Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

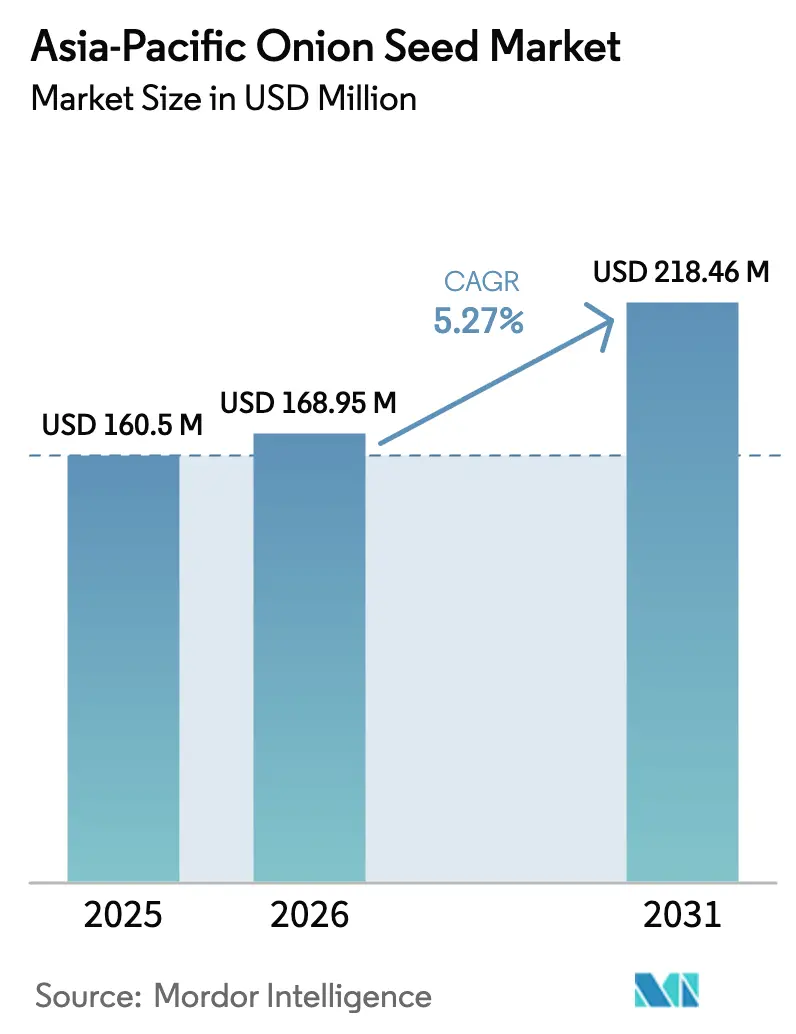

| Base Year Market Size (2025) | USD 160.5 Million |

| Market Size (2026) | USD 168.95 Million |

| Market Size (2031) | USD 218.46 Million |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

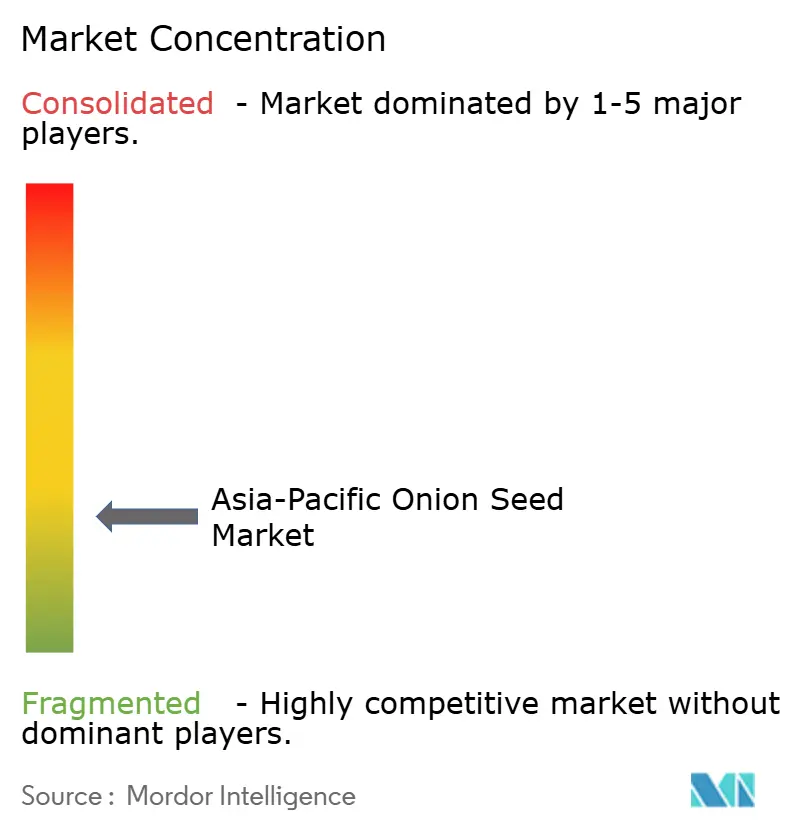

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Onion Seed Market Analysis by Mordor Intelligence

The Asia-Pacific onion seed market size was valued at USD 160.5 million in 2025 and estimated to grow from USD 168.95 million in 2026 to reach USD 218.46 million by 2031, at a CAGR of 5.27% during the forecast period (2026-2031). The current expansion cycle reflects rapid hybridization, a widening protected-cultivation footprint, and farmer incentives that tilt cost-benefit equations in favor of scientifically bred seed. Key value drivers include sustained public subsidies for certified seed, higher seed replacement ratios as triple-cropping systems proliferate, and on-farm trials demonstrating 20-30% yield premiums. Competitive strategies increasingly revolve around proprietary germplasm licensing, accelerated breeding timelines, and seed coating innovations that safeguard germination during erratic monsoon windows. Simultaneously, downstream processors are standardizing dry-matter and pungency specifications, incentivizing growers to adopt uniform, storage-stable cultivars that command price uplifts.

Key Report Takeaways

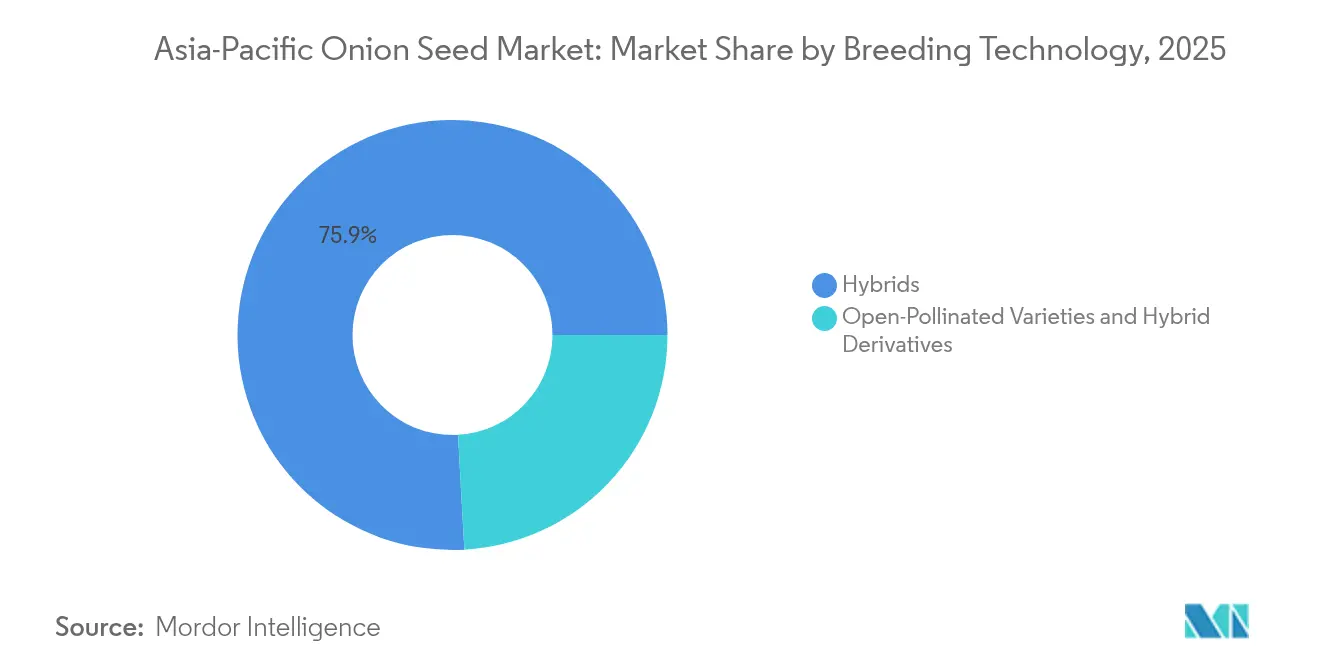

- By breeding technology, hybrids captured 75.88% of the Asia-Pacific onion seed market share in 2025, while open-pollinated varieties and hybrid derivatives are projected to deliver a 5.62% CAGR through 2031.

- By country, India led with 30.15% revenue share of the Asia-Pacific onion seed market size in 2025, while Bangladesh is expected to post the fastest growth at 6.74% CAGR between 2026 and 2031.

- By company ownership, the top five suppliers together held a 33.85% share of the Asia-Pacific onion seed market size in 2025, indicating scope for future consolidation among technology-focused entrants.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Onion Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of hybrid onion seeds for higher yields | +1.2% | India, China, Thailand, and Vietnam | Medium term (2-4 years) |

| Government subsidies for vegetable seed production in Asia-Pacific | +0.8% | Bangladesh, India, Nepal, and Myanmar | Short term (≤ 2 years) |

| Growing demand for processed onion products | +0.7% | China, India, Indonesia, and Philippines | Long term (≥ 4 years) |

| Expansion of protected cultivation | +0.9% | Japan, South Korea, China, and Thailand | Medium term (2-4 years) |

| Shift toward short-day varieties enabling triple-cropping | +0.6% | Bangladesh, Myanmar, Vietnam, and Thailand | Long term (≥ 4 years) |

| On-farm use of seed-coating polymers improving germination | +0.5% | Global, with early gains in India, China, and Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising adoption of hybrid onion seeds for higher yields

Hybrid penetration continues to climb because growers observe consistent 20–30% yield lifts over open-pollinated checks, documented in Bangladesh field trials that recorded bulb weights 1.6–1.8 times higher under optimal agronomy. The yield upside translates into stronger gross margins in land-constrained economies such as Japan and South Korea, where intensive systems require proven seed performance. Companies are responding with climate-resilient hybrids carrying heat and drought tolerance genes, a trait set that helps stabilize returns under rainfall variability. As distribution networks mature, the willingness of smallholders to pay premium seed prices is expected to rise, reinforcing hybrid market dominance.

Government subsidies for vegetable seed production in Asia-Pacific

Targeted subsidy frameworks covering 30–50% of certified seed costs are closing affordability gaps for smallholders in Bangladesh, India, Nepal, and Myanmar. Bangladesh’s policy response to a domestic seed deficit of 750 metric tons has already sparked local multiplication ventures that shorten supply chains and boost on-time availability. Nepal’s harmonized seed legislation under international treaties further lowers entry barriers for joint-venture breeding programs, incentivizing private investment. Collectively, these interventions underpin a structurally larger demand base for branded, quality-assured seed.

Shift toward short-day varieties enabling triple-cropping

Farmers in Bangladesh, Myanmar, Vietnam, and Thailand increasingly prefer short-day hybrids that mature within 90–100 days, freeing land for two additional rotations of cash crops. Triple-cropping unlocks cumulative income gains, making hybrid seed economics compelling despite higher up-front costs. Extension services demonstrate scheduling calendars that coordinate planting windows with market price peaks, elevating profitability and reinforcing variety stickiness.

Expansion of protected cultivation

Polytunnel and net-house acreage is expanding in Japan, South Korea, China, and Thailand, enabling year-round bulb production and specialized seed-to-seed programs. Furrow-bottom seeding methods tested in Japan highlight emergence gains under controlled microclimates. Seed producers leverage such environments to improve flowering synchronization and genetic purity, boosting seed yields and profitability. Cultivar portfolios optimized for protected settings fetch price premiums that offset higher infrastructure costs, reinforcing a virtuous cycle of technology adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of hybrid seeds for smallholders | -0.9% | Bangladesh, Myanmar, Vietnam, and Indonesia | Short term (≤ 2 years) |

| Seed-borne diseases and limited cold-chain storage | -0.7% | Tropical Asia-Pacific, Indonesia, and Philippines | Medium term (2-4 years) |

| Counterfeit seeds in fragmented informal channels | -0.5% | India, Bangladesh, Myanmar, and Pakistan | Long term (≥ 4 years) |

| Climate-induced bolting incidents reducing seed supply | -0.6% | China, India, Bangladesh, and Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of hybrid seeds for smallholders

Hybrid packs often sell for 3–5 times the price of open-pollinated alternatives, placing strain on cash-flow-dependent growers. Studies in Bangladesh underline that seedling costs remain a primary cultivation bottleneck, pushing farmers toward cheaper, uncertified stock.[2]Source: Bangladesh Agricultural Research Institute, “Purple Blotch Disease Management in Onion,” bari.gov.bd The inability to recycle hybrid seed forces annual purchases, amplifying perceived risk. Until financing tools such as microcredit and cooperative procurement mature, cost concerns will temper adoption speed, particularly in fragmented inland districts.

Seed-borne diseases and limited cold-chain storage

Tropical humidity fosters fungal pathogens that cut viability during transport and on-farm storage. Purple blotch outbreaks traced back to infected seed lots have inflicted yield penalties exceeding 20% in Bangladesh trials. Rural cold-chain gaps compel suppliers to rely on costly moisture-barrier packaging, escalating retail prices. Quality lapses erode farmer confidence in branded products, hampering broader market development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Drive Premium Market Expansion

Hybrids maintained a commanding 75.88% Asia-Pacific onion seed market share in 2025, propelled by evident yield, bulb uniformity, and shelf-life advantages. Large commercial estates and contract growers gravitate toward proprietary hybrids that satisfy processor-mandated specifications, elevating average selling prices and margins for seed companies. The segment benefits from sustained R&D outlays in marker-assisted selection and doubled-haploid platforms, shortening cultivar development cycles and fortifying intellectual-property moats under OECD seed-certification guardrails. Concurrently, open-pollinated varieties and hybrid derivatives chart a 5.62% CAGR, catering to price-sensitive smallholders who value incremental performance without annual royalty obligations.

The competitive narrative within hybrids is marked by increasingly specialized portfolios such as intermediate-day types that enable two or three rotations per year. Companies are also layering seed enhancements into premium packs, embedding polymer coatings and micronutrient priming to safeguard emergence. As climate volatility heightens, tolerance stacks for heat, drought, and purple blotch will shape cultivar differentiation. Improved open-pollinated lines will likely co-exist, meeting adoption thresholds in subsidy-supported distribution channels and offering a stepping-stone toward full hybrid adoption. Overall, hybrids will keep anchoring revenue, while derivative segments expand the total addressable market.

Geography Analysis

India maintains its position as the largest market with a 30.15% share in 2025. India spans temperate to tropical belts, supporting varietal niches from long-day types in Maharashtra to intermediate-day cultivars in Karnataka. The Asia-Pacific onion seed market size attributed to India is projected to widen as state governments continue 50% cost-sharing for hybrid seed packs, improving affordability among marginal growers. Market liberalization under the Seeds Act and an expanding roster of accredited certification labs facilitate private breeder participation, fostering a vibrant yet competitive playing field. Bangladesh emerges as the fastest-growing market at 6.74% CAGR for 2026-2031. Bangladesh’s acceleration stems from acute self-sufficiency ambitions. With an annual demand of 900 metric tons against 150 metric tons of domestic seed output, the government mobilizes farmer-producer organizations to manage decentralized seed villages.

Financing support through subsidized credit plus on-field demonstrations encourages adoption of purple-blotch-resistant hybrids, narrowing yield gaps and import bills. This scalable model converts base-of-pyramid growers into reliable, repeat customers for branded suppliers. China operates sophisticated state and private breeding hubs, benefiting from the seven-day germplasm-clearance regime in Hainan that slashes bureaucratic lead times. Domestic seed majors collaborate with provincial research stations to deliver heat-stress-tolerant lines tailored to northern plains and Yunnan highlands. Cross-licensing arrangements with multinational firms funnel advanced genetics into local pipelines, positioning China both as a demand sink and an export platform. Southeast Asian economies, including Thailand, Vietnam, and Indonesia, a tapping expanding food-service channels that require a consistent supply. Protected-cultivation grants and mechanized sowing initiatives, such as Thailand’s furrow-bottom seeding trials, also help with the adoption of precision-bred material. Yet informal retail points still command the majority of seed turnover, emphasizing the need for certification enforcement and branded awareness campaigns.

Competitive Landscape

The Asia-Pacific onion seed market shows moderate fragmentation; the leading five suppliers occupy 34.4% combined share, leaving headroom for consolidation. Bayer AG holds a significant market share, leveraging century-old breeding credentials and a diversified hybrid lineup optimized for both open-field and greenhouse systems. Groupe Limagrain maintains a strong position, underpinned by globally coordinated R&D funnels and robust distribution alliances. Sakata Seed Corporation, BASF, and Nong Woo Bio complete the top tier, each focusing on differentiated trait stacks and geographic expansion.

Strategic positioning hinges on intellectual-property protection and access to proprietary germplasm. Syngenta’s March 2024 arrangement with Emerald Seed Company grants exclusive global rights to elite onion genetics, fast-tracking hybrid releases adapted to Asia’s short-day production windows. Regional challengers exploit white-space territories such as Bangladesh’s riverine delta and Myanmar’s Central Dry Zone by offering cost-attuned open-pollinated upgrades if subsidy budgets falter. Technology bundling, pairing polymer coatings with micronutrient primers, is becoming a standard premiumization tactic that drives brand loyalty.

Climate adaptation intensifies the innovation race. Breeders allocate rising R&D shares toward heat-stable male-sterile lines, bolting resistance, and integrated pest-management compatibility. Meanwhile, regulatory harmonization under ASEAN biological control guidelines is expected to simplify cross-border seed flows, bolstering regional supply continuity. Over the medium term, merger prospects between mid-tier players appear likely as economies of scale in breeding, processing, and distribution become decisive for cost-competitive growth.

Asia-Pacific Onion Seed Industry Leaders

BASF

Sakata Seed Corporation

Bayer AG

Nong Woo Bio

Groupe Limagrain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Crystal Crop Protection's acquisition of IB Seeds expanded its vegetable and flower seed portfolio, with a focus on onion seeds. The acquisition strengthened Crystal's breeding capabilities and increased its market presence in India's horticulture segment, particularly for onion hybrids.

- March 2024: Syngenta Vegetable Seeds formed an exclusive licensing agreement with Emerald Seed Company to expand its onion seed portfolio. The partnership aims to increase global availability of high-quality onion genetics, with a focus on the Asia-Pacific region.

Asia-Pacific Onion Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Open Field are covered as segments by Cultivation Mechanism. Australia, Bangladesh, China, India, Indonesia, Japan, Myanmar, Pakistan, Philippines, Thailand, Vietnam are covered as segments by Country.Breeding Technology

| Hybrids |

| Open-Pollinated Varieties and Hybrid Derivatives |

Country

| Australia |

| Bangladesh |

| China |

| India |

| Indonesia |

| Japan |

| Myanmar |

| Pakistan |

| Philippines |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| Breeding Technology | Hybrids |

| Open-Pollinated Varieties and Hybrid Derivatives | |

| Country | Australia |

| Bangladesh | |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Myanmar | |

| Pakistan | |

| Philippines | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific |

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms