Automotive Airbags And Seatbelts Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

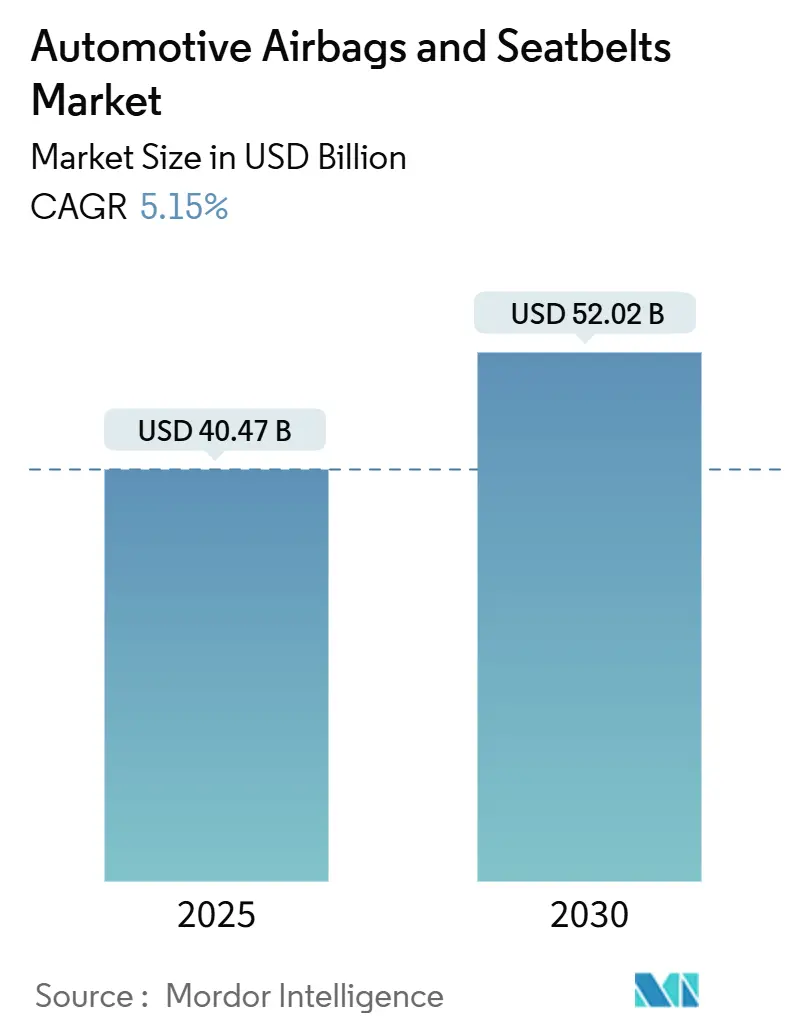

| Market Size (2025) | USD 40.47 Billion |

| Market Size (2030) | USD 52.02 Billion |

| Growth Rate (2025 - 2030) | 5.15% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Airbags And Seatbelts Market Analysis by Mordor Intelligence

The automotive airbags and seatbelts market reached USD 40.47 billion in 2025 and is forecast to expand at a 5.15% CAGR to USD 52.02 billion by 2030, underscoring the sector’s steady response to tougher passive-safety rules and the rapid electrification of vehicle platforms. Mandatory upgrades to FMVSS 208 and 305, more stringent Euro NCAP test scenarios, and Asia-Pacific crash-worthiness policies are pushing OEMs to deploy additional airbags, smarter seatbelts, and advanced occupant-state sensing in volume models[1]“Federal Motor Vehicle Safety Standards,” National Highway Traffic Safety Administration, nhtsa.gov. Suppliers who merge software-defined deployment logic with lightweight materials gain an edge as regulators press for holistic occupant protection at lower vehicle mass. The automotive airbags and seatbelts market also benefits from a broad shift toward modular restraint “domains,” which reduce wiring, simplify over-the-air updates, and contain warranty costs. At the same time, lingering Takata-era liability frameworks raise the cost of entry, favor incumbents with proven quality systems, and reinforce brand-related buyer preferences.

Key Report Takeaways

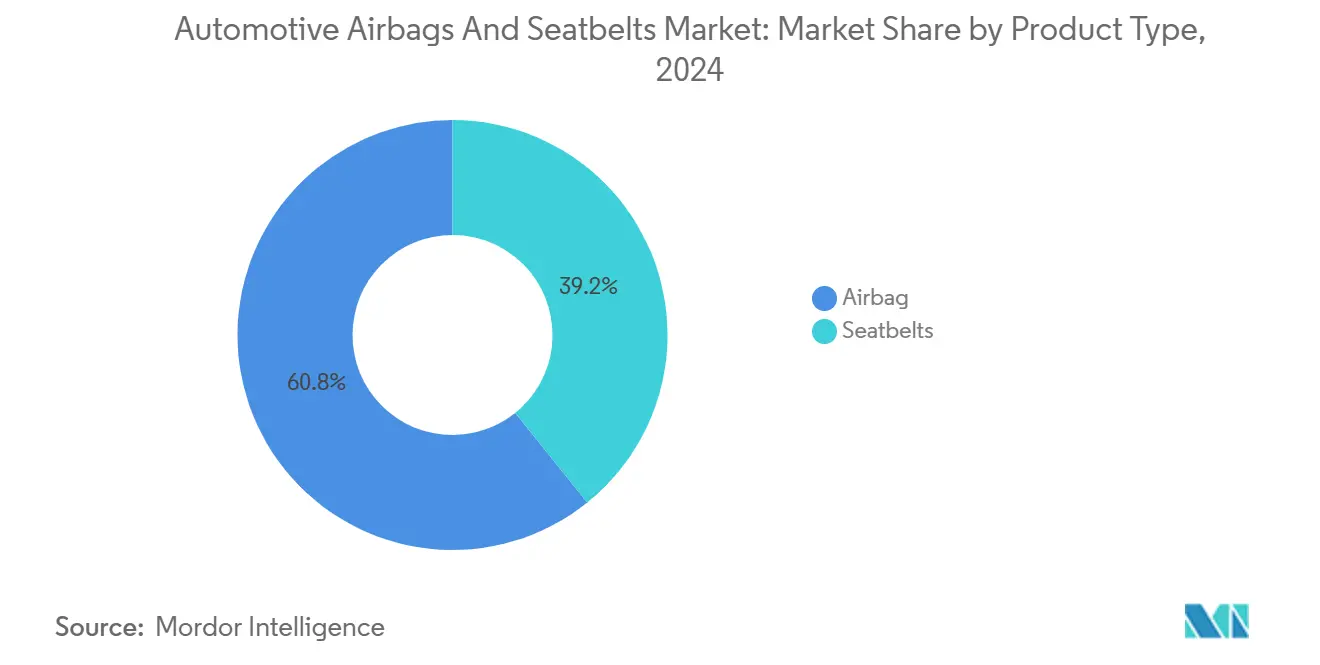

- By product type, airbags held a 60.78% share of the automotive airbags and seatbelts market in 2024, and are expected to record the fastest 9.41% CAGR through 2030.

- By vehicle type, passenger vehicles commanded 71.57% share of the automotive airbags and seatbelts market size in 2024; medium and heavy commercial vehicles are projected to post the highest 8.63% CAGR to 2030.

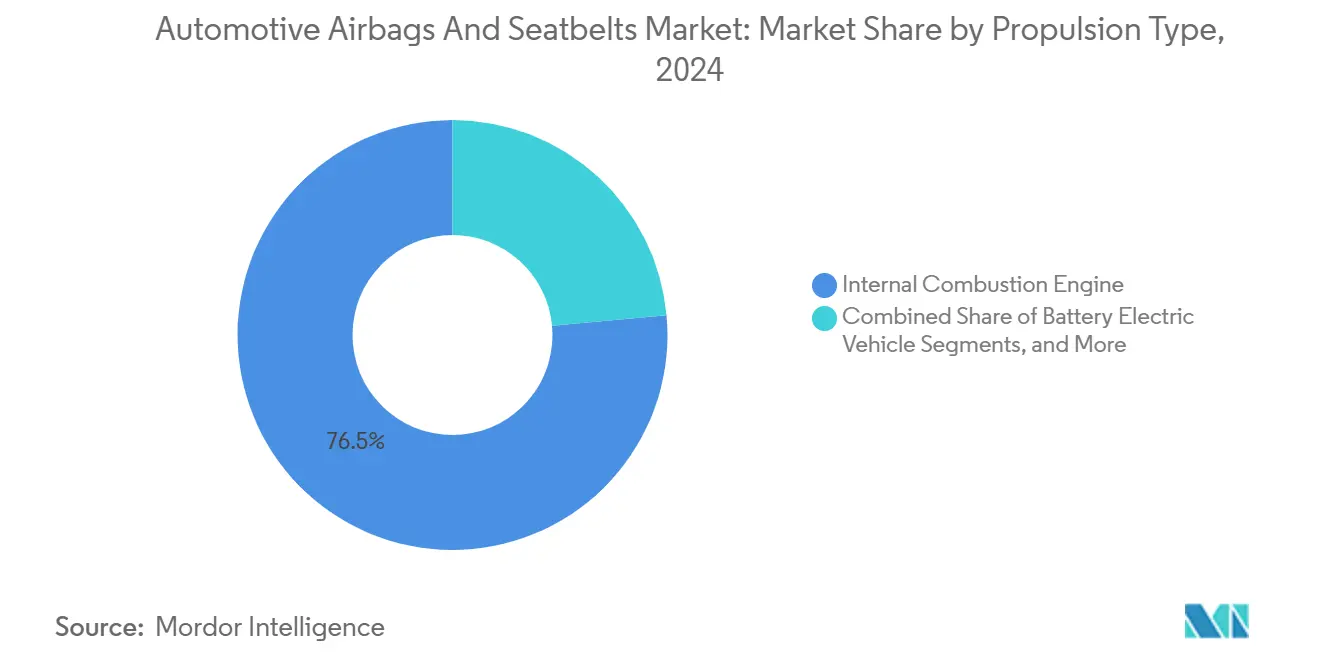

- By propulsion type, internal-combustion vehicles retained 76.47% of the automotive airbags and seatbelts market share in 2024, yet battery electric vehicles are forecast to climb at a 25.49% CAGR through 2030.

- By distribution channel, OEM sales captured 86.27% share of the automotive airbags and seatbelts market size in 2024, while the aftermarket is set to grow at 7.35% CAGR during the outlook period.

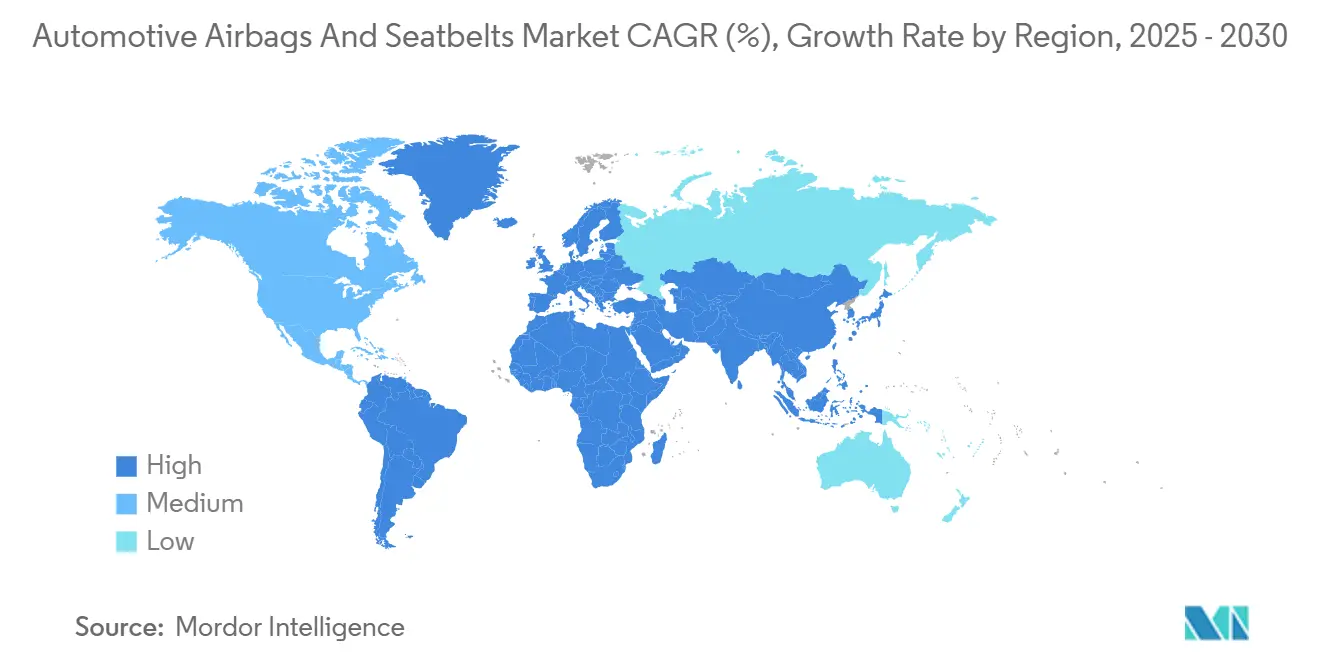

- By geography, Asia-Pacific led with 38.24% share of the automotive airbags and seatbelts market size in 2024; South America is on track for the strongest 9.02% CAGR to 2030.

Global Automotive Airbags And Seatbelts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Passive-Safety Mandates | +1.2% | Global, with early adoption in EU and North America | Medium term (2-4 years) |

| Restraint Layouts Requirements in EVs | +0.9% | Asia-Pacific core, spill-over to North America and EU | Long term (≥ 4 years) |

| Modular "Restraint Domain" Architectures | +0.7% | Global, led by premium OEMs | Medium term (2-4 years) |

| Lightweight Thermoplastic Inflator Housings | +0.6% | Global, with emphasis in EU due to emissions regulations | Short term (≤ 2 years) |

| Tier-1/Tier-2 Reshoring | +0.4% | North America and EU primarily | Medium term (2-4 years) |

| Occupant-State Sensing | +0.3% | Premium segments globally, early adoption in Germany and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Global Passive-Safety Mandates

Authorities are enlarging crash-test matrices to cover far-side impacts, oblique collisions, and vulnerable road-user scenarios. Europe’s GB 18384-2020 for electric cars and the United States’ updates to FMVSS 208 and 305 set higher baselines for frontal, side, and battery-intrusion protection. OEMs must blend occupant-state detection, seat-integrated belt tensioners, and external airbags to meet rising scores. Broader scope lifts bill-of-materials value per vehicle while locking in complex validation regimes that deter low-cost entrants. As regulators link five-star ratings to insurance premiums, customer demand for advanced restraints further accelerates uptake.

Surge in EV Platforms Requiring New Restraint Layouts

Battery placements shift weight distribution and remove engine-bay crumple zones, forcing fresh restraint kinematics. Side-curtain airbags now deploy earlier while belt pre-tensioners coordinate with battery fire-mitigation logic. Continental has developed software that reorders deployment sequencing for cell-to-body structures, highlighting how EV traits spark incremental content and consultancy revenue[2]“Automotive Safety Systems,” Continental AG, continental.com. The transformation lifts engineering hours per program and sets the stage for software-over-the-air calibration fees that extend supplier revenue over a vehicle’s life.

OEM Drive for Modular "Restraint Domain" Architectures

Vehicle makers are consolidating sensors, firing circuits, power management, and diagnostics into single control modules. ZF LIFETEC’s seat-integrated active belt tensioner combines load-limiter, motor drive, and haptic-feedback functions in one scalable package[3]“ZF LIFETEC Integrates Active Belt Tensioner into the Seat,” ZF LIFETEC, press.zf.com. The modular approach cuts wiring up to 30%, speeds platform reuse, and supports digital feature unlocks. Suppliers with system-on-chip know-how and global homologation labs are best placed to capture these high-value contracts.

Lightweight Thermoplastic Inflator Housings Cut Cost and CO₂

Thermoplastic composites slash inflator mass by 15-20% compared with aluminum while sustaining burst-pressure thresholds. The shift matches EU fleet-average CO₂ caps and lowers raw-material spending. Autoliv’s composite housings handle intricate gas-flow paths that muffle deployment noise, a benefit prized in quiet EV cabins[4]“Front Center Airbag,” Autoliv, autoliv.com. Rollout begins with premium models but cascades to high-volume B-segment cars as molding economies improve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility | -0.8% | Global, with acute impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Recall Liabilities and Litigation Costs | -0.6% | Global, with highest exposure in North America | Long term (≥ 4 years) |

| Competitive Margin Squeeze | -0.5% | Asia-Pacific primarily, expanding to emerging markets | Medium term (2-4 years) |

| Fragmented Aftermarket Quality Control | -0.3% | South America, Africa, and Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility of High-Tenacity Nylon 66 and Aramid Yarn Prices

Spot quotes for automotive-grade nylon 66 rose by double digits during recent petrochemical outages, squeezing fabric converters that operate on annual pricing with OEMs. Dependency on a handful of North American monomer plants amplifies risk. Weaving mills trial polyester blends, yet process changes require fresh air permeability and tear testing to obtain OEM release. Autoliv piloted 100% recycled polyester cushions in 2024, illustrating how material substitution can ease cost swings without diluting performance.

Recall Liabilities and Litigation Costs Post-Takata Crisis

United States and Japanese courts now mandate multi-year data retention, traceability down to propellant lots, and higher product-liability coverage. Litigation expenses inflate overhead, raise break-even volumes, and deter newcomers. Established Tier-1s absorb costs through global volumes, but small fabric stitchers and inflator startups struggle to self-insure, limiting market dynamism.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Airbags Drive Innovation While Seatbelts Add Intelligence

Airbags dominated the automotive airbags and seatbelts market with a 60.78% share in 2024, thanks to broader fitment counts and a regulatory push for far-side and pedestrian protection. Curtain-side models posted the fastest 9.41% CAGR through 2030, propelled by Euro NCAP protocols that reward head-injury mitigation. Front airbags still provide the highest absolute unit volume, but growth rates cool as global installation nears 100% penetration. Next-generation lower-leg and far-side bags expand content per vehicle, and ZF LIFETEC’s active heel airbag exemplifies the pivot toward coverage of overlooked injury zones.

Seatbelts evolve from passive tethers into mechatronic interfaces that tighten pre-crash, slack for comfort, and provide haptic feedback in lane-keep assists. Electric pretensioners, motorized adjusters, and belt-in-seat designs spread from convertibles to crossovers as electrification frees packaging space. Five-point harnesses migrate to on-highway medium trucks where fleets seek to reduce driver injury downtime. These advances boost average selling prices despite slower headline growth versus airbags, helping sustain balanced revenue streams within the automotive airbags and seatbelts market.

By Vehicle Type: Commercial Segments Deliver the Fastest Expansion

Passenger cars retained 71.57% share of the automotive airbags and seatbelts market in 2024, reflecting global production scale and mandatory dual-front airbag rules in more than 60 countries. Yet medium and heavy commercial vehicles are set for an 8.63% CAGR through 2030, fueled by infrastructure spending and stricter driver-protection statutes on long-haul corridors. High cabin height alters kinematics in rollovers, spurring uptake of rollover curtains and seat-integrated belts.

Light commercial vans lie between passenger cars and trucks, offering fertile ground for cross-segment technology transfer such as driver-assist linked belt pulsing. Fleet operators embrace safety upgrades to cut insurance premiums and address driver shortages, while regulators in India, Brazil, and China mandate truck frontal-impact norms that mirror passenger-car stringency. The resulting uplift widens unit values and deepens addressable volume for suppliers keen to diversify beyond the saturated car pool in the automotive airbags and seatbelts market.

By Propulsion Type: Battery Electric Designs Reshape Restraint Needs

Internal-combustion models still accounted for 76.47% share of the automotive airbags and seatbelts market size in 2024, but battery electric vehicles will climb at a 25.49% CAGR through 2030, as global zero-emission targets gain force. Battery packs under floors shift energy-absorption pathways, leading OEMs to specify multi-stage side curtains and ultra-quiet inflators that match low NVH cabins. Hybrid and plug-in variants demand dual compliance for both engine-forward and skateboard layouts, complicating calibration libraries.

Fuel-cell prototypes remain niche yet create unique burst-pressure and hydrogen-storage safety cases that test material durability. Ford’s patents for autonomous seating emphasize how propulsion and autonomy mutually reinforce innovation cycles, opening white-space vectors for novel airbag geometries. The propulsion lens thus stands central to forecasting bill-of-material variation inside the automotive airbags and seatbelts market.

By Distribution Channel: Aftermarket Gains Traction but OEMs Hold Sway

OEM channels captured 86.27% share of the automotive airbags and seatbelts market in 2024, as integrative safety parts leave little room for non-authorized sourcing. Over-the-air diagnostics and serialization tie inflators and modules to vehicle VINs, locking many replacement jobs into dealer networks. Still, the aftermarket will log a 7.35% CAGR through 2030, mostly from airbag control unit renewals after minor crashes and seatbelt part aging in warmer climates.

Emerging market regulators now require certified replacement parts, curbing counterfeit inflators that once flowed through informal channels. Tier-1s establish branded service lines and e-catalogs to secure lifecycle parts revenue, while insurers under total-loss thresholds shift toward repair instead of write-off, expanding demand visibility. In mature regions, classic-car electrification programs also spur niche orders for updated restraints, adding depth to the automotive airbags and seatbelts market.

Geography Analysis

Asia-Pacific held a 38.24% share of the automotive airbags and seatbelts market, buoyed by massive output in China, India, and increasingly Indonesia. Regional governments upgraded NCAP protocols and tied tax incentives to higher safety scores, lifting average airbags per vehicle and encouraging seatbelt load-limiter adoption. Local champions rely on long-term supply contracts with Autoliv and ZF LIFETEC factories in Shanghai, Chennai, and Chonburi. Japan remains the R&D nucleus for low-noise inflators and vision-based occupant sensing, seeding technology that migrates to high-volume Chinese sport-utility models within two model years. Asia-Pacific’s scale advantages and rising domestic demand fortify its lead in the automotive airbags and seatbelts market, even as component reshoring to ASEAN alters traditional intra-regional flows.

South America is the fastest-growing region with a 9.02% projected CAGR to 2030. Brazil enacted new CONTRAN rules mandating side-impact airbags in all M1-category cars from 2026, pulling forward content growth. Argentina and Chile aligned tariff codes to ease cross-border module trade, while Mercosur safety harmonization reduces certification duplication. Improved macro conditions help fleets refresh aging trucks, catalyzing seatbelt retrofits in logistics corridors connecting São Paulo, Santiago, and Asunción. Suppliers who previously imported fully built modules now localize cutting and sewing to dodge freight costs, injecting fresh wage-linked competitiveness into the automotive airbags and seatbelts market.

North America and Europe share mature yet innovation-led profiles. The United States sees momentum from pickup and SUV rollovers, necessitating longer side curtains and seat-mounted center airbags. Canada’s harsh climate drives corrosion-resistant retractor housings, fostering niche metallurgical projects. Europe focuses on sustainable materials, spotlighting Autoliv’s recycled polyester cushions, which align with EU taxonomy criteria.

Competitive Landscape

The automotive airbags and seatbelts market remains moderately concentrated. Autoliv leverages end-to-end module capability, multi-continent plant footprints, and early moves into thermoplastic inflators. ZF Friedrichshafen integrates TRW’s restraint assets and ramping seat-integrated belt tensioners. Joyson Safety Systems leverages vertically integrated cut-and-sew alongside sensing electronics. The rest of the field includes Continental, Hyundai Mobis, and several Chinese entrants that gained scale through domestic mandates.

Strategic plays revolve around vertical integration, AI-ready sensing, and raw-material security. Autoliv partnered with a North American nylon spinner to co-develop bio-based yarn, whereas ZF Friedrichshafen opened an R&D center in Yokohama focusing on edge-accelerator chips for adaptive deployment. Chinese rivals accelerate patent filings in cold-gas inflators, aiming to cut propellant sourcing risk. Mergers center on bolt-on software firms that map occupant posture and facial metrics. Partnerships between Tier-1s and battery-pack makers appear, seeking to harmonize crash pulse with thermal runaway barriers, further widening moats against newcomers in the automotive airbags and seatbelts market.

Barriers to entry have risen since the Takata recall, heightening documentation depth, insurance coverage, and long-term escrow funds. While this shields incumbents, it also motivates OEMs to dual-source to avoid single-supplier dependencies. Competitive tension thus spurs price discipline yet rewards differentiated technology. Successful firms monetize data harvested from in-vehicle sensors, offering fleet insurers crash-severity analytics that translate into lower premiums.

Automotive Airbags And Seatbelts Industry Leaders

ZF Friedrichshafen AG

Joyson Safety Systems

Continental AG

Denso Corporation

Autoliv Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Mack Trucks detailed passive and active safety suites on the Mack Pioneer, adding front and side curtain airbags along with a high-strength steel cab.

- June 2025: Volvo Cars unveiled a multi-adaptive safety belt intended to optimize occupant protection across diverse body frames and seating positions.

- February 2025: ZF LIFETEC introduced the first Active Heel Airbag aimed at preventing foot injuries in future interior layouts, with series production slated for 2028.

- September 2024: ZF LIFETEC deployed hybrid physical-virtual test protocols in three global tech hubs to accelerate restraint development cycles.

Global Automotive Airbags And Seatbelts Market Report Scope

| Airbag | By Airbag Position | Front Airbags |

| Knee Airbags | ||

| Curtain/Side Airbags | ||

| By Component | Airbag Module | |

| Inflator | ||

| Crash Sensor and ECU | ||

| Airbag Fabric | ||

| Seatbelt | By Type | 2-Point |

| 3-Point | ||

| 5-Point | ||

| Belt-in-Seat (BIS) | ||

| Automatic Seatbelts | ||

| By Component | Webbing | |

| Retractor | ||

| Buckle | ||

| Tongue | ||

| Anchor Points | ||

| Pillar Loop / D-Ring | ||

| Pretensioner | ||

| Load Limiter | ||

| Locking Mechanism | ||

| Adjustable Shoulder Strap | ||

| Others (screws, etc.) | ||

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Internal Combustion Engine |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-in Hybrid EV (PHEV) |

| Fuel Cell EV (FCEV) |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Airbag | By Airbag Position | Front Airbags |

| Knee Airbags | |||

| Curtain/Side Airbags | |||

| By Component | Airbag Module | ||

| Inflator | |||

| Crash Sensor and ECU | |||

| Airbag Fabric | |||

| Seatbelt | By Type | 2-Point | |

| 3-Point | |||

| 5-Point | |||

| Belt-in-Seat (BIS) | |||

| Automatic Seatbelts | |||

| By Component | Webbing | ||

| Retractor | |||

| Buckle | |||

| Tongue | |||

| Anchor Points | |||

| Pillar Loop / D-Ring | |||

| Pretensioner | |||

| Load Limiter | |||

| Locking Mechanism | |||

| Adjustable Shoulder Strap | |||

| Others (screws, etc.) | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Medium and Heavy Commercial Vehicles | |||

| By Propulsion Type | Internal Combustion Engine | ||

| Battery Electric Vehicle (BEV) | |||

| Hybrid Electric Vehicle (HEV) | |||

| Plug-in Hybrid EV (PHEV) | |||

| Fuel Cell EV (FCEV) | |||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| Spain | |||

| Italy | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | India | ||

| China | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| Turkey | |||

| Egypt | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

How large is the automotive airbags and seatbelts market in 2025?

The market stands at USD 40.47 billion in 2025 and is projected to reach USD 52.02 billion by 2030 at a 5.15% CAGR.

Which region contributes the most revenue to the automotive airbags and seatbelts market?

Asia-Pacific leads with 38.24% of 2024 revenue, reflecting high vehicle production in China and India.

What segment shows the highest growth in the automotive airbags and seatbelts market?

Battery electric vehicle restraint systems are forecast to expand at a 25.49% CAGR, outpacing all other propulsion groups.

Why are curtain-side airbags growing quickly?

New far-side and vulnerable road-user tests by Euro NCAP and similar bodies deliver higher ratings for vehicles equipped with curtain-side airbags, driving 9.41% CAGR in that sub-segment.

What drives aftermarket expansion in restraint systems?

Aging fleets and rising awareness of safety upkeep in emerging markets push aftermarket revenue at a 7.35% CAGR through 2030.

Page last updated on: