Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

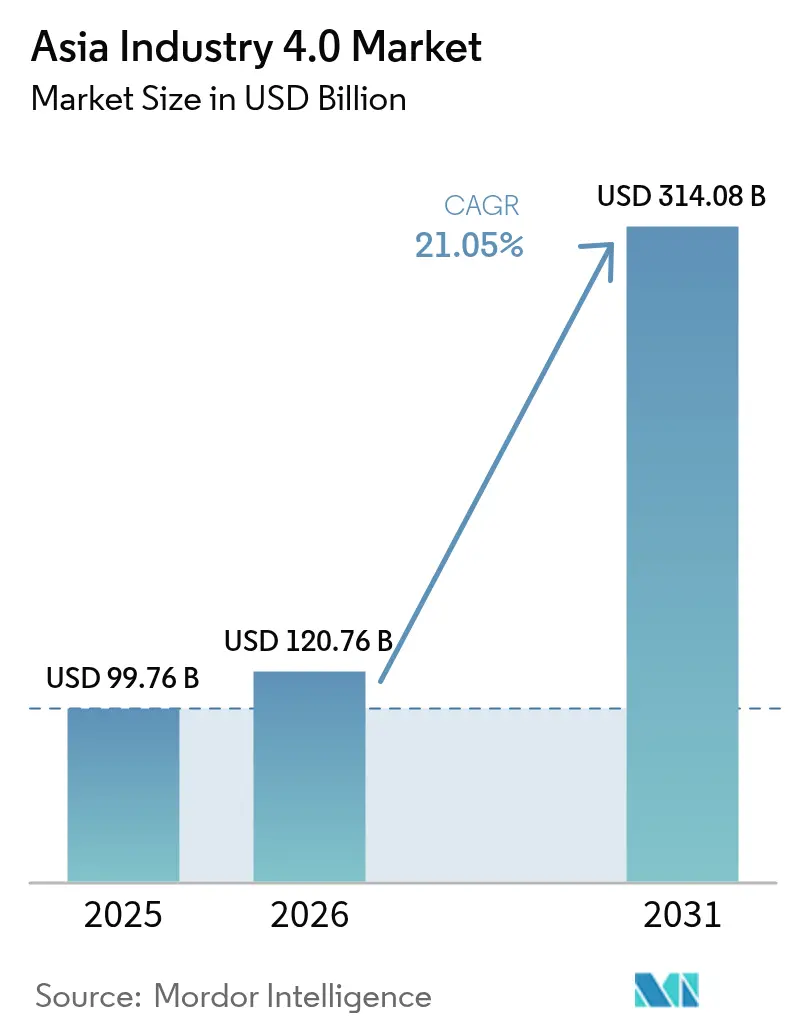

| Base Year Market Size (2025) | USD 99.76 Billion |

| Market Size (2026) | USD 120.76 Billion |

| Market Size (2031) | USD 314.08 Billion |

| Growth Rate (2026 - 2031) | 21.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Asia Industry 4.0 Market by Mordor Intelligence

The Asia Industry 4.0 market size is expected to grow from USD 99.76 billion in 2025 to USD 120.76 billion in 2026 and is forecast to reach USD 314.08 billion by 2031 at 21.05% CAGR over 2026-2031. Government-funded digitalization mandates, rising robotics adoption across electronics and electric vehicle supply chains, and the rapid expansion of private 5G networks collectively accelerate smart factory deployments across the region, positioning the Asia Industry 4.0 market as the global epicenter of digital manufacturing investment. Large enterprises continue to anchor transformative projects, but voucher-based incentives are drawing thousands of small and medium-sized manufacturers into the ecosystem, thereby widening the customer base and fueling additional demand for platform and services. Heightened carbon-neutral commitments and regional supply-chain resilience initiatives are further tilting capital budgets toward data-driven process optimization, advanced analytics, and edge computing solutions. Competitive intensity remains fluid as automation incumbents expand software portfolios while cloud hyperscalers deepen industrial partnerships, fostering a broader, more interconnected vendor landscape across the Asia Industry 4.0 market.

Key Report Takeaways

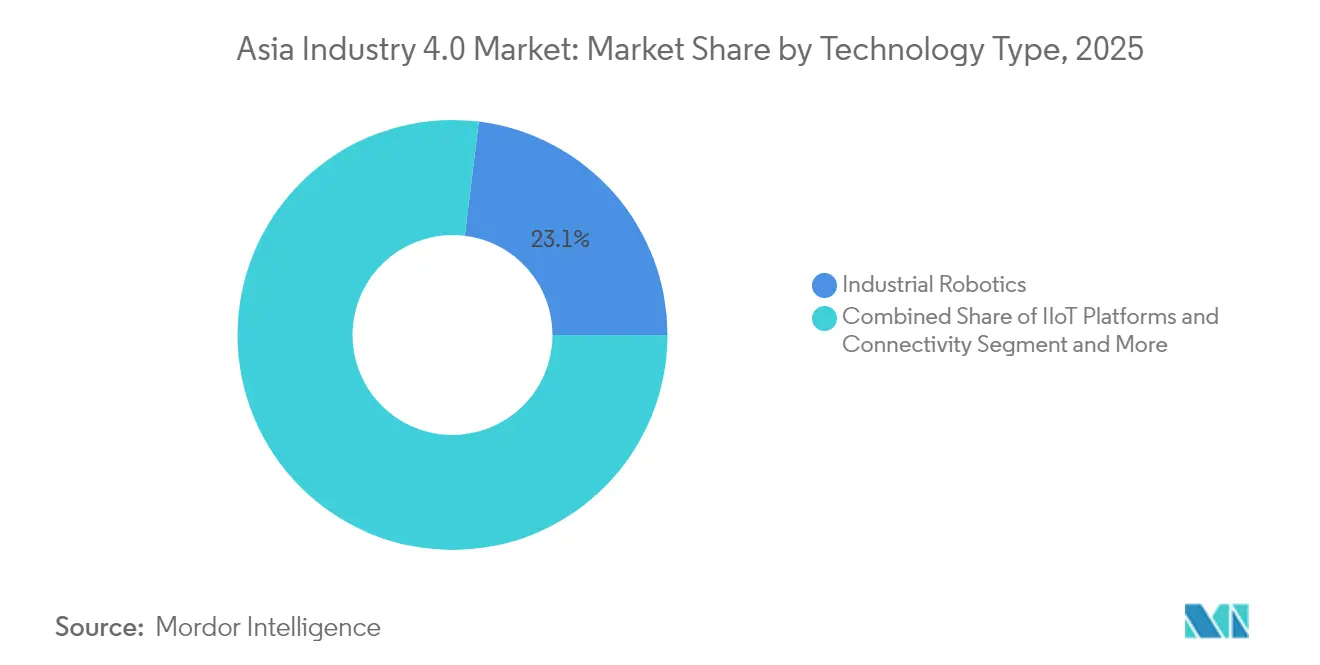

- By technology type, industrial robotics led with a 23.05% share of the Asia Industry 4.0 market in 2025; digital twin solutions are projected to expand at a 22.15% CAGR through 2031.

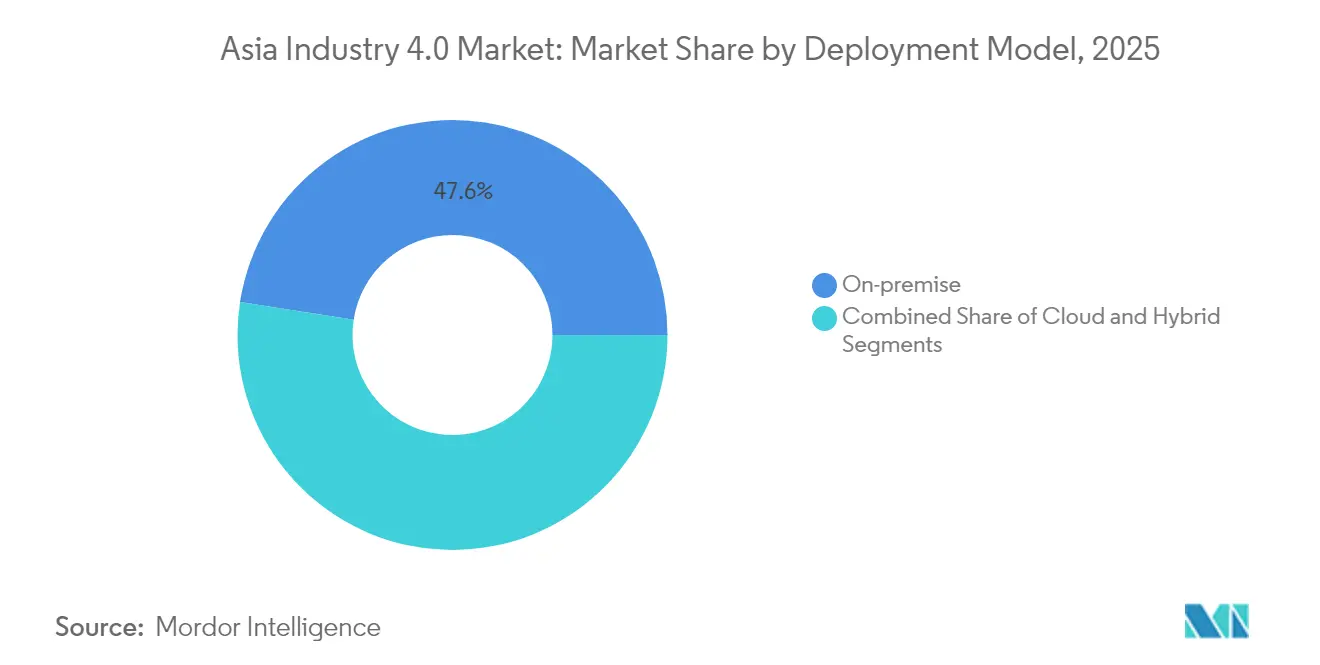

- By deployment model, on-premise implementations accounted for 47.55% of the Asia Industry 4.0 market size in 2025, while cloud approaches are forecasted to rise at a 21.20% CAGR through 2031.

- By end-user industry, discrete manufacturing captured a 20.65% revenue share in 2025; the aerospace and defense sector is advancing at a 21.95% CAGR over the same outlook period.

- By organization size, large enterprises accounted for 59.05% of the 2025 spend, whereas SMEs are expected to accelerate at a 21.70% CAGR through 2031.

- By geography, China maintained a 29.35% lead in 2025; India is expected to climb the fastest, with a 22.40% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Asia Industry 4.0 Market

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Pro-digital manufacturing stimulus packages | +3.5% | China, India, Japan, South Korea, ASEAN | Medium term (2-4 years) |

| Surging demand for industrial robotics | +2.8% | China, Japan, South Korea, Taiwan | Short term (≤ 2 years) |

| Government-funded SME digital vouchers | +2.1% | ASEAN, India, South Korea | Medium term (2-4 years) |

| Private 5G campus networks | +1.9% | China, Japan, South Korea, Singapore | Long term (≥ 4 years) |

| Carbon-neutral manufacturing mandates | +1.2% | Japan, South Korea, China, Singapore | Long term (≥ 4 years) |

| Regional supply-chain resilience schemes | +1.8% | India, Vietnam, Thailand, Malaysia, Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pro-digital manufacturing stimulus packages accelerate industrial transformation

Across Asia, cumulative government commitments exceed USD 200 billion for subsidies to smart factories, tax holidays, and low-interest loans. China’s 14th Five-Year Plan and India’s Production Linked Incentive schemes are lowering capital hurdles for automation projects and widening supplier eligibility in public procurement.[1]Source: Ministry of Electronics and Information Technology, “Production Linked Incentive Scheme,” meity.gov.in Japan’s Society 5.0 and South Korea’s K-Digital New Deal introduce additional grants and workforce upskilling programs that encourage vendors to adopt integrated, platform-based offerings. The Asia Industry 4.0 market benefits directly as component makers, systems integrators, and software providers experience synchronized demand across multiple verticals. Manufacturers receiving early stimulus support report 15%–20% productivity lifts within two years of deployment, reinforcing a positive feedback loop for follow-on investment.

Surging industrial-robotics demand transforms electronics and EV supply chains

In 2024, seventy percent of global robot installations took place in Asia, with China alone commissioning 290,000 new units for semiconductor packaging and battery-cell assembly.[2]Source: International Federation of Robotics, “World Robotics 2024,” ifr.org Growing electric-vehicle output in Shanghai and battery expansion in South Korea require micron-scale accuracy that only high-density robotics cells can deliver. Shorter takt times and 24/7 lights-out operations align with OEM goals to stabilize throughput during supply-chain shocks, reinforcing the Asia Industry 4.0 market’s migration toward autonomous production. Robotics makers now bundle vision sensors and AI-based quality analytics, enhancing system value and differentiating offerings in crowded bidding contests. Rapid paybacks often under two years in high-volume electronics lines are convincing finance teams to prioritize multi-robot cells over incremental manual upgrades.

Government-funded SME digital-transformation vouchers democratize advanced manufacturing

Voucher schemes covering 40%–50% of project costs allow small shops to adopt IoT sensors, MES software, and cloud analytics without balance-sheet strain. Singapore’s SMEs Go Digital and Thailand’s Smart SME programs disburse amounts that reach SGD 1 million (USD 740,000) per applicant, accelerating sensor retrofits on CNC machines and packaging lines. Voucher uptake increased in 2024, expanding the Asia Industry 4.0 market customer base beyond top-tier conglomerates. Systems integrators respond with templated solutions, reducing consulting hours by 30% and shortening commissioning cycles. The newfound competitiveness of digital-ready SMEs attracts multinational OEMs seeking resilient second-source suppliers.[3]Source: Asian Development Bank, “Green Manufacturing Finance,” adb.org

Private 5G campus networks enable ultra-low-latency industrial control systems

More than 200 private 5G deployments are now operational across Asian factories, achieving sub-millisecond latency for machine-vision quality checks and cooperative robot swarms. Hyundai’s Ulsan plant and Foxconn’s Shenzhen campus illustrate how dedicated spectrum improves reliability over Wi-Fi, supporting mobile robots in mixed human-machine environments.[4]Source: Ericsson, “5G for Industry Report 2024,” ericsson.com Data traffic remains on-premises, easing cybersecurity and intellectual property concerns while satisfying diverse data localization laws. Vendors of edge servers, network slices, and AI inference chips tap incremental revenue as private 5G spreads, propelling the Asia Industry 4.0 market toward real-time decision loops. Early adopters report 20% cuts in unplanned downtime and 30% faster product changeovers within the first operating year.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High upfront capex and unclear payback | -2.4% | India, Southeast Asia | Short term (≤ 2 years) |

| Acute OT-IT skills shortage | -1.8% | Vietnam, Indonesia, Philippines | Medium term (2-4 years) |

| Fragmented industrial data standards | -1.5% | China, India, ASEAN | Medium term (2-4 years) |

| Escalating cyber-insurance premiums | -1.2% | Japan, South Korea, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High upfront capital expenditure creates adoption barriers despite long-term benefits

Smart-factory retrofits often require USD 10-50 million per site, surpassing conventional equipment-replacement budgets for mid-tier manufacturers. Local banks in Vietnam and Indonesia rarely extend long-term loans for intangible software assets, forcing equity funding or delayed projects. Payback estimates hinge on predictive-maintenance savings and scrap reductions that remain unfamiliar to finance teams, suppressing approval rates even when internal rates of return align with corporate thresholds. The Asia Industry 4.0 market thus exhibits a bifurcation, where cash-rich multinational companies advance, while domestic suppliers lag behind. Capex-light subscription models are emerging, but uptake is limited by perceived vendor lock-in and ambiguous total cost-of-ownership frameworks.

Skills shortage and organizational resistance impede technology integration

60% of Asian manufacturers cite talent scarcity in cybersecurity, data science, and systems integration as their top barrier to digitization. University curricula trail industry demand, producing fewer than 200,000 certified OT-IT engineers annually across ASEAN. Change-management inertia compounds the gap, as line supervisors fear role redundancy, delaying the expansion of pilots. Family-owned enterprises, which are dominant in the textile and food-processing sectors, often centralize decisions with senior executives who lack direct exposure to emerging technologies. These dynamics slow Asia's Industry 4.0 market penetration despite fiscal incentives, prompting governments to sponsor technical training vouchers and apprenticeship programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: Digital twins outpace legacy robotics in strategic value creation

Industrial Robotics commanded a 23.05% share of the Asia Industry 4.0 market in 2025, driven by continued demand for electronics and battery-cell automation. However, Digital Twin platforms are growing at a 22.15% CAGR, asserting themselves as indispensable companions to physical automation by enabling virtual commissioning, predictive maintenance, and scenario planning. The Asia Industry 4.0 market size tied to digital-twin subscriptions is expected to triple by 2031 as license-based revenue models replace one-time software sales. Regional OEMs are bundling twins with robotics cells to minimize ramp-up times, cutting new-line validation from six months to three weeks. IIoT connectivity and edge analytics also experience double-digit growth, driven by the increasing availability of 5G and declining sensor costs. Blockchain remains a niche technology, but it is gaining traction in food safety and pharmaceutical serialization, while XR applications are assisting with remote maintenance for remote, rural factories. Vendors offering integrated stacks that merge twins, analytics, and AI vision stand to capture a higher wallet share as plant managers consolidate their suppliers.

Asian semiconductor fabs are adopting AI-assisted optical inspection tools that achieve sub-micron defect detection accuracy, a requirement for chips below the 5nm node. These tools feed data directly into digital-twin models, closing the loop between design and manufacturing. Japanese robotics manufacturers are now incorporating Nvidia-based GPU modules for on-arm AI inference, enhancing robotics cell flexibility without the need for external servers. Edge gateways ship with Time-Sensitive Networking (TSN) features to maintain deterministic traffic, crucial for synchronized multi-robot operations. As computing costs decrease, simulation throughput increases, allowing manufacturers to test hundreds of parameter combinations before a single physical change is made. This holistic approach cements the Asia Industry 4.0 market as an innovation sandbox where hardware and software co-evolve.

By End-user Industry: Aerospace and defense eclipses traditional discrete manufacturing momentum

Discrete manufacturing retained 20.65% of the Asia Industry 4.0 market share in 2025, driven by high-volume assembly of consumer electronics. Yet aerospace and defense companies are embracing additive manufacturing, digital twins, and predictive analytics at a 21.95% CAGR to meet stringent component tolerances and traceability mandates. Government defense-modernization budgets in Japan, South Korea, and India finance smart-factory retrofits at prime contractors, accelerating their supplier ecosystems. Electric-vehicle platforms in China and Southeast Asia further stimulate robotics density, particularly in battery and power electronics lines. Semiconductor fabs are expanding advanced-node production to meet the growing demand for AI chips, thereby increasing the adoption of defect-inspection vision systems and sub-micron motion controllers.

Food and beverage processors integrate blockchain traceability to comply with new safety labeling laws, while oil and gas operators deploy AI-driven asset-integrity platforms to extend well life. Energy and utilities firms invest in digital control centers that synchronize distributed renewable assets, driving the adoption of predictive maintenance software across turbine and inverter fleets. These dynamics collectively broaden the Asia Industry 4.0 market's customer mix, reducing segment concentration risk for technology vendors. As high-value verticals mature, service revenue from maintenance, upgrades, and data analytics is expected to outpace hardware growth, reshaping vendor business models toward recurring income streams.

By Deployment Model: Cloud gains parity with on-premise under hybrid governance models

On-premise deployment accounted for 47.55% of the Asia Industry 4.0 market share in 2025, reflecting lasting data-sovereignty concerns and existing SCADA investments. Cloud-native deployments, however, are growing at 21.20% CAGR as private 5G and edge-computing architectures address latency gaps. Hybrid models that keep mission-critical workloads on-premise while offloading analytics to hyperscaler clouds are becoming the default blueprint. The Asia Industry 4.0 market size associated with hybrid subscriptions is expected to surpass pure on-premise spend by 2028, driven by updated data-protection statutes in Japan and South Korea that clarify industrial data residency rules. SaaS pricing delivers predictable OPEX, resonating with finance teams wary of large capex spikes.

Edge computing nodes now bundle GPU acceleration, allowing AI models to run locally for real-time defect detection, after which summarized data is sent to the cloud for model retraining. Vendors like Microsoft and AWS partner with Japanese PLC makers to package secure connectors that simplify gateway provisioning. As a result, proof-of-concept cycles shorten, with full-scale rollouts completing in under 12 months for greenfield sites. Regulatory acceptance of encrypted data transfer facilitates multi-site analytics, enabling plant managers to benchmark performance across countries. This architectural flexibility supports segmented adoption paths, ensuring the Asia Industry 4.0 market can accommodate varied readiness levels across developing and advanced economies.

By Organization Size: SMEs narrow the capability gap through voucher-financed cloud platforms

Large enterprises retained 59.05% spending leadership in 2025, leveraging deep capital pools for end-to-end smart-factory conversions. Nonetheless, SME adoption is expanding at a 21.70% CAGR, propelled by subsidy vouchers and turnkey cloud platforms that mitigate integration complexity. The Asia Industry 4.0 market benefits as SME projects transition from pilot to scale, boosting total addressable installations for low-cost sensors, subscription-based MES, and pay-per-use digital twin services. SaaS vendors target the segment with template configurations, slashing deployment effort by 40%. Cloud-based dashboards present intuitive KPIs, sidestepping the need for in-house data scientists.

SME cluster adoption spurs positive network effects: as neighboring suppliers digitize, value-chain data flows enhance predictive-maintenance accuracy and reduce inventory buffers. Financing arms of automation OEMs bundle equipment leases with software subscriptions, aligning cash flows with realized savings. Workforce-training grants from ASEAN governments further ease the hurdles of change management. Collectively, these factors expand the Asia Industry 4.0 market customer pyramid, de-risking vendor dependence on megaprojects and smoothing revenue streams.

Geography Analysis

China controlled 29.35% of the Asia Industry 4.0 market in 2025, underpinned by the USD 1.4 trillion digital-economy allocation within the 14th Five-Year Plan, a nationwide industrial 5G rollout exceeding 200 private networks, and a dense domestic vendor base that accelerates turnkey system availability. Foreign suppliers face technology-export restrictions and local-content preferences, yet niche players in AI inspection and edge security still secure contracts by partnering with Chinese integrators.

India is the fastest-growing geography, charting a 22.40% CAGR through 2031 as Production Linked Incentive schemes inject USD 26 billion into electronics manufacturing and foreign OEMs expand “China+1” capacity in Tamil Nadu and Karnataka. A high supply of engineering talent supports rapid commissioning, while federal data-protection rules now permit secure cross-border analytics under standardized contractual clauses, encouraging hybrid-cloud deployments.

Japan and South Korea, although mature, continue to sustain mid-teen growth by advancing robotics, semiconductor packaging, and shipbuilding automation. Japan’s Society 5.0 framework supports demonstrator sites that showcase reference architectures to SMEs, thereby reinforcing the Asia Industry 4.0 market as a cross-border knowledge hub. Southeast Asia is aggregating rising demand as Thailand’s Eastern Economic Corridor, Malaysia’s Industry4WRD zones, and Vietnam’s diverse export manufacturing base attract greenfield investments that routinely specify digital twin, private 5G, and blockchain traceability capabilities from the outset.

Regulatory Landscape

Across Asia, Industry 4.0 compliance is shaped by national industrial-digitalization frameworks and sector regulators that increasingly address industrial data, AI governance, and connectivity for factories. In China, the Ministry of Industry and Information Technology and other central departments issued Implementation Opinions in June 2026 to promote high-quality development of the Industrial Internet, reinforcing coordinated infrastructure buildout and cross-sector integration that affects IIoT platforms, edge deployments, and industrial connectivity programs.

Southeast Asia continues to combine policy roadmaps with voluntary benchmarking and standards-oriented adoption programs. Vietnam’s Law on Digital Technology Industry (No. 71/2025/QH15) entered into force in January 2026, establishing a statutory framework for incentives and compliance around digital technology domains relevant to smart manufacturing (including AI and semiconductors). Thailand’s National Broadcasting and Telecommunications Commission published AI guidelines for telecommunications services in July 2026, using a risk-based governance approach that influences private 5G and connected-factory use cases delivered by telecom licensees. Regional alignment efforts such as the ASEAN smart manufacturing roadmap and Singapore’s Smart Industry Readiness Index (SIRI) support common assessment language and implementation guidance for manufacturers and solution providers operating across multiple Asian markets.

Competitive Landscape

The Asia Industry 4.0 market exhibits moderate fragmentation, with robotics dominated by ABB, Fanuc, Yaskawa, and KUKA, while cloud-edge convergence draws in Microsoft Azure, AWS, Alibaba Cloud, and Tencent Cloud, intensifying rivalry. Traditional automation providers are expanding into software platforms, such as Siemens’ MindSphere and Mitsubishi’s e-F@ctory, to strengthen end-to-end control proposals. Hyperscalers counter by embedding low-code connectors that shorten time to value, courting SMEs and greenfield projects.

Strategic moves emphasize ecosystem alliances: ABB’s acquisition of ASTI Mobile Robotics secures autonomous mobile integration, whereas Siemens’s USD 2 billion Asian expansion builds regional research and development and demo centers to localize solutions. Patent filings in industrial AI increased by 40% in 2024, with edge-vision start-ups attracting Series B rounds exceeding USD 50 million, signaling an intensifying innovation competition.

Cybersecurity providers such as Schneider Electric and Trend Micro partner with PLC vendors to offer zero-trust reference architectures, reflecting customer insistence on embedded security. White-space opportunities persist in niche sectors pharma serialization, upstream resource extraction, and off-grid renewable management, where solution depth trumps scale. The Asia Industry 4.0 market thus rewards vendors capable of aligning hardware lineage with data-driven service models that deliver continuous improvement.

Leaders of Asia Industry 4.0 Market

Mitsubishi Electric Corporation

ABB Ltd.

Siemens AG

Fanuc Corporation

Yokogawa Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large greenfield and brownfield capacity programs across automotive, electronics, and process industries are moving Industry 4.0 from pilots into production-scale requirements for robotics, digital twins, private 5G, and edge analytics. Examples in 2026 include Maruti Suzuki inaugurating the Kharkhoda vehicle manufacturing facility in India, built around a Suzuki Smart Factory concept that uses cobots and human-machine collaboration, and TCL inaugurating a Guangzhou smart manufacturing base designed for high-throughput air-conditioner production. These programs expand demand for factory connectivity, machine vision, MES, and cyber-resilient OT architectures, while also producing repeatable reference sites that systems integrators can replicate across supplier tiers.

Industrial connectivity and semiconductor-related investments also open whitespace for platform vendors and integrators in hybrid IT/OT, deterministic networking, and advanced packaging inspection workflows. In July 2026, Tower Semiconductor announced a dual-track strategic capacity expansion in Japan for 300mm silicon photonics with support from the Government of Japan, linking new fabs to requirements for digital process control, yield analytics, and simulation-led ramp. On connectivity, enterprise-scale provisioning becomes more accessible as Singtel, Thales, and Bridge Alliance enabled a multi-operator enterprise eSIM connectivity network in Asia Pacific based on GSMA SGP.32 specifications, and as private 5G lighthouse models such as Telkomsel and Pegatron in Batam show scaled device connectivity inside manufacturing campuses. There is also a practical demand for compliance-ready solutions that map to emerging AI and industrial-data governance, particularly where telecom and industrial regulators are tightening guidance on AI-enabled services and connected infrastructure.

Recent Industry Developments

- July 2026: Mitsubishi Electric signed an agreement to transfer a 70.0% stake in Mitsubishi Electric FA Industrial Products to Konecranes, subject to regulatory approval. The transaction reshapes Mitsubishi Electric’s factory-automation footprint while potentially expanding distribution and lifecycle service reach through an industrial handling specialist, influencing automation product availability and partner ecosystems in Asia.

- September 2025: Siemens AG announced an investment of USD 3.2 billion to add digital-factory hubs in Vietnam, Thailand, and Indonesia. The plan includes robotics training sites and private 5G testbeds, strengthening local implementation capacity for smart factory rollouts across Southeast Asia.

- June 2024: The International Federation of Robotics reported that 70% of global robot installations occurred in Asia in 2024, with China commissioning 290,000 new units. The scale of deployments reinforces Asia’s role as the lead adoption region for robotics-led smart manufacturing and supports downstream demand for integration software, vision systems, and connected-factory cybersecurity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Asia Industry 4.0 market is defined as spending tied to smart factory and digital manufacturing transformation, where software, connected systems, and automation are deployed to run production, quality, maintenance, and supply chain workflows in industrial sites across Asia.

Scope exclusions: We exclude general-purpose enterprise IT spend that is not directly connected to industrial operations (for example, standard office networking, generic HR systems, and unrelated consumer IoT devices).

Segmentation Overview

- By Technology Type

- Industrial Robotics

- IIoT Platforms and Connectivity

- Artificial Intelligence and Machine Learning

- Blockchain for Industrial Traceability

- Extended / Augmented / Mixed Reality

- Digital Twin

- 3-D Printing / Additive Manufacturing

- Other Technology Types

- By End-user Industry

- Discrete Manufacturing

- Automotive

- Oil and Gas

- Energy and Utilities

- Electronics and Foundry

- Food and Beverage

- Aerospace and Defence

- Other End-user Industries

- By Deployment Model

- On-premise

- Cloud

- Hybrid

- By Organisation Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By Country

- China

- Japan

- India

- South Korea

- South-East Asia

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for Asia manufacturing output, investment direction, and the pace of technology adoption that typically sits inside Industry 4.0 programs. We referenced public sources such as national statistics agencies across major Asian economies, the World Bank, UN Comtrade trade data, and standards and guidance from bodies such as ISO and IEC to understand how industrial connectivity and automation categories are defined.

To translate that context into measurable inputs, we also reviewed company annual reports, investor presentations, product literature, and reputable press coverage to map the main spend buckets that show up in factory modernization. Where needed, we used paid database subscriptions for company financials and intelligence, patent databases to track technology intensity, and shipment-level import and export data to sanity check hardware-linked indicators. These examples are not exhaustive, and many other sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with a mix of manufacturers, system integrators, automation specialists, and software and platform teams that support factory digitization across Asia. The goal was to confirm what buyers typically budget as Industry 4.0, how cloud versus on-premise decisions affect spend timing, and how quickly pilot projects move into scaled deployments by country and by plant type.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 18% | |

| Mid tier: 55% | Functional/Unit leaders: 24% | |

| Smaller Players: 18% | Managers: 58% |

Market-Sizing & Forecasting

Sizing was built using a combined top-down and bottom-up approach, where manufacturing and industrial investment signals were first converted into an addressable digitalization spend pool for Asia, and then split across common Industry 4.0 solution groups. To keep the model grounded, it relies on measured indicators such as manufacturing value added, automation and sensor hardware trade flows, private 4G and 5G rollout momentum for industrial sites, industrial robot installations, and observed cloud adoption for production systems.

After forming the regional total, we ran selective bottom-up checks using sampled supplier revenues, channel feedback on typical project sizes, and simple ASP times volume logic for categories closely linked to unit shipments (for example, robots and certain sensor classes). Where company reporting created coverage gaps, we used peer benchmarking and product mix splits supported by interviews, then adjusted totals when cross-checks indicated over-counting or under-counting.

For forecasting, we used scenario analysis supported by multivariate regression on key demand drivers, including factory capex cycles, labor cost pressure, electronics and EV supply chain expansion, and regulatory and incentive programs that push digital manufacturing. The final forecast path was kept aligned to what interviewees described as realistic rollout speeds, including the lag between proof-of-concept deployments and multi-plant scaling.

Data Validation & Update Cycle

Validation was handled through step-by-step checks that compare model outputs with independent signals, followed by analyst review before results are finalized. We tested for outliers by country and by spend category, rechecked currency conversions and timing, and reviewed whether growth rates matched adoption realities such as deployment lead times and integration bottlenecks.

When variances appeared versus external indicators, assumptions were revisited and, where needed, experts were re-contacted to clarify what was included and what was excluded. Reports are refreshed annually, with interim updates when material events occur such as major policy changes, sharp industrial production swings, or large shifts in automation investment sentiment. Before publication, a final pass is performed so clients receive the most current view available.

Mordor Intelligence's Asia Industry 4 0 Market Size Compared Against Other Published Estimates

Published market values for Asia Industry 4.0 often differ because teams do not all count the same spend, and they also use different base years, currency timing, and assumptions on how fast pilots scale into rollouts. Even when two studies use similar labels, the included technologies and end-use boundaries can move the total materially.

Some external estimates focus only on smart manufacturing software and connected factory platforms, while others lean mainly on industrial IoT connectivity plus devices. In Mordor Intelligence, the total is counted only when spend is directly tied to industrial operations in Asia, with adjacent general enterprise IT and non-industrial IoT removed, and then checked against multiple adoption signals (such as robot installations, industrial connectivity expansion, and manufacturing investment cycles).

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 99.76 B (2025) | |

| Trade Journal A | USD 52.90 B (2023) | Uses a smart manufacturing lens that is closer to factory digitalization programs, but the scope is narrower and appears to emphasize core software and analytics, with less coverage of broader Industry 4.0 technology buckets and cross-industry deployment spend. |

| Industry Bulletin B | USD 26.40 B (2023) | Tracks Asia Pacific industrial IoT only, which can exclude robotics, digital twin, XR, and other smart factory layers, and the base year and category mix are not always aligned to full factory modernization budgets. |

The spread in the table mainly comes from what is counted as part of an Industry 4.0 program and how much of the factory stack is included beyond connectivity. By keeping the scope tied to industrial use cases and by using repeatable checks on adoption indicators, the estimate stays traceable to clear inputs that can be reviewed and updated each cycle.

Key Questions Answered in the Report

How large is the Asia Industry 4.0 market in 2026?

The Asia Industry 4.0 market size is projected to reach USD 120.76 billion by 2026 and is expected to grow at a 21.05% CAGR to USD 314.08 billion by 2031.

Which technology segment is growing fastest in Asia?

Digital Twin solutions exhibit the highest growth, expanding at a 22.15% CAGR as manufacturers prioritize virtual commissioning and predictive maintenance.

Why is India the fastest-growing geography?

India benefits from Production Linked Incentive schemes, significant foreign direct investment, and an expanding electronics-manufacturing base, driving a 22.40% CAGR through 2031.

What deployment model is gaining momentum?

Cloud and hybrid deployments are accelerating at a 21.20% CAGR due to improved 5G connectivity and clearer data-residency regulations.

Which organizational tier is driving new demand?

SMEs are increasingly important, growing at a 21.70% CAGR, aided by government vouchers and subscription-based Industry 4.0 platforms.

Page last updated on: