Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 27.42 Billion |

| Market Size (2026) | USD 29.27 Billion |

| Market Size (2031) | USD 40.55 Billion |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Sweet Biscuits Market Analysis by Mordor Intelligence

The Asia-Pacific sweet biscuits market size is expected to grow from USD 27.42 billion in 2025 to USD 29.27 billion in 2026 and is forecast to reach USD 40.55 billion by 2031 at 6.74% CAGR over 2026-2031. Multiple market drivers contribute to this growth. The expanding middle-income population in the region increases its expenditure on packaged snacks, including sweet biscuits, due to higher disposable income levels. Cookies dominate the market, but sandwich biscuits are gaining traction due to their premium appeal and innovative flavors. Plastic remains the most commonly used material, but there is a noticeable shift toward sustainable options like recyclable boxes, driven by environmental concerns. On the ingredient front, wheat-based biscuits continue to lead, although there is increasing innovation with oats and other healthier alternatives. Plain-flavored biscuits hold the largest market share, but flavored variants are growing rapidly as consumers seek variety. The distribution landscape is also evolving. Traditional retail channels, such as supermarkets and convenience stores, still account for the majority of sales.

Key Report Takeaways

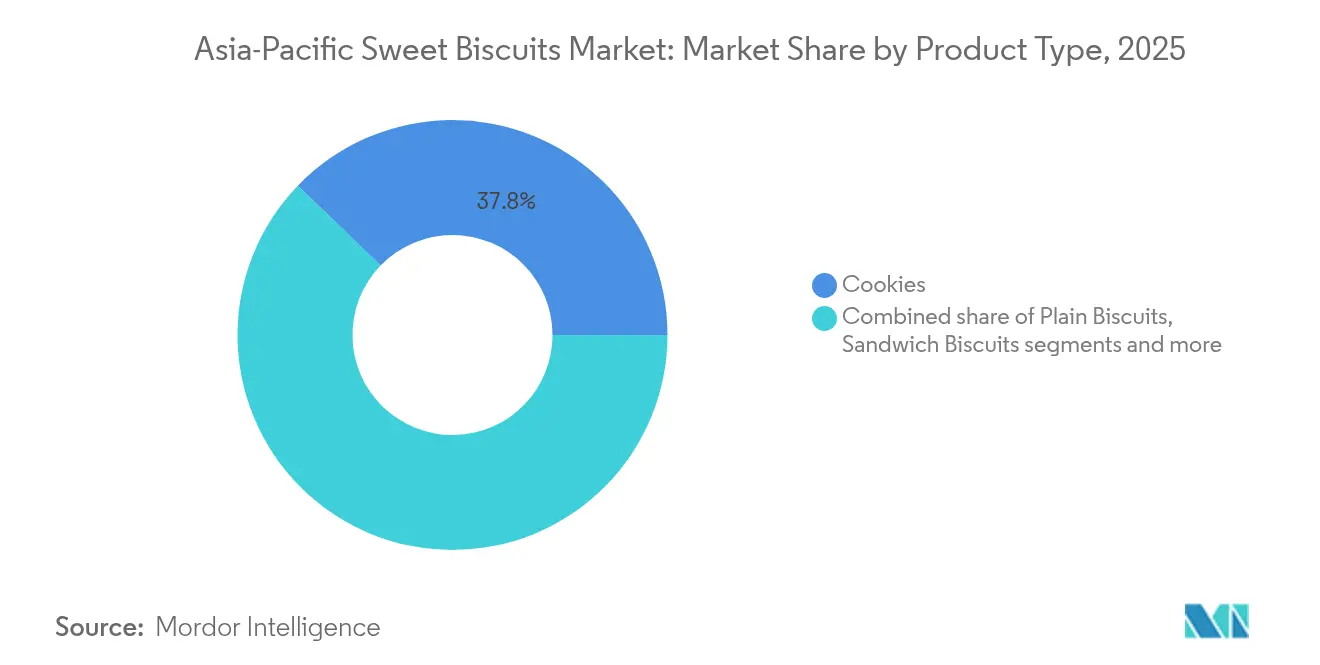

- By product type, cookies led with 37.78% of the sweet biscuits market share in 2025, whereas sandwich biscuits are advancing at a 6.86% CAGR to 2031.

- By packaging, plastic packets held 40.65% share of the sweet biscuits market size in 2025, while boxes are set to grow 6.98% CAGR through 2031.

- By ingredient base, wheat commanded 70.05% of the sweet biscuits market share in 2025; oat-based products are forecast to expand at 8.31% CAGR to 2031.

- By flavor profile, plain variants contributed 52.88% of the sweet biscuits market size in 2025, whereas flavored lines are rising at a 6.95% CAGR through 2031.

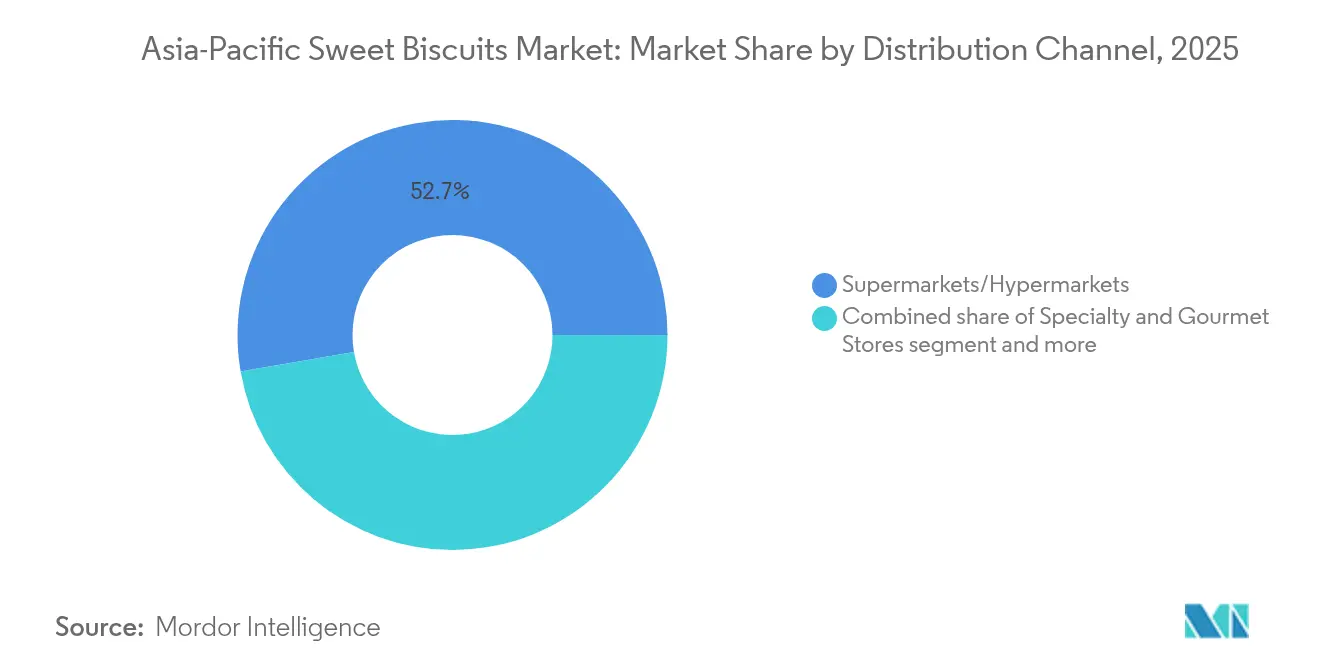

- By distribution channel, supermarkets/hypermarkets captured 52.72% revenue share in 2025; online retail is rising at 6.82% CAGR to 2031.

- By geography, China retained 28.12% share of the sweet biscuits market in 2025; India is on course for the fastest 8.02% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Sweet Biscuits Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for indulgent snack occasions | +1.2% | Higher impact in China, India, Southeast Asia | Medium Term (2-4 years) |

| Product innovation and flavor varieties | +0.9% | Asia-Pacific core, spill-over to emerging markets | Short Term (≤ 2 years) |

| Gifting culture boosts demand for sweet biscuits | +0.8% | China, India, Southeast Asia during festival seasons | Long Term (≥ 4 years) |

| Convenient portion packs and affordability | +1.1% | India, Indonesia, Philippines, Vietnam | Medium Term (2-4 years) |

| Children-centric and family-oriented marketing | +0.7% | Emphasis on urban centers | Long Term (≥ 4 years) |

| Growing middle class and increased spending power | +1.5% | India, Indonesia, Vietnam, Thailand | Long Term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Indulgent Snack Occasions

In the Asia-Pacific region, snacking is no longer just about satisfying hunger; it has become a way for people to find emotional comfort and connect socially. This behavior change has significantly increased the demand for premium sweet biscuits, even as inflation affects consumer spending. Many consumers are opting for indulgent varieties like chocolate-coated, cream-filled, and artisanal biscuits as a way to treat themselves or give as gifts. According to Mondelēz International’s 2024 State of Snacking report, 58% of consumers in the Asia-Pacific region look forward to snacks more than their main meals [1]Source: Mondelez International Inc., "2024-State of Snacking," mondelezinternational.com. Seasonal flavors, such as matcha or sakura variants in Japan, are also gaining popularity as they cater to local tastes and preferences. Brands are leveraging this trend by introducing culturally relevant and limited-edition flavors that resonate with consumers. For instance, Oreo (Mondelēz) launched its “Oreo Blackpink Limited Edition” in Southeast Asia, featuring berry-flavored cream and collectible packaging, which quickly became popular on social media and encouraged impulse buying.

Growing Middle Class and Increased Spending Power

In the Asia-Pacific region, countries like Indonesia, Vietnam, and Thailand are seeing a fast-growing middle-class population, which is leading to higher spending on packaged and indulgent food products, including sweet biscuits. As more people have extra income to spend, they are choosing better-quality and well-known biscuit brands, creating a clear trend toward premium products, even with rising costs. According to the USDA, the Southeast Asia population is projected to increase by 8% from 2023 to 2033, which will significantly increase the demand for branded snacks [2]Source: US Department of Agriculture, " Southeast Asia: Growing Potential for U.S. Agriculture", ers.usda.gov. To meet this demand, companies like Mondelez are building local factories to produce biscuits. For example, Mondelez’s factory in Vietnam makes Oreo and LU biscuits that are customized to match local tastes and budgets, making these products more appealing and accessible to a wider range of people. The disposable income in the Asia-Pacific region, measured as GDP per capita in terms of purchasing power parity, is around USD 21.59 thousand. This growing income level means that more consumers can afford to spend on premium snacks, allowing them to enjoy high-quality, indulgent products like sweet biscuits more often.

Children-Centric and Family-Oriented Marketing

In the Asia-Pacific region, changing family dynamics and a growing youth population are driving the demand for sweet biscuits, especially through products marketed for children and families. Countries like the Philippines, India, and Indonesia have a large number of young people, making children key influencers in household snack purchases. This has led brands to focus on creating products and marketing campaigns that appeal to families. For example, children often play a significant role in grocery shopping decisions, particularly for items like biscuits, cereals, and beverages, as highlighted by the Philippine News Agency. To meet this demand, companies such as Monde Nissin are investing heavily in expanding their production capacity. One notable example is their PHP 7.55 billion investment in Northern Luzon, aimed at increasing the supply of popular family-oriented products like SkyFlakes and Graham biscuits. These products are often marketed with themes of togetherness, sharing, and nutrition, striking a balance between appealing to children and addressing parents' concerns.

Gifting Culture Boosts Demand for Sweet Biscuits

Cultural and religious festivals across Asia-Pacific, such as Chinese New Year, Diwali, Hari Raya, and Eid, play a key role in boosting the demand for premium sweet biscuits, especially as gifts during these celebrations. Gifting is an important tradition during these festivals, which leads to a significant increase in biscuit sales. Brands often release special editions with eye-catching packaging and unique flavors that reflect the festive spirit. These products are designed to stand out on store shelves and appeal to consumers looking for thoughtful and visually appealing gifts. For example, in China, Danisa’s Danish Butter Cookies and Ferrero’s festive assortments are popular choices for gifting during the Lunar New Year. Similarly, in India, brands like Parle and Britannia launch special gift boxes during Diwali, featuring festive designs and messages. These seasonal offerings not only help brands achieve higher sales but also allow them to connect more deeply with consumers by aligning with cultural traditions and offering exclusive, limited-time products that enhance the festive experience.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Sugar-reduction regulations hampering growth | -0.6% | Indonesia, Thailand, and Singapore with regulatory leadership | Short term (≤ 2 years) |

| Rising raw material costs | -0.8% | Particularly affecting smaller manufacturers | Short term (≤ 2 years) |

| Competition from traditional savory snacks | -0.4% | India, China, Southeast Asia | Medium term (2-4 years) |

| Rising health consciousness | -0.5% | Japan, Australia, and urban centers across Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sugar-Reduction Regulations Hampering Growth

Across Asia-Pacific, governments are taking stronger steps to reduce sugar consumption, introducing regulations that are creating challenges for the sweet biscuits market. Countries like Singapore, with its Nutri-Grade labeling system, Thailand, which has implemented a sugar tax, and Indonesia, which is considering front-of-pack warnings, are leading these efforts. These regulations aim to tackle public health issues like obesity and diabetes by setting limits on sugar content and requiring clear labeling. The International Diabetes Federation reported that Japan's adult diabetic population reached 93.2 million in 2024 [3]Source: International Diabetes Federation, "Diabetes in Japan (2024)", idf.org . As a result, manufacturers are being pushed to reformulate their products to meet these new standards. This often involves using alternative sweeteners or reducing the sugar content, which can increase production costs. These changes can affect the taste of the biscuits, which is a major factor influencing consumer purchases in this category. According to reports from the USDA and local health agencies, these policies are putting pressure on brands to find a balance between meeting regulatory requirements and maintaining the taste that consumers expect. This balancing act could slow down innovation and limit growth in a market where taste plays a critical role in driving demand.

Competition from Traditional Savory Snacks

In many Asia-Pacific countries, traditional savory snacks like rice crackers in Japan, murukku in India, and shrimp chips in Southeast Asia remain highly popular, creating challenges for the growth of the sweet biscuits market. These snacks are deeply tied to local cultures and are often seen as more familiar and suitable for daily consumption. Many consumers prefer these savory options because they are perceived as healthier or more filling, especially when made with ingredients like lentils, pulses, or seaweed. Local vendors and small-scale producers dominate the market with affordable and flavorful options, making it harder for sweet biscuit brands to compete for shelf space and consumer spending. This strong preference for savory snacks, particularly in rural or price-sensitive areas, limits the opportunities for sweet biscuits to expand. To overcome this, sweet biscuit brands need to focus on creating unique flavors, introducing innovative products, or even blending sweet and savory elements to attract a wider audience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cookies Lead While Sandwich Biscuits Accelerate

In 2025, cookies accounted for 37.78% of the sweet biscuits market, driven by their widespread appeal and strong brand recognition from popular products like Oreo. These cookies have become a staple snack due to their consistent taste and quality, making them a favorite among consumers of all ages. Sandwich biscuits, which feature cream or chocolate fillings, are expected to grow faster than other formats, with a projected CAGR of 6.86%. Manufacturers are focusing on creating unique flavor combinations, such as coffee-flavored creams or layered textures, to appeal to adults seeking indulgent snack options. This strategy aligns with trends seen in the confectionery market, where innovation drives consumer interest.

Plain biscuits remain a key choice in price-sensitive regions, ensuring steady sales volumes, while chocolate-coated biscuits are gaining popularity in urban areas, supported by advancements in temperature-resistant coatings. Newer formats like protein-enriched, gluten-free, and functional biscuits are gradually carving out a niche in health-focused aisles. Although these emerging categories currently hold less than 2% of the market share, they are gaining attention as consumers increasingly prioritize health and wellness. This shift presents opportunities for manufacturers to diversify their offerings and cater to evolving consumer preferences.

By Packaging Type: Plastic Dominates as Boxes Gain Sustainability Momentum

Flexible plastic dominated the packaging market with a 40.65% share in 2025, mainly because it is cost-effective and provides strong protection against moisture, which is essential in Asia-Pacific's humid climate. However, increasing environmental concerns and stricter regulations on single-use plastics are pushing manufacturers to adopt more sustainable packaging options. Fiber-based boxes are gaining popularity and are expected to grow at a 6.98% CAGR, as they meet retailer sustainability standards and help companies avoid eco-taxes. For example, Mondelēz and Saica Group have introduced recyclable paper solutions that reduce virgin plastic usage by up to 25% per multipack, setting a benchmark for eco-friendly packaging in the industry.

Metal tins, on the other hand, continue to play a significant role in the market, especially for gifting purposes. These tins are particularly popular during festive seasons as they offer a premium and reusable packaging option, allowing manufacturers to charge higher prices. The shift toward sustainable packaging is not only driven by regulations but also by the growing demand from environmentally conscious consumers. As a result, the industry is increasingly focusing on innovative and sustainable packaging solutions to meet both regulatory requirements and consumer preferences.

By Ingredient Base: Wheat Foundation Challenged by Oat Innovation

Wheat flour remains the primary ingredient in sweet biscuits, making up 70.05% of formulations due to its widespread availability and ease of processing. However, consumer preferences are gradually shifting toward healthier options, leading to a rise in oat-based products. These products are growing at a strong 8.31% CAGR as more people focus on heart health and fiber-rich diets. In Japan, dietary guidelines recommend a daily fiber intake of over 20 grams for men, which has encouraged the use of ingredients like BARLEYmax and beta-glucan in sweet biscuits. This trend is helping oats transition from being a niche ingredient to becoming a mainstream choice in the industry.

In addition to oats, alternative grains such as sorghum and millet are gaining traction, especially in gluten-free or low glycemic index (GI) products. These grains are particularly appealing to health-conscious urban consumers who are willing to pay a premium for innovative and nutritious options. Manufacturers are leveraging these grains to cater to the growing demand for healthier snacks, which aligns with the broader trend of functional and specialty foods. This shift not only diversifies product offerings but also helps brands tap into a more affluent and health-aware customer base.

By Distribution Channel: Traditional Retail Leads While Digital Channels Surge

Supermarkets/hypermarkets accounted for 52.72% of sales in 2025, driven by their ability to showcase promotions and strategically place sweet biscuits near complementary products like beverages, encouraging additional purchases. These stores remain a preferred choice for consumers due to their wide product variety and convenience. In-store promotions and discounts further boost sales, making these outlets a dominant channel for sweet biscuits. Their physical presence also allows consumers to explore and compare products before purchasing, which is particularly appealing in regions where online shopping is less prevalent.

However, online channels are growing rapidly, with a projected CAGR of 6.82%, supported by the booming e-commerce market in countries like India. Direct-to-consumer websites and quick-commerce platforms are gaining traction as they offer lower listing fees and a broader range of products. These platforms also enable regional manufacturers to experiment with innovative offerings, such as subscription snack boxes, to attract a loyal customer base. Meanwhile, convenience stores in markets like Indonesia and the Philippines cater to immediate consumption needs, while vending machines and institutional sales provide additional revenue streams outside traditional retail formats.

By Flavor Profile: Plain Maintains Majority as Flavored Variants Accelerate

Plain sweet biscuits accounted for 52.88% of the market share in 2025, primarily due to their affordability and widespread appeal across different age groups. These biscuits are a staple choice for many consumers, offering simplicity and familiarity. However, the demand for flavored biscuits is growing rapidly, as consumers increasingly seek unique and exciting taste experiences. Flavored options, such as chocolate, vanilla, and fruit-infused varieties, are expected to drive nearly half of the market's growth and rise at a 6.95% CAGR through 2031. Flavors inspired by regional preferences, like matcha, pandan, and tropical fruits, are gaining popularity, helping brands cater to diverse consumer tastes in the Asia-Pacific region.

Innovative combinations and textures are also playing a significant role in boosting the appeal of flavored biscuits. Products that combine crunchy exteriors with creamy or soft fillings are particularly popular, as they offer a multi-sensory eating experience. Co-branded products, such as the Biscoff-Cadbury collaboration, are blending traditional flavors with modern twists, attracting both loyal and new customers. These innovations not only enhance the perceived value of the products but also help brands stand out in a competitive market. As a result, flavored biscuits are becoming a key growth driver in the sweet biscuits market, appealing to consumers looking for indulgence and variety.

Geography Analysis

China held a significant 28.12% share of the sweet biscuits market in 2025, driven by its large-scale production capabilities, efficient supply chains, and strong export performance. The country’s snack industry has already surpassed CNY 1 trillion in revenue, supported by initiatives like nationwide voucher schemes that encourage domestic consumption. Companies are expanding into smaller cities, with examples like Mingming Henmang operating over 14,000 outlets, which helps improve distribution and supports the growth of local and regional brands.

India is expected to grow at the fastest rate, with a projected CAGR of 8.02% through 2031, fueled by increasing disposable incomes and widespread smartphone adoption. These factors are driving higher demand for packaged snacks across both rural and urban areas. ITC has announced a five-year investment plan worth INR 200 billion, with 35%-40% allocated to FMCG expansion, focusing on flagship brands and introducing health-focused product lines. Additionally, partnerships like Mondelēz collaborating with Lotus Bakeries to produce Biscoff locally are leveraging India’s cost-effective manufacturing while offering diverse flavor options to consumers.

Southeast Asia offers varied growth opportunities across its markets. In Indonesia, the retail food sector reached really high level, with bakery products growing at over 10% annually. However, challenges like front-of-pack labeling and Halal compliance add to production costs. In Vietnam, the biscuits market shows potential for consolidation, with Orion Food Vina holding a dominant share in the Chocopie segment, supported by strong distribution networks and frequent product innovations. Meanwhile, in Thailand, companies are focusing on premium products and reduced-sugar options to align with sugar-tax regulations and cater to health-conscious consumers, particularly millennials.

Competitive Landscape

The sweet biscuits market is moderately fragmented, creating opportunities for companies to grow through mergers or by setting up new facilities. In India, ITC has emerged as the largest food player by leveraging its strong marketing strategies and rural distribution network for its Sunfeast and Dark Fantasy brands. This has allowed ITC to surpass Britannia in revenue in 2024. Regional players like Parle Products and Orion are focusing on micro-pricing strategies to protect their market share from global competitors.

Global companies are focusing on increasing production capacity and investing in research and development to stay competitive. For instance, Mondelēz acquired China’s Evirth in 2024 to strengthen its position in the USD 3 billion cake and pastry segment. The company opened a Center of Excellence in Singapore to develop snacks tailored for Southeast Asian markets. Companies are also adopting advanced technologies like AI for demand forecasting to optimize production schedules and augmented reality for maintenance, which helps reduce downtime and improve efficiency.

Sustainability has become a key focus area for companies in the sweet biscuits market. Efforts to reduce the use of virgin plastic, adopt renewable energy, and ensure traceable grain sourcing are aligning with retailer requirements and consumer preferences, especially among millennials. Companies that prioritize sustainability are gaining an edge by securing better shelf space in stores and avoiding potential regulatory penalties. These eco-friendly initiatives are not only meeting environmental goals but also helping businesses achieve tangible growth in market share.

Asia-Pacific Sweet Biscuits Industry Leaders

-

Mondelez International Inc.

-

ITC Limited

-

Britannia Industries Ltd.

-

Parle Products Pvt. Ltd.

-

Fujiya Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Monde Nissin has allocated PHP 7.55 billion to establish a new manufacturing facility in Northern Luzon. This facility will primarily focus on producing SkyFlakes and Graham biscuit lines, aiming to meet the growing demand for these popular products.

- February 2025: The Arnott's Group has opened a new 45,000 m² allergen-free facility in Rowville, Victoria. This state-of-the-art facility is designed to cater to the growing demand for allergen-free products.

- May 2024: Mondelēz has established a USD 5 million Biscuit and Baked Snacks Lab in Singapore. This facility aims to accelerate the development of innovative products tailored to meet the evolving preferences of consumers in the region.

Asia-Pacific Sweet Biscuits Market Report Scope

A sweet biscuit is a flour-based baked and shaped food product. In most countries, biscuits are typically hard, flat, and unleavened. They are usually sweet and may be made with sugar, chocolate, icing, jam, ginger, or cinnamon. Asia-Pacific sweet biscuits market is segmented by type, by distribution channel, and by country. Based on the product type, the market is segmented into plain biscuits, cookies, sandwich biscuits, chocolate-coated biscuits, and other sweet biscuits. By distribution channel, the market is segmented into supermarkets/ hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels, and by country into China, Japan, India, Australia, and the Rest of Asia-Pacific. For each segment, the market sizing and forecasts have been done on the basis of value (in USD billion).

By Product Type

| Plain Biscuits |

| Cookies |

| Sandwich Biscuits |

| Chocolate-Coated Biscuits |

| Others |

By Packaging Type

| Boxes |

| Plastic Packets/On-the-Pouches |

| Others (tins, jars, etc.) |

By Ingredient Base

| Wheat |

| Oat |

| Others |

By Flavor Profile

| Plain |

| Flavored |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty and Gourmet Stores |

| Online Retail |

| Other Distribution Channels |

By Geography

| China |

| Japan |

| India |

| South Korea |

| Indonesia |

| Thailand |

| Vietnam |

| Australia |

| New Zealand |

| Rest of Asia-Pacific |

| By Product Type | Plain Biscuits |

| Cookies | |

| Sandwich Biscuits | |

| Chocolate-Coated Biscuits | |

| Others | |

| By Packaging Type | Boxes |

| Plastic Packets/On-the-Pouches | |

| Others (tins, jars, etc.) | |

| By Ingredient Base | Wheat |

| Oat | |

| Others | |

| By Flavor Profile | Plain |

| Flavored | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty and Gourmet Stores | |

| Online Retail | |

| Other Distribution Channels | |

| By Geography | China |

| Japan | |

| India | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size of the Asia-Pacific sweet biscuits market?

The market is valued at USD 29.27 billion in 2026 and is projected to grow to USD 40.55 billion by 2031 at a 6.74% CAGR.

Which country is expanding fastest in regional sweet biscuit sales?

India holds the highest growth trajectory at an 8.02% CAGR between 2026 and 2031, spurred by rising incomes and rapid e-commerce expansion.

What product segment offers the greatest growth opportunity?

Sandwich biscuits are forecast to expand at a 6.86% CAGR, benefiting from premium fillings and innovative flavor combinations that lift margins.

Which retail channel is set to post the highest growth?

Online retail is climbing at a 6.82% CAGR, supported by widening internet penetration and quick-commerce models reaching consumers in mid-tier cities.

Page last updated on: