Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

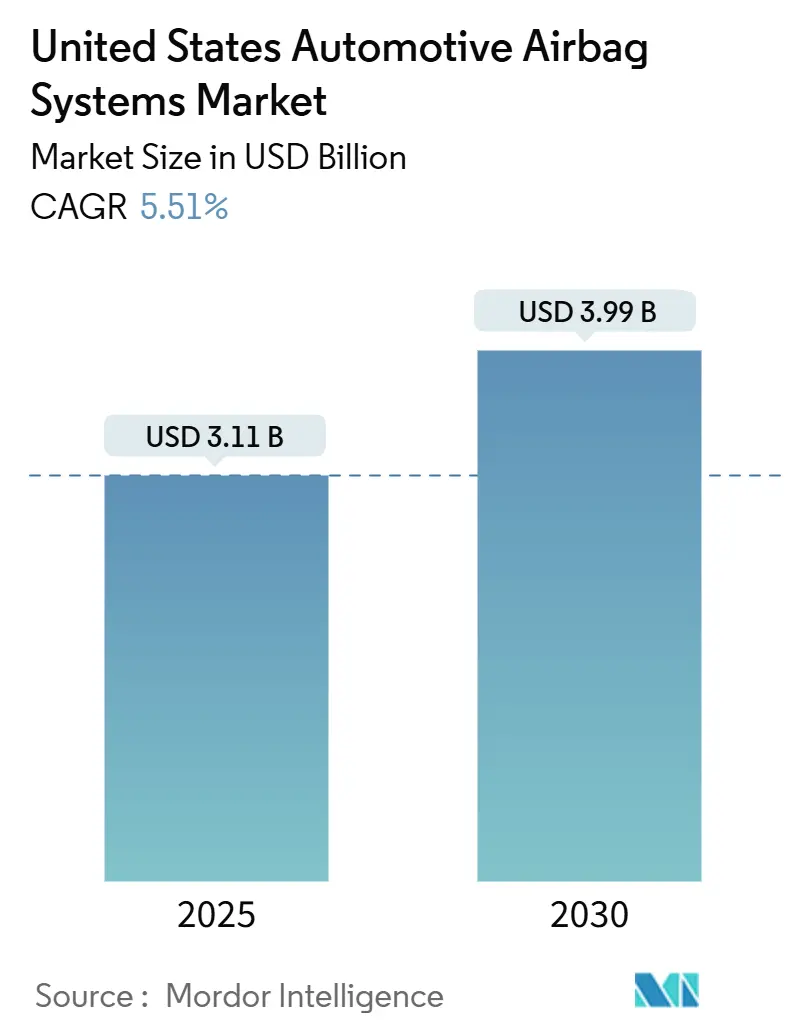

| Market Size (2025) | USD 3.11 Billion |

| Market Size (2030) | USD 3.99 Billion |

| Growth Rate (2025 - 2030) | 5.51% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Automotive Airbag Systems Market Analysis by Mordor Intelligence

The United States automotive airbag systems market size is USD 3.11 billion in 2025 and will rise to USD 3.99 billion by 2030, reflecting a 5.51% CAGR (2025-2030). Growth rests on stricter crash-test rules, the heavier mix of SUVs and pickup trucks, and the structural changes that battery-electric skateboard platforms impose on restraint packaging. A crash-rating competition among automakers, advances in semiconductor technology that enable electronic control units to operate in single-digit milliseconds, and predictive-maintenance sensors that warn drivers before inflators degrade are all reinforcing demand. At the same time, production plateaus in Midwest assembly hubs and tighter scrutiny of inflator quality temper volume leverage, yet the combined effect still keeps the market on a clear mid-single-digit trajectory through the decade.

Key Report Takeaways

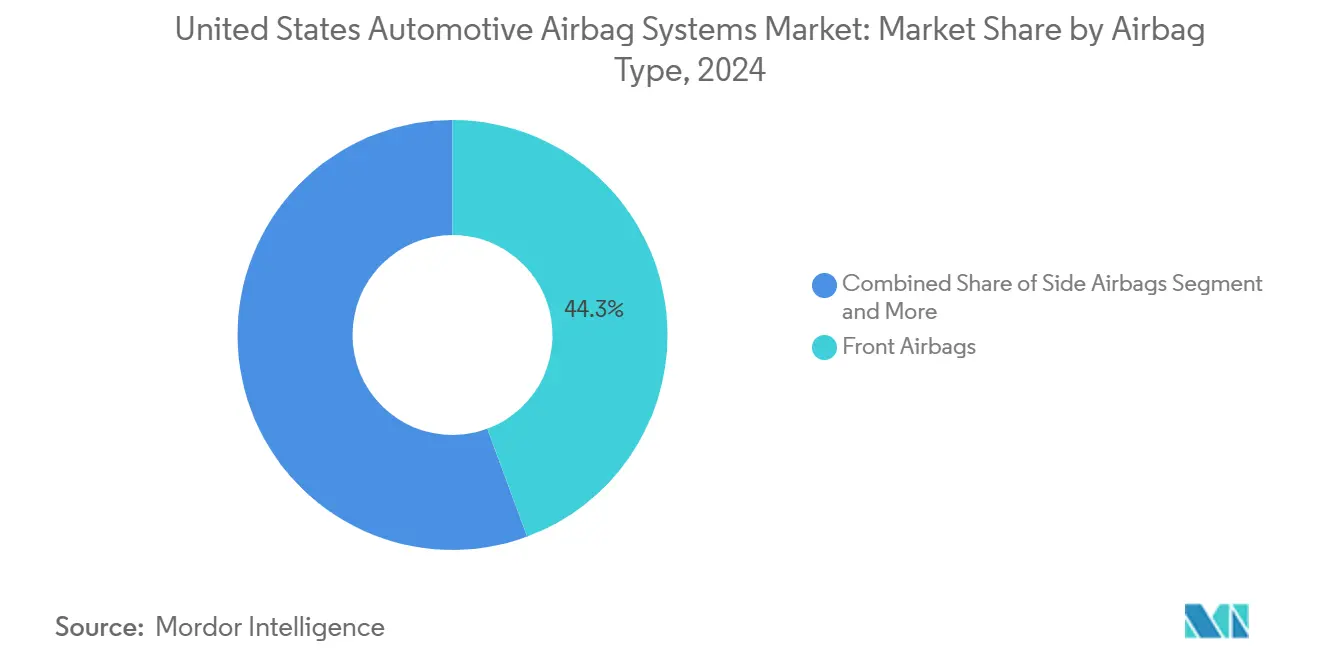

- By airbag type, front modules led with 44.34% revenue share in 2024, while curtain designs are projected to expand at a 7.22% CAGR through 2030.

- By vehicle type, passenger cars accounted for 63.73% of 2024 sales; however, medium and heavy commercial vehicles are expected to exhibit the highest forecast growth at a 6.46% CAGR to 2030.

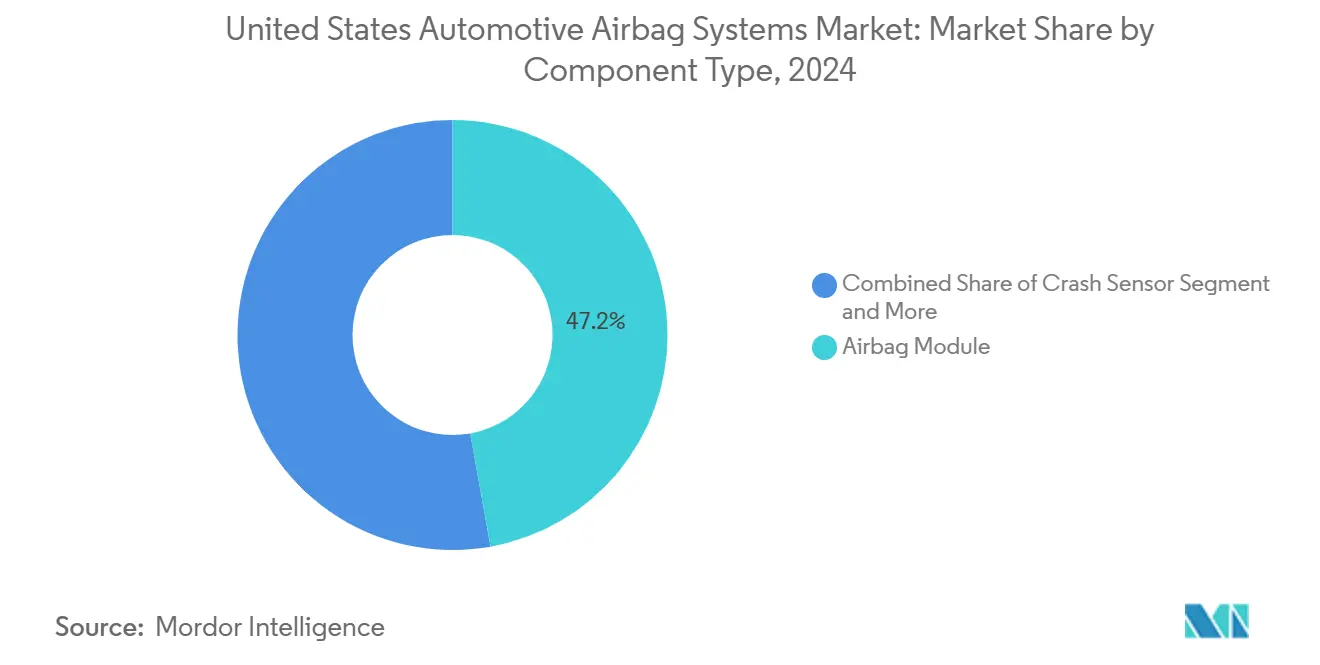

- By component, airbag modules captured 47.18% of 2024 revenue, and diagnostic sensors represent the fastest component line with a 6.92% CAGR outlook.

- By sales channel, the OEM route dominated with 86.58% of 2024 deliveries, while the aftermarket is expected to grow at a 6.19% CAGR as the fleet age lengthens.

- By region, the South region accounted for 34.22% of the 2024 turnover, whereas the West showed the quickest advance at a 6.32% CAGR through 2030.

United States Automotive Airbag Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SUV/Light-Truck Airbag Boost | +1.1% | South and West regions leading production shifts | Short term (≤ 2 years) |

| Safety Rating Pressure | +0.9% | National, with OEM prioritization in high-volume segments | Medium term (2-4 years) |

| FMVSS Airbag Mandates | +0.8% | National, with stricter enforcement in California and Northeast states | Long term (≥ 4 years) |

| EV Platforms Packaging Need | +0.7% | West and Northeast, with spillover to Midwest battery-belt states | Medium term (2-4 years) |

| Autonomous Cabin Airbags | +0.6% | West (California, Arizona) and select urban corridors | Long term (≥ 4 years) |

| Rear-Seat Inflatable Belts | +0.5% | National, with luxury-segment early adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

SUV and Light-Truck Mix Boosting Airbag Content

Light trucks and SUVs dominate U.S. retail sales, holding a significant share of the market. While compact sedans typically feature fewer airbags, light trucks and SUVs are equipped with more, enhancing safety. Consumers are willing to pay the additional cost, as the average transaction price accommodates the premium for the extra airbags. Geographically, the impact is notable, with major truck plants concentrated in states like Texas, Tennessee, and Alabama, creating strong demand near inflator facilities. This shift in vehicle mix significantly boosts the United States automotive airbag systems market.

Safety-Rating Pressure from NHTSA and IIHS

The IIHS has revised its moderate-overlap front test, now assessing performance with occupants seated closer to the panel [1]“Updated Moderate-Overlap Test,”, Insurance Institute for Highway Safety, iihs.org. This adjustment has significantly reduced chest injuries due to the implementation of dual-stage inflators with adaptive venting. Fleet buyers and insurers highly value a "Top Safety Pick" designation, prompting OEMs to allocate a larger portion of their passive-safety budgets to airbag tuning. Suppliers with in-house crash labs maintain a competitive advantage by quickly iterating prototypes. Meanwhile, smaller firms, despite offering lower base prices, face challenges in securing bids without validation capabilities. This competitive environment, driven by the pursuit of better ratings, continues to drive innovation and investment in the United States automotive airbag systems market.

EV Skateboard Platforms Creating New Packaging Demand

Battery-electric chassis reduces frontal crumple zones by approximately 18 cm. This adjustment causes inflators to reach full pressure more quickly compared to traditional combustion vehicles. Tesla’s dual-chamber airbag, adopted by Ford and Rivian, demonstrates how suppliers are developing faster gas profiles and reinforcing tethers around floor-mounted batteries. Finite-element modeling helps vendors identify those capable of maintaining fabric integrity during potential battery fires, even under extreme thermal loads. As the adoption of electric vehicles increases, the market is leveraging a specialized, higher-margin product stream associated with skateboard layouts.

FMVSS Mandates for Front & Side Airbags

Federal Motor Vehicle Safety Standards 208 and 214 remain the legal minimum, but the 2024 rulemaking proposes side-impact coverage for lighter crossovers that were previously exempt[2]“FMVSS No. 208 & 214 Proposed Amendments,”, National Highway Traffic Safety Administration, nhtsa.dot.gov. Automakers must retrofit torso and head bags by model year 2027, compressing design cycles and increasing per-vehicle restraint content. Southern plants that build compact SUVs see outsized tooling demand, and suppliers offering modular side-airbag cassettes win platform contracts that spread costs across multiple body styles. The regulation, therefore, adds volume certainty that underpins the United States automotive airbag systems market even as overall unit output levels off.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S. Vehicle Production Plateau | -0.6% | National, with acute impact in Midwest legacy assembly regions | Short term (≤ 2 years) |

| Recall Scrutiny Delays Programs | -0.4% | National, with concentrated risk for suppliers with single-source inflator lines | Medium term (2-4 years) |

| Lightweight Interiors Complicate Deployment | -0.3% | West and Northeast, where luxury and EV segments adopt advanced composites | Medium term (2-4 years) |

| ECU Costs Rising with Chip Shortages | -0.5% | National, with supply-chain bottlenecks in Asia-sourced microcontrollers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

U.S. Light-Vehicle Production Plateau

The total domestic output has remained stable, with expectations of limited growth as automakers continue to focus on improving margins rather than increasing production volumes. Utilization rates in manufacturing plants across the Midwest have declined, prompting suppliers to suspend airbag production lines. This has resulted in higher per-unit overhead costs and a reduction in profit margins. Companies with operations in Mexico have managed to alleviate some of the challenges. Still, the overall constraints continue to slightly impede the growth trajectory of the United States automotive airbag systems market.

Recall-Driven Supplier Scrutiny and Program Delays

Several ongoing investigations by the NHTSA are covering millions of vehicles, significantly extending module validation timelines. The prolonged humidity, vibration, and accelerated-aging tests now incur substantial costs per variant. These delays in revenue recognition have also driven a notable increase in insurance premiums. Reflecting the challenges posed by stringent oversight, some Tier-2 inflator firms have exited the United States market, unable to address the financial pressures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Airbag Type: Curtain Modules Gain as Oblique Tests Proliferate

Front airbags, already mandated, dominated the market with a 44.34% share. Curtain airbags, projected to grow at a 7.22% CAGR, are set to capture an even larger portion of the market by 2030. Dual-chamber designs, which maintain pressure for six seconds, comply with rollover and oblique-impact regulations. Additionally, integrated acoustic damping reduces cabin noise, enabling automakers to command premium prices. While side-torso bags hold the third position in the market, their growth is slowing. This is largely because they're now standard in nearly every new vehicle, shifting focus to center airbags designed to mitigate far-side impacts.

Curtain technology is also adapting to battery-EV packaging, positioning occupants closer to the vehicle's edge and heightening the risk of pole-crash injuries. Suppliers in the market, particularly those focusing on curtain modules, are now incorporating reinforced tethers and low-permeation fabrics. These enhancements are designed to withstand exposure to 400 °C battery fires, allowing them to tap into more lucrative sub-niches. On another note, knee airbags have reached a plateau. Crash-rating agencies have determined only marginal benefits over optimized belt geometry. As a result, OEMs are reallocating resources towards rear-seat inflatable belts, which are anticipated to gain traction by the end of the decade.

By Vehicle Type: Commercial Fleets Drive MHCV Penetration

Passenger cars still generate the majority of the United States automotive airbag systems market size, accounting for 63.73% of the 2024 revenue. In contrast, medium and heavy commercial vehicles are projected to register a 6.46% CAGR to 2030, reflecting regulatory signals that FMVSS 208 will be expanded to include Class 6–7 trucks. Fleet operators pre-install bags ahead of mandates to lower liability claims, creating an early mover advantage for Tier-1s that already qualify modules for harsher vibration loads.

Light-commercial pickups weighing below 4,500 kg continue to grow, benefiting from consumer crossover overlap. Bus penetration remains minor but is expected to increase when federal funding rules for transit coaches require frontal bags by 2027. Collectively, these non-passenger categories diversify revenue and hedge suppliers against the decline of sedans, reinforcing medium-term resilience for the market.

By Component: Diagnostic Sensors Embed Predictive Intelligence

Airbag modules accounted for 47.18% of the 2024 turnover, anchoring the core of the United States automotive airbag systems market. Inflators hold a leading position but face challenges due to commoditization, as stored-gas formats achieve comparable performance and safety standards. Crash sensors maintain a significant share, while control units follow closely behind. Both categories are impacted by semiconductor shortages, which hinder immediate growth in unit production. Diagnostic sensors, which account for only 3%, carry the highest 6.92% CAGR because OEMs transmit health data via telematics that flag inflator deterioration weeks before a failure could occur.

Predictive intelligence reduces false-positive warnings significantly, resulting in substantial savings in goodwill repairs. In the market, suppliers incorporating machine learning into their offerings not only achieve higher pricing but also secure ongoing royalties from software updates. This evolution shifts airbags from standalone hardware products to continuous software revenue generators, enhancing margins compared to traditional module assembly.

By Sales Channel: Aftermarket Gains from Fleet Aging

The OEM channel represented 86.58% of 2024 value, underpinned by contractual bundling of airbags with telematics and warranty terms that deter substitution. Aftermarket share is projected to post a robust 6.19% CAGR through 2030 as the national fleet age reaches 12.6 years. Independent collision shops purchase remanufactured modules at half the OEM price, capitalizing on cost gaps in vehicles beyond the factory warranty.

Quality concerns limit runaway growth; the NHTSA recalled three batches of aftermarket modules in 2024, highlighting the risk of counterfeit parts. Certified-remanufactured lines that meet OEM specifications and carry limited warranties appeal to insurers, allowing reputable suppliers to expand their presence in the United States automotive airbag systems industry without regulatory backlash. Over time, telematics-linked diagnostics may route post-crash parts orders directly to approved vendors, thereby tightening control while maintaining a slice of the aftermarket.

Geography Analysis

The South secured 34.22% of 2024 sales, reflecting 3.7 million light-vehicle builds concentrated in right-to-work states with SUV-heavy mixes. Inflator plants located in Texas and Tennessee have significantly reduced lead times, highlighting the region's importance in the market. Although growth has slowed due to a stabilization in assembly capacity, the increasing content per vehicle, driven by the popularity of multi-row SUVs, continues to support revenue generation.

The West logs the fastest 6.32% CAGR, propelled by California’s Advanced Clean Cars II rule requiring 68% zero-emission sales by 2030 [3]“Advanced Clean Cars II Final Rule,”, California Air Resources Board, arb.ca.gov. EV skateboard platforms built in Fremont and Nevada call for quicker-acting airbags with reinforced fabrics. In addition, the Phoenix and San Francisco robotaxi corridors serve as living labs for overhead and omnidirectional restraints, funneling pilot volume into Tier 1 roadmaps. Regulatory fragmentation, however, compels suppliers to stock dual inventories because California’s side-pole test runs at 40 km/h versus the federal 32 km/h standard, raising working capital.

The Northeast and Midwest together contribute a significant portion of revenue. However, their growth rate lags behind the national average as OEMs increasingly focus on southern regions. Despite this, Michigan's technical centers hold a majority of the nation's automotive R&D jobs, providing substantial influence during early design stages. This advantage secures a strong share of intellectual property in the market. However, challenges such as an aging workforce and underutilized plants hinder expansion, prompting suppliers to balance engineering hubs in the Northeast with more cost-efficient assembly operations in other areas.

Competitive Landscape

Autoliv, ZF Friedrichshafen, and Joyson Safety Systems dominate the United States automotive airbag systems market, controlling a significant share of the revenue. Autoliv, leveraging center-airbag successes for GM trucks, reported strong earnings in North America. ZF, focusing on innovation, acquired a majority stake in Sensata’s crash-sensor division, aiming to integrate lidar signals with restraint control, enabling seat belts to pre-tension milliseconds before an impact. Meanwhile, Joyson secured a major deal to supply curtain airbags for GM’s upcoming EV platform, featuring a dual-chamber design that inflates rapidly, meeting both rollover and oblique-crash standards.

Microcontrollers remain a critical factor for supply risks. ECU costs have risen significantly. Only suppliers with wafer contracts in Taiwan or plans for U.S. fabs are maintaining their margins. Asian inflator specialists are promoting stored-gas chemistries, which avoid propellant degradation. This innovation challenges established players on pricing in more commoditized segments. Additionally, software startups are gaining traction with cloud diagnostic platforms that predict failures before dashboard indicators activate. This development is creating a niche for data services within the traditional hardware ecosystem.

Patents related to seatbelt-integrated airbags and omnidirectional overhead modules reveal a divided strategy: Tier-1 giants are protecting high-volume OEM projects through vertical integration and collaborative development. Meanwhile, agile Tier-2 players are focusing on the aftermarket and commercial vehicle sectors, where cost is the primary driver for procurement. This dynamic creates a competitive yet stable market, one that values scale in modules while also rewarding specialized differentiation.

United States Automotive Airbag Systems Industry Leaders

Joyson Safety Systems

ZF Friedrichshafen AG

Autolive Inc.

Hyundai Mobis Co., Ltd.

Toyoda Gosei Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Volvo Trucks North America has announced that integrated side curtain airbags are now standard on its latest truck models for the North American market. This step highlights Volvo Trucks' ongoing leadership in the industry.

- July 2025: Mack Trucks unveiled the advanced safety technologies in its Mack® Pioneer, the company's top-tier highway truck. The Pioneer, reinforcing Mack's renowned dedication to durability and reliability, boasts a range of state-of-the-art safety features. These include front and side curtain airbags, a groundbreaking digital mirror system, and a robust steel cab engineered to surpass stringent safety benchmarks.

United States Automotive Airbag Systems Market Report Scope

The United States automotive airbag systems market report is segmented by airbag type (front airbag, side airbag, and more), vehicle type (passenger cars, LCVs, MHCVs, and buses and coaches), component (module, crash sensor, inflator, diagnostic sensor, control unit, and others), sales channel (OEM and aftermarket), and region (northeast, midwest, south, and west). The market forecasts are provided in terms of value (USD).

By Airbag Type

| Front Airbags |

| Side Airbags |

| Curtain Airbags |

| Knee Airbags |

| Center Airbags |

| Seatbelt Airbags |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

| Buses and Coaches |

By Component

| Airbag Module |

| Crash Sensor |

| Inflator |

| Diagnostic Sensor |

| Control Unit |

| Others |

By Sales Channel

| OEM |

| Aftermarket |

By Region

| Northeast |

| Midwest |

| South |

| West |

| By Airbag Type | Front Airbags |

| Side Airbags | |

| Curtain Airbags | |

| Knee Airbags | |

| Center Airbags | |

| Seatbelt Airbags | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles (LCVs) | |

| Medium and Heavy Commercial Vehicles (MHCVs) | |

| Buses and Coaches | |

| By Component | Airbag Module |

| Crash Sensor | |

| Inflator | |

| Diagnostic Sensor | |

| Control Unit | |

| Others | |

| By Sales Channel | OEM |

| Aftermarket | |

| By Region | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

How big is the United States airbag systems market in 2025?

It stands at USD 3.11 billion in 2025 and is on course to reach USD 3.99 billion by 2030.

What CAGR is forecast for United States airbag systems through 2030?

The market is set to grow at a steady 5.51% compound annual rate over 2025–2030.

Which airbag type will expand fastest over the next five years?

Curtain airbags are projected to post a 7.22% CAGR as IIHS oblique-impact tests raise side-head protection stakes.

Why are commercial vehicles important for future airbag demand?

FMVSS extensions and liability concerns push fleets to add airbags, driving a 6.46% CAGR in medium and heavy trucks.

Page last updated on: