automotive airbag silicone market size was USD 596.64 million in 2025 and is projected to attain USD 983.82 million by 2030, advancing at a 10.52% CAGR. Current demand stems from the convergence of stringent global safety mandates, electrified-vehicle platform constraints, and multilayer airbag architectures that collectively require high-performance silicone formulations. OEM programs targeting Euro NCAP’s 2030 zero-fatality objective translate to higher module counts per vehicle, while China’s forthcoming GB/T 3730.3-2027 standard uplifts mechanical and thermal benchmarks. Suppliers that master ultra-thin, high-temperature compounds are winning early design-ins as battery-electric vehicle (BEV) adoption spreads. Asia-Pacific’s production scale, rapid regulatory tightening, and competitive labor costs anchor its leadership even as Europe and North America prioritize premium, long-life grades. Across regions, automakers allocate larger development budgets to materials that can resist premature aging, capture lightweighting gains, and integrate recyclability, reinforcing value creation in the automotive airbag silicone market.

Key Report Takeaways

- By product type, Liquid Silicone Rubber (LSR) led with a 69.85% share of the automotive airbag silicone market in 2024, while Thermoplastic Silicone (TPSiV) is forecasted to expand at an 11.41% CAGR to 2030.

- By airbag position, curtain/side systems captured a 42.52% revenue share of the automotive airbag silicone market in 2024; knee airbags are projected to record the fastest CAGR, at 10.66%, through 2030.

- By vehicle type, passenger cars accounted for 63.27% of the automotive airbag silicone market size in 2024, while light commercial vehicles are projected to advance at an 11.13% CAGR over the forecast period.

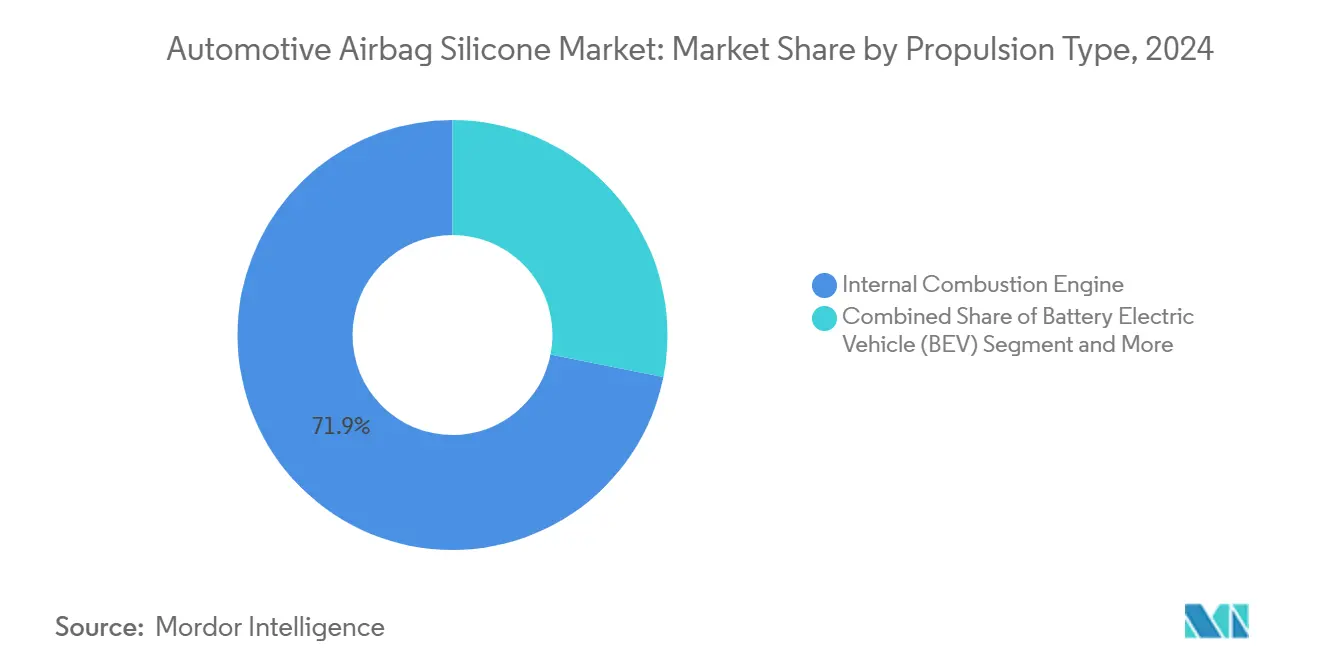

- By propulsion type, internal-combustion platforms held a 71.88% share of the automotive airbag silicone market in 2024, whereas BEVs are projected to exhibit an 18.73% CAGR to 2030.

- By distribution channel, OEM programs dominated with 78.96% share of the automotive airbag silicone market in 2024, as the aftermarket is projected to grow at a 12.01% CAGR on the back of replacement and retrofit demand.

- By Geography, Asia-Pacific captured 41.51% share of the automotive airbag silicone market in 2024 and is projected to grow at a 11.07% CAGR to 2030.

Global Automotive Airbag Silicone Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEV Platform Redesign | +1.9% | Global, with early gains in China, Europe, North America | Medium term (2-4 years) |

| Euro NCAP 2030 "Zero-Death" Road-Map | +1.8% | Europe & EU, spill-over to APAC and Americas | Long term (≥ 4 years) |

| Shift Toward LSR | +1.6% | Global | Short term (≤ 2 years) |

| Vehicle Safety Regulations | +1.4% | Global | Medium term (2-4 years) |

| Full-Vehicle Inflator-Compatibility Tests | +1.1% | China core, spill-over to APAC | Medium term (2-4 years) |

| Side and Curtain Airbag Adotion | +0.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

BEV Platform Redesign Needs Thinner, High-Temp Silicones

Battery-electric platforms compress under-dashboard real estate, forcing airbag modules into slimmer envelopes without sacrificing deployment reliability. Engineers, therefore, specify fluorosilicone blends that raise thermal-degradation onset by 15 – 20 °C while maintaining low-temperature flexibility. Cost premiums of 25 – 30% over standard grades are acceptable because warranty liabilities for thermal failure dwarf resin upcharges. Chinese EV brands fast-track such compounds across 2026 model launches, a move already mirrored in European joint ventures. As BEVs scale globally, the automotive airbag silicone market registers consistent mix-upgrade tailwinds.

Euro NCAP 2030 Zero-Death Roadmap Spurring Multi-Airbag Architectures

Euro NCAP’s long-range rating protocol compels OEMs to integrate up to 12 airbags per vehicle, increasing silicone consumption by as much as 60% relative to 2023 baselines. Once validated for European programs, the same architectures roll into North American and APAC nameplates to amortize tooling. Suppliers supplying curtain systems benefit most because side-impact tests carry heavy weighting. European tier-ones contract multiyear volumes, granting silicone producers clearer visibility on capacity planning and reinforcing revenue stability across the automotive airbag silicone market.

Shift Toward LSR for Lightweighting

Liquid Silicone Rubber lowers part mass by approximately 15 – 25% versus thermoplastic coatings and supports intricate vent patterns through precision injection molding. Weight savings translate directly into extended EV range, strengthening OEM resolve to favor LSR despite higher raw-material cost per kilogram. A 20,000 metric-ton expansion in Czechia will supply next-generation electromobility programs starting late-2025[1]Scott Alex, “Wacker to Build Czech Silicone Formulation Plant,” Chemical & Engineering News, cen.acs.org. Shorter cure cycles also trim energy utilization at module houses, widening LSR’s total-cost advantage.

Rising Vehicle-Safety Regulations

The World Forum for Harmonization of Vehicle Regulations (WP.29) adopted 38 amendments effective September 2025, including enhanced airbag durability requirements that address premature aging concerns. Simultaneously, the United States enforces upgraded FMVSS 213a side-impact child-protection measures[2]National Highway Traffic Safety Administration, “Federal Motor Vehicle Safety Standards; Child Restraint Systems-Side Impact Protection,” Federal Register, federalregister.gov. Harmonizing these mandates boosts global baseline requirements, accelerating the adoption of premium silicone chemistries with validated 15-year life performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Silicone Prices | -1.7% | Global | Short term (≤ 2 years) |

| Seat-Belt Integrated Inflatable Restraints | -1.3% | North America and EU, spill-over to APAC | Medium term (2-4 years) |

| Recycling Challenges | -1.2% | Europe and EU, spill-over to Global | Long term (≥ 4 years) |

| Push for Fluoropolymer Coatings | -0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Silicone-Monomer Prices

Silicon metal price swings are creating significant cost challenges for the silicone supply chain, with companies like Dow raising prices multiple times in 2024. Since raw materials account for nearly half of silicone product costs, fluctuations in metallurgical-grade silicon, driven by energy prices and Chinese policies, hit hard. Wacker Chemie mitigates this risk through partial self-supply from its Norway facility, giving it an edge during disruptions. Smaller suppliers, however, struggle to absorb these costs due to fixed-price contracts with OEMs. The impact is especially severe for premium silicone grades used in high-temperature EV applications, where raw material volatility translates into higher absolute costs.

Seat-Belt Integrated Inflatable Restraints Cutting Silicone Demand

New seat-belt integrated inflatable restraints could cut silicone demand by 20–30% in some vehicle segments. These systems embed inflation mechanisms into seat-belt webbing, reducing the need for traditional airbag modules. They are particularly appealing for knee and side airbags in space-constrained designs, making them attractive to OEMs. While luxury brands lead early adoption, broader rollout faces regulatory and consumer acceptance challenges. The trend is strongest in North America and Europe, creating regional demand shifts that complicate supplier planning and investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: LSR Dominance Faces TPSiV Challenge

The Liquid Silicone Rubber category captured a commanding 69.85% share of the automotive airbag silicone market size in 2024. Multiple OEM programs continue to specify LSR because its platinum-cure chemistry delivers consistent mechanical properties, minimal post-cure outgassing, and excellent adhesion to polyamide fabrics. These attributes are indispensable for modules requiring precise vent holes and integrated sealing ribs. TPSiV, however, records an 11.41% CAGR as manufacturers seek recyclable, thermoplastic processing routes that can shorten takt times while aligning with circular-economy policies.

TPSiV uptake spreads first in non-critical trim covers, then migrates toward secondary-bag chambers where tear strength requirements are lower. European sustainability regulations act as tailwinds, yet Asian mass-production hubs still favor LSR for its proven deployment reliability. Ongoing research into peroxide-free crosslink systems may narrow processing time disparities, helping LSR maintain share leadership within the automotive airbag silicone market despite growing TPSiV traction.

By Airbag Position: Curtain Systems Drive Innovation

Curtain and side airbags collectively constituted 42.52% of the automotive airbag silicone market in 2024, the largest slice within this segmentation. Euro NCAP and NHTSA side-impact protocols elevate these modules to mandatory status on virtually every platform, making them the prime consumption engine for silicones that blend high-tear fabrics with gas-permeation control layers. Silicone suppliers tailor rheology to encourage uniform coating even at the fast line speeds typical of high-volume seat-belt plants.

Knee airbags, with a 10.66% forecast CAGR, reflect cabin-layout changes linked to autonomous driving and flat-floor BEV architectures. Their smaller envelopes nonetheless target extreme deployment consistency, intensifying focus on low-volatile silicones that can weather prolonged cabin heat soak. Front airbags remain mature yet continue to evolve via dual-stage inflator tuning. This sustained baseline stabilizes revenue even if growth rates trail newer positions, ensuring balanced opportunity distribution inside the automotive airbag silicone market.

By Vehicle Type: Passenger Cars Lead, Commercial Segments Emerge

Passenger cars secured 63.27% automotive airbag silicone market share in 2024, reflecting both volume leadership and continued expansion in safety feature adoption. Safety-feature democratization across A- and B-segment hatchbacks in India, ASEAN, and Latin America fuels incremental volume, while premium EVs lift per-vehicle consumption by adding center-console and far-side bags. As ride-hailing fleets modernize, fleet operators emphasize 5-star ratings to limit liability, further lifting demand.

Light commercial vehicles, posting an 11.13% CAGR to 2030, adopt many of the same occupant-protection modules to comply with harmonized UNECE standards, albeit at slower rates because cost sensitivity tempers rapid spec inclusion. Medium- and heavy-duty trucks trail but show rising interest in driver-airbag upgrades tied to shortage-driven driver-retention incentives. Cross-segment diversity therefore stabilizes revenues and encourages global geographic spread for the automotive airbag silicone market.

By Propulsion Type: Electrification Reshapes Requirements

Internal-combustion platforms held 71.88% of the automotive airbag silicone market in 2024, reflecting the global vehicle parc’s enduring dominance. Nonetheless, the BEV sub-segment surges at an 18.73% CAGR, causing material science roadmaps to pivot toward ultra-slim, high-temperature silicone designs. Engineers now specify compounds able to tolerate battery heat soak, electromagnetic interference, and novel installation geometries inside skateboard chassis. These specialized needs expand the average selling price and margin within the automotive airbag silicone market size for BEV-oriented grades.

Hybrid and plug-in hybrid vehicles represent transitional pathways but still require robust silicone coatings because gasoline engines introduce thermal cycling not present in full EVs. Fuel-cell variants remain niche yet important technology demonstrators; silicone developers use such projects to validate hydrogen-resistant formulations that could migrate back into high-pressure systems in mainstream cars. Propulsion diversity, therefore, broadens the innovation canvas, sustaining R&D cycles and deepening entry barriers.

By Distribution Channel: OEM Dominance, Aftermarket Growth

OEM integration accounted for 78.96% of the automotive airbag silicone market in 2024, underpinned by long-cycle homologation processes and joint validation labs that favor entrenched supplier relationships. Module makers bundle silicone sourcing with fabric lamination contracts to lock pricing over multiyear production horizons. This reduces revenue volatility and supports continuous process-improvement programs between producers and tier-ones. Aftermarket volumes, advancing at 12.01% CAGR, arise from rising average vehicle age and regulatory pushes compelling the replacement of expired inflators after 10 – 15 years.

Emerging economies see parallel demand for retrofit kits where new safety rules cover existing fleets. Silicone suppliers targeting this channel adapt pack sizes, introduce rapid-cure field compounds, and partner with distributors specializing in collision-repair networks. Although aftermarket revenue remains smaller in absolute terms, its double-digit growth enriches the long-tail opportunity within the automotive airbag silicone market.

Geography Analysis

Asia-Pacific retained 41.51% share of the automotive airbag silicone market in 2024 and sustains the fastest regional CAGR of 11.07% through 2030. China dominates volume via massive passenger-car output and progressive safety mandates such as the GB/T 3730.3-2027 inflator-compatibility rule that heightens demand for durable, moisture-resistant silicones. India’s production-linked incentives invite fresh investments in airbag module lines, adding incremental uptake of LSR coatings. Japan and South Korea supply technology-intensive designs that adopt premium silicone blends, ensuring regional demand covers both volume and margin segments.

North America delivers a 6.91% CAGR, buoyed by NHTSA side-impact child-protection amendments that require high-tear curtain systems. The U.S. shift toward light-truck electrification layers in thermal-management constraints, prompting OEMs to endorse fluorosilane-modified silicones for steering-wheel and driver-bag applications adjacent to battery junction boxes. Canada and Mexico follow U.S. design cues, creating an integrated regional ecosystem for silicone supply.

Europe logs a 7.18% CAGR as the Euro NCAP zero-death roadmap drives platform redesign and elevates module counts. OEMs there also weigh end-of-life recyclability, granting Thermoplastic Silicone inroads for non-critical air chambers. Wacker Chemie’s new Czechia formulation plant underpins regional security of supply, shortening lead times for tier-two module houses. Though smaller in share, South America and the Middle East & Africa show steady progress as domestic safety regulations mature, unlocking long-tail upside for the automotive airbag silicone market.

Competitive Landscape

The automotive airbag silicone market exhibits moderate consolidation, creating competitive dynamics that favor scale advantages and technological differentiation. Dow, Wacker Chemie, and Momentive anchor their leadership through vertical integration, specialized compounding, and co-development agreements that embed them deeply in OEM validation loops. Wacker secures approximately one-fourth of its silicon-metal feedstock from a captive Norwegian smelter, insulating production from commodity swings and enabling aggressive volume-expansion plays.

Rivalry centers on BEV-specific materials capable of 150 °C continuous service life in crowded battery packs. Dow’s alliance with recycling start-up Circusil explores depolymerization routes that might slash Scope 3 emissions, a differentiator as automakers quantify embedded carbon. Meanwhile, Evonik’s 2025 merger of its Silica and Silanes operations into Smart Effects brings additive and coupling-agent expertise under one roof, advancing next-generation filler systems for ultrathin coatings.

New entrants focus on hybrid fluoropolymer-silicone blends for sensor housings and extreme-temperature zones but lack the process integration needed for safety-critical fabrics. Consequently, tier-one module makers maintain dual-sourcing yet continue to favor incumbents for bulk volumes. The landscape therefore balances innovation incentives with high switching costs, sustaining moderate concentration while leaving room for niche disruptors across the automotive airbag silicone market.

Automotive Airbag Silicone Industry Leaders

Dow Chemical Company

Wacker Chemie AG

Momentive Performance Materials Inc.

Elkem ASA

Shin-Etsu Chemical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Wacker Chemie started building a 20,000 metric-ton silicone-formulation facility in Karlovy Vary, Czechia, to serve electromobility and renewable-energy markets with room-temperature-vulcanizing grades .

- May 2025: Nexperia unveiled automotive-qualified silicon-carbide MOSFETs with low RDS(on) values, indirectly supporting BEV thermal-management system redesigns that influence airbag-module layout in high-voltage architectures.

- January 2025: Evonik launched the Smart Effects business line by merging Silica and Silanes operations, unlocking combined molecular-chemistry and particle-design capabilities for advanced automotive silicone compounds.

Global Automotive Airbag Silicone Market Report Scope

| Liquid Silicone Rubber (LSR) |

| Thermoplastic Silicone (TPSiV) |

| Front Airbags |

| Knee Airbags |

| Curtain/Side Airbags |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Internal Combustion Engine |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-In Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Liquid Silicone Rubber (LSR) | |

| Thermoplastic Silicone (TPSiV) | ||

| By Airbag Position | Front Airbags | |

| Knee Airbags | ||

| Curtain/Side Airbags | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion Type | Internal Combustion Engine | |

| Battery Electric Vehicle (BEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Plug-In Hybrid Electric Vehicle (PHEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive airbag silicone market in 2030?

The market is forecasted to reach USD 983.82 million by 2030, reflecting a 10.52% CAGR from 2025.

Which silicone product type currently dominates supply to airbag manufacturers?

Liquid Silicone Rubber holds 69.85% share owing to its superior mechanical and processing characteristics for safety-critical modules.

How fast is the BEV segment expanding for airbag silicone usage?

BEV platforms are advancing at an 18.73% CAGR because their compact designs demand ultra-thin, high-temperature silicone formulations.

Why are curtain airbags important for future growth?

Curtain units account for the largest position-based demand and benefit from stricter side-impact regulations that require high-tear, controlled-venting silicone coatings.

Which region contributes the most revenue to the market?

Asia-Pacific leads with 41.51% share, propelled by China’s production scale and fast-tightening safety standards.

Page last updated on: