Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

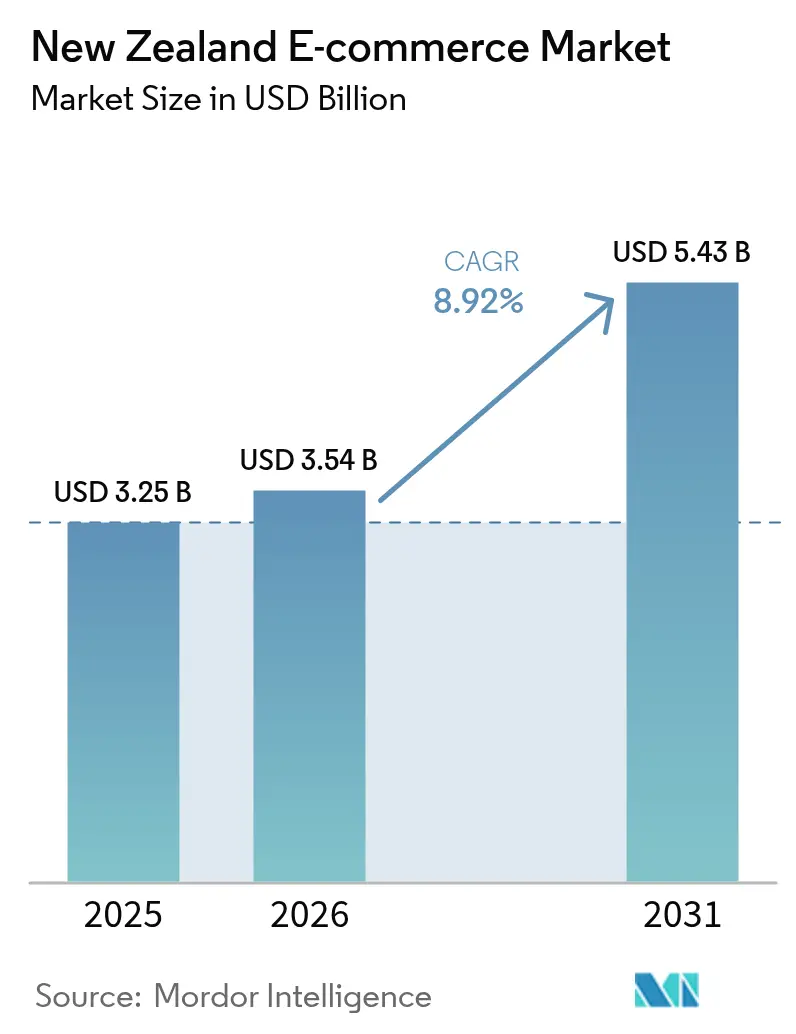

| Base Year Market Size (2025) | USD 3.25 Billion |

| Market Size (2026) | USD 3.54 Billion |

| Market Size (2031) | USD 5.43 Billion |

| Growth Rate (2026 - 2031) | 8.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

New Zealand E-commerce Market Analysis by Mordor Intelligence

The New Zealand e-commerce market size in 2026 is estimated at USD 3.54 billion, growing from 2025 value of USD 3.25 billion with 2031 projections showing USD 5.43 billion, growing at 8.92% CAGR over 2026-2031. Growing smartphone penetration, near-universal fibre coverage, and supportive government programmes create a favourable demand environment. Cross-border parcel agreements with Australia and China cut delivery friction and widen product availability, while payment innovations such as Buy Now Pay Later (BNPL) lift basket sizes and conversion. Retailers respond with integrated omnichannel strategies that blend in-store pickup, same-day delivery, and loyalty data analytics. Intensifying competition from global marketplaces pushes local incumbents to deepen AI-driven personalisation and invest in fulfilment automation.

Key Report Takeaways

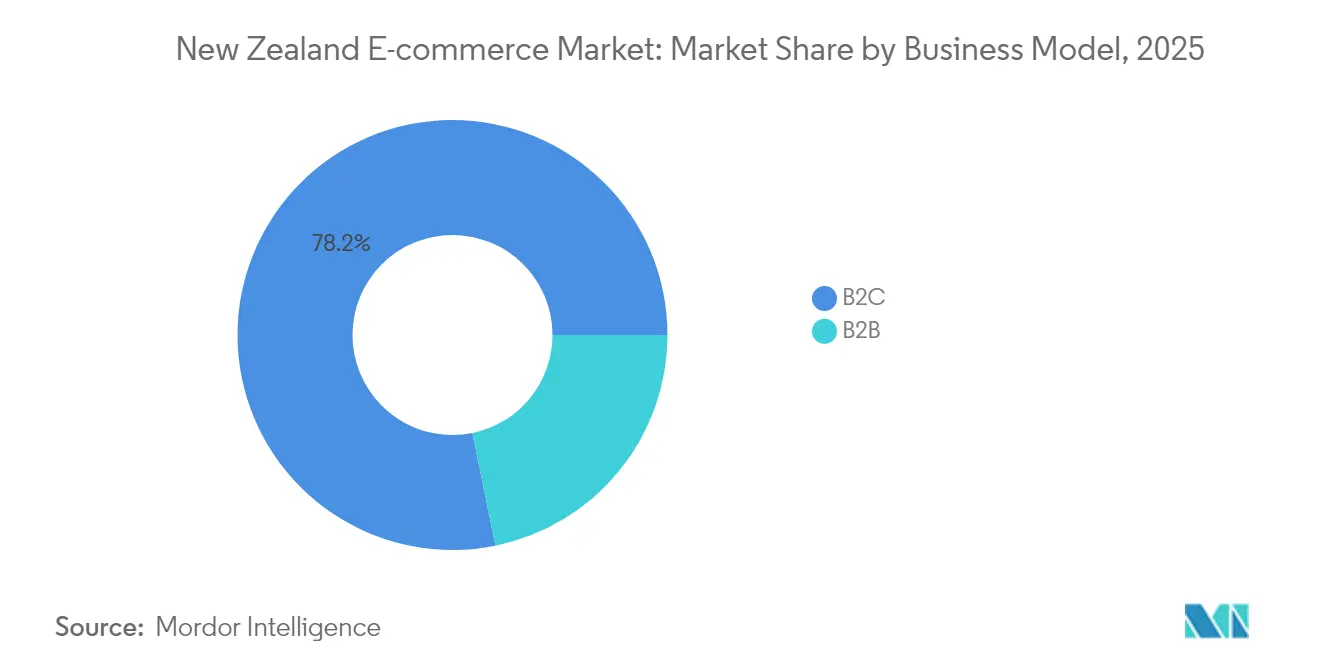

- By business model, B2C transactions led with 78.20% of the New Zealand e-commerce market share in 2025; B2B is expected to expand at an 11.25% CAGR through 2031.

- By device, smartphones accounted for 65.70% of the New Zealand e-commerce market size in 2025, and the segment is projected to grow at 10.12% CAGR to 2031.

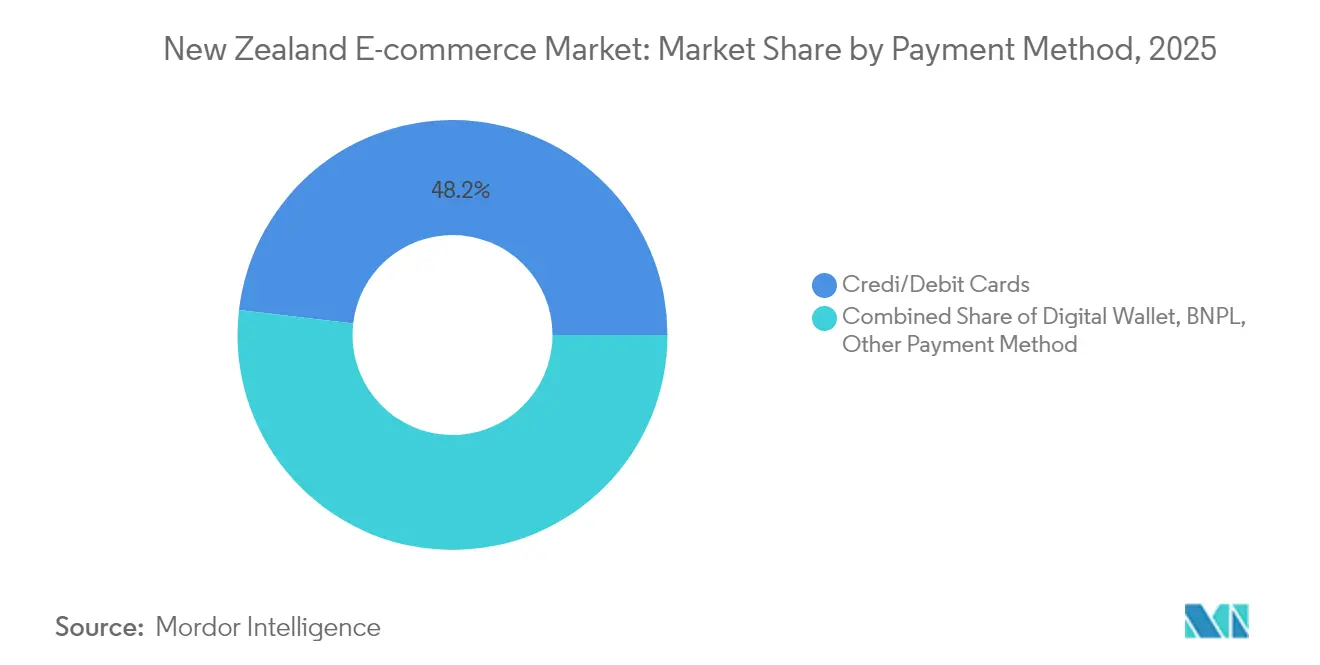

- By payment method, credit and debit cards held 48.15% share of the New Zealand e-commerce market size in 2025, while BNPL is the fastest-growing option at 14.05% CAGR.

- By B2C product category, consumer electronics commanded 17.65% of the New Zealand e-commerce market share in 2025; food & beverage is forecast to post the strongest 13.55% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

New Zealand E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Penetration of Mobile Commerce Driven by Rural Broadband Expansion | +1.8% | National, with strongest gains in rural South Island and West Coast regions | Medium term (2-4 years) |

| Rapid Adoption of BNPL Fueling AOV Growth among Gen Z | +2.1% | Urban centers (Auckland, Wellington, Christchurch) with spillover to regional areas | Short term (≤ 2 years) |

| Government Digital Boost Programme Accelerating SME Online Migration | +1.5% | National, concentrated in manufacturing hubs (Hamilton, Palmerston North) | Medium term (2-4 years) |

| Cross-Border Parcel Agreements Lowering Shipping Costs from AU & CN | +0.9% | National, with early gains in Auckland, Wellington, Christchurch | Long term (≥ 4 years) |

| Surge in Social Commerce Influencer Marketplace Post-COVID | +1.3% | Urban millennials and Gen Z concentrated in Auckland, Wellington | Short term (≤ 2 years) |

| Advancements in Last-Mile Delivery Robotics in Auckland | +0.6% | Auckland metropolitan area with potential expansion to Wellington | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Penetration of Mobile Commerce Driven by Rural Broadband Expansion

Fixed wireless now supplies 20% of national broadband, overcoming terrain challenges and enabling fast mobile checkout in remote communities.[1]GSMA, “Mobile Economy Asia-Pacific,” gsma.com Fibre reaches 87% of households, and urban connection exceeds 78%, so 5G roll-outs can deliver richer media and augmented-reality catalogues.[2]Commerce Commission, “Interchange Fees Draft Decision,” comcom.govt.nz Retailers gain incremental demand as previously underserved shoppers transact via social-commerce apps that embed one-click payment. Improved connectivity also reduces the digital divide, letting regional SMEs list inventories on large marketplaces at low incremental cost. The result is broader geographical demand dispersion and higher frequency of repeat purchases.

Rapid Adoption of BNPL Fueling Gen Z Spending Power

New Zealand’s BNPL user base accelerates as the Credit Contracts and Consumer Finance Act gives providers a clear compliance path that balances innovation with consumer safeguards. Gen Z shoppers embrace pay-in-four plans that remove up-front cost hurdles for electronics and fashion, lifting average order values for merchants. Retailers welcome BNPL because the fee burden is offset by higher conversion and lower cart abandonment. With cards still dominant, BNPL gains represent incremental—not cannibalised—volume, raising total retail sales. Competitive tension among providers leads to loyalty-linked instalment offers that nudge repeat usage across multiple merchants.

Government Digital Boost Programme Accelerating SME Online Migration

The NZD 40 million (USD 23.72 million) Digital Boost allocation gives regional SMEs free training modules, expert mentoring, and co-funded platform builds.[3]New Zealand Treasury, “Digital Boost Programme Funding,” treasury.govt.nz Participating firms report shorter sales cycles once integrated with online marketplaces, driving network effects that attract more suppliers. The programme’s outreach to Māori enterprises ensures inclusive growth, widening product diversity online. As SMEs digitise supply chains, demand rises for B2B e-procurement portals, stimulating service providers in logistics, payments, and cybersecurity. The initiative underpins the New Zealand e-commerce market by expanding the seller base and lifting professional standards.

Cross-Border Parcel Agreements Lowering Shipping Costs from AU & CN

The Closer Economic Relations pact removes most tariffs, and the Trade Single Window clears 93.9% of containers before arrival, trimming customs delays. Lower last-mile costs open gateway cities to small retailers that could not previously justify international dispatch. Concurrently, New Zealand brands exploit the same agreements to reach Australian consumers via fulfilment centres in Sydney and Melbourne, diversifying revenue streams. Logistics firms offer bundled cross-border solutions that integrate duty calculation at checkout, enhancing transparency for end consumers. Over time, cost parity between domestic and trans-Tasman shipping intensifies competition, forcing local sellers to differentiate through service and product authenticity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Coastal Shipping Costs Impeding South Island Delivery | -0.8% | South Island, particularly West Coast and Southland regions | Long term (≥ 4 years) |

| Rising Online Fraud Undermining Consumer Trust despite CERT NZ Efforts | -1.2% | National, with higher impact in urban areas with greater online activity | Short term (≤ 2 years) |

| Fragmented GST Rules on Low-Value Imports for Cross-Border Sellers | -0.7% | National, affecting international e-commerce platforms and cross-border retailers | Medium term (2-4 years) |

| Warehouse Labour Shortages Extending Fulfilment Lead-Times | -0.5% | Auckland, Wellington, Christchurch distribution hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Coastal Shipping Costs Impeding South Island Delivery

Domestic vessels absorb emissions-trading levies not imposed on global carriers, raising per-parcel costs to the South Island. Port infrastructure limits vessel size, hindering economies of scale and extending transit times. Elevated freight bills feed directly into checkout prices for West Coast consumers, muting demand relative to North Island peers. Retailers test micro-fulfilment hubs in Christchurch to shorten last-mile legs, yet inventory duplication pressures margins. Unless coastal shipping gains fuel-cost relief or capacity upgrades, the regional growth gap is likely to persist.

Rising Online Fraud Undermining Consumer Trust despite CERT NZ Efforts

Scam losses neared NZD 200 million (USD 118.62 million) in 2023, and 62% of shoppers encounter fraudulent messages monthly. Phishing remains prevalent even as banks roll out confirmation-of-payee systems and voluntary reimbursement schemes. CERT NZ issues timely alerts, but AI-powered social-engineering attacks evolve quickly, compelling merchants to invest in multi-factor authentication. Heightened anxiety slows adoption among older demographics and first-time buyers, restraining the reachable customer base in the short term. Education campaigns and secure-payment badges aim to rebuild confidence but require sustained effort.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Digital Transformation Redefines B2B Engagement

B2C retained 78.20% of the New Zealand e-commerce market share in 2025, yet B2B volumes are forecast to climb 11.25% CAGR as procurement platforms replace email-based ordering. This divergence means the New Zealand e-commerce market size for B2B transactions could almost double by 2031 if adoption stays on course. Traditional wholesalers digitise catalogues to reach long-tail customers, expanding SKU availability at marginal cost. The Digital Boost Programme lowers barriers by subsidising storefront creation for small manufacturers, thus enriching inventory diversity online.

Enterprises integrate AI-driven demand planning and automated reordering to curtail stock-outs, reinforcing loyalty to digital channels. Cross-border sourcing gains momentum because duty-paid pricing transparency reduces procurement risk. For B2C players, continued omnichannel refinement focuses on leveraging loyalty data to optimise personalised offers. As both models converge on customer-centricity, platform providers that can serve B2C and B2B workflows through a single codebase are positioned to capture incremental revenue streams.

By Device Type: Smartphones Cement a Mobile-First Paradigm

Smartphone commerce generated 65.70% of transaction value in 2025 and is expected to expand at 10.12% CAGR, making it the central channel for the New Zealand e-commerce market. Rising 5G penetration, coupled with fibre backhaul, cuts page-load latency and enables immersive product views that improve conversion. The New Zealand e-commerce market size delivered via mobile could surpass the USD 3.2 billion mark before 2031 if the trajectory holds.

Laptop and desktop sessions remain important for configurable or high-ticket B2B purchases requiring detailed specifications, but even these interactions often conclude on a handset. Retailers optimise progressive-web-app architecture to support offline browsing in rural locations with intermittent coverage. Social-commerce integrations on Instagram and TikTok funnel discovery directly into merchant carts, shortening the path to purchase. Voice assistants and conversational commerce add incremental revenue by capturing spontaneous orders, illustrating that mobile is not merely another screen but the anchor of the entire customer journey.

By Payment Method: BNPL Reshapes Checkout Preferences

Cards retained 48.15% share of the New Zealand e-commerce market size in 2025, but BNPL transactions are rising 14.05% annually, positioning the instalment model to rival credit within the decade. The New Zealand e-commerce market share of BNPL could exceed 20% by 2031 if adoption persists. Regulatory clarity reduces insolvency risk for providers, encouraging product innovation such as subscription-based BNPL for repeat grocery orders.

Merchants experience lower abandonment rates when multiple payment rails are offered at checkout. Digital wallets grow steadily, propelled by tokenised security and smartphone biometric authentication. Looking forward, embedded finance will blur lines between payment and loyalty, letting shoppers accumulate rewards simultaneously with instalment repayments. For acquirers, interchange-fee caps announced by the Commerce Commission may compress margins but also broaden acceptance among small merchants.

By B2C Product Category: Grocery Growth Challenges Electronics Supremacy

Consumer electronics captured 17.65% of the New Zealand e-commerce market share in 2025, buoyed by rapid upgrade cycles and global brand launches. Food & beverage is the growth outlier, set to expand 13.55% CAGR as same-day delivery and cold-chain investments scale nationwide. The New Zealand e-commerce market size for online grocery could reach USD 1.05 billion by 2031 at current run-rates.

Woolworths NZ’s 14.6% first-half 2025 online sales growth validates consumer appetite for convenient, scheduled delivery slots. Meanwhile, fashion leverages influencer-led TikTok campaigns to drive impulse buys, and furniture retailers deploy AR tools that allow in-home product visualisation. Category incumbents experiment with subscription models and dynamic pricing algorithms to maximise lifetime value, recognising that frequency and basket mix vary dramatically by vertical.

Geography Analysis

Auckland anchors the New Zealand e-commerce market with its high population density, international airport, and concentration of fulfilment centres. Wellington follows, driven by public-sector procurement and a strong professional-services base that fuels B2B demand. Christchurch acts as the South Island gateway, and its technology cluster helps offset higher shipping costs through data-driven route planning efficiencies.

Regional broadband initiatives extend fibre to 87% of households and fixed-wireless to remote terrain, ensuring that the New Zealand e-commerce market size expands beyond city limits. As rural connectivity improves, niche artisanal brands from Central Otago and Hawke’s Bay list on national platforms, adding localisation depth. Cross-border trans-Tasman trade remains concentrated in Auckland due to port proximity, but Wellington’s government facilitation accelerates customs clearance.

The Closer Economic Relations agreement reduces tariffs, promoting bi-directional flows with Australia, while the NZ–EU Free Trade Agreement broadens European product availability. However, South Island shoppers still encounter delivery premiums because coastal shipping lacks scale. Micro-fulfilment pilots in Dunedin target faster last-mile service, hinting at future regional parity once cost structures improve.

Competitive Landscape

The market displays moderate fragmentation: the top domestic marketplace, Trade Me, generated NZD 369.8 million (USD 223 million) revenue in 2024, but its share has slipped as Amazon and Temu intensify discount-led campaigns. Traditional bricks-and-mortar groups pivot into omnichannel, with Briscoe Group raising online penetration to 19.69% of its NZD 791.5 million (USD 477 million) turnover in 2025.

Technology investment defines winners. Woolworths NZ uses AI route-optimisation and an Everyday Rewards data loop to deliver same-day groceries and upsell private-label products. Logistics challengers, such as Maersk’s Hamilton cold-chain facility, underpin perishable-goods expansion, while fintech entrants enable embedded BNPL at checkout. Payment cost regulation by the Commerce Commission may narrow processing fee spreads, levelling the playing field for smaller sellers.

White-space opportunity exists in rural fulfilment and specialist B2B platforms serving agriculture tech and precision manufacturing. Firms that combine last-mile innovation with sustainable packaging likely secure share as consumer climate awareness grows. Competitive intensity is forecast to heighten as cross-border sellers exploit tariff relief, compelling domestic incumbents to refine value propositions rather than rely on captive geography.

New Zealand E-commerce Industry Leaders

Trade Me

Fishpond Ltd.

Woolworths New Zealand Limited

Farmers Trading Co.

The Warehouse Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Air New Zealand signed a five-year deal with Tata Consultancy Services to implement AI-driven fleet and crew scheduling, cutting turnaround times and potentially enabling faster cargo-linked e-commerce deliveries.

- March 2025: Briscoe Group posted a NZD 60.6 million net profit and unveiled a Marketplacer platform, signalling a strategic push to aggregate third-party sellers and lift SKU count without inventory risk.

- February 2025: Yamaha Motor agreed to acquire Robotics Plus to integrate autonomous orchard vehicles with data-driven farm management. The move positions Yamaha to cross-sell precision agriculture tools through B2B e-commerce channels, deepening the New Zealand e-commerce market’s agri-tech offering.

- December 2024: The Commerce Commission issued a draft decision to cap interchange fees, which could save merchants USD 260 million annually and free cash for e-commerce platform investments.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the New Zealand e-commerce market as the gross merchandise value (GMV) generated when goods or services are ordered and paid for online by domestic residents, whether the site is local or cross-border. Sales completed through mobile sites and apps are fully counted, while click-and-collect orders are included only when the payment is processed online.

Scope exclusion: Purely digital content (music, video, software downloads) and peer-to-peer resale of used items fall outside the present sizing.

Segmentation Overview

- By Business Model

- B2C

- B2B

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

We interview marketplace operators, third-party logistics providers, payment-service executives, and omnichannel retailers across Auckland, Wellington, and Christchurch. Conversations probe average transaction values, return rates, and the share of offshore parcels. Then, survey findings from frequent online shoppers help us test adoption curves for mobile checkout and BNPL usage. These inputs let us recalibrate secondary data and stress-test early model outputs.

Desk Research

Mordor analysts begin with official, open data, monthly retail e-commerce turnover from Statistics New Zealand, customs parcel-import records, Reserve Bank card-payment dashboards, and Commerce Commission filings. These are enriched with industry white papers from NZ Post Business IQ, OECD digital-trade indicators, and International Trade Administration briefs that outline cross-border flows. To profile corporate activity, we pull financials from D&B Hoovers and news from Dow Jones Factiva, checking trends such as BNPL penetration or marketplace fee shifts. Additional insights come from trade associations like Retail NZ and reports issued by the Ministry of Business, Innovation and Employment. The sources above are illustrative; many other documents are reviewed to validate figures and fill information gaps.

Market-Sizing & Forecasting

A top-down build starts with Statistics NZ retail data, to which we apply an online-penetration matrix by product group, followed by adjustments for cross-border imports and cash-on-delivery leakage. Select bottom-up checks, sampled marketplace GMV, courier parcel volumes, and average selling-price × unit estimates anchor the totals. Key variables monitored include smartphone share of checkouts, card-not-present fee trends, rural broadband coverage, consumer confidence, and GST thresholds on low-value imports. Forecasts run through a multivariate regression: real disposable income, mobile-commerce share, and parcel-delivery density explain over 85 percent of variance, with ARIMA used for short-run smoothing.

Data Validation & Update Cycle

Every draft model passes variance checks against prior releases and third-party macro controls before two-stage peer review. An annual refresh is standard, yet material events, payment-rule changes or postal strikes trigger interim updates. A last-minute pass guarantees clients receive the freshest baseline.

Why Mordor's New Zealand E-commerce Baseline Earns Trust

Published figures often diverge because firms vary in scope, valuation basis, and refresh cadence.

Mordor's disciplined inclusion rules, dual-path modeling, and yearly source audits narrow these gaps, giving decision-makers a dependable starting point.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.25 B (2025) | Mordor Intelligence | - |

| USD 6.8 B (2024) | Regional Consultancy A | Counts full consumer-to-consumer resale and digital media, inflating GMV |

| USD 6.8 B (2025) | Trade Journal B | Uses total online spend, not GMV, and omits cross-border deduction |

These comparisons show how broader scopes or differing value bases raise totals. By selecting a focused GMV definition and balancing top-down statistics with bottom-up reality checks, Mordor Intelligence delivers a transparent, repeatable baseline that clients can explain and defend in board-room decisions.

Key Questions Answered in the Report

What is the current value of the New Zealand e-commerce market?

The market is worth USD 3.54 billion in 2026 and is forecast to grow to USD 5.43 billion by 2031.

Which business model is growing fastest?

B2B e-commerce is advancing at an 11.25% CAGR as enterprises digitise procurement and supply chains.

How important is mobile commerce in New Zealand?

Smartphones generated 65.70% of 2025 online sales and are projected to rise 10.12% CAGR, making mobile the primary shopping channel.

What segment will lead future growth in product categories?

Food & beverage is expected to post a 13.55% CAGR through 2031, driven by same-day delivery and cold-chain investments.

How is regulation influencing payment trends?

Interchange-fee caps and BNPL consumer-protection rules encourage merchants to offer diverse, lower-cost payment options that enhance checkout conversion.

What are the biggest restraints on e-commerce expansion?

High coastal shipping costs to the South Island and rising online fraud both suppress growth, subtracting a combined 2% from forecast CAGR.

Page last updated on: