Aspergillosis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

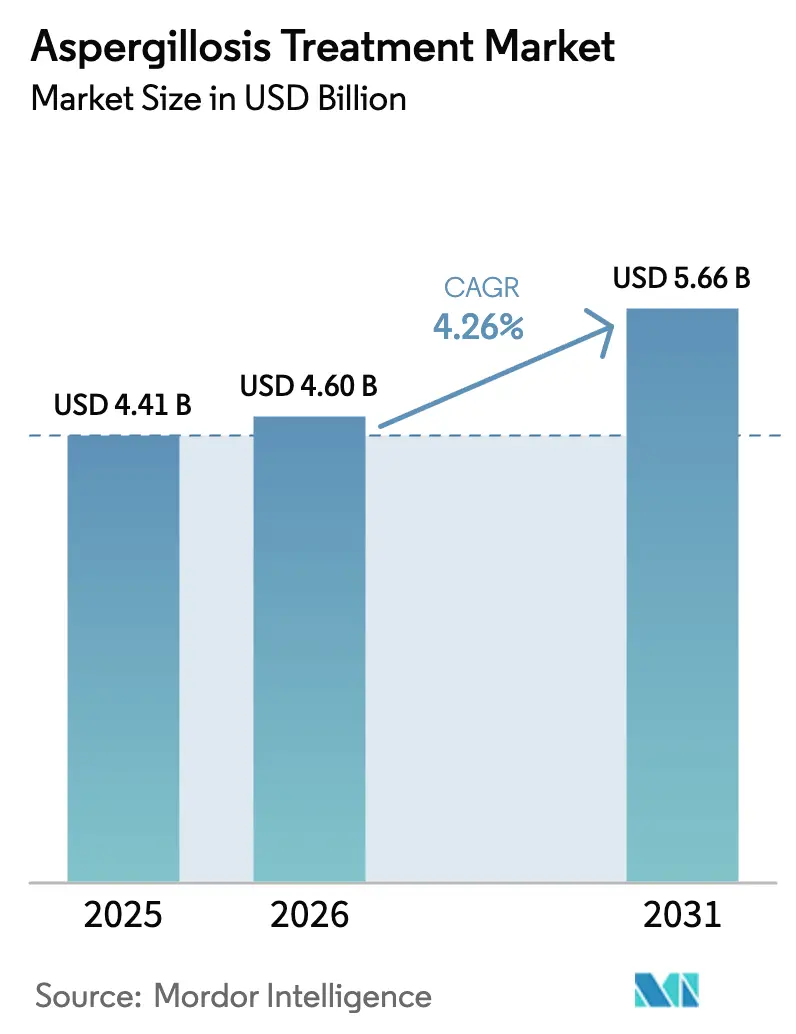

| Market Size (2026) | USD 4.6 Billion |

| Market Size (2031) | USD 5.66 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aspergillosis Treatment Market Analysis by Mordor Intelligence

Aspergillosis treatment market size in 2026 is estimated at USD 4.6 billion, growing from 2025 value of USD 4.41 billion with 2031 projections showing USD 5.66 billion, growing at 4.26% CAGR over 2026-2031. A steady rise in immunocompromised patient numbers, wider geographic circulation of Aspergillus spores as temperatures climb, and continuous regulatory support for next-generation antifungals collectively underpin market expansion. Nevertheless, escalating azole resistance, supply-chain fragility for active pharmaceutical ingredients (APIs), and high treatment costs temper the growth trajectory, compelling stakeholders to diversify drug classes and innovate delivery formats. Intensifying clinical trials around novel triazoles, weekly-dosed echinocandins, and orotomide agents illustrate how industry leaders are positioning to capture emerging opportunities within the aspergillosis treatment market, even as environmental and resistance pressures reshape product-mix priorities.

Key Report Takeaways

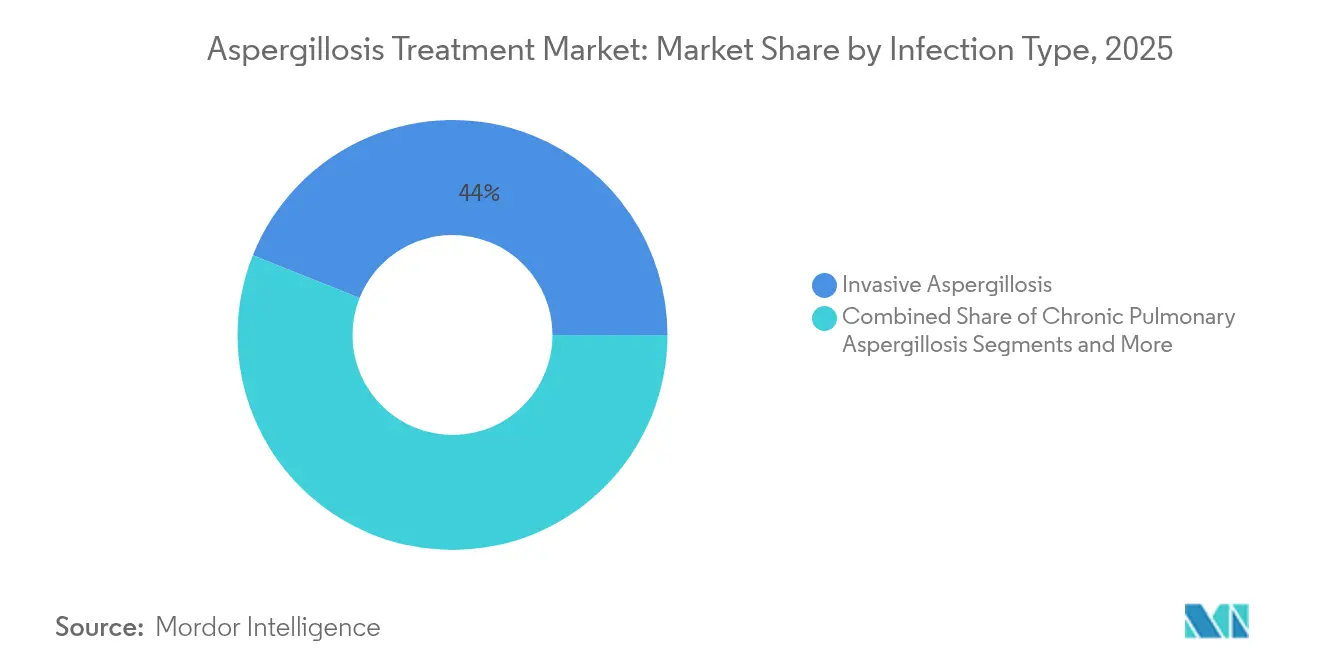

- By infection type, invasive aspergillosis led with 43.95% revenue share in 2025, while allergic aspergillosis is projected to expand at a 6.72% CAGR to 2031.

- By drug class, azoles accounted for 52.19% of aspergillosis treatment market share in 2025; echinocandins hold the fastest projected CAGR at 7.79% through 2031.

- By formulation, intravenous products represented 47.05% of the aspergillosis treatment market size in 2025; inhaled dry-powder formulations are forecast to grow at 7.21% CAGR.

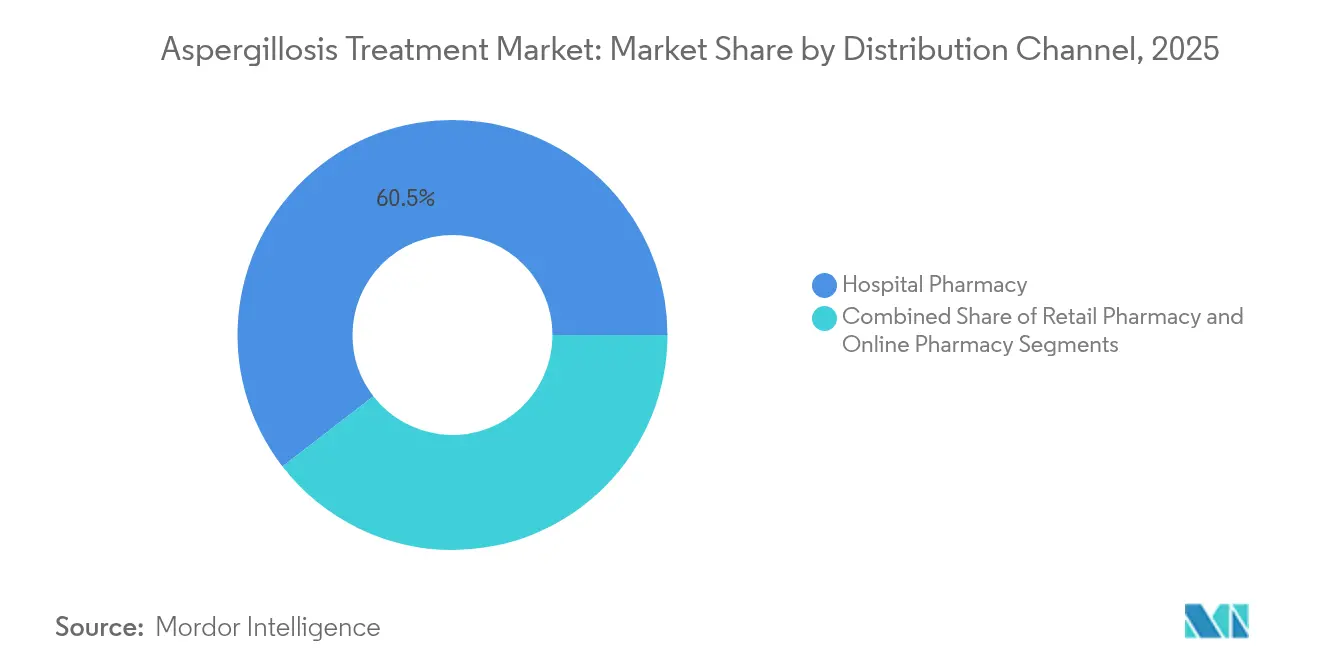

- By distribution channel, hospital pharmacies dominated with a 60.48% share in 2025, whereas online pharmacies are expected to rise at 8.15% CAGR.

- By patient category, hematopoietic stem-cell transplant recipients held 35.74% of 2025 sales; COPD and severe asthma patients show the highest CAGR at 7.24%.

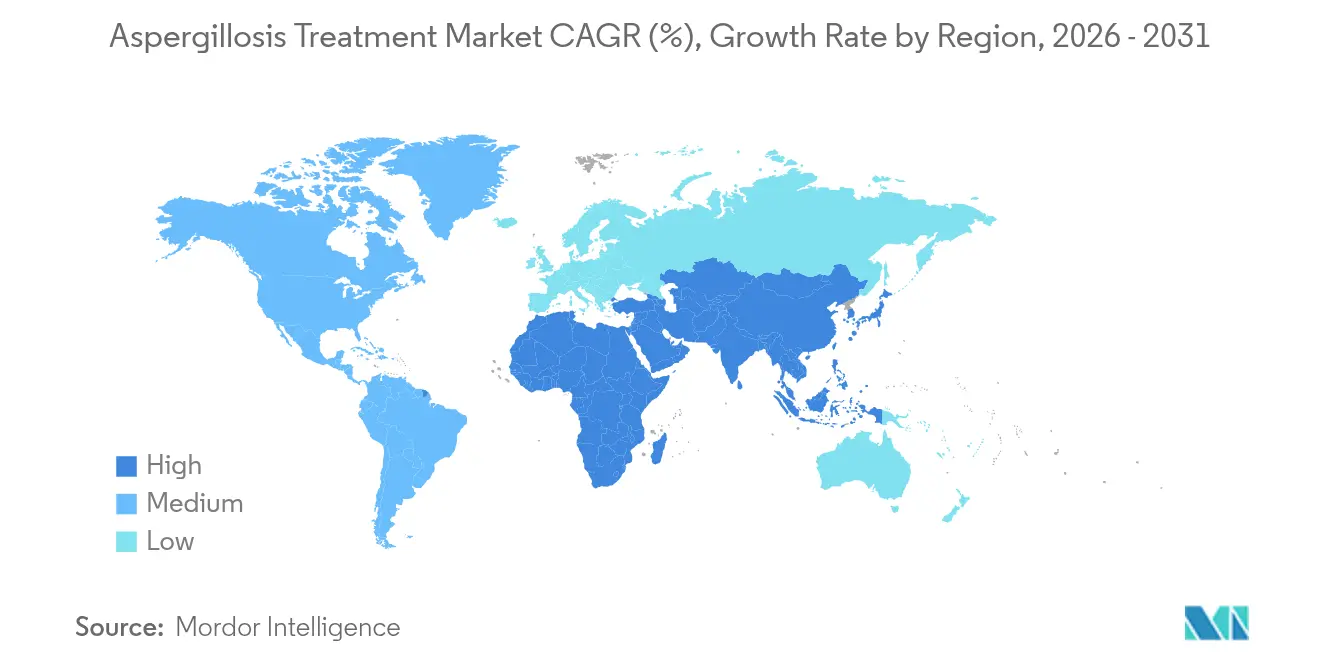

- By geography, North America commanded 33.12% of global revenue in 2025, while Asia Pacific is the fastest-growing region at 6.55% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aspergillosis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing incidence among immunocompromised patients | +1.2% | Global; highest in North America & Europe | Medium term (2-4 years) |

| Rising solid-organ & stem-cell transplant volumes | +0.8% | Global; fastest growth in Asia Pacific | Long term (≥ 4 years) |

| Advancements in rapid molecular diagnostics | +0.6% | North America & Europe, extending to APAC | Short term (≤ 2 years) |

| Accelerated approvals of next-gen triazoles & echinocandins | +0.7% | Regulatory-active regions worldwide | Medium term (2-4 years) |

| Climate-change-driven spore proliferation | +0.4% | Europe & North America, spreading globally | Long term (≥ 4 years) |

| Breakthrough inhaled & nano-formulation delivery platforms | +0.5% | Initially North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Incidence Among Immunocompromised Patients

An expanding pool of immunocompromised individuals—which now includes a larger cohort of hematopoietic stem-cell transplant recipients, intensive-care influenza cases, and COVID-19 survivors—continues to propel the aspergillosis treatment market. Invasive pulmonary aspergillosis appears in 15.3% of influenza ICU cases, versus 9.5% in severe community-acquired pneumonia.[1]Meng-Jer Hsieh, “Invasive Pulmonary Aspergillosis Among Patients with Severe Community-Acquired Pneumonia,” Pneumonia, biomedcentral.comMortality often exceeds 50% despite appropriate therapy. Excessive broad-spectrum antibiotic use disrupts microbial balance, contributing to 9.8% fungal infection incidence among ICU patients. Metagenomic sequencing now detects additional pathogens in 21% of samples, supporting earlier, targeted therapy. Collectively, these factors reinforce sustained demand within the aspergillosis treatment market.

Rising Solid-Organ & Stem-Cell Transplant Volumes

Global transplant expansion deepens the prophylactic and therapeutic need for mold-active agents. Updated ECIL guidelines recommend isavuconazole, micafungin, and caspofungin for acute myeloid leukemia cases undergoing chemotherapy, underscoring the centrality of mold protection.[2]Johan Maertens, “Primary Antifungal Prophylaxis in Hematological Malignancies,” Leukemia, nature.com Kidney transplant recipients, though facing lower incidence, still rely on voriconazole or isavuconazole. Post-tuberculosis chronic pulmonary aspergillosis prevalence, reaching 69.4% IgG positivity in Indonesia, widens the therapeutic base. Thus, transplant growth secures a long-run revenue anchor for the aspergillosis treatment market.

Advancements in Rapid Molecular Diagnostics

Next-generation PCR panels, whole-genome sequencing, and combined biomarker algorithms slash time-to-result from days to mere hours. The standardized Aspergillus PCR assay adopted by EORTC guidelines exemplifies the shift. Real-time melting-curve PCR reaches detection thresholds of 0.05 pg/µL in 4–6 hours. When galactomannan pairs with β-D-glucan, pooled sensitivity rises to 84% and specificity to 76%. As quick, precise diagnosis improves outcomes, it also increases overall prescription volumes, buoying the aspergillosis treatment market.

Accelerated Approvals of Next-Gen Triazoles & Echinocandins

Breakthrough- and orphan-designated products such as olorofim and rezafungin shorten review cycles and broaden therapeutic choices. Rezafungin won European approval in 2024 with weekly dosing convenience. Olorofim carries FDA breakthrough status and is in Phase 3 against standard-of-care regimens. In parallel, fosmanogepix secured USD 268 million BARDA funding, reflecting governmental commitment to antifungal innovation. Regulatory momentum sustains innovation pipelines that underpin future sales growth in the aspergillosis treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating azole resistance & limited novel classes | -1.1% | Europe & North America; growing globally | Short term (≤ 2 years) |

| High total cost of antifungal therapy | -0.7% | Universal; most acute in emerging markets | Medium term (2-4 years) |

| Agricultural azole use driving cross-resistance | -0.5% | Europe & North America | Long term (≥ 4 years) |

| API supply-chain fragility causing drug shortages | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Azole Resistance & Limited Novel Classes

Multi-azole-resistant Aspergillus fumigatus strains carry elevated mutation rates tied to msh6 G233A variants, accelerating cross-class resistance.[3]Michael J. Bottery, “Elevated Mutation Rates in Multi-azole Resistant Aspergillus fumigatus,” Nature Communications, nature.com Environmental fungicide pressure perpetuates pan-azole resistance without fitness loss. The WHO lists A. fumigatus as a critical priority fungus, urging surveillance upgrades. Limited drug-class diversification means resistant isolates threaten standard regimens, directly constraining revenue potential for the aspergillosis treatment market.

High Total Cost of Antifungal Therapy

Hospital stays for aspergillosis in cirrhotic patients exceed 22.9 days on average, quadrupling charges versus uninfected cases. Spain recorded EUR 1.4 million in 2012 inpatient costs, and expenses remain volatile. While newer azoles improve outcomes, their premium prices strain budgets in resource-limited settings, restraining wider adoption across the aspergillosis treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infection Type: Invasive Forms Drive Market Leadership

Invasive aspergillosis held 43.95% of 2025 revenue, anchored by high mortality—sometimes surpassing 85% in vulnerable cohorts—and the need for intensive, prolonged intervention. The aspergillosis treatment market size for invasive forms will keep growing as COVID-19-associated pulmonary aspergillosis, detected in up to 20% of severe cases, enlarges the critical-care segment. Chronic pulmonary aspergillosis is also edging upward, with Indonesian post-TB incidence reaching 14.5% by therapy end.

Allergic aspergillosis records a 6.72% CAGR through 2031, the fastest within infection types. US prevalence surveys show ABPA at 2.8 per 10,000 in asthma and 183.7 per 10,000 in cystic fibrosis. Revised 2024 ISHAM guidelines now recommend combined prednisolone–itraconazole for recurrent flares. Enhanced recognition and diagnostic access will sustain segment-level momentum within the aspergillosis treatment market.

By Drug Class: Azoles Maintain Leadership Despite Resistance Pressures

Azoles contributed 52.19% of 2025 sales, spearheaded by voriconazole and isavuconazole, which deliver 53% response rates compared with 32% for conventional amphotericin B. However, 27.84% of FDA-reported cardiac events link to triazoles, elevating safety scrutiny. Resistance growth is prompting hospitals to intensify stewardship, yet the aspergillosis treatment market still relies heavily on this class.

Echinocandins post the highest 7.79% CAGR. Weekly-dosed rezafungin matches caspofungin efficacy while improving adherence. Novel agents such as olorofim add further options, although commercialization timelines will shape uptake patterns.

By Formulation: Intravenous Delivery Dominates Critical Care

Intravenous formulations represented 47.05% of the aspergillosis treatment market size in 2025, reflecting immediate therapeutic need in ICU settings. Liposomal amphotericin B remains vital, though nephrotoxicity caps its use; global initiatives aim to lower formulation costs.

Inhaled dry-powder formats grow at 7.21% CAGR, leveraging improved lung retention and reduced systemic exposure. The FDA underscores their prophylactic utility for high-risk patients, making them a key innovation frontier within the aspergillosis treatment market.

By Distribution Channel: Hospital Pharmacies Anchor Critical Care Access

Hospital pharmacies managed 60.48% of global sales in 2025 thanks to stewardship expertise, therapeutic drug monitoring, and rapid access to alternate regimens when resistance emerges. Their dominance should persist given ICU demand and complex drug-interaction management inherent to azole therapy.

Online pharmacies accelerate at 8.15% CAGR, driven by chronic disease management and telemedicine integration. Extended oral treatment courses for chronic pulmonary aspergillosis translate into sizable remote dispensing volumes, especially in advanced economies.

By Patient Category: Transplant Recipients Lead High-Risk Populations

Hematopoietic stem-cell transplant recipients accounted for 35.74% of 2025 value, necessitating prophylaxis regimens featuring isavuconazole or echinocandins per updated ECIL guidance. Cell-free DNA monitoring augments early detection, enabling prompt therapeutic adjustment.

COPD and severe asthma patients show the swiftest 7.24% CAGR. Biomarkers such as C-reactive protein achieve 91.2% sensitivity for invasive aspergillosis in COPD cohorts, supporting earlier intervention. Broader screening will keep these populations pivotal within the aspergillosis treatment market.

Geography Analysis

North America held 33.12% of 2025 revenue, buoyed by rapid adoption of molecular diagnostics, sizable transplant programs, and robust funding for antifungal R&D. BARDA’s USD 268 million support for fosmanogepix illustrates governmental willingness to de-risk late-stage development. The FDA’s formal breakpoints for voriconazole guide stewardship and encourage uptake of susceptibility testing. ABPA prevalence data—2.8 per 10,000 asthma and 183.7 per 10,000 cystic fibrosis patients—reinforces the addressable base. Ongoing pilot programs for inhaled antifungal prophylaxis and widespread insurance coverage together anchor North America as the reference market for global launches within the aspergillosis treatment market.

Asia Pacific represents the fastest-growing region at 6.55% CAGR. China reports Aspergillus fumigatus dominance at 75.14% of isolates, with invasive pulmonary aspergillosis mortality reaching 68.87%. Indonesia’s I-CHROME survey underscores post-TB chronic pulmonary aspergillosis prevalence, with 69.4% IgG positivity. Japan finds 3.5% coinfection rates between nontuberculous mycobacteria disease and aspergillosis, markedly worsening prognosis. Rising transplant activity, improving reimbursement, and broader guideline implementation collectively underpin Asia Pacific’s brisk aspergillosis treatment market expansion.

Europe faces a duality of strong regulatory support and mounting environmental threats. The EMA’s approval of rezafungin and generic posaconazole widens therapeutic choice. Yet climate models project significant northward spread of Aspergillus habitats, potentially exposing millions more residents. Spain’s hospital cost data—peaking at EUR 1.4 million in 2012—highlights persistent economic strain. Agricultural azole usage furthers resistance, compelling European labs to scale surveillance and stewardship, reshaping procurement strategies across the aspergillosis treatment market.

Competitive Landscape

The aspergillosis treatment market remains moderately fragmented. Pfizer, Merck, and Astellas leverage extensive distribution networks and established antifungals such as voriconazole, posaconazole, and isavuconazole. Strategic extensions include Pfizer’s regional licensing of Cresemba in Asia Pacific, triggering USD 2.5 million milestone payments in 2025. Merck capitalizes on key segments via liposomal amphotericin B and echinocandin pipelines, while Astellas collaborates on inhaled formulations to sustain share within the aspergillosis treatment market.

Emerging innovators pursue distinct mechanisms and advanced delivery. F2G’s olorofim, an orotomide, and SCYNEXIS’s ibrexafungerp, the first oral glucan synthase inhibitor, illustrate the pivot beyond azoles and polyenes. Nanotechnology ventures focus on pulmonary and ocular targeting, while RNA-interference platforms advance dual-targeting antifungals capable of bypassing entrenched resistance.

Strategic M&A and funding alliances accelerate development. Basilea’s USD 268 million BARDA deal de-risks late-stage fosmanogepix trials. Licensing of weekly-dosed rezafungin to international partners broadens market access faster than stand-alone launches. Collectively, these moves signal a competitive race to address resistance and delivery challenges underpinning the future aspergillosis treatment market.

Aspergillosis Treatment Industry Leaders

Merck & Co., Inc

Basilea Pharmaceutica Ltd

Pfizer Inc.

Astellas Pharma

Sandoz

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Basilea Pharmaceutica secured up to USD 268 million from BARDA to advance fosmanogepix and BAL2062 for invasive mold infections.

- June 2025: Basilea recorded a second USD 2.5 million milestone as Pfizer’s Asia Pacific Cresemba sales passed contractual thresholds.

- March 2025: Climate-linked spread of Aspergillus prompted Biosergen to accelerate development of BSG005, a novel broad-spectrum antifungal.

Global Aspergillosis Treatment Market Report Scope

As per the scope of the report, aspergillosis treatment mainly consists of various antifungal agents and corticosteroids. Aspergillosis is a group of disorders caused by fungi known as Aspergillus. The conditions mainly affect people with compromised immune conditions.

The aspergillosis treatment market is segmented by type, drug class, route of administration, distribution channel, and geography. Based on type, the market is segmented as allergic aspergillosis, chronic aspergillosis, invasive aspergillosis, and aspergillomas. On the basis of drug class, the market is segmented into antifungal agents and other drug classes. Based on the route of administration, the market is segmented as oral drugs, ointments, powders, and other routes of administration. Based on distribution channel, the market is segmented as hospital pharmacy, retail pharmacy, and other distribution channels. The report also covers the market sizes and forecasts for the aspergillosis market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Allergic Aspergillosis |

| Chronic Pulmonary Aspergillosis |

| Invasive Aspergillosis |

| Azoles |

| Polyenes |

| Echinocandins |

| Allylamines & Others |

| Oral |

| Intravenous |

| Inhaled Dry-Powder |

| Nebulized / Other Targeted Delivery |

| Hospital Pharmacy |

| Retail Pharmacy |

| Online Pharmacy |

| Hematopoietic Stem-Cell Transplant (HSCT) Patients |

| Solid-Organ Transplant (SOT) Recipients |

| ICU / Critical-Care Patients |

| COPD & Severe Asthma Patients |

| Others (e.g., CGD, HIV) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Infection Type | Allergic Aspergillosis | |

| Chronic Pulmonary Aspergillosis | ||

| Invasive Aspergillosis | ||

| By Drug Class | Azoles | |

| Polyenes | ||

| Echinocandins | ||

| Allylamines & Others | ||

| By Formulation | Oral | |

| Intravenous | ||

| Inhaled Dry-Powder | ||

| Nebulized / Other Targeted Delivery | ||

| By Distribution Channel | Hospital Pharmacy | |

| Retail Pharmacy | ||

| Online Pharmacy | ||

| By Patient Category | Hematopoietic Stem-Cell Transplant (HSCT) Patients | |

| Solid-Organ Transplant (SOT) Recipients | ||

| ICU / Critical-Care Patients | ||

| COPD & Severe Asthma Patients | ||

| Others (e.g., CGD, HIV) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the aspergillosis treatment market size in 2026 and how fast is it growing?

The market is valued at USD 4.6 billion in 2026 and is projected to expand at a 4.26% CAGR through 2031.

Which infection type currently generates the most revenue?

Invasive aspergillosis leads the infection-type category with 43.95% of global revenue in 2025.

Which drug class is expected to grow the fastest?

Echinocandins show the highest forecast CAGR at 7.79% because they retain activity against azole-resistant strains and offer weekly dosing options.

Why is Asia Pacific the fastest-growing regional market?

Rising transplant volumes, expanding diagnostic capacity, and high mortality rates from invasive disease drive a 6.55% CAGR in Asia Pacific.

How is azole resistance affecting treatment strategies?

Escalating azole resistance is reducing first-line effectiveness, prompting a shift toward echinocandins, weekly-dosed rezafungin, and novel classes like orotomides.

What formulation trend is gaining momentum for prophylaxis and targeted therapy?

Inhaled dry-powder antifungals, such as next-generation voriconazole powders, are seeing 7.21% CAGR thanks to improved lung retention and lower systemic toxicity.

Page last updated on: