Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

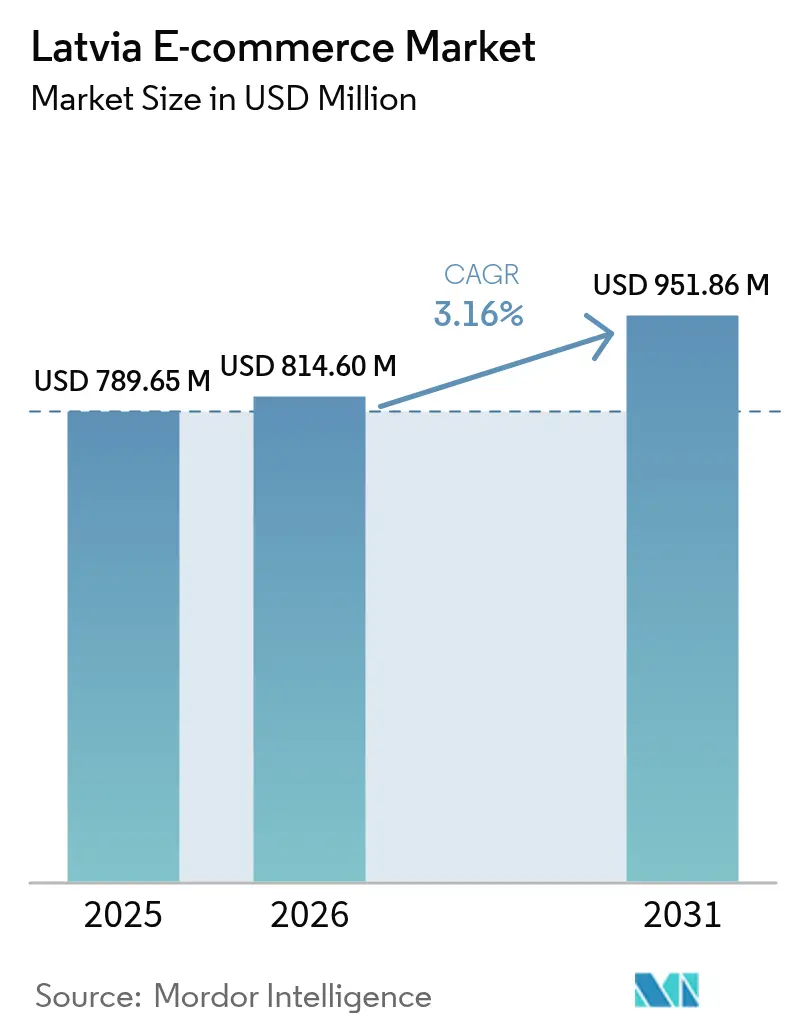

| Base Year Market Size (2025) | USD 789.65 Million |

| Market Size (2026) | USD 814.60 Million |

| Market Size (2031) | USD 951.86 Million |

| Growth Rate (2026 - 2031) | 3.16% CAGR |

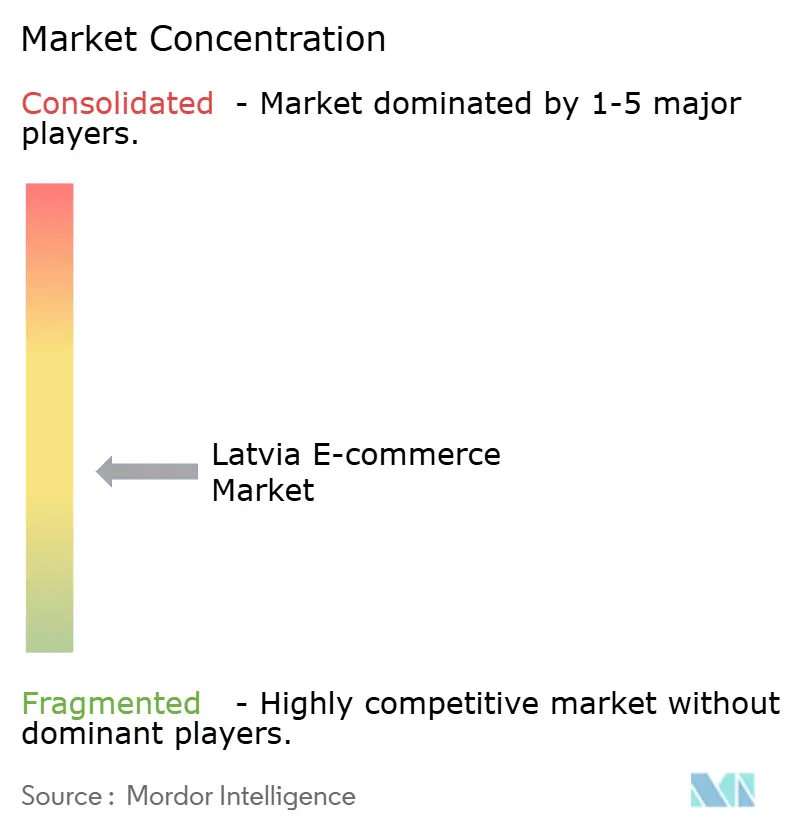

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latvia E-commerce Market Analysis by Mordor Intelligence

The Latvia e-commerce market size was valued at USD 789.65 million in 2025 and estimated to grow from USD 814.6 million in 2026 to reach USD 951.86 million by 2031, at a CAGR of 3.16% during the forecast period (2026-2031). Stable broadband connectivity, 5G roll-outs, and a population in which 62% already shop online keep demand resilient even as headline inflation moderates. Mobile devices dominate check-out journeys, while mandatory e-invoicing rules are accelerating digital procurement among firms. Payments innovation—especially instant transfers and BNPL—supports basket-conversion, and a dense parcel-locker network sustains next-day delivery expectations in urban Riga, Liepāja, and Daugavpils. However, ageing demographics and rural last-mile gaps temper the overall growth rate of the Latvia e-commerce market.

Key Report Takeaways

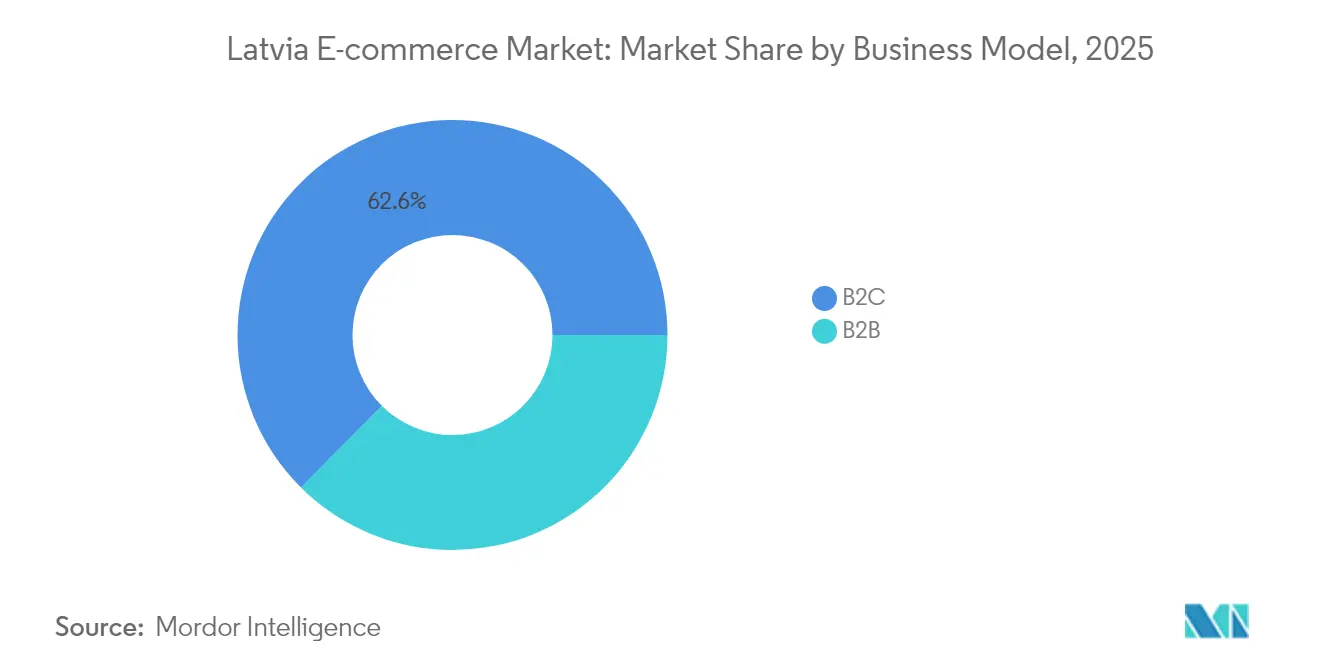

- By business model, B2C commanded 62.55% of the Latvia e-commerce market share in 2025, while B2B is projected to expand at 4.95% CAGR to 2031.

- By device type, smartphones captured 57.62% revenue share of the Latvia e-commerce market in 2025; mobile transactions are pacing ahead at a 5.88% CAGR through 2031.

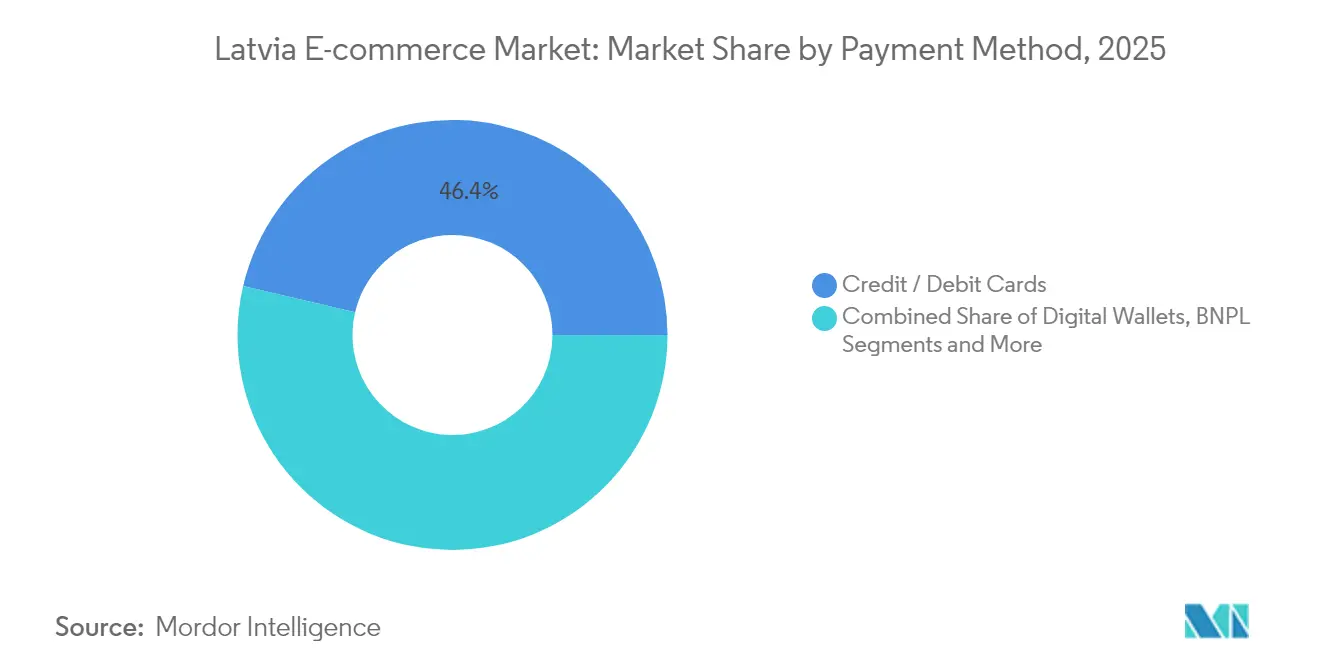

- By payment method, credit/debit cards accounted for 46.35% share of the Latvia e-commerce market size in 2025, whereas BNPL solutions are growing at 5.03% CAGR to 2031.

- By product category, fashion and apparel led with 12.32% of the Latvia e-commerce market share in 2025; food and beverages is on track for a 6.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Latvia E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing number of e-shoppers | +3.1% | National, with higher impact in urban centers | Medium term (2-4 years) |

| Rising internet penetration and 5G rollout | +1.1% | National, with early gains in Riga, Jurmala, Liepaja | Medium term (2-4 years) |

| Expansion of instant and card-based digital payments | +0.8% | National | Short term (≤ 2 years) |

| Rapid adoption of Buy-Now-Pay-Later and SEPA instant transfers | +0.6% | National, with higher impact in urban areas | Short term (≤ 2 years) |

| AI-driven price comparison boosting marketplace traffic | +0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Number of E-shoppers

Latvia’s online-buyer ratio climbed to 65% of the population in 2024, up from 51% in 2021. Senior citizens are increasingly comfortable purchasing via digital channels, expanding the accessible customer pool and forcing merchants to design intuitive storefronts and plain-language service menus. Roughly 42.17% of residents now buy online at least once a month, generating 10.1% of national retail revenue and contributing 1.5% to GDP. Retailers are responding with simplified sign-in flows, guest check-out options, and wider SKU ranges. Loyalty programs are shifting from points to experiential rewards—early access or free locker delivery—to retain this broader demographic.

Rising Internet Penetration and 5G Rollout

Latvia’s operators are scaling 5G, with Bite Latvia aiming for 75% population reach. Faster uplinks enhance live-commerce streams and AR product demos, reinforcing mobile conversion. LMT’s private 5G network at Baltic Container Terminal demonstrates industrial use-cases, lowering dwell times for sea-freight and shortening e-commerce lead times. Public funds of EUR 16.5 million (USD 17.9 million) target gigabit speeds in underserved rural nodes, reducing the urban-rural digital divide that constrains the Latvia e-commerce market.

Expansion of Instant and Card-Based Digital Payments

Twenty-one percent of euro-area day-to-day transactions took place online in 2024, up from 17% in 2022. [1]European Central Bank, “Study on the Payment Attitudes of Consumers in the Euro Area (SPACE) 2024,” ecb.europa.eu Latvian issuers now support 24/7 card clearing and SEPA instant transfers across 53% of current accounts. Real-time settlement shrinks merchant cash-conversion cycles and reduces chargeback risk. Checkout pages offering one-tap card tokenization report lower cart abandonment, especially on mobile screens. Merchants also capitalize on lower acquirer fees for SEPA instant rails relative to legacy card interchange.

Rapid Adoption of Buy-Now-Pay-Later and SEPA Instant Transfers

BNPL volumes are projected to grow 5.20% CAGR, unlocking demand among credit-averse consumers. Installment options raise average order values for consumer electronics and furniture. The EU Instant Payments Regulation encourages pan-European real-time rails, cutting Borderless transfer costs. Latvian gateways that combine BNPL scoring with instant-credit disbursement see improved approval rates and faster merchant settlement, critical for SMEs with limited working capital.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU VAT compliance burden for non-EU sellers | -0.6% | National, with higher impact on cross-border commerce | Medium term (2-4 years) |

| Sparse last-mile logistics in rural municipalities | -0.4% | Rural regions, particularly in Latgale and Vidzeme | Medium term (2-4 years) |

| Ageing population limiting basket-value growth | -0.3% | National, with higher impact in regions with older demographics | Long term (≥ 4 years) |

| Parcel-locker saturation squeezing delivery margins | -0.2% | Urban centers, particularly Riga and regional hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU VAT Compliance Burden for Non-EU Sellers

Foreign merchants must register for Latvian VAT from the first euro of turnover, facing upfront compliance costs and local-language filings. While the OSS scheme streamlines quarterly returns, the regime still requires evidence archiving inside the EU for 10 years—a hurdle for small Asian sellers. Intermediary marketplaces pass on the administrative overhead via higher commission, making certain low-margin SKU categories unviable. As a result, product variety narrows and price competition softens, marginally muting growth within the Latvia e-commerce market. Trade bodies lobby for enhanced digital guidance portals in English and simplified small-parcel thresholds, yet material relief remains unlikely before 2027.

Sparse Last-Mile Logistics in Rural Municipalities

Urban Latvia enjoys locker density of up to 1 unit per 1,700 residents, but Latgale averages 1 locker per 9,000 residents. Couriers add fuel surcharges for remote deliveries, inflating shipping fees on bulky goods. Food-and-beverage e-grocers therefore limit service radii, slowing penetration of the fastest-growing category. Pilot drone-drop programs remain at proof-of-concept level because Latvian airspace rules require beyond-visual-line-of-sight exemptions. Until rural hubs achieve critical order density, operators will continue to subsidize journeys, reducing profitability and dragging on the Latvia e-commerce market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Digitalization Accelerates

The B2C segment represented 62.55% of the Latvia e-commerce market in 2025, underscoring its historic dominance in consumer retail. Mandated structured e-invoicing, however, is stimulating the B2B corridor, which is forecast to grow at 4.95% CAGR to 2031. The Latvia e-commerce market size attributable to B2B transactions is projected to approach USD 388.1 million by 2031, driven by procurement portal upgrades and ERP-gateway integrations. Large suppliers are onboarding SMEs through subscription-based catalogs that cut purchase-order cycle times by 70%.

Twenty-eight indigenous B2B platforms operate as of April 2025, with several leveraging Pay-per-invoice financing to improve buyer liquidity. Cross-dock warehouses near the Port of Riga shorten re-export timelines for Baltic trade, enhancing vendor stickiness. Direct-selling models—recording EUR 78 million (USD 83.6 million) in 2024 sales—augment income opportunities for 59,000 micro-entrepreneurs, many of whom adopt hybrid online–offline fulfillment. This convergence blurs the line between retail and wholesale, sustaining a nuanced value chain that underpins the Latvia e-commerce market.

By Device Type: Mobile-First Strategy Dominates

Smartphones generated 57.62% of 2025 transaction value, putting handsets at the center of the Latvia e-commerce market. Average mobile data usage of 13 GB per connection per month enables high-definition product videos and livestream shopping. Latvia e-commerce market size for mobile channels is expected to cross USD 624.8 million by 2031, outpacing desktop at a 5.88% CAGR. Retailers convert impulse traffic by embedding single-click checkout buttons and leveraging biometric authentication.

Desktop still underpins high-ticket B2B orders where procurement officers require multi-tab comparisons. Tablets and smart TVs form a nascent 4% slice, yet are rising on the back of connected-home adoption. Government statistics show 48.2% of SMEs with basic digital skills in 2023, up 12.5 percentage points year-over-year. That capability expansion positions firms to optimize across screen sizes and fuels omnichannel resilience within the Latvia e-commerce market.

By Payment Method: BNPL Disrupts Traditional Options

Cards retained 46.35% share of the Latvia e-commerce market size in 2025, yet BNPL is the momentum story, advancing 5.03% CAGR. Integration of open-banking APIs reduces credit-decision latency to seconds, pushing BNPL approval rates toward 81%. Instant SEPA rails settle both down-payments and subsequent installments, amplifying cash-flow certainty for merchants.

Digital wallets and account-to-account transfers benefit from PSD2 strong-customer-authentication rules that favor tokenized credentials over static PAN data. The digital euro project aims to cap offline payment fees, potentially displacing cash-on-delivery in rural areas and bolstering financial inclusion. As regulation stabilizes, payment mix diversification reduces single-rail dependency, supporting sustainable growth for the Latvia e-commerce market.

By B2C Product Category: Food and Beverages Surge

Fashion and apparel captured 12.32% Latvia e-commerce market share in 2025, fortified by lenient return policies and influencer-driven merchandising. Nevertheless, food and beverages is forecast to post 6.07% CAGR to 2031, lifting its contribution to the Latvia e-commerce market size to nearly USD 146 million. BARBORA fulfilled 2.7 million Baltic orders in 2023, demonstrating the scalability of temperature-controlled logistics.

Consumer electronics keeps momentum due to high digital literacy and AI-augmented comparison sites. Beauty, DIY, and home furnishings ride content-commerce tactics such as virtual try-ons and room-visualizers. Together, long-tail categories buffer overall market volatility, reinforcing diversification in the Latvia e-commerce market.

Geography Analysis

Riga accounts for the lion’s share of the Latvia e-commerce market, supported by superior 5G coverage, average household incomes 19% above the national median, and locker density that ensures sub-24-hour delivery. Daugavpils, Liepāja, and Jelgava trail but exhibit higher growth curves as their retail ecosystems digitalize. Urban parcel-locker installations climbed 22% in 2024, though operators warn of saturation that may compress courier margins.

Rural districts in Latgale and Vidzeme struggle with service frequency; half-empty courier routes increase per-parcel costs, limiting grocery penetration. The government’s Recovery and Resilience Plan finances gigabit backhaul and community locker hubs, expected online by 2027. Cross-border trade flourishes due to Latvia’s role as a Baltic entrée, yet extended shipping intervals from Asian sellers accentuate the merits of European fulfillment nodes.

Logistics reforms at the Port of Riga—bolstered by LMT’s private 5G network—improve container processing and lower demurrage, indirectly enhancing import lead-times for marketplace sellers. As secondary cities mature, geographic revenue dispersion will broaden, embedding regional inclusivity within the Latvia e-commerce market.

Regulatory Landscape

Latvia e-commerce operators operate under a largely EU-harmonized rulebook covering consumer protection, platform governance, and tax compliance. The Consumer Rights Protection Centre (PTAC) oversees distance-selling requirements under the Consumer Rights Protection Law, including mandatory pre-contract disclosures and withdrawal rights, and it also serves as Latvia's Digital Services Coordinator for enforcement of the EU Digital Services Act (DSA), with authority to inspect services and require cessation of infringements.

On the B2B/B2G digitization side, structured e-invoicing and related data submission to the State Revenue Service (VID) is mandatory from 1 January 2026 for B2G, G2G, and G2B, using structured XML aligned to UBL 2.1 and PEPPOL BIS Billing 3.0 (CIUS). Cross-border sellers also face shifting landed-cost rules, with VID noting that from 1 July 2026 the customs-duty exemption for low-value consignments up to EUR 150 is revoked and replaced with a flat EUR 3 duty per item, followed by an additional EUR 2 Union handling fee per declared item from 1 November 2026. This change raises compliance and checkout-price transparency requirements for non-EU shipments.

Value Chain Analysis

Latvia's e-commerce value chain covers demand generation (merchant sites, marketplaces, and performance marketing), transaction enablement (payments, fraud controls, and accounting), and execution (inventory, fulfillment, cross-border clearance, and last mile). Marketplaces and webstores route demand through PSPs and bank rails, where the uptake of instant transfers and BNPL is shaping checkout design, while structured e-invoicing requirements bring accounting and ERP integrations closer to the core transaction flow, especially for B2G/G2B procurement.

Downstream, fulfillment and delivery performance depends on 3PLs and parcel networks and is reinforced by an extensive parcel-locker ecosystem in urban hubs, while rural service density remains a constraint. The ecosystem is also becoming more coordinated through sector collaboration: the Latvian E-commerce Association (LATEKA), launched in 2026 with members spanning merchants and enablers (including logistics and financial services brands), provides a connector for standards, shared practices, and dialogue with authorities. This tightens linkages between platforms, payment providers, and delivery operators.

Competitive Landscape

The Latvia e-commerce market operates in a fragmented setting where the top five players hold about 38% combined revenue. Local champion 220.lv receives 2.5 million monthly visits, leveraging localized UX and same-day locker delivery. Maxima’s BARBORA platform scales dark-store picking for grocery, lifting the chain’s total Latvian revenue beyond EUR 1 billion (USD 1.1 billion) in 2024.

Amazon and AliExpress channel demand for niche electronics and hobby supplies, forcing domestic sites to deepen category expertise and enhance Latvian–language support. November 2024’s merger between Printful and Printify unites two of the country’s headline tech scale-ups, pooling R&D spend on on-demand manufacturing APIs that underpin cross-border merchant services.

Competitive advantage increasingly hinges on AI-driven personalization, express delivery windows, and frictionless payments. Smaller retailers forge alliances with 3PL locker networks to defray last-mile costs. Regulatory oversight by Latvia’s Competition Council—quantified as EUR 51.2 million public benefit per annum—maintains price transparency and curbs anticompetitive behavior, fostering a level playing field for the Latvia e-commerce market.

Latvia E-commerce Industry Leaders

Amazon.com, Inc.

220.lv (Pigu Group)

Alibaba Group – AliExpress

Maxima Latvija SIA (e-Maxima)

Rimi Latvia SIA (Barbora.lv)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Mandatory structured e-invoicing for B2G, G2G, and B2B from 1 January 2026 creates a near-term opportunity for e-commerce-adjacent software and service providers that can simplify invoice creation, validation, and submission workflows to VID while keeping merchant and procurement systems aligned with UBL 2.1 and PEPPOL BIS Billing 3.0 (CIUS). It also supports B2B corridor digitization through voluntary adoption that began in March 2026 ahead of the scheduled mandatory B2B requirement in 2028, favoring platforms that bundle catalogs, payments, and compliant invoicing into one flow.

Sector organization and public digital investment provide additional opportunity signals. LATEKA's establishment in May 2026 offers a single industry interface for quality and trust programs and for promoting exportable e-commerce services (development, payments integration, and logistics tooling). In parallel, Latvia's 2026 Digital Decade roadmap cites 43 measures backed by a EUR 2.2 billion budget across areas including cloud, cybersecurity, and AI, supporting vendor demand for secure commerce infrastructure, identity and risk controls, and automation that reduces administrative burden for merchants and public buyers.

Recent Industry Developments

- July 2026: The European Commission fined AliExpress EUR 550 million for illegal product sales and safety non-compliance under the EU Digital Services Act. The decision raises the bar for marketplace governance and seller vetting across Latvia-facing cross-border platforms, pushing more resources toward product safety governance and traceability.

- May 2026: The Latvian E-commerce Association (LATEKA) was established, gathering merchants, logistics and financial services brands to coordinate standards and trust programs. The group provides a single industry interface for quality and exportable e-commerce services, strengthening dialogue with authorities and supporting cross-border trade.

- November 2024: Printful and Printify announced a merger, combining Latvia-linked on-demand manufacturing and e-commerce enablement scale-ups. The consolidation strengthens the upstream merchant-services layer that supports cross-border selling from Latvia-based ecosystems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the Latvia e-commerce market is defined as the value of goods and services purchased through online channels where the order is placed digitally and the transaction is tied to Latvia-based demand and fulfillment flows.

Scope exclusions: This sizing excludes purely peer-to-peer classifieds transactions, ride-hailing, and third-party meal delivery orders that are booked through apps or platforms.

Segmentation Overview

- By Business Model

- B2C

- B2B

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with public signals that describe Latvia's online buying behavior and the overall retail environment. We refer to official statistics on ICT usage and online purchasing from Latvia's Central Statistical Bureau, along with Eurostat retail trade series for context on turnover, seasonality, and macro shifts that can spill over into online sales.

To keep the model grounded, we also use sources such as Bank of Latvia and ECB releases for payment trends, Universal Postal Union and postal operator publications for parcels and delivery capacity, and International Telecommunication Union indicators for connectivity and broadband coverage. Company annual reports, investor presentations, and reputable press are used to understand category mix, discounting intensity, and channel changes. In a few cases, paid databases are used for company financials and news screening, and for patent lookups when digital commerce features and payments innovations need confirmation. This list is not exhaustive, and many other sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to test what the desk research cannot fully answer, especially around the split between domestic and cross-border orders, the typical order value, and how fast mobile checkout is growing. We speak with marketplace operators, webstore managers, logistics and parcel network participants, payment ecosystem experts, and category specialists across Latvia, and then we re-check key assumptions with buyers and channel-side contacts where needed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 15% | APAC: 48% |

| Mid tier: 55% | Functional/Unit leaders: 32% | EMEA: 29% |

| Smaller Players: 20% | Managers: 53% | Americas: 23% |

Market-Sizing & Forecasting

Sizing uses a top-down and bottom-up mix, where the main build starts from Latvia's retail and online shopping penetration signals and then gets translated into an e-commerce value pool using category weights and average order value checks. When the market total is formed, it is corroborated with selective bottom-up approximations such as sampled webstore revenue ranges, marketplace GMV indicators where available, and channel checks on order volumes multiplied by realistic price baskets.

A few inputs that matter in Latvia include the share of residents buying online, parcel and delivery throughput trends (including locker usage patterns), the domestic versus cross-border share of orders, payment method shifts (cards, instant transfers, BNPL), and the mix of higher ticket categories such as electronics versus frequent purchase categories such as personal care. Where a variable is missing for a specific year, we use a conservative interpolation anchored to known official time series, and then confirm the direction through primary feedback.

Forecasting is done using scenario analysis with an exponential smoothing backbone, because adoption and spending tend to move steadily but can swing with inflation and promotions. Assumptions for growth are reviewed with local experts, and then we test the outputs against expected internet user growth and retail demand conditions before finalizing the curve.

Data Validation & Update Cycle

Validation is handled through multiple checks so that one data series does not over-influence the final number. We compare the model outputs with independent signals such as online buyer penetration, parcel activity direction, and retail trend indicators, and then we investigate any large variance before sign-off.

A second analyst review is applied to the key assumptions, including the domestic and cross-border split and average order value progression, followed by a final logic check on currency conversion timing and year alignment. The report is refreshed annually, and interim updates are triggered when material events show up, such as tax or invoicing changes, sharp shifts in logistics capacity, or major payment adoption moves. Before delivery, we run a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Latvia Ecommerce Market Estimate Compared With Other Published Estimates

Published estimates for Latvia e-commerce can vary a lot, even when the same country name is used, because the definition of what counts as an online transaction is not always consistent. Differences usually show up in what is included, how cross-border revenue is treated, and whether the number reflects retail goods only or also adds adjacent app-based services.

Ride-hailing and third-party meal delivery are common add-ons in broader digital commerce tallies, and those sit outside Mordor Intelligence's Latvia e-commerce scope, which pushes some public figures higher even before forecasting assumptions are considered. The spread can also come from using GMV versus net revenue, applying aggressive mobile-led growth rates without matching them to Latvia's parcel and payment reality, or converting EUR to USD using different average rates for the year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 789.65 M (2025) | |

| Digital Data Publisher A | USD 805.00 M (2025) | Often presented as retail e-commerce revenue, which can apply different treatments for marketplace sales and cross-border order capture, and may not align to the same service exclusions. |

| Industry Report Studio B | USD 870.00 M (2025) | Typically mixes forecast-led growth with broader digital commerce cues and may use GMV-style totals, which can inflate results when promotions, returns, and platform take-rates are not normalized. |

The table shows that most of the gap is explained by scope and measurement choices, not by a single demand indicator moving sharply in Latvia. By tying the total to clear online purchase participation, parcel and payments signals, and then stress-testing order value assumptions through interviews, the final number stays traceable and repeatable from year to year.

Key Questions Answered in the Report

What is the current size of the Latvia e-commerce market?

The Latvia e-commerce market size is USD 814.6 million in 2026 and is forecast to reach USD 951.86 million by 2031.

Which segment is expanding fastest?

B2B transactions are projected to grow at 4.95% CAGR between 2026 and 2031, spurred by mandatory e-invoicing.

How important is mobile commerce in Latvia?

Mobile devices already generate 57.62% of transaction value in 2025 and are growing at 5.88% CAGR, making mobile optimization a strategic priority.

What payment trends should merchants watch?

Cards still hold 46.35% share in 2025, but BNPL solutions and SEPA instant transfers are gaining traction, lowering abandonment rates.

Which product category shows the highest growth outlook?

Online food and beverages sales are expected to climb at 6.07% CAGR through 2031 as grocery delivery becomes mainstream.

How fragmented is the competitive landscape?

With the top five players accounting for about 38% of sales, the market remains competitive, offering room for niche specialists and new entrants.

Page last updated on: