Astronaut Space Suits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

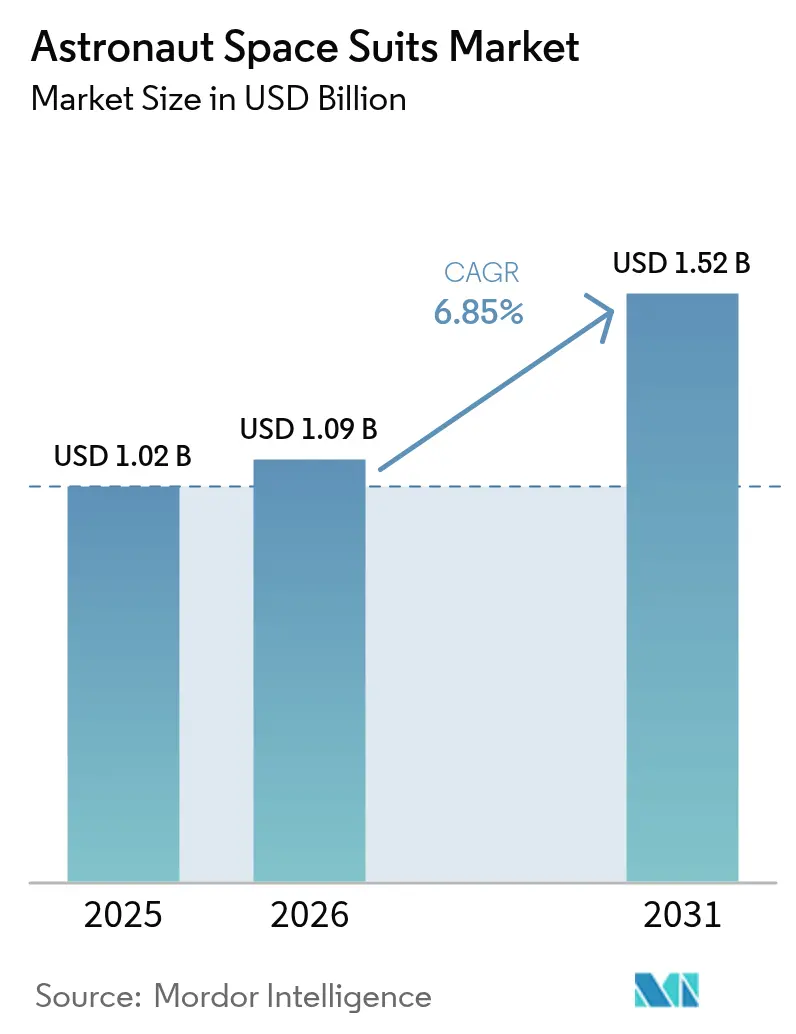

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Astronaut Space Suits Market Analysis by Mordor Intelligence

Astronaut space suits market size in 2026 is estimated at USD 1.09 billion, growing from 2025 value of USD 1.02 billion with 2031 projections showing USD 1.52 billion, growing at 6.85% CAGR over 2026-2031. This expansion reflects widening demand beyond the historical government-only customer base as commercial space tourism, private lunar programs, and national exploration initiatives adopt next-generation life-support systems. The transition toward privately funded spacewalks—underscored by SpaceX’s first commercial EVA during the Polaris Dawn mission in September 2024—confirms that agile commercial developers now match performance standards once defined by NASA. North America preserves its lead through Artemis procurement, yet Asia-Pacific delivers the quickest growth as China, India, and the UAE elevate human-spaceflight budgets. Supply-chain resilience has emerged as a structural driver, prompting consolidation such as Ingersoll Rand’s USD 2.325 billion purchase of ILC Dover to secure pressure-garment capacity.

Key Report Takeaways

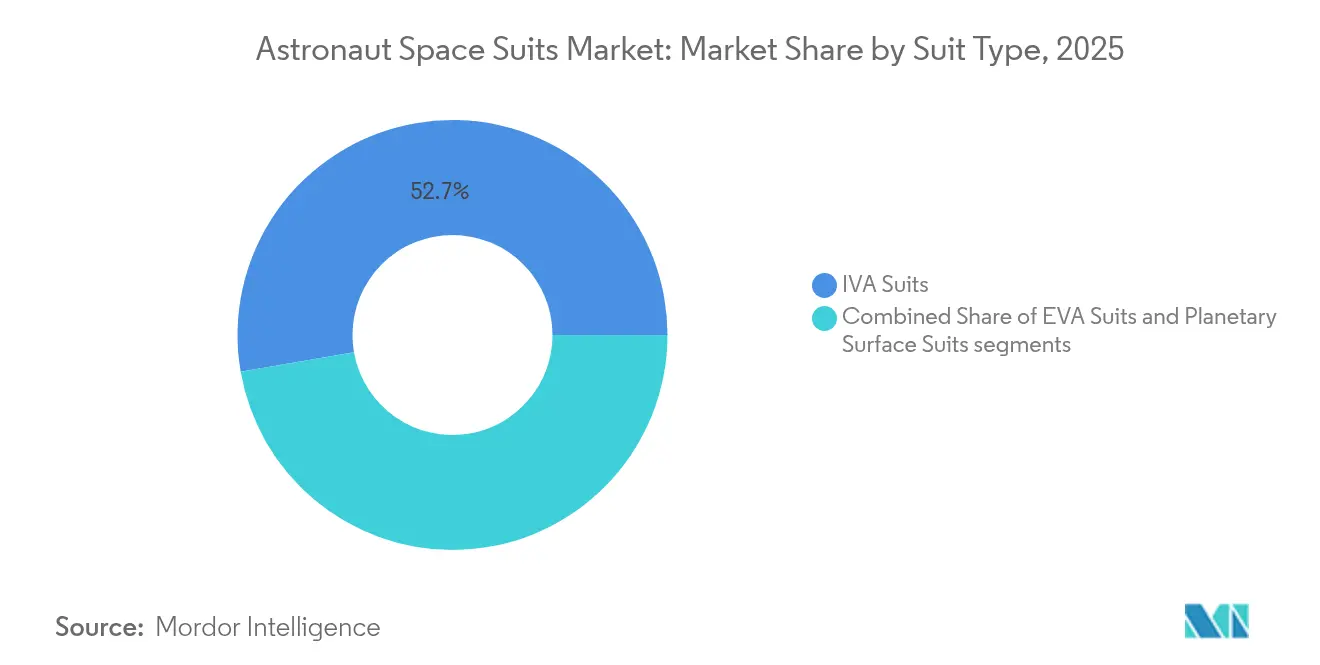

- By suit type, IVA suits held 52.74% of the astronaut space suits market share in 2025, while planetary surface suits are forecasted to grow at an 8.63% CAGR through 2031.

- By end user, government space agencies accounted for 61.62% of the astronaut space suits market size in 2025, whereas commercial operators are poised for an 7.98% CAGR to 2031.

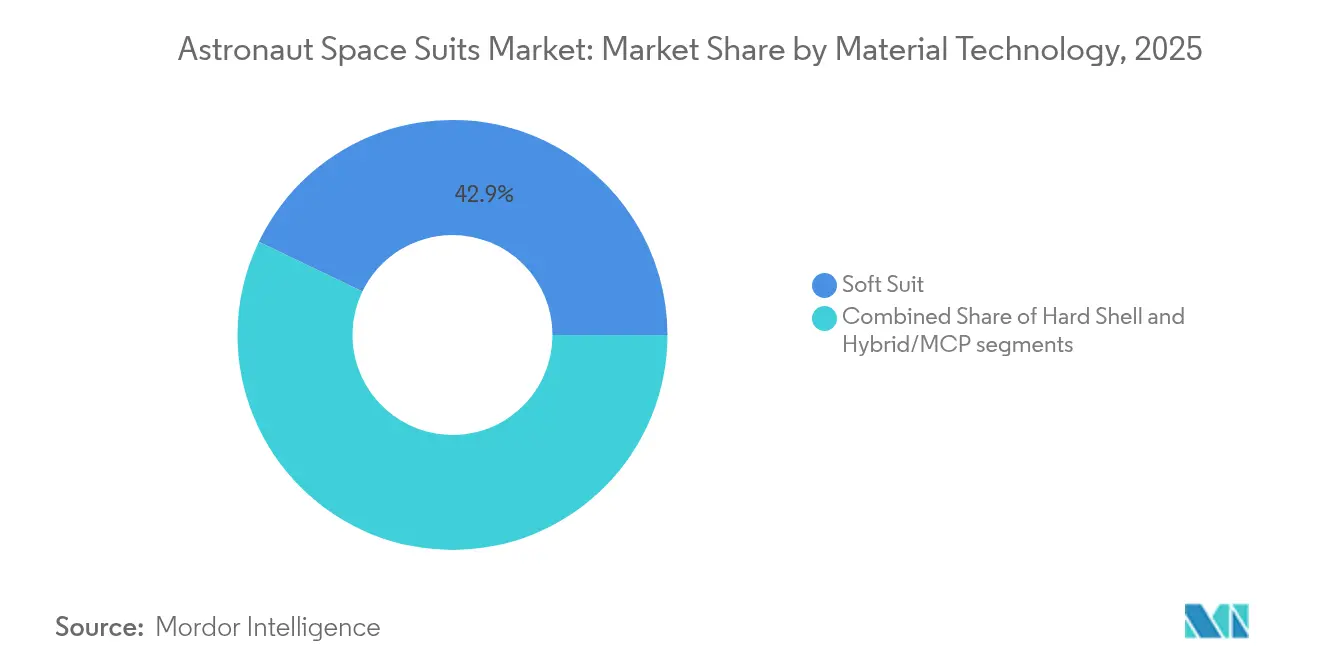

- By material technology, soft suit designs led with 42.85% share of the astronaut space suits market in 2025; hybrid/MCP technology is expected to expand at a 9.8% CAGR.

- By life-support architecture, distributed-system PLSS dominated with 38.74% share in 2025, and suitport-integrated systems are projected to record a 8.96% CAGR.

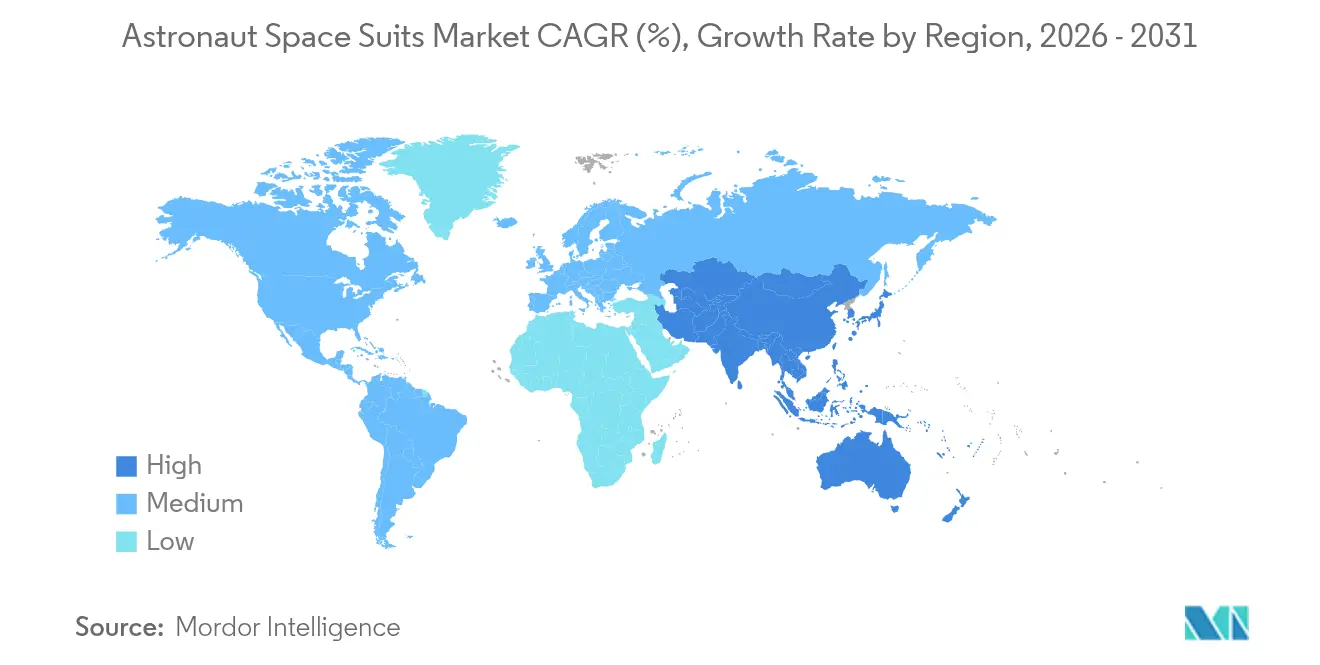

- By geography, North America commanded a 39.85% share in 2025, while Asia-Pacific is set to register the fastest 8.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Astronaut Space Suits Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Artemis and Artemis II lunar missions boost EVA suit demand | +1.8% | North America, international partners | Medium term (2-4 years) |

| Commercial space-tourism flight frequency surges | +1.2% | Global, led by North America and APAC | Short term (≤ 2 years) |

| Extended ISS and Gateway operations create refurbishment backlog | +0.9% | North America and Europe | Medium term (2-4 years) |

| Rising national budgets for new space powers | +1.5% | APAC core, Middle East expansion | Long term (≥ 4 years) |

| Closed-loop water-recycling suit tech for greater than 8-hr EVAs | +0.7% | Global | Medium term (2-4 years) |

| Modular exoskeleton add-ons lower astronaut fatigue | +0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Artemis and Artemis II Lunar Missions Boost EVA Suit Demand

NASA’s Artemis schedule has moved planetary-surface suit development to the top of R&D agendas. Axiom Space’s AxEMU prototype passed thermal-vacuum trials at Johnson Space Center, validating performance in -370°F environments that dominate the lunar south pole.[1]Source: NASA, “AxEMU Testing Updates,” nasa.gov Delays that may push Artemis III to 2027 have not slowed technical advances in dust-mitigation layers and miniaturized power-and-cooling subsystems. Prada’s contribution of high-tensile yarns plus ergonomic patterning illustrates cross-sector design infusion that blends luxury with mission safety. Eight-hour EVA capability, wider joint articulation, and lighter portable life-support systems set new performance floors that influence every tier of the astronaut space suits market.

Commercial Space-Tourism Flight Frequency Surges

Virgin Galactic’s 12th suborbital flight in June 2024 proved repeatable operations and previewed Delta-class vehicles arriving in 2026.[2]Virgin Galactic, “Flight Log 2024,” virgingalactic.com Blue Origin’s April 2025 New Shepard flight—featuring an all-female manifest—underscored the shift toward personalized IVA garments that trade some durability for passenger comfort. The sector anticipates more than 500 private astronauts by 2030, pushing manufacturers toward higher-volume, modular production lines. SpaceX’s EVA work on Polaris bridges tourism and professional mission standards, narrowing the capability gap and enlarging the market's addressable portion of the astronaut space suits.

Extended ISS and Gateway Operations Create Refurbishment Backlog

Only 18 functional Extravehicular Mobility Units remain, each past original design life, and water-leak incidents cancelled multiple 2024 spacewalks.[3]Ryan Whitwam, “ISS Water Leak Cancels Spacewalk,” gizmodo.com Collins Aerospace withdrew from its USD 97 million xEVAS contract, concentrating NASA risk on Axiom Space. Gateway’s dual-environment requirement—microgravity EVAs and lunar-surface sorties—fuels demand for convertible architectures. NASA’s Next-Generation Life-Support program emphasizes regenerative CO₂ and humidity control systems, pushing the astronaut space suits market toward componentized, in-orbit maintenance models.

Rising National Budgets for New Space Powers Drive Demand

China unveiled the Wangyu lunar suit in September 2024, matching its 2030 crewed landing target and bypassing Western supply chains. India’s Gaganyaan mission invests in indigenous IVA designs while evaluating Russian backups. The UAE and Saudi Arabia channel sovereign funds into human-flight hardware, preferring local co-production that bolsters technology transfer. These parallel programs expand the astronaut space suits industry footprint yet fragment sourcing standards, spurring joint-venture and licensing opportunities for established suppliers.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-high R&D and qualification cost per design iteration | −1.3% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Fragile supply chain for aerospace-grade fabrics and electromech | −0.8% | Global, concentrated in North America | Short term (≤ 2 years) |

| Glove dexterity limits complex on-orbit tasks | −0.6% | Global, critical for ISS and lunar operations | Medium term (2-4 years) |

| Liability ambiguity for privately owned EVA suits | −0.4% | North America and Europe, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ultra-High R&D Plus Qualification Cost Per Design Iteration

Collins Aerospace’s exit from xEVAS highlights how re-certification of each life-critical modification multiplies expenditure and risk beyond commercial ROI thresholds. Dual compliance with NASA human-rating and FAA commercial-spaceflight rules lengthens development cycles, favoring firms with legacy certification infrastructures. Capital intensity, not intellectual property, has become the principal barrier to new entrants in the astronaut space suits market.

Fragile Supply Chain for Aerospace-Grade Fabrics and Electromechanical Components

Titanium sourcing disruptions tied to Russia-Ukraine sanctions stretch lead times and raise costs for joint-bearing rings. Aerospace microchips remain on 52-week procurement windows, delaying the suit avionics assemblies. Ingersoll Rand’s takeover of ILC Dover cuts one independent pressure-garment supplier from the roster, heightening single-point-of-failure exposure.[4]McKinsey & Company, “Semiconductor supply chain recovery,” mckinsey.com Smaller firms rely on digital traceability tools to gain Tier-1 acceptance, but high up-front integration costs blunt their scaling potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Suit Type: Planetary Surface Suits Drive Innovation

IVA suits captured 52.74% of the astronaut space suits market share in 2025, buoyed by their near-universal role aboard Crew Dragon, Starliner, and Soyuz vehicles. Enhanced Starliner IVA garments delivered improved torso flexibility during a 2024 ISS tour, reinforcing the segment’s incumbency. The astronaut space suits market size for Planetary Surface Suits is projected to grow at an 8.63% CAGR as Artemis, the Wangyu program, and commercial lunar tourism schedules converge. Axiom Space’s AxEMU dust-mitigation skirts and China’s parallel MPC-hybrid prototypes exemplify mobility-first design, embedding haptic guidance and 4G voice telemetry. Across the forecast, EVA replacement cycles accelerate as aging EMUs approach end-of-life and fail to meet current safety guidelines.

Planetary surface suits represent the technology frontier. Mechanical counter-pressure panels cut bulk without sacrificing cabin pressure, while graphene-infused fabrics deflect thermal spikes from sun-shadow transitions. Modular thigh ports accept sensor pods for geology tools, expanding scientific throughput per sortie. Apollo-era ankle restrictions limited traverse distance; new lower-torso bearings enlarge step stride by 32%, raising productivity metrics attractive to lunar-mining investors. Consequently, innovation in this sub-segment sheds R&D spillovers into IVA refresh programs, reinforcing the broader astronaut space suits market.

By End User: Commercial Operators Accelerate Growth

Government agencies maintained 61.62% of the astronaut space suits market share in 2025, thanks to NASA’s multi-year commitments and China’s state-funded programs. Artemis procurement alone covers surface-suit deliveries through 2032, anchoring volumes for primary contractors. Yet, the astronaut space suits market size is attributable to commercial operators, and it is forecasted to expand at an 7.98% CAGR as Virgin Galactic, Blue Origin, and SpaceX scale flight cadence. Following the Polaris Dawn EVA, private EVA capability now rivals ISS operations in complexity, shrinking the performance gap.

Commercial growth alters production economics. Standardized sizing, simplified closure systems, and quick-swap glove modules cut per-unit costs by up to 25%. Merchandising rights around celebrity passenger flights create secondary revenue streams for manufacturers offering co-branded garments. Regulatory clarity under the US Commercial Space Launch Competitiveness Act allows operators to self-certify IVA equipment if passenger risk disclosures meet FAA thresholds, speeding time-to-market for new designs.

By Material Technology: Hybrid Solutions Gain Momentum

Soft suit configurations led with a 42.85% share in 2025, valued for dependable layered-fabric approaches refined over decades of Shuttle and ISS service. Still, the astronaut space suits market predicts Hybrid/MCP concepts to rise at a 9.8% CAGR. MIT’s BioSuit lent credibility to mechanical-counter pressure theory, and subsequent shape-memory alloy musculature lifted mobility without adding pump mass. The astronaut space suits industry expects volume commitments to follow once hybrid prototypes clear micro-gravity wear tests.

Hybrid adoption heightens cross-sector material innovation. Thin-film shielding combines titanium and tantalum, delivering 25 times more radiation blockage and trimming weight by 25% compared with lead-lined layers techbriefs.com. The University of Delaware demonstrated self-healing polymers that reseal pin-prick micrometeoroid breaks in under 60 seconds. Such advances dovetail with closed-loop life support as lighter suits accommodate larger battery packs, extending EVA windows beyond 8 hours.

By Life-Support Architecture: Suit port Integration Emerges

Distributed-system PLSS designs held a 38.74% share in 2025 because modular oxygen, fan, and scrubber placement support multi-mission flexibility. Nonetheless, Suitport-Integrated Systems are expected to log a 8.96% CAGR as surface habitats and pressurized rovers adopt plug-and-play ingress. The astronaut space suits market benefits from Cornell University’s 87%-efficient urine recycling cartridge, shrinking water carry-mass and enabling week-long sorties. Suitport docking preserves cabin cleanliness and slashes pre-breathing time, which is critical for quick-response repairs on Gateway’s exterior.

Backpack PLSS remains relevant where mission rules require full independence, such as contingency EVAs or tourist acrobatics inside a free-flying capsule. For these, adaptive exoskeleton actuators tuned by admittance control have reduced metabolic oxygen draw by 15.88% during NASA Neutral-Buoyancy Lab trials, hinting at convergence between power-assist robotics and pressure-garment design.

Geography Analysis

North America generated 39.85% of 2025 revenue, anchored by NASA’s sustained Artemis funding and SpaceX’s vertically integrated manufacturing. The region’s astronaut space suits market benefits from established pressure-garment supply lines in Delaware, Texas, and Florida. US export-control frameworks favor domestic sourcing, though Canada’s contribution of life-support avionics to Gateway keeps cooperation intact. A renewed congressional budget top-up in 2025 extends EVA refurbishment spending to 2032, providing volume predictability for prime contractors.

Asia-Pacific posts the fastest 8.55% CAGR, powered by China’s dual ISS-class station and lunar ambitions. The Wangyu program’s emphasis on sovereign components—from bearing seals to PLSS processors—creates parallel ecosystems that bypass Western ITAR constraints. India’s Gaganyaan module partners with private firms in Bengaluru to mature IVA ventilation packs by 2026, aiming for regional export potential. South Korea and Japan leverage extant spacesuit testbeds at JAXA’s Tsukuba complex, collaborating on radiation-shielded textiles suitable for cislunar orbits.

Europe remains steady, mobilizing ESA’s Pextex initiative to engineer basalt-fiber fabrics that repel lunar dust. The astronaut space suits market size attributable to ESA could rise once the Gateway assembly ramps, as Airbus and Thales Alenia Space provide suitport docking hardware. National space agencies in France and Germany co-finance Spartan Space’s IVA prototype, enhancing the continent’s autonomy. Eastern European suppliers in Poland and the Czech Republic incubate micro-pump technologies, securing a foothold in the value chain as bigger primes consolidate.

The Middle East pivots from satellite focus to human spaceflight. The UAE’s Mohammed bin Rashid Space Centre pilots extravehicular training with refurbished Russian Orlan units before ordering indigenous designs trained on desert dust trials replicating lunar regolith. Saudi Arabia earmarked funding to co-locate a pressure-garment plant inside the NEOM industrial zone, courting Western partners with tax incentives. These moves diversify the astronaut space suits market and hedge against single-region shocks.

Regulatory Landscape

The market operates under a layered framework of government human-rating requirements and emerging commercial-space standards. NASA anchors technical requirements for crew health and performance via NASA-STD-3001 Volume 2 (Spacesuits). A February 2025 update to Section 11.0 specifies IVA and EVA suit performance, safety, and health requirements, while the May 2024 Exploration EVA (xEVA) System Compatibility Standards (EHP-10028) codify interface requirements between suits and Artemis hardware.

Commercial human spaceflight oversight in the United States is shaped by the FAA Office of Commercial Space Transportation under 14 CFR Part 460, which emphasizes occupant safety, risk disclosure, and informed consent for launch and reentry. Alongside agency standards, ASTM Committee F47 work, including WK85994 under F47.05, is developing test methods relevant to lunar regolith hazards, such as textile abrasion and impact resistance. The US Department of Commerce compendium of commercial space industry standards (June 2024) also points to a broader push toward harmonized, multi-stakeholder standards as commercial EVA activity expands.

Value Chain Analysis

The value chain runs from aerospace-grade textiles, bearings and seals, microelectronics, valves, batteries, and oxygen and CO2 scrubbing hardware to pressure-garment fabrication, life-support integration (PLSS and avionics), and verification and validation using thermal-vacuum, neutral buoyancy, and dust or regolith simulants. Mission operations support then feeds into refurbishment and recertification, with NASA acting as a primary orchestrator through requirements and acceptance testing, even as the xEVAS structure shifts key responsibilities to contractors for design authority, qualification, and sustainment services.

Upstream fragility and downstream qualification cycles are the main bottlenecks, especially given low-volume production and long lead times for space-rated electronics and joint hardware. The April 2026 NASA OIG audit (IG-26-006) reinforces concentration risk after Collins Aerospace was descoped from xEVAS task orders (June 2024), leaving Axiom Space as the sole remaining active developer for both lunar and microgravity suits under the current program. To address dependency exposure, Axiom has leaned on vertical integration for selected subsystems and non-traditional supplier partnerships, including Prada for soft goods and Oakley for visor systems, to broaden the industrial base across suit subassemblies.

Competitive Landscape

The astronaut space suits market shows moderate concentration. Legacy suppliers such as ILC Dover, David Clark Company, and Oceaneering remain essential due to flight-qualified manufacturing lines, yet they face agile competitors. ILC Dover’s June 2024 acquisition by Ingersoll Rand consolidates elastomer molding and tension-restraint weaving under one corporate umbrella, potentially tightening supply pricing. Axiom Space differentiates through Prada-backed textiles that merge fashion-grade aesthetics with functional thermal padding, elevating brand appeal among tourism operators. SpaceX’s proprietary EVA suit program eliminates third-party margins while showcasing vertically integrated life-support R&D, pressuring incumbents on cost and schedule.

Strategic behavior bifurcates along customer lines. Government-focused incumbents emphasize exhaustive qualification and component redundancy, producing small annual batches yet locking multi-year contracts. Commercial players court faster design iteration and cost reduction, partnering with additive-manufacturing shops to 3-D print titanium ducting in days rather than months. USPTO tracked patent filings show a 16% uptick in mechanical counter-pressure and wearable sensor intellectual property with partial federal sponsorship during 2024.

Mergers and acquisitions activity expands capability breadth. Paragon Space Development Corporation evaluates merging with a European PLSS valve specialist to localize production for ESA missions. Sure Safety fosters licensing deals for emerging Asian programs, offering low-cost IVA ensembles that comply with ISRO standards. Meanwhile, Metakosmos pioneers AI-driven fitment scanning, enabling batch-manufacturing semi-custom suits that cut lead times by 40%. Competitive dynamics, therefore, involve both scale consolidation and niche specialization, reinforcing medium concentration levels.

Astronaut Space Suits Industry Leaders

RTX Corporation

ILC Dover, LP

Axiom Space, Inc.

Paragon Space Development Corporation

Space Exploration Technologies Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The most visible near-term whitespace is at the intersection of interoperability and services-based sustainment. The April 2026 NASA OIG report (IG-26-006) flagged the need for an interoperability standards plan between Artemis lunar vehicles and spacesuits, creating room for interface management, verification tooling, and standardized suit-to-vehicle hardware that can apply across multiple lunar assets. In parallel, NASA's xEVAS approach, where the agency rents services rather than owning suit hardware, supports recurring opportunities in refurbishment, recertification, spares provisioning, and configuration management as ISS EVAs continue and Gateway requirements broaden multi-environment use cases.

Commercial EVA activity and tourism-driven IVA demand also create a pathway for higher-volume, modular garments, though the market remains constrained by qualification cost and schedule volatility. The shift to a single active xEVAS developer after Collins Aerospace exited its task orders (June 2024) concentrates demand and also highlights supplier readiness gaps for critical subsystems and test capacity. That creates openings for sub-tier entrants in space-rated textiles and abrasion-resistant materials aligned with ASTM F47 efforts, as well as electronics and valve suppliers that can meet traceability and human-rating documentation requirements. Evidence of active productization and partner-led subsystem development continues with Axiom Space and Prada unveiling the AxEMU inner Liquid Cooling and Ventilation Garment (June 2026), which underscores ongoing investment in component-level upgrades that can cascade into both government EVA and commercial mission suit variants.

Recent Industry Developments

- June 2026: Axiom Space and Prada unveiled the Liquid Cooling and Ventilation Garment (LCVG), the inner layer for the AxEMU lunar spacesuit. The reveal formalized a key subsystem intended to support thermal management and crew comfort during long-duration EVAs, and it signals a supply-chain model that brings non-traditional soft-goods expertise into a flight-critical program.

- July 2025: Axiom Space reported the next-generation spacesuit was crew tested for the first time in NASA's Neutral Buoyancy Laboratory. The milestone advanced human-in-the-loop evaluation for fit, mobility, and operability, supporting downstream qualification and maintainability work for both lunar and microgravity configurations.

- June 2024: NASA and Collins Aerospace mutually agreed to descope Collins' task orders under the xEVAS contract, ending its role as a primary provider for ISS spacesuit development. The change reduced competitive redundancy inside the program and increased reliance on the remaining contractor base for next-generation EVA capability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of astronaut space suits and major suit-level subsystems used for crewed missions, including IVA and EVA configurations, and surface-capable variants when they are procured as part of a suit program.

Scope exclusions: It excludes general-purpose aerospace protective clothing, diver suits, and unrelated life-support equipment that is not designed and qualified as part of an astronaut suit system.

Segmentation Overview

- By Suit Type

- IVA Suits

- EVA Suits

- Planetary Surface Suits (xEMU / AxEMU)

- By End User

- Government Space Agencies

- Commercial Launch and Space-Tourism Operators

- Defense and Research Institutions

- By Material Technology

- Soft Suit

- Hard Shell

- Hybrid/Mechanical Counter-Pressure (MCP)

- By Life Support Architecture

- Backpack PLSS

- Distributed-system PLSS

- Suitport-Integrated Systems

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping suit demand to real mission activity and funded programs, because this market is small and contract-driven. We review public procurement releases and budget documents from space agencies, and then cross-check those signals with mission manifests and public program milestones.

For fact building, sources used include items such as NASA budget and procurement updates, ESA public documents, U.S. Government Accountability Office reports, UN Office for Outer Space Affairs references, and peer-reviewed aerospace and human-factors journals that discuss suit design constraints and testing outcomes. We also rely on company filings, investor presentations, press releases, and credible aerospace press to confirm contract timing and program scope. Where needed, paid subscriptions are used for company financials and news screening, and for patent lookups on suit materials, life-support, and mobility features. These desk research sources are not exhaustive, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs come from interviews and structured surveys with suit designers, subsystem suppliers, program managers, integrators, and downstream users involved in crewed missions. We cover perspectives across Americas, EMEA, and APAC, so procurement cadence, qualification timelines, and pricing logic can be compared across government and commercial programs. The respondent feedback is then used to tighten assumptions that were unclear from public data.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 19% | APAC: 42% |

| Mid tier: 49% | Functional/Unit leaders: 40% | EMEA: 35% |

| Smaller Players: 20% | Managers: 41% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where mission cadence, active crew programs, and public budget and contract signals are used to reconstruct yearly spend on IVA, EVA, and surface-capable suit programs. To keep the totals grounded, results are then corroborated through selective bottom-up checks, such as sampled contract values, suit program roll-ups, and simple volume by estimated average pricing for a limited set of procurements.

Key model inputs include announced crewed mission counts and schedules, the number of astronauts trained or assigned to missions, suit replacement and refurbishment cycles, qualification and test timelines that shift deliveries, and the mix of suit types required by mission profile (IVA versus EVA versus surface activity). We also track signals like funding allocations for exploration programs and the share of new development versus sustainment work, because these factors move pricing and timing in different ways.

Forecasts are produced using scenario analysis tied to program start dates and funding visibility, and then smoothed with simple time-series checks where historical spend patterns exist. When procurement values are not disclosed, gaps are handled by using comparable program benchmarks from similar contract structures and by validating ranges through interviews before finalizing the yearly run-rate.

Data Validation & Update Cycle

Checks are run at multiple steps so the final series stays consistent with real-world activity. We compare outputs against independent signals such as publicly announced contract awards, budget line items, and mission schedule changes, and then investigate any sharp jumps that do not match those external cues.

A second analyst review is completed to confirm that scope rules, currency handling, and timing of awards versus deliveries have been applied consistently. If large variances appear during review, follow-up outreach is triggered to re-test the key assumptions. Reports are refreshed annually, and interim updates are made when material events occur, such as major contract wins, program delays, or a change in mission cadence. Before delivery, a fresh pass is done so clients receive the most recently updated view.

Mordor Intelligence's Astronaut Space Suits Market Estimate Compared With Other Published Estimates

Published market numbers for astronaut space suits can look far apart because each study draws the line differently on what is counted, and because contract timing is treated differently across years. Differences also come from how IVA and EVA programs are blended, how refurbishment versus new-build spend is handled, and whether values are recognized at award date or delivery date.

The main gap comes from whether sustainment and refurbishment activity is counted as full suit value or only as program services, and from how mission-driven demand is converted into yearly spend, where Mordor Intelligence counts suit program value only when it maps to astronaut-qualified IVA or EVA systems tied to funded procurements and mission schedules.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.09 B (2026) | |

| Trade Journal A | USD 0.90 B (2023) | Uses an earlier base year and may recognize value closer to shipments and deliveries, and it can undercount development-stage programs that have awards but limited near-term deliveries. |

| Industry Publisher B | USD 0.87 B (2024) | Applies a longer forecast window with higher growth assumptions and may include adjacent protective gear and broader program spending, which can pull the starting market value down or shift it across years. |

Overall, the spread in estimates is mostly explained by timing and scope, especially how award value, development work, and refurbishment are treated across IVA and EVA programs. By tying the total to mission cadence and funded procurement signals, and then checking the result with contract-based approximations, we keep the model traceable to clear inputs that a reader can reproduce and stress-test.

Key Questions Answered in the Report

What is the current value of the astronaut space suits market?

The astronaut space suits market is valued at USD 1.09 billion in 2026.

How fast is the astronaut space suits market expected to grow?

It is forecasted to progress at a 6.85% CAGR, reaching USD 1.52 billion by 2031.

Which suit type is growing the fastest?

Planetary Surface Suits are projected to expand at an 8.63% CAGR because of sustained lunar-mission demand.

Why are commercial operators important to future demand?

Space tourism and private EVA programs show an 7.98% CAGR, shifting volumes toward higher-frequency, standardized production.

What regions will offer the highest growth opportunities?

Asia-Pacific leads growth with an 8.55% CAGR, driven by China’s lunar plans and India’s Gaganyaan program.

How is technology evolving within the astronaut space suits industry?

Mechanical counter-pressure hybrids, suitport integration, and closed-loop water recycling are key innovations targeting longer, safer EVAs.

Page last updated on: