Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

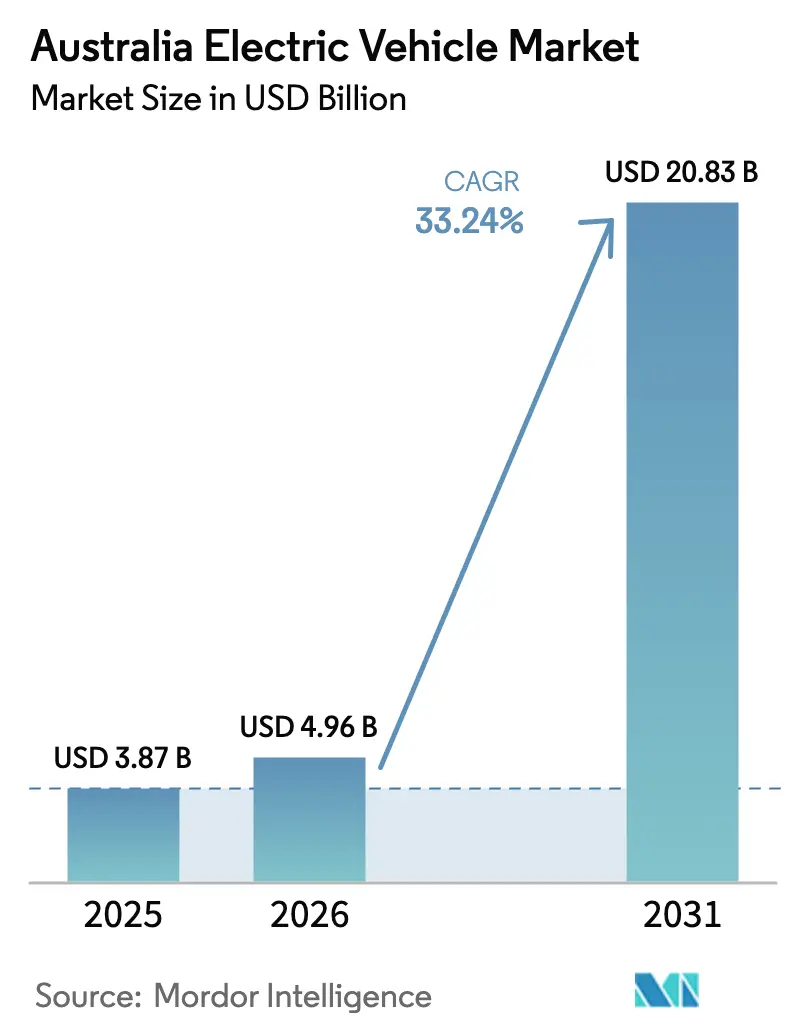

| Base Year Market Size (2025) | USD 3.87 Billion |

| Market Size (2026) | USD 4.96 Billion |

| Market Size (2031) | USD 20.83 Billion |

| Growth Rate (2026 - 2031) | 33.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Electric Vehicle Market Analysis by Mordor Intelligence

The Australia electric vehicle market size was valued at USD 3.87 billion in 2025 and is estimated to grow from USD 4.96 billion in 2026 to reach USD 20.83 billion by 2031, at a CAGR of 33.24% during the forecast period (2026-2031). The nation’s new Vehicle Efficiency Standard, effective January 2025, is forcing automakers to increase battery-electric vehicle allocations, while state rebates and fringe-benefit tax waivers lower ownership costs and widen the addressable base. Chinese brands are intensifying price competition in the sub USD 30,000 bracket, eroding Tesla’s first-mover advantage and nudging legacy OEMs to accelerate right-hand-drive launches. Inter-city fast-charging corridors now span every mainland capital, easing range anxiety and enabling longer-distance household adoption. Corporate decarbonization pledges by ASX-listed companies, combined with Australia’s world-leading rooftop solar penetration, are amplifying total-cost-of-ownership advantages that favor EV uptake.

Key Report Takeaways

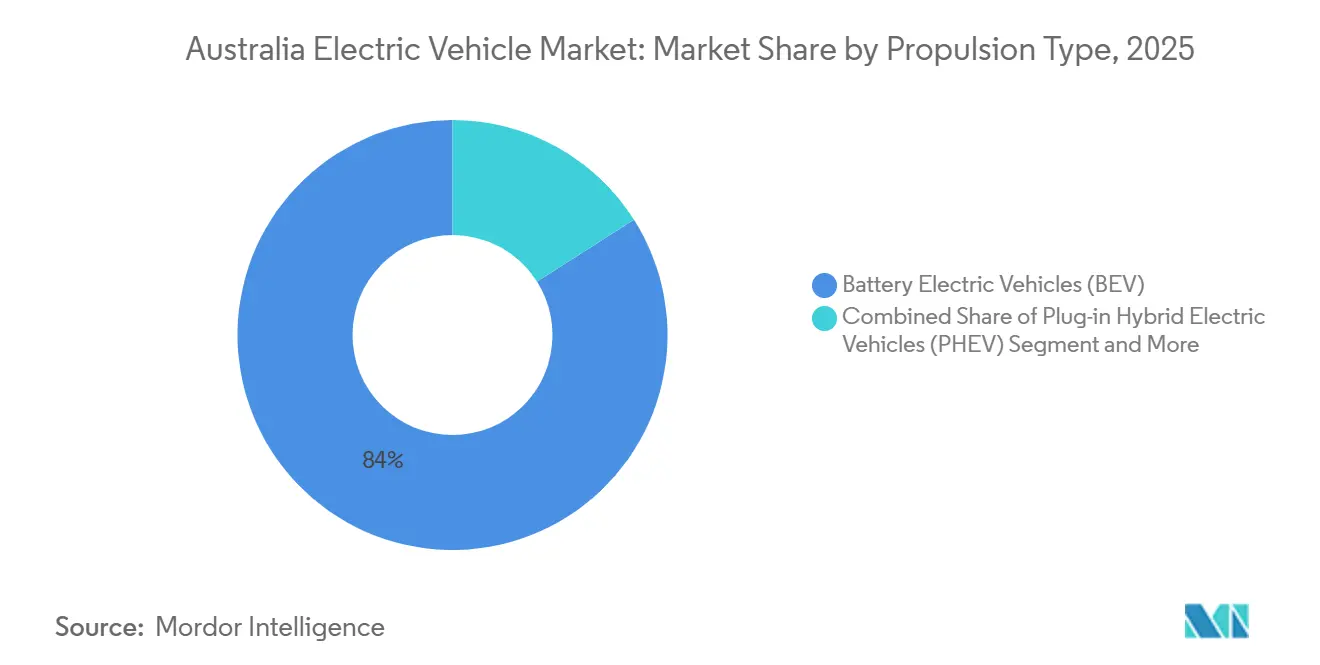

- By propulsion type, battery-electric vehicles accounted for 84.01% in 2025, while fuel-cell electric vehicles are on track for a 43.15% CAGR through 2031.

- By vehicle type, passenger cars accounted for 83.25% of 2025 registrations, while light commercial vehicles are the fastest-growing segment, with a 35.02% CAGR to 2031.

- By range, the 200-400 km group held a 47.13% share in 2025, whereas the 400-600 km cohort is projected to grow at a 34.12% CAGR by 2031.

- By battery chemistry, nickel-cobalt chemistries accounted for 58.23% of battery demand in 2025; meanwhile, lithium iron phosphate cells are projected to rise at a 37.55% CAGR by 2031.

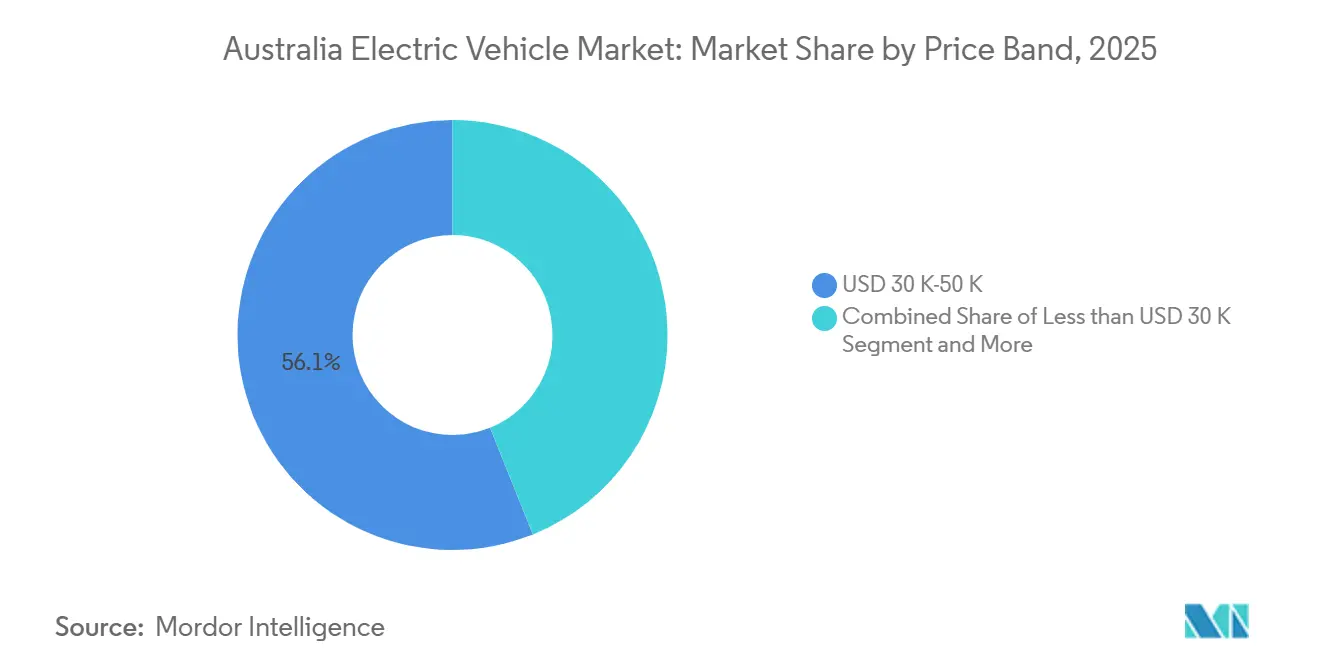

- By price band, the USD 30,000-50,000 models accounted for 56.11% of 2025 sales, but sub-USD 30,000 models are expanding at a 38.24% CAGR by 2031.

- By ownership model, private individuals held a 74.25% share in 2025, while corporate fleets are advancing at a 34.75% CAGR by 2031.

- By state/territory, Queensland captured 30.05% of 2025 deliveries, while New South Wales is forecast to accelerate at 36.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Electric Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Entry of Sub-USD 30 K Brands | +7.1% | Metro and peri-urban markets nationwide | Short term (≤ 2 years) |

| Federal and State Incentive Schemes | +6.2% | NSW, VIC, QLD, ACT | Medium term (2-4 years) |

| Expansion of Inter-City Fast-Charging | +5.8% | Interstate highways nationwide | Medium term (2-4 years) |

| New Vehicle Efficiency Standard | +5.4% | National | Medium term (2-4 years) |

| Corporate Fleet Decarbonization Commitments | +4.5% | Major metros nationwide | Long term (≥ 4 years) |

| High Rooftop Solar Penetration | +3.9% | QLD, SA, WA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Entry of Sub-USD 30 k Chinese Brands (BYD, MG) Broadening Consumer Base

BYD, MG, and GWM have begun offering compact EVs in Australia at more affordable prices, positioning them significantly below established competitors. These manufacturers utilize cost-effective Lithium Iron Phosphate batteries, reducing battery expenses while still achieving competitive ranges. Standard inclusions such as adaptive cruise control, 360-degree cameras, and over-the-air updates help dispel any notions of compromise associated with budget models. Additionally, fringe-benefit-tax exemptions further lower effective lease costs over a multi-year period[1]“Fringe Benefits Tax Exemption for Electric Cars,” Australian Taxation Office, ato.gov.au. Consequently, Australia’s electric vehicle market is witnessing a surge in demand, particularly from first-time buyers who were once priced out of the segment.

Federal and State Incentive Schemes Accelerating EV Uptake

New South Wales provides rebates and waives stamp duty. Queensland offers subsidies, while the ACT removes both stamp duty and registration fees. Victoria's decision to repeal its road-user charge in 2024 eliminated a significant barrier to adoption. Fleet operators take advantage of these jurisdictional differences by registering vehicles in regions with the most attractive incentives and deploying them nationwide. With the addition of federal fringe-benefit-tax relief, many electric vehicles (EVs) now achieve price competitiveness with internal combustion engine (ICE) alternatives at the point of purchase. This comprehensive support is expected to significantly enhance the growth rate during the forecast period.

Expansion of Inter-City Fast-Charging Corridors (NRMA, Chargefox, Evie)

NRMA, Chargefox, and Evie Networks have installed numerous DC fast chargers, significantly reducing average highway gaps[2]“Electric Vehicle Fast-Charging Network,” NRMA, nrma.com.au. Priority 150-350 kW hardware restores 300 km of range in 20-30 minutes, easing charging-time anxiety. The Perth-Albany corridor in Western Australia now features strategically placed chargers, paving the way for a surge in EV tourism. To address grid-capacity challenges in rural towns, battery-backed demand-management systems, supported by federal grants, have been introduced. As corridor coverage improves, consumers are increasingly gravitating towards mid-range models, leading to a notable shift in market dynamics.

New Vehicle Efficiency Standard Creating Supply-Side Push

By the mid-term, the NVES will impose stricter CO₂ emission limits for passenger cars, with further tightening expected by the long-term. Vehicles exceeding these limits will face significant penalties for each additional gram of emissions. Toyota, Volkswagen, and Hyundai must expand zero-emission allocations or buy credits from EV-heavy competitors like Tesla and BYD. Automakers increasingly bundle EVs with profitable ICE utes to hit fleet targets and guarantee domestic supply. The rule turns compliance into the dominant constraint, ensuring EV availability even if retail sentiment cools. This supply-side mandate underpins long-run price competitiveness and volume growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited EV Ute/4x4 Availability | -4.2% | Rural WA, NT, QLD | Medium term (2-4 years) |

| Supply Chain Bottlenecks and Wait Times | -3.8% | National | Short term (≤ 2 years) |

| Suburban Grid Constraints | -3.1% | Fringe suburbs of major metros | Medium term (2-4 years) |

| Immature Used-EV Resale Market | -2.9% | Metro used-car hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of EV Utes / 4x4 Models Vital for Rural Buyers

Utes account for 20% of national new-vehicle demand, yet only LDV’s eT60 and BYD’s Shark 6 PHEV are available and compromise on towing or range. Ford’s Ranger PHEV and F-150 Lightning remain unallocated for right-hand-drive production, preserving diesel dominance. Rural operators need 3.5-ton towing and 400 km real-world range at sub-USD 70,000 price points, specifications that current batteries cannot deliver profitably. Limited options slow rural adoption and subtract an estimated 4.2 percentage points from market CAGR. OEMs that first satisfy ute buyers stand to capture a lucrative white-space segment.

Supply Shortages and Extended Wait-Lists for Popular Models

In 2024, buyers of the Tesla Model Y and Hyundai Ioniq 5 faced significant waiting periods[3]“Ioniq 5 Delivery Update,” Hyundai Motor Company Australia, hyundai.com.au. This delay was due to right-hand-drive build slots being prioritized for the larger markets of the United Kingdom and Japan. Consumers, unwilling to endure long waits, turned to Chinese brands with shorter lead times, resulting in a decline in the incumbents' market share. In response, OEMs are contemplating local assembly to secure their allocations. However, the pipeline's tightness is expected to continue for the foreseeable future. This situation not only defers demand but also encourages brand switching, thereby impacting market growth. Market volumes are expected to stabilize once global capacity for right-hand-drive models expands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Battery Dominance With Fuel-Cell Upside

Battery Electric Vehicles (BEVs) captured 84.01% of 2025 registrations, while Fuel-cell Electric Vehicles (FCEVs) sold fewer units yet promise a 43.15% CAGR by 2031 as hydrogen corridors emerge. The growing allocation of BYD, Tesla, and MG models ensures that BEVs retain their structural leadership despite penalties on hybrids from NVES. Plug-in hybrids address regional buyers’ range concerns, though real-world charging habits will ultimately determine the environmental benefits. Fuel-cell uptake hinges on Canberra–Sydney refueling nodes scheduled for the coming years, with Hyundai’s Nexo fleet pilots guiding early demand. Overall, the choice of propulsion remains a core variable influencing the trajectories of Australia's electric vehicle market.

Metro commuters are opting for BEVs due to their low running costs, while regional drivers continue to value the versatility of PHEVs. Government fleet targets are driving an increased focus on zero-emission purchases, bolstering confidence in large BEV orders and their residual values. Although FCEV costs remain high, transitioning LNG infrastructure to hydrogen offers a viable medium-term solution for long-distance freight. Consequently, while batteries will drive mainstream growth, the diversity of propulsion methods is set to expand rather than contract.

By Vehicle Type: LCV Electrification Outpaces Passengers

Passenger Cars owned 83.25% of the 2025 volume, yet Light Commercial Vehicles logged a 35.02% CAGR, positioning them as swing contributors to the Australian electric vehicle market share through 2031. Supermarket chains deploy LDV eDeliver 9 vans on 150-km metro routes, proving compelling total-cost-of-ownership advantages. Depot charging aligns with solar PV generation, flattening demand peaks and supporting grid stability. Corporate fleet refresh cycles of three to five years will fuel a secondary-market wave from 2027, expanding affordability for sole traders and SMEs.

In contrast, medium-duty truck electrification remains in its early stages. Battery weight trims payloads by up to 1.5 tons, limiting adoption to volume-constrained parcels and beverage runs. Volvo’s FM Electric pilots indicate that cost break-even is achieved only when daily distances remain under 250 km. Nonetheless, federal grants for zero-emission freight corridors could accelerate the adoption of medium-duty vehicles late in the decade. Passenger segments, meanwhile, wrestle with the absence of electric utes, delaying rural adoption until credible tow-capable models appear.

By Range: 400-600 km Segment Erodes Anxiety

The 400-600 km bracket surged at a 34.12% CAGR, eroding the dominance of 200-400 km models, which still accounted for 47.13% of 2025 sales. Improved charging density now permits 300-km cars to traverse Sydney–Melbourne with two stops, though surveys show buyers still demand a psychological buffer of 400 km. Battery costs have declined since 2022, making longer-range variants financially viable, which supports an upshift in the mix and boosts the Australian electric vehicle market size for mid-range trims. Premium models exceeding 600 km remain niche status symbols due to steep price premiums.

Additional inter-city chargers are likely to moderate future range escalation, steering consumers back toward 300-350 km cars that strike a balance between cost and weight. Automakers are trialing subscription-based battery upgrades, allowing owners to unlock extra range for holiday road trips. Such flexibility could realign expectations and reduce over-specification of battery capacity, improving per-kilowatt utilization across the fleet.

By Battery Chemistry: LFP Gains Mirror Chinese Ascent

Nickel-Cobalt chemistries held a 58.23% share in 2025 but face steady erosion as Lithium Iron Phosphate (LFP) cells expand at 37.55% CAGR, spearheaded by Chinese OEM imports. LFP’s superior thermal stability reduces insurance premiums and simplifies pack architecture, enabling cell-to-body designs that help reclaim some of the energy-density deficit. Tesla’s switch to LFP for Model 3 RWD trims shaved a significant share off the bill of materials, driving price competition across the Australian electric vehicle market. Premium marques will retain Nickel Cobalt Manganese (NCM)/Nickel Cobalt Aluminum (NCA) for 500-km-plus variants, where range trumps cost.

Reduced cobalt dependence shields buyers from supply risks linked to geopolitical tensions in Central Africa, reinforcing the sustainability narrative that underpins government fleet mandates. Recycling players are scaling LFP-dedicated processes, signaling confidence in chemistry-specific circular-economy economics. As costs fall, LFP penetration is expected to capture parity share with nickel-based chemistries by 2028.

By Price Band: Barbell Structure Emerges

The USD 30,000-50,000 tier, which owned 56.11% of the 2025 volume, is now under siege from sub-USD 30,000 entrants expanding at a 38.24% CAGR. Fringe-benefit-tax exemptions on vehicles below the luxury-car threshold sharpen corporate appetite for Tesla Model 3 and Hyundai Ioniq 5 leases, sustaining mid-band strength. Value-seeking private buyers, however, gravitate toward MG4 and BYD Dolphin offers, compressing the ownership-cost gap with ICE substitutes. Above USD 50,000 demand remains resilient among performance and luxury enthusiasts, insulated from price sensitivity.

Expect a barbell outcome: aggressive volume growth at the bottom end and healthy margins at the top, while the middle becomes contested terrain in the Australian electric vehicle industry. Legacy automakers must decide whether to match Chinese brands on price or differentiate through design and after-sales service to defend segment share.

By Ownership Model: Fleets Seed Secondary Market

Private buyers accounted for 74.25% in 2025; however, corporate fleets are projected to grow at a 34.75% CAGR by 2031, as Woolworths, Qantas, and Telstra electrify their logistics and service vehicles. Tax exemptions and guaranteed utilization often mean fleets secure factory allocations ahead of retail orders, thereby smoothing supply volatility in the Australian electric vehicle market. Government agencies aim to achieve 75% low-emission procurement by 2025, thereby anchoring baseline demand even during consumer downturns.

Fleet vehicles will enter the used market after typical three-year lease cycles, alleviating today’s residual-value uncertainty that suppresses private-buyer confidence. This pipeline could reduce the resale-value gap between EVs and ICE counterparts by 2028, accelerating mainstream acceptance. Subscription models, such as Karmo’s partnership with AUSEV, further democratize EV access by enabling month-to-month use without long-term financial commitments.

Geography Analysis

New South Wales is poised to overtake Queensland as the most significant contributor to the Australian electric vehicle market by 2028, with a 36.14% CAGR by 2031, driven by a substantial incentive package and an enduring rebate. Queensland’s subsidy drove an early 30.05% share in 2025, yet its slower charging corridor rollout tempers long-term momentum. Victoria recovered from its abandoned road-user charge and now targets notable zero-emission sales by 2031, aided by reliable port access that shortens delivery times.

The Australian Capital Territory maintains national leadership on a per capita basis, thanks to zero stamp duty and free registration, as well as its dense urban geography that neutralizes range anxiety. Western Australia and South Australia remain mid-single-digit contributors; vast distances and a later start to corridor development constrain uptake, though new tourism-route chargers are closing the gap. Tasmania and the Northern Territory lag behind due to a scarcity of dealerships and concerns about extreme climate-driven battery degradation, but targeted grants for off-grid solar-plus-storage are beginning to shift momentum.

Fragmented state policies complicate OEM allocation decisions, prompting some buyers to purchase in Sydney or Melbourne and register vehicles interstate. Harmonizing incentives could unlock two to three percentage points of incremental CAGR for the Australian electric vehicle market by reducing administrative friction and balancing inventory flows.

Competitive Landscape

Chinese challengers are chipping away at Tesla's once-dominant position. In recent times, Tesla's market share has declined, while competitors like BYD have gained traction, and MG has emerged as a significant player. As Chinese imports achieve price-feature parity, they squeeze profit margins, prompting established automakers to accelerate their local launches or risk a decline in market share. The electric ute segment presents an opportunity; with BYD's Shark 6 PHEV being the sole affordable option, a substantial market remains ripe for disruption.

Tesla leverages vertical integration and its Supercharger network, yet Chargefox and Evie's expansion is eroding that advantage. BYD supplies battery packs to Toyota’s forthcoming bZ4X variant, signaling an increasing level of coopetition that blurs traditional rivalries. Polestar positions between mass-market Chinese brands and German luxury, while Rivian’s 2024 trademark filings hint at a premium ute launch targeting adventure-lifestyle buyers. The combined share of the top three fell 10 percentage points year over year, underscoring a shift toward multipolar competition in the Australian electric vehicle market.

Legacy incumbents counter by bundling PHEV variants, refreshing ICE mainstays, and lobbying for transitional incentives, but global right-hand-drive allocation constraints limit near-term impact. Expect continued fragmentation as new brands exploit price gaps and as OEMs experiment with agency sales models to retain margin in an increasingly crowded channel.

Australia Electric Vehicle Industry Leaders

Tesla Inc.

SAIC Motor Corp., Ltd. (MG Motor Australia)

Toyota Motor Corporation

BYD Company Limited

Hyundai Motor Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: GWM unveiled the Ora 5 SUV in China at CNY 91,800 (~USD 13,040), signaling a future ultra-low-cost entrant for Australia.

- October 2025: Honda Australia confirmed the Super-ONE compact EV for a late-2026 launch, targeting urban commuters and squaring off against BYD Atto 1.

- June 2025: BYD announced the Atto 2 electric SUV featuring blade-battery cell-to-body construction, with Q4-2025 local deliveries aimed at undercutting the MG ZS EV.

- May 2025: Australian EV ute maker AUSEV partnered with subscription provider Karmo to broaden access via flexible month-to-month contracts.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Australian electric vehicle market as the annual sales value and in-use stock of battery-electric, plug-in hybrid, hybrid, and fuel-cell passenger cars together with light, medium, and heavy commercial vehicles that are factory-built and road-legal. Values are tracked in USD and units across propulsion, range, battery chemistry, price band, ownership model, and state-level splits.

Scope Exclusion: Two-wheelers, off-highway machinery, retrofit conversions, and all charging-hardware revenue lie outside this report's scope.

Segmentation Overview

- By Propulsion Type

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Hybrid Electric Vehicles (HEV)

- Fuel-Cell Electric Vehicles (FCEV)

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium-Duty Commercial Vehicles

- Heavy-Duty Commercial Vehicles

- By Range

- Less than 200 km

- 200-400 km

- 400-600 km

- More than 600 km

- By Battery Chemistry

- Nickel Cobalt Manganese (NCM)/ Nickel Cobalt Aluminum (NCA)

- Lithium Iron Phosphate (LFP)

- Lithium Manganese Oxide (LMO)

- Others

- By Price Band

- Less than USD 30 K

- USD 30 K-50 K

- Above USD 50 K

- By Ownership Model

- Private Individuals

- Corporate Fleets

- Government Fleets

- By State / Territory

- New South Wales

- Victoria

- Queensland

- Western Australia

- South Australia

- Australian Capital Territory

- Rest of Australia

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with OEM sales heads, fleet managers, charge-point operators, and energy regulators across New South Wales, Victoria, and Queensland. These exchanges clarified transaction prices, supply wait-times, and likely compliance responses to the New Vehicle Efficiency Standard, sharpening key model assumptions.

Desk Research

We began by mapping historical registrations from open datasets such as the Federal Chamber of Automotive Industries' VFACTS, the Australian Bureau of Statistics motor-vehicle census, and the Department of Infrastructure's Green Vehicle Guide. We then linked them to policy levers drawn from Commonwealth and state gazettes. Charger density and grid headroom were traced through Australian Energy Regulator filings, ARENA dashboards, and Electric Vehicle Council scorecards. Company filings, investor decks, and D&B Hoovers supplied pricing and margin clues, while IEA Global EV Outlook, UN Comtrade, and Volza shipment codes anchored global context. The sources named are illustrative; many further materials supported data gathering and verification.

Market-Sizing & Forecasting

A blended top-down and bottom-up approach was applied. National registration totals were projected through a penetration-rate pool linked to battery cost curves, fast-charger rollout, fleet electrification targets, and NVES penalty trajectories. These were then reconciled with sampled dealer ASP × volume roll-ups. Core variables included quarterly BEV share of new sales, average battery-pack price per kWh, connectors per 100 km of highway, corporate fleet electrification pledges, and state rebate envelopes. Forecasts to 2030 rely on multivariate regression with ARIMA overlays, and supplier roll-ups bridge residual data gaps.

Data Validation & Update Cycle

Outputs pass anomaly checks against import statistics and electricity-demand patterns before senior review. We refresh the model annually and trigger interim updates when policy or supply shocks materially shift any driver. Every delivery is preceded by a fresh validation pass.

Why Mordor's Australia Electric Vehicle Baseline Commands Reliability

Published estimates often diverge because researchers mix vehicle classes, bundle ancillary revenue, or apply different currency years. By limiting scope to road-registered cars and commercial vehicles, valuing everything in constant 2024 dollars, and revisiting inputs each year, Mordor delivers a steadier compass for decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.96 B (2025) | Mordor Intelligence | - |

| USD 8.57 B (2024) | Regional Consultancy A | Includes micro-mobility and aftermarket parts; no inflation adjustment |

| USD 16.20 B (2024) | Global Consultancy B | Combines Australia & NZ and folds charger revenue |

The comparison shows that once geography, vehicle basket, and ancillary revenue are harmonized, Mordor's disciplined, variable-based approach yields a transparent baseline clients can replicate and stress-test with confidence.

Key Questions Answered in the Report

How big is the Australia electric vehicle market today and how fast is it growing?

The market generated USD 4.96 billion in 2026 and is projected to reach USD 20.83 billion by 2031, reflecting a 33.24% CAGR during 2026-2031.

Which price band is growing fastest?

Sub-USD 30,000 models, led by BYD Dolphin and MG4, are expanding at a 38.24% CAGR as Chinese brands flood the entry segment with feature-rich cars.

Why are EV wait-lists still long in Australia?

Limited right-hand-drive production slots favor larger United Kingdom and Japanese markets, creating domestic shortages for high-demand models such as Tesla Model Y and Hyundai Ioniq 5.

What is holding back rural EV adoption?

The absence of affordable electric utes with 400 km towing range, plus sparse fast-charging infrastructure, limits uptake among rural buyers.

Page last updated on: