Epinephrine Autoinjector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

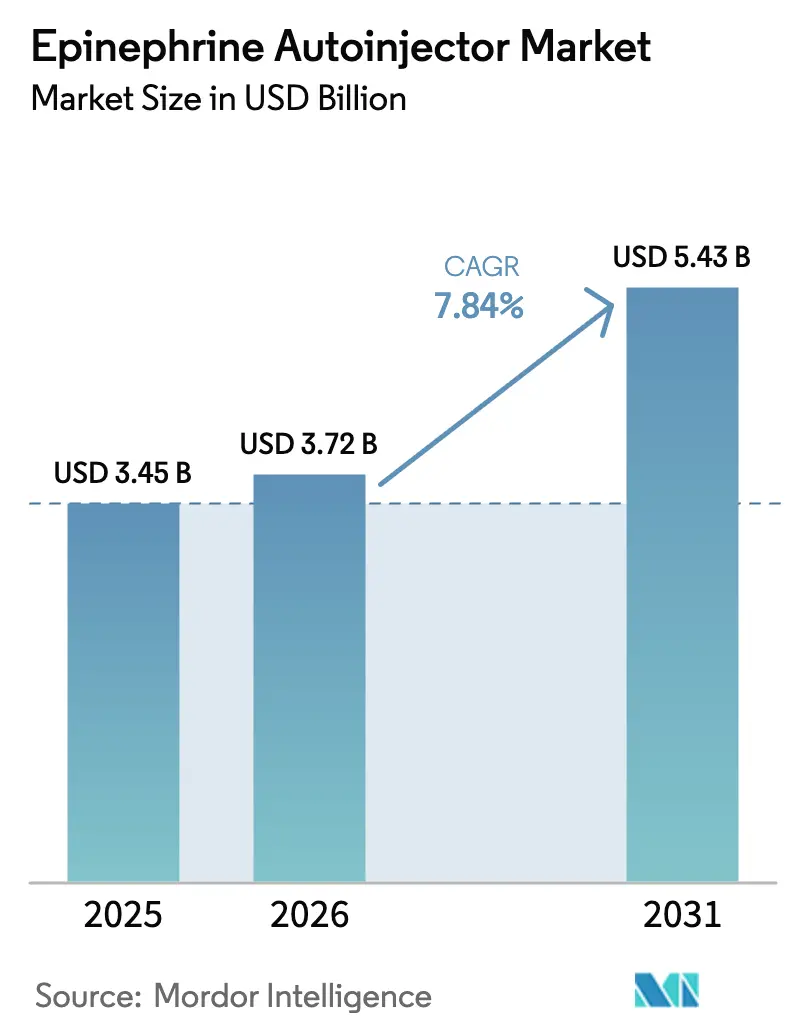

| Market Size (2026) | USD 3.72 Billion |

| Market Size (2031) | USD 5.43 Billion |

| Growth Rate (2026 - 2031) | 7.84% CAGR |

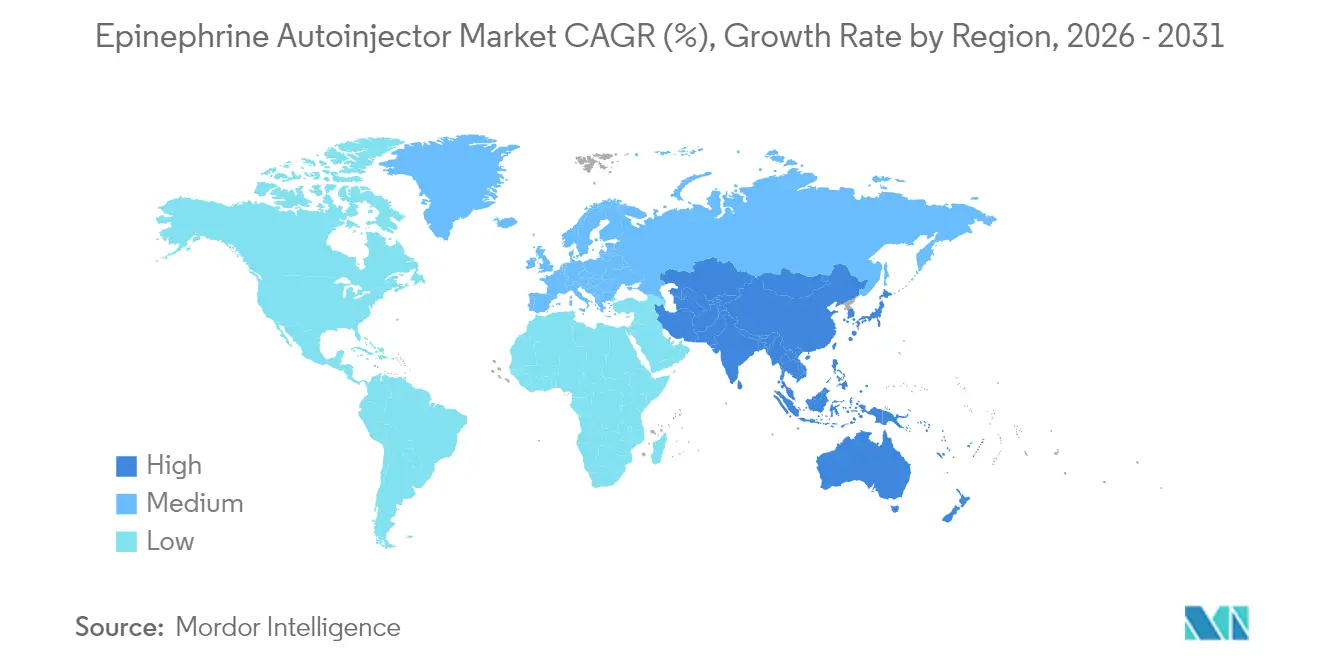

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

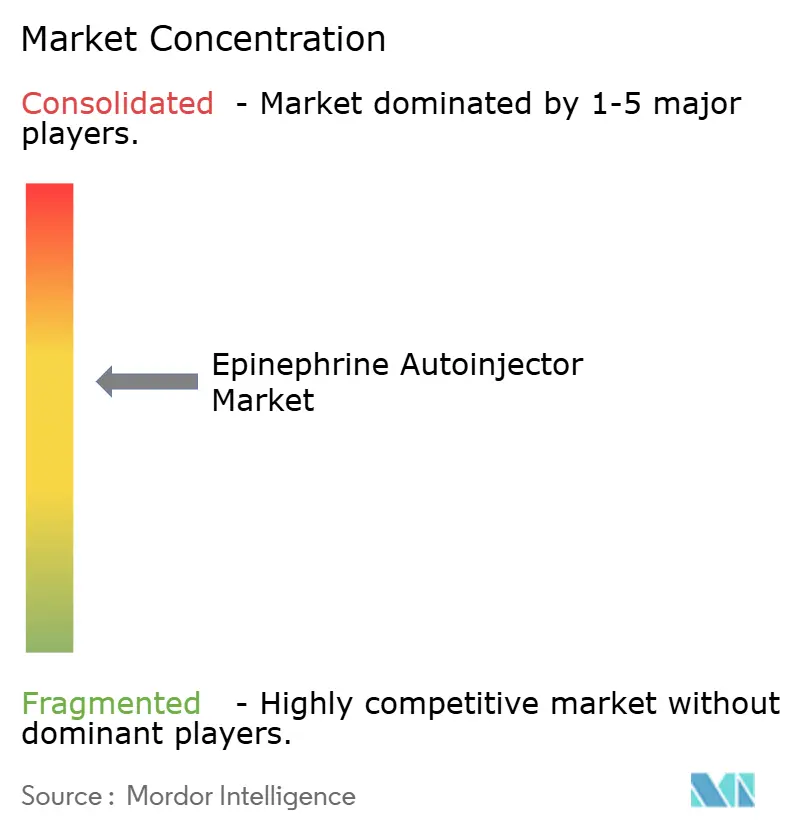

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Epinephrine Autoinjector Market Analysis by Mordor Intelligence

The epinephrine autoinjector market size was valued at USD 3.45 billion in 2025 and estimated to grow from USD 3.72 billion in 2026 to reach USD 5.43 billion by 2031, at a CAGR of 7.84% during the forecast period (2026-2031). The sustained rise stems from wider allergy prevalence, mandatory device stocking in public spaces and progressive reimbursement reforms that are lowering financial barriers for patients. Alternative delivery formats such as the needle-free neffy nasal spray have broadened treatment options rather than cannibalising demand, because they pull previously hesitant users into active care pathways. Production capacity is scaling in tandem: SHL Medical’s 2025 United States plant opening expands domestic autoinjector output, while contract development organisations are adding lines to hedge supply chain risk. State price-cap laws and pharmacy-benefit-manager formulary listings now support multi-pack purchasing, which encourages households to store devices at home, work and school. At the same time, sustainability commitments by device makers and integrated digital features that track expiration dates are reshaping product development priorities.

Key Report Takeaways

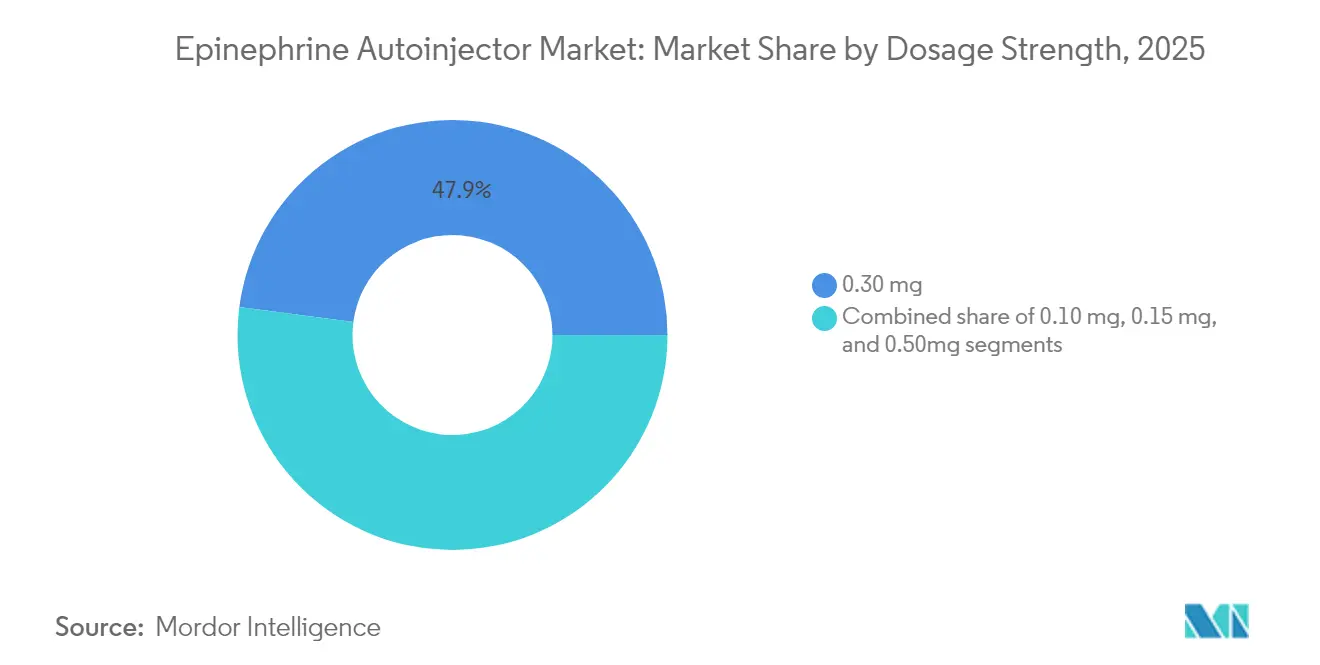

- By dosage strength, the 0.30 mg format led with 47.92% revenue share in 2025 and the 0.10 mg pediatric strength is advancing at a 13.62% CAGR.

- By age-group, individuals >12 years accounted for 60.88% of the epinephrine autoinjector market size in 2025; children <6 years represent the fastest segment with a 12.31% CAGR.

- By end-user, hospitals captured 46.12% revenue in 2025, while the schools & universities segment exhibits a 12.96% CAGR through 2031.

- By geography, North America held 42.25% of the epinephrine autoinjector market share in 2025; Asia-Pacific is projected to post the fastest 11.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Epinephrine Autoinjector Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Burden Of Severe Allergic Disorders | +2.1% | North America and Europe, rising in Asia-Pacific | Long term (≥ 4 years) |

| Favorable Regulatory And Reimbursement Ecosystem | +1.8% | North America and EU, expanding into Asia-Pacific | Medium term (2-4 years) |

| Expansion Of Generic And Authorized Generic Offerings | +1.5% | United States, Canada and Europe | Short term (≤ 2 years) |

| Growth In Point-Of-Care Self-Administration Culture | +1.3% | Developed markets worldwide | Medium term (2-4 years) |

| Integration Of Advanced Digital Health Features | +0.9% | North America and EU core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Institutional Stocking Mandates Across Public Spaces | +0.8% | North America and EU, selective Asia-Pacific adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Global Burden of Severe Allergic Disorders

Rapid growth in food, drug and environmental allergies is reshaping demand patterns. Approximately 40 million Americans report Type I allergic reactions each year. Pediatric incidence is climbing fastest, with 1 in 13 children now living with food allergies. As clinicians adopt earlier screening and community health campaigns stress rapid response, prescription volumes for rescue devices have multiplied. The dynamic is self-reinforcing: wider diagnosis raises market penetration, more devices in circulation improve outcomes and positive outcomes encourage additional screening. Manufacturers are responding with age-specific doses and needle-free formats, ensuring that new patient cohorts find a comfortable delivery option.

Favorable Regulatory and Reimbursement Ecosystem

Flexible regulators and payors are clearing a path for broader access. The FDA approved neffy nasal spray in 2024 and quickly added a pediatric indication in March 2025[1]U.S. Food and Drug Administration, “FDA Approves First Epinephrine Nasal Spray for Anaphylaxis,” fda.gov. National formularies at OptumRx, Cigna Healthcare and Navitus now include the product, together reaching about 20 million covered lives. New York State has capped the consumer price of a two-pack at USD 100 starting in 2026, removing a key barrier in a price-sensitive demographic[2]Food Allergy Research & Education, “New York Passes Autoinjector Price Cap,” foodallergy.org. Europe mirrored the trend by granting central approval plus eight-year data exclusivity for EURneffy, sending a clear signal that innovation addressing unmet need will receive regulatory support. Meanwhile, Medicare Part D classifies many generics as preferred, pushing down patient co-pays and lifting fill rates in senior populations.

Growth in Point-of-Care Self-Administration Culture

Public health messaging now frames anaphylaxis as a condition that demands instant action outside hospital walls. Human-factor studies recorded 100% correct dosing with neffy versus 35% errors for traditional injections in a controlled simulation. Fear of needles has long limited compliance; removing that obstacle unlocks a previously reluctant segment. Educational initiatives reinforce user confidence: the neffy inSchools program donates free units and trains personnel, while digital tutorials standardise technique across regions. Device innovation further cuts mis-fires through audible prompts, colour-coded caps and auto-retract needles, supporting the cultural shift toward everyday self-management.

Institutional Stocking Mandates Across Public Spaces

Legislation requiring devices in schools, universities, sports arenas and transport hubs is cementing baseline volume growth. The School Access to Emergency Epinephrine Act has inspired nearly every United States jurisdiction to recommend or mandate on-site units, bolstering a segment that already grows at a 13.50% CAGR. Implementation guidance from state health departments specifies staff training, storage conditions and liability protections, creating a turnkey procurement blueprint[3]New York State Department of Health, “School Epinephrine Stocking Guidance,” health.ny.gov. California’s Education Code sets similar standards and requires ongoing competency refreshers. Workplace programmes are following the same model, especially in hospitality and manufacturing, where allergen exposure risk is high.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently High Out-Of-Pocket Costs | -1.2% | Most acute in United States | Short term (≤ 2 years) |

| Vulnerabilities In Manufacturing And Supply Networks | -0.8% | Global, pronounced in Europe and Asia-Pacific | Medium term (2-4 years) |

| Emergence Of Non-Injection Epinephrine Delivery Modalities | -0.6% | Early adoption in North America and Europe | Long term (≥ 4 years) |

| Sustainability Concerns Around Disposable Devices | -0.4% | Led by European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistently High Out-of-Pocket Costs

Although generic expansion is narrowing list prices, many United States insurance plans carry high deductibles, leaving families with average prescription expenses of USD 328.03 and mean out-of-pocket costs of USD 31.90. Households typically purchase multiple packs to cover home, school and travel, compounding cost burden. Plan formularies also shift annually, forcing patients to navigate new authorisation rules. Assistance programmes cap co-pays for some, yet the uninsured remain exposed. Financial strain can delay refills past expiration, leaving patients unprotected during an emergency and limiting maximum market penetration.

Vulnerabilities in Manufacturing and Supply Networks

Device recalls expose the fragility of current supply. In 2024 Emerade 300 mcg and 500 mcg units were withdrawn after ISO 11608 tests found premature activation and delivery failures[4]Bausch & Lomb U.K. Ltd., “Emerade Recall Notice,” bausch.co.uk. With only a handful of sterile-filling facilities certified for lifesaving autoinjectors, any production halt tightens global inventory. New capacity is on the way: SHL Medical opened a Tennessee plant and BD invested USD 10 million to expand syringe output, but regulatory validation of fresh lines is lengthy. Until redundancy is established, temporary shortages and region-specific rationing remain plausible.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage Strength: Pediatric Formulations Drive Innovation

The 0.30 mg format dominated revenue with 47.92% share in 2025 because it targets adults and adolescents who account for most prescriptions. Yet the 0.10 mg pediatric dose advances at a 13.62% CAGR through 2031. The epinephrine autoinjector market size for this strength benefits directly from FDA approval of neffy 1 mg for children weighing 15-30 kg, which arrived in 2025. Pharmacokinetic studies show pediatric users achieve higher epinephrine plasma exposure from nasal delivery than adults, supporting weight-based titration. Manufacturers have redesigned plunger force and needle length for smaller musculature, improving tolerability. Clinics that treat severe infant allergies now maintain three strengths in inventory, widening reorder baskets.

As prescribers match dose to precise weight bands, the 0.15 mg bridge option retains relevance for children graduating from the lowest category. At the upper end, 0.50 mg caters to patients with mast-cell disorders or obesity. Production complexity rises as barrel diameter and spring force vary by SKU, raising tooling costs. Quality control protocols must keep dose-delivery variance tight, especially for pediatric units where under-dosing carries heightened risk. Successful vendors amortise engineering overhead by leveraging modular platform designs and common component families.

By Age-Group: Early Childhood Segment Accelerates

Users older than 12 years held 60.88% of the epinephrine autoinjector market share in 2025. Growth momentum now tilts toward younger cohorts, with children <6 years delivering the fastest 12.31% CAGR through 2031. Early allergy screening in pediatric wellness visits and childcare regulations that require rescue medications on site drive the surge. Caregiver surveys in Japan found that 57.6% of affected children always carry a device, up sharply after public health campaigns, yet there is still room for improvement. Device design that includes larger safety caps and bright colour cues makes administration faster for non-medical staff.

Children aged 6-12 years occupy a transitional band: they begin self-management but still need adult oversight. Adolescents often face peer pressure, so slim-profile injectors and smartphone connectivity encourage discreet carriage. Apps send refill reminders and enable GPS tracking if a unit is misplaced. These features yield higher adherence, supporting recurring replacement cycles that feed steady revenue into the epinephrine autoinjector market.

By End-User: Hospitals Lead, Schools Surge

Hospitals controlled 46.12% of revenue in 2025. Emergency departments insist on ready stocks across trauma bays and operating rooms. Automatic restock triggers within crash-cart software keep turnover brisk, anchoring baseline demand for the epinephrine autoinjector market. Outside acute care, schools and universities now show the fastest growth at 12.96% CAGR. State mandates plus donation programmes remove budget barriers, while liability shields empower trained staff to act promptly.

Homecare remains substantial: every prescription is usually a two-pack, and allergists frequently issue three or four packs so households can stage devices widely. EMS units need ruggedised devices with extended shelf life. Manufacturers gain competitive edge by offering universal mounting brackets and tamper-evident seals that meet ambulance regulatory codes. Workplace stocking represents an emerging micro-segment. Major airlines and large event venues have begun to add nasal sprays to first-aid cabinets, expanding point-of-care coverage and enlarging the epinephrine autoinjector market.

Geography Analysis

North America remains the largest contributor, delivering 42.25% of 2025 global revenue. The United States blends strong insurance coverage with proactive advocacy by groups such as Food Allergy Research & Education, driving high per-capita device counts. Federal aviation regulations and state price-cap measures add structural floors under demand. Canada’s universal pharmacare covers epinephrine for children in multiple provinces, smoothing volume across demographic tiers. Mexico’s market is smaller but growing as private insurers extend allergy benefits and urban clinics purchase stock for on-site emergencies.

Asia-Pacific is the fastest growing at an 11.32% CAGR through 2031. Diagnostic capacity is expanding rapidly in tertiary hospitals across China, Japan and South Korea. ARS Pharmaceuticals, through ALK-Abelló, filed for neffy approval in all three countries in 2024, signalling confidence in regulatory receptivity. Japan’s Ministry of Health already subsidises autoinjectors for paediatric food allergy, although utilisation studies reveal missed opportunities when children forget to carry devices. Awareness campaigns now target parents and sports coaches, reinforcing carriage behaviour. Australia, with long travel distances between medical facilities, regards self-administration devices as critical; its Pharmaceutical Benefits Scheme lists multiple strengths with generous subsidies.

Europe holds a mature but steady share. EMA approval of EURneffy in 2024 set a precedent for alternative delivery systems. Sustainability imperatives resonate: ALK-Abelló has pledged a 42% carbon-emission cut by 2030, and procurement consortia in Scandinavia now evaluate life-cycle impact scores alongside price alk.net. Germany’s statutory insurance reimburses autoinjectors at fixed reference prices, making generics competitive. The United Kingdom relies on both National Health Service procurement and private-school purchasing, creating dual channels. Italy and Spain have strengthened paediatric-food-allergy guidelines, prompting higher community use.

Emerging territories in the Middle East, Africa and South America still face affordability constraints yet benefit from foreign direct investment in private hospitals and from growing middle-class insurance uptake. Gulf Cooperation Council nations require autoinjectors in large public venues, and medical tourism hubs in the United Arab Emirates stock multiple strengths to cater to visiting patients. Brazil’s Anvisa updated anaphylaxis guidelines in 2024, foreshadowing tender opportunities for suppliers who can meet regional labelling and language requirements.

Competitive Landscape

The epinephrine autoinjector market shows moderate concentration. Viatris leads with EpiPen but reported USD 115.5 million in Q2 2024 sales, down from USD 127.5 million the prior year, indicating competitive erosion. Teva sells an authorised generic that absorbs cost-sensitive demand, while Amneal and Sandoz explore fill-finish partnerships to enter the category. ARS Pharmaceuticals holds first-mover advantage in needle-free delivery, and its licensing agreements grant ALK-Abelló exclusive rights in Europe and selected Asia-Pacific markets.

Mergers and capacity expansions are reshaping supply dynamics. Altaris combined Kindeva Drug Delivery with Meridian Medical Technologies in February 2025, creating a contract development organisation with more than 300 autoinjector patents and vertically integrated sterile filling capability. SHL Medical opened a Tennessee factory in 2025 to localise production, a strategic hedge against global logistics volatility. BD raised syringe and needle output by over 40% in its Nebraska plant, reflecting confidence that injectable formats will coexist with sprays.

Innovation differentiators now include smart-device integration, viscous-biologic compatibility and eco-friendly materials. Antares Pharma, in collaboration with Pfizer, progressed the QuickShot platform for high-viscosity drugs, illustrating spill-over potential from epinephrine into broader therapeutic areas. Device recyclability also gains traction; several manufacturers have piloted take-back schemes that recover plastic and metal components. First movers in circular design may secure preferential scoring in European public tenders, giving them an edge over laggards. The combined effect of technological, regulatory and environmental positioning will determine future ranking within the epinephrine autoinjector market.

Epinephrine Autoinjector Industry Leaders

-

Viatris Inc

-

Teva Pharmaceutical Industries Ltd.

-

Kaléo Inc.

-

Amneal Pharmaceuticals LLC

-

Sandoz

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ARS Pharmaceuticals launched neffy 1 mg nasal spray for children weighing 15–<30 kg in the United States, accompanied by a co-pay programme capping insured patient cost at USD 25.

- March 2025: The FDA approved neffy 1 mg for emergency treatment of Type I allergic reactions in children aged 4 years and older weighing 15–<30 kg.

- February 2025: Altaris announced the combination of Kindeva Drug Delivery and Meridian Medical Technologies, forming a leading global drug-device CDMO.

- January 2025: BD invested USD 10 million to expand United States manufacture of safety-engineered syringes and needles, raising capacity by more than 40%.

- January 2025: ARS Pharmaceuticals filed neffy 2 mg dossiers in Canada and the United Kingdom via partner ALK-Abelló.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the epinephrine autoinjector market as all factory-filled, spring-loaded devices that deliver a fixed dose of epinephrine intramuscularly for the emergency treatment of anaphylaxis, regardless of dosage strength or patient age. The market was valued at USD 3.45 billion in 2025 and is forecast to reach USD 5.15 billion by 2030.

Prefilled syringes, intranasal sprays, manual ampoules, and compounded kits are outside our scope.

Segmentation Overview

-

By Dosage Strength

- 0.10 mg

- 0.15 mg

- 0.30 mg

- 0.50 mg

-

By Age-Group

- <6 Years

- 6-12 Years

- > 12 Years

-

By End-User

- Hospitals

- Clinics

- Homecare Individuals

- Schools & Universities

- Emergency Medical Services (EMS)

-

Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed allergists, emergency physicians, pharmacy buyers, and device assemblers across North America, Europe, and Asia-Pacific. These conversations clarified real-world unit uptake by dosage, refill behavior, and the likely substitution rate once intranasal alternatives arrive, allowing us to fine-tune assumptions drawn from desk work.

Desk Research

We began with public health and trade data from sources such as the World Allergy Organization, the US FDA's device recall database, Eurostat trade codes for "epinephrine preparations," and the Anaphylaxis Registry in Europe, which together provided baseline incidence, import-export flows, and recall frequencies. Company 10-K filings, selected hospital procurement dashboards, and press releases on generic launches helped us trace price erosion patterns. Paid tools used judiciously included D&B Hoovers for manufacturer revenues and Dow Jones Factiva for device launch timelines. The sources cited illustrate our reference set and are not exhaustive.

Market-Sizing & Forecasting

We built an integrated top-down model by reconstructing global demand from prevalence-to-treated-patient pools, layering prescription penetration rates and average annual refills. Select bottom-up checks, namely manufacturer shipment roll-ups and sampled average selling price × volume, served as reality tests before finalizing totals. Key variables include: (1) documented anaphylaxis incidence per 100,000 population, (2) epinephrine pen refill frequency, (3) generic market share progression, (4) weighted average device ASP, and (5) regional reimbursement coverage ratios. Five-year forecasts employ multivariate regression that links unit demand to allergy incidence growth and generic penetration, with scenario analysis around potential FDA approval of nasal epinephrine. Gaps in bottom-up data were bridged through expert-validated proxy multipliers from comparable markets.

Data Validation & Update Cycle

Model outputs pass two analyst reviews, variance checks against independent prescription audits, and outlier reconciliation. Reports refresh each year, and we trigger interim updates when material events, major recalls, regulatory approvals, or price shocks, occur. A fresh validation sweep is completed before delivery.

Why Mordor's Epinephrine Autoinjector Baseline Commands Reliability

Published figures often differ because research firms pick dissimilar device definitions, dosing clusters, and price assumptions, and they refresh at different cadences.

Key gap drivers include whether prefilled syringes are counted, how aggressively generic ASP declines are modeled, and the frequency at which patient refill behavior is re-benchmarked. Mordor's scope mirrors only spring-loaded autoinjectors, uses interview-verified refill rates, and revises currency and incidence data annually, which keeps our baseline current.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.45 B (2025) | Mordor Intelligence | - |

| USD 2.83 B (2024) | Global Consultancy A | Counts select prefilled syringes and assumes slower generic uptake |

| USD 2.50 B (2023) | Industry Association B | Applies 2019-2021 ASP averages and omits Latin America in base year scope |

These comparisons show that once differing scope choices and pricing horizons are adjusted, Mordor's disciplined, annually refreshed model offers decision-makers the most transparent, reproducible baseline available.

Key Questions Answered in the Report

What is the projected value of the epinephrine autoinjector market by 2031?

The market is forecast to reach USD 5.43 billion by 2031.

Which region is growing the fastest in the epinephrine autoinjector market?

Asia-Pacific is expanding at an 11.32% CAGR through 2031 due to rising allergy awareness and pending approvals for needle-free sprays.

Why is the 0.10 mg dosage segment gaining momentum?

Early childhood allergy diagnoses and the approval of age-appropriate formulations such as neffy 1 mg underpin a 13.62% CAGR for this strength.

How are schools influencing demand for autoinjectors?

Legislative mandates and donation programs drive a 12.96% CAGR in the schools & universities segment as institutions must stock devices and train staff.

What factors limit wider adoption despite generic entry?

Persistent out-of-pocket costs, supply-chain recalls and sustainability concerns temper growth, although policy interventions aim to ease these pressures.

Are needle-free alternatives expected to replace traditional autoinjectors?

Needle-free sprays broaden choice and may capture share, yet premium pricing and the entrenched installed base mean injectable devices will coexist for the foreseeable future.

Page last updated on: