Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

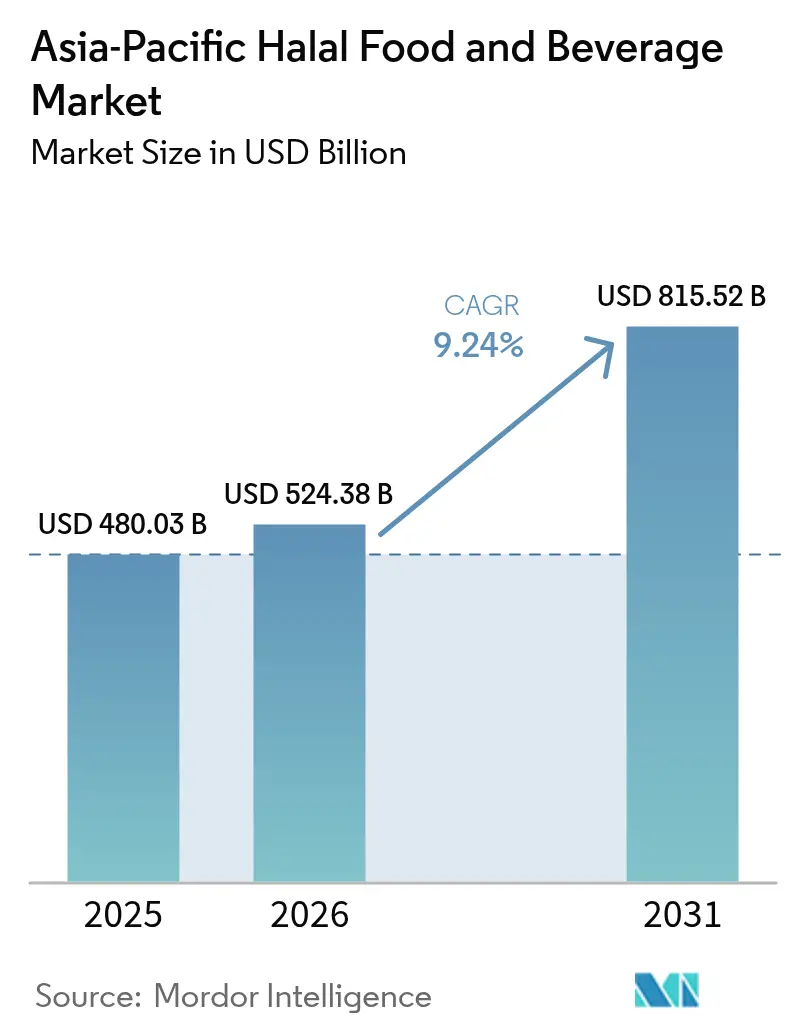

| Base Year Market Size (2025) | USD 480.03 Billion |

| Market Size (2026) | USD 524.38 Billion |

| Market Size (2031) | USD 815.52 Billion |

| Growth Rate (2026 - 2031) | 9.24% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Halal Food And Beverage Market Analysis by Mordor Intelligence

Asia-Pacific halal food and beverage market size in 2026 is estimated at USD 524.38 billion, growing from 2025 value of USD 480.03 billion with 2031 projections showing USD 815.52 billion, growing at 9.24% CAGR over 2026-2031. This trajectory reflects structural demand anchored in demographic momentum rather than cyclical consumption patterns. Indonesia commanded 36.54% of regional revenue in 2024, yet Malaysia will outpace all peers with a 10.22% CAGR through 2030, driven by its government's systematic push to position the nation as a global halal hub through JAKIM's mutual recognition agreements with 85 certifying bodies worldwide. The growth differential between these neighbors illustrates how regulatory sophistication, not just Islamic population size, determines market velocity. Headline risks center on certification fragmentation and counterfeit labeling. Despite ASEAN's 2024 push for mutual recognition, divergent standards across Indonesia (BPJPH), Malaysia (JAKIM), Thailand (CICOT), and Singapore (MUIS) force exporters to maintain parallel compliance systems, inflating costs according to industry consultations. Counterfeit halal logos proliferate in markets with weak enforcement, eroding consumer trust and creating reputational hazards for legitimate brands. Meanwhile, non-halal alternatives priced 15-25% below certified products tempt cost-sensitive buyers in India and China, where Islamic minorities lack the purchasing power to consistently absorb halal premiums. Functional beverages, plant-based proteins, and ready meals outpace legacy staples as urban consumers swap lengthy preparation for convenience. Divergent national standards, however, inflate multi-market compliance costs and create white-space opportunities for agile suppliers that can navigate regulatory fragmentation faster than multinationals.

Key Report Takeaways

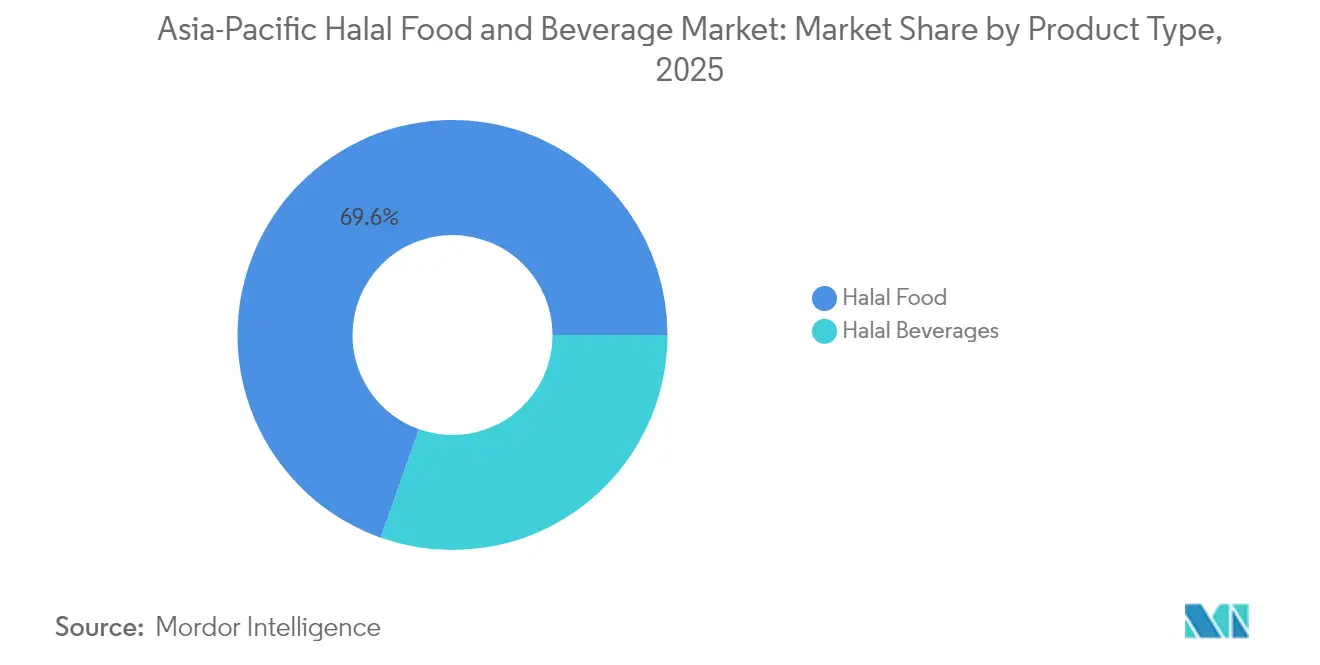

- By product type, halal food captured 69.58% of 2025 revenue, while beverages are forecast to expand at a 9.52% CAGR through 2031.

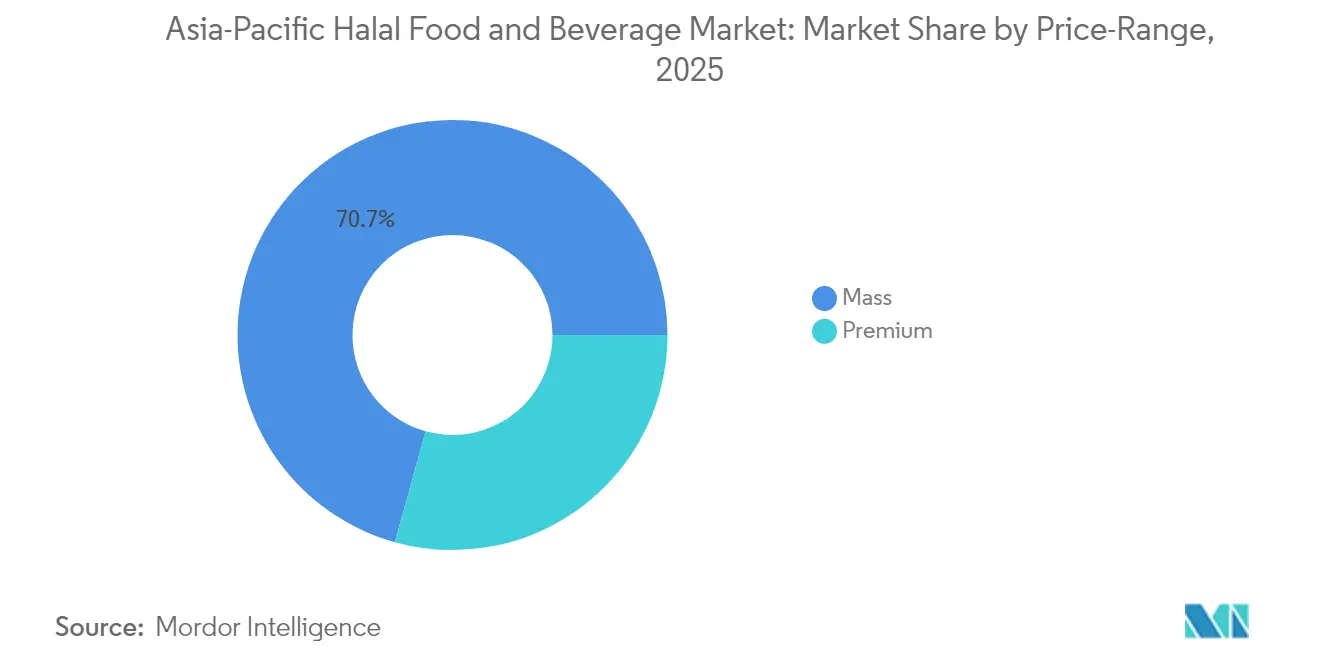

- By price range, mass-market goods held 70.68% of 2025 sales; premium products are projected to grow at a 10.05% CAGR.

- By distribution channel, supermarkets and hypermarkets retained 43.10% of 2025 spending, whereas online retail is set to rise at a 9.63% CAGR.

- By geography, Indonesia accounted for 36.10% of 2025 revenue; Malaysia is expected to post the fastest 10.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Halal Food And Beverage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Islamic population boosts halal product demand | +2.1% | Indonesia, Malaysia, India, Bangladesh, with spillover to Singapore and Australia | Long term (≥ 4 years) |

| Halal-compliant ready meals and dairy alternatives expansion | +1.5% | Urban centers across Indonesia, Malaysia, Singapore, and Japan (Islamic-friendly tourism) | Medium term (2-4 years) |

| Growing consumer demand for safe, quality-assured foods | +1.3% | APAC (Asia-Pacific)core (Indonesia, Malaysia, Singapore), expanding to China and India | Medium term (2-4 years) |

| Improved supply-chain traceability via blockchain and technology solutions | +0.9% | Indonesia (SiHalal), Malaysia (HalalChain pilots), Singapore (smart logistics hubs) | Short term (≤ 2 years) |

| Modern retail expansion improves halal accessibility region-wide | +1.2% | Indonesia, Malaysia, India, China (tier-2 cities), Australia (multicultural suburbs) | Medium term (2-4 years) |

| Diversified halal product range across many food categories | +1.4% | APAC, with innovation clusters in Malaysia, Singapore, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Islamic Population Boosts Halal Product Demand

Demographic momentum underpins the 9.35% CAGR as Asia-Pacific's Islamic population expands from 1.1 billion in 2024 toward 1.3 billion by 2030, per UN population projections[1]Source: Economic and Social Commission for Asia and the Pacific, "Asia-Pacific Population and Development Report 2023", un.org. Indonesia alone houses 237 million Islamics, while India's 200 million Islamic minority represents the world's third-largest Islamic population. This scale creates a captive base for halal-certified staples, yet purchasing power varies dramatically: Indonesian per-capita halal spending reached USD 420 in 2024, versus USD 180 in India, per government trade data. The gap explains why Indonesia's 36.54% market share dwarfs India's despite comparable Islamic populations. Malaysia's proactive halal industrialization strategy, codified in its 2024-2030 National Halal Masterplan, positions the country to capture diaspora demand across Singapore, Brunei, and Southern Thailand, leveraging JAKIM's brand equity as a gold-standard certifier.

Halal-Compliant Ready Meals and Dairy Alternatives Expansion

Urbanization and dual-income households drive demand for convenient, shelf-stable halal meals. Indonesia's ready-meal segment grew year-on-year in 2024, fuelled by e-commerce penetration and cold-chain infrastructure upgrades funded by government logistics initiatives. Plant-based dairy alternatives, oat milk, almond yogurt, are gaining traction among health-conscious Islamics who view them as inherently halal, bypassing certification complexities tied to animal-derived ingredients. Nestlé's 2024 launch of halal-certified plant-based condensed milk in Malaysia signals multinational recognition of this shift. Japan's halal ready-meal market, though niche, expanded in 2024 as tourism rebounds and Islamic visitors seek certified convenience foods at airports and train stations, per Japan Halal Association data.

Growing Consumer Demand for Safe, Quality-Assured Foods

Halal certification has evolved beyond religious compliance into a proxy for food safety and ethical sourcing, appealing even to non-Islamic consumers. A 2024 survey by Indonesia's BPJPH found that 18% of halal-certified product buyers were non-Islamics attracted by perceived quality assurance. This halo effect amplifies market potential, particularly for exports to China, where food safety scandals have eroded trust in domestic brands. Malaysia's halal-certified baby food exports to China surged in 2024, per Malaysian External Trade Development Corporation data, as Chinese parents equate JAKIM certification with rigorous safety protocols [2]Source: Malaysia External Trade Development Corporation, "EXPORT PROMOTION", matrade.gov.my. The trend suggests halal positioning can command premium pricing beyond Islamic-majority markets, provided brands invest in consumer education.

Diversified Halal Product Range Across Many Foods Categories

Beyond meat and poultry, halal certification now spans confectionery, bakery, savory snacks, sauces, and baby food. Malaysia's Secret Recipe launched halal-certified cakes in 15 new flavors in 2024, targeting gifting occasions during Ramadan and Eid. Indonesia's Ramly introduced halal-certified frozen seafood, capitalizing on coastal demand for convenient protein. Japan's Bourbon Corporation obtained halal certification for select biscuit lines in 2024, aiming to capture Islamic tourist spending at convenience stores. This category proliferation diversifies revenue streams and insulates the market from single-category shocks, such as avian flu outbreaks that periodically disrupt poultry supply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented halal certification standards vary across countries | -1.2% | ASEAN core (Indonesia, Malaysia, Thailand, Singapore), with export friction to China, Japan, and Australia | Medium term (2-4 years) |

| Risk of mislabelling or counterfeit halal certification | -0.8% | Indonesia, India, China (weak enforcement zones), with reputational spillover across APAC | Short term (≤ 2 years) |

| Competition from cheaper non-halal or uncertified alternatives | -1.0% | India, China, Philippines (price-sensitive Islamic minorities) | Medium term (2-4 years) |

| Supply-chain complexity challenges halal integrity maintenance | -0.7% | Multi-country supply chains (Indonesia-Malaysia-Singapore trade corridors), cold-chain gaps in rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Halal Certification Standards Vary Across Countries

Despite ASEAN's 2024 mutual recognition framework, practical harmonization remains elusive. Indonesia's BPJPH mandates on-site slaughter audits, while Malaysia's JAKIM accepts video documentation, creating procedural mismatches that delay cross-border approvals. Thailand's CICOT and Singapore's MUIS impose distinct labeling requirements, forcing exporters to redesign packaging for each market. According to studies, it was found that certification costs for a single product across four ASEAN markets averaged USD 45,000, versus USD 12,000 for a single-country certification. This fragmentation disproportionately burdens small and medium enterprises, consolidating market share among multinationals with dedicated regulatory teams. Compliance with JAKIM and BPJPH standards, the region's most stringent, has become a de facto prerequisite for pan-ASEAN distribution, marginalizing producers who lack resources to meet dual benchmarks.

Risk of Mislabeling or Counterfeit Halal Certification

Counterfeit halal logos proliferate in markets with weak enforcement infrastructure. Indonesia's BPJPH conducted 1,200 raids in 2024, seizing products bearing fake halal stamps, per Ministry of Religious Affairs reports. India's lack of a centralized halal authority enables rogue certifiers to issue dubious approvals, eroding consumer confidence. A 2024 investigation documented Chinese manufacturers affixing halal logos to non-compliant products destined for Southeast Asian markets, exploiting lax customs inspections. These incidents trigger brand crises: when a Malaysian retailer unknowingly stocked mislabeled Indonesian snacks in 2024, social media backlash forced a nationwide recall, costing the distributor an estimated USD 3 million. Blockchain traceability systems promise mitigation, but adoption remains nascent outside Singapore and Malaysia.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beverages Outpace Traditional Food Growth

Halal food commanded 69.58% of 2025 revenues, anchored by staples like meat, poultry, dairy, and bakery products that form the dietary core for Islamic households. Within this segment, ready meals and dairy alternatives are expanding rapidly as urbanization shortens meal preparation time and plant-based diets gain cultural acceptance. Meat, poultry, and seafood remain the largest subsegment, driven by high per-capita consumption in Indonesia and Malaysia, yet face margin pressure from volatile feed costs and avian flu outbreaks that periodically constrain supply. Confectionery and savory snacks benefit from impulse purchasing and gifting traditions during Islamic festivals, while baby food enjoys premiumization as middle-class parents prioritize nutrition and halal assurance. Bakery products and condiments serve as everyday essentials, offering stable but low-growth revenue streams.

Halal beverages, forecast to grow at 9.52% CAGR through 2031, are capturing share from traditional food categories as functional drinks, cold-pressed juices, and plant-based milk alternatives resonate with health-conscious millennials. Malaysia's F&N Holdings launched a halal-certified collagen drink in 2024, targeting beauty-conscious Islamic women, while Indonesia's Orang Tua Group introduced a halal energy drink fortified with date extract, blending tradition with modern wellness trends. Japan's halal beverage market, though small, is expanding as convenience stores stock certified options for Islamic tourists and residents. The beverage segment's faster growth reflects lower certification complexity, most drinks avoid animal-derived ingredients, and higher margins compared to commodity food items.

By Price Range: Premium Gains as Incomes Rise

Mass-market products held 70.68% of 2025 revenues, serving price-sensitive buyers who prioritize affordability over brand prestige. This segment includes unbranded staples, private-label offerings, and economy packs sold through traditional grocery stores and wet markets. Indonesia's dominance in the mass segment reflects its large lower-middle-class population, where halal certification is expected but premium pricing is unaffordable. India's halal market skews heavily toward mass offerings, as Islamic minorities face income constraints that limit discretionary spending.

Premium halal products, forecast to grow at 10.05% CAGR through 2031, cater to affluent urbanites who equate halal with organic, ethically sourced, and artisanal qualities. Malaysia's Kawan Food introduced a premium line of halal-certified frozen dim sum in 2024, priced 35% above standard offerings, targeting expatriates and upper-income locals. Singapore's halal premium segment benefits from high per-capita incomes and a cosmopolitan consumer base willing to pay for provenance and sustainability certifications alongside halal compliance. Australia's halal-certified grass-fed beef, exported to Malaysia and Indonesia, commands a 40% premium over grain-fed alternatives, per Australian Meat Processor Corporation data. The premium segment's faster growth underscores a broader shift: halal is transitioning from a baseline religious requirement to a lifestyle choice that signals health, ethics, and quality.

By Distribution Channel: Online Retail Disrupts Traditional Models

Supermarkets and hypermarkets captured 43.10% of 2025 sales, leveraging scale, convenience, and promotional firepower to dominate halal distribution. Indonesia's Alfamart and Indomaret, Malaysia's Aeon and Giant, and Singapore's FairPrice anchor this channel, offering dedicated halal sections and private-label products. Convenience and grocery stores serve neighborhood demand, particularly in rural areas where modern retail penetration remains low. These outlets stock fast-moving halal staples but lack the SKU breadth of hypermarkets.

Online retail stores, forecast to grow at 9.63% CAGR through 2031, are reshaping halal commerce as e-commerce platforms like Shopee, Lazada, and Tokopedia integrate halal filters and certification badges into search interfaces. Indonesia's halal e-commerce sales surged in 2024, driven by pandemic-induced digital adoption and improved cold-chain logistics that enable fresh and frozen halal product delivery. Malaysia's Salaam Market, a dedicated halal e-commerce platform, reported year-on-year growth in 2024, attracting brands seeking direct-to-consumer channels. Singapore's RedMart and Australia's Coles Online expanded halal-certified SKUs in 2024, responding to multicultural demand for home delivery. The online channel's faster growth reflects its ability to aggregate niche halal products that lack shelf space in physical stores, serving long-tail demand for specialty items like halal-certified supplements, gourmet sauces, and imported confectionery.

Geography Analysis

Indonesia claimed 36.10% of 2025 revenues, a dominance rooted in its 237 million Islamics and mandatory halal certification law that took full effect in October 2024. Law 33/2014 and its implementing regulation (GR 42/2024) compel every food and beverage manufacturer, domestic and foreign, to secure BPJPH approval, creating a compliance moat that favors established players with certification expertise. Indonesia's halal market is bifurcated: urban centers like Jakarta and Surabaya exhibit premiumization trends, while rural areas remain price-sensitive and reliant on traditional retail. The government's 2024 launch of the SiHalal blockchain platform aims to streamline certification, reducing approval timelines from 6 months to 8 weeks, which could democratize market access for small and medium enterprises. Indonesia's halal exports, particularly instant noodles and palm oil-based products, reached USD 8.2 billion in 2024, per Ministry of Trade data, positioning the country as a regional halal manufacturing hub.

Malaysia, forecast to grow at 10.07% CAGR through 2031, leverages JAKIM's global brand equity to attract halal-conscious consumers and investors. The government's 2024-2030 National Halal Masterplan targets USD 12 billion in halal exports by 2030, up from USD 7.1 billion in 2024, through tax incentives for halal-certified manufacturers and R&D grants for halal innovation. Malaysia's halal logistics infrastructure, including dedicated halal ports and warehouses, ensures segregation and traceability that command premium pricing in export markets. The country's halal pharmaceutical and cosmetics sectors are expanding alongside food, creating cross-category synergies. Singapore, though small, serves as a regional halal entrepôt, leveraging its port infrastructure and regulatory clarity to facilitate intra-ASEAN halal trade. MUIS certification is recognized across Southeast Asia, enabling Singapore-based brands to scale regionally with minimal friction.

China, Japan, India, and Australia represent emerging halal markets with distinct growth drivers. China's 25 million Islamics, concentrated in Xinjiang and Ningxia, are increasingly affluent, driving demand for halal-certified imports, particularly Malaysian baby food and Indonesian snacks. Japan's halal market, though niche, expanded in 2024 as Islamic tourism rebounded post-pandemic and convenience stores stocked certified options. India's 200 million Islamics represent latent demand constrained by income levels and fragmented certification, yet urban centers like Delhi and Hyderabad are witnessing premiumization. Australia's halal-certified meat exports to Indonesia and Malaysia reached USD 1.8 billion in 2024, per Australian Meat Processor Corporation data, underscoring the country's role as a halal protein supplier rather than a domestic consumption market. The Rest of Asia-Pacific, including Bangladesh, Pakistan, and the Philippines, contributes fragmented demand shaped by local certification regimes and income disparities.

Competitive Landscape

The Asia-Pacific halal food and beverages market operates at a moderate concentration, where multinational corporations coexist with regional specialists and local incumbents. Nestlé, Cargill, and Unilever deploy global supply chains and R&D budgets to secure halal certifications across multiple jurisdictions, yet face agility constraints when navigating Indonesia's BPJPH or Malaysia's JAKIM protocols. Regional players like Kawan Food, QL Resources, and Ramly leverage deep local knowledge and established certifier relationships to outmaneuver multinationals in speed-to-market. Competitive strategies center on certification portfolio breadth, traceability transparency, and premiumization.

Firms that secure dual JAKIM-BPJPH approvals unlock pan-ASEAN distribution, while those investing in blockchain traceability systems differentiate on authenticity and food safety. Opportunities abound in halal-certified functional foods, plant-based proteins, and e-commerce-exclusive SKUs that bypass traditional retail gatekeepers. Emerging disruptors include halal-focused direct-to-consumer brands that leverage Instagram and TikTok for customer acquisition, bypassing supermarket slotting fees.

Technology adoption varies: Singapore-based firms integrate IoT and AI for supply-chain optimization, while Indonesian SMEs rely on manual processes, creating a digital divide that shapes competitive positioning. Compliance with ISO 22000 (food safety management) and HACCP (hazard analysis) standards is becoming table stakes, as retailers demand third-party audits alongside halal certification to mitigate reputational risk.

Asia-Pacific Halal Food And Beverage Industry Leaders

-

Nestlé S.A.

-

Unilever PLC

-

Cargill, Incorporated

-

BRF S.A.

-

QL Foods Sdn Bhd (QL Resources)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: OTOKI Corporation officially kicked off sales of its halal-certified JIN RAMEN in Indonesia, signaling a significant entry into the world's second-largest instant noodle market. After securing halal certification from the Indonesian Ulema Council (MUI) in December 2024, OTOKI wrapped up import licensing (ML) in early August and is poised to roll out sales by year-end via prominent hypermarkets and supermarkets nationwide.

- November 2025: General Mills teamed up with the US Dairy Checkoff programme to introduce YoBark, a yogurt-based snack designed to provide families with a healthier snacking choice. These refrigerated YoBark treats blend yogurt with Nature Valley's granola, a brand under General Mills, delivering a rich flavor experience. The initiative seeks to bolster yogurt's foothold in the snacking market.

- April 2024: Malaysia's halal industry was set for global expansion with the establishment of the China-Malaysia Halal Food Industrial Park in Perak. The initiative, a collaboration between the China-Malaysia Investment Holding Group and the Perak Islamic Economic Development Corporation, was formalized in a recent agreement, as reported by The Star. This partnership aimed to establish a hub for halal research, production, certification, and trade, bolstering Malaysia's position in the global halal market.

Asia-Pacific Halal Food And Beverage Market Report Scope

The Asia-Pacific halal food and beverage market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into halal food and halal beverages. By distribution channel, the market is segmented into hypermarkets/supermarkets, convenience/grocery stores, online retail stores, and other distribution channels. By geography, the market is segmented into China, Japan, India, Australia, Indonesia, Malaysia, Singapore, Rest of the Asia-Pacific. The market forecasts are provided in terms of value (USD).

Product Type

| Halal Food | Dairy and Dairy Alternatives | |

| Confectionery | ||

| Bakery Products | ||

| Savory Snacks | ||

| Meat, Poultry and Seafood | Red Meat | |

| Seafood | ||

| Poultry | ||

| Baby Food | ||

| Ready Meals | ||

| Condiments and Sauces | ||

| Other Product Types | ||

| Halal Beverages | ||

Distribution Channel

| Hypermarkets/Supermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

Geography

| China |

| Japan |

| India |

| Australia |

| Indonesia |

| Malaysia |

| Singapore |

| Rest of Asia-Pacific |

| Product Type | Halal Food | Dairy and Dairy Alternatives | |

| Confectionery | |||

| Bakery Products | |||

| Savory Snacks | |||

| Meat, Poultry and Seafood | Red Meat | ||

| Seafood | |||

| Poultry | |||

| Baby Food | |||

| Ready Meals | |||

| Condiments and Sauces | |||

| Other Product Types | |||

| Halal Beverages | |||

| Distribution Channel | Hypermarkets/Supermarkets | ||

| Convenience/Grocery Stores | |||

| Online Retail Stores | |||

| Other Distribution Channels | |||

| Geography | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Indonesia | |||

| Malaysia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

How large is the Asia-Pacific halal food market in 2026?

It is valued at USD 524.38 billion with a 9.24% CAGR outlook to 2031.

Which country contributes the most revenue?

Indonesia leads with 36.10% of 2025 regional sales under BPJPH mandates.

Which segment is expanding fastest?

Halal beverages, driven by functional and plant-based launches, forecast a 9.52% CAGR to 2031.

Page last updated on: