ASEAN Waterproofing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

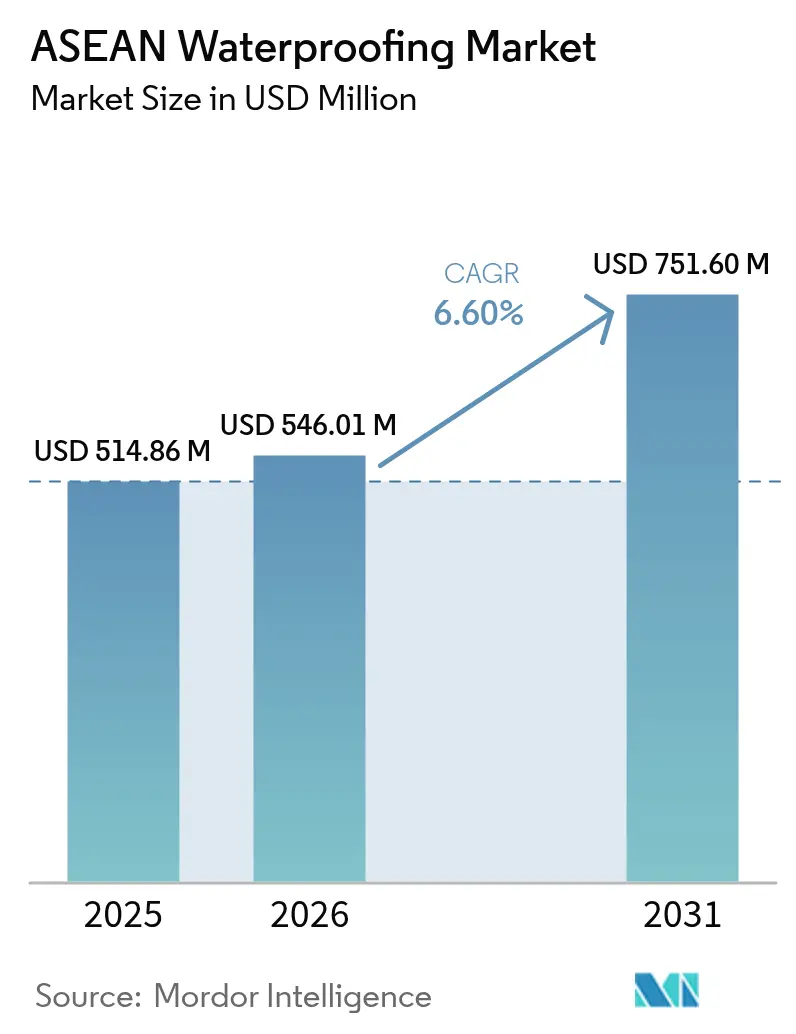

| Base Year Market Size (2025) | USD 514.86 Million |

| Market Size (2026) | USD 546.01 Million |

| Market Size (2031) | USD 751.60 Million |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

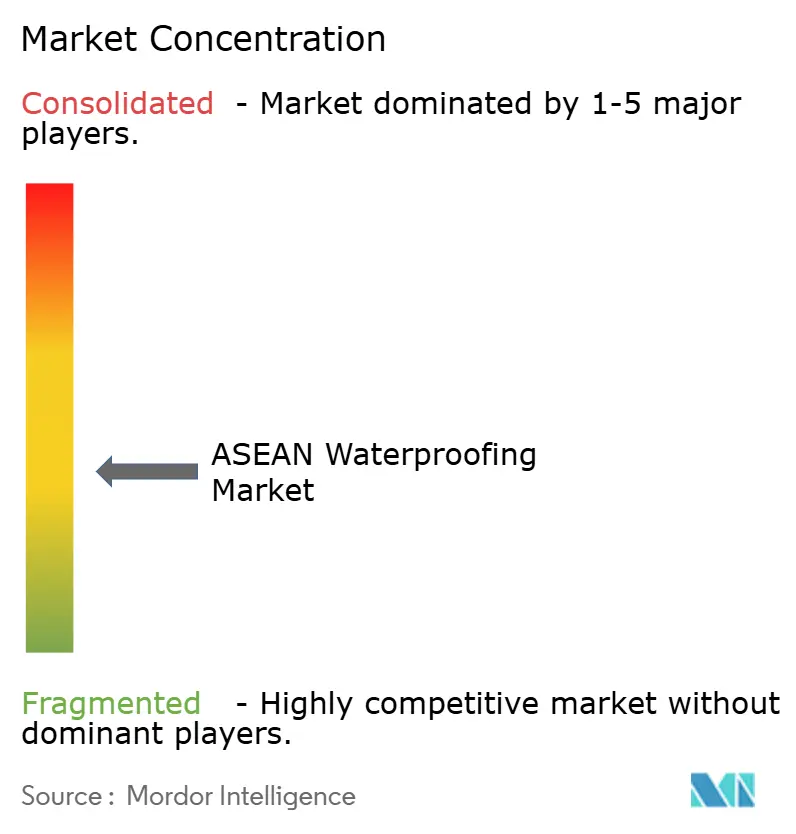

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Waterproofing Market Analysis by Mordor Intelligence

The ASEAN Waterproofing Market size is projected to expand from USD 514.86 million in 2025 and USD 546.01 million in 2026 to USD 751.60 million by 2031, registering a CAGR of 6.60% between 2026 to 2031. Record infrastructure budgets, tightening green-building codes, and broader access to preferential tariff corridors are driving momentum in the industry. These corridors reduce landed costs for high-performance membranes. Governments are now incorporating lifecycle-cost clauses into tenders. This shift is moving demand away from short-lived cementitious coatings and toward polymer membranes, which come with 15-year warranties. Developers in Jakarta, Manila, and Kuala Lumpur are increasingly opting for below-grade and rooftop systems. These systems are designed to resist hydrostatic pressure and root penetration. Meanwhile, in Singapore, the Super Low Energy standards incentivize assemblies that minimize thermal bridging. As a result, the policy and financing landscape turns durability into a bankable asset class, prompting suppliers to validate tropical-aging performance through accredited laboratories and digital batch tracking.

Key Report Takeaways

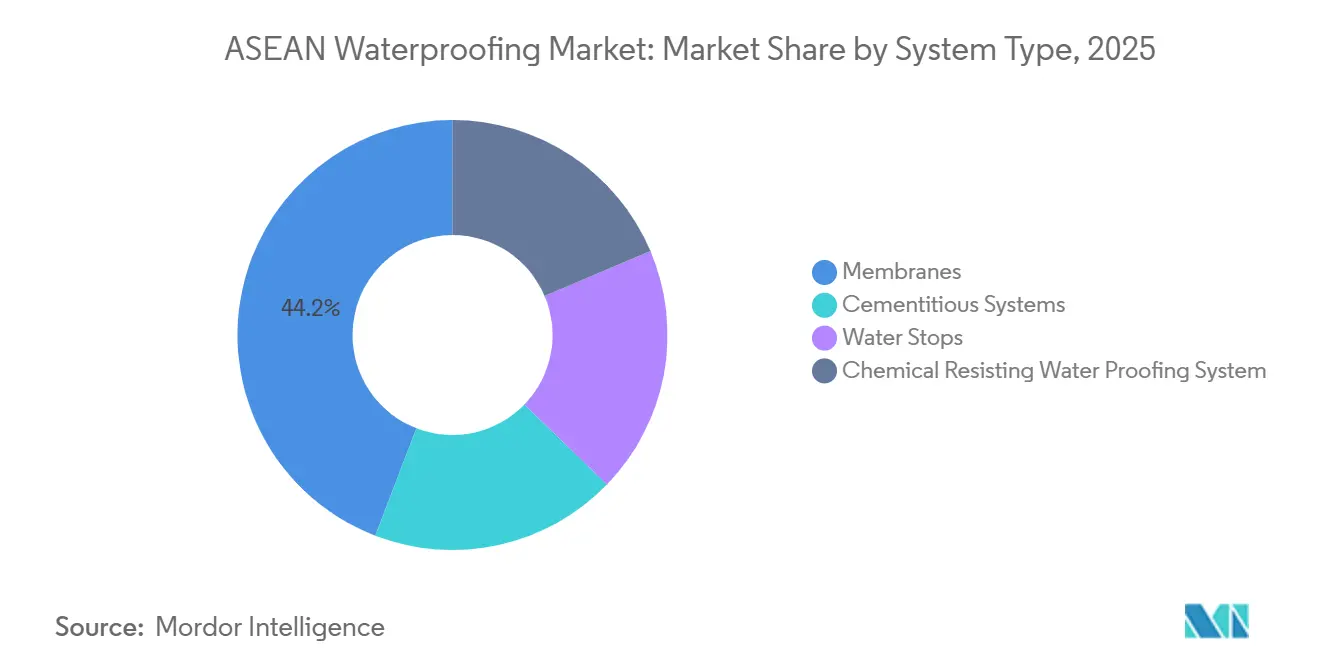

- By system type, membranes held 44.15% of the ASEAN waterproofing market share in 2025, and the segment is projected to expand at a 7.09% CAGR in the forecast period of 2026-2031.

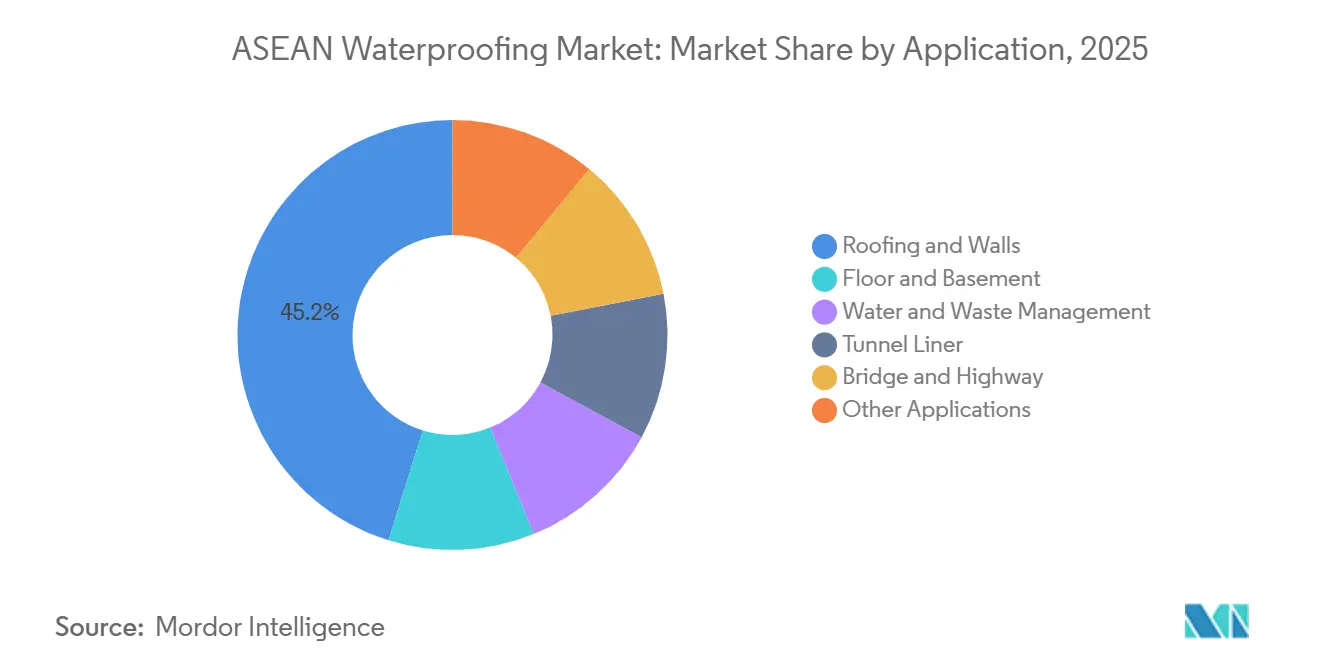

- By application, roofing and walls accounted for 45.18% of the ASEAN waterproofing market size in 2025 while advancing at a 7.35% CAGR in the forecast period of 2026-2031.

- By geography, Indonesia led with 31.46% revenue share in 2025, whereas Singapore is set to record the fastest 7.19% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Waterproofing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government infrastructure-spending surge | +1.8% | Indonesia, Vietnam, Thailand (core); Philippines, Malaysia | Medium term (2-4 years) |

| Residential housing boom in urban ASEAN | +1.5% | Indonesia (Jakarta, Surabaya), Philippines (Metro Manila), Malaysia (Klang Valley) | Short term (≤ 2 years) |

| Tropical-climate moisture challenges | +1.2% | Global ASEAN (monsoon belt), elevated in coastal cities | Long term (≥ 4 years) |

| Green-roof initiatives in megacities | +0.9% | Singapore, Jakarta, Bangkok, Kuala Lumpur | Medium term (2-4 years) |

| Lower import tariffs via ASEAN FTAs | +0.6% | Intra-ASEAN trade corridors (Vietnam-Thailand, Indonesia-Malaysia) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Infrastructure-Spending Surge

Public budgets are reaching unprecedented levels. By 2025, Vietnam will have approved more than 560 projects, with a significant portion financed by private consortia. Thailand has also approved numerous flood-control and expressway projects. Indonesia's Nusantara capital city, supported by a substantial financial envelope, specifies polymer-modified membranes for its peat-soil foundations. Each tender includes a warranty clause of at least ten years and explicitly excludes low-spec sheets. Multinational firms with ISO 9001 certifications and tropical-aging test reports have captured a significant share of the public-sector volume. This consistent influx of capital has anchored demand, even as residential cycles have softened.

Residential Housing Boom in Urban ASEAN

In a bid to address a significant housing backlog, Indonesia has set an ambitious goal to complete several million housing units between 2025 and 2029. In early 2025, Malaysia experienced a surge in housing starts. By mid-2025, Metro Manila reported an increase in issued residential permits. Banks are now mandating water ingress guarantees for high-rise mortgages. This requirement is prompting developers to transition from site-mixed coatings to factory-made membranes, which offer traceable batch numbers. Urban high-rises, equipped with podium car parks and rooftop amenities, face persistent wet areas, necessitating heightened technical specifications. As a result, the housing surge has expanded the market for premium systems and accelerated the upskilling of contractors.

Tropical-Climate Moisture Challenges

Annual rainfall between 2,000 mm and 4,000 mm exerts hydrostatic pressure, exceeding the tensile limits of basic cement layers within seven years. In light of this, Singapore's regulatory body found that a notable share of defect claims in 2025 stemmed from water ingress. This insight prompted the enforcement of mandatory wet-area testing for buildings exceeding 15 floors. Concurrently, Indonesia's coastal regions face challenges from saline capillary rise, threatening polymer chains. However, this issue can be addressed by adding UV and salt-fog stabilizers. In a tactical move, Sika's acquisition of Elmich in 2025 allowed the firm to merge drainage and root-barrier layers into unified SKUs. This advancement notably diminishes the puncture risk linked to green roofs. Consequently, there is a marked uptick in demand for TPO and EPDM sheets, celebrated for their high elongation retention even after a decade in tropical climates. This moisture-driven strain not only fine-tunes product mixes but also accelerates replacement cycles, boosting value density in the Asia-Pacific waterproofing market during the forecast period of 2026–2031.

Green-Roof Initiatives in Megacities

By 2025, Singapore's Green Mark 2021 initiative incentivized projects with significant roof greening by awarding them bonus floor area, which led to the installation of numerous green roofs. Starting in 2024, Jakarta mandated that commercial towers exceeding 10,000 m² must feature vegetated roofs. This requirement has transformed membrane designs, as the introduction of planters creates point loads and necessitates regular irrigation. To reduce stormwater runoff, Bangkok has been subsidizing green-roof expenses for regions within the Chao Phraya flood zone. While all three cities have adopted a standard requiring ASTM D5514 root-penetration resistance, they have notably excluded asphalt felts from this requirement. As a result, suppliers combining waterproofing with drainage composites are capitalizing on the opportunity, commanding premium prices and navigating expedited building-permit processes efficiently.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.8% | Global ASEAN (polymer, bitumen supply chains) | Short term (≤ 2 years) |

| Skilled waterproofing-labor shortage | -0.6% | Indonesia, Philippines, Myanmar (acute); Vietnam, Thailand | Medium term (2-4 years) |

| Counterfeit/low-spec membrane influx | -0.5% | Indonesia, Philippines, Vietnam (price-sensitive residential segments) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Late in 2024, refinery outages across the Middle-East triggered a dip in the global asphalt supply. This shortfall caused an increase in the prices of styrene-butadiene-styrene feedstock in the fourth quarter. As a result, extruders in the ASEAN region experienced a contraction in gross margins, leading to production halts at several Indonesian plants for weeks. BASF’s 2024 report highlighted "persistent raw-material headwinds," which contributed to a decline in sales of construction chemicals across the Asia-Pacific. While multinationals with their own polymer assets navigated these challenges, regional independents without hedging cover lost market share. These price fluctuations have caused companies to hesitate in committing to fixed-price bids, extending project award cycles, and slowing the growth rate of the ASEAN waterproofing market.

Skilled Waterproofing-Labor Shortage

By 2025, only a small proportion of construction workers in Indonesia held formal waterproofing certificates. In the Philippines, the skills agency certified only a limited number of applicants in 2025, representing a minor segment of the active workforce[1]Technical Education and Skills Development Authority, “Certification Statistics 2024,” tesda.gov.ph. Myanmar continues to lack a standardized curriculum. Poor seam welding has significantly increased rework rates, prompting some developers to revert to cementitious systems, despite their higher lifecycle costs. Sika offers free applicator training at its numerous retail points across Indonesia; however, the training capacity still lags behind the growing demand. Consequently, this labor scarcity has hindered the adoption of premium solutions and slightly reduced the forecasted growth for the 2026–2031 period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Membranes Capture Durability-Driven Spend

In 2025, membranes captured 44.15% of the ASEAN waterproofing market share, with projections indicating growth at a 7.09% CAGR during the forecast period of 2026–2031. This growth rate surpasses all competitors, primarily because polymer sheets and spray-applied liquids now feature independent 15-year tropical warranties. These warranties meet the thresholds that lenders require for toll-road public-private partnerships. Cementitious coatings continue to serve cost-sensitive mid-rise housing; however, they are losing market share as banks transition to lifecycle-cost underwriting. Water stops maintain a niche role at tunnel joints, and while chemical-resistant linings are essential for industrial tanks, they do not significantly contribute to growth.

In Singapore, Arkema has introduced a new PA11 line, offering bio-based liquid membranes that can be spray-cured within 48 hours[2]Arkema, “PA11 Plant Launch,” arkema.com. This innovation eliminates seams and reduces labor requirements. The market is experiencing consolidation, as demonstrated by Sika's acquisition of Gulf Seal in 2025, following a significant output increase from a Bekasi plant expansion. Rapid training programs are embedding application expertise directly at the point of sale, shifting the competitive focus from product variety to speed.

By Application: Roofing and Walls Dominate Green-Building Budgets

In 2025, roofing and walls accounted for 45.18% of the ASEAN waterproofing market, with projections indicating a CAGR of 7.35% during the forecast period of 2026–2031. Singapore incentivized vegetated roofs, offering a bonus floor area for those covering at least half the deck. Concurrently, Jakarta mandated green roofs on towers exceeding 10,000 m². These initiatives led to a surge in the adoption of root-resistant membranes in 2025. Following closely are basement slabs and podium car parks, especially after insurers increased premiums on buildings lacking certified wet-area protection.

While tunnel liners for Indonesia’s Trans-Sumatra tollway and Vietnam’s high-speed railway bolstered growth, they caused sporadic demand spikes rather than steady demand. Upgrades to water and waste infrastructure in peri-urban regions of Vietnam and the Philippines have broadened the market for chemical-resistant membranes. This shift is largely attributed to premium systems, which, despite their higher price compared to asphalt felt, deliver double the service life, highlighting their value proposition.

Geography Analysis

In 2025, Indonesia commanded a dominant 31.46% share of the ASEAN waterproofing market. By late 2024, the construction sector was a significant contributor to the GDP, with the government targeting millions of housing completions annually through 2029. Major undertakings, including the Nusantara new capital and the Trans-Sumatra tollway, spurred demand for tunnel-liner sheets. However, a skills gap within the labor force impeded the adoption of advanced systems. While Sika's expansion in retail points facilitated easier access for installers, a mere fraction of the workforce possessed certifications, raising quality concerns that could hinder growth.

Singapore, starting from a modest base, is witnessing the swiftest compound annual growth rate (CAGR) at 7.19% projected through the forecast period of 2026–2031. This uptick is largely due to the Super Low Energy code, which penalizes thermal bridges and mandates third-party wet-area testing for skyscrapers. Elevated labor costs, surpassing the ASEAN average, have driven transaction values beyond those of regional peers. Following Sika's acquisition of Elmich, the company is poised to deliver bundled solutions, especially green-roof packages that not only cut installation time to two days but also align with faster approval processes.

Thailand, Vietnam, the Philippines, Malaysia, and Myanmar share the rest of the market pie. Thailand's development blueprint emphasizes flood control and elevated expressways. However, with residential starts plummeting to historic lows in late 2025, the market experienced a cyclical downturn. After clearing a substantial number of social units in 2025, Vietnam is now eyeing a tunnel-focused high-speed rail, setting the stage for polymer-modified bitumen liners. The Philippines issued a considerable volume of building permits in mid-2025, but financing hurdles delayed the shift to completed projects. In early 2025, Malaysia experienced a construction value boom, spurred by transit-oriented zoning in Kuala Lumpur. On the other hand, Myanmar's scenario is mixed: while the post-crisis rebuilding phase ushered in opportunities for greenfield infrastructure, the absence of skills certification stunted the adoption of premium membranes.

Competitive Landscape

The ASEAN waterproofing market is moderately fragmented. Geography, with its numerous inhabited islands, complicates distribution and amplifies the value of local plants and retail footprints. Regional players, capitalizing on duty-free imports of SBS polymers from South Korea, have significantly reduced prices compared to European competitors without compromising quality. The competitive edge now lies in application speed and warranty duration: brands that train applicators and complete jobs in two days secure repeat business, sidelining catalog-only competitors. While counterfeit products cloud the residential market, digitized QR batch labels enable multinationals to verify authenticity. Securing ISO 9001 credentials and ASTM D5147 tropical-aging data has become a prerequisite for public tenders. This evolution has funneled most megaproject volumes to global entities, relegating local producers to price-sensitive segments. As a result, the ASEAN waterproofing market is gravitating towards medium concentration, with active acquisition pipelines still underway.

ASEAN Waterproofing Industry Leaders

Sika AG

Saint-Gobain

MAPEI S.p.A.

Arkema

Pidilite Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Eternity Waterproofing entered a distribution alliance with Mapei Far East to widen market access across Southeast Asia, combining Eternity's regional expertise with Mapei's global product portfolio and technical support infrastructure.

- February 2025: Saint-Gobain finalized the acquisition of Fosroc, strengthening its ASEAN construction-chemicals footprint, particularly in waterproofing.

ASEAN Waterproofing Market Report Scope

Waterproofing is the application of impermeable layers on the surfaces of foundations, walls, roofs, and other parts of a building, which can be concrete, membranes, or fabric, to prevent water penetration.

The waterproofing systems market is segmented by system type, application, and geography. By system type, the market is segmented into cementitious systems, membranes, water stops, and chemical resisting waterproofing systems. By application, the market is segmented into roofing and walls, floor and basement, water and waste management, tunnel liner, bridge and highway, and other applications. The report also covers the market size and forecasts for the market in 7 countries across the region. For each segment, the market sizing and forecasts are done based on value (USD).

| Cementitious Systems |

| Membranes |

| Water Stops |

| Chemical Resisting Water Proofing System |

| Roofing and Walls |

| Floor and Basement |

| Water and Waste Management |

| Tunnel Liner |

| Bridge and Highway |

| Other Applications |

| Malaysia |

| Indonesia |

| Thailand |

| Singapore |

| Philippines |

| Vietnam |

| Myanmar |

| By System Type | Cementitious Systems |

| Membranes | |

| Water Stops | |

| Chemical Resisting Water Proofing System | |

| By Application | Roofing and Walls |

| Floor and Basement | |

| Water and Waste Management | |

| Tunnel Liner | |

| Bridge and Highway | |

| Other Applications | |

| By Geography | Malaysia |

| Indonesia | |

| Thailand | |

| Singapore | |

| Philippines | |

| Vietnam | |

| Myanmar |

Key Questions Answered in the Report

What is the projected value of the ASEAN waterproofing market in 2026 and 2031?

The ASEAN Waterproofing Market size is projected to expand from USD 546.01 million in 2026 to USD 751.60 million by 2031, registering a CAGR of 6.60% between 2026 to 2031.

Which system type is growing fastest across Southeast Asia?

Membranes, expanding at a 7.09% CAGR through 2031 on the back of 15-year warranty requirements.

Why are roofing and wall applications attracting premium spend?

Green-building codes in Singapore and Jakarta demand root-resistant, UV-stable assemblies that outperform legacy asphalt felt.

Which country shows the strongest growth momentum?

Singapore posts the highest CAGR at 7.19% through 2031, driven by Super Low Energy building standards.

How does raw material volatility affect suppliers?

Asphalt and polymer price swings compress gross margins and delay fixed-price project awards.

What strategies help firms combat counterfeit membranes?

Digital QR batch tracking, ISO 9001 certification, and on-site applicator training improve authenticity checks and installation quality.

Page last updated on: