Market Overview

| Study Period | 2017 - 2029 |

|---|---|

| Forecast Data Period | 2025 - 2029 |

| Historical Data Period | 2017 - 2023 |

| Market Size (2025) | USD 2.32 Billion |

| Market Size (2029) | USD 7.93 Billion |

| Growth Rate (2025 - 2029) | 35.92% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Fuel Cell Vehicles Market Analysis by Mordor Intelligence

The Asia-Pacific Fuel Cell Vehicles Market size is estimated at 2.32 billion USD in 2025, and is expected to reach 7.93 billion USD by 2029, growing at a CAGR of 35.92% during the forecast period (2025-2029).

The Asia-Pacific fuel cell vehicles industry is experiencing unprecedented transformation through strategic partnerships and technological innovations. Major automotive manufacturers are forming alliances to accelerate the development and commercialization of hydrogen fuel cell vehicles. In January 2023, Dongfeng Motor Corporation and Honda announced a collaborative effort to develop hydrogen fuel cell trucks, demonstrating the industry's commitment to sustainable transportation solutions. Toyota and Hino have established partnerships with major convenience store chains, including Seven-Eleven, FamilyMart, and Lawson, to introduce light-duty fuel cell electric trucks, creating a comprehensive ecosystem for widespread adoption. These collaborations are crucial in addressing technical challenges and reducing development costs while accelerating market penetration.

The regulatory landscape across the Asia-Pacific region continues to evolve, with governments implementing supportive policies and financial incentives to promote fuel cell vehicle adoption. South Korea has extended its purchase subsidy program for electric vehicles until 2024 for passenger cars and 2025 for buses and trucks, with vehicles priced below KRW 60 million eligible for full subsidies. This structured approach to incentivization has created a favorable environment for both manufacturers and consumers. Chinese state-backed initiatives are equally ambitious, with companies like Beiqi Foton Motor committing USD 2.6 billion to alternative energy vehicles, including fuel cell technology engines, with plans to deploy 200,000 new energy commercial vehicles by 2025.

Technological advancements in fuel cell technology systems are driving significant improvements in vehicle performance and efficiency. Hyundai Motor Group's commitment of USD 6.7 billion toward FCV development by 2030 exemplifies the industry's focus on innovation and scale. Manufacturers are achieving breakthroughs in fuel cell stack design, hydrogen storage systems, and overall vehicle architecture. These developments are particularly evident in the commercial vehicle sector, where fuel cell technology offers advantages in terms of range, payload capacity, and refueling time compared to battery-electric alternatives.

The expansion of hydrogen refueling infrastructure is progressing rapidly across the region, with governments and private sector players investing in refueling networks. Japanese automotive manufacturers are collaborating with energy companies to establish hydrogen supply chains and refueling stations, creating a sustainable ecosystem for hydrogen mobility. In China, energy companies are making substantial investments in hydrogen production and distribution networks, while South Korean authorities are implementing comprehensive hydrogen economy roadmaps. This coordinated approach to infrastructure development is essential for addressing one of the primary barriers to widespread hydrogen transportation adoption.

Asia-Pacific Fuel Cell Vehicles Market Trends and Insights

Asia-Pacific's auto loan interest rates reflected varying national economic strategies, with some countries emphasizing stimulation while others took a more conservative stance

- Over the past few years, there have been noticeable changes in these figures. Indonesia and India notably reduced their auto loan rates, signaling potential efforts to bolster the automotive sector in the face of fluctuating sales. Japan, adhering to its legacy, sustained its nominal rates, an indicator of its persistent ultra-loose monetary policy. Malaysia, after a sharp dip in 2021, seemed to regain its footing in 2022, hinting at an adaptive economic recalibration. New Zealand and the Philippines, meanwhile, navigated a descending path. Thailand, with a plunge in 2020, retraced some steps upward by 2022. Australia's journey was intriguing, with a steady climb each year, possibly indicating a blend of economic resilience and strategic divergence from its regional peers.

- During 2017-2023 period, Asia-Pacific showcased a panorama of fluctuating interest rates for auto loans. Indonesia stood out with the steepest rates oscillating between 10% and11%, clearly underlining its economic landscape. In stark contrast, Japan's rates remained consistently below 1%, reflecting its long-standing policy of low-interest rates to boost economic activity. Australia and New Zealand moved along a more stable trend with a slight increase by 2019. Meanwhile, the Philippines, though starting from a moderate base in 2017, marked a dramatic ascent, peaking over 7% in 2019. India maintained a steady rhythm, keeping within the 9-10% bracket, while Malaysia's course was slightly upward. Conversely, Thailand embraced a gentle downward slope.

The surging demand for electric vehicles (EVs) in Asia is prompting global automakers to introduce new offerings, thereby expanding the EV and battery pack market

- In response to the escalating demand for electric vehicles (EVs) in the Asia-Pacific region, numerous automakers are aligning their strategies to unveil innovative products tailored to this burgeoning market. One important instance is the announcement made by Skoda in January 2023, where it shared plans to introduce a cutting-edge electric SUV in India. This vehicle stands out due to its formidable 82-kWh battery, boasting an impressive range exceeding 500 kilometers on a singular charge. With its launch slated for late 2023, Skoda's move is emblematic of the broader trend sweeping across the region. Such introductions are poised to not only fuel the EV demand but also drive the proliferation of battery packs in various Asia-Pacific countries.

- As public transportation becomes increasingly integral to urban life in the Asia-Pacific, it is inspiring a new generation of manufacturers to debut novel, eco-friendly models. In a significant move in April 2022, the pioneering India-based startup, GreenCell Mobility, unveiled its electric mobility bus service brand, NueGo. GreenCell has plans to revolutionize intercity commutes by deploying 750 premium electric buses across three key regions in India, encompassing the South, North, and West. While the initial phase will witness the rollout of 250 buses across 24 cities, the long-term vision underscores the company's commitment to enhancing green public transportation. Such initiatives signal a promising surge in electric public transit solutions, setting the pace for broader adoption across Asia-Pacific in the coming years.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Countries like Australia, India, and Indonesia project a steady upward trajectory in GDP per capita, suggesting robust economic strategies and potential investment in the automotive industries

- The Asia-Pacific's diverse consumer spending trends on vehicle purchases not only reflect the region's evolving economic conditions but also highlight the shifting consumer preferences and vehicular market dynamics across countries

- From 2017 to 2030, the shared rides segment is poised for significant transformations, marked by a resilient rebound from the pandemic and a notable increase, largely driven by technology and sustainability

- The Asia-Pacific region's EV infrastructure has seen remarkable growth, with China leading the charge, India showing immense potential, and other nations steadily catching up, promising a robust EV future

- Asia-Pacific is witnessing a resurgence in the logistics performance index, driven by infrastructural developments and technological advancements

- Asia-Pacific's fuel prices have been influenced by global events, with recent rises due to economic recovery and demand resurgence and future trends leaning toward stabilization amid a transition to sustainable energy solutions

- Asia-Pacific displays a panorama of economic evolution: from the relentless pursuits of emerging economies to the recalibrations of established ones, painting a picture of resilience, adaptation, and ambition

- Asia-Pacific’s varied inflation rates reflect the diverse economic challenges and responses of each nation, from battling pandemic-induced fluctuations to aiming for future stability through strategic economic policies

- APAC's rapid electric vehicle demand and sales growth are driven by government initiatives and commercial vehicle electrification

- The demand for EVs in Asia-Pacific is fueled by falling battery prices

- The used car sales segment displays resilience with consistent growth trends, influenced by evolving consumer behaviors, economic dynamics, and regional developments

- Asia-Pacific is leading the charge in fuel cell vehicle production, with Japan and South Korea spearheading development through substantial OEM investments and robust government support

Segment Analysis: Vehicle Type

Buses Segment in Asia-Pacific Fuel Cell Vehicles Market

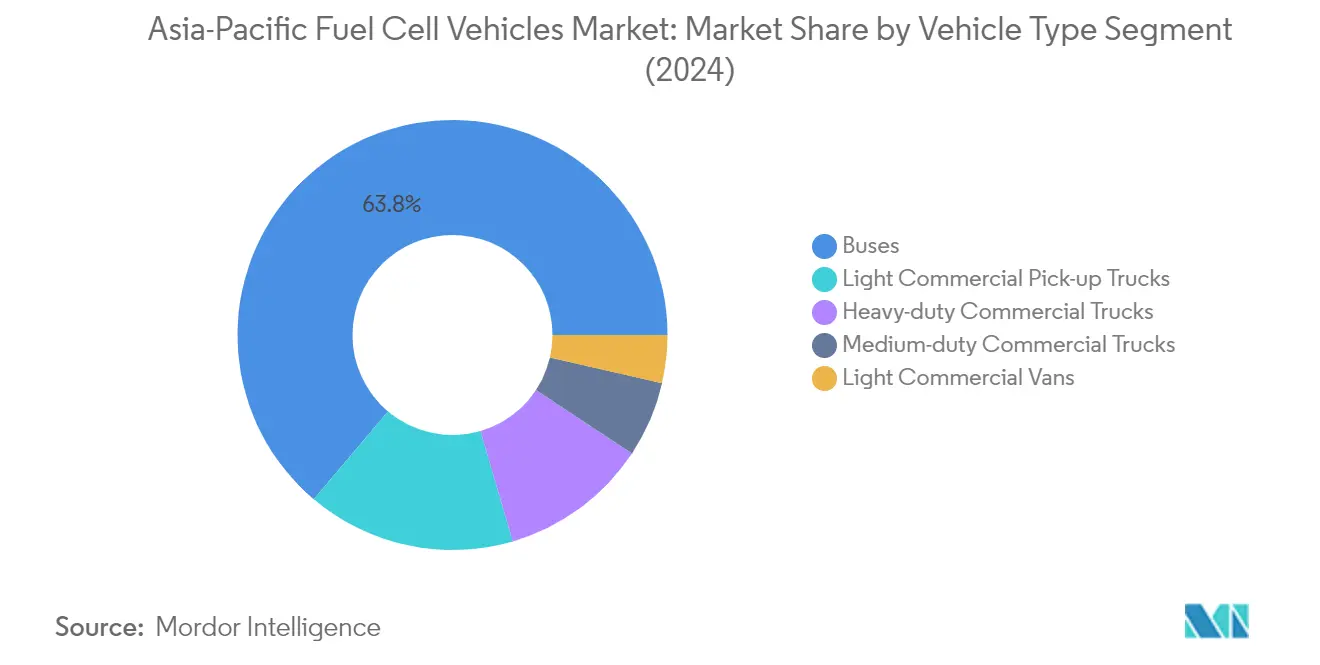

The fuel cell electric bus segment dominates the Asia-Pacific fuel cell vehicles market, commanding approximately 64% market share in 2024. This significant market position is driven by increasing government initiatives to decarbonize public transportation systems across major Asian cities. The segment's leadership is further strengthened by substantial investments in hydrogen fuel system development and the growing adoption of zero-emission buses by public transit authorities. Major metropolitan areas are increasingly transitioning their public transportation fleets to fuel cell electric buses, recognizing their advantages in terms of longer operating range and shorter refueling times compared to battery electric alternatives. The segment's dominance is also supported by favorable government policies and subsidies aimed at promoting clean energy transportation solutions in urban areas.

Medium-duty Commercial Trucks Segment in Asia-Pacific Fuel Cell Vehicles Market

The medium-duty commercial trucks segment is emerging as the fastest-growing segment in the Asia-Pacific fuel cell vehicles market, with a projected growth rate of approximately 56% during 2024-2029. This remarkable growth is attributed to the increasing adoption of fuel cell truck technology in urban logistics and regional distribution applications. The segment's expansion is driven by the growing demand for zero-emission vehicle delivery vehicles in metropolitan areas, coupled with stricter emission regulations in major Asian cities. Fleet operators are increasingly recognizing the advantages of fuel cell trucks in medium-duty applications, particularly their ability to combine zero emissions with operational flexibility and minimal downtime for refueling. The segment's growth is further supported by expanding hydrogen infrastructure and decreasing costs of fuel cell technology.

Remaining Segments in Vehicle Type

The remaining segments, including heavy-duty commercial trucks, light commercial pick-up trucks, and light commercial vans, each play distinct roles in shaping the Asia-Pacific fuel cell vehicles market. Heavy-duty commercial trucks are gaining traction in long-haul transportation and port operations, where the high energy density of hydrogen vehicle fuel cells provides a competitive advantage. Light commercial pick-up trucks are finding applications in various sectors, particularly in regions with developing hydrogen infrastructure. Light commercial vans are increasingly being adopted for last-mile delivery services in urban areas, where zero-emission zones are becoming more prevalent. These segments collectively contribute to the diverse application landscape of fuel cell technology in commercial transportation.

Asia-Pacific Fuel Cell Vehicles Market Geography Segment Analysis

Asia-Pacific Fuel Cell Vehicles Market in Japan

Japan continues to dominate the Asia-Pacific fuel cell vehicle market, commanding approximately 98% of the total market share in 2024. The country's leadership position is underpinned by its comprehensive hydrogen society strategy, which emphasizes hydrogen as a pivotal energy source for achieving carbon neutrality by 2050. Japan's success in the hydrogen fuel cell vehicle sector is driven by substantial government investments in hydrogen technology and infrastructure development. The country has implemented specific policies supporting FCV development and deployment, including significant subsidies for vehicle purchases and funding for hydrogen refueling station construction. Japanese automakers have established themselves as global leaders in hydrogen automotive technology, continuously innovating and improving vehicle performance while reducing costs. The nation's robust research and development ecosystem, coupled with strong collaboration between industry players and government agencies, has created a favorable environment for FCV advancement. Furthermore, Japan's strategic focus on developing a comprehensive hydrogen supply chain has helped address one of the key challenges facing FCV adoption - the availability of hydrogen fuel infrastructure.

Asia-Pacific Fuel Cell Vehicles Market in India

India's hydrogen fuel cell vehicle market is experiencing remarkable growth, with a projected CAGR of approximately 107% from 2024 to 2029. The country's aggressive push towards clean mobility solutions has created a conducive environment for FCV adoption. India's approach to hydrogen mobility development is characterized by a unique blend of government initiatives and private sector participation. The country has been actively developing its hydrogen ecosystem, with several pilot projects and demonstrations showcasing the potential of fuel cell vehicle technology in various transportation applications. Major automotive manufacturers are increasingly investing in FCV research and development facilities within India, recognizing the country's potential as a key market for hydrogen mobility solutions. The government's emphasis on reducing oil imports and achieving energy independence has led to supportive policies for alternative fuel technologies, including hydrogen fuel cells. Additionally, India's strong automotive manufacturing base and engineering expertise provide a solid foundation for localizing FCV production and reducing costs. The country's focus on developing green hydrogen production capabilities further strengthens its position in the FCV market.

Asia-Pacific Fuel Cell Vehicles Market in China

China's hydrogen fuel cell vehicle market demonstrates remarkable dynamism, supported by the country's comprehensive strategy for hydrogen mobility development. The nation's approach combines strong policy support with substantial industrial investment, creating a robust ecosystem for FCV growth. Chinese authorities have implemented various initiatives to promote hydrogen fuel cell technology, including subsidies for research and development, demonstration projects, and infrastructure development. The country's vast manufacturing capabilities and supply chain advantages have enabled rapid scaling of FCV production while reducing costs. Local governments across China have been actively supporting the deployment of fuel cell vehicles, particularly in public transportation and logistics applications. The nation's commitment to developing a world-class hydrogen energy industry has attracted significant investment from both domestic and international players. Furthermore, China's strategic focus on establishing hydrogen industrial clusters has created centers of excellence for FCV technology development and commercialization. The country's emphasis on developing indigenous intellectual property in fuel cell technology has led to numerous technological breakthroughs and innovations.

Asia-Pacific Fuel Cell Vehicles Market in Other Countries

The hydrogen fuel cell vehicle market in other Asia-Pacific countries, including South Korea, Australia, Indonesia, Malaysia, and Thailand, exhibits varying degrees of development and potential. These nations are actively formulating and implementing hydrogen strategies, recognizing the crucial role of hydrogen powertrain technology in their energy transition plans. Each country brings unique strengths to the regional FCV ecosystem - South Korea's advanced automotive manufacturing capabilities, Australia's abundant renewable energy resources for green hydrogen vehicle production, and Southeast Asian nations' growing focus on sustainable transportation solutions. These markets are characterized by increasing collaboration between government agencies, research institutions, and private sector players to advance FCV technology and infrastructure development. The diversity of approaches to FCV adoption across these countries contributes to the overall robustness of the Asia-Pacific fuel cell vehicle market. Their collective efforts in developing hydrogen infrastructure, implementing supportive policies, and fostering innovation create a dynamic environment for the growth of the regional FCV industry.

Competitive Landscape

Top Companies in Asia-Pacific Fuel Cell Vehicles Market

The leading companies in the Asia-Pacific fuel cell vehicles market are demonstrating a strong commitment to technological advancement and market expansion through various strategic initiatives. Companies are heavily investing in research and development to enhance fuel cell technology efficiency, improve vehicle performance, and reduce production costs. Strategic partnerships and collaborations have become increasingly common, particularly in developing hydrogen refueling infrastructure and sharing technological expertise. Product innovation remains a key focus, with companies introducing new hydrogen fuel cell powertrain vehicle models across different segments, from passenger cars to commercial vehicles. Operational agility is demonstrated through flexible manufacturing capabilities and adaptable supply chain networks, while geographic expansion is pursued through strategic market entry and localization strategies. Companies are also actively participating in government-supported programs and initiatives to accelerate the adoption of fuel cell vehicles and develop supporting infrastructure.

Consolidated Market Led By Asian Conglomerates

The Asia-Pacific fuel cell vehicles market exhibits a highly consolidated structure dominated by established automotive conglomerates, particularly from Japan and South Korea. These major players leverage their extensive manufacturing capabilities, established distribution networks, and strong brand presence to maintain their market positions. The market is characterized by significant barriers to entry, including high technological requirements, substantial capital investments, and the need for specialized expertise in proton exchange membrane fuel cell technology. Local players, while present in specific markets, typically operate through partnerships or joint ventures with major automotive manufacturers to access technology and market expertise.

The market has witnessed strategic consolidation through various forms of collaboration rather than traditional mergers and acquisitions. Companies are forming strategic alliances and joint ventures to share development costs, reduce risks, and accelerate technological advancement. These partnerships often extend beyond automotive manufacturers to include energy companies, infrastructure providers, and technology firms, creating an interconnected ecosystem that supports the growth of the fuel cell vehicle market. This collaborative approach has become increasingly important as companies seek to establish comprehensive hydrogen mobility solutions.

Innovation and Infrastructure Drive Future Success

Success in the Asia-Pacific fuel cell vehicles market increasingly depends on companies' ability to balance technological innovation with cost optimization. Incumbent players must focus on scaling up production to achieve economies of scale while continuously investing in research and development to maintain their technological edge. Building strong partnerships with hydrogen infrastructure providers and government agencies is crucial for expanding the refueling network. Companies also need to develop comprehensive service networks and after-sales support to enhance customer confidence and address maintenance concerns. Additionally, establishing robust supply chains for critical components and materials will be essential for maintaining competitive advantages.

For emerging players and contenders, differentiation through specialized applications or market segments offers a viable path to market entry. Success will require developing strategic partnerships with established players or technology providers while focusing on specific regional markets or vehicle segments where competition is less intense. Companies must also closely monitor and adapt to evolving regulatory frameworks, particularly regarding safety standards and environmental regulations. The ability to offer competitive financing solutions and innovative business models, such as hydrogen mobility as a service, will become increasingly important for gaining market share. Furthermore, investing in customer education and awareness programs will be crucial for expanding market acceptance and addressing concerns about fuel cell technology.

Asia-Pacific Fuel Cell Vehicles Industry Leaders

Daimler AG (Mercedes-Benz AG)

Honda Motor Co. Ltd.

Hyundai Motor Company

Nissan Motor Co. Ltd.

Toyota Motor Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2023: Honda's next-generation fuel cell system made its Chinese debut. It is mainly applied to fuel cell electric vehicles, commercial vehicles, fixed power supply, and engineering machinery.

- May 2023: Dongfeng Nissan Venucia unveiled a new technology matrix. The company will continue to adhere to the three technical routes of battery electric, plug-in hybrid, and hydrogen energy in parallel to build DD-i super hybrid technology and the V–π platform and actively develop hydrogen energy technologies for FCVs (fuel cell vehicles).

- April 2023: DFM launched its development in the new energy field in 2021. In terms of platform development, it built three electrified platforms. In terms of technology innovation, it adheres to the parallel technical routes of PHREV, battery electric, and hydrogen energy. In terms of hydrogen power R&D, it established the Qingzhou technology brand, covering power from 20 kW to 300 kW and meeting the needs of various passenger and commercial vehicles.

Asia-Pacific Fuel Cell Vehicles Market Report Scope

Commercial Vehicles are covered as segments by Vehicle Type. Australia, China, India, Indonesia, Japan, Malaysia, South Korea, Thailand, Rest-of-APAC are covered as segments by Country.Vehicle Type

| Commercial Vehicles | Buses |

| Heavy-duty Commercial Trucks | |

| Light Commercial Pick-up Trucks | |

| Light Commercial Vans | |

| Medium-duty Commercial Trucks |

Country

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| South Korea |

| Thailand |

| Rest-of-APAC |

| Vehicle Type | Commercial Vehicles | Buses |

| Heavy-duty Commercial Trucks | ||

| Light Commercial Pick-up Trucks | ||

| Light Commercial Vans | ||

| Medium-duty Commercial Trucks | ||

| Country | Australia | |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| South Korea | ||

| Thailand | ||

| Rest-of-APAC |

Market Definition

- Vehicle Type - The category includes passenger cars and commercial vehicles.

- Vehicle Body Type - Under Passenger Cars, the category includes Hatchbacks, Sedans, Sports Utility Vehicles, and Multi-purpose Vehicles; for Commercial Vehicles, it covers Light Commercial Pick-up Trucks, Light Commercial Vans, Medium-duty Commercial Trucks, Heavy-duty Commercial Trucks, and Medium and Heavy Duty Buses.

- Fuel Category - The category exclusively covers Fuel Cell Electric Vehicles (FCEV).

| Keyword | Definition |

|---|---|

| Electric Vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| BEV | A BEV relies completely on a battery and a motor for propulsion. The battery in the vehicle must be charged by plugging it into an outlet or public charging station. BEVs do not have an ICE and hence are pollution-free. They have a low cost of operation and reduced engine noise as compared to conventional fuel engines. However, they have a shorter range and higher prices than their equivalent gasoline models. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all-electric vehicles as well as plug-in hybrids. |

| Plug-in Hybrid EV | A vehicle that can be powered either by an ICE or an electric motor. In contrast to normal hybrid EVs, they can be charged externally. |

| Internal combustion engine | An engine in which the burning of fuels occurs in a confined space called a combustion chamber. Usually run with gasoline/petrol or diesel. |

| Hybrid EV | A vehicle powered by an ICE in combination with one or more electric motors that use energy stored in batteries. These are continually recharged with power from the ICE and regenerative braking. |

| Commercial Vehicles | Commercial vehicles are motorized road vehicles designed for transporting people or goods. The category includes light commercial vehicles (LCVs) and medium and heavy-duty vehicles (M&HCV). |

| Passenger Vehicles | Passenger cars are electric motor– or engine-driven vehicles with at least four wheels. These vehicles are used for the transport of passengers and comprise no more than eight seats in addition to the driver’s seat. |

| Light Commercial Vehicles | Commercial vehicles that weigh less than 6,000 lb (Class 1) and in the range of 6,001–10,000 lb (Class 2) are covered under this category. |

| M&HDT | Commercial vehicles that weigh in the range of 10,001–14,000 lb (Class 3), 14,001–16,000 lb (Class 4), 16,001–19,500 lb (Class 5), 19,501–26,000 lb (Class 6), 26,001–33,000 lb (Class 7) and above 33,001 lb (Class 8) are covered under this category. |

| Bus | A mode of transportation that typically refers to a large vehicle designed to carry passengers over long distances. This includes transit bus, school bus, shuttle bus, and trolleybuses. |

| Diesel | It includes vehicles that use diesel as their primary fuel. A diesel engine vehicle have a compression-ignited injection system rather than the spark-ignited system used by most gasoline vehicles. In such vehicles, fuel is injected into the combustion chamber and ignited by the high temperature achieved when gas is greatly compressed. |

| Gasoline | It includes vehicles that use gas/petrol as their primary fuel. A gasoline car typically uses a spark-ignited internal combustion engine. In such vehicles, fuel is injected into either the intake manifold or the combustion chamber, where it is combined with air, and the air/fuel mixture is ignited by the spark from a spark plug. |

| LPG | It includes vehicles that use LPG as their primary fuel. Both dedicated and bi-fuel LPG vehicles are considered under the scope of the study. |

| CNG | It includes vehicles that use CNG as their primary fuel. These are vehicles that operate like gasoline-powered vehicles with spark-ignited internal combustion engines. |

| HEV | All the electric vehicles that use batteries and an internal combustion engine (ICE) as their primary source for propulsion are considered under this category. HEVs generally use a diesel-electric powertrain and are also known as hybrid diesel-electric vehicles. An HEV converts the vehicle momentum (kinetic energy) into electricity that recharges the battery when the vehicle slows down or stops. The battery of HEV cannot be charged using plug-in devices. |

| PHEV | PHEVs are powered by a battery as well as an ICE. The battery can be charged through either regenerative breaking using the ICE or by plugging into some external charging source. PHEVs have a better range than BEVs but are comparatively less eco-friendly. |

| Hatchback | These are compact-sized cars with a hatch-type door provided at the rear end. |

| Sedan | These are usually two- or four-door passenger cars, with a separate area provided at the rear end for luggage. |

| SUV | Popularly known as SUVs, these cars come with four-wheel drive, and usually have high ground clearance. These cars can also be used as off-road vehicles. |

| MPV | These are multi-purpose vehicles (also called minivans) designed to carry a larger number of passengers. They carry between five and seven people and have room for luggage too. They are usually taller than the average family saloon car, to provide greater headroom and ease of access, and they are usually front-wheel drive. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the sales volume with their respective average selling price (ASP). While estimating ASP factors like average inflation, market demand shift, manufacturing cost, technological advancement, and varying consumer preference, among others have been taken into account.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.