Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

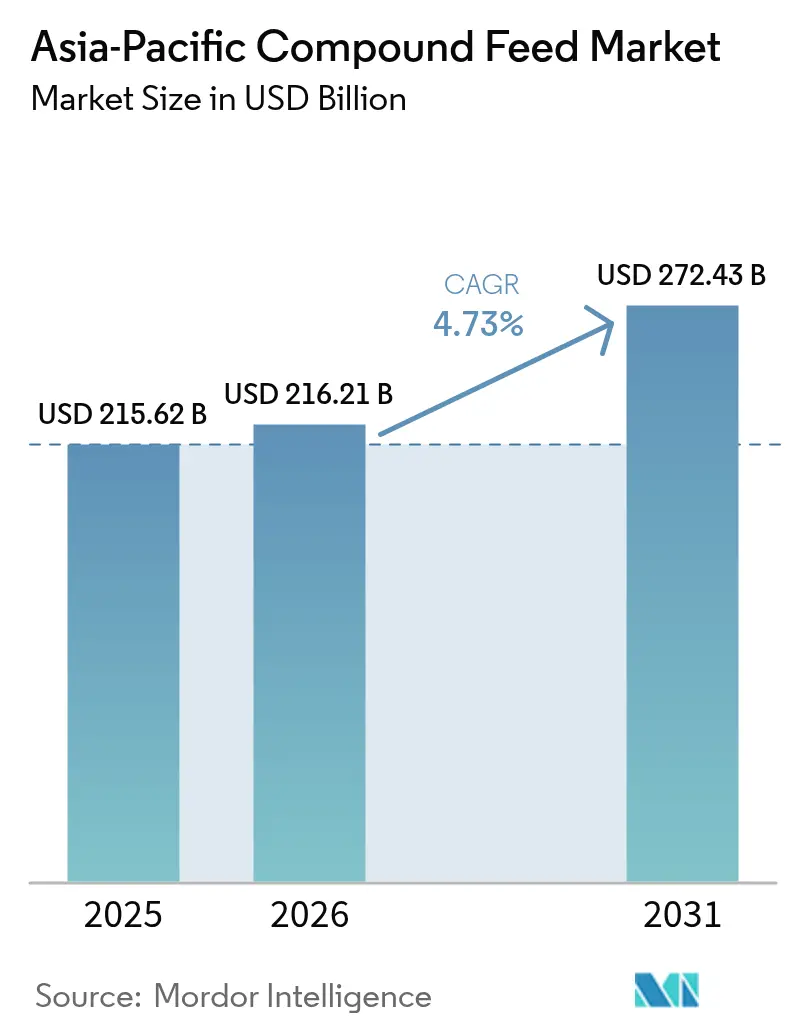

| Base Year Market Size (2025) | USD 215.62 Billion |

| Market Size (2026) | USD 216.21 Billion |

| Market Size (2031) | USD 272.43 Billion |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

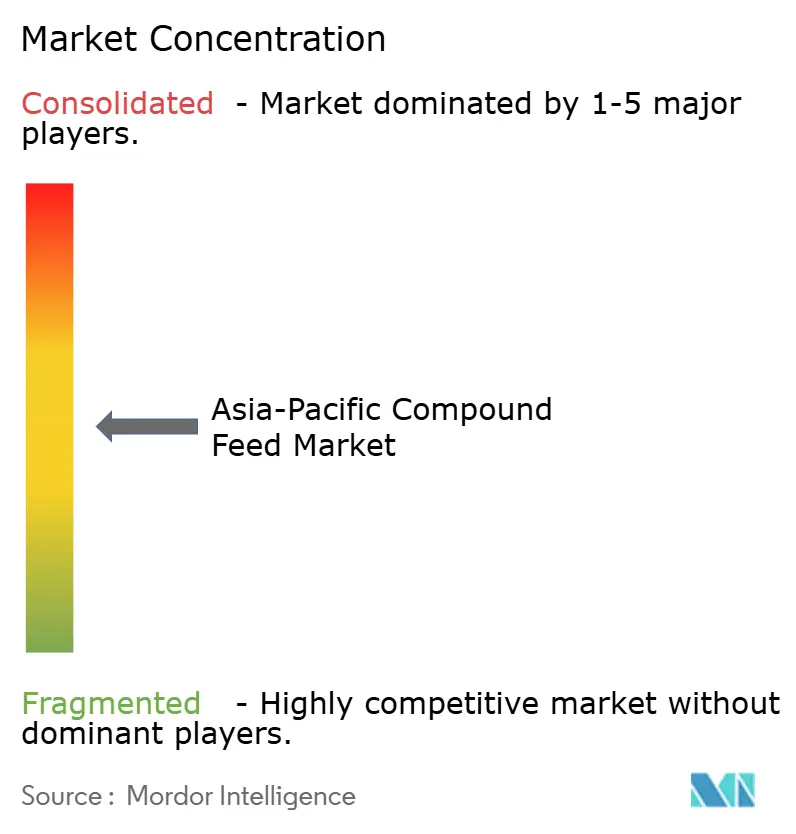

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Compound Feed Market Analysis by Mordor Intelligence

The Asia-Pacific compound feed market size was valued at USD 215.62 billion in 2025 and is estimated to grow from USD 216.21 billion in 2026 to reach USD 272.43 billion by 2031, growing at a 4.73% CAGR over 2026-2031. Rising household incomes across tier-2 and tier-3 cities, increased enforcement against antibiotic growth promoters, and swift adoption of precision nutrition platforms are reshaping product formulation and procurement behavior. Cereals still underpin rations, yet multi-enzyme premixes and probiotic blends are spreading quickly as mills seek to offset higher raw-material costs following the 2024 corn price spike. Digital trade on Alibaba and JD portals is compressing distributor margins while shortening lead times for lysine and vitamin shipments into Indonesia and the Philippines. Meanwhile, government incentives for recirculating aquaculture in Vietnam and offshore cage systems in China are accelerating demand for nutrient-dense aquatic pellets.

Key Report Takeaways

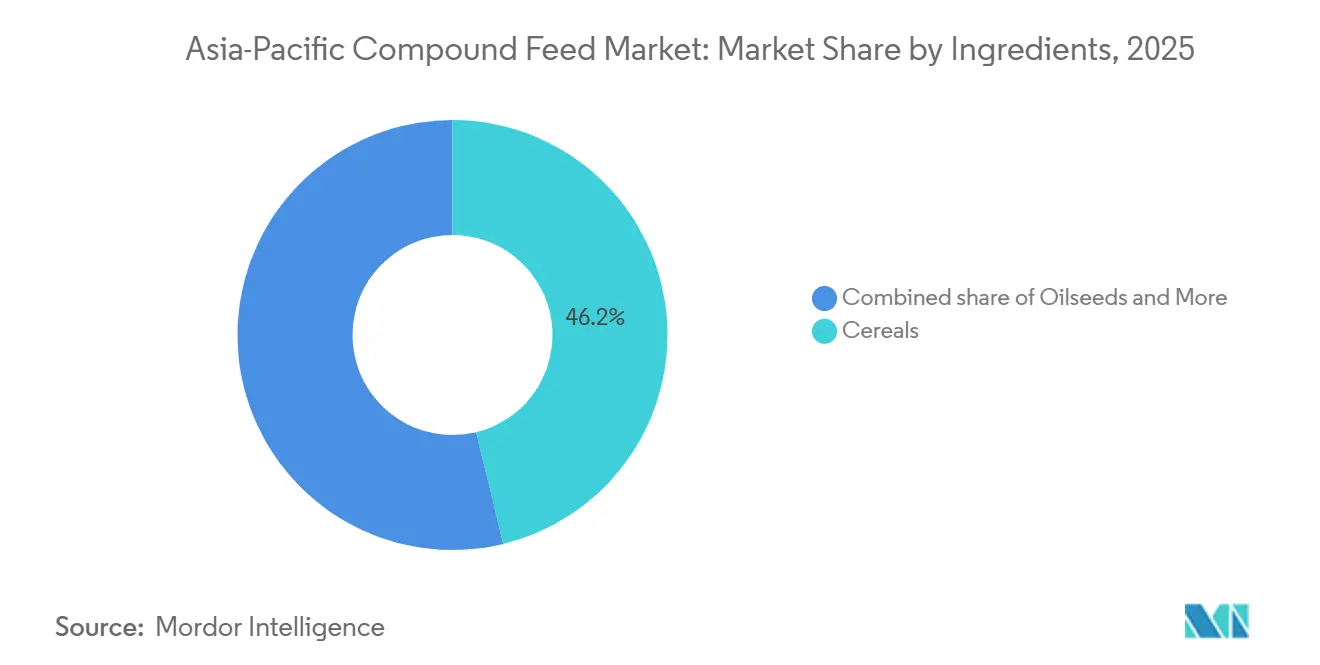

- By ingredients, cereals commanded 46.2% of the Asia-Pacific compound feed market share in 2025, while supplements are projected to grow at a 5.2% CAGR to 2031.

- By supplements, amino acids accounted for 34% of the Asia-Pacific compound feed market share in 2025, and probiotics are projected to grow at a 4.5% CAGR to 2031.

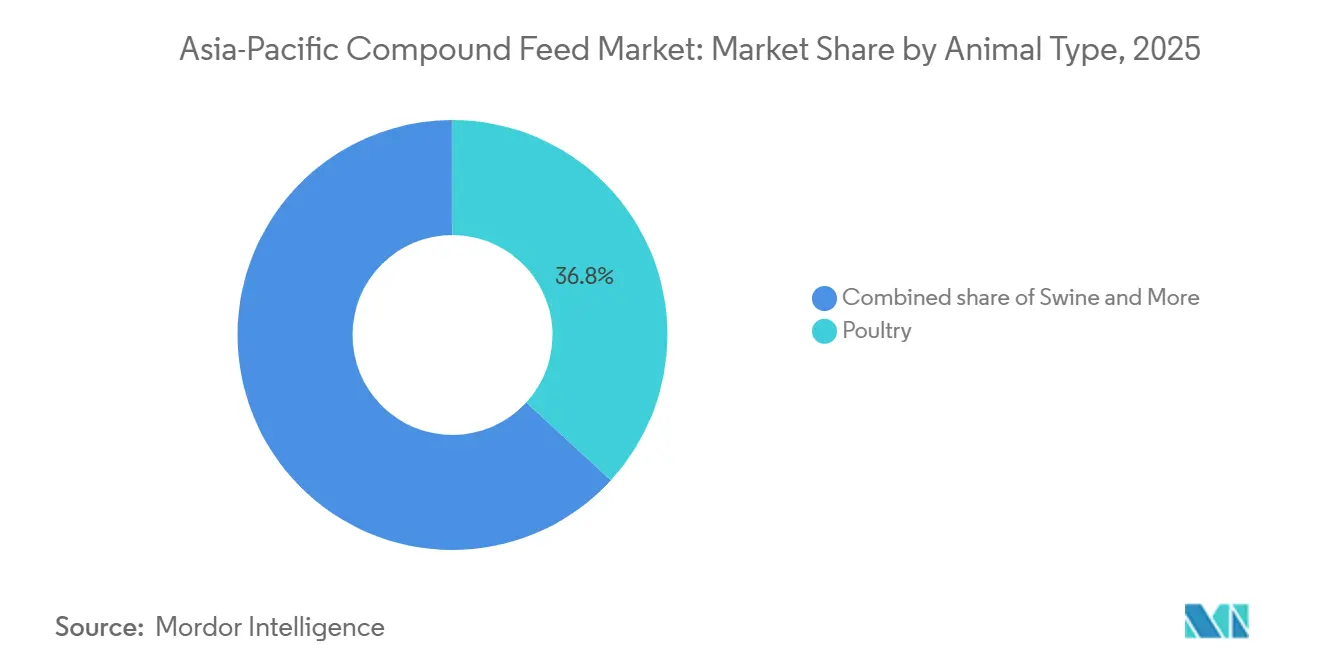

- By animal type, poultry accounted for 36.8% of the Asia-Pacific compound feed market size in 2025, and aquaculture is advancing at a 6.8% CAGR through 2031.

- By form, pellets accounted for 55.7% of the Asia-Pacific compound feed market in 2025, whereas liquid feed is projected to expand at a 5.3% CAGR over 2026-2031.

- By geography, China accounted for 47.1% of the market share in 2025, whereas Vietnam is forecast to post the fastest CAGR of 4.9% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Compound Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for animal protein | +0.6% | China, India, Vietnam, Indonesia, Thailand, and Philippines | Medium term (2-4 years) |

| Expansion of commercial aquaculture | +0.7% | Vietnam, Thailand, China, India, and Indonesia | Long term (≥ 4 years) |

| Government subsidies for feed mills | 0.6% | India, China, Vietnam, andThailand | Short term (≤ 2 years) |

| Growth of e-commerce feed ingredient trade | +0.4% | China, India, Indonesia, Vietnam, and Thailand | Medium term (2-4 years) |

| Genomic breeding driving precision nutrition | +0.5% | China, Thailand, Vietnam, and Australia | Long term (≥ 4 years) |

| Enzymatic feed additive cost reductions | +0.3% | China, Thailand, and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Animal Protein

Income growth across South and Southeast Asia lifted per-capita meat intake. According to the Basic Animal Husbandry Statistics (BAHS) 2025 report, the per capita meat availability in India for the 2024-25 fiscal year was 7.51 kg per person. This reflects a consistent rise in meat production and protein accessibility, with total production for 2024-25 amounting to 10.50 million metric tons [1]Source: Department of Animal Husbandry and Dairying, "Release of Basic Animal Husbandry Statistics-2025," dahd.gov.in. In China, chicken meat production in 2025 increased to 16,200 thousand metric tons, up from 15,350 thousand metric tons in 2024, as large vertically integrated white broiler producers continued to expand capacity despite persistent low margins [2]Source: Foreign Agricultural Service, "China: Poultry and Products Annual," fas.usda.gov. Urban consumers in tier-2 cities are willing to pay more for antibiotic-free chicken, encouraging mills to blend organic acids, enzymes, and probiotics. As substitution accelerates, soybean meal alternatives are likely to secure a larger slice of the Asia-Pacific compound feed market.

Government Subsidies for Feed Mills

Government grants, subsidies, and strategic infrastructure funds for feed mills are driving the Asia-Pacific compound feed market. For instance, the Indian government launched the Animal Husbandry Infrastructure Development Fund (AHIDF) under the Atma Nirbhar Bharat Abhiyan stimulus package. The AHIDF was approved to incentivize investments by individual entrepreneurs, private companies, and Farmers' Producer Organizations (FPOs) in establishing dairy processing and value-addition infrastructure, meat processing and value-addition infrastructure, and animal feed plants [3]Source: Department of Animal Husbandry & Dairying, "Animal Husbandry Infrastructure Development Fund (CS)," dahd.gov.in. In April 2023, Japan's Ministry of Agriculture, Forestry, and Fisheries (MAFF) implemented a special measure under the Compound Feed Price Stabilization System to enhance feed compensation payments to livestock, poultry, and swine producers. This measure revised a formula that had been limiting feed support payments when feed costs remained high for over a year. While subsidies intensify competition by compressing margins, they also promote automation, reducing labor costs and improving batch consistency, thereby strengthening competitive efficiency within the Asia-Pacific compound feed market.

Genomic Breeding Driving Precision Nutrition

Charoen Pokphand Foods Public Company Limited conducted sequencing of thousands of broilers in the year 2024, aligning amino acid profiles with their metabolic requirements and achieving a significantly improved feed conversion ratio compared to standard diets. Tongwei Co., Ltd. developed tilapia lines in 2023 with considerably faster growth rates, which necessitated higher levels of lysine and methionine, resulting in the inclusion of crystalline amino acids as a notable portion of the ration weight. Australia’s national science agency has recommended a substantial increase in trace minerals to support advancements in cattle genetics, while precision feeding practices are effectively reducing nitrogen and phosphorus losses, a key focus in countries such as Japan and South Korea. Genetic advancements are playing a critical role in driving premium formulations within the Asia-Pacific compound feed market.

Growth of E-Commerce Feed Ingredient Trade

Transactions involving lysine, methionine, and vitamins on Alibaba’s 1688.com platform grew significantly, enabling Indonesian mills to bypass traditional agents. JD’s next-day fulfillment services in China's highly populated provinces helped reduce the need to maintain large safety stocks and lower associated financing costs. Blockchain pilot programs are being utilized to trace soybean meal shipments from Brazil to mills in Thailand, enabling higher premiums for lots certified as non-GMO. Distributor margins have declined significantly, prompting traditional traders to shift their focus to on-site advisory services and mycotoxin testing. The ongoing adoption of digital procurement methods is anticipated to continue transforming the structure of the compound feed market in the Asia-Pacific region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile corn and soybean prices | -0.6% | China, India, Thailand, Vietnam, Indonesia, and Philippines | Short term (≤ 2 years) |

| Surge in fermented single-cell proteins | -0.3% | China, Japan, Australia, and South Korea | Long term (≥ 4 years) |

| Stricter antibiotic-free regulations | -0.4% | China, Japan, Australia, South Korea, Vietnam, and Thailand | Medium term (2-4 years) |

| Mycotoxin contamination escalation | -0.3% | India, Vietnam, Thailand, and Indonesia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Antibiotic-Free Regulations

China has implemented fines of up to CNY 500,000 (USD 70,000) for violations of its antibiotic growth promoter ban. This has led feed mills to adopt alternatives, such as organic acids and probiotics, which have increased input costs. In Japan, regulations on tetracycline antibiotic residues in animal products, particularly in kidney and muscle tissues, have established maximum residue limits (MRLs) for compounds like oxytetracycline in specific samples. These regulations have prompted exporters from Thailand and Vietnam to modify their livestock practices. In South Korea, the introduction of a traceability portal has added administrative requirements. While variability in probiotic quality presents challenges to adoption, premium retail channels provide incentives for compliant producers, thereby influencing value distribution within the Asia-Pacific compound feed market.

Mycotoxin Contamination Escalation

In 2024, Indian corn was found to contain aflatoxin levels exceeding Vietnam's permissible limit, prompting costly imports from Australia. In Thailand, a significant portion of domestically produced corn was found to be contaminated with deoxynivalenol, while China rejected a large quantity of Ukrainian grain due to contamination concerns. The use of binders, although increasing production costs, has demonstrated inconsistent effectiveness, particularly in addressing deoxynivalenol contamination. Furthermore, uneven enforcement of regulations across various provinces in Indonesia has created uncertainty, reducing confidence and increasing the costs associated with formulation in the Asia-Pacific compound feed market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredients: Cereals Anchor Formulations, Supplements Accelerate

Cereals are the largest ingredient and contributed 46.2% of the Asia-Pacific compound feed market share in 2025, led by corn, which supplied the majority of cereal tonnage and remained indispensable for energy density. Wheat has traditionally played a secondary role in ruminant feed formulations, primarily valued for its gluten content, which improves pellet binding. Soybean meal has been a key ingredient, and rapeseed and sunflower meals are gaining prominence, particularly in regions where reliance on soybean imports poses risks to profit margins. Oils, such as soybean and palm, are included sparingly due to concerns over rancidity. Molasses is primarily used in ruminant and liquid feeds. Other raw materials, including rice bran and distillers dried grains, are utilized as feed mills capitalize on localized surpluses.

Supplements scaled faster, expanding at a 5.2% CAGR through 2026-2031, as antibiotic-free mandates and precision feeding drive demand for enzymes and probiotics. The shift confirms cereals’ centrality while highlighting a progressive remix of the Asia-Pacific compound feed market toward higher-value micro-ingredients. Supplements are poised for leadership with enzymes, probiotics, and organic acids raising feed efficiency and allowing mills to trim costly fish-meal and soybean-meal shares. Crystalline amino acids account for a significant share of supplement revenues and are steadily gaining importance as genomic selection necessitates more precise targets for lysine and methionine. The use of antibiotics has significantly decreased due to regulatory restrictions, creating greater opportunities for the adoption of functional additives. This transition contributes to improved profit margins, as supplements typically command a higher price per kilogram than bulk cereals, thereby supporting the diversification of earnings within the Asia-Pacific compound feed market.

By Supplements: Amino Acids Dominate, Probiotics Outpace

Amino acids are the largest segment, accounting for 34% of the Asia-Pacific compound feed market size in 2025. Lysine and methionine top the list because they correct protein imbalances in corn–soybean diets and cut nitrogen excretion, a compliance win in Japan and South Korea where nutrient runoff caps apply. Indian integrators utilized enzyme packages to substitute soybean meal with sunflower meal, achieving cost savings while maintaining daily weight gain. Rising e-commerce volumes on Alibaba and JD platforms have trimmed lysine delivery times to under ten days and narrowed distributor margins. These efficiencies reinforce amino acids as the pricing and volume cornerstone of the Asia-Pacific compound feed market size for supplements.

Probiotics are the fastest-growing supplement line, projected to expand at a 4.5% CAGR through 2031 as regulators curb the use of antibiotic growth promoters. China approved 42 probiotic strains in 2025, yet uneven provincial enforcement keeps smaller mills cautious and sustains demand for certified products from multinational suppliers. Retailers in Australia and Japan pay premiums for poultry raised on probiotic-fortified rations. As enforcement tightens and field data accumulate, probiotics are positioned to deliver the greatest incremental value within the broader Asia-Pacific compound feed market.

By Animal Type: Poultry Dominates, Aquaculture Surges

Poultry is the largest animal segment and accounted for 36.8% of the Asia-Pacific compound feed market revenue in 2025, as broiler output across China and India remained volume-heavy and feed-intensive. Ruminant feed also expanded, supported by increasing dairy demand in India and Australia. Other segments, including equine and pet feed, maintain higher profit margins. The poultry segment remains a key contributor, supporting formulation scale, supplier negotiation leverage, and baseline growth in the Asia-Pacific compound feed market.

Aquaculture is the momentum driver, forecast to climb at a 6.8% CAGR through 2031. Shrimp and pangasius proliferation in Vietnam, along with offshore cage initiatives in Guangdong, are driving the adoption of protein floating pellets with water stability beyond 2 hours. Recirculating aquaculture in the Asia-Pacific region has increased regional output, tightened nutrient specifications, and boosted enzyme usage, thereby enhancing the overall value density within the compound feed market share held by aquafeed suppliers.

By Form: Pellets Prevail, Liquid Feed Gains Traction

Pellets are the largest form and accounted for 55.7% of the Asia-Pacific compound feed market revenue in 2025 on the back of superior feed conversion and ease of handling. Mash held a significant share of the market, as it is preferred by smallholder poultry farmers seeking to minimize equipment investment. Crumbles were primarily used as starter feeds, as their particle size is well-suited for chick beaks. Liquid feed was mainly utilized in Denmark-style swine systems, which are increasingly being adopted in northern China. Furthermore, automation and heat treatment of pellets help reduce pathogen loads, reinforcing the strong position of pellets in the Asia-Pacific compound feed market.

Liquid feed is projected to exhibit the fastest 5.3% CAGR through 2031, as integrators chase labor savings and exploit wet by-products such as whey and bakery waste. Extruded floating pellets are increasingly being adopted in aquaculture. While the recovery of equipment costs remains a challenge, the growing labor scarcity and the availability of by-products are driving the rising use of liquid and extruded forms in the Asia-Pacific compound feed market.

Geography Analysis

China is the largest geography and accounts for 47.1% of the Asia-Pacific compound feed market share in 2025. The nation’s corn production, although substantial, was insufficient to meet overall demand, resulting in a significant shortfall that necessitated imports and contributed to cost fluctuations. The enforcement of strict penalties for antibiotic residues has led to higher formulation costs, while products in the premium-certified category continue to command considerably higher retail prices. Financial support for automation initiatives under the latest Five-Year Plan encouraged leading companies, including Tongwei Co., Ltd. and New Hope Liuhe Co., Ltd., to significantly expand their production capacity. These measures underscore China’s commitment to improving quality standards and ensuring regulatory compliance in the Asia-Pacific compound feed market.

Vietnam is set to outpace peers, with a forecast 4.9% CAGR to 2031, driven by vibrant shrimp and pangasius sectors. Tax incentives under Decree 13 attracted De Heus Animal Nutrition B.V. (Royal De Heus Group) and Charoen Pokphand Foods Public Company Limited to the regions of Dong Thap and Can Tho, significantly increasing feed production capacity by the middle of the decade. Guangdong Haid Group Co., Ltd.'s (Guangzhou Haihao Investment Co., Ltd.) rapid expansion in the shrimp feed market demonstrates how focused research and development, when aligned with government-supported aquaculture clusters, can effectively challenge established competitors. The ongoing risk of mycotoxin contamination in corn sourced from India continues to elevate input costs. However, the use of binding agents and the importation of grain from Australia have ensured a consistent supply, supporting the steady growth of the compound feed market in the Asia-Pacific region.

India, Japan, Thailand, and Australia collectively contributed significantly to the Asia-Pacific compound feed market in 2025, each influenced by distinct factors. India’s modernization fund aims to enhance production capacity. However, recurring challenges related to monsoon variability continue to affect the stability of corn procurement. In Japan, stricter residue limits have encouraged exporting countries to shift toward antibiotic-free practices, driving a growing demand for probiotics and organic acids. Thailand’s Board of Investment incentives have led to numerous certifications under international feed safety standards, aligning the country’s feed industry with the requirements of premium global markets. In Australia, while the National Residue Survey reported minimal instances of non-compliance, increasing retailer demand for certified antibiotic-free meat is driving feed mills to adopt cleaner, safer formulations. These factors collectively influence the competitive dynamics of the Asia-Pacific compound feed market across both developed and emerging economies.

Regulatory Landscape

Across Asia-Pacific, feed regulation is tightening around additive approvals, antibiotic controls, and documentation requirements, shifting more compliance responsibility onto mills and additive suppliers. In China, the Ministry of Agriculture and Rural Affairs (MARA) has paired enforcement of antibiotic growth promoter restrictions, with stated fines up to CNY 500,000 for violations, with frequent technical updates that specify which substances can be used and how they must be applied.

Recent updates also indicate faster rule changes for market access. In June 2026, MARA issued an announcement approving new feed additives while revising the Feed Ingredients Catalog and amending the Code for Safe Use of Feed Additives, requiring manufacturers to keep formulations and labels aligned with the updated catalog. Vietnam has been moving administrative workflows toward digital compliance, with new self-declaration procedures for domestic and imported animal feed supplements implemented via an official electronic portal from May 18, 2026, and policy work continuing on broader food-safety governance reforms that are scheduled for National Assembly submission in October 2026. India has likewise tightened controls on cross-border flows of premixes and supplements; the Department of Animal Husbandry and Dairying issued an order in March 2025 restricting imports of animal feed additives and premixes to a regulated list, while the Bureau of Indian Standards (BIS) has continued updating ingredient specifications such as IS 5065:2025 for meat meal used in poultry feed.

Competitive Landscape

The Asia-Pacific compound feed market is characterized by moderate concentration, with the five largest suppliers accounting for significant combined revenue in 2025. Charoen Pokphand Foods Public Company Limited, New Hope Liuhe Co., Ltd., Cargill, Incorporated, and Guangdong Haid Group Co., Ltd. (Guangzhou Haihao Investment Co., Ltd.) employ vertical integration to secure access to raw materials and downstream demand, buffering them against spikes in corn and soybean costs. Capacity additions target growth hot spots. De Heus Animal Nutrition B.V. (Royal De Heus Group) inaugurated an aquatic feed plant worth USD 18.6 million in Can Tho, Vietnam, in September 2023. Located in the Tra Noc II Industrial Park, the 2.7-hectare facility has an annual production capacity of 240,000 metric tons of high-quality, specialized feed for pangasius (tra and basa) fish.

Technology adoption serves as a key differentiator. Guangdong Haid Group Co., Ltd. (Guangzhou Haihao Investment Co., Ltd.) integrated genomic data with pellet design, achieving a double-digit market share in Vietnam’s shrimp segment within six months. New Hope Liuhe Co., Ltd. implemented a cloud-based formulation engine that connects 180 mills, reducing recipe error rates by 12% during periods of volatile input markets. Smaller and midsize mills, with limited capacity to invest in automation, are experiencing reduced profit margins, suggesting further consolidation in the Asia-Pacific compound feed market.

E-commerce disruption compounds pressure on legacy distributors. Alibaba's and JD's ingredient portals have significantly reduced traditional markups, prompting intermediaries to shift their focus to on-farm advisory and laboratory services. Patent filings in phytase and probiotic strains by Novozymes and BASF SE reveal intensifying innovation aimed at serving antibiotic-free feeders. Meanwhile, niche entrants pursue premium functional niches, such as omega-3-fortified broiler diets or thermotolerant enzymes, to secure higher margins within the wider Asia-Pacific compound feed market.

Asia-Pacific Compound Feed Industry Leaders

-

Charoen Pokphand Foods Public Company Limited

-

New Hope Liuhe Co., Ltd.

-

Cargill, Incorporated

-

Tongwei Co., Ltd.

-

Guangdong Haid Group Co., Ltd. (Guangzhou Haihao Investment Co., Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity modernization and species specialization are creating whitespace for compound feed producers that can deliver quality, traceability, and higher-performance formulations. In India, investment-backed capacity additions are anchoring this shift, with Cargill opening a dairy feed plant in Wazirabad, Punjab in February 2026 with 400,000 metric tons of annual capacity (INR 300 crore), which supports commercial dairy systems that increasingly seek consistent pellets, mineral packs, and protein optimization. In Southeast Asia, new projects highlight the opportunity around localized supply and faster service levels, including PT Malindo Feedmill Tbk's announced USD 40-46 million investment for a new feed mill in Lampung, Indonesia (completion scheduled for Q3 2026).

Aquaculture remains the most formulation-intensive demand center in the region and is supporting premiumization through nutrient-dense aquatic pellets, enzymes, and functional additives, particularly where governments are incentivizing recirculating aquaculture and offshore cage systems. BioMar's February 2026 announced expansion of its Wuxi, China aquafeed facility, adding a new line aimed at doubling capacity for specialty products, points to pull from high-end species and early growth-stage feeds. Tighter antibiotic residue thresholds, notably in China, also reinforces the ingredient and additive opportunity, while faster procurement of amino acids and vitamins through platforms such as Alibaba and JD shortens replenishment cycles and raises the value of digitally enabled formulation and compliance documentation.

Recent Industry Developments

- June 2026: PT Malindo Feedmill Tbk announced a USD 40-46 million investment to build a new feed mill in Lampung, Indonesia, with completion scheduled for Q3 2026. The project adds regional manufacturing capacity closer to poultry and livestock clusters, helping shorten delivery lead times and improve supply continuity during commodity price swings.

- February 2026: Cargill opened a dairy feed plant in Wazirabad, Punjab, India, with annual capacity of 400,000 metric tons and an investment of INR 300 crore. The facility strengthens Cargill's local production footprint for compound dairy feed and increases competitive pressure on regional mills through scale, automation, and tighter quality control.

- November 2025: Louis Dreyfus Company inaugurated a specialty feed protein production line in Tianjin, China, with capacity of 60,000 metric tons focused on fermented soybean meal. By expanding availability of highly digestible, value-added proteins for livestock and aquaculture, the move supports reformulation away from costlier conventional meals and aligns with demand for functional ingredients.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the value of commercially manufactured compound feed sold for farm animals across Asia-Pacific, counted at the point of sale by feed mills and branded suppliers, and measured in USD.

Scope exclusions: On-farm mixed rations, raw grains and oilseed meals sold as single ingredients, and purely veterinary medicines are excluded unless they are sold as compound feed inputs in standard feed formulations.

Segmentation Overview

-

By Ingredients

- Cereals

- Oilseeds

- Oils

- Molasses

- Supplements

- Other Ingredients

-

By Supplements

- Vitamins

- Amino Acids

- Antibiotics

- Enzymes

- Antioxidants

- Acidifiers

- Prebiotics

- Probiotics

- Other Supplements

-

By Animal Type

- Ruminant

- Swine

- Poultry

- Aquaculture

- Other Animal Types

-

By Form

- Pellets

- Mash

- Crumbles

- Liquid Feed

-

By Geography

- China

- India

- Japan

- Thailand

- Vietnam

- Australia

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set up the demand pool and pricing logic, and then to cross-check results by country and animal type. We referred to public sources such as FAOSTAT for livestock and aquaculture production trends, national agriculture ministries for feed policy and production notes, customs and tariff portals for corn and soybean meal trade signals, and central bank releases for exchange-rate timing.

In parallel, company annual reports, investor presentations, reputable association websites, and trusted press coverage were reviewed to track feed mill capacity additions, product mix shifts, and formulation changes that can move average selling prices. Where helpful, we also used paid subscriptions for company financials and news, and a patent database to spot additive and formulation directions that may affect pricing over time. The sources listed here are illustrative, and many other public and paid references were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what desk research cannot show consistently, such as realized feed price movement by animal type, how fast integrators change formulations, and how much volume is bought through contract supply versus spot orders. We engaged with feed mill leaders, procurement and nutrition teams, and distribution-focused managers across major APAC markets so assumptions on volumes, mix, and pricing could be corrected before final totals were locked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | |

| Mid tier: 57% | Functional/Unit leaders: 32% | |

| Smaller Players: 15% | Managers: 53% |

Market-Sizing & Forecasting

Sizing starts with a top-down reconstruction of compound feed demand by linking animal output and herd or flock levels to feed conversion patterns and feed intensity, which are then adjusted for the share of commercial compound feed versus informal feeding. Once the country totals are built, selective bottom-up checks are used, such as a sample roll-up of feed mill revenues, capacity utilization checks, and volume times average price tests for common feed types, so obvious gaps can be corrected.

Key inputs used in the model include livestock and aquaculture production volumes, feed-to-meat or feed-to-egg conversion ranges, shifts in species mix (poultry, swine, ruminants, and aquatic), raw material price direction for corn and oilseed meals, and supplement penetration that changes realized selling prices. Where local price series were incomplete, gaps were handled using trade-linked proxies and interview-confirmed price spreads by animal type, followed by a consistency check against inflation and currency moves.

Forecasting is run through scenario analysis supported by exponential smoothing on core drivers, and then tuned using expert feedback on likely raw material cycles, disease recovery patterns, and the pace of feed mill modernization. Growth is not applied uniformly, since some countries show faster aquaculture expansion while others depend more on poultry integration, so the outlook is built country by country and then rolled up to the region.

Data Validation & Update Cycle

Outputs are validated in steps, starting with internal consistency checks across volume, price, and implied feed use per unit of animal output. Model results are compared against independent signals such as grain import direction, changes in livestock production, and announced feed mill capacity, and any large variance is reviewed by another analyst before sign-off.

If a number sits outside expected ranges, the drivers are re-checked and, when needed, experts are re-contacted to confirm whether the change is structural or driven by a temporary event like a raw material spike or disease-related stocking shifts. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is completed so clients receive the latest updated view.

Mordor Intelligence's Asia Pacific Compound Feed Market Market Size Measured Against Other Published Estimates

Published values for Asia-Pacific compound feed do not always line up, even when the topic sounds the same. Differences usually come from what is counted as compound feed versus broader animal feed, which year is treated as the base, and how price movement is handled when grains and oilseed meals swing.

A second set of gaps comes from geography handling and refresh timing, because some publishers use older currency conversion points or apply a uniform price assumption across multiple countries and animal types. In our checks, the biggest swings usually show up when aquafeed is treated inconsistently, or when on-farm mixed feed and single-ingredient sales get blended into the total without a clear adjustment.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 215.62 B (2025) | |

| Industry Publisher A | USD 243.86 B (2024) | This figure is presented for a broader animal feed scope and an earlier base year, and it can include wider feed categories beyond commercially manufactured compound feed, which pushes the total upward versus a tighter definition. |

| Regional Consultancy B | USD 81.69 B (2022) | The estimate appears to use a narrower counted universe or a different valuation basis, and the year is not aligned with the current base, which makes the value look materially smaller when compared across a later pricing cycle. |

The spread mainly reflects scope and year alignment rather than a single modeling trick, so volumes are tied to animal output and then priced using grain and oilseed meal movements by country and species, with annual refresh and interview-based checks on formulation shifts, which is the specific discipline applied in Mordor Intelligence.

Key Questions Answered in the Report

What is the projected value of Asia-Pacific compound feed by 2031?

The sector is anticipated to reach USD 272.43 billion by 2031, expanding at a 4.73% compound annual pace between 2026 and 2031.

Which supplement category currently contributes the largest revenue?

Amino acids hold about 34% of supplement turnover in 2025, because lysine and methionine correct protein imbalances and help mills meet stricter nitrogen-runoff rules.

Why are probiotics gaining momentum in regional feed formulations?

Tightening antibiotic-residue limits have driven a 4.5% compound annual growth outlook through 2031, for probiotics, with Lactobacillus blends cutting shrimp mortality up to 12% in recent Thai trials.

How is digital procurement changing ingredient sourcing?

Platforms operated by Alibaba and JD have reduced lead times for lysine and vitamin shipments to under ten days and shaved roughly three percentage points off distributor margins.

Which country is forecast to post the fastest growth through 2031?

Vietnam is projected to rise at a 4.9% compound annual rate through 2031, fueled by shrimp and pangasius aquaculture and supportive tax holidays for new feed mills.

Page last updated on: