Automated Border Control Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.74 Billion |

| Market Size (2031) | USD 5.76 Billion |

| Growth Rate (2026 - 2031) | 16.02% CAGR |

| Fastest Growing Market | Asia |

| Largest Market | Europe |

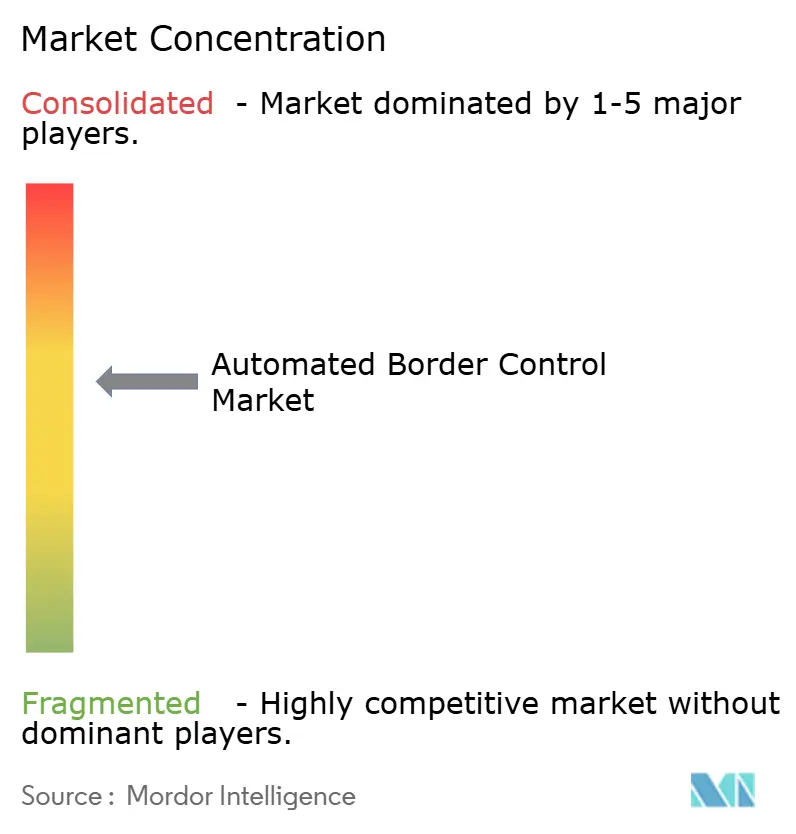

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automated Border Control Market Analysis by Mordor Intelligence

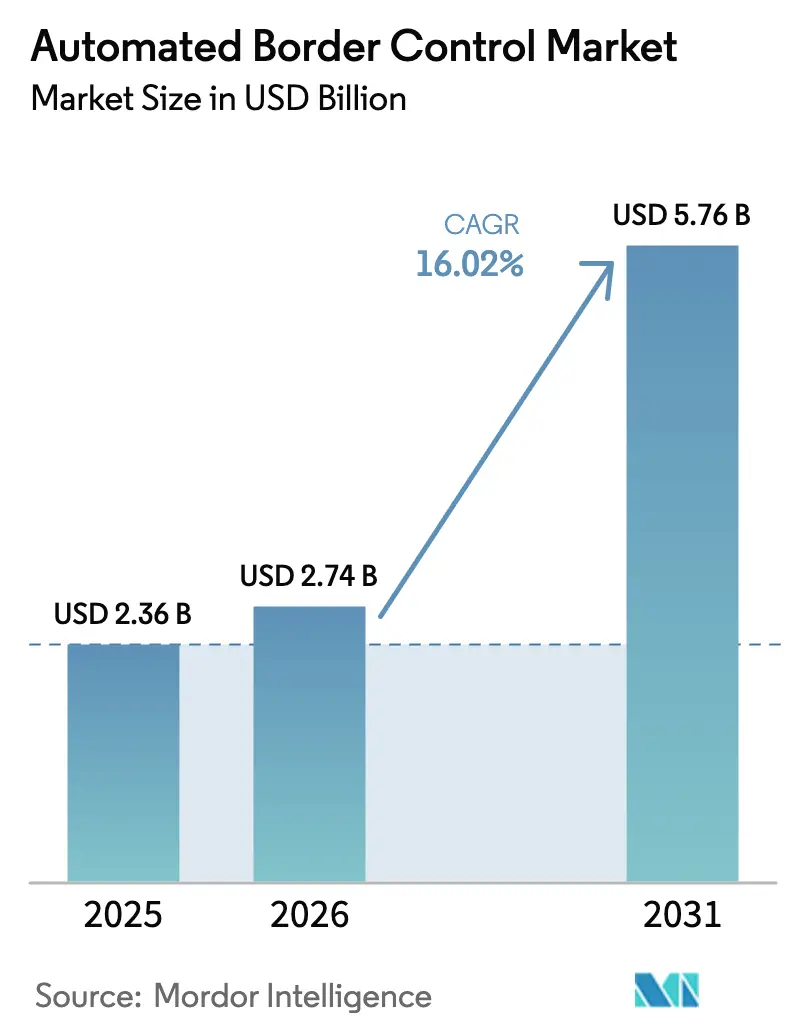

The automated border control market size was valued at USD 2.36 billion in 2025 and estimated to grow from USD 2.74 billion in 2026 to reach USD 5.76 billion by 2031, at a CAGR of 16.02% during the forecast period (2026-2031). Expansion synchronizes with three converging forces: mandatory biometric programs such as the European Entry/Exit System (EES), rising passenger numbers that have returned to pre-pandemic levels, and aggressive public-sector funding earmarked for smarter borders. Governments anchor procurement on systems that shorten processing times, strengthen identity assurance, and plug directly into national watch-list databases. Suppliers that combine hardware, cloud software, and artificial intelligence now win a larger share of multiyear contracts, while modular architectures lower rollout risk for emerging states. Geopolitical unrest continues to raise the threat profile at airports and land ports, accelerating adoption of facial-recognition and analytics engines that can screen travelers in seconds.

Key Report Takeaways

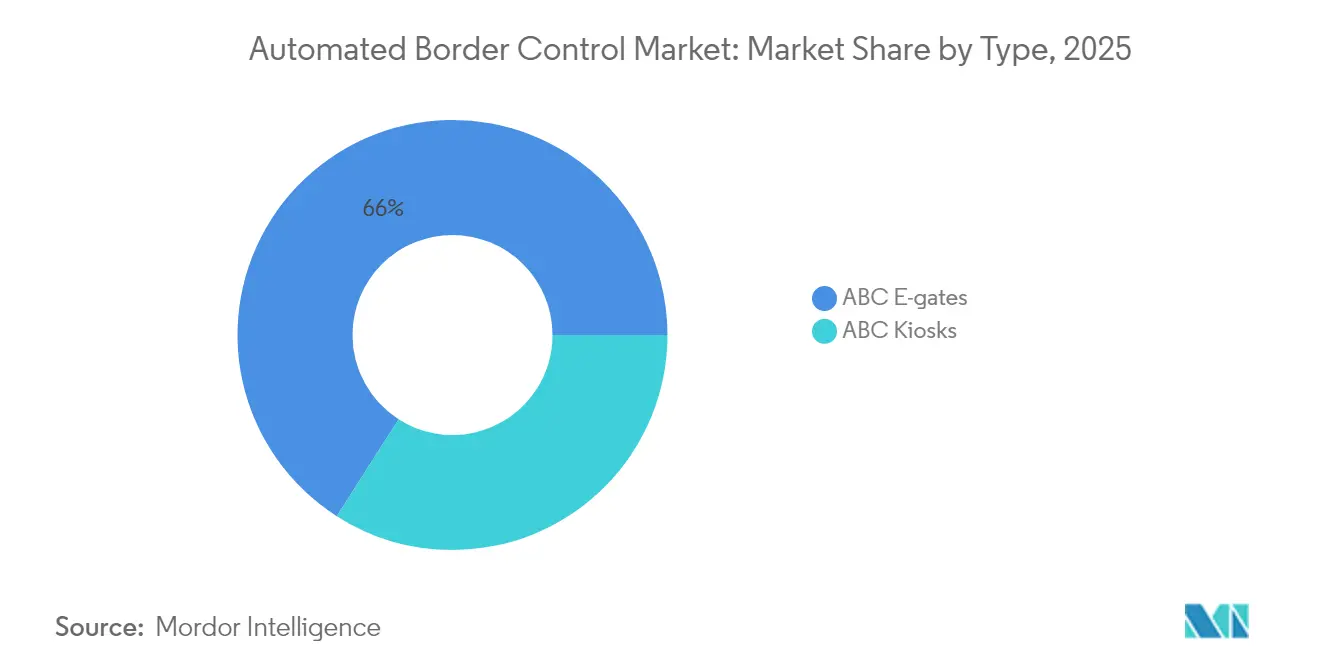

- By type, e-gates led with 65.95% revenue share in 2025; kiosks are projected to expand at a 17.12% CAGR to 2031.

- By offering, hardware captured 60.85% of the automated border control market size in 2025, whereas software is forecast to grow at 16.18% through 2031.

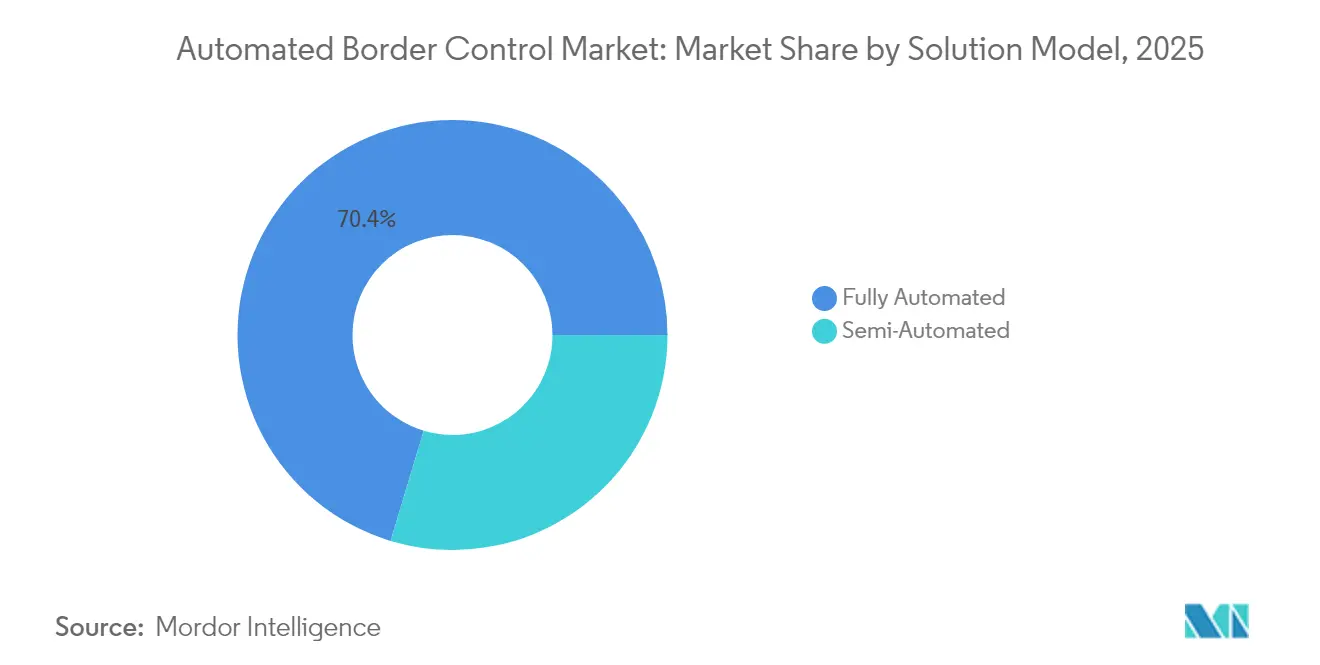

- By solution model, fully automated systems held 70.35% of the automated border control market share in 2025, while semi-automated models are advancing at a 16.46% CAGR.

- By mode of operation, one-step processing commanded 78.20% share of the automated border control market size in 2025; two-step systems will accelerate at 16.12% CAGR.

- By end-use application, airports represented 82.90% of revenue in 2025; land ports show the highest projected CAGR at 17.05% through 2031.

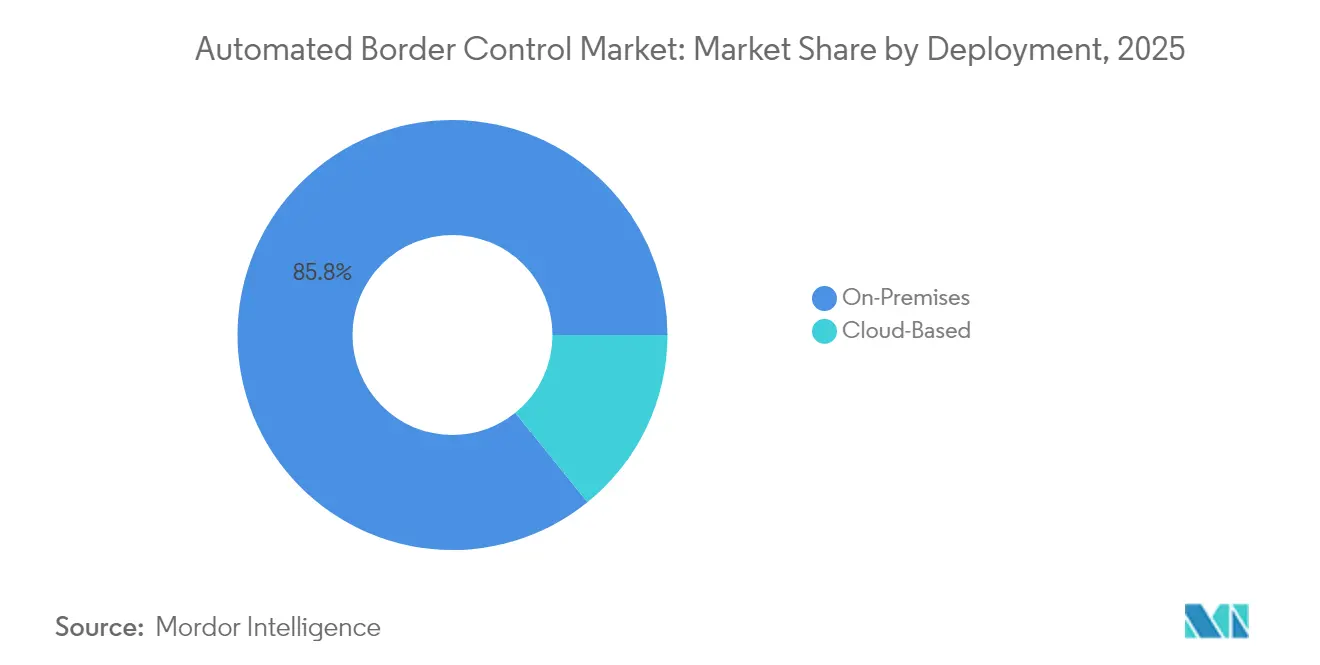

- By deployment, on-premises installations held 85.80% share of the automated border control market size in 2025, yet cloud platforms are growing at 16.62%.

- By throughput capacity, 200-400 passengers per hour systems led with 43.60% share, while >400 passengers per hour systems are forecast to expand at 17.08% CAGR.

- By region, Europe accounted for 42.95% of revenue in 2025, and Asia is the fastest-growing region with an 18.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automated Border Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing passenger traffic requiring seamless border processing | +3.2% | Europe and Asia-Pacific core; North America spill-over | Medium term (2-4 years) |

| Heightened government focus on counter-terrorism funding | +2.8% | North America primary; global influence | Short term (≤ 2 years) |

| Rising adoption of contactless biometrics for pandemic-resilient hubs | +2.1% | Global; early gains in Singapore, UAE, Australia | Medium term (2-4 years) |

| Mandatory EU Entry/Exit System roll-out | +4.5% | Europe primary; global standards influence | Short term (≤ 2 years) |

| AI-powered facial recognition throughput gains | +2.3% | Global; mega-airports | Medium term (2-4 years) |

| Airline–airport A-CDM programs in Asia | +1.8% | Asia-Pacific core; Latin America emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory EU Entry/Exit System Driving ABC Gate Installations

Scheduled for October 2025, the EES obliges 29 Schengen states to enroll third-country nationals’ biometrics through automated kiosks and e-gates. Member states have six months to achieve compliance after European Commission approval, stretching procurement into 2026 and beyond.[1]European Union, “Revised timeline for the EES and ETIAS,” travel-europe.europa.euSuppliers must enable direct integration with eu-LISA databases, prompting rapid upgrades from legacy gates to interoperable smart lanes. The regulation is already influencing adjacent markets as non-EU airports replicate EES technical specifications to maintain visa-waiver reciprocity.

Heightened Government Focus on Counter-Terrorism and Border-Security Funding

The United States allocated USD 60.8 billion in discretionary funding for homeland security in 2025, including USD 127 million channelled to Customs and Border Protection technology.[2]Department of Homeland Security, “Budget in Brief Fiscal Year 2025,” gsa.gov Canada earmarked CAD 355.4 million (USD 262 million) for traveller modernization projects. These budgets prioritise AI-enabled threat detection, cloud analytics, and multi-modal biometrics, underlining how fiscal stimulus accelerates the automated border control market.

AI-Powered Facial Recognition Improving Throughput at Mega-Airports

Singapore’s Changi Airport clears travellers in 10 seconds using advanced facial matching, processing 1.5 million visitors in the first 15 days after launch. NEC’s algorithm, verified at 99.88% accuracy by NIST, now operates in 80 airports.[3]NEC Corporation, “NEC Face Recognition Technology Ranks First,” nec.com Gateless corridors that scan up to 100 passengers per minute enable operators to meet surging traffic without expanding physical footprints.

Rising Adoption of Contactless Biometrics for Pandemic-Resilient Travel Hubs

Zayed International Airport will become the first facility to mandate biometric boarding across all checkpoints in 2025, replacing physical documents and reducing disease-transmission risk. UAE authorities enroll first-time visitors once, then re-use templates for future trips, demonstrating a lifecycle approach that cuts repetitive processing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biometric data-privacy concerns under GDPR and similar laws | -2.1% | Europe primary; global influence | Medium term (2-4 years) |

| High upfront CAPEX for emerging-nation border points | -1.8% | Africa, Latin America, Southeast Asia | Long term (≥ 4 years) |

| Spoofing and liveness-detection downtime risks | -1.2% | Global | Short term (≤ 2 years) |

| Legacy IT and passport databases | -1.5% | Africa, South America, Caribbean | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Biometric Data-Privacy Concerns under GDPR and Similar Laws

Strict retention rules oblige vendors to partition databases and deploy edge masking, inflating development cost and elongating certification cycles. The EU delayed the EES partly to finalise data-protection impact assessments, illustrating regulatory friction. North American agencies now publish privacy impact statements as standard, adding transparency but also administrative overhead. Although compliance raises barriers to entry, it ultimately favours incumbents with proven governance frameworks, shaping competitive dynamics in the automated border control market.

High Up-front CAPEX for Emerging-Nation Border Points

Land crossings in developing economies often lack fibre backbones and secure power, elevating installation budgets. Public-private partnerships are closing the gap, with reimbursable service agreements funding additional officer hours and equipment in the United States and pilot P3s emerging in Latin America. Vendors offering modular, solar-powered kiosks or automated border control as a service lower adoption hurdles, yet the pace remains slower than in developed regions, tempering global growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: E-gates Retain Leadership While Kiosks Accelerate

E-gates generated 65.95% of 2025 revenue, anchoring the automated border control market size at major hubs through high throughput and a compact footprint. Standardisation of ICAO compliance and multi-biometric modules has lowered integration risk, encouraging airports to bundle e-gates into terminal refresh programs. Modular designs shorten installation time, letting operators phase works without shutting lanes, a critical advantage during peak travel seasons.

Kiosks, registering a 17.12% CAGR, appeal to operators seeking flexible deployment in space-constrained settings or during leasehold upgrades. Units can be relocated if passenger flows shift, offering agility unmatched by fixed e-gate arrays. Software updates delivered over secure networks extend functionality across the installed base, ensuring continuous alignment with evolving risk models. As more land ports pilot kiosk programs, vendors address ruggedisation and weatherproofing, widening application scope and enlarging the automated border control market.

By Offering: Hardware Dominance Faces Rapid Software Upside

Hardware captured 60.85% of 2025 revenue, reflecting the upfront cost of biometric cameras, document readers, and obstruction-detect sensors. Precision optics and high-durability materials underpin mean-time-between-failure metrics demanded by regulators. Yet software is scaling 16.18% annually, outstripping headline growth. Cloud-native analytics offload heavy computation from edge devices, lowering hardware spec and operating temperature requirements. Authorities value real-time dashboards that correlate traveller risk scores with lane-level performance, letting duty managers re-allocate staff dynamically.

Subscription models are replacing perpetual licences, converting capital outlay into predictable operating expense. SaaS features like continuous threat-intel feeds and AIOps-based predictive maintenance elevate lifecycle performance, reinforcing the strategic gravity of software within the automated border control market.

By Solution Model: Full Automation Dominates, Semi-Automation Gains Traction

Fully automated lanes processed 70.35% of travellers in 2025 by combining document scanning, facial capture, and database checks in one pass. Operators cite labour-cost avoidance and predictable cycle times as core benefits. Semi-automated architectures, however, post a 16.46% CAGR because they let officers intervene when anomalies surface. Malaysia’s forthcoming Automatic Biometric Identification System embeds a human-in-the-loop layer for exceptional vetting.This dual-path strategy supports risk-based operations while sustaining throughput. It also positions vendors to monetise analytics modules that guide inspectors to outlier cases.

By Mode of Operation: One-Step Design Preferred

One-step systems owned 78.20% of 2025 revenue. Singapore’s passport-free corridor shows why: clearance fell from 25 seconds to 10 seconds, translating to higher gate turns and better passenger satisfaction. Two-step processes nevertheless log a 16.12% growth rate due to EES and certain Middle East deployments that separate enrolment from exit checks. The automated border control market now offers modular kits that can reconfigure from two-step to one-step as regulations lift.

Two-step models separate document authentication from biometric verification, erecting layered defences that frustrate sophisticated forgeries. ICAO promotes this architecture for high-risk crossings. Operators deploy dedicated enrolment kiosks followed by e-gates, ensuring complete capture even when traveller familiarity is low. Analytics triggered after the document step can alert officers ahead of the face match, shortening response time.

By End-Use Application: Airport Dominance Meets Land Port Momentum

Airports contributed 82.90% of 2025 revenue, leveraging controlled environments and predictable passenger profiles. Hub operators fold ABC investments into multi-billion terminal expansions, embedding lanes within architectural sightlines that support intuitive way-finding. Integration with airline DCS and bag-drop infrastructure allows kerb-to-gate biometrics, elevating dwell-time monetisation in retail concessions.

Land ports are advancing at 17.05% CAGR as cross-border commerce lifts vehicle and pedestrian volumes. Modernisation programs bundle biometric lanes with non-intrusive inspection to cut smuggling while maintaining flow. Seasonal traffic spikes around public holidays highlight the resilience benefits of automation. Combined, these trends extend the automated border control market well beyond aviation.

By Deployment: On-Premises Systems Preserve Security Sovereignty

On-premises arrays safeguarded 85.80% of 2025 installations because many states still require physical control over citizen data. Cloud, though, advances at 16.62% CAGR as encryption, sovereignty zones, and edge gateways ease security concerns. SAIC’s hybrid rollout fuses cloud analytics with local biometric caches for US border checkpoints, cutting maintenance visits while retaining data sovereignty.Commercial models now bundle software licences with usage-based fees, making cloud attractive for smaller states that lack data centres. This evolution widens market access and underpins future demand for continuous-delivery updates across the automated border control market.

By Throughput Capacity: High-Volume Lanes Gain Momentum

Systems rated for 200-400 passengers per hour accounted for 43.60% of demand in 2025, fitting most terminal footprints. However, >400 passengers per hour platforms rise at 17.08% CAGR. NEC’s gateless corridor authenticates 100 people a minute, cutting queue length by half. Operators chasing mega-hub status view such performance as a prerequisite for slot additions and airline partnerships.Lower-capacity options remain relevant at secondary airports and ferry terminals, maintaining diversity in vendor portfolios and sustaining total automated border control market growth.

Geography Analysis

Europe held 42.95% of 2025 revenue. Member states pour capital into EES-compliant kiosks and gates to avoid fines and passenger disruption. The Czech Republic alone ordered 58 kiosks and 94 e-towers from secunet for airport and land checks secunet. The UK allocated GBP 3.5 million (USD 4.7 million) to retrofit port lanes.Germany, France, Italy, and Spain each launched multiyear tenders, compelling vendors to ramp European assembly lines and local support teams.

Asia registers an 18.02% CAGR and will surpass Europe on annual installations by 2028. Singapore moved all checkpoints to automated lanes, processing 1.5 million travellers in 15 days. China’s Gongbei Port added 20 “card-free” channels for Guangdong-Hong Kong-Macao integration. India scaled Fast-Track Immigration to 21 airports after a successful Delhi pilot that enrolled 18,400 users. Japan commissioned NEC kiosks at Haneda to support 60 million-visitor targets.North America ranks third by spend but leads in per-site budgets. The Infrastructure Investment and Jobs Act funds 50 land-port modernisations. Canada invests CAD 1.3 billion (USD 959 million) in border security, including CAD 355.4 million for traveller modernisation. The automated border control market thus benefits from stable federal appropriations that guarantee contract visibility for prime contractors and niche biometric firms.

Regulatory Landscape

Automated border control (ABC) deployments are increasingly shaped by supranational digital-border programs and parallel privacy and biometric-use obligations. In Europe, the Entry/Exit System (EES) became fully operational across Schengen external border crossing points on 10 April 2026. This has locked in requirements for biometric registration and system interoperability with eu-LISA-run large-scale IT, and it is accelerating replacement and upgrade cycles for gates, kiosks, and associated back-end connectivity.

At the same time, governments are tightening the data layer that supports automated admissibility. Regulation (EU) 2025/12 mandates automated collection and transfer of Advance Passenger Information (API) for external border checks, supporting a single data entry approach across Member States. Outside the EU, the UK Home Office Pathway to Contactless is supported by the Immigration (Biometric Information etc.) (Amendment) Regulations 2025, while the United States advanced its biometric entry/exit legal framework through final rulemaking that updates 8 CFR parts 215 and 235. This reinforces the need for compliant biometric capture and processing at ports of entry.

Value Chain Analysis

The ABC value chain starts with component suppliers for biometric capture and document authentication (cameras, e-Passport readers, liveness sensors, and ruggedized lane hardware). It then moves into algorithm and software layers (biometric matching, orchestration, analytics, middleware/SDKs), and finally to prime contractors and integrators that deliver end-to-end lanes, connect to national watchlists, and harden networks for regulated environments. In Europe, eu-LISA operates the central EES infrastructure and defines the interfaces that national border authorities and operators must connect to. That dynamic shifts value toward interoperability tooling, integration services, and compliance-ready data exchange rather than standalone gate supply alone.

Downstream, airport, land-port, and seaport operators typically procure through public tenders or government-to-government frameworks, then depend on installation, certification, and lifecycle support (spares, software updates, and performance monitoring). In large rollouts, constraints often sit in integration and operations, including queue management, staffing for exceptions, and physical lane layout, rather than device availability. As automation expands beyond aviation, including US CBP enabling Mobile Passport Control for eligible pedestrians at select land crossings, deployment design also draws in customs or immigration agencies, carriers, and identity ecosystem partners that influence data-sharing requirements.

Competitive Landscape

The market shows moderate concentration. Thales, IDEMIA, NEC, and Vision-Box anchor global share by offering vertically integrated stacks covering enrolment, verification, and orchestration. IN Groupe’s planned acquisition of IDEMIA’s Smart Identity division would lift combined sales above EUR 1 billion (USD 1.06 billion), reinforcing the strategic premium on scale for sovereign-ID tenders. Consolidation allows portfolio cross-selling, including travel documents, civil IDs, and e-gate hardware, strengthening lock-in with government clients.

Differentiation shifts toward AI accuracy, liveness detection, and cloud orchestration. Smaller specialists such as Secunet exploit high-assurance software certifications to win EU public-sector contracts. Meanwhile, travel-tech giant Amadeus entered the space through its Vision-Box purchase, reflecting convergence between passenger-processing and border-control ecosystems. Supplier success increasingly depends on lifecycle support, data-governance compliance, and the ability to orchestrate heterogeneous fleets of kiosks and gates, shaping future rivalry inside the automated border control market.

White-space remains in emerging regions where funding gaps curb adoption. Vendors collaborate with development banks and infrastructure funds to structure availability-payment models that bundle maintenance and capacity-building. Such financing innovation can unlock latent demand, offering new revenue frontiers across the automated border control market.

Automated Border Control Industry Leaders

Atos SE

Veridos GmbH

Cognitec Systems GmbH

Magnetic Autocontrol GmbH

NEC Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A central opportunity runs through mandatory modernization cycles tied to smart-border rollouts and the need to retrofit legacy infrastructure to updated compliance baselines. With the EU EES reaching full operational status in April 2026, procurement is geared toward EES-aligned kiosks, e-gates, and back-end integration. It also adds demand for orchestration software that supports two-step enrollment and one-step clearance configurations across mixed fleets. Adoption benchmarks are tightening performance expectations as well: GDRFA Dubai reported millions of Smart Gate users in H1 2026 alongside sub-5-second average clearance times, which reinforces pull for higher-throughput lanes, improved liveness detection, and real-time operational analytics.

Another opportunity sits in land and multi-jurisdiction border expansion, where automation extends from passenger halls to pedestrian and vehicle workflows and raises requirements for ruggedization, new capture form factors, and cross-entity data exchange. Momentum also shows up in US CBP extending Mobile Passport Control to eligible pedestrians at select land border crossings, and in interoperability efforts such as a US DHS and CARICOM IMPACS memorandum aimed at multilateral biometric information sharing. Airports in growth corridors are adding capacity and refreshing passenger-processing stacks, including Manila International Airport deploying additional biometric eGates within a large modernization program and European airports replacing earlier-generation installations with next-generation ABC lanes. Together, these developments support a pipeline for vendors that can integrate hardware, software, and compliance governance under public-sector procurement constraints.

Recent Industry Developments

- April 2026: The European Union made the Entry/Exit System (EES) fully operational across Schengen external border crossing points, moving border processing from manual passport stamping toward biometric registration and digital verification. The change increases near-term integration and upgrade activity for EES-aligned kiosks, gates, and interfaces to eu-LISA-operated systems, and it raises interoperability requirements for vendors serving multiple Member States.

- December 2025: NEC partnered with emaratech to deploy six biometric smart gates at the crew immigration area in Dubai for flydubai. The deployment extends automated biometric processing into a specialized operational flow (aircrew), expanding the set of use cases that suppliers can address beyond standard passenger halls and reinforcing the role of local platform partners in Gulf deployments.

- November 2025: Bangladesh approved a direct government-to-government procurement involving Veridos GmbH for e-passport booklets and training under a project that includes Automated Border Control Management. The approval links national ePassport programs with downstream ABC readiness, supporting end-to-end identity infrastructure buildouts that can later scale to airports and land ports.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers automated border control systems used at regulated border checkpoints to verify travelers using electronic travel documents and live biometrics, which then enable self-service clearance through e-gates or kiosks.

Scope exclusions: Manual-only inspection booths and non-biometric perimeter surveillance systems are excluded from this sizing.

Segmentation Overview

- By Type

- ABC E-gates

- ABC Kiosks

- By Offerings

- Hardware

- Document Authentication System (DAS)

- Biometric Verification System (BVS)

- Face Recognition

- Fingerprint Recognition

- Iris Recognition

- Palm and Vein Recognition

- Software

- Border Management Software

- Middleware and SDKs

- Analytics and Reporting

- Services

- Installation and Integration

- Maintenance and Support

- Consultancy and Training

- Hardware

- By Solution Model

- Fully Automated

- Semi-Automated

- By Mode of Operation

- One-Step Process

- Two-Step Process

- By End-Use Application

- Airports

- Land Ports

- Seaports

- Rail Terminals

- By Deployment

- On-Premises

- Cloud-Based

- By Throughput Capacity

- Less than 200 Passengers/Hour

- 200-400 Passengers/Hour

- Above 400 Passengers/Hour

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia and New Zealand

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Kenya

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with travel and border flow indicators so the demand pool could be framed realistically before any pricing assumptions were applied. We reviewed public sources such as IATA passenger traffic releases, ICAO aviation statistics, Eurostat air transport tables, and UNWTO tourism dashboards, which help explain where throughput pressure is rising.

To align the security and identity side, we also referred to sources such as U.S. DHS and CBP publications, European Commission documents and eu-LISA program updates, and peer-reviewed biometrics and security journals for adoption patterns and typical performance requirements. Company filings, investor presentations, tender notices, and reputable press were used to map deployment announcements and service intensity, and patent databases were checked to understand where technology emphasis is shifting. A paid subscription for company financials and a global contracts and tenders database were used selectively to confirm deal timing and pricing ranges where public data was unclear. These sources are illustrative, and we used additional public references for cross-checks and clarification.

Primary Interviews and Surveys

Primary discussions were completed with airport operators, border agency stakeholders, system integrators, and component and software specialists so the model reflects how projects are specified and procured. We used these inputs to clarify which deployments count as ABC, how many lanes or gates are typically installed per site, and how pricing shifts with multimodal biometrics, document reader requirements, and maintenance scope across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 18% | APAC: 45% |

| Mid tier: 53% | Functional/Unit leaders: 33% | EMEA: 36% |

| Smaller Players: 19% | Managers: 49% | Americas: 19% |

Market-Sizing & Forecasting

The core sizing uses a top-down build where passenger traffic and cross-border movements are translated into addressable checkpoint volumes, then filtered by the share of lanes that are eligible for self-service processing. Once that demand pool is established, we apply adoption and replacement cycles for e-gates and kiosks to estimate annual spending.

To keep the result practical, selective bottom-up checks were run using sampled deployment counts by airport and border type, typical gates-per-lane layouts, and an average selling price range that is split between hardware, software, and ongoing services. Inputs that mattered most in this market included international passenger throughput trends, share of ePassport holders, biometric modality mix (face versus fingerprint or iris), procurement lead times visible in tenders, and service and maintenance attach rates after installation. Where public data was missing for smaller land and seaport sites, gaps were handled by using region-level penetration bands agreed during expert calls, and then stress-tested against known rollouts.

For forecasting, we relied on scenario analysis supported by short time-series smoothing for travel recovery and capacity expansion, since deployment timing can be lumpy and policy-driven. Growth paths were adjusted using interview consensus on project backlogs, refresh cycles for older gates, and expected shifts in pricing as standards and biometric performance requirements evolve.

Data Validation & Update Cycle

Outputs are validated by comparing implied spending per passenger processed, implied units shipped versus installation intensity, and regional splits versus publicly visible rollout plans. When a variance shows up, we revisit assumptions, re-check currency conversions, and re-contact selected experts if the change is tied to a new tender, program delay, or policy update.

Before sign-off, the model is reviewed in steps, first at the assumption level and then at the final totals, so outliers can be corrected with traceable reasoning. The report is refreshed annually, and interim updates are made when a material program award, regulatory change, or travel shock meaningfully shifts the near-term outlook. Right before delivery, a final analyst pass is completed so clients receive the most current view.

Mordor Intelligence's Automated Border Control Market Size Compared Against Other Published Estimates

It is normal to see different market sizes for automated border control because publishers may count different border automation items, pick different base years, or apply different ways to convert project wins into yearly revenue. Another reason is timing, since the market can move quickly when large airport programs are awarded or delayed.

The spread usually comes from refresh cadence and how pricing is carried forward, especially when systems shift from new installs to upgrades and service renewals. Currency timing also matters because contracts are often awarded in local currencies, and a rate taken at signing can differ from a yearly average rate used in a consistent model, which then changes the USD totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.74 B (2026) | |

| Global Consultancy A | USD 1.85 B (2025) | Uses an earlier base year and a shorter near-term view, which can undercount the later wave of airport modernization programs and the service revenue that follows initial deployments. |

| Industry Publisher B | USD 1.20 B (2024) | Likely reflects a narrower revenue capture and a different timing of contract conversion into recognized revenue, and the impact of exchange rate timing is not always standardized across regions. |

The table shows that year selection and revenue recognition timing can shift the number materially even when all publishers describe the same general concept. By refreshing exchange rates and ASP progressions on a scheduled cycle, and then re-checking them with recent tender and deployment signals, Mordor Intelligence keeps the total aligned to what is being installed and supported in that specific year.

Key Questions Answered in the Report

What is the current size of the automated border control market?

The market is valued at USD 2.74 billion in 2026 and is forecast to reach USD 5.76 billion by 2031.

Which region commands the largest share of automated border control installations?

Europe holds 42.95% of revenue due to mandatory EES compliance across 29 Schengen states.

Why are kiosks growing faster than e-gates?

Kiosks fit land ports and budget-constrained projects, posting a 17.12% CAGR compared with e-gates’ mature base.

How will cloud deployment affect adoption?

Cloud platforms grow at 16.62% CAGR by lowering maintenance costs and enabling centralized analytics, despite sovereignty hurdles.

What are the main barriers for emerging markets?

High upfront CAPEX and complex integration with legacy systems delay large-scale projects in Africa and Latin America.

How do privacy regulations influence technology choices in Europe?

GDPR and the EU AI Act drive demand for on-premises storage, encryption, and consent mechanisms, increasing system complexity and cost.

Page last updated on: