Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.72 Billion |

| Market Size (2026) | USD 12.18 Billion |

| Market Size (2031) | USD 14.79 Billion |

| Growth Rate (2026 - 2031) | 3.94% CAGR |

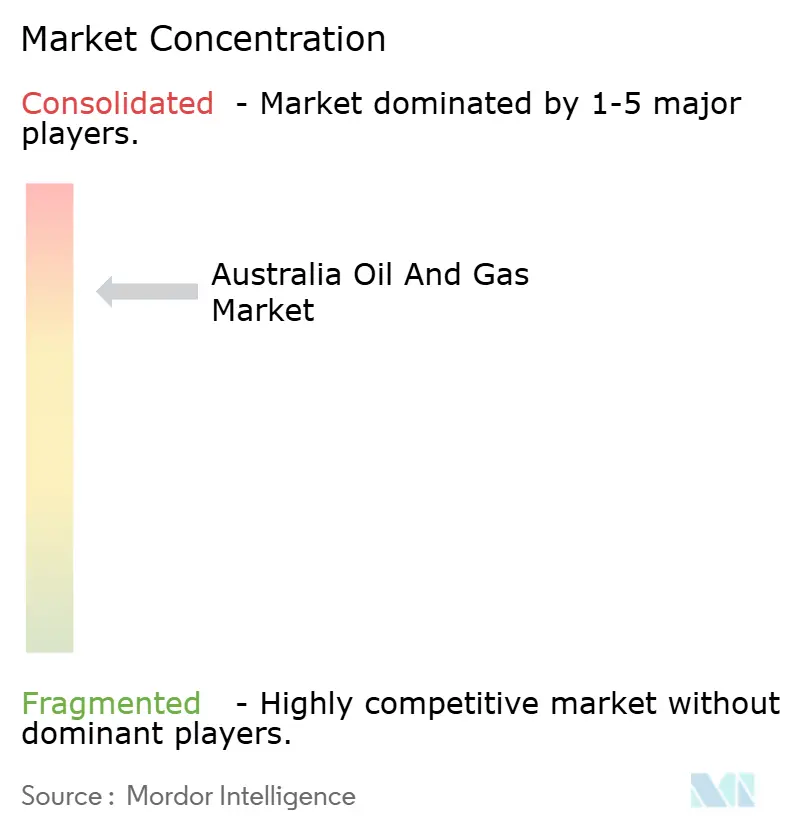

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Oil And Gas Market Analysis by Mordor Intelligence

The Australia Oil And Gas Market size was valued at USD 11.72 billion in 2025 and estimated to grow from USD 12.18 billion in 2026 to reach USD 14.79 billion by 2031, at a CAGR of 3.94% during the forecast period (2026-2031).

A USD 60 billion decommissioning backlog, rapid adoption of digital oil-field systems that cut offshore operating spending by as much as 83%, and surging off-grid demand from critical minerals mining are redefining competitive priorities within the Australian oil and gas market. Heightened domestic gas shortages, an expanding Asian LNG customer base, and tightening Scope 1 caps under the Safeguard Mechanism drive upstream capital toward CCS-ready blue-hydrogen schemes, while infrastructure bottlenecks in Eastern Australia sustain premium pipeline tariffs. Offshore Western Australia remains the production nucleus, yet onshore coal seam gas and Northern Territory shale prospects provide shorter-cycle growth options that help stabilize supply variance. Intensifying renewable penetration, meanwhile, compresses gas-fired power margins and underscores the need for integrated carbon-management services that preserve the long-term relevance of the Australian oil and gas market.

Key Report Takeaways

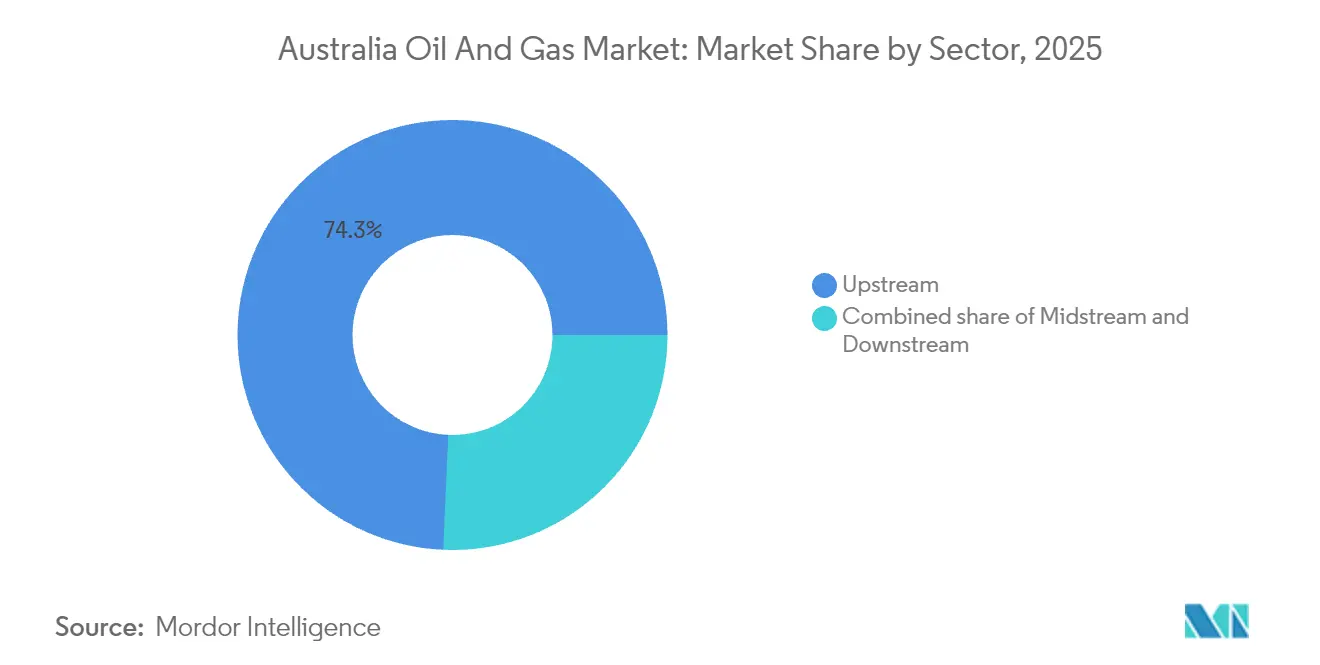

- By sector, upstream operations held 74.31% of Australia's oil and gas market share in 2025, and their 4.38% CAGR to 2031 is the fastest among core value-chain activities.

- By location, offshore assets commanded 85.40% of 2025 revenue and are forecast to expand at a 4.18% CAGR on the back of large-scale digital operations rollouts.

- By service, construction services captured 46.55% of the revenue in 2025, while decommissioning is set to lead growth at a 5.42% CAGR through 2031, as end-of-life platforms transition into dismantling programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising domestic & Asian LNG demand | +1.20% | National, with concentration in Western Australia and Queensland | Medium term (2-4 years) |

| Expansion of pipeline & gas-storage infrastructure | +0.80% | National, with focus on Eastern Australia gas corridors | Long term (≥ 4 years) |

| CCS-linked blue-hydrogen projects unlocking new gas off-take | +0.60% | South Australia, Northern Territory, Western Australia | Long term (≥ 4 years) |

| Digital oil-field & remote-ops cutting offshore OPEX | +0.90% | Offshore Western Australia, Bass Strait, Browse Basin | Short term (≤ 2 years) |

| Fast-track exploration permits under NOPTA reforms | +0.40% | Commonwealth offshore waters | Medium term (2-4 years) |

| Critical-minerals boom driving diesel & LNG off-grid use | +0.50% | Western Australia, Northern Territory, Queensland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Domestic & Asian LNG Demand

Domestic wholesale gas prices averaged USD 12-15 per gigajoule in 2024, almost twice the level of exported cargo benchmarks, highlighting the tight local balance that sustains premium contract prices and assures robust cash flows for exporters. Industrial buyers are increasingly securing long-term deals to shield their operations from volatility, which locks in forward revenue for producers but perpetuates supply tension that shapes policy debates around reservation schemes. Japan and South Korea are sourcing Australian LNG for blue-hydrogen conversion, extending the commodity’s strategic role beyond power generation and amplifying future off-take certainty within the Australian oil and gas market. Streamlined NOPSEMA approvals for expansion trains shorten cycle times, although regional community pushback continues to challenge schedule adherence. The interplay of constrained domestic supply, resilient Asian demand, and regulatory facilitation supports sustained liquefied natural gas (LNG) utilization and underpins the growth outlook of the Australian oil and gas market.

CCS-linked Blue-Hydrogen Projects Unlocking New Gas Off-take

Santos commenced CO₂ injection at the Moomba CCS hub in September 2024, targeting 1.7 million t per year and positioning legacy gas assets for low-carbon hydrogen output that satisfies Safeguard Mechanism trajectories.(1)Santos Ltd., “Moomba CCS Project Update,” santos.com Converting the Bayu-Undan field into a regional carbon-storage site offers Southeast Asian emitters an affordable sequestration option, monetizing depleted reservoirs while extending LNG infrastructure relevance. Blue-hydrogen projects reach break-even at gas prices as much as 30% below liquefaction thresholds when carbon-credit revenue offsets capture expenditures, bolstering competitiveness against green variants in hard-to-abate industrial segments. Integrated CCS enables upstream operators to sell both molecules and decarbonization services, a dual-income structure that enhances project bankability. This paradigm shift recasts gas reserves from transition risk to transition enabler, strengthening investment appetite across the Australian oil and gas market.

Digital Oil-Field & Remote-Ops Cutting Offshore OPEX

Woodside’s Angel platform now requires 5,000 person-hours annually, compared to 30,000 before automation, validating how edge analytics and robotics shrink logistics footprints in remote basins. Predictive maintenance algorithms reduce unscheduled downtime, thereby improving recovery factors and extending reservoir economic life —a crucial advantage as Safeguard compliance raises cost baselines. The Scarborough field deploys uncrewed surface vessels for seismic and environmental monitoring, eliminating helicopter sorties, reducing weather-related deferrals by 40%, and cutting fuel burn that drives Scope 1 exposure. Local technology vendors such as Harvest Technology Group have installed digital twins across 15 operator portfolios, fostering a domestic service ecosystem that reduces reliance on foreign engineering talent. These proof points accelerate sector-wide adoption, making digital transformation an essential pillar of competitiveness in the Australian oil and gas market.

Fast-Track Exploration Permits Under NOPTA Reforms

NOPTA reforms trimmed exploration approval cycles from 18-24 months to roughly 12 months by enabling concurrent safety and environmental reviews, unlocking 82 wells drilled in 2024, of which 60 were appraisal wells with near-term tie-back potential.(2)National Offshore Petroleum Safety and Environmental Management Authority, “2024 Annual Offshore Performance Report,” nopsema.gov.au Preference for applications embedding CCS or electrification strengthens the investment case for low-carbon supply, aligning exploration with national emissions objectives. The streamlined pathway eases capital deployment risk, particularly for smaller independents that previously struggled with protracted timeframes. Federal policy clarity contrasts with fragmented state regimes, yet even onshore moratoria are subject to review as supply security climbs in political priority. Faster permitting thus stimulates a broader prospect inventory, which reinforces long-term throughput for pipelines, LNG plants, and the wider Australian oil and gas market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating renewable-power penetration | -0.70% | National, with strongest impact in South Australia and Tasmania | Medium term (2-4 years) |

| Declining conventional reserves → higher lift costs | -0.90% | Bass Strait, Carnarvon Basin, Cooper Basin | Long term (≥ 4 years) |

| Safeguard-Mechanism Scope-1 emission caps (2025-30) | -0.60% | National, affecting all major production facilities | Short term (≤ 2 years) |

| Community opposition delaying on-/off-shore projects | -0.40% | Northern Territory, New South Wales, Great Australian Bight | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Renewable-Power Penetration

Australia added 9.6 GW of renewable capacity in 2024, pushing South Australia's renewable generation to 70% and resulting in periods of negative wholesale prices, which reduce gas peaker run-time and revenue. Battery installations and pumped-hydro projects are increasingly supplying frequency control, thereby diminishing the ancillary-service income historically earned by gas turbines. State-sponsored renewable energy zones bypass thermal generation nodes, further eroding gas demand in new industrial parks. These trends reduce domestic offtake avenues for coal seam gas, intensifying reliance on export channels already capacity-constrained. Developers must therefore justify new gas projects on the merits of export and hydrogen alone, thereby elevating commercial risk and tempering growth prospects for the Australian oil and gas market.

Safeguard-Mechanism Scope-1 Emission Caps (2025-30)

The tightening of the Safeguard Mechanism introduces a 4.9% annual baseline decline, which will cost major operators USD 2-3 billion through 2030 under prevailing Australian Carbon Credit Unit pricing. For Santos, this equates to USD 400-500 million in yearly compliance, incentivizing asset rationalization and accelerated CCS deployment. Woodside earmarked USD 5 billion for abatement programs, illustrating the capital intensity needed to align pre-existing portfolios with regulatory trajectories. Smaller producers face proportionally higher burdens, which may trigger asset divestments or consolidation, thereby reshaping the competitive chessboard. While the mechanism ultimately steers the sector toward lower-carbon models, it constrains free cash flow for exploration and discretionary projects throughout the Australian oil and gas market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Dominance Drives Blue-Hydrogen Transition

The upstream segment accounted for 74.31% of 2025 revenue within the Australian oil and gas market, and its 4.38% CAGR forecast to 2031 underscores how enhanced recovery techniques and carbon-capture projects underpin production resilience despite maturing fields. Blue-hydrogen initiatives, such as the Moomba hub and Bayu-Undan repurposing, stitch CCS economics into gas sales, enabling upstream operators to extract a higher realized value than traditional LNG alone. Midstream activities benefit from sustained throughput demand and pipeline tariff premiums that arise from Eastern Australia bottlenecks, yet expansion remains capital-intensive as route approvals confront landholder concerns. Downstream refining struggles with declining gasoline demand and renewable diesel mandates, but pivots toward petrochemical feedstocks and low-carbon fuels that leverage existing process units.

Upstream investment strategies now combine infill drilling, subsea tie-backs, and remote-asset management to keep lift costs from rising in depleted reservoirs, while carbon-credit revenue generated by CCS drives incremental returns that buffer volatile spot LNG prices. Midstream firms continue to implement loop and compression upgrades to enhance deliverability into southeastern hubs, where wholesale prices peak, a trend that reinforces pipeline revenue stability. By contrast, refining rationalization may accelerate as electric-vehicle uptake pressures gasoline margins, although residual demand from heavy transport preserves a core utilization floor. Collectively, these dynamics ensure the upstream segment remains the anchor of value creation, shaping strategic capital flows across the Australian oil and gas market.

By Location: Offshore Assets Lead Digital Transformation

Offshore installations captured 85.40% of market value in 2025 and are projected to record a 4.18% CAGR as autonomous operations, fiber-optic reservoir monitoring, and uncrewed surface vessels redefine cost structures and safety benchmarks. Federal jurisdiction provides permitting certainty that contrasts with onshore regulatory fragmentation, enabling large projects, such as Scarborough and Browse, to proceed under clearer environmental frameworks. Deep-water developments leverage shared floating production, storage, and offloading units to dilute capital overhead across adjacent fields, sustaining economies of scale that remain out of reach for many onshore ventures.

Onshore growth is nevertheless meaningful in Queensland’s coal seam gas sector, which supplies backfill feedstock to Gladstone LNG while reducing unit logistics costs through dense well clusters. The Beetaloo Basin holds significant shale potential, yet it carries a social license risk that elongates development timelines and may impose additional water management expenses. Victoria’s fracking ban and New South Wales’s exploration limits confine investor appetite, although incremental production from legacy Cooper Basin fields still offsets some eastern-seaboard demand. Overall, the offshore segment’s digital-enabled productivity gains strengthen its dominance, but onshore plays continue to provide short-cycle volumes that mitigate supply variability within the Australian oil and gas market.

By Service: Decommissioning Emerges as Growth Engine

Construction and brownfield expansion services held a 46.55% share of 2025 expenditure, reflecting ongoing facility build-outs and maintenance across the North West Shelf, Gippsland, and Surat hubs. Yet decommissioning exhibits the highest momentum at a 5.42% CAGR through 2031, catalyzed by the government’s USD 60 billion Offshore Resources Decommissioning Roadmap and December 2024 formation of the Offshore Decommissioning Directorate, which clarified liability and tax-deductibility rules. Platform dismantling contracts, such as Allseas’s 12-unit Gippsland award and McDermott’s Harriet Alpha project, affirm the commercial scale and technical complexity of upcoming work scopes.

Contractors specializing in heavy-lift, subsea cutting, and rig recycling face a multi-decade backlog, while operators weigh partial removals against full-facility clearance to meet emerging environmental expectations. Concurrently, predictive-maintenance programs and integrity analytics extend asset life, where they also defer abandonment duty and smooth workforce utilization curves for service suppliers. Turnaround services remain essential for aging LNG trains and gas plants, although the person-hour intensity has decreased as robotics perform internal vessel inspections that previously required scaffolding and confined-space entry. The interplay of life-extension technology and statutory retirement milestones will shape the revenue mix of construction, maintenance, and dismantling, redefining service-sector competitiveness throughout the Australian oil and gas market.

Geography Analysis

Western Australia anchors export activity, with the North West Shelf, Pluto, and Ichthys ventures supplying steady LNG cargoes to North Asia while new digital platforms extend field life and efficiency. Scarborough’s first gas in October 2024 validated the unmanned-vessel surveillance model, reinforcing investor confidence in remote operations for frontier basins. The state’s established marine support infrastructure and federal regulatory clarity streamline project sanctioning, sustaining its primacy within the Australian oil and gas market.

Queensland’s coal seam gas industry underpins three Gladstone LNG plants, providing flexible backfill that mitigates reservoir decline elsewhere and supports domestic offtake through interconnected pipeline grids. High pipeline-tariff differentials across the Wallumbilla hub encourage spot-market arbitrage, while exploration expenditures rose 57.3% year-on-year to USD 390.1 million by December 2024, signaling renewed appraisal momentum. Eastern Australia’s tight supply, however, exposes manufacturers to elevated input costs, sparking political debate about reservation mechanisms that could redirect export volumes inward.

The Northern Territory’s Beetaloo Basin aims to commercialize shale gas, but development faces community resistance and water-use constraints that complicate approval timelines. South Australia’s Cooper Basin hosts the Moomba CCS-blue-hydrogen complex, positioning the state as a carbon-services hub that attracts regional emitters seeking reliable sequestration. Tasmania showcases near-100% renewable power generation, while maintaining a small LNG import capacity for industrial peaking, illustrating its geographic diversity in the energy mix. Victoria’s aging Bass Strait fields are facing depletion, prompting operators to consider near-term decommissioning or tie-backs to shared hubs, whereas New South Wales limits exploration to designated zones, constraining reserve replacement. These regional distinctions collectively influence capital allocation and supply security across the Australian oil and gas market.

Competitive Landscape

Woodside, Santos, and a cohort of international majors dominate integrated operations; yet, market concentration remains moderate, as mid-tier independents capitalize on niche opportunities and new entrants pursue energy-transition strategies. The ADNOC-led consortium’s USD 18.7 billion bid for Santos, announced in November 2024, could recalibrate ownership patterns and intensify competitive pressure on LNG marketing channels if completed.(5)Santos Ltd., “Response to ADNOC Consortium Proposal,” santos.com Strategic differentiation increasingly hinges on digital operations proficiency, with Woodside’s unmanned platforms and Santos’s CCS integration setting performance benchmarks that others rush to emulate.

Operators allocate larger shares of capital expenditure (capex) to emissions-reduction projects, as evidenced by Woodside’s USD 5 billion abatement commitment and Origin’s divestment of upstream assets to finance renewable growth, reflecting how shareholder expectations are pivoting toward decarbonization credentials. International oil companies leverage their global technology portfolios to secure project operatorship, as totalEnergies applies its floating offshore wind expertise to electrify remote platforms, thereby lowering Scope 1 emissions and meeting Safeguard trajectories. Simultaneously, local service firms specializing in autonomy, AI analytics, and heavy-lift decommissioning gain exportable expertise, reshaping competitive dynamics within the Australian oil and gas market supply chain.

Regulatory compliance costs under the Safeguard Mechanism act as a scale filter, advantaging capital-strong players who can fund offset projects or incorporate internal carbon prices into investment decisions. NOPSEMA’s safety oversight preserves operational standardization; however, the agency’s accelerated approvals reward project proponents who embed CCS or electrification into early design. As renewable penetration rises, gas producers with integrated hydrogen or carbon-management pathways secure superior market access, reinforcing a virtuous circle of technology leadership and policy alignment that is redefining the contours of rivalry across the Australian oil and gas market.

Australia Oil And Gas Industry Leaders

TotalEnergies SE

Chevron Corporation

BP PLC

Shell PLC

ExxonMobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: The Australian Government established the Offshore Decommissioning Directorate to oversee USD 60 billion in end-of-life work spanning 30-50 years, providing process clarity that accelerates platform removal schedules.

- November 2024: An ADNOC-led consortium tabled a USD 18.7 billion acquisition offer for Santos, the largest prospective deal in the sector's history and a potential catalyst for reshaping the LNG portfolio.

- October 2024: Woodside achieved first gas at Scarborough, employing uncrewed surface vessels that reduce offshore operating costs by more than 80% while enhancing safety.

- September 2024: Santos initiated CO₂ injection at Moomba CCS, Australia’s first commercial-scale sequestration project, capable of storing 1.7 million t per year tied to blue-hydrogen output.

Australia Oil And Gas Market Report Scope

Oil and natural gas markets are major industries in the energy market and play an influential role in the global economy as the world's primary fuel source. The processes and systems involved in producing and distributing oil and gas are highly complex, capital-intensive, and require state-of-the-art technology.

The Australian oil and gas market is segmented by sector into upstream, midstream, and downstream. The market sizing and forecasts have been done based on volume (thousand barrels per day).

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Service

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

| By Sector | Upstream |

| Midstream | |

| Downstream | |

| By Location | Onshore |

| Offshore | |

| By Service | Construction |

| Maintenance and Turn-around | |

| Decommissioning |

Key Questions Answered in the Report

What is the current value of the Australia oil and gas market?

The Australia oil and gas market size reached USD 12.18 billion in 2026 and is forecast to keep expanding through 2031.

How fast is the sector growing over 2026-2031?

Aggregate revenue is projected to rise at a 3.94% CAGR as operators pursue higher-value, lower-carbon opportunities.

Which segment holds the largest revenue share?

Upstream operations led with 74.31% of Australia oil and gas market share in 2025, reflecting LNG export dominance.

Why is decommissioning considered a growth engine?

More than USD 60 billion in end-of-life offshore work has been identified, giving decommissioning a 5.42% CAGR through 2031.

How are emission regulations affecting investment?

Tightening Scope 1 caps under the Safeguard Mechanism redirect capital toward CCS, electrification, and digital optimization projects.

Where are new exploration permits being accelerated?

NOPTA reforms cut approval times in Commonwealth offshore waters by about 35%, stimulating renewed appraisal drilling activity.

Page last updated on: