Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

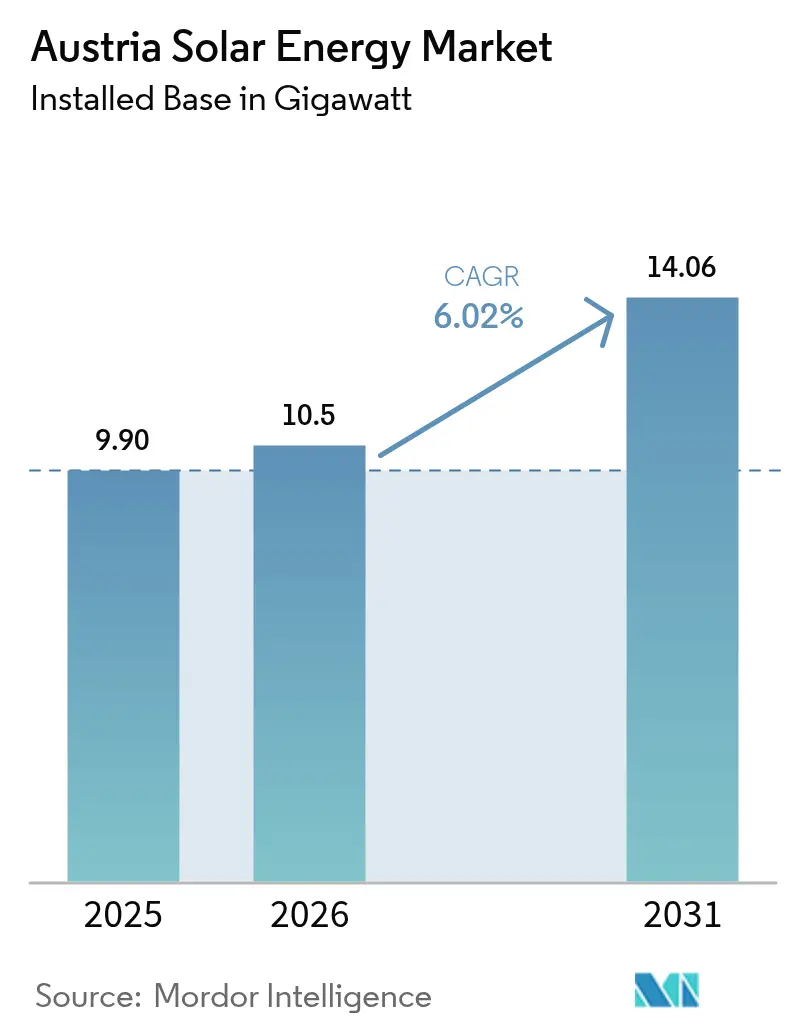

| Base Year Market Size (2025) | 9.90 gigawatt |

| Market Volume (2026) | 10.5 gigawatt |

| Market Volume (2031) | 14.06 gigawatt |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Solar Energy Market Analysis by Mordor Intelligence

The Austria Solar Energy Market size is expected to grow from 9.90 gigawatt in 2025 to 10.5 gigawatt in 2026 and is forecast to reach 14.06 gigawatt by 2031 at 6.02% CAGR over 2026-2031.

Momentum stems from the Erneuerbare-Ausbau-Gesetz mandate for 11 TWh of annual photovoltaic generation by the end of the decade and the country's alignment with the European Union's 2030 renewable electricity target. Rapid declines in module costs, a reinstated VAT exemption for systems below 35 kW, and a EUR 60 million rooftop subsidy have shortened residential payback periods to fewer than nine years. At the same time, agrivoltaic projects such as Burgenland Energie's 164 MW Tadten plant illustrate how dual land-use models circumvent traditional permitting frictions while adding new revenue streams. Distribution-grid bottlenecks, skilled-labor shortages, and rooftop fire-safety codes temper this outlook, yet have not reversed overall growth.

Key Report Takeaways

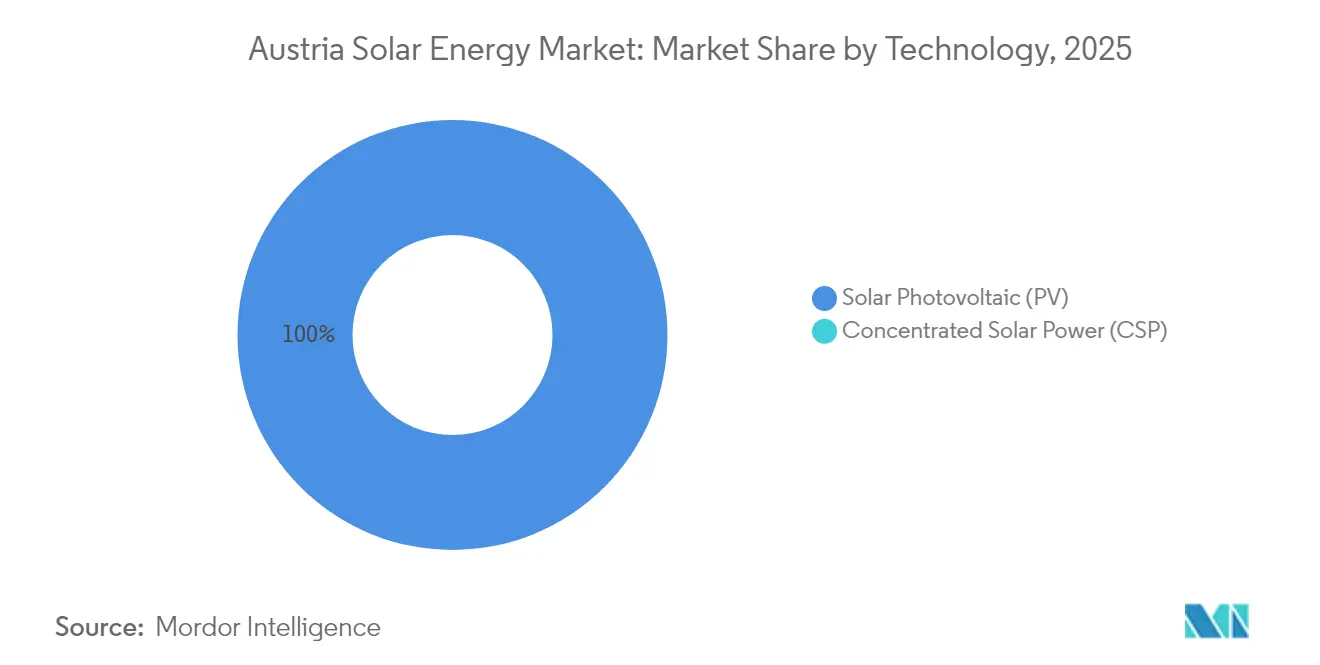

- By technology, solar photovoltaic retained 100.00% share of the Austria solar energy market in 2025 and is set to advance at a 6.02% CAGR through 2031.

- By grid type, on-grid systems held 99.28% of the Austria solar energy market share in 2025 and are forecast to grow at a 6.55% CAGR to 2031.

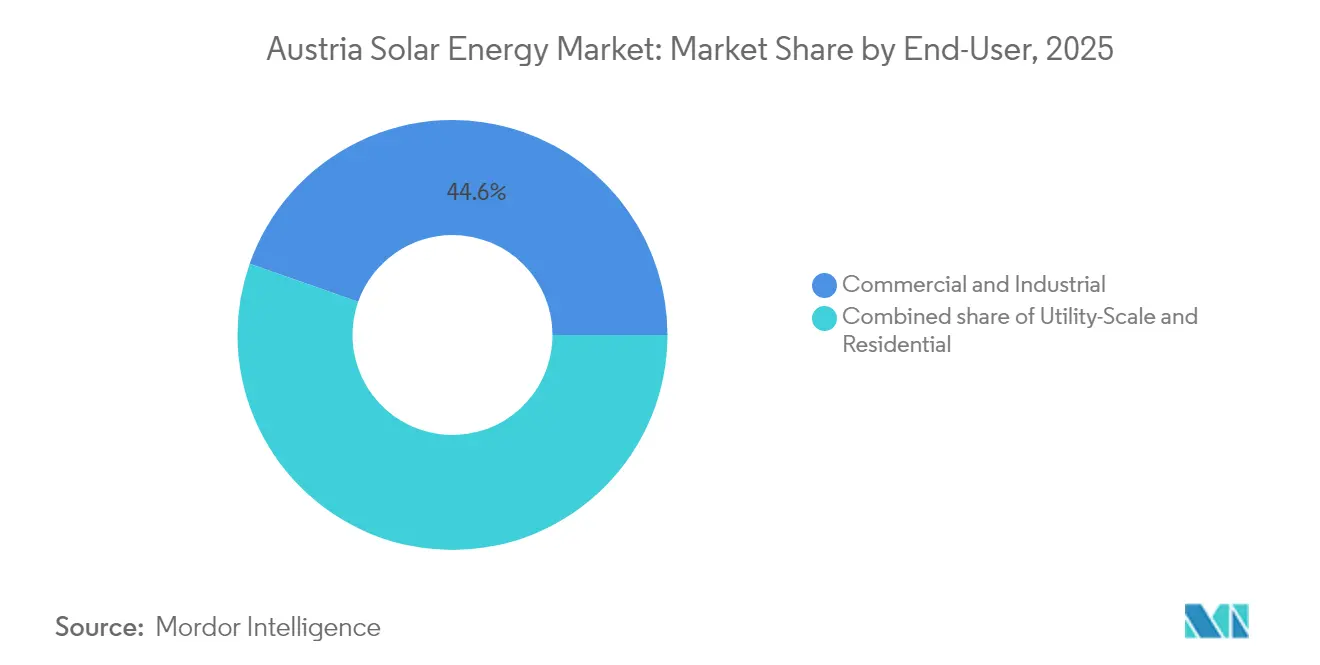

- By end-user, commercial and industrial installations controlled 44.62% of the Austria solar energy market size in 2025, whereas the residential segment is expanding at a 9.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Austria Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generous investment subsidy & feed-in tariff scheme | 1.80% | National, notably Vienna, Lower Austria, Burgenland | Short term (≤ 2 years) |

| EU 2030 100% renewable-electricity target | 1.20% | National, EU-wide alignment | Long term (≥ 4 years) |

| Rapid decline in PV module LCOE | 1.50% | National | Medium term (2-4 years) |

| Surge in corporate PPAs from energy-intensive industry | 0.90% | Burgenland, Lower Austria, Vienna | Medium term (2-4 years) |

| Agri-PV pilots unlocking dual land-use potential | 0.60% | Burgenland, Styria | Long term (≥ 4 years) |

| Citizen-owned energy cooperatives scaling community solar | 0.40% | Rural Lower Austria, Styria, Carinthia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Generous Investment Subsidy & Feed-in Tariff Scheme

Austria is allocating EUR 60 million in rooftop incentives for 2025, which reimburse EUR 1,000–1,500 per kWp for systems with a capacity below 10 kWp. The VAT exemption reinstated in 2025 for installations under 35 kW further reduces household payback periods to seven to nine years, accelerating the residential uptake that underpins the Austrian solar energy market. A “Made in Europe” 20% bonus diverts procurement toward suppliers such as Fronius and Greenonetec, counterbalancing lower-priced Asian imports. Demand spikes at each funding window exhaust the budget within four months, creating cyclical installation rushes that complicate labor scheduling and strain installer margins. Although subsidies improve economics, they do not ease grid congestion or skilled-labor gaps, meaning some approved projects still miss the construction season.

EU 2030 100% Renewable-Electricity Target

The binding EU directive requires Austria to increase its solar capacity to at least 12–13 GW by 2030, resulting in an 11 TWh production mandate under domestic law. Non-compliance would jeopardize access to EU climate funds, shielding policy continuity from domestic politics. The directive exposes supply-chain vulnerabilities, since Austria imports most modules and inverters; tariff shocks or shipping disruptions could derail timelines. The 10% year-on-year decline in 2024 additions to 2.2 GW highlighted how grid and permitting frictions, not demand, impede progress. Unless approvals and interconnections accelerate, the target risks slipping by 1–2 TWh, triggering the costly purchase of foreign renewable certificates.

Rapid Decline in PV Module LCOE

Polysilicon prices fell from USD 35/kg in 2022 to USD 7–8/kg in 2024, resulting in a 50–60% decrease in module costs.[1]International Energy Agency, “PV Module Cost Trends 2024,” iea.org Utility-scale LCOE now ranges between EUR 0.04 and 0.06 per kWh, making new PV arrays about 30–40% cheaper than gas-fired peakers. Residential systems cost EUR 1,200–1,800 per kWp, making them viable even without subsidies in high-irradiance regions such as Carinthia and Styria. Borealis’s 70 GWh-per-year PPA at EUR 0.05–0.06 per kWh confirms corporate appetite for long-term price certainty below wholesale levels. However, Austria’s lack of domestic module production leaves the Austria solar energy market exposed to any rebound in global pricing or trade disputes.

Surge in Corporate PPAs from Energy-Intensive Industry

Industrial electricity accounted for roughly 25 TWh in 2024, equal to 8–12% of operating expenses for heavy manufacturers. The Borealis-Burgenland Energie contract guarantees 70 GWh per year from 2026 at a fixed price under retail rates, showcasing a template that could anchor 6–8 GW of future capacity if replicated across Austria’s 50–60 large sites. Vienna Airport’s on-site arrays now cover 30% of demand, reducing transmission losses and enhancing security of supply. Yet typical PPAs run 15–20 years, longer than many corporate planning cycles, and a shortage of standardized contracts slows deal flow. Credit-enhancement solutions remain limited, further constraining uptake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land-use permitting bottlenecks for ground-mount plants | -0.80% | Burgenland, Lower Austria | Short term (≤ 2 years) |

| Distribution-grid congestion & interconnection delays | -0.70% | Lower Austria, Burgenland | Medium term (2-4 years) |

| Skilled-labor shortage for PV installation & O&M | -0.50% | National, acute in Vienna | Short term (≤ 2 years) |

| Stricter rooftop fire-safety codes raising CAPEX | -0.30% | National, especially urban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Land-Use Permitting Bottlenecks for Ground-Mount Plants

Agricultural land claims extend approval cycles for ground-mount systems to 12–24 months, inflating financing costs by up to 10% as interest accrues during delays. The federal structure means each province sets unique criteria; Lower Austria enforces wider setbacks than Styria, which approves degraded-land sites within ten months. Developers familiar with Spain’s streamlined rules perceive Austrian processes as risky, limiting international participation and concentrating projects among domestic utilities. Without harmonization, Austria could fall 1–2 GW short of its 2030 target.

Distribution-Grid Congestion & Interconnection Delays

High penetration in Lower Austria and Burgenland results in a 2–3% curtailment of potential output during summer peaks. Interconnection queues for projects exceeding 10 MW can stretch up to 18 months, while residential rooftops receive priority approvals under simplified rules. EVN’s plan to add 70 MW of batteries by 2027 will help absorb surplus generation; however, until the upgrades are in place, curtailment persists. Commercial developers face disputes over grid extension cost allocation, which delays financing decisions. Export capacity to neighboring grids is capped at 2–3 GW, resulting in some summer generation being stranded.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Monopoly Reflects Climate Realities

Solar photovoltaic captured 100.00% of installations in 2025 as Austria’s diffuse irradiance renders concentrated solar power uneconomic. The Austria solar energy market size for PV reached 9.90 GW and is on course for a 6.02% CAGR, underpinned by bifacial modules that already power 25–30% of new utility plants. Single-axis trackers are used in 40–50% of ground-mount projects, increasing yields by up to 25% while adding EUR 100–150 per kWp to the capital cost, a premium that is only acceptable above a 10 MW scale. High-altitude arrays like Wien Energie’s 15 MW Ratten plant generate 15–20% more winter output thanks to snow reflectance. The absence of CSP eliminates thermal-storage cogeneration, so lithium-ion batteries or pumped hydro must bridge the intermittency.

Continued PV dominance simplifies installer training and supply logistics, yet exposes the Austria solar energy market to PV-specific disruptions, including polysilicon shortages or inverter component scarcity. Module imports from Asia exceeded 75% of the volume in 2024; any trade restrictions could slow down builds. Conversely, EU manufacturers benefit from the 20% “Made in Europe” bonus, nudging procurement toward regional suppliers and cushioning geopolitical shocks.

By Grid Type: On-Grid Dominance Masks Off-Grid Niches

On-grid installations represented 99.28% of the Austria solar energy market share in 2025 and are forecast to grow at a 6.55% CAGR to 2031, outperforming the total market as residential rooftops and utility farms connect to strong networks covering 99.9% of households. Off-grid capacity of 0.72% serves alpine huts and remote farm buildings where line extension costs exceed EUR 50,000 per km. On-grid hybrid plants, such as EVN's 20 MW PV plus 5 MW battery site at Theiss, earn EUR 0.02–0.03 per kWh from balancing services in addition to energy sales.

The Austrian solar energy market size for on-grid systems is expected to continue expanding, driven by distribution firms' investments of EUR 3 billion to upgrade digital substations and add 70 MW of storage by 2027. Off-grid demand grows at a 4.06% CAGR, constrained by limited site availability. IEC 62109 compliance adds EUR 200–400 per kW in safety equipment for grid-connected arrays, thereby reducing the price differential with off-grid systems. Thus, remote cabins remain the primary off-grid adopters, a niche that is unlikely to exceed 20 MW nationally by 2030.

By End-User: Residential Surge Challenges C&I Leadership

Commercial and industrial rooftops commanded 44.62% of the Austria solar energy market in 2025, driven by warehouse mandates and cost-hedging PPAs. Yet, residential arrays will grow at a 9.78% CAGR, positioning households for a 40.00–42.00% share by 2031. Subsidies and VAT relief reduce payback periods to below nine years, while 675 renewable energy communities monetize their surplus at peer-to-peer prices higher than feed-in tariffs.

C&I growth moderates to single-digit rates as prime rooftops saturate and grid fees rise for large offtakers. Vienna Airport’s installation of 8–10 MW illustrates the scale benefits, covering approximately 30% of its consumption. Utility-scale farms, the smallest end-user tranche at 20–25%, deliver the lowest LCOE of EUR 0.04–0.06 per kWh but face 12–24 month permitting cycles and land conflicts, slowing expansion. Grid operators must invest in smart meters and responsive tariffs to manage two-way flows as prosumer numbers swell, a task baked into EVN’s upgrade roadmap.

Geography Analysis

Lower Austria and Burgenland contributed 58.73% of the 2025 capacity additions, owing to irradiance levels of 1,100–1,300 kWh/m² and ample flat land. Lower Austria installed roughly 1.36 GW in 2025, supported by EVN’s target of more than 300 MWp of new arrays by 2030. Burgenland hosts flagship projects, such as the 164 MW Tadten agrivoltaic plant and PÜSPÖK’s 257 MWp pipeline, attracting EUR 150–200 million of cross-border investment and leveraging access to Hungarian and Slovak grids.

Vienna, constrained by its roof area, still added 165–215 MW in 2025 through municipal mandates; Wien Energie aims to exceed 100 MWp by early 2025 for district heating electrification. Styria’s alpine sites, including the 15 MW Ratten plant at an elevation of 1,200 m, capture high winter yields that mitigate seasonal gaps. Upper Austria and Carinthia are accelerating through cooperative models, with Carinthia hosting the highest per-capita energy community count nationwide, underscoring the social acceptance benefits. The cross-border export capacity of 2–3 GW eases summer surpluses, yet leaves 10–15% of potential generation curtailed during periods of congestion. EUR 80–100 million in EU co-financing will upgrade lines by 2028, adding 1–1.5 GW export headroom and reducing curtailment risk. Differential permitting speeds—eight months in Styria versus 18 months in Lower Austria—lead developers to favor fast-track provinces, leaving slower regions behind. Battery deployment of 70 MW by 2027 will buffer local imbalances, but until then, curtailment persists.

Regulatory Landscape

Austria's solar PV deployment is primarily governed by the Renewable Energy Expansion Act (Erneuerbare-Ausbau-Gesetz, EAG), which sets the national pathway to reaching 100% of electricity consumption with domestic renewables by 2030 and includes an 11 TWh photovoltaic contribution mandate. The EAG support framework runs PV and storage through scheduled funding calls for larger plants (including OeMAG mechanisms), and these recurring call windows in 2026 affect installer backlogs and project timing.

Permitting and grid build-out are also targeted through the Renewable Energy Expansion Acceleration Act (EABG), promulgated on July 1, 2026, to accelerate approval procedures for energy facilities, grid infrastructure, and storage. Oversight sits with Energie-Control Austria (E-Control), which supervises electricity market operations and the functioning of support instruments, while annual financing parameters are set through instruments such as the Renewable Energy Contribution Regulation 2026 (Erneuerbaren-Foerderbeitragsverordnung 2026), linking end-user contributions to the continuation of PV and hybridization support.

Competitive Landscape

The top five players, Wien Energie, Verbund AG, EVN, Burgenland Energie, and KPV Solar, captured 35–40% of capacity additions in 2024, leaving the Austria solar energy market moderately fragmented. Wien Energie operates across generation, retail, and district heating, leveraging alpine bifacial arrays and trackers to boost winter output. Verbund AG, traditionally hydro-centric, entered ground-mount PV with its 2.7 MWp Güssing park, signaling a EUR 1–1.5 billion renewable pivot by 2030.

International inverter makers vie for grid-code compliance. Fronius’s 98.3% efficient Verto series now serves 30% of residential demand and benefits from the “Made in Europe” 20% subsidy uplift. Huawei and SolarEdge compete on cost and digital monitoring, yet they must also accommodate Austrian fire-safety regulations that mandate additional disconnect switches. Agrivoltaic specialists, such as PÜSPÖK Group, target dual-use niches, while energy cooperatives reduce acquisition expenses through peer-to-peer platforms like eFriends, thereby reshaping customer engagement.

Certification under IEC 62109 and 60364-7-712 creates entry barriers that favor established suppliers. Small installers partner with certified vendors to avoid the cost of independent conformity testing, preserving local competition.[4]Austrian Standards Institute, “Fire-Safety Upgrades for Rooftop PV 2024,” austrian-standards.at Technology strategies diverge: Wien Energie premiumizes through high-altitude, tracker-equipped arrays, whereas KPV Solar emphasizes low-cost fixed-tilt rooftops qualifying for “Made in Europe” subsidies. Such differentiation keeps the Austria solar energy market dynamic despite consolidation tendencies.

Austria Solar Energy Industry Leaders

Wien Energie GmbH

Verbund AG

KPV Solar GmbH

Fronius International GmbH

Energetica Industries GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity lies in projects that convert constrained land and urban surfaces into PV capacity while staying aligned with the EAG pathway (11 TWh from PV as part of the 2030 domestic 100% renewable electricity requirement). The federal PV sector strategy targeting panels on one million rooftops, together with the high on-grid share (99.28% in 2025), keeps the rooftop pipeline central for both residential and C&I demand, particularly as ground-mount permitting cycles typically run 12-24 months. In dense areas with limited contiguous land, Vienna's infrastructure-linked deployments (such as PV on transit and on heritage-constrained rooftops) and the scaling of renewable energy communities offer repeatable models.

A second opportunity cluster involves PV-plus-storage and flexibility integration aimed at reducing curtailment and delays tied to interconnection queues in Lower Austria and Burgenland. The 2026 funding rounds expanding solar-plus-storage rebates, with thousands of applications, support demand pull for hybrid systems, while grid operators' battery plans (including EVN's planned 70 MW by 2027) provide execution pathways for developers and suppliers across inverters, EMS, and storage. Larger projects also benefit from utility and corporate procurement structures, reflected in the Burgenland Energie-Borealis offtake structure noted in the broader market context, along with growing utility-hardware partnerships that package hybrid inverters and batteries into standardized residential offers.

Recent Industry Developments

- July 2026: OeBB and Burgenland Energie inaugurated a 6.6 MWp tracking agrivoltaic plant in Donnerskirchen that supplies 16.7 Hz traction power directly into the railway grid. The project extends agrivoltaics from land-use optimization into sector-coupled infrastructure supply and adds a new offtake pathway beyond conventional public-grid injection.

- June 2026: Austria opened a second 2026 solar-plus-storage support round with an expanded budget reported at EUR 48.76 million, covering 9,327 applications. The high volume of applications points to a shift from standalone PV toward paired systems, which can better manage congestion and self-consumption, affecting inverter, battery, and installer demand.

- December 2024: Burgenland Energie finalized the 164 MW Tadten agrivoltaic project, supplying 70 GWh annually under a Borealis PPA. Completion reinforced agrivoltaics as a bankable utility-scale format in Austria and provided a reference structure for long-term corporate offtake tied to large new PV assets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as Austria's solar power industry, measured mainly through installed capacity added and in operation for solar technologies across grid-connected and off-grid systems during the study period.

Scope exclusions: We exclude broader power generation assets that do not use solar energy, and we also exclude non-energy products and services that are not directly tied to solar system deployment.

Segmentation Overview

- By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- By Grid Type

- On-Grid

- Off-Grid

- By End-User

- Utility-Scale

- Commercial and Industrial (C&I)

- Residential

- By Component (Qualitative Analysis)

- Solar Modules/Panels

- Inverters (String, Central, Micro)

- Mounting and Tracking Systems

- Balance-of-System and Electricals

- Energy Storage and Hybrid Integration

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to establish the factual base for Austria, where the market can be tracked using transparent energy and policy records. We relied on public energy statistics and system registries such as those from Statistik Austria, Austria's energy regulator and grid-related publications, and international sources such as IEA and IRENA for definitions and cross-checks. For trade and supply-side signals, we used customs and trade statistics such as UN Comtrade, and we also reviewed peer-reviewed papers to validate performance assumptions and technology adoption patterns.

Alongside those, we reviewed company filings, investor presentations, association updates, and trusted press coverage to identify project timelines and policy changes that can shift installations. In a few places, paid subscriptions were used for company financials and intelligence and for patent lookups, mainly to confirm participant activity and product direction rather than to directly size demand. The sources listed above are illustrative, and many other public materials were reviewed to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work focused on confirming what is actually being built and connected, and what is being delayed, which is hard to assess from announcements alone. We spoke with a mix of developers, EPCs, component distributors, O&M firms, and large end users, and then used these conversations to validate installation run-rates, pricing movement, and permitting and grid-connection lead times across Austria.

Expert feedback was also used to test desk assumptions around rooftop versus ground-mounted momentum, financing availability, and how incentives and net metering rules influence adoption in different customer groups.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 16% | APAC: 44% |

| Mid tier: 57% | Functional/Unit leaders: 41% | EMEA: 32% |

| Smaller Players: 18% | Managers: 43% | Americas: 24% |

Market-Sizing & Forecasting

Market sizing was built using a top-down and bottom-up logic, where national installation and capacity signals are first reconstructed from Austria-facing energy and grid indicators, and then checked against supplier and channel reality. The top-down spine uses items such as annual PV additions (MW), cumulative installed capacity (MW), grid-connection activity, and policy-driven deployment targets, which are then converted into a consistent capacity series for the study years.

Once that view was formed, selective bottom-up approximations were used to see if the totals make sense. These checks included sampled project pipelines, EPC throughput discussions, and price-per-watt and module and inverter availability conversations, followed by adjustments when mismatches were found. Where bottom-up inputs were missing for a niche area (for example, smaller off-grid installations), gaps were handled by using proportional splits informed by expert shares and then validating those splits against observed connection data.

For forecasting, we relied on scenario analysis supported by short, clear drivers, and then aligned the outcomes with what interviewees expect for Austria over the next few years. Variables used in the forecast include expected auction and subsidy continuity, rooftop permitting pace, grid congestion and upgrade timelines, typical project lead times, and the direction of system costs (modules, inverters, and balance-of-system).

Data Validation & Update Cycle

Validation was done by comparing model outputs against independent signals, and then reviewing any large gaps before sign-off. If a year shows an unusual jump or drop, we re-check the underlying drivers, including policy events, one-off project commissioning, and temporary supply constraints, and we re-contact sources when the explanation is not strong enough.

A multi-step internal review is used so that assumptions, units, and conversions stay consistent from history through forecast. Reports are refreshed annually, and interim updates are made when material events occur, such as major incentive redesigns or large pipeline shifts. Before delivery, a final fresh pass is completed so clients receive the latest updated view available at that time.

Mordor Intelligence's Austria Solar Energy Market Estimate Compared With Other Published Estimates

Published numbers for Austria solar energy often do not match because the market is not always measured the same way, and the forecast window can also change how the current year appears across sources. Differences usually come from what is counted as solar, whether the unit is capacity or value, how grid-connected systems are treated, and how quickly assumptions are updated after policy or pricing shifts.

Solar thermal capacity sits outside Mordor Intelligence's scope here, which is one reason some published totals land higher or lower when sources mix technologies or roll up broader renewable capacity. Gaps also appear when aggressive build-out targets are treated as installed reality, when price-per-watt declines are applied too quickly, or when older exchange-rate timing is used for conversions in value-based narratives (even if the headline unit shown is GW).

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.90 B (2025) | |

| Industry Marketplace A | USD 5.24 B (2025) | Often presented as a broader solar energy number without clearly separating PV from adjacent solar technologies, and the capacity base can be closer to annual additions rather than cumulative installed stock. |

| Project Tracker B | USD 8.50 B (2024) | Uses a point-in-time installed capacity signal tied to project commissioning disclosures, which can undercount smaller rooftop systems and can lag fast-moving interconnection activity. |

Looking across the three figures, the spread is largely explained by what gets included in the technology set and whether the number reflects cumulative installed capacity or a narrower installation snapshot. Our approach keeps the math traceable to Austria-specific deployment indicators, and it is then checked with on-the-ground feedback so the final view stays realistic and repeatable.

Key Questions Answered in the Report

What capacity will Austrian solar reach by 2031?

Installed capacity is forecast to hit 14.06 GW by 2031, reflecting a 6.02% CAGR from 2026.

How large is the residential share of solar in Austria?

Residential systems will rise from 2025’s sub-40% level to about 40.00–42.00% of total capacity by 2031 on 9.78% CAGR growth.

Which provinces add the most solar each year?

Lower Austria and Burgenland together accounted for roughly 58.73% of 2025 additions thanks to favorable irradiance and land availability.

Why are agrivoltaic projects gaining traction?

Elevated panels protect crop yields while securing faster permits, and they could deliver 15–20% of new capacity by 2031.

Which companies lead Austrian solar development?

Wien Energie, Verbund AG, EVN, Burgenland Energie, and KPV Solar collectively control about 35–40% of recent capacity growth.

What limits large utility-scale solar in Austria?

Lengthy land-use permits, grid-connection delays, and local opposition extend timelines to 12–24 months, slowing expansion relative to rooftops.

Page last updated on: