Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | |

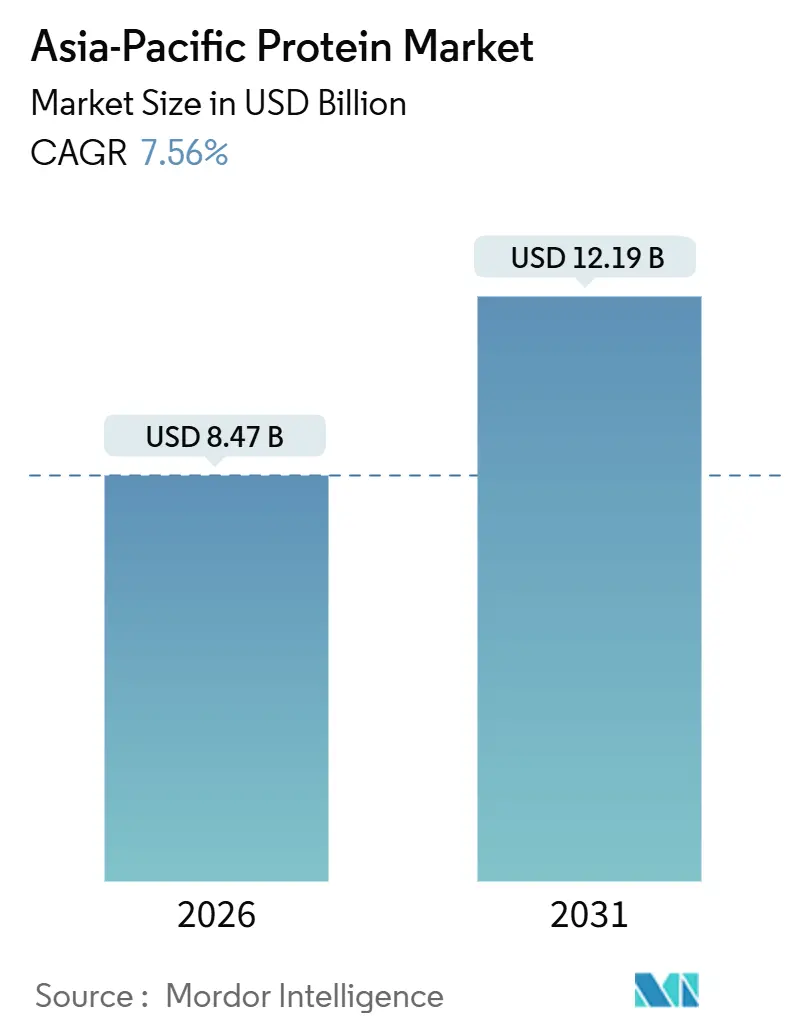

| Market Size (2026) | USD 8.47 Billion |

| Market Size (2031) | USD 12.19 Billion |

| Growth Rate (2026 - 2031) | 7.56% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Protein Market Analysis by Mordor Intelligence

The Asia Pacific protein market size is valued at USD 8.47 billion in 2026 and is projected to climb to USD 12.19 billion by 2031, advancing at a 7.56% CAGR during the forecast period. In China and India, robust sovereign food-security programs are steering the growth trajectory, alongside a widening uptake of sports nutrition and a steady pivot toward value-added isolates and hydrolysates. Processor strategies are bifurcating: while established dairy cooperatives double down on whey concentrates, venture-backed fermentation start-ups race to commercialize microbial proteins, sidestepping the volatility of milk and oilseed prices. In Indonesia, India, and China, mandatory protein-fortification policies are expanding the total addressable demand pool. Moreover, direct-to-consumer e-commerce channels now represent over one-third of the region's supplement sales, effectively cutting retail mark-ups and accelerating brand proliferation. While the Asia Pacific protein market enjoys a boost from the post-ASF recovery in animal agriculture, the economics of precision fermentation and regulatory ambiguities surrounding novel proteins temper the near-term optimism.

Key Report Takeaways

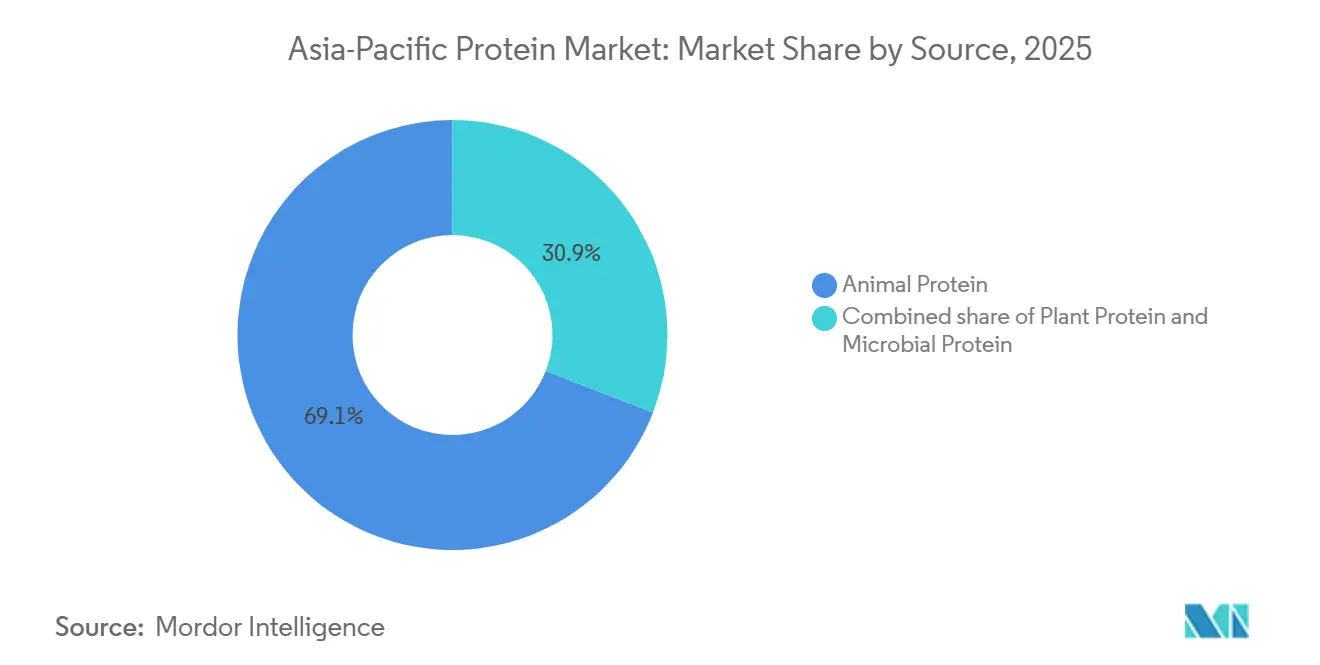

- By source, animal protein held a 69.13% share in 2025, while microbial protein is forecast to register the fastest 9.53% CAGR through 2031.

- By form, concentrates commanded 46.71% of revenue in 2025; hydrolysates are projected to expand at an 8.40% CAGR.

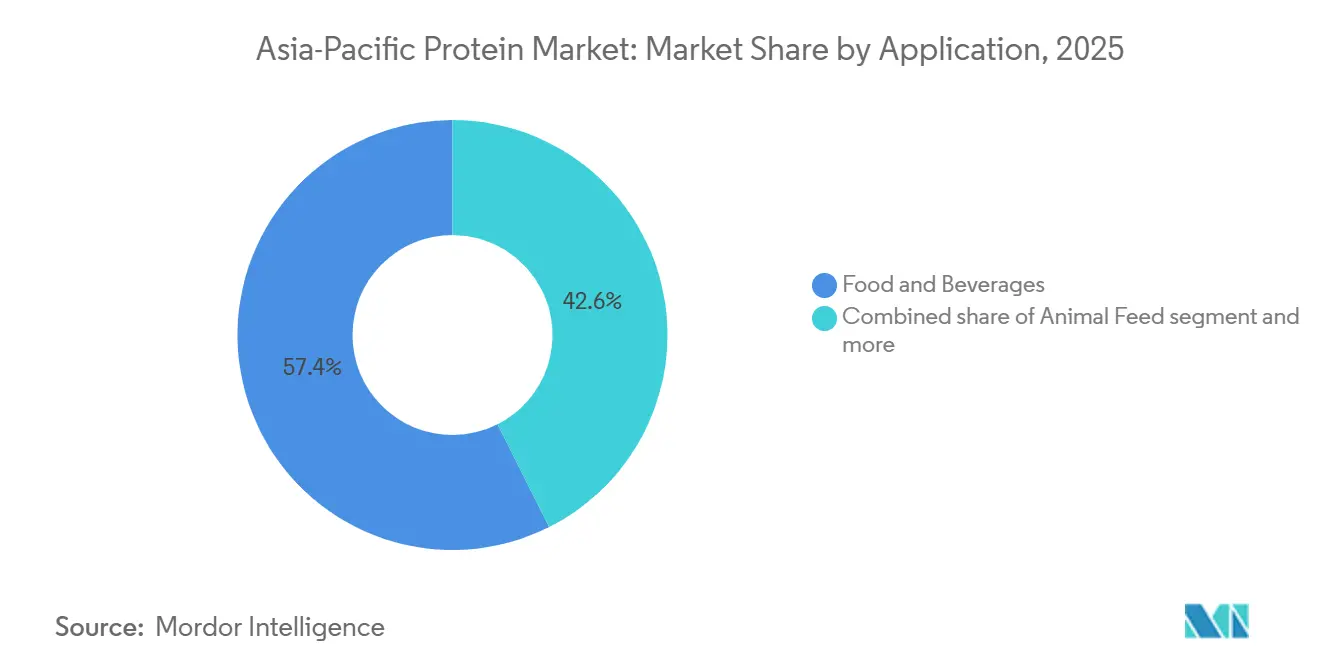

- By end user, food and beverage applications led with 57.42% of demand in 2025, whereas sport and performance nutrition is advancing at an 8.15% CAGR.

- By geography, China captured 43.52% of regional revenue in 2025, yet Indonesia is the fastest-growing market at an 8.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth in sports nutrition and active lifestyle products | 1.2% | China, India, South Korea, urban Southeast Asia | Short term (≤ 2 years) |

| Government food security targets fueling domestic protein self-sufficiency | 1.5% | China, India, Indonesia | Medium term (2-4 years) |

| Advances in precision fermentation lowering production costs | 0.8% | Global, with early adoption in Singapore, South Korea, Japan | Long term (≥ 4 years) |

| E-commerce enabling DTC distribution of niche protein formats | 0.9% | China, India, Indonesia, Thailand | Short term (≤ 2 years) |

| Recovery of animal protein supply chains post-ASF and HPAI outbreaks | 0.7% | China, Vietnam, Thailand, Philippines | Short term (≤ 2 years) |

| Mandatory protein fortification policies in select Asia-Pacific countries | 1.1% | Indonesia, India, China, Philippines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid growth in sports nutrition and active lifestyle products

As disposable incomes rise and urban gym memberships surge, consumers are increasingly gravitating towards high-protein shakes, bars, and functional snacks. Glanbia's performance-nutrition unit in the Asia-Pacific region boasted a 14% year-on-year revenue growth in 2025, with China and India driving the momentum, contributing to 68% of the added volume. Regulatory bodies are also playing a role; in the first half of 2025, South Korea greenlit 12 new sports-nutrition SKUs, expanding the market beyond traditional whey powders. E-commerce giants like Douyin and WeChat mini-programs are streamlining the market entry process, reducing the need for middlemen. This agility enables brands to experiment with lactose-free blends, combining whey isolates with rice or pea protein. While urban consumers earning over USD 15,000 annually represent the primary target audience, there's still untapped potential in rural areas. Ongoing advancements in flavor masking and rapid-absorption hydrolysates are poised to keep the momentum going in the medium term.

Government food security targets fueling domestic protein self-sufficiency

In 2024, Beijing's State Council allocated CNY 50 billion in subsidies in the form of insurance, aiming to boost soy-protein self-sufficiency by 2030 and reduce dependence on imported soybean meal[1]Source: Organisation for Economic Co-operation and Development, “Agricultural Policy Monitoring and Evaluation 2025,” oecd.org. This initiative is part of China's broader strategy to enhance food security and reduce vulnerability to global supply chain disruptions. In 2025, India's National Mission on Edible Oils and Oilseeds set aside INR 110 billion (USD 1.32 billion) to enhance domestic output of soybean and pulse proteins, addressing a persistent 60% reliance on imports[2]Source: Press Information Bureau, “National Mission on Edible Oils,” pib.gov.in. The program focuses on increasing cultivation areas, improving seed quality, and providing financial support to farmers. Under Presidential Regulation 18/2024, Indonesia mandates that by 2027, 40% of protein in government food-aid programs must be sourced locally, channeling investments into crushing plants in Java and Sumatra. This regulation aims to strengthen the domestic agricultural sector and reduce dependency on imported protein sources. Together, these initiatives redirect over USD 2 billion in annual imports to local supply chains. While challenges like fragmented farmer cooperatives and infrastructure gaps pose risks, public-private partnerships are actively working to address these issues by fostering collaboration between governments, private investors, and local stakeholders.

Advances in precision fermentation lowering production costs

Singapore's A STAR committed SGD 120 million in grants to pilot facilities, to commercialize egg-white and casein analogs for halal export markets. This initiative aims to cater to the growing demand for halal-certified protein alternatives, particularly in Southeast Asia and the Middle East. South Korea's CJ CheilJedang, at its Incheon plant, achieved a 42% energy saving per kilogram of microbial protein through AI-optimized nutrient dosing. This technological advancement highlights the potential for cost reduction and sustainability in microbial protein production. Japan's NEDO invested JPY 8 billion into algae-protein consortia, focusing on nutrition for the elderly, capitalizing on the nation's aging demographic as a testing ground. The project seeks to address the increasing nutritional needs of Japan's elderly population while exploring scalable applications for algae-based proteins. Even with capital expenditure challenges, fermentation plants, while costing three times more than soy-extraction units, indicate a promising scaling pathway post-2027, bolstered by efficiency gains and public subsidies. These developments collectively underscore the growing momentum in alternative protein markets driven by innovation, demographic shifts, and supportive government policies.

E-commerce enabling DTC distribution of niche protein formats

In 2025, direct-to-consumer channels accounted for a significant portion of China's protein-supplement sales, a notable rise from the double-digit figures recorded in 2023. Brands in China are increasingly turning to livestream commerce, allowing them to sidestep the margins typically associated with brick-and-mortar stores. Following suit, India has seen its online protein retail surge at a 31% CAGR, bolstered by subscription models that ensure consistent monthly orders. In Indonesia, 62% of protein-supplement transactions were conducted online in 2025. This trend was supported by the cash-on-delivery option, which caters to the country's limited credit-card usage. In Thailand, Central Retail unveiled a dedicated protein vertical in 2025, collaborating with Kerry Group to provide same-day delivery services in Bangkok and Chiang Mai. While this swift transition to direct channels offers niche brands enhanced visibility and valuable data feedback, it also intensifies price competition and underscores the need for robust logistics networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw milk and oilseed prices compress processor margins | -0.6% | Global, acute in India, China, Australia | Short term (≤ 2 years) |

| Regulatory uncertainty for novel proteins (cultivated, insect) | -0.4% | Japan, China, India; Singapore exempt | Medium term (2-4 years) |

| Facility registration and tariff barriers pose challenges to imported inputs. | -0.5% | National, affecting importers and multinational ingredient suppliers | Medium term (2–4 years) |

| Emerging domestic producers face talent gaps in quality assurance. | -0.3% | Regional, prevalent in Tier-2 and Tier-3 manufacturing clusters across the region | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile raw milk and oilseed prices compress processor margins

In 2024, U.S. WPC80 export prices to Asia fluctuated between USD 3.20 and USD 4.85 per kilogram, a 52% range that compelled processors to either hedge or confront spot-market risks[3]Source: United States Department of Agriculture, “Dairy: World Markets and Trade,” esmis.nal.usda.gov. This volatility in pricing created significant challenges for market participants, particularly those reliant on stable input costs for production planning. Erratic monsoons in July 2025 led to a 38% year-on-year surge in India's soybean prices, squeezing crusher margins and driving up soy-isolate costs, which further strained the supply chain for plant-based protein manufacturers. Late in 2024, China released 500,000 tons of soybean reserves, stabilizing crushing spreads and providing temporary relief to the market. However, by mid-2025, domestic isolate prices were still 22% higher than the 2023 average, reflecting persistent cost pressures. In 2025, Fonterra implemented a 9% price increase on whey protein, coinciding with a 14% rise in feed and energy costs for Australian dairy farmers, which added to the financial burden on the dairy sector. Such price fluctuations are prompting food manufacturers to pivot towards rice or wheat protein, where functionality allows, thereby challenging the market for premium isolates and reshaping protein sourcing strategies.

Regulatory uncertainty for novel proteins (cultivated, insect)

Japan's health ministry, responding to industry petitions, has delayed finalizing safety guidelines for cricket protein. This hold-up has pushed retail launches to the sidelines, allowing only limited food-service pilots to proceed. In 2024, China designated cultivated meat as a "new food resource." This move set off extensive toxicology and allergenicity reviews, with industry experts estimating a timeline of four to six years. In December 2024, India retracted its draft regulations on insect protein, facing cultural resistance. This withdrawal has left the pathways for approval in limbo. Singapore stands apart, having greenlit 16 SKUs of cultivated meat. However, due to steep production costs, these products find their way only to upscale restaurants. Meanwhile, Thailand has given the nod to insect protein for animal feed, but it's still off the table for human consumption. This limitation has pushed start-ups like Nutrition Technologies to focus solely on export markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Microbial Gains Despite Animal-Protein Dominance

In 2025, animal protein claimed a dominant 69.13% share of the Asia Pacific protein market, propelled by rising demand for whey concentrates in both sports nutrition and infant formulas. While traditional dairy proteins like casein and egg derivatives cater to specific formulation needs, underscoring the segment's versatility, dairy-based proteins still set the standard for functionality, digestibility, and pricing. Their established role in performance and medical nutrition cements animal protein's leading position. However, this dominance faces challenges from regulatory scrutiny and sustainability concerns.

On the other hand, microbial protein is emerging as the fastest-growing segment, with projections indicating a robust 9.53% CAGR through 2031. This growth is fueled by rapid advancements in fermentation infrastructure, edging it closer to cost parity with traditional animal sources. Its allure lies in being antibiotic-free, non-GMO, and sustainably produced, making it a preferred choice for progressive formulators. Furthermore, active venture funding in precision-fermentation startups from Singapore and South Korea highlights the industry's belief in microbial protein's potential to challenge dairy's supremacy, contingent on continued regulatory clarity and growing consumer acceptance.

By Form: Hydrolysates Command Premium Despite Concentrate Volume Lead

In 2025, concentrates dominated the Asia Pacific protein market, claiming a substantial 46.71% share. Their strong price-to-functionality advantage has made them a staple in bakery, beverage, and feed applications. This versatility and cost efficiency have solidified their status as the go-to choice for both large-scale producers and value-driven formulations. While there's a push towards higher-value formats, concentrates remain pivotal, driving volume growth and establishing pricing benchmarks throughout the supply chain. To stay competitive, manufacturers are adopting partial hydrolysis techniques, boosting digestibility without compromising on cost.

Hydrolysates are on a rapid ascent, projected to grow at an impressive 8.40% CAGR through 2031. This surge is predominantly driven by China's GB 10765 infant-formula standards, which lean towards pre-digested proteins for enhanced absorption. The premium pricing of these proteins, especially in infant and clinical nutrition, further propels the segment's revenue growth. Industry players like Arla Foods Ingredients and Hilmar Cheese are ramping up capacities to leverage this regulatory momentum. Meanwhile, the rising popularity of clear-protein beverages in Japan and South Korea underscores the acceptance of hydrolyzed whey, celebrated for its quick recovery and hypoallergenic properties.

By End User: Sport Nutrition Outpaces Food Despite Smaller Base

In 2025, the Asia Pacific protein market saw food and beverages dominate, capturing 57.42% of the revenue. This expansive category includes bakery items, dairy alternatives, meat substitutes, and ready-to-eat meals, underscoring the integral role of protein in daily diets. Within the food sector, dairy and its alternatives take the lead. Whey concentrates enhance yogurt and cheese substitutes, while soy and pea isolates are foundational to plant-based milks and frozen treats. Both the meat and bakery sectors experience consistent growth, driven by population demands, utilizing soy, wheat, and gluten proteins for binding and texture. In beverages, ready-to-drink protein shakes are gaining momentum, especially in China and India, as urban lifestyles prioritize convenience.

Sport and performance nutrition is the fastest-growing segment, with projections of an 8.15% CAGR through 2031. This growth is fueled by rising gym memberships, the influence of marketing personalities, and a heightened understanding of protein's benefits for recovery and fitness. The lines between this segment and supplements are increasingly blurred, thanks to innovations in ready-to-mix and portable powders catering to varied fitness needs. In China, Japan, and India, brand ecosystems are gravitating towards premium, clean-label, and functional attributes. Consequently, sports nutrition is not just boosting protein demand but also spurring product differentiation in the wider functional foods arena.

Geography Analysis

China, with a commanding 43.52% share of the revenue, solidifies its dual identity as both a consumption powerhouse and an emerging producer. In the provinces of Heilongjiang and Shandong, state subsidies amounting to CNY 50 billion are bolstering soy crushing and fermentation hubs. However, a notable 68% of whey inputs for domestic infant-formula brands still come from imports, highlighting a vulnerability in the supply chain. Thanks to Alibaba's backing, e-commerce platforms have surged direct-to-consumer protein sales to constitute 38% of the overall supplement turnover. This shift not only diversifies brands but also heightens price competition. While cultivated meat faces regulatory scrutiny, commercial rollouts remain a distant prospect, likely not before 2028. For the time being, microbial protein finds its niche in feed and pilot projects.

Indonesia stands out with the highest projected CAGR of 8.24% through 2031. This growth is largely driven by a government fortification mandate, stipulating 6 grams of protein per 100 grams in subsidized staples. In response to this rising demand, Wilmar International has ramped up its soy-protein capacity by 18,000 tons in 2024. However, distribution challenges arise as cold-chain deficiencies limit the reach of dairy-based proteins outside major metropolitan areas. E-commerce platforms dominate the landscape, accounting for 62% of supplement sales. They adeptly utilize cash-on-delivery methods to navigate the challenges posed by low credit card penetration. Meanwhile, the government, through BPOM audits, ensures strict compliance in the sector.

Countries like India, Japan, South Korea, Thailand, Vietnam, Malaysia, and Australia each contribute distinct narratives to the protein market. In a significant policy shift, India's FSSAI has greenlit the use of domestically sourced pea and chickpea isolates in fortified staples, reducing the nation's dependence on imported whey. Meanwhile, Japan grapples with its own challenges: while pending guidelines on insect protein stall local commercialization, the NEDO agency is championing algae-protein research and development, especially for elder nutrition. South Korea has harnessed AI to cut down energy inputs in fermentation processes. In Thailand, a revival in pork-feed demand follows the establishment of ASF-free zones. Vietnam witnesses a resurgence in soy-meal sales, buoyed by a rebound in its pig population. Malaysia's halal regulations are steering Singaporean startups towards egg-white analogs that meet approval standards. And in a strategic pivot, Australia's Fonterra is shifting focus from bulk powder exports to the more lucrative native whey isolates. Together, these varied country-specific developments weave a complex tapestry of opportunities and challenges in the Asia Pacific protein market.

Competitive Landscape

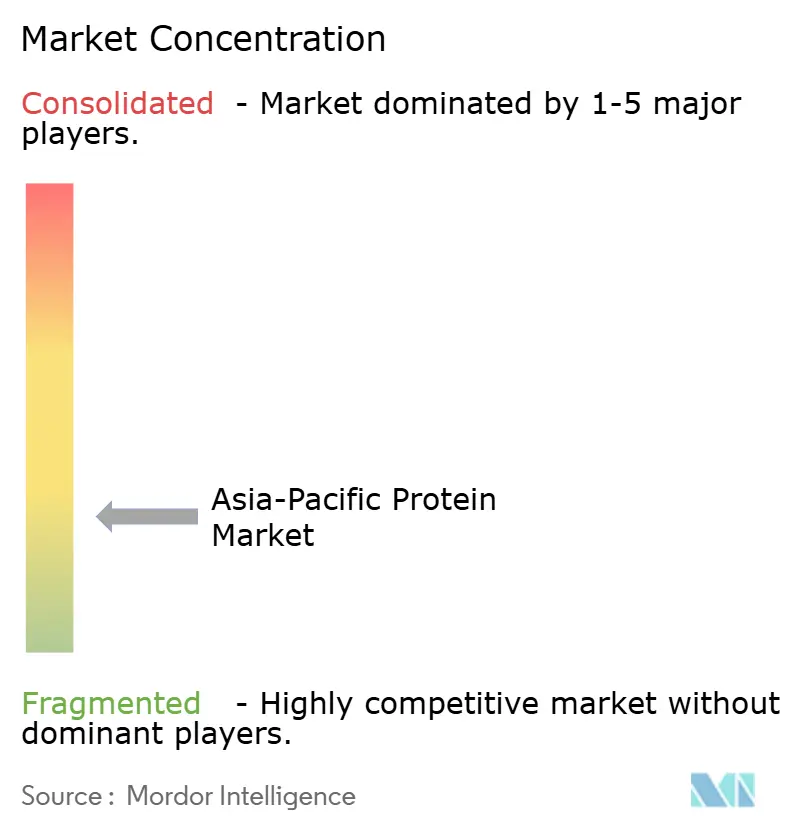

In the Asia-Pacific protein market, fragmentation is moderate. While multinational dairy cooperatives like Fonterra, Glanbia, and FrieslandCampina dominate the whey and casein supply chains, they face margin compressions of up to 18% due to price competition from Eastern European processors. Leading the charge in plant-protein extraction are ADM, Ingredion, and Roquette. Notably, Roquette's recent 25,000 t expansion in pea protein gives it a sharper edge in dairy-alternative formulations. In a strategic move, Wilmar International utilizes its integrated crushing operations in Indonesia and Malaysia to provide cost-effective soy concentrates, catering to regional fortification programs. Meanwhile, venture-backed disruptors such as Nutrition Technologies, Corbion, and CJ CheilJedang are making strides in scaling microbial and insect proteins, positioning themselves as buffers against agricultural volatility.

Patent activity is buzzing around enzymatic hydrolysis and AI-driven fermentation. In 2024-25, Arla Foods Ingredients secured three patents focused on mitigating bitterness in whey-hydrolysate beverages. These patents aim to enhance the sensory profile of whey-based products, making them more appealing to consumers. On another front, CJ CheilJedang's innovative real-time nutrient-dosing algorithm boasts an impressive 42% energy savings for every kilogram of microbial protein produced. This breakthrough not only reduces production costs but also aligns with sustainability goals by minimizing energy consumption.

Sports nutrition stands out as the most fiercely contested domain. Capitalizing on a USD 45 million Series D funding, India's MuscleBlaze has swiftly established four same-day-delivery warehouses, enabling them to undercut global brands by as much as 25% in online pricing. This aggressive pricing strategy, combined with improved logistics, allows MuscleBlaze to capture a significant share of the growing sports nutrition market in India. Emerging as lucrative opportunities are niches like 'beauty-from-within' collagen, insect protein tailored for aquaculture feed, and algae isolates catering to elderly nutrition. Early entrants in these segments can command price premiums until the market stabilizes and margins normalize. These white-space opportunities are driven by evolving consumer preferences, with collagen gaining traction for its skin and health benefits, insect protein offering a sustainable solution for aquaculture, and algae isolates addressing the specific nutritional needs of aging populations.

Asia-Pacific Protein Industry Leaders

Archer Daniels Midland Company

Darling Ingredients Inc.

Fonterra Co-operative Group Limited

International Flavors & Fragrances, Inc.

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Fonterra, targeting Asian sports-nutrition customers, invested AUD 65 million (USD 43 million) to boost its Stanhope, Victoria site with an additional 12,000 t of native whey-isolate capacity. This investment aligns with the growing demand for high-quality protein ingredients in the Asian market, particularly within the sports-nutrition segment.

- September 2024: Fonterra has opened its sixth application centre in china which enables the rapid launch of innovative product applications in response to market trends and local customers' needs.

- August 2024: Global dairy co-operative Fonterra and natural ingredient manufacturer Superbrewed Food have teamed up to boost sustainable food production. The partnership combines Superbrewed’s biomass protein platform with Fonterra’s dairy processing, ingredients, and application expertise to develop additional nutrient-rich, functional biomass protein.

- May 2024: Nitta Gelatin India Limited (NGIL), a collaboration between Nitta Gelatin of Japan and the Kerala State Industrial Development Corporation, initiated its collagen peptide expansion project at its Kakkanad facility. The project involves an investment of INR 200 crore.

Asia-Pacific Protein Market Report Scope

Proteins refer to substances derived from natural sources (animal, plant, or microbial) that have been isolated or concentrated through processing to be used as additives in other products. The scope of the report includes segmentation by source, form, application, and geography. By source, the market is segmented into animal protein, microbial protein, and plant protein. Based on the form, the market is segmented into concentrates, isolates, hydrolysates, and other forms. Based on the end user, the market is segmented into animal feed, food and beverages, personal care and cosmetics, supplements, baby food and infant formula, elderly nutrition and medical nutrition, and sports/performance. Also, the report delves into major economies across the region, providing a detailed analysis on India, China, Australia, Japan, Indonesia, Malaysia, South Korea, Thailand, Vietnam, and the rest ofthe Asia-Pacific. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

By Source

| Animal Protein | Casein and Caseinates |

| Collagen | |

| Egg Protein | |

| Gelatin | |

| Insect Protein | |

| Milk Protein | |

| Whey Protein | |

| Other Animal Proteins | |

| Microbial Protein | Algae Protein |

| Mycoprotein | |

| Plant Protein | Hemp Protein |

| Pea Protein | |

| Potato Protein | |

| Rice Protein | |

| Soy Protein | |

| Wheat Protein | |

| Other Plant Proteins |

Form

| Concentrates |

| Isolates |

| Hydrolysates |

| Other Forms |

End User

| Animal Feed | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Alternative Products | |

| Meat/Poultry/Seafood and Meat Alternative Products | |

| RTE/RTC Food Products | |

| Snacks | |

| Personal Care and Cosmetics | |

| Supplements | |

| Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | |

| Sport/Performance Nutrition |

Country

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| South Korea |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Source | Animal Protein | Casein and Caseinates |

| Collagen | ||

| Egg Protein | ||

| Gelatin | ||

| Insect Protein | ||

| Milk Protein | ||

| Whey Protein | ||

| Other Animal Proteins | ||

| Microbial Protein | Algae Protein | |

| Mycoprotein | ||

| Plant Protein | Hemp Protein | |

| Pea Protein | ||

| Potato Protein | ||

| Rice Protein | ||

| Soy Protein | ||

| Wheat Protein | ||

| Other Plant Proteins | ||

| Form | Concentrates | |

| Isolates | ||

| Hydrolysates | ||

| Other Forms | ||

| End User | Animal Feed | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternative Products | ||

| Meat/Poultry/Seafood and Meat Alternative Products | ||

| RTE/RTC Food Products | ||

| Snacks | ||

| Personal Care and Cosmetics | ||

| Supplements | ||

| Baby Food and Infant Formula | ||

| Elderly Nutrition and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

| Country | Australia | |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms