Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

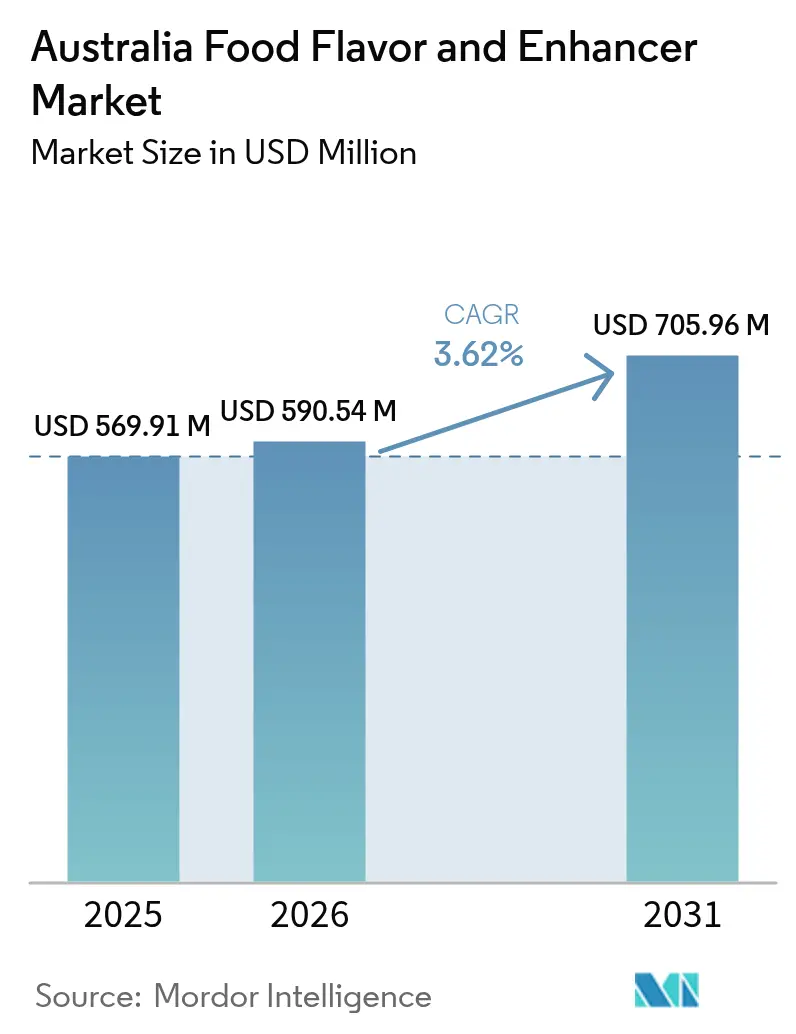

| Base Year Market Size (2025) | USD 569.91 Million |

| Market Size (2026) | USD 590.54 Million |

| Market Size (2031) | USD 705.96 Million |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Food Flavors and Enhancers Market Analysis by Mordor Intelligence

The Australian food flavor and enhancer market size is expected to grow from USD 569.91 million in 2025 to USD 590.54 million in 2026 and is forecast to reach USD 705.96 million by 2031 at 3.62% CAGR over 2026-2031. This growth trajectory is primarily attributed to Australian consumers' increasing preference for clean-label formulations, coupled with a regulatory environment that balances safety requirements with innovation opportunities. The market is witnessing significant developments in the beverage sector, where manufacturers are investing in sophisticated masking technologies to improve the palatability of nutritional beverages. In the dairy segment, processors are strategically utilizing flavor solutions to transform conventional milk products into premium offerings, capturing higher profit margins. The market dynamics are further evolving with precision-fermentation companies securing substantial investments to develop economically viable umami and savory flavors, presenting a competitive challenge to established synthetic flavor manufacturers. In response to these market shifts, traditional flavor companies are strengthening their position through strategic vertical integration, enhanced automation processes, and establishing transparent botanical sourcing practices to navigate global raw material supply challenges.

Key Report Takeaways

- By application, beverages captured 32.21% of the Australia Food Flavors and Enhancers Market share in 2025; the dairy segment is projected to expand at a 4.16% CAGR through 2031.

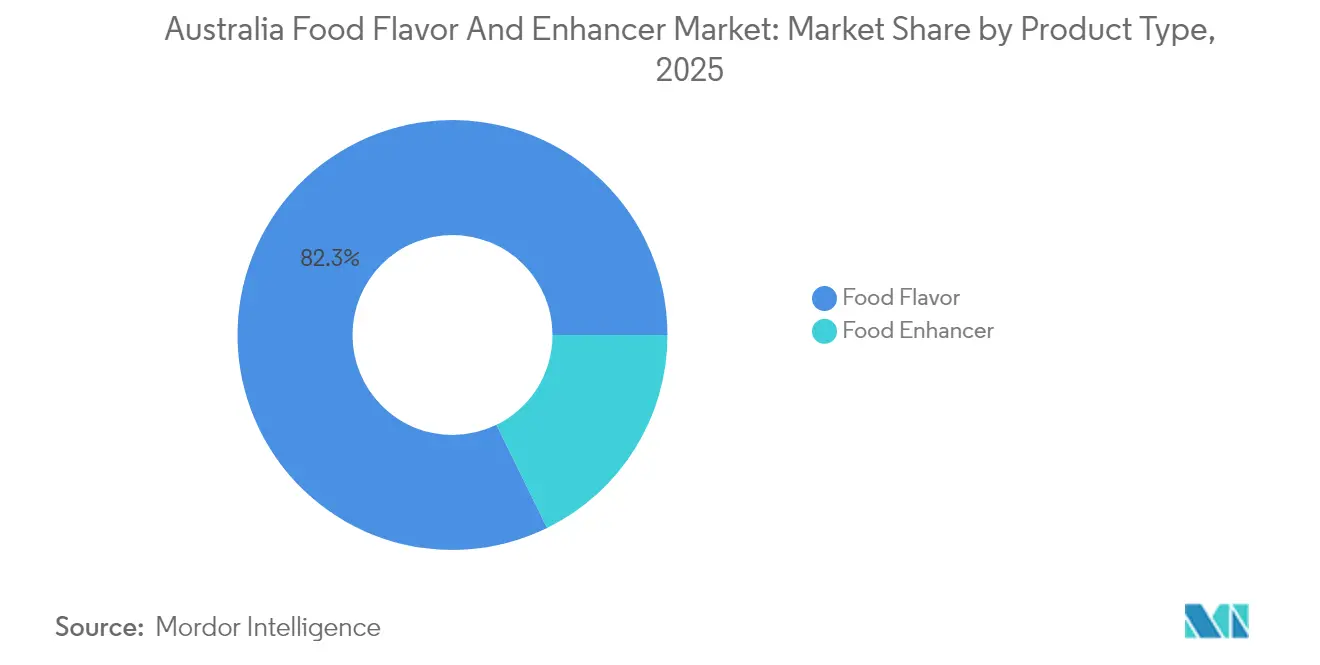

- By product type, food flavors commanded 82.25% share of the Australia Food Flavors and Enhancers Market size in 2025, while food enhancers are poised for 4.47% CAGR growth to 2031.

- By type, synthetic flavors led with 45.54% revenue share in 2025; natural flavors are advancing at a 3.97% CAGR over the forecast period.

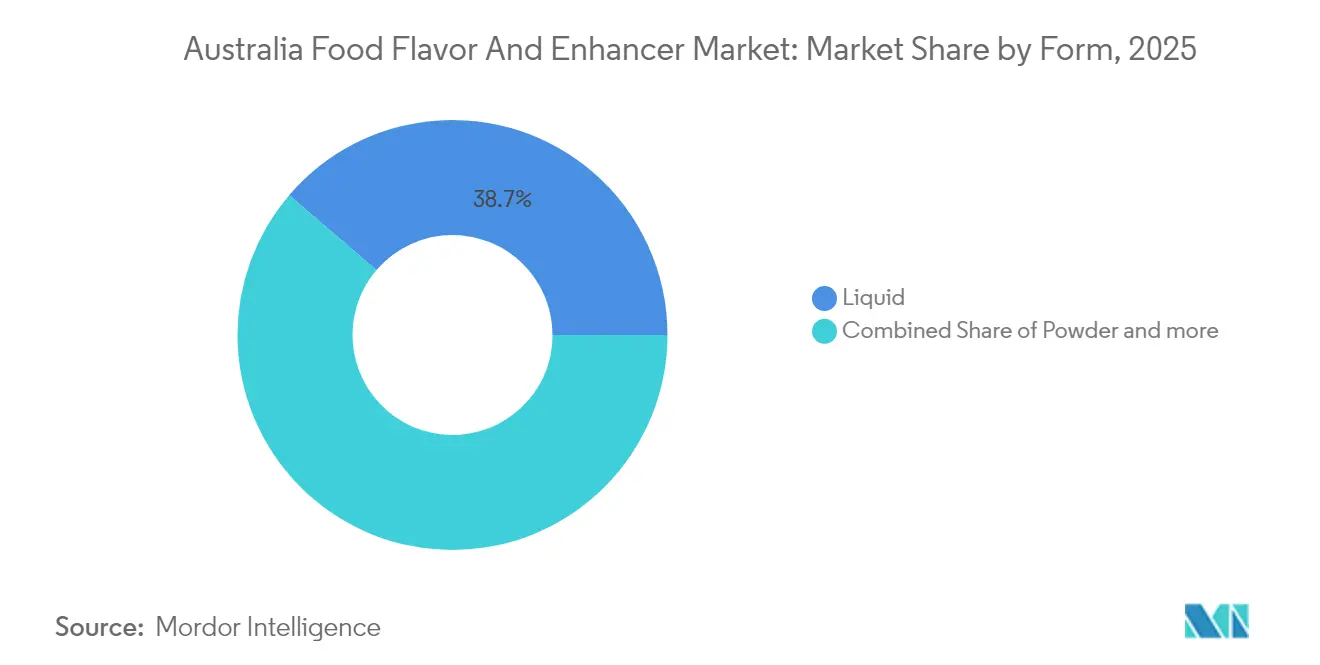

- By form, liquid systems held 38.74% share of the Australia Food Flavors and Enhancers Market size in 2025, while powder forms record the strongest 4.49% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Food Flavors and Enhancers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand for natural and organic flavors | +0.8% | National, with early gains in Melbourne, Sydney, Brisbane | Medium term (2-4 years) |

| Increasing demand for convenience and ready-to-eat foods | +0.6% | National, strongest in urban centers | Short term (≤ 2 years) |

| Growing use of functional foods requiring masking flavors | +0.7% | National, spill-over to export markets | Medium term (2-4 years) |

| Advances in bio-fermentation and precision fermentation for flavor creation | +0.5% | National, with research and development concentration in Victoria, NSW | Long term (≥ 4 years) |

| Increasing innovation in taste-modulating flavors for health beverages | +0.4% | National, export-oriented production | Medium term (2-4 years) |

| Consumers' increasing willingness to explore diverse and premium taste profiles | +0.3% | National, premium segment focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Natural and Organic Flavors

The ongoing demographic shift in Australia has created significant competitive advantages for suppliers who strategically invest in botanical extraction capabilities and maintain transparent supply chains. The Food Standards Australia New Zealand (FSANZ) approval framework has evolved to favor naturally-derived ingredients that demonstrate established safety profiles. In response to these changes, Australian manufacturers have actively begun reformulating their existing product portfolios while simultaneously developing new product lines that incorporate natural flavor systems. This market evolution has generated increased demand for vanilla, citrus, and herb-based extracts across the food and beverage industry. The premium pricing structure associated with natural flavors has enabled both suppliers and food manufacturers to achieve higher profit margins, which in turn fuels continuous market growth, even in the face of volume constraints in the natural ingredients supply chain.

Increasing Innovation in Taste-Modulating Flavors for Health Beverages

Australia's functional beverage segment has evolved through advanced taste-masking solutions, particularly in sports nutrition and wellness products. Kerry Group's implementation of salt and sugar reduction technologies has improved both volume growth and profitability, with the company recording significant margin improvements. Australian beverage manufacturers continue to address the technical challenges of incorporating functional ingredients while maintaining palatability, especially in protein-enriched and low-sugar products. The market potential includes export opportunities, as Australian taste-modulating systems gain traction across Asia-Pacific regions with similar regulatory frameworks and consumer preferences. The Food Standards Australia New Zealand (FSANZ) consultation regarding 3-fucosyllactose in infant formula demonstrates regulatory support for functional ingredients requiring taste masking. This regulatory framework establishes precedents for additional functional ingredients that need taste enhancement, creating new opportunities for specialized flavor manufacturers in the region.

Growing Use of Functional Foods Requiring Masking Flavors

Australia's aging population and health-conscious consumer base drive demand for functional foods that deliver therapeutic benefits without compromising taste experience. The intersection of the pharmaceutical and food industries creates opportunities for flavor enhancers that mask bitter, metallic, or off-note characteristics common in nutraceutical formulations. International Flavors and Fragrances' Q1 2025 performance, with Taste segment growth of 7% year-over-year, reflects global demand patterns that are particularly pronounced in developed markets like Australia. Australian food manufacturers are increasingly incorporating probiotics, plant proteins, and bioactive compounds that require sophisticated masking technologies. The regulatory environment supports this trend, with FSANZ's streamlined approval processes for established functional ingredients reducing time-to-market for innovative formulations. Export opportunities amplify domestic demand, as Australian-developed functional food products gain traction in Asian markets where similar demographic and health trends are emerging.

Advances in Bio-fermentation and Precision Fermentation for Flavor Creation

Australia has established itself as a regional center for advanced flavor production technologies through investments in cellular agriculture and precision fermentation. Companies such as Eden Brew, Cauldron, and All G Foods have received substantial funding for precision fermentation projects, which has increased the demand for specialized flavor systems compatible with these new ingredients. The adoption of bio-fermented flavors enhances supply chain stability by reducing reliance on climate-sensitive agricultural inputs. The Food Standards Australia New Zealand (FSANZ) approval of genetically modified corn line DAS1131 shows regulatory support for biotechnology in food production, establishing a framework for bio-fermented flavor ingredients [1]Source: Food Standards Australia New Zealand, “Approval report – Application A1280,” foodstandards.gov.au. Australian flavor manufacturers are expanding their fermentation capabilities to serve both local and international markets, particularly focusing on umami and savory flavors for plant-based protein products. As production volumes increase, the cost advantages of these technologies become more evident, potentially transforming the flavor industry's cost structure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory requirements for food additives | -0.4% | National, FSANZ jurisdiction | Long term (≥ 4 years) |

| Fluctuating raw material prices affecting cost structures | -0.6% | National, import-dependent categories | Short term (≤ 2 years) |

| Supply chain disruptions leading to inconsistent ingredient availability | -0.5% | National, with export market impacts | Medium term (2-4 years) |

| Limited shelf life of natural flavor ingredients | -0.3% | National, affecting natural segment growth | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Requirements for Food Additives

The Food Standards Australia New Zealand (FSANZ) maintains a comprehensive pre-market assessment framework that prioritizes consumer safety. However, this framework inadvertently creates significant barriers to innovation within the flavor and enhancer ingredients market. A notable example is the agency's evaluation process for genetically modified corn line DAS1131, which requires extensive safety assessments and mandatory public consultation periods. These regulatory requirements place a substantial burden on ingredient suppliers, particularly impacting smaller companies and innovative startups. The high compliance costs and expertise requirements have resulted in market consolidation, favoring established companies with substantial regulatory experience and financial resources. Product manufacturers face additional challenges in their development cycles, as they must factor in potential regulatory approval delays when planning new product launches. While international standards, such as those established by Codex Alimentarius for flavor enhancers like disodium 5'-ribonucleotides and disodium 5'-inosinate, offer some regulatory pathways, Australia's unique labeling requirements and country-specific safety assessments continue to add layers of complexity that restrict overall market growth [2]Source: Food and Agriculture Organization of the United Nations, “Food Additive Details,” fao.org.

Fluctuating Raw Material Prices Affecting Cost Structures

Commodity price volatility creates significant margin pressure that constrains market expansion, particularly in natural flavor segments dependent on agricultural inputs. The global cocoa crisis analyzed by Kerry Group demonstrates substantial price increases and projected supply shortfalls for several years, highlighting the raw material challenges facing Australian flavor suppliers. Australia's import dependence for key flavor ingredients increases its exposure to global price fluctuations and supply chain disruptions. According to the Australian Bureau of Statistics, food ingredient imports show considerable monthly variations, with organic and inorganic chemicals imports experiencing a notable decline, indicating supply chain volatility [3]Source: Australian Bureau of Statistics, “International Trade in Goods,” abs.gov.au. Currency fluctuations further complicate the situation, as Australian dollar weakness increases import costs while potentially benefiting export-oriented manufacturers. While suppliers implement vertical integration strategies and long-term supply contracts to mitigate risks, these approaches require substantial capital investment that limits growth in other areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Food Flavors Dominate Despite Enhancer Innovation

Food flavors maintain a dominant position in Australia's food processing industry, commanding an 82.25% market share in 2025. This substantial market presence underscores their essential role across various food applications, from ready-to-eat meals to beverages and snacks. Meanwhile, food enhancers have emerged as the fastest-growing segment, advancing at a 4.47% CAGR through 2031. This growth pattern indicates a significant market transformation, as manufacturers increasingly prioritize functional enhancement over conventional flavoring methods to meet evolving consumer preferences for products that deliver both taste satisfaction and nutritional benefits.

The food enhancer segment's expansion is primarily driven by the integration of umami compounds and sophisticated taste modulation systems, enabling manufacturers to reformulate products while maintaining their appeal. These enhancers prove particularly valuable in health-focused formulations where traditional flavoring approaches fall short of meeting both regulatory requirements and taste expectations. Kerry Group's innovative developments in salt and sugar reduction technologies serve as a prime example of how enhancers create additional value beyond basic flavoring, allowing food manufacturers to achieve compliance with health regulations while ensuring their products remain appealing to consumers.

By Type: Natural Flavors Gain Ground Against Synthetic Dominance

Synthetic flavors maintain their dominant position with a 45.54% market share in 2025. This leadership stems from their established advantages in cost efficiency and ability to deliver consistent performance across various applications. However, the market dynamics are shifting as natural flavors emerge as the fastest-growing segment, achieving a 3.97% CAGR, primarily due to increasing consumer demand for clean-label products.

This fundamental market transformation creates new operational requirements for suppliers, who must now develop specialized technical capabilities and forge different supply chain relationships compared to synthetic flavor production. The industry is experiencing clear premiumization, with consumers demonstrating willingness to pay higher prices for natural ingredients. Generation Z's influence has become particularly significant in this transition, with Kerry's research highlighting how their strong preferences for sustainability and authenticity are reshaping purchasing patterns across all age groups.

By Form: Liquid Systems Lead While Powder Applications Accelerate

Powder forms are projected to grow at 4.49% CAGR through 2031, supported by their significant advantages in convenience and extended shelf-life characteristics. These benefits have become increasingly important for Australia's export-oriented food processing industry, where manufacturers need reliable and stable product forms for international distribution. The technological advancements in powder processing have enhanced their appeal, particularly in markets where product longevity is a crucial consideration.

Liquid forms currently dominate with a 38.74% market share in 2025, maintaining their strong position in beverage and dairy applications where instant solubility and uniform distribution are essential requirements. However, the market dynamics are shifting as manufacturers increasingly prioritize product stability and ease of handling in their operations. The advancement of encapsulation and spray-drying technologies has particularly benefited powder forms, enabling better flavor retention and extended product life. This technological evolution aligns perfectly with Australia's geographic position and export-focused business model, where the ability to maintain product stability during long-distance transport has become a significant competitive advantage in international markets.

By Application: Beverages Lead While Dairy Shows Strongest Growth

The beverage segment commands a substantial 32.21% market share in 2025, demonstrating Australia's robust presence in the functional beverage market. This significant market position is reinforced by the country's well-established capabilities in premium product exports, which have consistently met international quality standards and consumer preferences.

The dairy applications segment has emerged as the market's growth engine, advancing at a 4.16% CAGR through 2031. This expansion is underpinned by Australia's strategic shift toward value-added dairy products and premium export offerings. The country's reputation for stringent regulatory compliance and pristine production environments has strengthened its position in both domestic and international markets. This growth trajectory is further supported by industry restructuring initiatives, as exemplified by Bega Cheese's strategic decisions to consolidate its Tasmanian operations while investing in specialized production facilities to enhance operational efficiency.

Geography Analysis

Australia's food flavor and enhancer market demonstrates a distinct concentration in major urban centers, with Melbourne, Sydney, and Brisbane emerging as primary hubs for manufacturing and innovation activities. The country's unique geographic position as an island continent influences its supply chain dynamics, naturally fostering the development of local production capabilities and strengthening regional partnerships. The growing export opportunities in Asia-Pacific markets have prompted manufacturers to focus on premium product development and advanced shelf-life extension technologies, addressing the specific needs of international trade.

The Food Standards Australia New Zealand (FSANZ) regulatory framework, which oversees both Australian and New Zealand markets, offers significant operational advantages for suppliers active in both territories. However, the presence of country-specific requirements continues to introduce complexity into product development cycles and registration procedures. Victoria and New South Wales have established themselves as key manufacturing centers, housing major production facilities that cater to both domestic consumption and export demands, reflecting the broader concentration of Australia's food processing industry.The Australian Food and Grocery Council's ongoing assessment of manufacturing cost pressures across regions has highlighted opportunities for efficiency-focused suppliers and innovative production technologies. State-level variations in regulatory interpretation and industry support programs play a crucial role in shaping investment decisions, with several regions offering attractive incentives for biotechnology advancement and sustainable manufacturing initiatives. The geographic distribution of end-user industries has created natural specialization opportunities, exemplified by the strong presence of dairy processing in Victoria and tropical fruit processing in Queensland, enabling flavor suppliers to develop targeted regional expertise.

Competitive Landscape

The Australian food flavor and enhancer market exhibits moderate competition characterized by fragmentation, creating diverse opportunities across the industry landscape. This market structure enables both global corporations and local suppliers to establish their presence and serve different market segments. Companies have adopted strategic approaches focused on vertical integration and regional partnerships, primarily to maintain control over their supply chains and protect themselves against fluctuations in raw material prices.

Major international companies, including Kerry Group, Givaudan, and International Flavors & Fragrances, maintain their market positions through extensive scale advantages and substantial research capabilities. Local companies have carved out their niches by focusing on specialized applications and maintaining close customer relationships. The market presents new opportunities, particularly in bio-fermentation applications and functional food formulations, where traditional suppliers have not yet developed comprehensive capabilities. The industry is witnessing the emergence of precision fermentation companies and biotechnology startups that are introducing alternative production methods, bypassing conventional supply chains.

Companies across the market are increasingly implementing automation and digital technologies to address rising labor costs, with significant investments in AI-driven flavor development and advanced analytics for demand forecasting. This technological adoption is showing promising results, as demonstrated by Sensient Technologies' 13.4% growth in local currency across the Asia-Pacific region, including Australia, indicating strong potential for expansion in 2024. The regulatory environment, governed by FSANZ, plays a crucial role in shaping competitive dynamics through its approval requirements. While these regulations tend to favor established companies with regulatory expertise, they also create opportunities for innovative firms that can successfully navigate the compliance process.

Australia Food Flavors and Enhancers Industry Leaders

Givaudan

DSM-Firmenich

Kerry Group

International Flavors & Fragrances Inc.

Sensient Technologies Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Australian Mint Oils expanded its flavors range with new offerings including Blue Raspberry, Pink Lemonade, and Pineapple Coconut. These flavors cater to diverse applications such as beverages, confectionery, nutraceutical gummies, and oral care.

- November 2024: DSM-Firmenich launched its Best-In-Class Milk portfolio, introducing Smart Milk flavors and Dynarome DA technology to enhance plant-based milk alternatives. These innovations replicate dairy’s creamy, buttery taste and texture while masking off-notes, addressing key consumer taste and nutrition concerns.

- June 2023: Tate & Lyle reaffirmed its commitment to sustainable sourcing as a core business obligation. The company emphasizes partnerships that promote regenerative agriculture and responsible supply chains, aiming to drive positive environmental and social impacts while supporting customers' sustainability goals in the food and beverage sector.

Australia Food Flavors and Enhancers Market Report Scope

Australia Food Flavors and Enhancers Market is segmented by type that includes flavors and flavor enhancers. The flavor section is further segmented into natural flavors, synthetic flavors, and nature-identical flavors. Based on Application, the market is segmented into bakery, confectionery, dairy, beverages, savory snacks, soups and sauces, and others.

By Product Type

| Food Flavor |

| Food Enhancer |

By Type

| Natural |

| Synthetic |

| Nature Identical |

By Form

| Powder |

| Liquid |

| Others |

By Application

| Dairy |

| Bakery |

| Confectionery |

| Savory Snack |

| Meat |

| Beverage |

| Other Applications |

| By Product Type | Food Flavor |

| Food Enhancer | |

| By Type | Natural |

| Synthetic | |

| Nature Identical | |

| By Form | Powder |

| Liquid | |

| Others | |

| By Application | Dairy |

| Bakery | |

| Confectionery | |

| Savory Snack | |

| Meat | |

| Beverage | |

| Other Applications |

Key Questions Answered in the Report

How large is the Australia Food Flavors and Enhancers Market in 2026?

It is valued at USD 590.54 million and is projected to reach USD 705.96 million by 2031.

Which application currently drives the greatest revenue?

Beverages account for 32.21% of revenue due to Australia’s thriving functional drink segment.

Which segment is expected to grow the fastest through 2031?

Dairy applications are forecast to register a 4.16% CAGR as producers premiumize flavored yogurts and milks.

What is the main driver behind rising use of natural flavors?

Younger consumers link sustainability and authenticity with clean labels, allowing brands to charge premium prices.

How are companies mitigating raw-material price volatility?

Strategies include multi-origin sourcing, futures contracts, and precision-fermentation alternatives that reduce reliance on volatile crops.

Page last updated on: