Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.64 Billion |

| Market Size (2026) | USD 1.76 Billion |

| Market Size (2031) | USD 2.14 Billion |

| Growth Rate (2026 - 2031) | 3.91% CAGR |

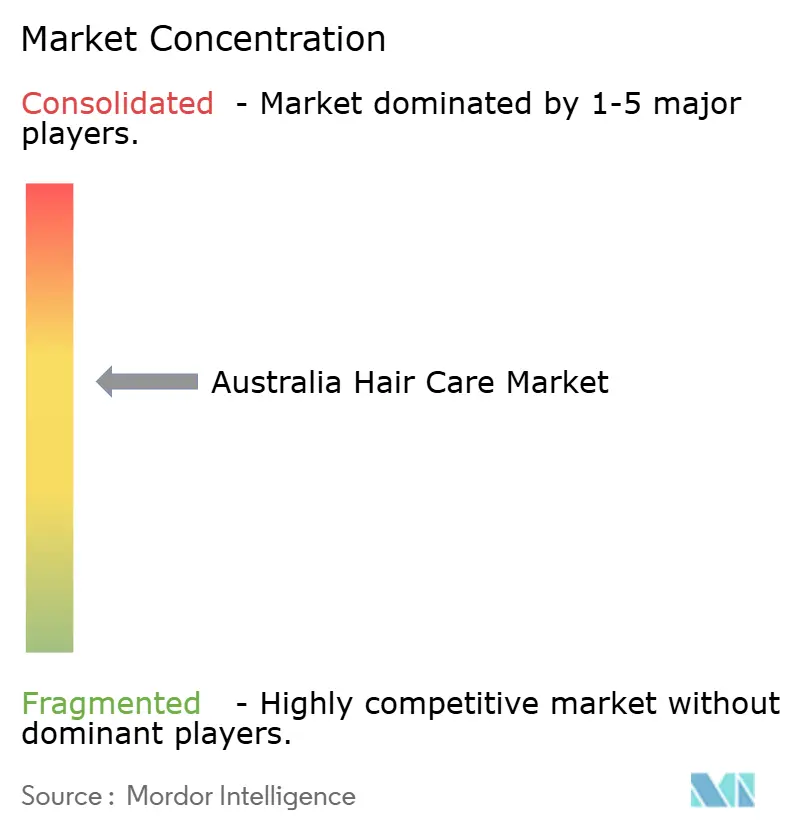

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Hair Care Market Analysis by Mordor Intelligence

The Australia Hair Care Market size was valued at USD 1.64 billion in 2025 and estimated to grow from USD 1.76 billion in 2026 to reach USD 2.14 billion by 2031, registering a CAGR of 3.91% during the forecast period 2026-2031. The hair care market in Australia is growing, driven by increasing consumer focus on scalp health and damage repair. Consumers are seeking products that address concerns such as anti-hair-fall, hydration, and bond strengthening, tailored to challenges like sun exposure, hard water, and frequent styling. There is a rising demand for clean-label and natural formulations, including sulfate-free, silicone-free, vegan, and botanical-based products, as shoppers pay closer attention to ingredient lists and prefer gentle, daily-use options. The strong salon culture in the country contributes to premiumization, with professional treatments influencing at-home routines that incorporate masks, serums, and leave-in conditioners. Furthermore, social media trends and influencer-driven routines are encouraging product experimentation, particularly in areas like color protection, curl definition, and personalized care for specific hair types. This has led to increased product rotation and the adoption of multi-step routines, moving beyond the traditional shampoo-and-conditioner approach.

Key Report Takeaways

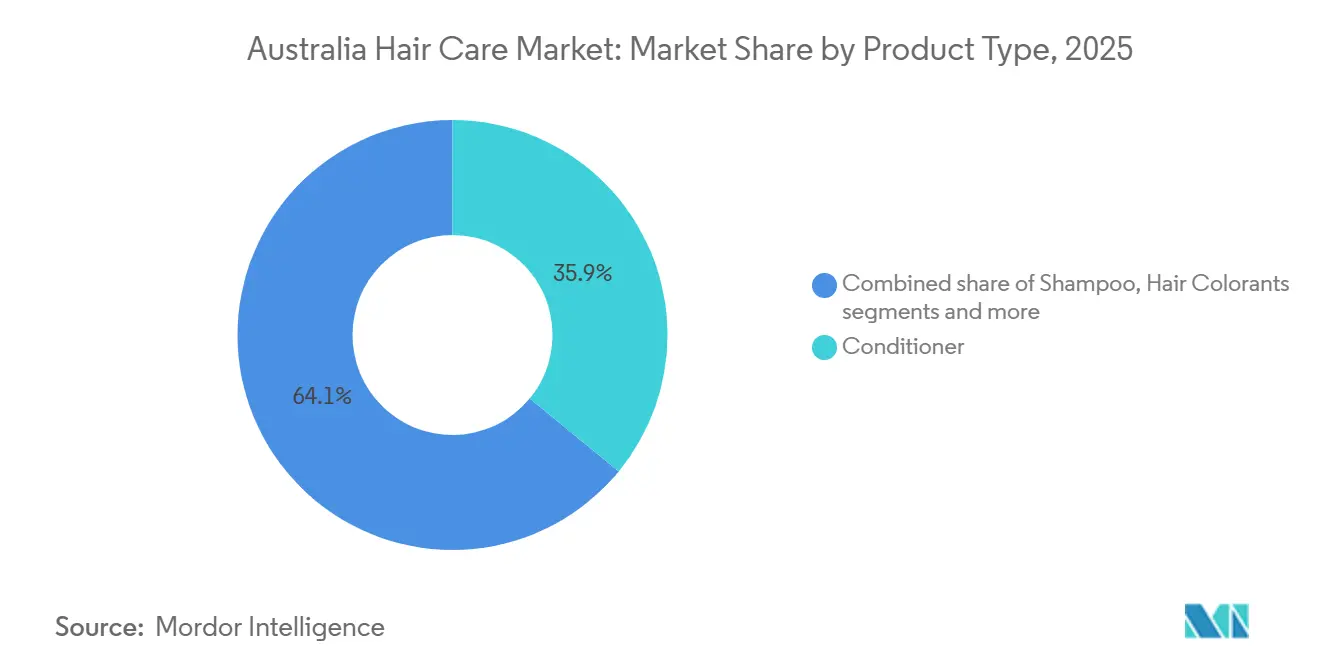

- By product type, conditioner led with 35.94% of Australia hair care market share in 2025, whereas hair styling products are forecast to clock the fastest 5.01% CAGR through 2031.

- By category, conventional offerings controlled 83.74% share in 2025, while organic products are on track for a 5.64% CAGR during 2026-2031.

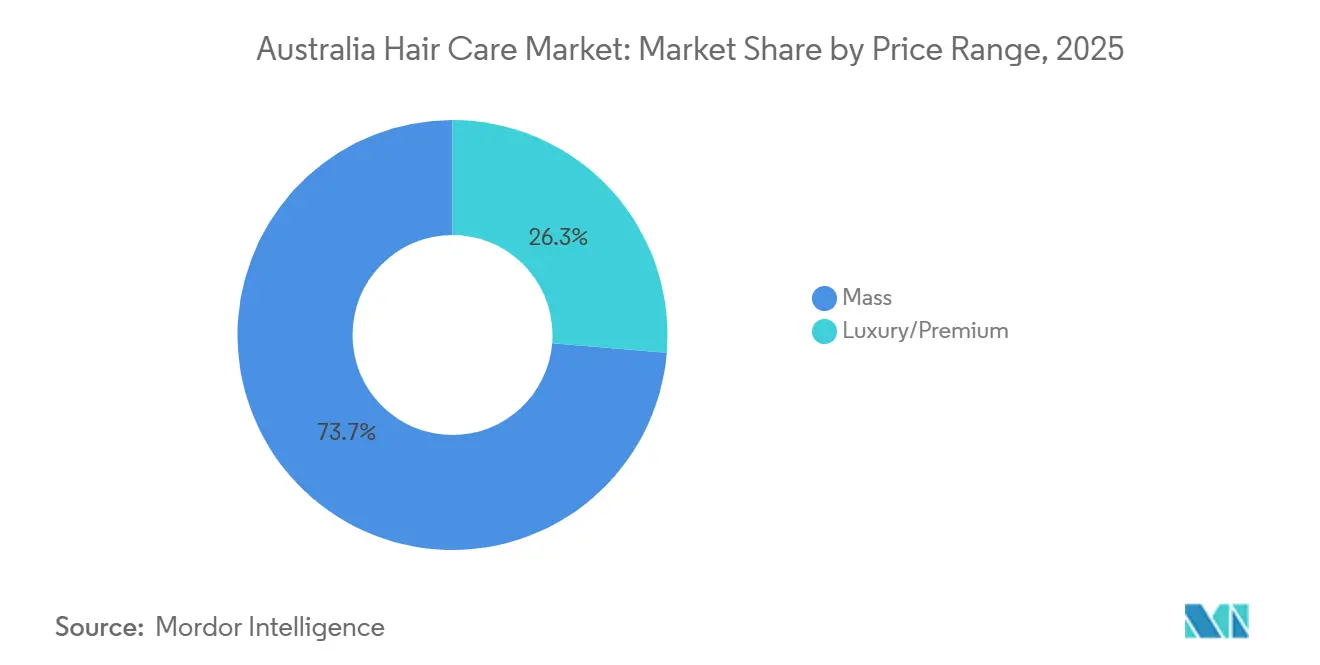

- By price range, mass products dominated with 73.68% share in 2025, yet luxury/premium is projected to expand at a robust 5.90% CAGR.

- By distribution channel, supermarkets/hypermarkets captured 41.55% share in 2025, but online retail stores are positioned for a leading 6.15% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising focus on scalp wellness and holistic hair care routines | +0.9% | National, with early adoption in Sydney, Melbourne, Brisbane metro areas | Medium term (2-4 years) |

| Ageing consumers driving demand for anti-hair-fall and coloring products | +0.8% | National, concentrated in 50+ demographic cohorts | Long term (≥ 4 years) |

| Continuous innovation in hair color formulations | +0.6% | National, premium channel focus | Medium term (2-4 years) |

| Shift toward sustainable products and eco-friendly packaging | +0.7% | National, stronger in urban centers and Gen Z/Millennial segments | Long term (≥ 4 years) |

| Expansion of the men's grooming category | +0.5% | National, with higher penetration in metro markets | Medium term (2-4 years) |

| Increasing preference for customized hair care solutions | +0.4% | National, early adopters in digital-native channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising focus on scalp wellness and holistic hair care routines

The concept of "skinification" in hair care, applying the same level of care to the scalp as to facial skin, is transforming product formulations and consumer habits. Brands are increasingly emphasizing scalp serums, exfoliants, and microbiome-balancing treatments as essential components of hair care routines rather than optional extras. For example, in October 2025, Kadūra Beauty, a Sydney-based company, entered the Australian haircare market with a clean, botanical-focused product line aimed at health-conscious consumers. The vegan, pH-balanced formulations are free from silicones, sulphates, and microplastics, combining native botanicals such as Guarana, Kakadu Plum, and Lemon Peel Oil with proven active ingredients to deliver salon-quality results. The product range includes Shea Sanctuary Conditioner, Root Revival Shampoo, Deep Clean Scalp Scrub, Root Revival Scalp Serum, Hydra Bomb Hair Mask, and Botanical Hair Perfume Oil, all designed to balance performance with eco-responsibility. This trend is not limited to premium brands; mass-market players are also adopting scalp-focused messaging to justify higher price points and stand out in the competitive shampoo and conditioner market. Additionally, the shift is influencing hair styling products, as consumers increasingly prefer lightweight, non-comedogenic formulations that avoid clogging hair follicles.

Ageing consumers driving demand for anti-hair-fall and coloring products

Australia's ageing population is increasingly influencing hair care purchasing patterns, driving demand for anti-hair-fall treatments and hair coloring products designed to support a youthful appearance. Older consumers often face issues such as thinning hair, greying, and reduced hair density, prompting the use of strengthening shampoos, scalp tonics, and gentle dyes tailored for sensitive scalps. In response, brands are focusing on mild, nourishing formulations that offer conditioning and coverage benefits, moving beyond purely cosmetic coloring. This demographic trend is notable: as per the World Bank Group, Australia had 4,821,999 individuals aged 65 and above in 2024, expanding the key consumer base for restorative and appearance-enhancing hair care products[1]Source: The World Bank Group, "Population ages 65 and above, total - Australia," data.worldbank.org.

Shift toward sustainable products and eco-friendly packaging

Increasing environmental awareness is driving Australian consumers to choose hair care products that prioritize sustainability and eco-friendly packaging. Consumers are showing a preference for biodegradable formulas, plant-based ingredients, refillable packaging, and bottles made from recycled or recyclable materials, while avoiding products associated with microplastics or excessive plastic waste. In response, brands are launching concentrated shampoos, solid bars, and low-water formulations to minimize packaging and reduce transportation impacts. These products also feature transparent labeling regarding sourcing and environmental impact. This shift toward sustainable consumption is shaping purchasing decisions across both mass-market and premium segments, positioning eco-friendly practices as a significant competitive factor in the Australian hair care market.

Expansion of the men’s grooming category

The growth of the men’s grooming segment is significantly contributing to the expansion of the Australian hair care market, as men increasingly adopt comprehensive personal care routines beyond basic shampoo usage. There is a growing demand for products such as scalp-care shampoos, anti-dandruff solutions, styling creams, pomades, and hair-thickening treatments tailored to male hair types and shorter washing cycles. Marketing efforts emphasizing professional appearance and self-care, combined with the influence of barbershops and social media trends, are driving repeat purchases and the use of multiple products. This trend is further supported by demographic factors, according to the World Bank Group, males constituted 50% of Australia’s population in 2024, offering a substantial and engaged consumer base for targeted hair care products[2]Source: The World Bank Group, "Population, male (% of total population) - Australia," data.worldbank.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns about harmful effects of synthetic ingredients | -0.4% | National, amplified by social media and influencer scrutiny | Short term (≤ 2 years) |

| Strict safety standards and regulatory requirements | -0.3% | National, enforced by TGA, AICIS, ACCC | Medium term (2-4 years) |

| Strong rivalry among domestic and global brands | -0.5% | National, intensified in metro markets (Sydney, Melbourne, Brisbane) | Medium term (2-4 years) |

| Counterfeit products affecting market growth | -0.3% | National, concentrated in online marketplaces and gray-market channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Concerns about harmful effects of synthetic ingredients

Consumer concerns regarding formaldehyde-releasing preservatives, parabens, sulfates, and silicones limit formulation flexibility and compel brands to reformulate to remain competitive. The Therapeutic Goods Administration (TGA) regulates cosmetics under the Therapeutic Goods Act 1989, while the Australian Industrial Chemicals Introduction Scheme (AICIS) evaluates chemical safety, creating a dual compliance requirement. Additionally, the Consumer Goods (Cosmetics) Information Standard 2020 mandates full ingredient disclosure, enabling consumers to closely examine formulations and increasing scrutiny of controversial ingredients[3]Source: Therapeutic Goods Administration, "Consumer Goods (Cosmetics) Information Standard 2020" tga.gov.au. This regulatory and consumer-driven environment presents challenges for brands. Reformulating to exclude synthetic ingredients often raises costs and may compromise performance attributes such as lather, preservation, or sensory experience. On the other hand, retaining legacy formulations risks reputational harm and potential market share loss to clean-beauty competitors. These pressures are particularly significant for mass-market brands that rely on cost-effective synthetic ingredients, constraining their volume growth and driving defensive innovation strategies.

Strict safety standards and regulatory requirements

Australia's regulatory framework, encompassing the Therapeutic Goods Administration (TGA), Australian Industrial Chemicals Introduction Scheme (AICIS), and Australian Competition and Consumer Commission (ACCC), enforces stringent safety testing, labeling, and advertising standards. These regulations increase market entry costs and delay product launches. While they safeguard consumers and build trust, smaller brands often face challenges due to limited regulatory expertise and financial resources required for compliance. The framework also contributes to information asymmetry, as established companies use regulatory complexity to create barriers to entry, leaving new entrants exposed to delays and legal risks. Additionally, international brands must address Australia's unique requirements, which differ from European Union or United States standards. This often necessitates market-specific formulations or labeling, leading to fragmented supply chains and reduced economies of scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Styling Products Outpace Cleansing Staples

In 2025, conditioners accounted for 35.94% of the product-type market share, making it the largest segment. This dominance is attributed to growing consumer awareness of the importance of conditioning for hair health and manageability. Shampoos, while essential, face increasing competition from low-poo and no-poo trends that promote reduced wash frequency, thereby limiting their growth potential. Hair colorants benefit from dual demand, older consumers seeking gray coverage and younger consumers experimenting with fashion shades. However, the segment faces margin pressures due to advancements in at-home color products, which are narrowing the performance gap with salon services.

Hair styling products, projected to grow at a CAGR of 5.01% through 2031, represent the fastest-growing segment. This growth is driven by the flexibility of work-from-home arrangements, which encourage styling experimentation, and the influence of social media on appearance standards. Additionally, styling products enjoy higher per-unit margins compared to shampoos and conditioners, as they are perceived as discretionary enhancements rather than essential commodities. This perception enables brands to charge premium prices for products such as texturizing sprays, heat protectants, and finishing serums.

By Category: Organic Gains Ground, But Conventional Dominates

Conventional products accounted for 83.74% of the market share in 2025, driven by established consumer preferences, price sensitivity, and the performance benefits of synthetic ingredients in areas such as lathering, preservation, and sensory attributes. In contrast, organic formulations are projected to grow at a CAGR of 5.64% through 2031, supported by the increasing popularity of clean-beauty trends and third-party certification programs like ACO and COSMOS. This growth is primarily concentrated in premium and specialty channels, where consumers are willing to pay higher prices for perceived health and environmental advantages.

Conventional brands are adopting strategies such as launching "clean" sub-brands or reformulating key products to exclude controversial ingredients, thereby blurring the lines between conventional and organic categories. This dual-brand approach enables established players to maintain market share across different price segments without cannibalizing their existing product lines. The organic category's growth is further supported by regulatory developments, such as Australia's alignment with international organic standards, which facilitates imports and exports and allows niche brands to expand regionally.

By Price Range: Premium Outpaces Mass as Consumers Trade Up

Mass-market products accounted for a 73.68% market share in 2025, supported by supermarket and hypermarket distribution channels, competitive promotional pricing, and long-established brand recognition. These products benefit from widespread availability and affordability, making them accessible to a broad consumer base. However, the luxury and premium segments are projected to grow at a compound annual growth rate (CAGR) of 5.90% through 2031. This growth is driven by aging demographics, as older consumers increasingly seek high-quality and effective products, along with a growing emphasis on product efficacy and the trend toward premiumization in self-care.

Premium brands justify their higher price points, which are 2 to 3 times that of mass-market equivalents, by emphasizing ingredient-focused narratives. These include the use of advanced components such as peptides, bond-building technologies, and botanical actives, which appeal to consumers seeking enhanced benefits. Meanwhile, mass-market brands aim to defend their market share through innovation, such as introducing new product formulations, and channel optimization to improve distribution efficiency. However, mass-market growth faces structural challenges, including rising private-label penetration, which offers lower-cost alternatives, intense promotional activity that compresses margins, and a shift in consumer preferences toward premium or organic alternatives, which are perceived as offering better quality and sustainability.

By Distribution Channel: Online Retail Surges as Supermarkets Plateau

Supermarkets/hypermarkets accounted for a 41.55% market share in 2025, benefiting from their widespread presence, convenience, and promotional strategies. Woolworths and Coles lead the grocery retail segment, offering one-stop shopping experiences that encourage hair care product purchases. However, growth in this channel aligns with the overall market rate, limited by a narrower product assortment, lack of personalized services, and competition from specialty and online channels. Convenience and grocery stores cater to fill-in trips but lack the product range necessary to drive discovery or premiumization. Health and wellness stores, such as pharmacies, leverage their trusted advisor role and professional-grade product assortments.

Online retail s aretores projected to grow at a CAGR of 6.15% through 2031, marking the fastest growth among all channels. This expansion is driven by direct-to-consumer brands, subscription-based models, and digital-native consumers who prioritize convenience and product reviews over in-store shopping. Gen Z consumers, in particular, demonstrate a strong preference for online shopping, including social commerce and online-only purchasing, influencing how brands allocate their marketing and distribution resources. Established companies are investing in proprietary e-commerce platforms and partnerships with online marketplaces to meet digital demand. Meanwhile, digitally native brands bypass traditional retail channels, reducing incumbents' channel margins and prompting portfolio adjustments.

Geography Analysis

The Australia Hair Care Market demonstrates distinct dynamics at the national level, with metropolitan areas such as Sydney, Melbourne, and Brisbane serving as key hubs. These cities are characterized by higher disposable incomes, diverse populations, and trend-conscious consumers, which drive the demand for premium products and the adoption of innovative offerings. The higher disposable incomes in these areas allow consumers to spend more on premium and luxury hair care products, while the multicultural populations contribute to a diverse range of hair care needs and preferences. Additionally, the trend-conscious nature of consumers in these cities fosters a market environment that readily embraces new product innovations and premiumization trends.

The regulatory framework in Australia, overseen by the Therapeutic Goods Administration (TGA), the Australian Industrial Chemicals Introduction Scheme (AICIS), and the Australian Competition and Consumer Commission (ACCC), ensures stringent safety and labeling standards. This regulatory environment enhances consumer trust but also increases compliance costs for international market entrants. The Consumer Goods (Cosmetics) Information Standard 2020 requires full ingredient disclosure, enabling consumers to evaluate product formulations closely and driving demand for clean-label products. The requirement for full ingredient disclosure empowers consumers to make informed purchasing decisions, particularly favoring products with transparent and clean-label formulations. This has led to a growing preference for products that are free from harmful chemicals and align with consumer values regarding health and sustainability.

Australia's alignment with international organic and sustainability certifications, such as Australian Certified Organic (ACO), COSMOS, and B Corp, supports cross-border trade. These certifications provide assurance of product quality and sustainability, making it easier for Australian brands to meet international standards and expand into global markets. This alignment allows niche brands to expand regionally and facilitates the export of Australian brands, particularly to Asia-Pacific markets. The Asia-Pacific region, with its growing middle-class population and increasing demand for organic and sustainable products, presents significant opportunities for Australian hair care brands to scale their operations and establish a strong presence in these markets.

Regulatory Landscape

Hair care products sold in Australia sit within a split framework that covers chemical introduction, product classification, and consumer protection. For most shampoos, conditioners, and styling products positioned as cosmetics, ingredient and labeling compliance is shaped by the Consumer Goods (Cosmetics) Information Standard 2020 (mandatory ingredient labeling), while industrial chemical obligations for cosmetic ingredients are handled through the Australian Industrial Chemicals Introduction Scheme (AICIS) under the Industrial Chemicals Act 2019.

When products move into therapeutic positioning, such as medicated anti-dandruff treatments or claims related to hair growth, Therapeutic Goods Administration (TGA) oversight under the Therapeutic Goods Act 1989 may apply, including potential inclusion in the Australian Register of Therapeutic Goods (ARTG). In parallel, the Australian Competition and Consumer Commission (ACCC) sets expectations for labeling and advertising claims, so brands need to substantiate what they say and keep product classification aligned, especially for scalp-treatment and problem-solution lines.

Competitive Landscape

The Australia Hair Care Market exhibits moderate concentration, with global companies such as Procter & Gamble, Unilever, L'Oréal, and Henkel holding a significant market share. This dominance is driven by their extensive product portfolios, large-scale marketing efforts, and multi-channel distribution networks. These companies utilize umbrella brand strategies (e.g., L'Oréal's Elvive, Garnier, and Kérastase, which cater to both mass-market and luxury segments) to appeal to consumers across various price points and life stages. Additionally, they invest in innovation to counter competition from clean-beauty brands and digitally native challengers.

Opportunities are arising in personalized formulations, scalp-health treatments, and sustainable packaging innovations, which can achieve premium pricing without necessitating significant R&D investments. Personalized formulations cater to individual consumer needs, offering tailored solutions that enhance user satisfaction and loyalty. Scalp-health treatments address growing consumer awareness of hair and scalp wellness, creating a niche market with high growth potential. Sustainable packaging innovations align with increasing environmental concerns, appealing to eco-conscious consumers and enabling brands to differentiate themselves in the market.

Emerging players are utilizing direct-to-consumer models to bypass traditional retail channels, leveraging social media and influencer collaborations to enhance brand visibility while reducing customer acquisition costs compared to the mass-media strategies employed by established competitors. However, counterfeit products, especially on online platforms, undermine consumer trust and profit margins, with premium brands being particularly affected due to challenges in controlling gray-market distribution and enforcing intellectual property rights effectively.

Australia Hair Care Industry Leaders

-

The Procter & Gamble Company

-

Unilever PLC

-

Henkel AG & Co. KGaA

-

L’Oréal SA

-

Kao Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven transparency and the shift toward scalp-health create room for differentiated, claim-disciplined product architectures in Australia. The Consumer Goods (Cosmetics) Information Standard 2020 has normalized full ingredient disclosure, increasing consumer scrutiny of sulfates, silicones, preservatives, and other debated inputs. It also raises the bar for evidence-backed marketing under ACCC oversight, which favors brands that pair clear on-pack communication with formulation strategies aligned to clean-label and sensitive-scalp positioning, including microbiome-supportive routines and multi-step regimens influenced by salon culture.

Sustainability and circularity are also moving beyond packaging claims, which widens the practical scope for initiatives tied to manufacturing and waste recovery. In May 2026, Cooper Delivered highlighted its development of sustainable shampoo bar manufacturing and circular waste systems in Katanning, Western Australia, indicating ongoing investment in low-water formats and local supply chain resilience. At the same time, programs such as Sustainable Salons (scaled across more than 1,500 salons in Australia and New Zealand, with reported capability to recover up to 95% of salon waste) provide a professional-channel pathway for brands to test refill, collection, and recycled-material initiatives.

Recent Industry Developments

- April 2026: Aussie (Procter & Gamble) launched a new Dry Shampoo Collection with three variants: Instant Refresh, Instant Volume, and Instant Texture. The rollout expands mass-accessible styling and refresh formats that support multi-step routines and between-wash use, enabling higher-frequency purchases beyond core shampoo and conditioner.

- December 2025: Pantene (Procter & Gamble) released the limited-edition Alix x Pantene Kit featuring the Abundant & Strong 3-Step System in partnership with creator Alix Earle. The collaboration highlights how influencer-led bundles can drive trial and basket-building for treatment systems positioned around shedding reduction and strengthening.

- July 2024: SheaMoisture (Unilever, distributed by Chemcorp International) introduced the Aloe Butter Scalp Care System in Australia, including a sulphate-free shampoo and a pre-wash masque among four products. The launch broadened retail access to scalp-care-focused ranges and reinforced demand for textured-hair and moisture-first positioning in mainstream channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Australia hair care market is counted as the value of hair cleansing, conditioning, coloring, and styling products sold through retail and professional-linked channels within Australia, measured in current US dollars.

Scope exclusions: Hair tools and appliances (such as dryers, straighteners, and clippers) are excluded from this market definition.

Segmentation Overview

-

By Product Type

- Shampoo

- Conditioner

- Hair Colorants

- Hair Styling Products

- Other Hair Care Products

-

By Category

- Organic

- Conventional

-

By Price Range

- Mass

- Luxury/Premium

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Health and Wellness Stores

- Online Retail Stores

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

To build the starting data set, we leaned on public, non-paywalled sources that explain demand conditions and category movement in Australia, including household spending and retail turnover context from the Australian Bureau of Statistics. Trade and tariff releases from the Australian Border Force and UN Comtrade were also used as directional checks on import intensity for packaged personal care, which helps in sense-checking supply availability.

We also reviewed materials that describe products and claims trends, such as National Industrial Chemicals Notification and Assessment Scheme (AICIS) guidance for ingredient and compliance context, plus peer-reviewed cosmetic science literature for common formulation and performance themes. Company annual reports, investor presentations, and retailer and association websites were used to understand channel mix, promotion intensity, and pricing cues. Where a public document was not granular enough, paid subscription inputs for company financials and shipment-level import and export indicators were used as supporting inputs. These desk research sources are illustrative, and many other public and paid references were reviewed to collect, cross-check, and clarify data points.

Primary Interviews and Surveys

Primary conversations were used to pressure-test the desk view and fill gaps that are hard to read from public data, especially around price ladders, promo depth, and how fast sub-categories like treatments and colorants are rotating. We spoke with a mix of manufacturers, distributors, retailers, salon-side sellers, and category managers across Australia so assumptions on channel shares, mix shifts, and average selling price (ASP) movement could be confirmed before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | |

| Mid tier: 56% | Functional/Unit leaders: 43% | |

| Smaller Players: 17% | Managers: 45% |

Market-Sizing & Forecasting

The core sizing starts with a top-down build that reconstructs the demand pool from Australia-focused category spending and retail channel turnover signals, which are then split into hair care using category mix inputs. Results are then corroborated with selective bottom-up approximations, such as sampled price per pack checks across key channels multiplied by estimated movement ranges, followed by supplier and distributor sense-checks.

Inputs that matter most in this market include price tier mix (mass versus premium), channel mix shifts (supermarkets, specialty, convenience, and online), and product mix movement across shampoo, conditioner, colorants, and styling. We also track promo intensity and private label presence where it is visible, because these two items can shift value even when unit movement looks stable. When a channel or product line has thin public visibility, the gap is handled by using proxy shares from adjacent categories and then re-tested in interviews until the ranges narrow.

For forecasting, we used scenario analysis supported by a simple multivariate regression as a cross-check, where the drivers include household consumption trend, retail turnover, and expected pricing progression. The final forecast path is the one that stays consistent with the category cues shared by market participants and the observed pace of premiumization in Australia.

Data Validation & Update Cycle

Before sign-off, estimates are triangulated across independent signals so the value totals align with what the market can realistically absorb through the main channels. Outliers are flagged when growth jumps cannot be explained by pricing, mix, or a visible distribution shift, and then the assumption is revisited with follow-up checks.

A second analyst reviews the model structure, year-on-year movement, and key assumptions, after which a final review is completed to confirm the story matches the numbers. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major pricing resets, channel disruptions, or regulation-driven claim changes. Right before delivery, we do a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Australia Hair Care Market Market Size Compared With Other Published Estimates

Published market sizes for Australia hair care can look different even when the topic sounds the same, because the counted products, pricing basis, and the time window behind the estimates are not always aligned. Differences also come from how each study treats premiumization, promotions, and whether the split by channel is updated using fresh retailer reality.

Hair tools and appliances sit outside Mordor Intelligence's scope, which removes a common add-on bucket that can quietly inflate totals in beauty and personal care sizing, especially when value is taken at higher retail price points.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.64 B (2025) | |

| Industry Publisher A | USD 1.36 B (2025) | Often reflects a narrower valuation lens with limited visibility on promo depth and premium mix, which can understate value in channels where pricing ladders move quickly. |

| Syndicated Source B | USD 1.34 B (2024) | Uses an earlier base year and may apply a different retail selling price and tax treatment, which shifts the total when converted and rolled forward. |

The spread in the table is mainly explained by scope alignment, base-year timing, and how price progression is handled across channels. By tying the total to observable channel movement and re-checking the key mix assumptions, the final number stays traceable to inputs that can be repeated and updated each year.

Key Questions Answered in the Report

How big will the Australia hair care market be by 2031?

It is projected to reach USD 2.14 billion, expanding at a 3.91% CAGR from 2026 to 2031.

Which segment is expected to grow fastest through 2031?

Hair styling products are set to post the highest 5.01% CAGR as consumers seek salon-quality finishing at home.

Is online retail overtaking supermarkets for hair products?

Online retail stores are forecast to grow at 6.15% CAGR outpacing supermarkets.

Why are premium hair care brands gaining traction?

Aging populations demanding bond-repair science and scalp treatments are willing to pay premiums, driving luxury/premium growth of 5.90% CAGR.

Page last updated on: