Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

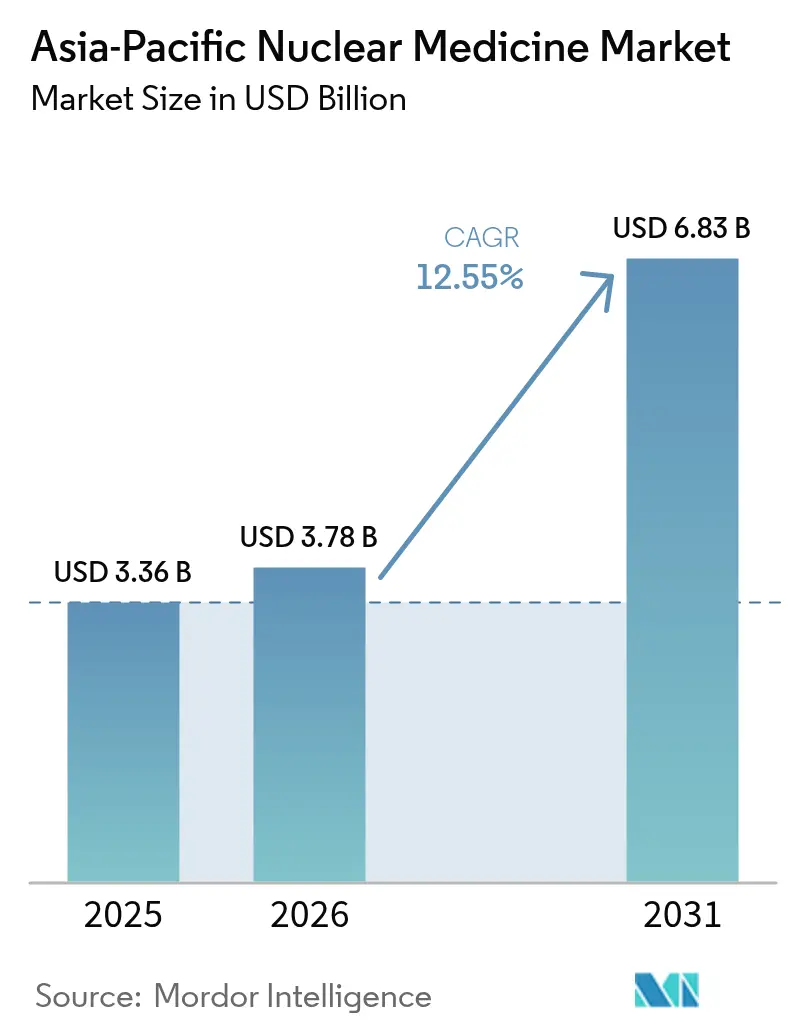

| Base Year Market Size (2025) | USD 3.36 Billion |

| Market Size (2026) | USD 3.78 Billion |

| Market Size (2031) | USD 6.83 Billion |

| Growth Rate (2026 - 2031) | 12.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Nuclear Medicine Market Analysis by Mordor Intelligence

The Asia-Pacific nuclear medicine market size was valued at USD 3.36 billion in 2025 and estimated to grow from USD 3.78 billion in 2026 to reach USD 6.83 billion by 2031, at a CAGR of 12.55% during the forecast period (2026-2031). Growth reflects the region’s decisive shift toward precision oncology and theranostics, backed by expanding hybrid imaging fleets, widening radiopharmaceutical pipelines, and steady public-sector investment in isotope production. China’s 1,000-plus nuclear medicine departments, India’s expanding network of 300 centers of excellence, and Australia’s early adoption of PSMA-targeted agents anchor this expansion. Clinical workloads are rising most sharply in oncology and cardiology, while supply-chain partnerships are easing access to short-lived isotopes. Continued regulatory harmonization is expected to lower approval timelines, enabling a broader roll-out of radioligand therapy programs across emerging economies.

Key Report Takeaways

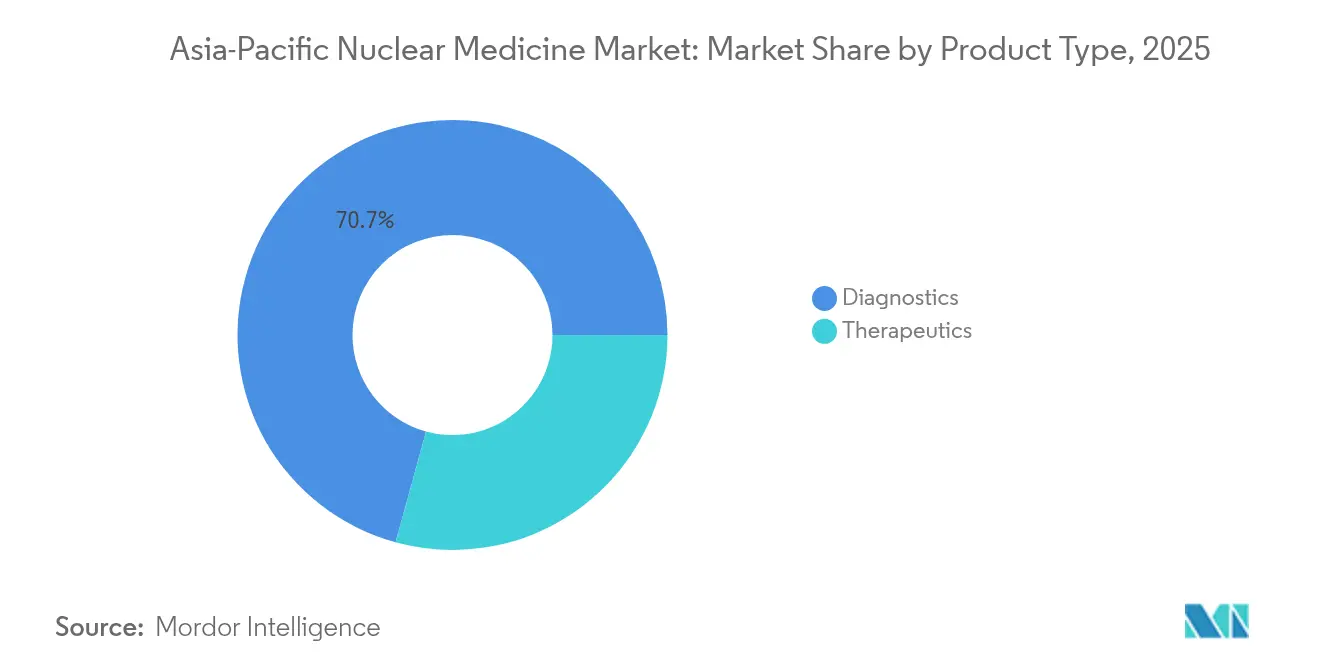

- By product type, diagnostics led with 70.74% of the Asia-Pacific nuclear medicine market share in 2025; therapeutics is projected to grow at a 17.02% CAGR through 2031.

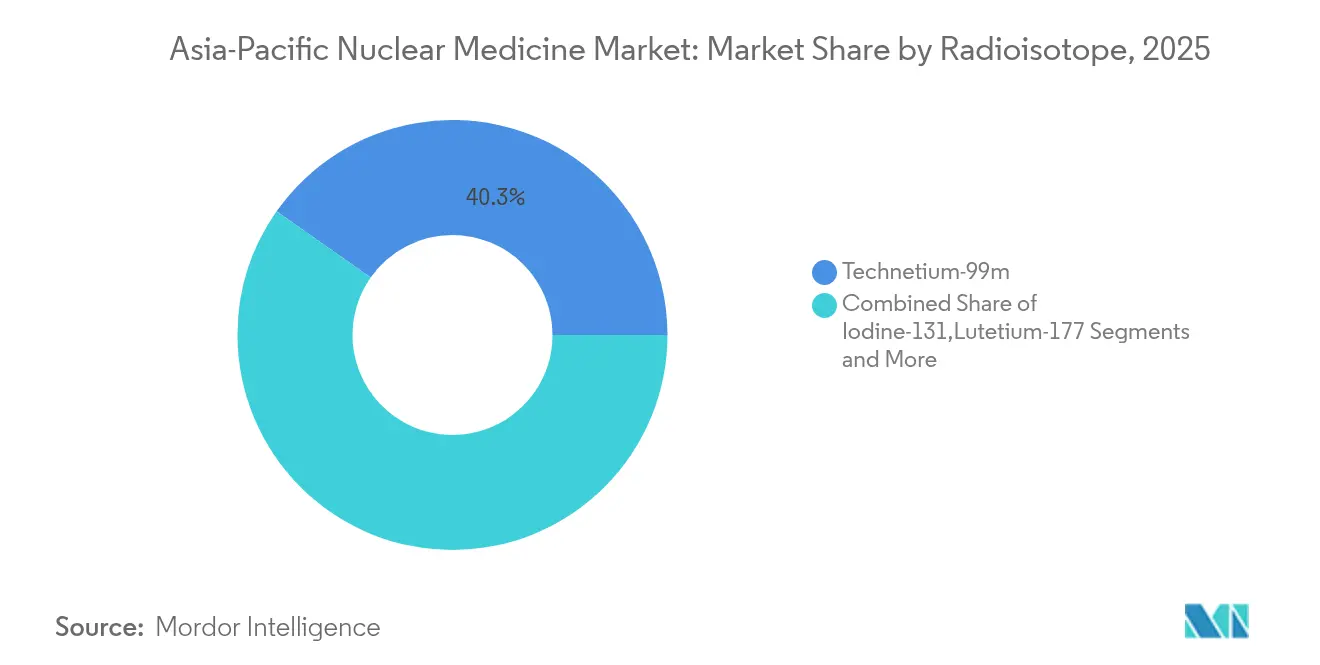

- By radioisotope, technetium-99m accounted for 40.25% of the Asia-Pacific nuclear medicine market size in 2025, while lutetium-177 is forecast to expand at a 11.95% CAGR to 2031.

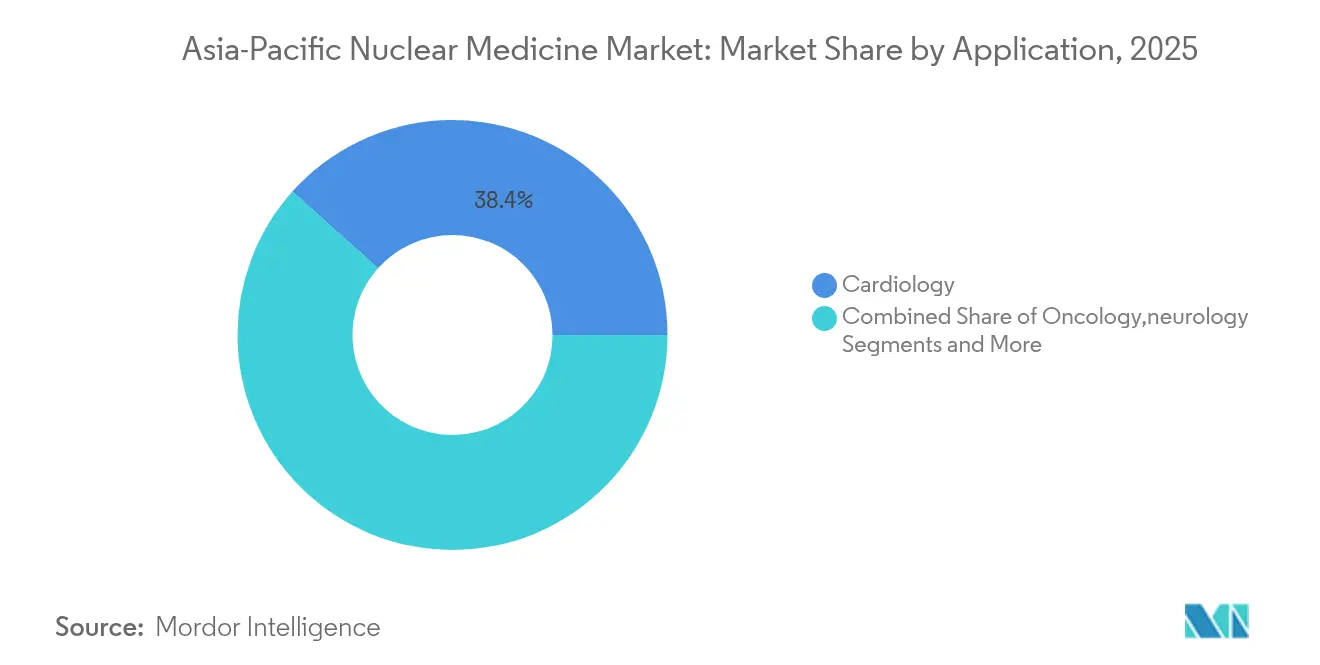

- By application, cardiology represented 38.37% of the Asia-Pacific nuclear medicine market share in 2025 and oncology applications are advancing at a 14.39% CAGR through 2031.

- By end user, hospitals held 56.74% share of the Asia-Pacific nuclear medicine market size in 2025; specialized radiopharmacies are growing at a 14.45% CAGR between 2026-2031.

- By geography, China commanded 29.12% of the Asia-Pacific nuclear medicine market in 2025, whereas India is expanding at a 13.75% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Asia-Pacific Nuclear Medicine Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden Of Cancer & Cardiovascular Diseases | +3.2% | Global, highest in East Asia and Southeast Asia | Long term (≥ 4 years) |

| Rising Adoption of Hybrid Imaging Technologies | +2.8% | China, Japan, Australia, South Korea | Medium term (2-4 years) |

| Government Initiatives and Healthcare Infrastructure Development | +2.1% | India, China, Philippines, Thailand | Long term (≥ 4 years) |

| Expansion of Molecular Imaging Applications and Personalized Medicines | +1.9% | Japan, Australia, Singapore, South Korea | Medium term (2-4 years) |

| Rising Awareness and Demand for Theranostics | +1.7% | Global, early adoption in developed APAC markets | Short term (≤ 2 years) |

| Initiatives taken by Market Players and Launch of Products | +1.0% | Global, concentrated in major markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Cancer and Cardiovascular Diseases

Asia accounts for 49.2% of global cancer cases and 56.1% of cancer deaths, with lung malignancies topping incidence tables in large populations such as China and Indonesia. The region also records pronounced cardiovascular disease prevalence, as East Asia reports 1,014.06 heart-failure patients per 100,000 population versus 389.97 per 100,000 in South Asia.[1]Jian Zhang, “Epidemiology and Burden of Heart Failure in Asia,” JACC: Asia, jacc.org These epidemiological patterns create sustained demand for both SPECT and PET procedures in oncology and cardiology. Ageing demographics in Japan and South Korea are intensifying oncologic caseloads that require early detection through nuclear imaging. High smoking rates—54.4% among Indonesian men and 41.5% among Chinese men—suggest a continued pipeline of pulmonary cancers that will rely on molecular imaging for staging and therapy monitoring. Consequently, the Asia-Pacific nuclear medicine market is positioned as a critical component of regional disease-management strategies.

Rising Adoption of Hybrid Imaging Technologies

Total-body PET/CT scanners installed at institutions such as Sun Yat-sen University Cancer Center have completed 30,000 examinations in three years, cutting radiation exposure and acquisition times.[2]Shuxian An, “Pathway to Approval of Innovative Radiopharmaceuticals in China,” Journal of Nuclear Medicine, jnm.snmjournals.orgUpright CT platforms launched at Keio University Hospital improve diagnostic confidence for musculoskeletal and respiratory assessments in elderly patients. SPECT systems are transitioning to semiconductor detectors that deliver higher spatial resolution and shorter scan windows. Artificial-intelligence algorithms embedded in these hybrid modalities enable automated lesion detection and quantitative analytics, which reduce reporting time and support remote reading in underserved locations. As procurement programs in China, Japan, and Australia emphasize whole-body scanners, the Asia-Pacific nuclear medicine market gains a technology refresh cycle that boosts procedure volumes and diagnostic accuracy.

Government Initiatives and Healthcare Infrastructure Development

India’s Bhabha Atomic Research Centre is expanding domestic isotope production while eLORA online portals accelerate facility licensing. China’s Mid- and Long-Term Development Plan (2021-2035) targets production capacity sufficient to treat 10 million patients annually by 2035. The Philippines opened a Nuclear Medicine Research and Innovation Center aimed at lowering PET scan costs and serving as a regional training hub.[3]Ma. Cristina Arayata, “Nuclear Med Facility to Lower Cost for Cancer Treatment,” Philippine News Agency, pna.gov.ph South Korea allocated KRW 300 billion to a small-modular-reactor complex in Gyeongju, paving the way for domestic actinium-225 production. These policy actions enlarge cyclotron fleets, improve workforce depth, and align reimbursement schedules, collectively lifting the Asia-Pacific nuclear medicine market over the long term.

Expansion of Molecular Imaging Applications and Personalized Medicines

Sixty percent of nuclear medicine procedures in Asia-Pacific are predicted to involve theranostic protocols within the next decade. Japan approved lutetium oxodotreotide in four year back, and clinical optimization now allows sharper image quality through refined collimator settings. Korean trials mapping FDG and PSMA uptake profiles enhance therapy selection for metastatic prostate cancer. Novel tracers such as 18F-FAPI-04 achieve higher standardized-uptake values for peritoneal metastasis compared to FDG, influencing chemotherapy planning in Chinese centers. These advances widen the clinical reach of radiopharmaceuticals beyond traditional oncology domains into fibrosis, inflammation, and infectious disease, further reinforcing the Asia-Pacific nuclear medicine market.

Restraints Impact Analysis of Asia-Pacific Nuclear Medicine Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX For Cyclotrons & Imaging Equipment | -2.3% | Emerging markets: India, Philippines, Thailand, Indonesia | Long term (≥ 4 years) |

| Complex Multi-Agency Isotope Transport Regulations | -1.8% | Global, particularly cross-border shipments in APAC | Medium term (2-4 years) |

| Short Half-Life Isotope Supply Chain Risk | -1.5% | Regional, affecting remote areas and smaller markets | Short term (≤ 2 years) |

| Shortage Of Certified Nuclear-Medicine Pharmacists Outside Tier-1 Cities | -1.2% | India, China, Southeast Asia secondary markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for Cyclotrons and Imaging Equipment

Emerging economies face budget constraints when acquiring PET/CT scanners that can cost USD 2-5 million, plus annual service contracts approaching USD 200,000. The Philippines, for example, operates only three cyclotrons, all in Manila, which inflates travel expenses for provincial patients. In India, stringent quality-assurance standards for PET systems escalate procurement timelines and compliance costs. Capital needs extend to radiation-shielded hot cells, Good Manufacturing Practice suites, and certified staff, pushing payback periods beyond five years in many public hospitals. Limited reimbursement policies often shift financial burden to patients, potentially delaying adoption of next-generation theranostics. As a result, the Asia-Pacific nuclear medicine market must rely on public-private partnerships and concessional financing to overcome infrastructure barriers.

Complex Multi-Agency Isotope Transport Regulations

Radiopharmaceuticals must satisfy pharmaceutical, nuclear-safety, and customs requirements, each managed by separate agencies in most Asia-Pacific nations. Documentation varies by country, causing routing delays that shorten the usable life of products such as fluorine-18. Alpha emitters face additional scrutiny because of higher radiotoxicity, requiring specialized packaging and escorts across international borders. Each regulatory checkpoint adds indirect costs that can raise final dose prices by up to 30% in small markets. Although the International Atomic Energy Agency promotes standard templates, adoption is uneven, leaving smaller suppliers at a disadvantage. This fragmentation dampens the growth potential of the Asia-Pacific nuclear medicine market until harmonized frameworks become operational.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Asia-Pacific Nuclear Medicine Market Segment Analysis

By Product Type:

Diagnostics Retain the Volume Advantage While Therapeutics AccelerateDiagnostics accounted for 70.74% of the Asia-Pacific nuclear medicine market in 2025, driven by well-established SPECT and PET applications in myocardial perfusion, tumor staging, and brain imaging. Multi-head gamma cameras now achieve higher count sensitivity, which shortens scan times and improves patient throughput. Cardiac stress protocols benefit from new solid-state detectors that lower radiation dose without compromising image quality. Hospitals across China and Japan have standardized PET/CT for oncology work-ups, creating consistent demand for technetium-99m and fluorine-18 doses. Procedure volumes are supported by public insurance schemes that reimburse both tracer and scanner time, stabilizing revenue for service providers.

Therapeutics, though smaller today, is rising at a 17.02% CAGR. Lutetium-177 dotatate gained approvals for neuroendocrine tumors and is rapidly expanding into prostate cancer therapy through Pluvicto roll-outs. Alpha emitters such as actinium-225 promise higher linear-energy transfer, enhancing cell kill in micro-metastatic disease. South Korea’s plan to initiate domestic actinium-225 production by mid-2025 will shorten supply lines and lower dose costs. Clinical guidelines are evolving to include radioligand therapy earlier in treatment algorithms, especially for prostate and thyroid malignancies. Continuous data generation from regional registries strengthens payor confidence and accelerates reimbursement, expanding the Asia-Pacific nuclear medicine industry footprint in therapeutics.

By Radioisotope:

Technetium-99m Dominates, Lutetium-177 Leads GrowthTechnetium-99m retained 40.25% share of the Asia-Pacific nuclear medicine market size in 2025. Its 6-hour half-life and favorable photon energy underpin its ubiquity in bone, renal, and myocardial imaging. Nevertheless, reliance on ageing reactors for molybdenum-99 production exposes the region to periodic shortages, prompting countries such as Australia and Japan to evaluate accelerator-based supply solutions. Digital logistics platforms in China now track generator shipments in real time, mitigating stock-out risk for remote clinics.

Lutetium-177, posting a 11.95% CAGR, anchors the therapeutic pipeline through versatile beta-emission profiles that are suitable for both imaging and therapy. SHINE-Primo Biotech agreements extend non-carrier-added lutetium-177 access to Taiwan, Japan, and Singapore, which collectively support more than 25 clinical trials. The isotope’s 6.7-day half-life facilitates regional shipping without excessive decay loss, addressing a key distribution challenge for shorter-lived agents. Fluorine-18 continues to expand in oncology imaging, while gallium-68-based tracers gain traction in infection and inflammation mapping. Early research on terbium-161 and thorium-228 signals an impending diversification of therapeutic isotopes, broadening revenue streams for the Asia-Pacific nuclear medicine market.

By Application:

Cardiology Commands Volume, Oncology Drives ExpansionCardiology represented 38.37% of the Asia-Pacific nuclear medicine market in 2025 as heart-failure prevalence and ischemic-heart-disease screening programs sustain high SPECT activity. Stress-rest imaging protocols now average 12 minutes per phase using high-efficiency cameras, improving patient comfort. Hybrid PET/CT perfusion is gaining acceptance for multivessel coronary disease assessment, particularly in Japan and Australia. Hospitals are integrating AI-based motion-correction software that reduces artifacts, raising diagnostic confidence in obese or arrhythmic patients.

Oncology is the fastest-growing clinical area, expanding at 14.39% CAGR as Asia’s cancer burden surges. PSMA-PET has become standard for biochemical-recurrence work-ups in prostate cancer, tipping surgical decision-making toward targeted approaches. Total-body PET produces dynamic whole-body pharmacokinetic maps that optimize radionuclide dosimetry, a capability being exploited in Chinese phase III trials of lutetium-177 therapies. Novel FAPI agents identify desmoplastic reaction in pancreatic and colorectal tumors, opening windows for anti-fibroblast strategies. As imaging transitions from simple lesion detection to treatment response assessment, the Asia-Pacific nuclear medicine market embeds itself deeper in oncology care pathways.

By End User:

Hospitals Dominate, Radiopharmacies Gain MomentumHospitals captured 56.74% of the Asia-Pacific nuclear medicine market share in 2025. Academic medical centers in Beijing, Seoul, and Melbourne combine nuclear medicine, surgery, and medical oncology teams under one roof, fostering multidisciplinary decision-making. These institutions are also the primary sites for clinical trials, attracting industry partnerships and technology donations. Many teaching hospitals run in-house cyclotrons that supply both patient care and research needs, ensuring tracer availability even during global shortages.

Specialized radiopharmacies are growing at 14.45% CAGR as theranostic procedures require just-in-time synthesis and rigorous GMP documentation. Contract-manufacturing organizations in Singapore and Sydney are scaling isotope distribution to satellite clinics that lack on-site production. Business models often bundle tracer supply, quality-control analytics, and regulatory support, reducing administrative overhead for smaller hospitals. In India and Indonesia, new radiopharmacies are being co-located with private diagnostic imaging chains, broadening patient access while diversifying revenue for investors. Academic institutes and specialty clinics play crucial roles in early technology adoption yet face staffing shortages that limit geographic reach.

Geography Analysis

China Nuclear Medicine Market

China accounted for 29.12% of the Asia-Pacific nuclear medicine market in 2025, supported by more than 1 million PET/CT scans a year and 12,000 trained professionals across 1,000 departments. The National Medical Products Administration has cleared over 40 radiopharmaceuticals, streamlining clinical adoption and shortening time-to-market for local manufacturers. Integrated AI platforms that link imaging, pathology, and genomic data are being piloted at top cancer centers, positioning China for leadership in precision oncology.

India Nuclear Medicine Market

India is advancing at a 13.75% CAGR, fueled by 300 centers of excellence, government support for cyclotron installation, and private-sector collaborations that accelerate tracer distribution. Quality-control frameworks enforced by the Atomic Energy Regulatory Board are enhancing patient safety, while public-insurance expansions widen procedure reimbursement. These catalysts solidify India as a key growth engine for the Asia-Pacific nuclear medicine market.

APAC Nuclear Medicine Market

Australia and South Korea serve as innovation hubs. Australia’s Therapeutic Goods Administration leads regional approvals of advanced radioligand therapies, and domestic GMP sites now manufacture both FDG and lutetium-177 doses for domestic and export markets. South Korea’s Yonsei Cancer Center treated over 200 prostate-cancer patients with heavy-ion therapy in its first operational year, and actinium-225 production is slated for mid-2025. Emerging economies such as the Philippines and Thailand are expanding isotope supply chains through new cyclotrons outside capital cities, lowering patient travel costs and improving procedure uptake.

Competitive Landscape

The Asia-Pacific nuclear medicine market is consolidating as multinational device and isotope suppliers seek local manufacturing control. GE Healthcare’s USD 183 million acquisition of Nihon Medi-Physics grants full access to a 28.2 billion-JPY radiopharmaceutical portfolio and expands tracer supply to more than 500 Japanese hospitals. Siemens Healthineers and Philips are embedding artificial-intelligence analytics into hybrid scanners that automate lesion contouring, while Canon Medical Systems markets upright CT units for senior care facilities.

White-space opportunities revolve around alpha-emitting therapies and underserved geographies. Thor Medical’s thorium-228 supply agreement with AdvanCell underpins a pipeline of targeted alpha treatments for hematologic and solid tumors. Clarity Pharmaceuticals is advancing copper-based theranostics with extended half-lives that simplify logistics for remote clinics. SHINE Technologies scales lutetium-177 output through a new partnership that covers Taiwan, Japan, South Korea, and Singapore, ensuring consistent isotope flow for clinical trials and commercial programs.

Competitive differentiation now centers on integrated service offerings. Vendors bundle cyclotron leasing, tracer supply, AI-enabled imaging software, and clinical-training modules to secure multi-year contracts with hospital networks. Intellectual-property filings for new ligands and chelators are rising, with more than 60 Asia-Pacific applications recorded in 2024 alone. As domestic manufacturers ramp capacity, price competition is expected to intensify, benefiting payors and widening access across the Asia-Pacific nuclear medicine industry.

Asia-Pacific Nuclear Medicine Industry Leaders

GE Healthcare

Seimens Healthineers

Curium Pharma

Telix Pharmaceuticals

China Isotope & Radiation Corp. (CIRC)

- *Disclaimer: Major Players sorted in no particular order

Asia-Pacific Nuclear Medicine Market Companies Covered in this Report

- GE Healthcare

- Siemens Healthineers

- Koninklijke Philips

- Canon

- Curium Pharma

- Telix Pharmaceuticals

- Bracco Imaging S.p.A.

- Nordion

- NTP Radioisotopes SOC Ltd.

- China Isotope & Radiation Corp. (CIRC)

- Advanced Accelerator Applications (Novartis)

- Jubilant Radiopharma

- AdvanCell (Australia)

- Shenzhen Mindray Bio-Medical

- Institute of Nuclear Energy Research (Taiwan)

- Jiangsu Huayi Technology

- Zhejiang Jiutai New Drug

- Cyclopharma Laboratories

Recent Industry Developments in Asia-Pacific Nuclear Medicine Market

- March 2025: GE Healthcare completed the acquisition of Nihon Medi-Physics, consolidating its leadership in Japanese molecular imaging.

- January 2025: SHINE Technologies and Primo Biotech signed an exclusive distribution accord for non-carrier-added lutetium-177 across Taiwan, Japan, South Korea, and Singapore.

- December 2024: Thor Medical and AdvanCell entered a five-year thorium-228 supply agreement to support alpha-therapy programs in Australia.

- July 2024: Australia’s TGA approved Pluvicto for PSMA-positive metastatic castration-resistant prostate cancer under enhanced post-marketing surveillance.

Asia-Pacific Nuclear Medicine Market Report Scope and Research Methodology

Market Definition and Coverage

According to Mordor Intelligence, the Asia-Pacific nuclear medicine market covers diagnostic and therapeutic radio-pharmaceuticals that deliver or detect gamma, beta, or alpha emissions inside patients for imaging or targeted therapy. The study values only commercial sales of ready-to-use isotopes and labeled compounds supplied to hospitals, specialized pharmacies, and imaging centers across China, Japan, India, Australia, South Korea, and the rest of the region.

Scope exclusion: Equipment sales, radio-isotope production reactors, and stable isotopes sold for research are outside our baseline.

Segments Covered in This Report

- By Product

- Diagnostics

- SPECT

- PET

- Therapeutics

- Alpha Emitters

- Beta Emitters

- Brachytherapy Isotopes

- Diagnostics

- By Radioisotope

- Technetium-99m

- Iodine-131

- Fluorine-18

- Lutetium-177

- Others

- By Application

- Oncology

- Cardiology

- Neurology

- Endocrinology

- Other Applications

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Academic & Research Institutes

- Specialty Clinics

- Geography

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Primary Research

To verify secondary signals, Mordor analysts interview radiopharmacists, oncology clinicians, and isotope distributors in China, India, Japan, and Australia. Discussions probe average selling prices, patient throughput, and likely uptake of lutetium-177 and fluorine-18 agents, helping us refine utilization rates and future mix shifts.

Desk Research

Our analysts first compile publicly available fundamentals. Government bodies such as the Chinese National Health Commission, the Pharmaceuticals and Medical Devices Agency of Japan, India's Atomic Energy Regulatory Board, and the Australian Radiation Protection and Nuclear Safety Agency provide counts of licensed nuclear medicine sites, installed PET and SPECT units, and procedural volumes. Trade groups like the World Nuclear Association, WNA Asia chapter, and the Society of Nuclear Medicine and Molecular Imaging release whitepapers on isotope supply and clinical adoption. Company 10-Ks, IPO filings, customs shipment records, and Factiva news help us trace pricing shifts and new capacity announcements. We also reference D&B Hoovers for audited financials of regional radiopharmacy chains. This list is illustrative; many additional documents inform desk work.

Market-Sizing & Forecasting

We construct a top-down model that starts with regional procedure counts and dose-per-scan norms, which are then multiplied by blended ASPs gathered above. Supplier roll-ups of technetium generators and sampled hospital purchase orders act as a selective bottom-up check before final adjustment. Key variables tracked include PET penetration in oncology, cardiology prevalence, generator replacement cycles, government reimbursement ceilings, and isotope export-import balances. A multivariate regression with PET install growth, cardiovascular disease incidence, and average therapy doses drives the 2025-2030 forecast. Any data gaps, for instance in smaller ASEAN markets, are bridged through proportional scaling against verified imaging equipment bases.

Data Validation & Update Cycle

Outputs pass a two-tier analyst review, variance tests versus external benchmarks, and senior sign-off. The dataset refreshes each year, with interim updates triggered by material events such as reactor outages or new reimbursement codes.

How Mordor Intelligence's Asia-Pacific Nuclear Medicine Market Size Compares to Other Published Estimates

Published estimates often diverge because firms mix equipment with isotopes, use differing ASP ladders, or freeze exchange rates early.

Key gap drivers include scope drift toward imaging hardware, aggressive dose-growth assumptions, and infrequent model refreshes that miss recent supply expansions or currency swings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.36 B (2025) | Mordor Intelligence | - |

| USD 4.06 B (2024) | Regional Consultancy A | Includes cameras and generators, single-year FX fix |

| USD 2.30 B (2025) | Trade Journal B | Excludes therapeutics, relies on hospital survey sample only |

The comparison shows that Mordor's disciplined scope, yearly currency recalibration, and dual-track validation yield a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current size of the Asia-Pacific nuclear medicine market?

The Asia-Pacific nuclear medicine market stands at USD 3.78 billion in 2026.

How fast is the Asia-Pacific nuclear medicine market expected to grow?

The market is forecast to expand to USD 6.83 billion by 2031, registering a 12.55% CAGR.

Which country leads the Asia-Pacific nuclear medicine market?

China holds 29.12% of regional revenue, supported by more than 1,000 nuclear-medicine departments and 1 million PET/CT scans each year.

Which radioisotope is growing the fastest in Asia-Pacific?

Lutetium-177 is the fastest-rising isotope, advancing at a 11.95% CAGR through 2031 due to expanding radioligand therapy approvals.

What segment is expanding quickest within the Asia-Pacific nuclear medicine market?

Therapeutics is growing the fastest, posting a 17.02% CAGR as radioligand therapies gain reimbursement and clinical-guideline support.

Page last updated on: