Anti-microbial Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

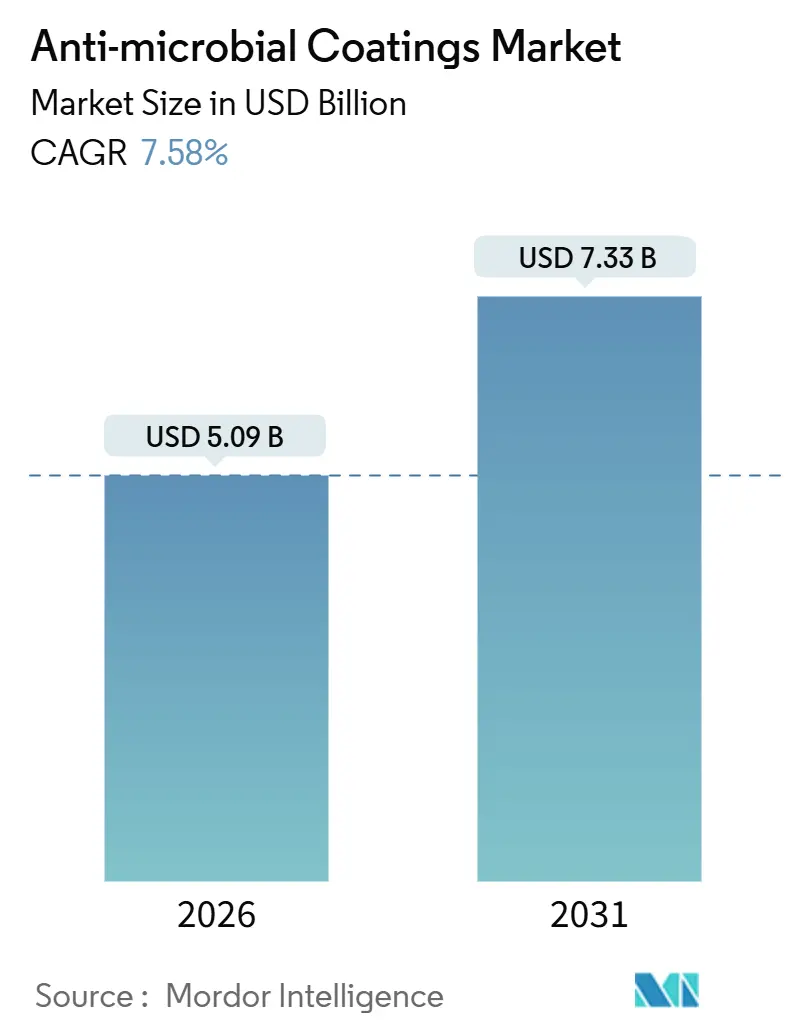

| Market Size (2026) | USD 5.09 Billion |

| Market Size (2031) | USD 7.33 Billion |

| Growth Rate (2026 - 2031) | 7.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-microbial Coatings Market Analysis by Mordor Intelligence

The Anti-microbial Coatings Market size is estimated at USD 5.09 billion in 2026, and is expected to reach USD 7.33 billion by 2031, at a CAGR of 7.58% during the forecast period (2026-2031). Wide-ranging mandates that target healthcare-associated infections, the build-out of cold-chain infrastructure across emerging Asia, and tightening VOC caps in the United States and European Union underpin this trajectory. Silver-based chemistries presently dominate procurement, yet regulatory and end-user interest in bio-derived actives is steering formulators toward organic alternatives that avoid metal-ion leaching concerns. Liquids remain the preferred coating form, though nano-engineered treatments are scaling quickly as electronics OEMs demand thin films that preserve touch-interface performance.

Key Report Takeaways

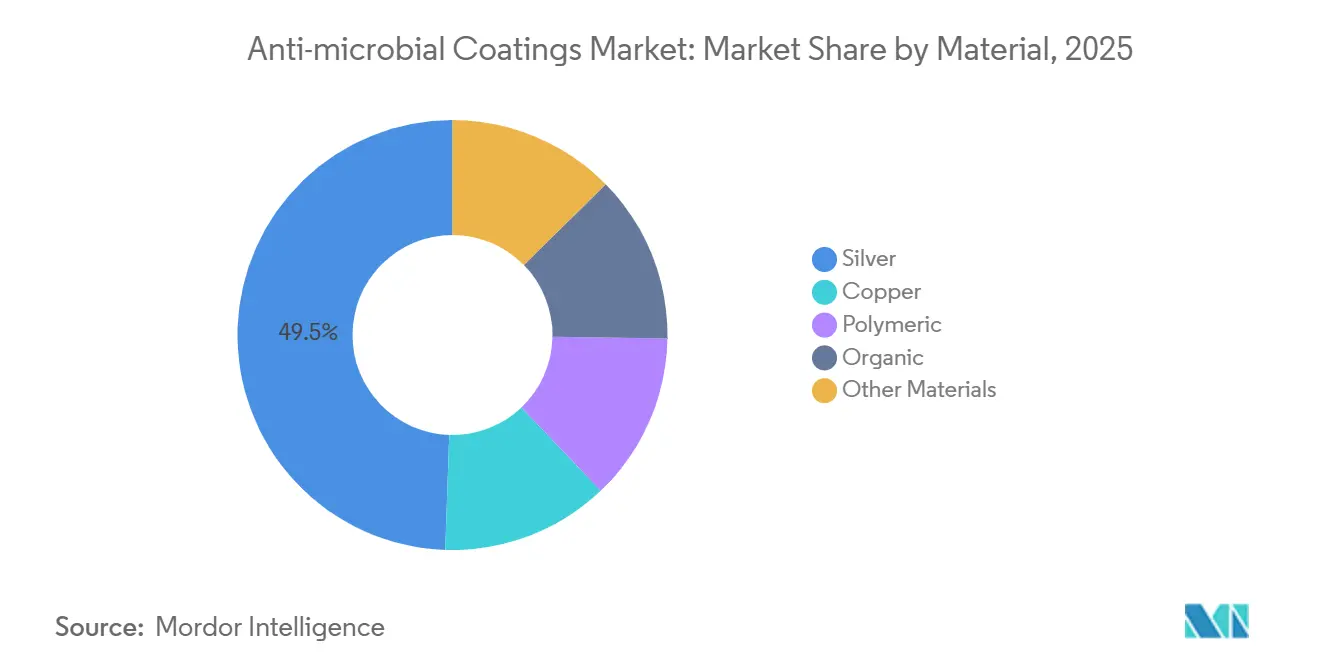

- By material, silver captured 49.45% of the anti-microbial coatings market share in 2025; organics are forecast to expand at a 9.72% CAGR through 2031.

- By coating form, Liquid (Solvent- and Water-borne) held 45.71% revenue share in 2025, while others are set to post an 8.84% CAGR to 2031.

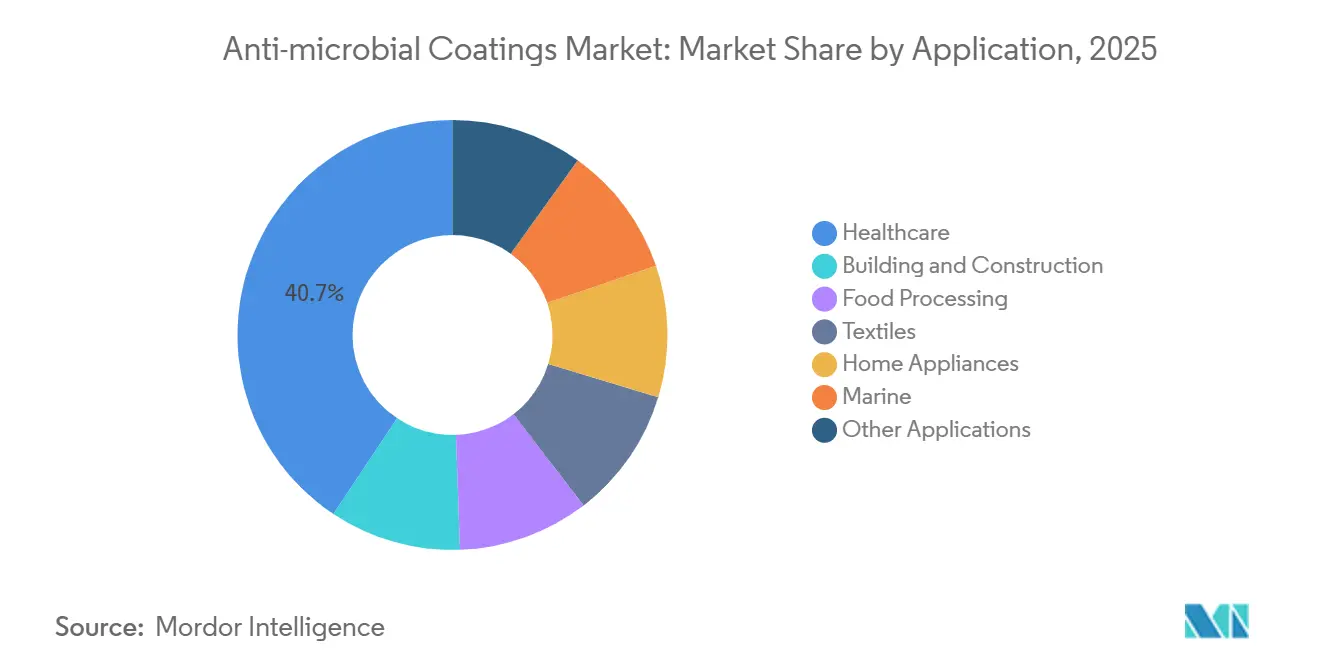

- By application, healthcare environments accounted for 40.66% of the anti-microbial coatings market size in 2025; building and construction is projected to advance at a 7.94% CAGR through 2031.

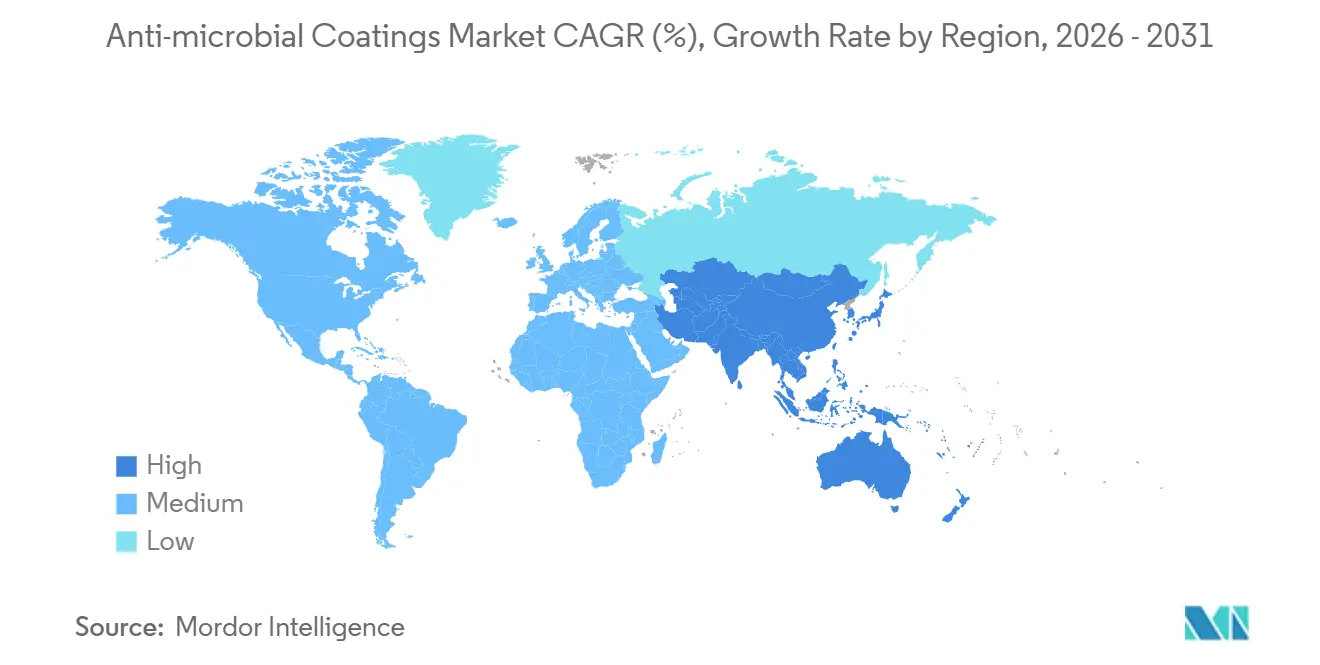

- By geography, North America led with 45.27% revenue share in 2025; Asia-Pacific is poised for a 9.08% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Anti-microbial Coatings Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HAI-reduction programs accelerating hospital surface coating uptake in North America | +1.8% | North America, spillover to Western Europe | Medium term (2-4 years) |

| Cold-chain expansion in India & ASEAN propelling antimicrobial powder demand | +1.5% | India, Indonesia, Vietnam, Thailand | Long term (≥ 4 years) |

| Touch-interface hygiene requirements driving electronics OEM coating integration | +1.2% | Global, led by East Asia | Short term (≤ 2 years) |

| VOC-cap compliance shifting demand toward water-borne & nano formulations | +1.4% | North America & EU, early adoption in Japan | Medium term (2-4 years) |

| Smart self-sanitizing public-transit surfaces linked to micro-mobility adoption | +0.9% | Urban centers in North America, EU, select APAC cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

HAI-Reduction Programs Accelerating Hospital Surface Coating Uptake in North America

The Centers for Disease Control and Prevention reported in 2025 that environmental surfaces contribute up to 40% of pathogen transmission in acute-care settings[1]Centers for Disease Control and Prevention, “National Action Plan to Prevent HAIs,” cdc.gov. Updated CDC guidance now recommends EPA-registered antimicrobial coatings on bed rails, IV poles, and nurse call buttons as a Tier 2 intervention, elevating permanent surface engineering alongside hand hygiene. The Joint Commission incorporated coating audits into its 2025 accreditation surveys, pushing lagging facilities toward retrofits. Reimbursement penalties of up to 3% for hospitals with above-median HAI rates create a direct financial incentive to invest in durable antimicrobial infrastructure. Suppliers have responded with silver-ion and copper-alloy coatings that maintain efficacy for up to five years, repositioning antimicrobial coatings as a capital asset instead of a consumable expense.

Cold-Chain Expansion in India & ASEAN Propelling Antimicrobial Powder Demand

India’s National Cold Chain Mission earmarked INR 40 billion (USD 480 million) in 2024 and mandates antimicrobial powder coatings on refrigerated warehouses and transport containers[2]Ministry of Food Processing Industries, “Cold Chain Project Guidelines,” mofpi.gov.in. Revised Good Distribution Practice guidelines, effective January 2025, require ISO 21702-certified antiviral coatings in vaccine storage, following cold-chain failures during the COVID-19 campaign. ASEAN regulators mirror the move: Indonesia’s BPOM Regulation No. 12/2025 stipulates antimicrobial treatment in pharmaceutical hubs, and Vietnam allocated USD 120 million to upgrade seafood cold chains that serve EU customers. Electrostatic powder application ensures uniform coverage on corrugated metal and minimizes VOC emissions, aligning with occupational-safety requirements.

Touch-Interface Hygiene Requirements Driving Electronics OEM Coating Integration

Post-pandemic hygiene awareness has led consumer-electronics brands to embed antimicrobial coatings into touchscreens, keyboards, and wearables. The IEC 62368-1 standard now contains an antimicrobial annex, giving OEMs a compliance path for devices used in healthcare and food-service settings. Apple disclosed in 2025 that 38% of its component suppliers apply silver-ion or quaternary-ammonium coatings, up from 12% in 2023. Samsung filed 14 patents between 2024 and 2025 covering nano-silver deposition that preserves touchscreen capacitance. The FDA issued draft guidance in June 2025 recommending antimicrobial coatings on reusable medical devices with touchscreen interfaces.

VOC-Cap Compliance Shifting Demand Toward Water-Borne & Nano Formulations

A US EPA rule effective January 2025 caps VOC content at 250 g/L for architectural coatings and 420 g/L for industrial maintenance products. The EU Industrial Emissions Directive pushes limits even lower in enclosed spaces, effectively banning solvent-borne formulations unless vapor-recovery systems are installed. Water-borne antimicrobial coatings now account for 62% of North American product launches, up from 41% in 2023. Sherwin-Williams introduced a zero-VOC antimicrobial latex in March 2025 that achieved GREENGUARD Gold certification for low chemical emissions. Scale economies and optimized dispersion stabilizers are narrowing the cost premium of water-borne and nano-engineered products.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of technological awareness in developing & under-developed nations | -1.1% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Emission-toxicity concerns for active ingredients | -0.8% | Global, most acute in the EU | Medium term (2-4 years) |

| Chilean copper-ore supply strikes inflating raw-material costs | -0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of Technological Awareness in Developing & Under-Developed Nations

World Health Organization data show that only 15% of public hospitals in low-income countries reference durable surface treatments in infection-control protocols, compared with 78% in high-income economies. Limited familiarity with ISO 22196 and ISO 21702 standards leaves procurement officials without benchmarks to assess coating claims. Training gaps compound the issue; only 22% of facility managers in sub-Saharan Africa had formal education on antimicrobial coatings, versus 61% in North America. Price sensitivity also restrains uptake, as antimicrobial coatings can command a 30-50% premium over conventional paints. Suppliers are piloting demonstration projects with multilateral lenders to showcase efficacy and build local credibility.

Emission-Toxicity Concerns for Active Ingredients

The European Chemicals Agency reclassified several quaternary ammonium compounds as substances of very great concern in 2025, forcing manufacturers to submit extensive environmental fate studies. The US EPA’s Safer Choice program now excludes triclosan and triclocarban, limiting their use in green-building projects. Solvent-borne coatings emit formaldehyde and benzene derivatives that trigger occupational-safety restrictions. Public sentiment mirrors regulatory action; 54% of Western European consumers surveyed by Nielsen in 2025 said they avoid products labeled as containing “chemical antimicrobials”.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Silver Dominance Challenged by Organic Surge

Silver retained the leading 49.45% revenue share in 2025, underpinned by broad-spectrum efficacy and a regulatory track record that simplifies product approval. Hospitals prefer silver-based coatings that demonstrate multi-year performance, which helps reduce total lifecycle costs. Organic actives, quaternary ammonium, chitosan, and essential-oil derivatives are growing at 9.72% annually through 2031, capturing share in applications that prioritize minimal metal leaching. Copper formulations face input-cost volatility linked to Chilean supply disruptions, driving producers toward polymeric matrices that cut metal usage. Graphene oxide, photocatalytic titanium dioxide, and other emerging materials remain niche but attract sustained R&D investment from suppliers seeking performance at lower cost or toxicity.

Rising ecotoxicity scrutiny has pushed formulators to decouple efficacy from metal loading. Polymer-encapsulated biocides extend release kinetics, allowing a 30-40% reduction in active-ingredient use. Hybrid approaches such as graphene–silver composites target the same antimicrobial log-reduction while cutting silver content by up to 60%, making them attractive where end-users face budget constraints or green-building criteria. As bio-based options scale, competitive pricing is likely to narrow the historical premium of silver-ion coatings.

By Coating Form: Nano-Engineered Treatments Outpace Liquids

Liquid coatings, water-borne and solvent-borne combined, held 45.71% of revenue in 2025, favored for brush and roller application during healthcare and commercial-building retrofits. Water-borne systems align with VOC caps, whereas solvent-borne liquids maintain a foothold in marine and heavy-industry settings where surface preparation is inconsistent. Electrostatic powder coatings are expanding in cold-chain logistics and home appliances because they deliver uniform film thickness and low VOC emissions.

Others (Nano-Engineered Sprays and Films and Surface Modification Treatments) achieved the fastest 8.84% CAGR forecast, addressing the electronics sector’s need for sub-micron coatings that do not impair touch sensitivity. Surface-modification treatments such as plasma polymerization are gaining ground in medical devices that undergo autoclave sterilization. The antimicrobial coatings market share of nano treatments will continue to rise as mass-production techniques drive down unit costs and as regulators favor solvent-free processes.

By Application: Building & Construction Acceleration Reshapes Demand

Healthcare generated 40.66% of revenue in 2025, led by hospital surface retrofits triggered by stricter accreditation audits. Medical device coatings command high margins but face lengthy FDA review. Building & construction is the fastest-growing application at a 7.94% CAGR, stimulated by HVAC mandates under ASHRAE Standard 188 that target biofilm prevention in air-handling components. Recent updates to US building codes now reference antimicrobial treatments in evaporator coils and drain pans.

Food-processing facilities are adopting antimicrobial floor and wall systems to comply with the FDA Food Safety Modernization Act environmental-monitoring rules. Textile and marine applications round out demand, with maritime coatings shifting to silicone-based foul-release systems following the International Maritime Organization’s cybutryne ban. Home-appliance manufacturers leverage coatings for product differentiation; refrigerator interiors and washing-machine drums coated with silver-ion systems claim enhanced hygiene as a key selling point.

Geography Analysis

North America captured 45.27% of 2025 revenue, supported by CDC guidance that elevated antimicrobial coatings in infection-control protocols and by EPA VOC regulations that accelerate water-borne adoption. Canada follows a similar path, permitting antimicrobial claims on reusable equipment surfaces, while Mexico retrofits food-processing plants to preserve US export eligibility. Zero-VOC formulations are quickly becoming the standard in healthcare and education tenders, favoring suppliers with advanced water-borne portfolios.

Asia-Pacific is the highest-growth region at a 9.08% CAGR, driven by India’s National Cold Chain Mission, China’s aggressive hospital-construction pipeline, and Korea’s electronics OEM integration. India targets a 50% vaccine spoilage reduction by 2028 through mandatory antimicrobial coatings in refrigerated logistics. China’s 14th Five-Year Plan schedules 1,400 new hospitals that must meet infection-control specifications, including coated high-touch surfaces. South Korea’s supplier code of conduct for electronics components now mandates ISO 22196 certification, accelerating standardization across the value chain.

Europe’s market is shaped by strict Biocidal Products Regulation oversight and VOC caps that encourage bio-based and water-borne solutions. Germany recommends antimicrobial coatings in transit and education infrastructure, while the United Kingdom’s National Health Service mandates ISO 22196 retesting every 18 months. Food-processing adoption in France and marine transitions in Italy reflect broader EU environmental priorities. South America and Middle East-Africa remain nascent but show isolated growth pockets tied to hospital construction programs in Brazil and Saudi Arabia.

Competitive Landscape

The Anti-microbial Coatings Market is moderately concentrated. Incumbents defend hospital and marine niches through proprietary formulations registered with the EPA and equivalent bodies, yet face margin pressure from innovators such as BioCote and Microban that license ion-exchange technologies to OEMs. Disruptors like Novapura leverage grape-seed polyphenols to sidestep substance-of-very-high-concern classification, resonating with green-building specifiers. Vertical integration strategies, such as Lonza’s acquisition of a silver-nanoparticle producer, help secure feedstock and lower costs. Toll-manufacturing partnerships allow Asian suppliers to localize production in North America and Europe to meet public procurement origin requirements.

Anti-microbial Coatings Industry Leaders

Akzo Nobel N.V.

PPG Industries, Inc.

The Sherwin-Williams Company

3M

Axalta Coating Systems, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Engineers at the University of California, San Diego, unveiled a spray-on antibacterial coating. This solution can be directly applied to plant leaves, bolstering their defenses against harmful bacterial infections and enhancing their resilience to drought.

- June 2024: NEI Corporation unveiled NANOMYTE AM-100EC, a cutting-edge micron-thick coating. This innovative coating not only offers easy-to-clean features but also boasts antimicrobial properties, making it suitable for diverse surfaces. Notably, it adheres robustly to various materials, such as plastics, metals, and ceramics, frequently found in high-touch applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the antimicrobial coatings market as the annual value generated by formulated surface coatings, liquid, powder, or thin-film, that incorporate active or passive agents able to suppress or eliminate bacteria, fungi, or viruses on treated substrates in healthcare, construction, consumer, marine, food-processing, and other industrial environments.

Scope exclusion: Adhesives, post-application disinfectant sprays, and standalone antimicrobial additives sold for in-house compounding are not included.

Segmentation Overview

- By Material

- Silver

- Copper

- Polymeric

- Organic

- Other Materials

- By Coating Form

- Powder

- Liquid (Solvent- and Water-borne)

- Others (Nano-Engineered Sprays and Films, Surface Modification Treatments)

- By Application

- Building and Construction

- Food Processing

- Textiles

- Home Appliances

- Healthcare

- Marine

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed coating formulators, infection-control officers, HVAC installers, and building specifiers across North America, Europe, and Asia-Pacific. Discussions explored average selling prices, silver loading levels, regulatory cost pass-throughs, and adoption barriers, helping us refine penetration assumptions and validate demand inflection points revealed by desk work.

Desk Research

We began with publicly available sources such as the CDC's National Healthcare Safety Network on hospital-acquired infections, Eurostat's construction output series, UN Comtrade trade codes for HS 3208/3209, and US EPA antimicrobial registration lists. Industry association white papers, including the American Coatings Association and the European Powder Coatings Federation, and peer-reviewed journals supplied efficacy and cost benchmarks. Company 10-Ks and investor decks clarified revenue splits, which were further checked in D&B Hoovers. These illustrative references are a subset of the broader secondary corpus consulted throughout the project.

Market-Sizing & Forecasting

A top-down consumption model converts production volumes of architectural paints, medical devices, HVAC units, and high-touch fixtures into an addressable surface pool, to be further filtered through antimicrobial penetration rates derived from interviews. Bottom-up checks, sampled ASP multiplied by volume at key distributors, are layered in to calibrate totals. Core variables include silver price trends, new hospital bed additions, HVAC replacement cycles, global floor-space completions, and surgical device shipments. Multivariate regression, enriched with scenario analysis for raw-material volatility, projects demand through 2030 while gap-handling flags segments with thin data and applies confidence ranges approved by senior reviewers.

Data Validation & Update Cycle

Outputs pass anomaly screens, variance checks against external macro indicators, and a dual-analyst review before sign-off. Reports refresh every twelve months, with interim updates triggered by material regulatory or supply-chain shifts. A final sanity pass is completed immediately prior to client delivery.

Why Our Anti-microbial Coatings Baseline Earns Trust

Published estimates often diverge because firms adopt different product scopes, geographic roll-ups, price points, and refresh cadences.

Key gap drivers include whether surface-modification films and service revenues are folded into the total, the aggressiveness of penetration curves in healthcare, treatment of currency inflation, and the frequency of model recalibration.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.74 B (2025) | Mordor Intelligence | - |

| USD 12.85 B (2024) | Global Consultancy A | Combines antimicrobial films and additive masterbatches, inflating base value |

| USD 4.6 B (2023) | Trade Journal B | Earlier base year and excludes Asia's building segment |

| USD 3.31 B (2025) | Regional Consultancy C | Relies on limited OEM survey, omits medical-device coatings |

These comparisons show that while other publishers swing wide, Mordor's disciplined scope selection, mixed-method modeling, and annual update cycle deliver a balanced, transparent baseline that decision-makers can confidently rely on.

Key Questions Answered in the Report

What is the projected value of the antimicrobial coatings market in 2031?

What is the projected value of the antimicrobial coatings market in 2031?

Which region is expected to grow the fastest over the next five years?

Which region is expected to grow the fastest over the next five years?

Which material currently holds the largest share of global revenue?

Which material currently holds the largest share of global revenue?

Why are nano-engineered coatings gaining popularity in consumer electronics?

Why are nano-engineered coatings gaining popularity in consumer electronics?

How are regulatory VOC limits shaping formulation choices?

How are regulatory VOC limits shaping formulation choices?

Page last updated on: