Geotextile Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

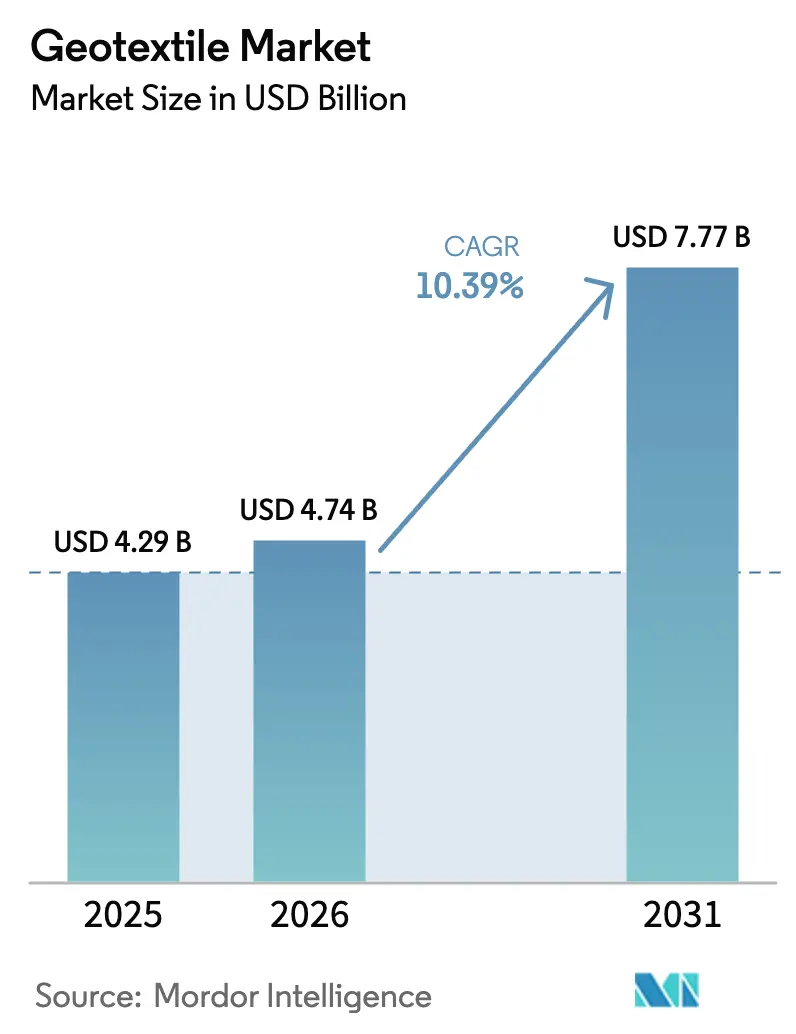

| Market Size (2026) | USD 4.74 Billion |

| Market Size (2031) | USD 7.77 Billion |

| Growth Rate (2026 - 2031) | 10.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Geotextile Market Analysis by Mordor Intelligence

The Geotextile Market size is expected to grow from USD 4.29 billion in 2025 to USD 4.74 billion in 2026 and is forecast to reach USD 7.77 billion by 2031 at 10.39% CAGR over 2026-2031. Growth rests on highway and landfill regulations that reward engineered separation and drainage fabrics, while competitive pricing for polypropylene continues to outweigh sustainability preferences. Procurement norms now emphasize verified performance, prompting suppliers to integrate design software, bio-based polymers, and digital monitoring into their bids to secure long-term contracts. Surging demand from the U.S. Infrastructure Investment and Jobs Act, China’s National Highway Network Plan, and the EU Landfill Directive underpins a steady pipeline of road, mining, and waste-management projects. Volatile feedstock prices and tightening rPET availability temper margins, yet the shift toward value-added advisory services supports price resilience. Regional converters remain relevant in tailings-dam liners and agricultural drainage where just-in-time delivery outweighs brand scale, keeping the overall market moderately fragmented.

Key Report Takeaways

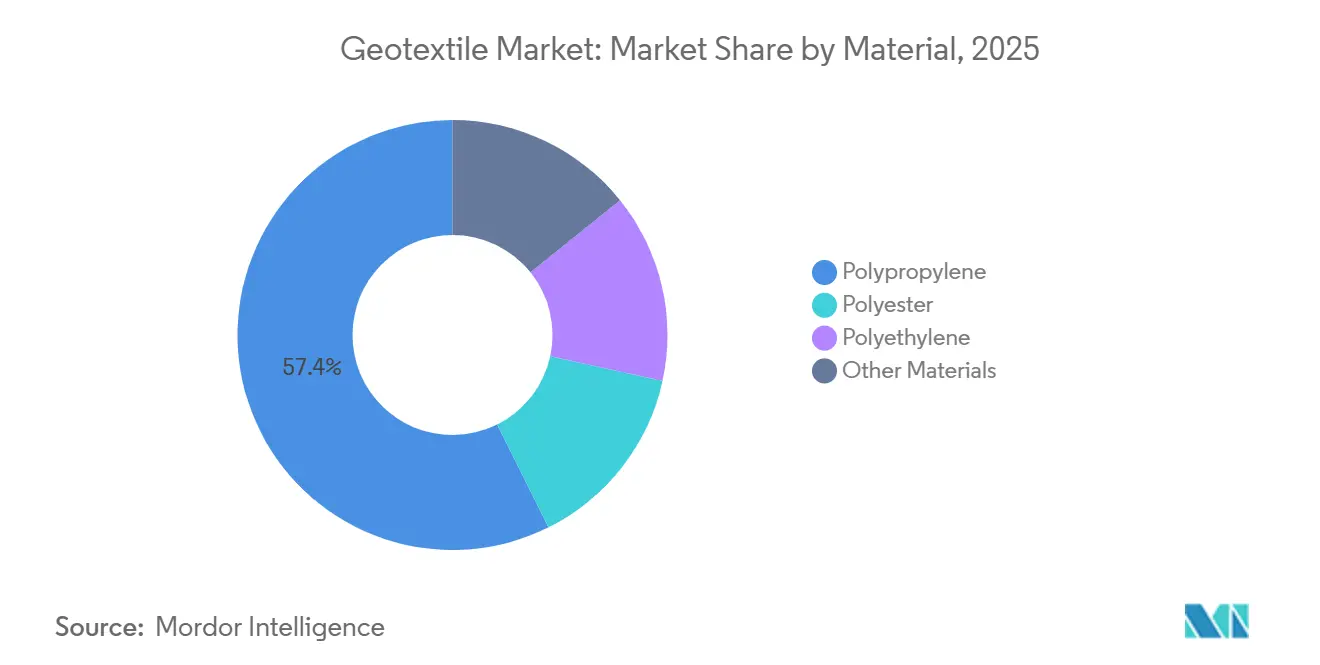

- By material, polypropylene held 57.38% of geotextile market share in 2025 and is forecast to expand at an 11.33% CAGR through 2031.

- By fabric type, woven captured 45.26% revenue share in 2025; non-woven fabrics are advancing at an 11.54% CAGR to 2031.

- By function, separation commanded 30.12% of the geotextile market size in 2025 and is progressing at a 12.24% CAGR through 2031.

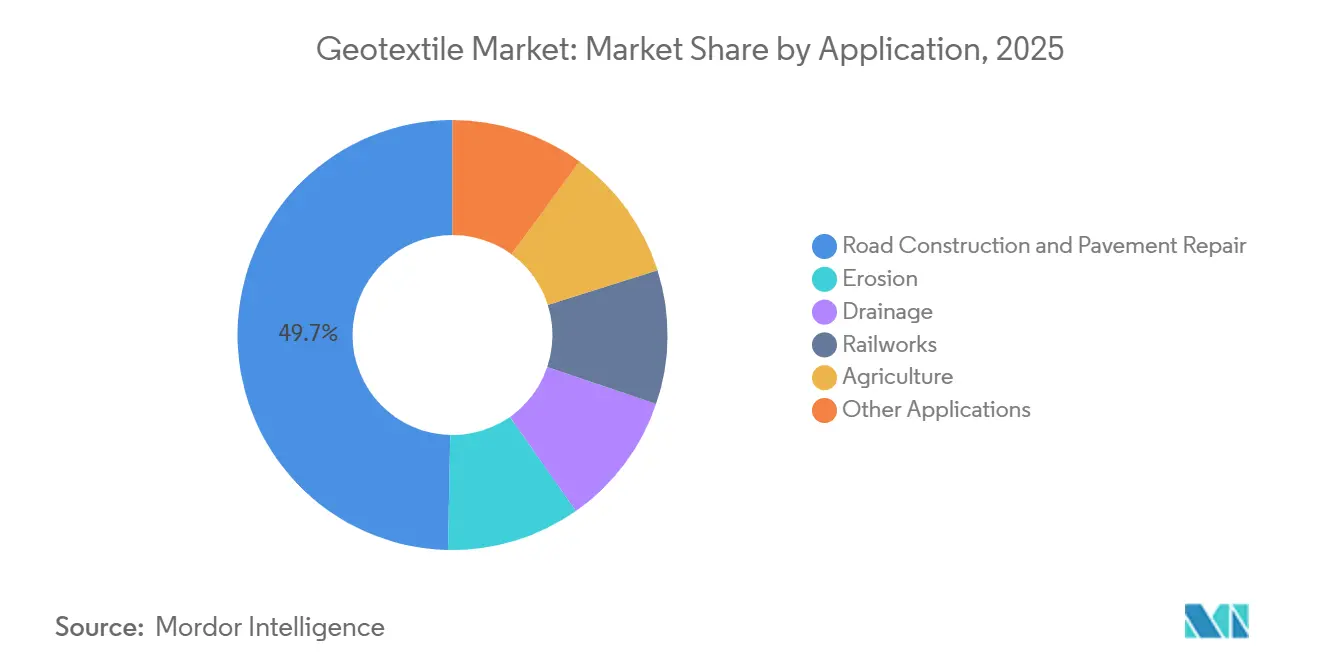

- By application, road construction and pavement repair led with 49.67% of revenue in 2025 and the segment is projected to record the fastest CAGR at 12.57% to 2031.

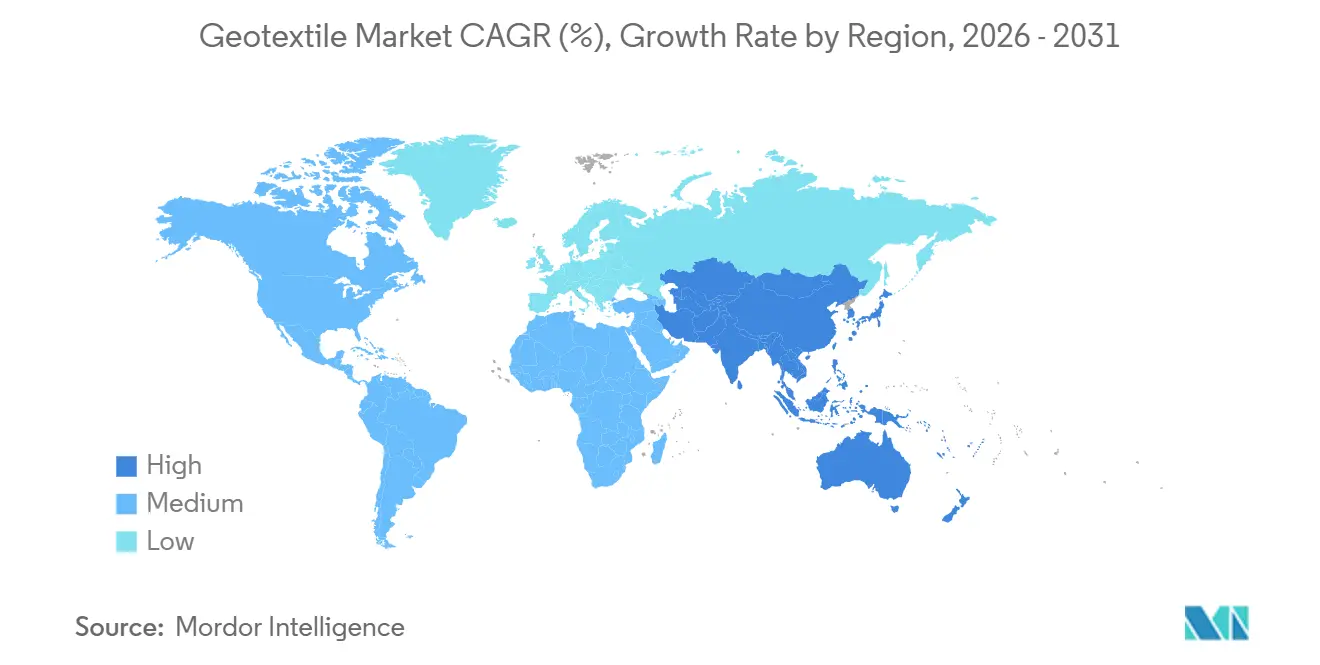

- By geography, Asia-Pacific led with 39.58% of revenue in 2025 and is projected to record the fastest CAGR at 11.89% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Geotextile Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption in Road and Highway Infrastructure Projects | +3.2% | Global, with concentration in Asia-Pacific (China, India, ASEAN) and North America | Medium term (2-4 years) |

| Rising Demand for Filtration and Drainage in Water-Management Assets | +2.1% | Global, with early gains in Europe, North America, and water-stressed APAC regions | Long term (≥ 4 years) |

| Stricter Global Landfill and Wastewater Regulations | +1.8% | Europe (EU Landfill Directive), North America (EPA Subtitle D), emerging enforcement in APAC | Short term (≤ 2 years) |

| Accelerating Investment in Mining Tailings-Dam De-Risking | +1.5% | Global, with focus on Chile, Peru, Australia, Canada, South Africa | Medium term (2-4 years) |

| Mandatory Capping Layers Under EU Landfill Directive | +1.4% | Europe (EU-27), with spillover to UK and candidate countries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption in Road and Highway Infrastructure Projects

The FY2026 U.S. federal budget earmarks USD 111.3 billion for highways, including USD 7.2 billion for bridge replacement, cementing a multi-year pull for separation and reinforcement fabrics. India awarded 8,500 kilometers of national highways during 2025, embedding geotextile layers to curb settlement in monsoon regions. China cleared 4,200 kilometers of expressways in early 2026 and now mandates soil-reinforcement geosynthetics for soft-clay corridors in Jiangsu and Zhejiang. Across ASEAN, connectivity corridors use non-woven filtration layers beneath crushed-stone bases to stem fines migration. Contracts have shifted from lowest bid to performance-based deals that bundle warranties and remote monitoring, favoring suppliers with integrated design platforms.

Rising Demand for Filtration and Drainage in Water-Management Assets

EU utilities spent EUR 18 billion on stormwater upgrades in 2025, codifying geotextile-wrapped perforated pipes in German and Dutch drainage norms to prolong service life to 50 years. The U.S. EPA disbursed USD 6.8 billion under the Clean Water State Revolving Fund in 2025, with many plants adopting geotextile filtration layers in constructed wetlands to meet suspended-solids limits. India’s Jal Jeevan Mission scales infiltration galleries lined with geotextiles across arid states, while Australia’s Murray-Darling Basin modernization finances subsurface drains wrapped in needle-punched fabrics to curb salinity. These programs reposition geotextiles as engineered systems that deliver measurable OPEX reductions rather than generic textile inputs.

Stricter Global Landfill and Wastewater Regulations

The 2024 EU Landfill Directive amendment compels multi-layer caps featuring drainage geotextiles, raising demand to 40–50 million m² for retrofits alone[1]European Commission, “EU Landfill Directive Amendment 2024,” ec.europa.eu . California’s Title 27 revision now specifies 2,200 N minimum puncture resistance, a 15% hike that favors calendered polypropylene. China updated its landfill code in 2025 to enforce separation layers in leachate systems, adding up to 10 million m² yearly. Compliance pushes fabricators to invest in heat-setting lines while recycling and testing documentation becomes procurement gatekeepers across the Atlantic.

Accelerating Investment in Mining Tailings-Dam De-Risking

GISTM adoption across 80 miners mandates independent dam reviews by 2028, accelerating retrofits that install drainage blankets to relieve pore pressure[2]International Council on Mining and Metals, “GISTM Implementation Report 2025,” icmm.com . Vale earmarked USD 1.8 billion in 2025 for Brazilian dam decommissioning that specifies geotextile-wrapped drains to expedite consolidation. BHP’s Escondida commits USD 450 million for tailings expansion in 2026 using reinforced lifts that leverage woven fabrics rated at 100 kN/m tensile strength. South Africa’s draft rules mirror this, forecasting 4 million m² incremental demand. Large miners lock multi-year buying frameworks, while juniors buy spot, fostering a two-tier pricing environment.

Restraints Impact Analysis of Geotextile Market*

| Restraint | (~) x`% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude Oil Linked Volatility in Polypropylene and Polyester Prices | -1.6% | Global, with acute impact in import-dependent regions (ASEAN, Middle-East, Africa) | Short term (≤ 2 years) |

| rPET Diversion to Beverage Packaging Tightening PET Supply | -0.9% | Europe (EU Plastics Strategy), North America (California SB 54), emerging in APAC | Medium term (2-4 years) |

| Design-Engineering Talent Gap in Emerging Markets | -0.7% | APAC (excluding Japan, South Korea), Latin America, Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil-Linked Volatility in Polypropylene and Polyester Prices

Polypropylene is projected at USD 1,150/ton in Asia during Q1 2026, 18% above Q4 2025 after OPEC+ cuts squeezed naphtha supply. European polyester staple fiber hit EUR 1,420/ton (USD 1,530) on refinery outages and high gas prices. Fabricators lock customer prices for 12–18 months but procure resin monthly, eroding margins when spikes exceed 15%. Smaller converters without hedging instruments face cash-flow stress, leading to project delays or downgraded fabric specs.

rPET Diversion to Beverage Packaging Tightening PET Supply

The EU Plastics Strategy mandates 30% recycled content in PET bottles by 2030, diverting roughly 1.2 million tons of rPET from industrial outlets. California’s SB 54 enforces 25% rPET by 2027, pushing North American spot prices to USD 1,680 / ton, a 35% premium to virgin PET. Geotextile producers either absorb cost or revert to virgin polyester, undermining sustainability claims and elevating polypropylene as a cheaper substitute.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geotextile Market Segment Analysis

By Material:

Polypropylene Continues to Dominate on Cost and Chemical ResistancePolypropylene held 57.38% of 2025 revenue and is growing at an 11.33% CAGR to 2031 as transportation agencies prioritize alkaline-soil resistance over recycled content. Polyester is constrained by rPET scarcity and remains indispensable for high-tensile applications like tailings-dam reinforcement. Polyethylene occupies niche in UV-intensive landfill caps where conformability justifies its premium. Natural fibers such as coir and jute fill in short-term erosion control across South Asia and East Africa. Bio-based polypropylene pilots target 30% renewable feedstock by 2028, yet must close a 25% cost gap before scaling.

Polypropylene’s hydrophobicity prevents moisture-induced subgrade weakening, extending pavement life by up to 20 years on Chinese and Indian motorways. Polyester’s elongation at break above 50% retains traction in embankment lifts requiring extreme strain absorption. Polyethylene’s UV stability secures use in exposed coastal revetments where service life exceeds 50 years. Natural fibers meet biodegradable mandates on gentle slopes but remain limited by tensile ceilings below 20 kN/m.

By Fabric Type:

Non-Woven Uptake Mirrors Conformability NeedsWoven commanded 45.26% revenue in 2025 for high-load reinforcement of unpaved roads and rail beds that demand more than 1,400 N grab tensile strength. Non-wovens are the fastest risers at 11.54% CAGR through 2031, answering landfill and drainage specs that require more than 1×10⁻³ m/s permeability. Knitted geotextiles handle specialized revetments where 3-D interlocking boosts soil retention. Hybrid lines combining woven yarn grids with non-woven filter webs emerge to meet ballast and soft-soil dual requirements.

EU landfill caps effectively prescribe non-woven drainage layers, creating sticky demand through 2030. Asia-Pacific miners are upgrading to woven fabrics rated at ≥100 kN/m for tailings dams, a strength unattainable for standard needle-punched webs. India’s 2025 pavement guidance, however, opens light-traffic roads to spunbond non-wovens, triggering a cost-down swing for rural corridors.

By Function:

Separation Leads as Agencies Eye Pavement LongevitySeparation topped 30.12% of 2025 revenue and is racing at a 12.24% CAGR to 2031 because agencies find it extends overlays by up to two decades. Drainage is growing due to robust water-utility spending, while filtration is growing due to wetlands and irrigation schemes. Reinforcement drives demand as mining, haul roads, and embankments rely on high-tensile woven fabrics. Protection layers occupy the balance, cushioning geomembranes in landfills and reservoirs.

The Federal Highway Administration’s 2025 guidance effectively mainstreamed separation fabrics across 45% of soft-soil interstate miles. Water utilities retrofit storm drains with geotextile-wrapped pipes to hit TSS discharge caps, bumping drainage demand. Reinforcement uptake is concentrated in Chilean copper and Australian iron ore mines where heavy haul dictates more than 100 kN/m tensile specs.

By Application:

Road Construction Anchored by Fiscal StimulusRoad construction and pavement repair contributed 49.67% of 2025 revenue and grow at a compelling 12.57% CAGR on the USD 350 billion U.S. stimulus and Asia-Pacific highway booms. Erosion is expanding as coastal states armor shorelines against extreme weather. Agricultural subsurface systems in Australia and India fuel drainage. Railworks grow due to China’s high-speed network and India’s Dedicated Freight Corridor. Mining, coastal containment, and other applications of tailings liner failures are linked to compliance with the Global Industry Standard on Tailings Management (GISTM).

Geography Analysis

APAC Geotextile Market

Asia-Pacific generated 39.58% of 2025 revenue and is outpacing peers at 11.89% CAGR on China’s expressway surge and India’s Bharatmala builds that standardize polypropylene separation layers. Southeast Asia invested USD 18 billion in 2025 for cross-border highways, specifying non-woven filtration fabrics to minimize fines migration. Japan and South Korea, with limited greenfield land, pivot to rehabilitation and coastal erosion works that prefer high-strength woven polyester.

North America Geotextile Market

North America is buoyed by the Infrastructure Investment and Jobs Act and Canada’s CAD 33.5 billion allocation. FY2026 budgets earmark USD 111.3 billion for U.S. highways, sustaining long-cycle demand despite labor and permitting delays that push some procurement into 2027. Mexico bundles geotextile supply into turnkey EPC deals to compress timelines on federal corridors.

EMEA and South America Geotextile Market

Europe mandates add 40–50 million m² of drainage layers through 2030. Germany’s UBA pushes permeability thresholds that tilt demand toward needle-punched webs, while the UK enforces protection layers to block root and rodent puncture. South America is led by Brazil’s BRL 45 billion PAC roads and coastal ports. The Middle-East and Africa is paced by Saudi Arabia’s NEOM highway grid and UAE desert road stabilization.

Regulatory Landscape

Geotextile demand is shaped by civil-engineering performance standards and procurement rules that specify test methods, minimum mechanical properties, and traceable compliance documentation. In the United States, agencies and conservation programs commonly reference AASHTO M 288 for geotextile classification and USDA NRCS requirements that cite ASTM methods, such as ASTM D6461 for temporary silt fence applications. This supports a broader procurement preference for qualification by verified index properties rather than brand-only approvals.

Trade and local-content policies increasingly affect sourcing for polymer-based geosynthetics on publicly funded work. Under the U.S. Build America, Buy America (BABA) framework, FHWA guidance has indicated most polymer-based geosynthetics are treated as construction materials, which triggers final assembly and 55% domestic content requirements for Federal-aid projects starting October 1, 2026. Tariffs under U.S. HTS Chapter 56 and additional duties on some Chinese-origin textile inputs also influence landed costs, while China has refreshed national standards, for example, GB/T 17642-2025 for geosynthetics-related applications, adding another compliance layer for suppliers supporting multi-country EPC and infrastructure programs.

Value Chain Analysis

The geotextile value chain begins with upstream petrochemical and polymer producers supplying polypropylene (PP), polyester (PET, including rPET streams), and polyethylene, followed by additive suppliers and fiber producers. Converters transform resin into filaments, staple fibers, or tapes, and then manufacture geotextiles through extrusion, spinning, weaving or knitting, needle punching, and calendering, before finishing, slitting, and packaging. Quality control and certification are key midstream activities, supported by standardized test regimes, including tensile and hydraulic properties under ISO methods such as ISO 10319 and ISO 11058, alongside ASTM methods, to meet DOT, landfill, mining, and water-asset specifications.

In the downstream portion of the chain, products are sold directly to EPCs and civil contractors, distributed through regional fabricators and installers, and supplied via project-based tenders and multi-year framework contracts. Polymer chip costs remain a major economic driver, which amplifies the effect of crude-oil-linked PP and PET volatility highlighted in the market overview. Sustainability and documentation expectations are also becoming more prominent at the customer interface, with tools such as Environmental Product Declarations (EPDs) used in bidding to support embodied-carbon and traceability requests, pushing producers to expand testing capacity, digital documentation, and technical-service capabilities.

Competitive Landscape

Top suppliers - Freudenberg, Solmax, HUESKER, Naue, and Fibertex - held 44% revenue in 2025, leaving ample runway for regional entities. Freudenberg’s 2025 bio-based polypropylene pilot targets 30% renewable feedstock by 2028. Solmax acquired a 120,000 m² Indian plant in February 2026, adding 15 million m² annual woven capacity for Bharatmala tenders. HUESKER landed a EUR 28 million landfill-retrofit contract covering 45 German sites through 2027.

Digital differentiation rises as Solmax and Naue deploy cloud design tools that cut over-specification by up to 15% and embed suppliers early in project scoping. Patent activity centers on multi-functional needle-punched webs that deliver drainage and filtration simultaneously. Chinese converters undercut EU makers by 20% on FOB terms, pushing incumbents toward high-certification niches such as mining liners and hazardous-waste containment. Overall rivalry is moderate; switching costs are anchored in lab approvals and contractor familiarity, preserving stable mid-single-digit EBITDA margins for top players.

Geotextile Industry Leaders

HUESKER International

Naue GmbH & Co. KG

Fibertex Nonwovens A/S

Solmax

Freudenberg Performance Materials

- *Disclaimer: Major Players sorted in no particular order

Geotextile Market Companies Covered in this Report

- ACE Geosynthetics

- AFITEXINOV

- AGRU America Inc.

- Amcor plc

- Asahi Kasei Advance Corporation

- Carthage Mills

- CMC

- Fibertex Nonwovens A/S

- Freudenberg Performance Materials

- HUESKER International

- Industrial Fabrics, Inc.

- KayTech

- Mattex Geosynthetics

- Naue GmbH & Co. KG

- Officine Maccaferri Spa

- Owens Corning

- Solmax

- Thrace Group

Market Opportunities and Future Outlook

Capacity localization and regional manufacturing footprints are an opportunity area as infrastructure and environmental programs increase demand for short lead times, stable specifications, and tender-ready documentation. In January 2026, Exeed Geotextile opened a 175,000 sq. ft. facility in the Sharjah Airport International Free Zone (SAIF Zone), citing annual capacity for non-woven geotextiles and polypropylene fibers, which supports faster supply into Middle East infrastructure and drainage projects. Similar localization themes appear in March 2026, when Alujain Corporation and Beaulieu International Group formed a joint venture to expand geotextile production activities in Yanbu, Saudi Arabia, improving proximity to large road and industrial corridor builds and reducing reliance on long-haul imports.

Sustainability-driven product differentiation is also moving beyond recycled content into biodegradable and bio-based solutions for erosion control, remediation, and temporary works that require controlled service life. Naue highlighted biodegradable erosion-control solutions such as Secumat Green 3D mesh during 2026 communications, and academic work published in 2026 has demonstrated biodegradable functionalized nonwovens for remediation use cases, pointing to a route for suppliers targeting projects that weigh end-of-life and microplastic concerns. At the same time, procurement rules that tighten documentation and domestic-content compliance, including U.S. BABA requirements starting October 1, 2026, create whitespace for suppliers that can package certification, design support, and traceable sourcing into turnkey bids for highways, landfills, and water-management assets.

Recent Industry Developments in Geotextile Market

- July 2026: HUESKER Group announced Basetrac Plate, a load-distribution solution for temporary traffic access manufactured with a 100% recycled plastic core. The launch reinforces circular-economy positioning in construction logistics and temporary access works, and it broadens the companys offering around separation and load management use-cases tied to infrastructure projects.

- April 2025: HUESKER Group acquired Sineco International, an Italian drainage technology specialist, expanding its drainage and erosion-control portfolio. The acquisition adds complementary know-how and product breadth that can increase value per project in water-management, transport, and environmental applications where drainage performance is specified and verified.

- December 2024: Solmax consolidated its European nonwoven geotextile production at a new facility near Paris and outlined a plan to close its Linz (Austria) and Bezons (France) plants over two years. The consolidation concentrates manufacturing and quality systems for faster fulfillment into landfill and infrastructure projects, supporting cost and service improvements in a region shaped by stringent containment and cap requirements.

Geotextile Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the geotextile market covers revenue from permeable textile sheets used with soil, rock, or waste to separate, filter, drain, reinforce, or protect in civil and environmental projects. It includes synthetic and natural material formats that are sold for construction and related end uses.

Scope exclusions: This sizing excludes non-textile geosynthetics such as geomembranes, geogrids, geofoams, and geocomposites.

Segments Covered in This Report

- By Material

- Polypropylene

- Polyester

- Polyethylene

- Other Materials

- By Fabric Type

- Woven

- Non-woven

- Knitted

- By Function

- Separation

- Drainage

- Filtration

- Reinforcement

- Protection

- By Application

- Road Construction and Pavement Repair

- Erosion

- Drainage

- Railworks

- Agriculture

- Other Applications (Mining Operations, Coastal and Waterway Protection, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Thailand

- Malaysia

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- South Africa

- Nigeria

- Egypt

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping where geotextiles are consumed, then translating that demand into realistic pricing and supply availability. We use public infrastructure and construction indicators from sources such as the US Census Bureau construction data, Eurostat construction output series, and national statistics offices in major consuming countries.

To avoid relying on one signal, we also check trade and material context using sources such as UN Comtrade for HS-level trade flows and the USGS for broader industrial materials context where it helps. Technical and usage cues come from peer reviewed civil engineering journals, supported by standards and guidance documents from organizations such as ASTM International. Company annual reports, investor presentations, and reputable press releases are reviewed to confirm capacity moves and demand themes, and paid subscription sources for company financials and patent databases are used selectively to improve coverage of privately held converters and product innovation. The sources listed here are illustrative, and additional public and paid references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test assumptions on application mix, typical price bands by fabric type, and the pace at which nonwoven formats are replacing older solutions in drainage and roadworks. We spoke with manufacturers, distributors, contractors, and engineering consultants across APAC, EMEA, and the Americas, then rechecked outliers with follow-up discussions when replies did not align with what desk indicators were suggesting.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | APAC: 44% |

| Mid tier: 49% | Functional/Unit leaders: 40% | EMEA: 36% |

| Smaller Players: 18% | Managers: 46% | Americas: 20% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where construction activity and civil engineering demand signals are converted into an addressable fabric requirement, then translated into value using realistic price ranges. To keep the model grounded, we use inputs such as road and rail project intensity, drainage and erosion control adoption in public works, landfill and containment build-outs, and the regional split between woven and nonwoven usage, since that mix affects how the value pool is formed.

After the demand pool is established, we check results using selective bottom-up approximations, including sampled manufacturer and converter revenue disclosures, channel checks on typical selling prices, and volume cues from trade and import patterns in key consuming regions. Where bottom-up coverage is thin, gaps are handled by applying conservative penetration ranges tied to the project mix local experts described, and then rebalancing so regional totals stay consistent with macro construction indicators.

Forecasting uses scenario analysis supported by short regression checks, with key drivers including infrastructure spend cycles, urbanization pressure, and raw material price movement for polymers that influence geotextile pricing. Assumptions for price progression and adoption are reviewed with interview inputs, and sensitivity bands are kept visible so the final forecast can be reproduced and stress-tested.

Data Validation & Update Cycle

Outputs are validated through multiple checks, since a single-source market value can drift when one indicator spikes. We compare final totals against independent signals such as construction output trends, trade movement consistency, and the implied per-project fabric intensity to identify if any region appears overstated.

When a variance is found, we review the drivers, recheck the input series, and trigger a short re-contact with the most relevant respondent type to confirm what changed in the field. Before sign-off, the model goes through a second analyst review focused on unit logic, currency conversion timing, and year-to-year continuity. The report is refreshed annually, with interim updates when material events occur, followed by a final pre-delivery pass so clients receive the latest updated view.

Mordor Intelligence's Geotextile Market Estimate Compared With Other Published Estimates

Published market values for geotextiles can vary significantly, even when the topic name appears identical across sources. Differences usually come from what is counted as a geotextile versus nearby geosynthetics, the base years selected, and how pricing changes are treated when raw material costs move.

The table shows a wide spread for 2025, and in Mordor Intelligence's model the USD 4.29 B figure is limited to permeable textile products only, which keeps geomembranes and other non-textile geosynthetics outside the revenue total even if they are used on the same jobsite. Some publishers also appear to use a broader bundle that includes adjacent products, or they apply a single global average selling price that does not reflect regional mix shifts between woven and nonwoven formats, which can lift the headline number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.29 B (2025) | |

| Industry Publisher A | USD 8.35 B (2025) | Uses a broader scope that can blend geotextiles with adjacent geosynthetic products and applies a pricing path that is less tied to region-level mix between woven and nonwoven formats. |

| Research Group B | USD 8.41 B (2025) | Appears to include a wider end-use bundle and a different base-year alignment, which can inflate the 2025 value when material categories and application boundaries are not kept strictly textile-only. |

Looking across the three values, scope control is the largest driver, followed by how price and mix are carried forward year to year. The approach stays traceable because each major step is tied to construction and civil works demand signals, then cross-checked with practical price ranges shared by market participants.

Key Questions Answered in the Report

How fast is the geotextile market expected to grow through 2031?

The market is projected to progress at a 10.39% CAGR, reaching USD 7.77 billion by 2031.

Which material accounts for the largest share of current demand?

Polypropylene holds 57.38% of 2025 revenue due to cost effectiveness and chemical resistance.

What drives non-woven geotextile uptake?

Landfill and drainage regulations that require high permeability and conformability push non-woven adoption at an 11.54% CAGR.

Which region offers the strongest growth outlook?

Asia-Pacific leads with an 11.89% CAGR through 2031 as China and India finance large highway programs.

Page last updated on: