Slovak Republic E-commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

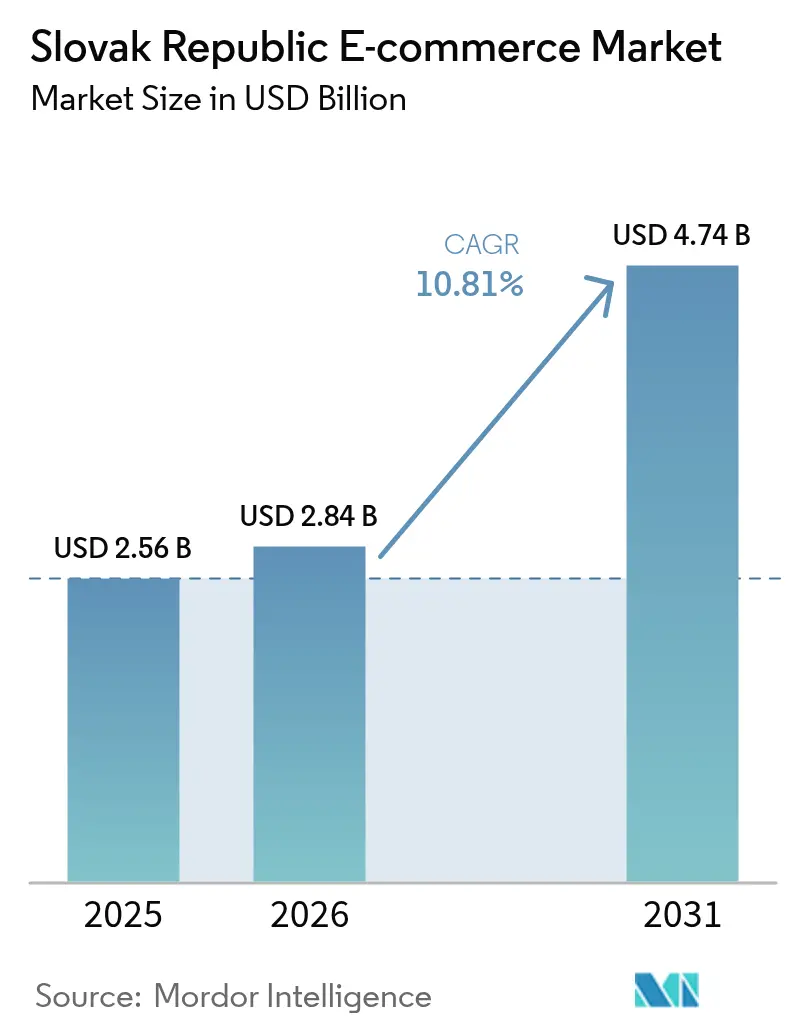

| Base Year Market Size (2025) | USD 2.56 Billion |

| Market Size (2026) | USD 2.84 Billion |

| Market Size (2031) | USD 4.74 Billion |

| Growth Rate (2026 - 2031) | 10.81% CAGR |

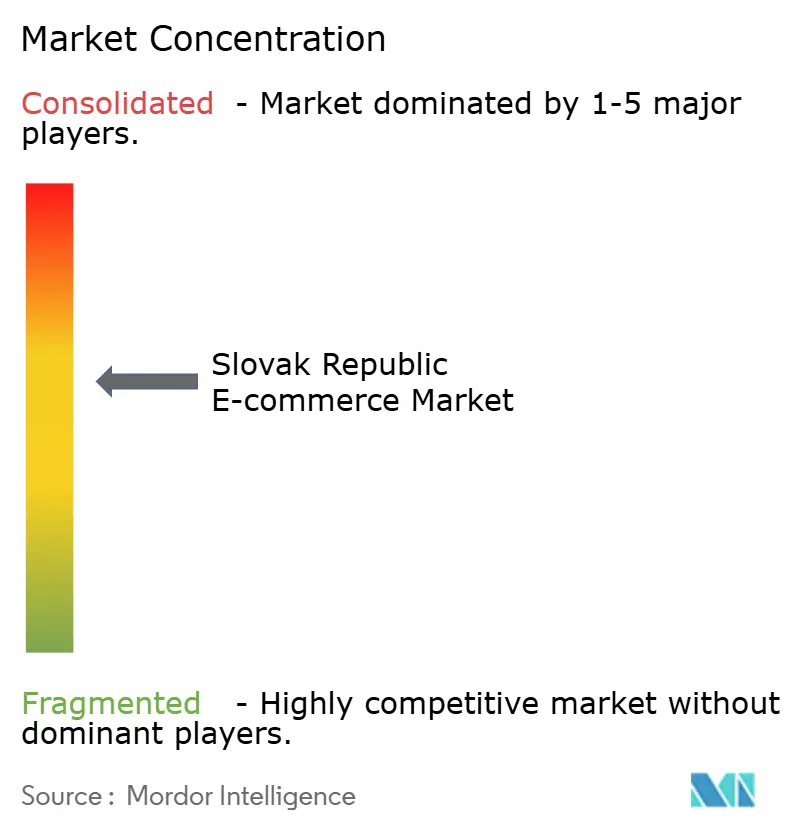

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Slovak Republic E-commerce Market Analysis by Mordor Intelligence

The Slovakia e-commerce market size is expected to grow from USD 2.56 billion in 2025 to USD 2.84 billion in 2026 and is forecast to reach USD 4.74 billion by 2031 at 10.81% CAGR over 2026-2031. Sustained smartphone penetration, widespread 5G coverage and rising comfort with instant payments keep digital spending on a steep upward curve, while higher parcel-locker density and streamlined cross-border pricing rules reduce frictions for both buyers and sellers. Domestic platforms continue to leverage same-day delivery as a loyalty lever, whereas international entrants gain ground through aggressive pricing and brand variety. Regulatory actions—ranging from mandatory instant payments to higher VAT—raise compliance costs yet also catalyze technology upgrades that improve user experience and security. Overall, the Slovakia e-commerce market is moving from early-growth to scale-out phase, with performance now driven by logistics precision, payment flexibility and customer trust rather than basic internet access.

Key Report Takeaways

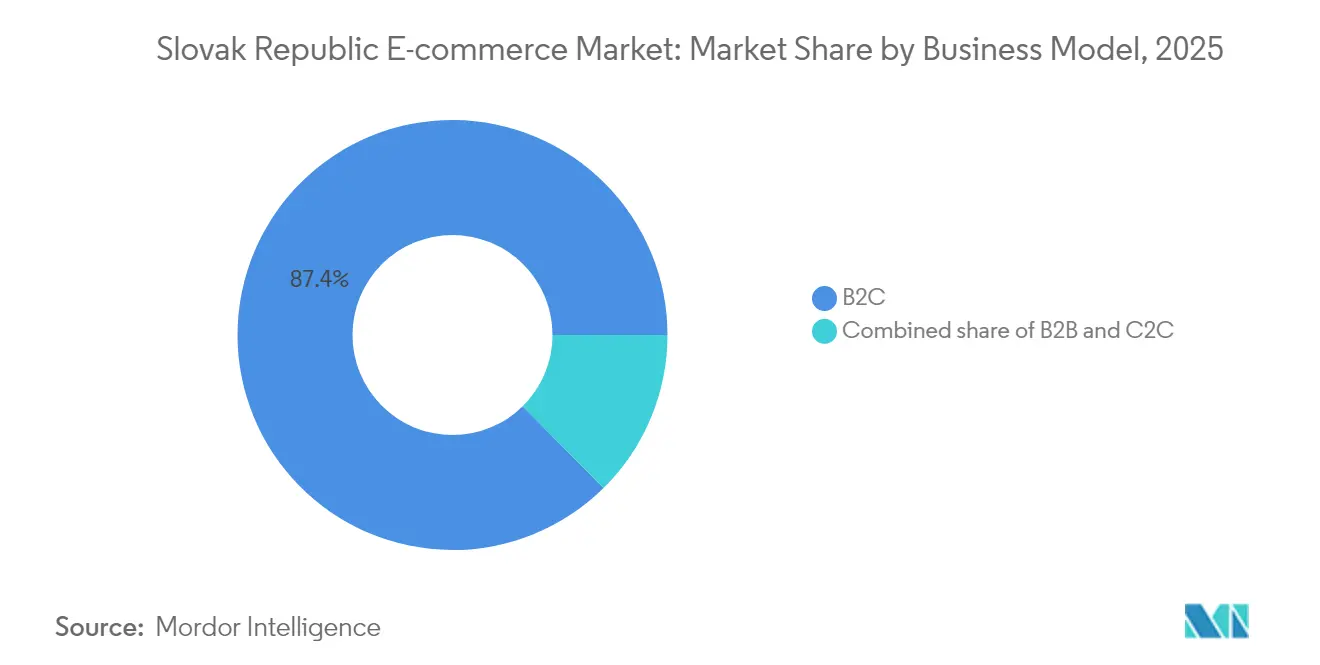

- By business model, the B2C segment captured 87.40% of Slovakia e-commerce market share in 2025, while B2B is projected to register the fastest 14.67% CAGR through 2031.

- By device type, smartphones commanded 55.30% of the Slovakia e-commerce market size in 2025 and are projected to grow at a 12.63% CAGR to 2031.

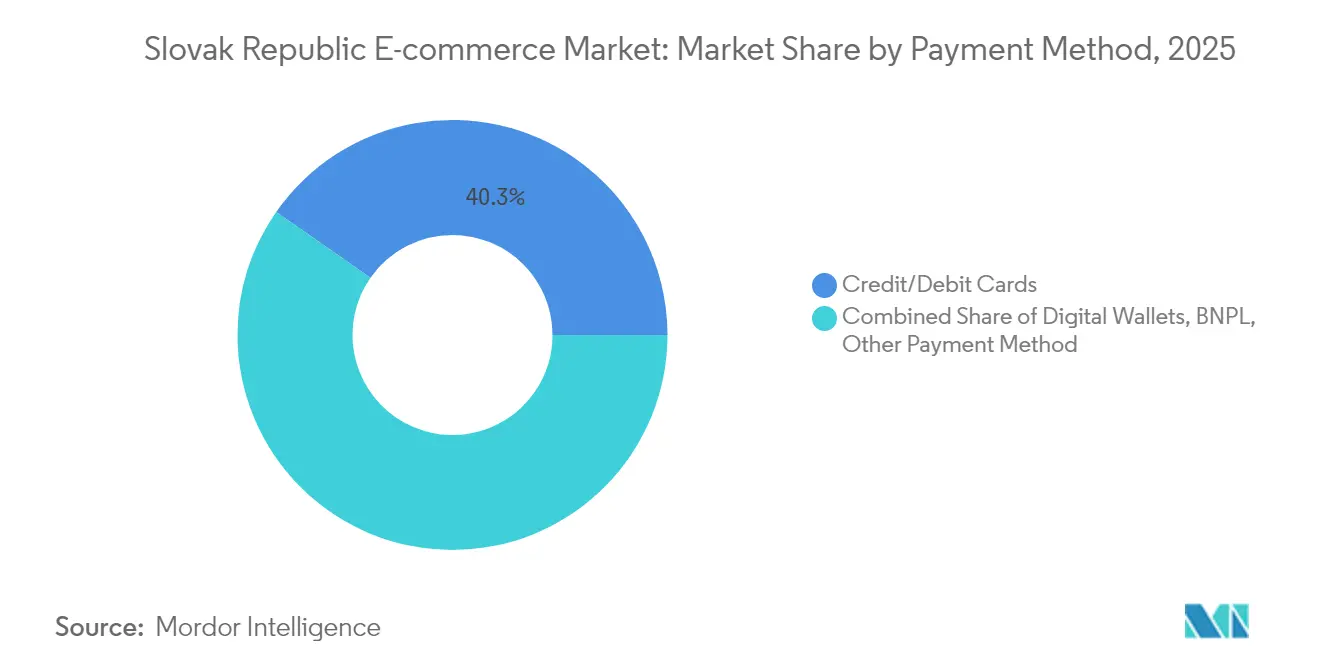

- By payment method, credit and debit cards held 40.30% share of the Slovakia e-commerce market size in 2025, while Buy-Now-Pay-Later is set to advance at 13.31% CAGR through 2031.

- By product category, fashion and apparel led with 25.90% revenue share in 2025; food and beverage is forecast to expand at a 12.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Slovak Republic E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Parcel-Locker Density Accelerating Rural Last-mile Delivery | +1.8% | National, with concentrated gains in rural regions and smaller cities | Medium term (2-4 years) |

| EU Cross-border Price-Transparency Regulation Propelling Online Price Competition | +1.2% | EU-wide, with spillover effects in cross-border trade corridors | Short term (≤ 2 years) |

| Buy-Now-Pay-Later (BNPL) Uptake Elevating Average Order Values | +2.1% | National, with higher adoption in urban centers and younger demographics | Short term (≤ 2 years) |

| Domestic Marketplaces' Same-day Delivery Programs Boosting Consumer Trust | +1.5% | Urban centers, expanding to suburban areas | Medium term (2-4 years) |

| Nation-wide eID & Qualified Trust Services Simplifying Digital On-boarding | +0.9% | National, with enhanced impact in B2B segments | Long term (≥ 4 years) |

| 5G Coverage Expansion Catalyzing Mobile-Commerce Growth | +2.3% | National, with priority deployment in major cities and industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Parcel-locker density accelerating rural last-mile delivery

More than 1,400 pick-up points and 300 automated lockers run by Packeta enable rural shoppers to collect parcels without premium surcharges, lowering the traditional delivery cost penalty by nearly 35%. Locker locations near bus terminals and retail hubs compress the “last-mile” distance, which in turn shrinks fulfilment time and carbon emissions. Packeta reported a doubling of its Slovak customer base over 2021-2024, a signal that dependable rural service converts latent demand into actual orders. Logistic firms also benefit from higher drop-density ratios that enhance load factors and curb vehicle kilometres. As the EU Green Deal rewards low-emission distribution, continued locker deployment is expected to stay on strategy for both operators and policymakers.

EU cross-border price-transparency regulation propelling online price competition

Since mid-2024 all merchants shipping into Slovakia must display duties, taxes and delivery fees upfront, closing loopholes that once let overseas sellers mask true landed costs.[1]Global VAT Compliance, “EU E-commerce VAT Package,” globalvatcompliance.com Domestic platforms that already complied with VAT disclosure now appear more trustworthy, narrowing the perception gap with large foreign marketplaces. The regulation arrives concurrently with Slovak VAT rising from 20% to 23%, making transparent pricing a source of differentiation rather than a mere legal tick-box. Early analytics show basket-abandonment rates dropping by 4-5 percentage points on sites that highlight final checkout totals. Competitive pressure thus shifts from hidden discounts toward service quality and speed, a shift favourable to local merchants with lean logistics.

Buy-Now-Pay-Later uptake elevating average order values

BNPL volumes are compounding at 13.49% through 2030, outpacing overall online payment growth and lifting retailer ticket size by 25–40%. Young Slovaks prefer instalment structures that carry no revolving-credit interest yet preserve monthly cash flow, a behaviour consistent with wider euro-area caution toward consumer debt. Surveys suggest BNPL does not cannibalise card usage but instead layers on top, giving merchants multiple levers to convert shoppers. Regulatory guardrails that mandate clear repayment schedules have increased confidence and reduced default risk, making BNPL both a revenue and retention tool.

Domestic marketplaces’ same-day delivery programs boosting consumer trust

Alza.sk and Mall.sk now guarantee same-day windows in Bratislava and Košice, supported by micro-fulfilment hubs located inside city limits. Academic modelling shows customer satisfaction scores rising 15–20% when deliveries arrive within six hours, creating a durable loyalty advantage. Local players can execute these promises at lower cost than cross-border rivals that ship from distant warehouses. During peak periods such as Black Friday, domestic carriers maintain 98% on-time performance, outclassing global averages by a full six points. Same-day service has therefore morphed from luxury perk to baseline expectation in the Slovakia e-commerce market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cash-on-Delivery Dependence Escalating Reverse-Logistics Costs | -1.4% | National, with higher impact in rural and older demographic segments | Short term (≤ 2 years) |

| Warehousing Shortfall along D1 Corridor Constraining Peak-season Fulfilment | -0.8% | Western Slovakia, particularly Bratislava-Trnava corridor | Medium term (2-4 years) |

| VAT-Fraud Scrutiny on Third-Country Parcels Raising Compliance Burden | -1.1% | National, with higher impact on cross-border e-commerce operations | Short term (≤ 2 years) |

| IT-Talent Shortage Inflating Platform Modernisation Costs | -0.9% | National, with concentrated impact in Bratislava and major urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cash-on-delivery dependence escalating reverse-logistics costs

Although digital wallets and cards keep gaining share, 52% of Slovak shoppers still opt to pay at the door, mirroring euro-area cash habits.[2]European Central Bank, “Cash Usage in the Euro Area 2024,” ecb.europa.eu COD adds an extra 15–25% to per-parcel logistics expense because failed deliveries and refunds trigger two-way transport. The April 2025 financial-transaction tax ironically nudges consumers toward cash withdrawals, possibly reinforcing COD rather than reducing it. Higher operational costs squeeze SME margins, curtailing their ability to invest in user-experience upgrades. Short-term relief depends on incentive schemes such as discounted shipping for prepaid orders and loyalty rewards for card usage.

Warehousing shortfall along D1 corridor constraining peak-season fulfilment

Prime-grade space along the Bratislava-Trnava logistics hot-spot is less than 3% vacant, forcing e-commerce operators into secondary facilities that lack high-bay racking and automation interfaces. Seasonal compression—from Singles’ Day through post-Christmas returns—exacerbates capacity gaps, leading to stockouts or delayed dispatch. Wildberries’ planned EUR 200 million (USD 217 million) investment in a new distribution centre highlights both the opportunity and capital requirement.[3]EurobuildCEE, “Wildberries to Build New Slovak Hub,” eurobuildcee.com Until new platforms come online, merchants mitigate risk by staging buffer inventory in Czech or Austrian hubs, adding cross-border complexity and customs breakpoints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2C scale dominates while B2B gains digital tailwinds

B2C transactions accounted for 87.40% of total online turnover in 2025, equating to a Slovakia e-commerce market size of USD 2.24 billion. Fast checkout flows, personalised recommendations and loyalty wallets keep the mass-market flywheel spinning. Alza.sk alone recorded USD 412.6 million in domestic revenue and 17% annual growth, buoyed by its same-day delivery pledge and cash-back scheme. Household consumption still propels the bulk of GMV; however, consumer surveys reveal that 87% of Slovaks weigh inflation when considering discretionary buys, so platforms now emphasise bundled promotions and low-cost parcel options to protect basket value.

The B2B channel’s 14.67% CAGR signals structural change rather than cyclical lift. Only 13% of Slovak SMEs sold online in 2024, yet government digital-voucher programs financed by EUR 2.3 billion (USD 2.44 billion) public funds aim to close this gap. Corporate buyers appreciate e-catalogue self-service, instant invoice generation and integration with ERP suites. Cross-docking and consolidated pallet shipping reduce per-order costs against the still-fragmented COD norm in consumer trade. As eID infrastructure matures, vendor onboarding times shorten, making electronic procurement more attractive for municipalities and large enterprise frameworks.

By Device Type: Mobile commerce sets the pace for omnichannel conversions

Smartphones generated 55.30% of 2025 web sales and are projected to climb at 12.63% CAGR through 2031, taking the largest slice of Slovakia e-commerce market share. Users cite frictionless biometric login and one-click payment tokens as top purchase enablers. Average session times on mobile apps reached 10.4 minutes, eclipsing desktop averages by 28%. Retailers now roll out progressive web apps that cache catalogue content, shave load times and maintain functionality in low-signal rural areas.

Desktop and laptop still handle high-value B2B orders and configurator-heavy purchases such as consumer electronics, keeping a 35.10% contribution to GMV. Voice-assisted shopping via smart speakers is nascent but grows in double digits among affluent households. The extension of 5G to 80% of the populace places Slovakia in the top quartile of European speed indices, underscoring the long-term case for immersive video commerce and AR fittings.

By Payment Method: Cards secure primacy yet alternative rails surge

Card rails captured 40.30% of total 2025 payments, giving them the biggest slice of Slovakia e-commerce market size in monetary terms. The Single Euro Payments Area (SEPA) Instant scheme, made compulsory in 2025, now clears transfers in under 10 seconds, making bank-to-bank a credible substitute for wallets. Although adoption is still formative, merchant service fees average one-third of card interchange, creating margin headroom.

BNPL gross merchandise value, while only 7% of payments, is expanding at 13.31% CAGR as Generation Z prioritises budget smoothing over classic credit. Providers deploy AI-based risk scoring that mines open-banking APIs rather than legacy bureau files, cutting default probability by 20 basis points. Digital-wallet share also edges up, helped by biometric tokens embedded in Android and iOS secure enclaves. The April 2025 tax on cash withdrawals nudges consumers toward non-cash methods, yet COD stubbornness holds in rural areas where broadband access lags.

By B2C Product Category: Fashion leads, food accelerates

Fashion and apparel retained 25.90% category share in 2025, equal to USD 663.2 million of the Slovakia e-commerce market size. Fast-fashion imports coexist with a rising cohort of local labels curated by the Slovak Fashion Council, which aggregates discovery into a national design map. Shein’s 31.6% growth proves that price-sensitive demand remains potent, but circular models such as second-hand marketplaces grow briskly, echoing Generation Z sustainability priorities.

Food and beverage revenue is smaller at present but is on track for a 12.42% CAGR, the highest in any category. COOP Jednota’s EUR 2.042 billion (USD 2.16 billion) turnover includes 24/7 automated stores and dark-store fulfilment that meet same-day delivery benchmarks. Convenience gaps—less than one-hour windows and temperature-controlled packaging—are being tackled with AI-powered routing and micro-fulfilment robotics. Electronics, beauty and furniture keep steady single-digit expansion, each benefiting from embedded AR product visualisation and bundled service add-ons such as extended warranties or assembly.

Geography Analysis

Slovakia occupies a strategic node on the European trade lattice, with the D1 motorway and the TEN-T Rhine-Danube corridor funnelling goods between Western markets and the Balkans. In 2024 the corridor handled 68% of national parcel volume, giving the Bratislava-Trnava zone a logistics density unmatched in the region. EU membership means frictionless customs clearance for most inbound flows, yet the VAT hike to 23% forces merchants to fine-tune price points relative to Czech and Austrian competitors.

GDP advanced 2.0% in 2024 and is projected to post 1.8% growth in 2025, a stability that bodes well for discretionary e-spend. Services contribute 58.5% of output and employ 62% of workers, reinforcing a consumer-centric ecosystem that drives the Slovakia e-commerce market. Urbanisation levels above 53% funnel demand into compact city cores where micro-fulfilment and bicycle couriers operate efficiently.

Cross-border shopping remains a sizeable slice of GMV; German, Czech and Austrian web shops enjoy linguistic affinity and fast truck routes. Amazon.de is the de-facto gateway for long-tail items lacking local supply. The EU Digital Single Market agenda, covering data-flow harmonisation and consumer-rights alignment, lowers hurdles for Slovak sellers seeking out-bound expansion. Conversely, these same policies intensify rivalry at home, pushing domestic players to double down on customer intimacy and value-added services.

Regulatory Landscape

Slovak e-commerce operators work under a layered compliance framework that combines Act No. 22/2004 Coll. on Electronic Commerce with consumer-rights enforcement led by the Slovak Trade Inspection (SOI). A near-term milestone is Act No. 108/2024 Coll. on Consumer Protection, which adds obligations for online marketplaces and e-shops effective July 31, 2026, covering information duties, complaint handling, and marketplace transparency.

Tax and reporting rules for digital commerce are also tightening. Act No. 384/2025 Coll. sets revenue registration via the eKasa system (with oversight and certifications linked to the Financial Directorate), while the Ministry of Finance submitted a draft VAT Act amendment on May 27, 2026 to incorporate measures from the EU VAT in the Digital Age (ViDA) package. The draft includes a move toward mandatory B2B e-invoicing from January 1, 2027, plus updates affecting platform-economy VAT treatment. Separately, Digital Services Act (DSA) enforcement in Slovakia is anchored by the Council for Media Services for illegal-content compliance under the media-services framework.

Value Chain Analysis

The Slovak e-commerce value chain runs from merchant onboarding and catalog operations (webshops and marketplaces) to payment acceptance (cards, SEPA Instant transfers, wallets and BNPL), then order orchestration, fulfillment, and last-mile delivery through home and out-of-home networks. Platform tooling is increasingly supported by regional enablers such as Shoptet, while marketplaces use their reach to aggregate demand. The April 2026 Shoptet-Allegro partnership shows how storefront software, marketplace access, and cross-border selling are bundled to reduce go-to-market friction for SMEs.

Warehousing and transport capacity are still the main operational bottlenecks and differentiators. Larger players are investing in high-throughput hubs and urban-proximity formats: Alza inaugurated its SKLC3 logistics center in Bernolakovo in February 2026 (86,000 sq m) and then added a connected showroom footprint in Bernolakovo in April 2026. This sequence tightens the link between fulfillment speed, pickup convenience, and customer experience. Parcel networks, including locker and pickup-point operators such as Packeta, and grocery fulfillment tied to store assets (for example, Tesco Online Nakupy) shape last-mile economics. Fiscal and data-reporting requirements, including eKasa under Act No. 384/2025, also feed back into POS, ERP, and checkout integration choices across merchants and logistics partners.

Competitive Landscape

The top five platforms account for an estimated 68% of online revenue, signalling a moderately consolidated playing field. Alza.sk leads with USD 412.6 million, followed by Mall.sk at USD 99.5 million and Dr. Max at USD 79 million; together they hold roughly 40% share. International fast-fashion entrant Shein posted 31.6% growth but remains a mid-tier player by turnover. Competitive vectors have shifted from pure price toward speed, assortment curation and digital identity integration.

Strategic investments concentrate on fulfilment automation and AI-driven personalisation. Dr. Max leverages prescription-history analytics to suggest wellness bundles, achieving 55% online revenue growth in 2024. Alza.sk retrofitted its Bratislava hub with autonomous mobile robots that lift pick-rates to 350 units per hour. Mall.sk’s marketplace pivot opens its platform to third-party sellers, mitigating inventory risk and broadening SKU depth.

M&A and funding flows underline a race for logistics scale. Wildberries plans a EUR 200 million (USD 217 million) Slovak distribution facility, while Rohlik Group secured USD 170 million in fresh equity to speed expansion into new Slovak cities. Zebra Technologies’ acquisition of local 3D vision firm Photoneo tightens the technology supply chain around warehouse robotics. Looking ahead, ESG credentials such as low-carbon delivery and recyclable packaging may become decisive differentiators as EU taxonomy disclosures filter into consumer perception.

Slovak Republic E-commerce Industry Leaders

Alza.sk

Itesco.sk

Nay.sk

H&M (HM.com/sk)

Mall.sk

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-led digitization is opening a tangible systems-upgrade window across Slovak online retail. The Ministry of Finance consultation draft (May 27, 2026) to incorporate ViDA measures into the VAT Act, including mandatory B2B e-invoicing from January 1, 2027 and changes tied to the platform economy, increases demand for invoice automation, tax determination, and digital data reporting capabilities that can be connected to ERP and marketplace back ends. At the same time, mandatory revenue registration via eKasa under Act No. 384/2025 Coll. (from January 1, 2026) keeps pressure on merchants, marketplaces, and solution providers to standardize checkout, payment capture, and reporting workflows.

In execution terms, the clearest opportunity clusters around where Slovakia is already investing and where current constraints are documented: high-throughput fulfillment and faster urban delivery, alongside simplified cross-border selling. Capacity moves by leaders, including Alza's Bernolakovo logistics buildout in 2026, point to continued investment in automation-ready hubs. Partnerships such as Shoptet with Allegro in April 2026 also show active effort to reduce technical friction for SMEs to expand beyond Slovakia. Government digital-transformation steering by MIRRI SR, through national roadmaps aligned to the EU Path to the Digital Decade, supports further adoption of digitized public and business services. This reinforces demand for identity-enabled onboarding, secure payments, and interoperable commerce tooling, particularly across the under-penetrated SME segment selling online.

Recent Industry Developments

- June 2026: Alza.sk opened its first physical AlzaBeauty shop in Bratislava (OC Nivy), expanding into a specialized omnichannel format with a curated assortment of beauty products and brands. The move broadens category depth beyond electronics-led roots and uses a high-footfall location to convert offline discovery into online replenishment and loyalty.

- March 2025: Heureka Group partnered with GoWit to deploy data-driven retail media across multiple Central European countries, including Slovakia. The rollout helps merchants monetize marketplace and comparison-shopping traffic through targeted advertising while adding a new performance marketing lever tied to on-platform conversion signals.

- December 2024: Zebra Technologies agreed to acquire Slovak 3D-vision specialist Photoneo to strengthen capabilities used in warehouse automation. The deal tightens access to machine-vision components that support faster picking, sorting, and quality control, which are central to high-throughput e-fulfillment operations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this methodology, the Slovak Republic e-commerce market is defined as the value of goods and services that are ordered through online portals by end users in Slovakia. The order is placed digitally and the transaction is completed through an online checkout.

Scope exclusions: This sizing excludes pure digital content downloads, online gambling, and informal social-media trading. It also avoids counting loyalty-app-only spending and marketplace GMV as direct sales.

Segmentation Overview

- By Business Model

- B2C

- B2B

- C2C

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us set the boundary and build a clean demand story before any calculations were finalized. We relied on public statistics and official releases that signal online retail activity and household spending, such as Eurostat, the Statistical Office of the Slovak Republic, the European Commission, and OECD datasets.

To avoid over-counting, we also reviewed payment and delivery related indicators and sector notes from sources such as the National Bank of Slovakia, customs and trade statistics, and public documents from postal and logistics bodies. Company filings, investor presentations, and credible business press were used to validate how fast the online channel mix is shifting and how promotional intensity impacts average order values. In addition, paid databases for company financials and news, plus an import/export shipment-level database, were selectively used to cross-check larger retailers and cross-border flows. These are illustrative sources, and many other public documents were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what share of retail demand is captured through digital checkout, and how the mix shifts by category, delivery method, and cross-border buying. We spoke with online sellers, payment and logistics-linked experts, and industry advisors to test assumptions, close gaps from desk research, and confirm whether pricing and return behavior were changing in ways that would affect market value.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 44% |

| Mid tier: 49% | Functional/Unit leaders: 30% | EMEA: 29% |

| Smaller Players: 20% | Managers: 56% | Americas: 27% |

Market-Sizing & Forecasting

The core sizing logic uses a top-down build that starts from Slovakia-level retail and household consumption signals, then reconstructs the online share using observable adoption indicators, followed by category-level splits to keep the total realistic. To keep the outcome grounded, we corroborated totals with selective bottom-up checks, such as sampled retailer revenue ranges, typical average order value patterns, and volume proxies tied to delivery intensity and transaction behavior shared by interviewees.

Key inputs that moved the model included internet shopping penetration, card and digital payment usage in retail, parcel shipment growth for business-to-consumer flows, cross-border online purchase incidence, and price inflation effects that shift basket values. Where direct data was thin, for example for small merchant activity, we used conservative proxying based on comparable retailer mixes and then re-tested the implied spend per online buyer with experts.

For forecasting, scenario analysis was used to reflect how consumer confidence, inflation, and delivery cost changes can push online conversion up or down, and then the selected path was checked against primary feedback on expected discounting and category momentum. The final forecast is therefore not a single mechanical extrapolation, but a set of explained assumptions that can be revisited when new signals appear.

Data Validation & Update Cycle

Validation was done through multiple checks that look for internal consistency and real-world fit. We compared model outputs against independent signals such as household spend trends, parcel and delivery growth, and observed shifts in payment usage, and then reviewed any large variances before numbers were finalized.

Anomalies, like sudden jumps in implied spend per buyer or unrealistic category shares, were flagged for analyst review and corrected only after re-checking the underlying drivers and re-contacting sources when needed. Reports are refreshed annually, and interim updates are made when material events occur that can move demand or pricing. Before delivery, a final analyst pass is completed to ensure the estimates reflect the latest available data and assumptions.

Mordor Intelligence's Slovak Republic Ecommerce Market Size Compared Against Other Published Estimates

Published values for Slovakia e-commerce often do not match because teams choose different definitions of what counts as an online sale. They also vary in how they treat cross-border buying, returns, and taxes in the final value.

Payment usage shifts, parcel flow growth, and the implied online spend per buyer are the practical checks that keep Mordor Intelligence aligned to orders that go through a true digital checkout, which reduces the risk of inflating totals by mixing in marketplace GMV or informal commerce.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.56 B (2025) | |

| Industry Association A | USD 2.90 B (2025) | This figure commonly counts marketplace GMV and seller-to-seller marketplace transactions as direct e-commerce value, and it is often reported closer to gross merchandise value rather than checked-out sales net of cancellations. |

| Trade Journal B | USD 2.10 B (2025) | This estimate typically uses a narrower retail-only scope and may exclude cross-border purchases delivered into Slovakia, and it can also apply conservative assumptions on online share progression during high inflation periods. |

The spread in values mainly comes from what is included in the online sales boundary and how cross-border and marketplace activity is treated in the math. By tying the market total back to observable demand signals and then re-checking the implied spend logic with primary respondents, the estimate stays traceable to clear steps and can be repeated when new data is released.

Key Questions Answered in the Report

What is the current size of the Slovakia e-commerce market?

The market generated USD 2.84 billion in 2026 and is on track to reach USD 4.74 billion by 2031.

Which business model leads online sales in Slovakia?

B2C accounts for 87.40% of sales, though B2B is expanding rapidly at a 14.67% CAGR.

How important is mobile commerce in Slovakia?

Smartphones already drive 55.30% of transactions and will grow at 12.63% CAGR as 5G coverage expands.

Which payment method is growing fastest?

Buy-Now-Pay-Later is the fastest riser, advancing at 13.31% CAGR while lifting average order values.

What category shows the highest growth potential?

Online food and beverage sales are forecast to grow at 12.42% CAGR, the quickest among product groups.

Who are the dominant players in the Slovakia e-commerce industry?

Alza.sk, Mall.sk and Dr. Max together hold about 40% of revenue, with Shein and Wildberries emerging as aggressive challengers.

Page last updated on: