Artificial Tears Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

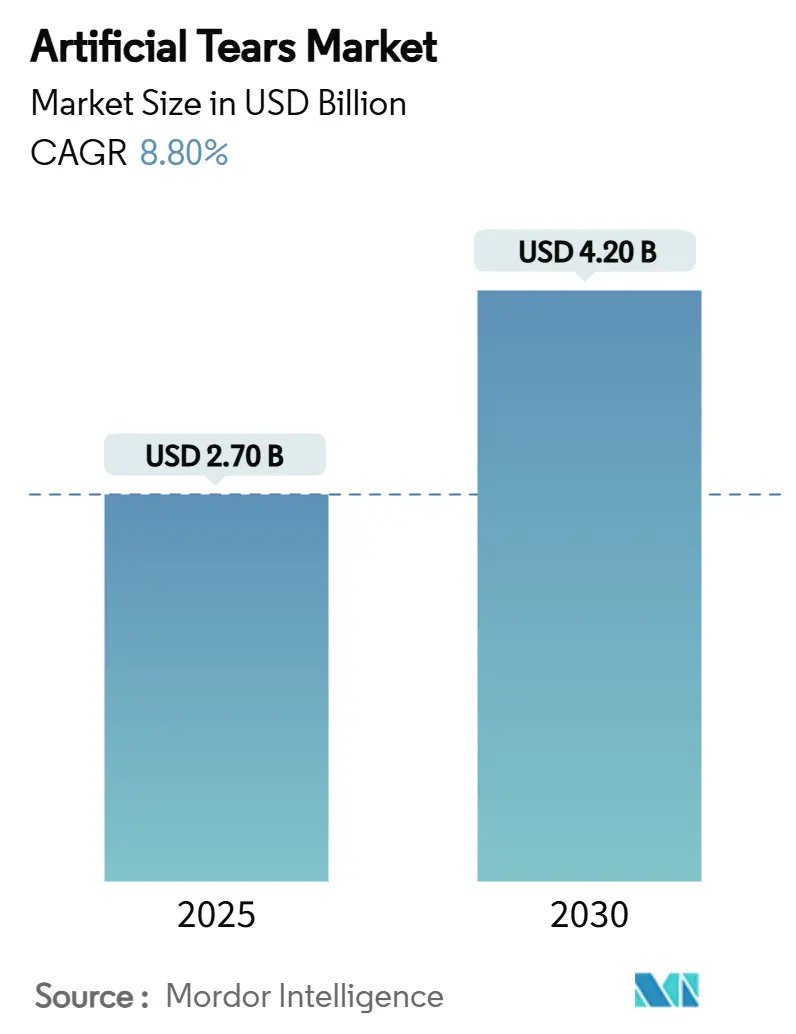

| Market Size (2025) | USD 2.70 Billion |

| Market Size (2030) | USD 4.20 Billion |

| Growth Rate (2025 - 2030) | 8.80% CAGR |

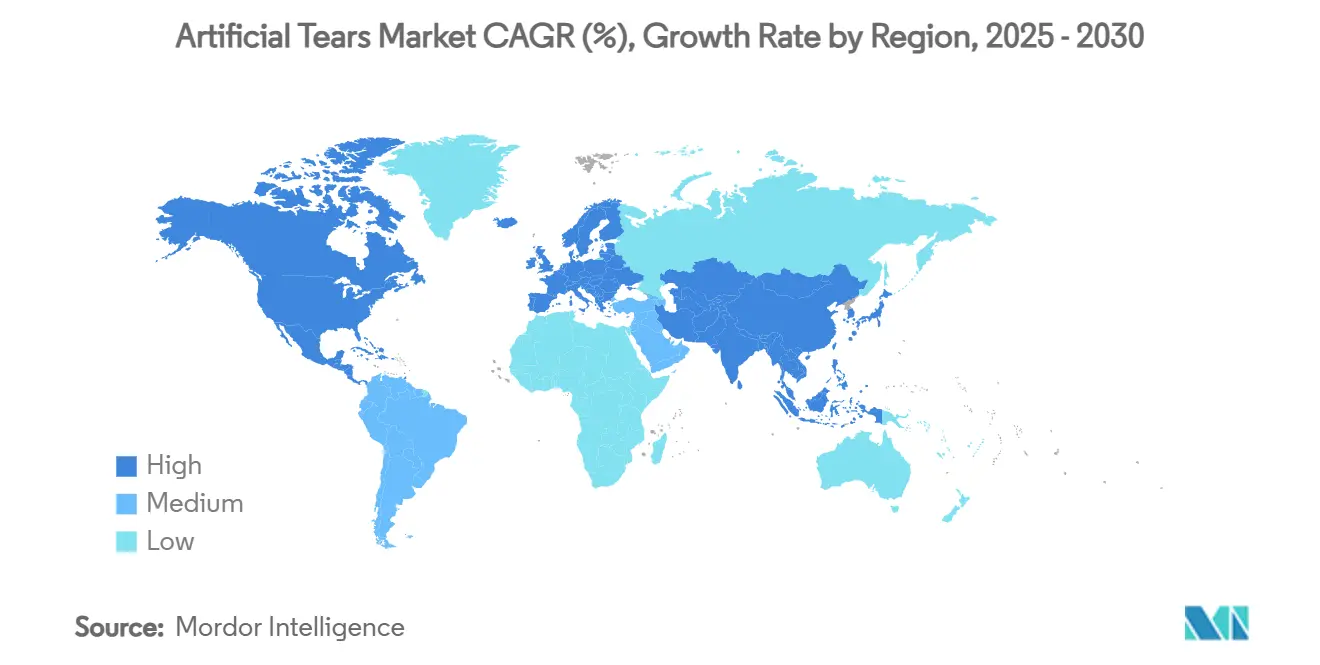

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Tears Market Analysis by Mordor Intelligence

The artificial tears market size reached USD 2.70 billion in 2025 and is forecast to attain USD 4.20 billion by 2030, advancing at an 8.8% CAGR. Growth stems from a larger population of older adults, more hours spent on digital screens, and wider insurance coverage for ophthalmic care. Preservative-free lines now dominate unit sales because they relieve chronic dry eye without benzalkonium chloride irritation. Digital retail is expanding faster than store-based channels as online pharmacies pair low prices with subscription refill programs. Competitive intensity is rising as branded leaders defend price premiums against private-label rivals and invest in sterile manufacturing upgrades in response to recent FDA warning letters. Smart droppers and biomimetic tear-film formulations represent the next wave of differentiation as firms target better adherence and closer physiologic performance.

Key Report Takeaways

- By formulation, preservative-free products held 54.7% of the artificial tears market share in 2024 while growing at an 8.4% CAGR through 2030.

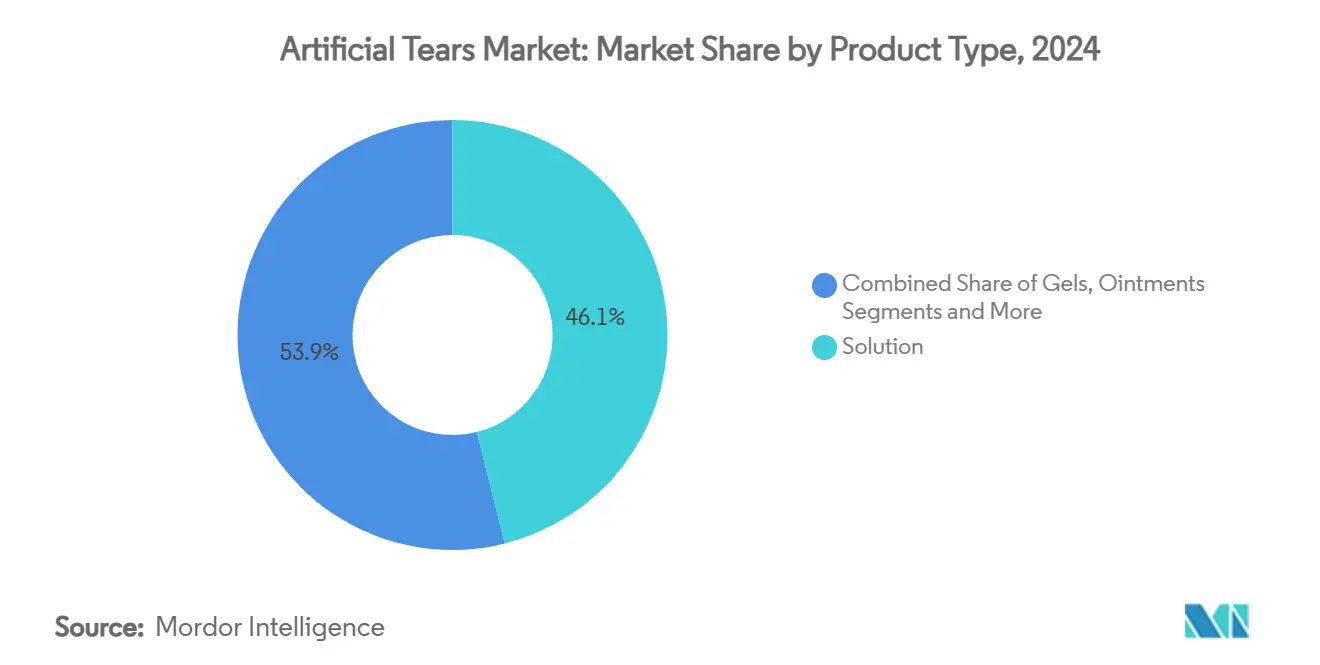

- By product type, solutions commanded 46.1% share of the artificial tears market in 2024, whereas gels are on track for a 7.7% CAGR to 2030.

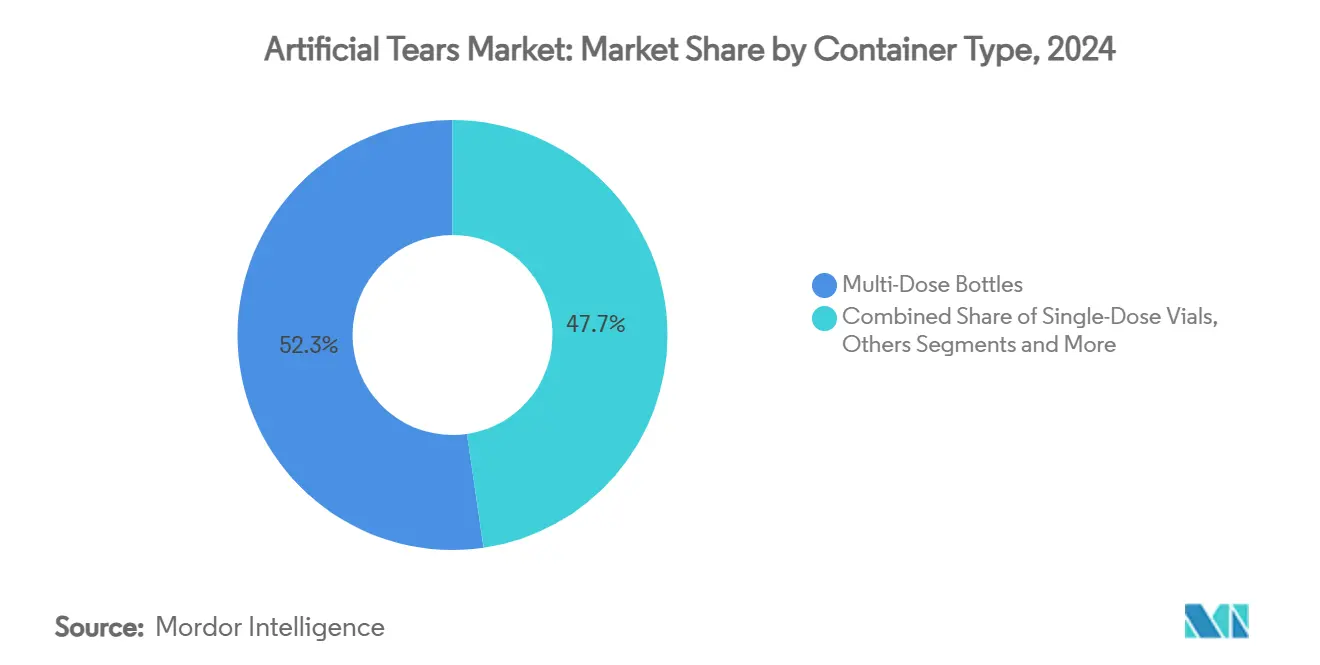

- By container type, multi-dose bottles led with a 52.3% share in 2024; single-dose vials are forecast to expand at a 9.1% CAGR by 2030.

- By application, dry eye syndrome accounted for 62.9% of the artificial tears market size in 2024, yet contact-lens moisture use is advancing at a 10.1% CAGR.

- By distribution channel, retail pharmacies held a 43.7% share in 2024, while online pharmacies are projected to post a 12.3% CAGR.

- By geography, North America contributed 35.9% of 2024 revenue, whereas Asia Pacific is set to rise at a 6.9% CAGR to 2030.

Global Artificial Tears Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Screen-Time Surge | +2.10% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Higher Clinical Adoption Of Preservative-Free Formulations | +1.80% | Global, led by Europe & North America | Medium term (2-4 years) |

| Rapid OTC Switch Approvals In Key Markets | +1.40% | North America & Europe primarily | Short term (≤ 2 years) |

| Emerging Reimbursements For Dry-Eye Management | +1.20% | North America, expanding to Europe | Medium term (2-4 years) |

| Smart-Dropper Adherence Tech Integration | +0.90% | Developed markets initially | Long term (≥ 4 years) |

| Biomimetic Tear-Film R&D Breakthroughs | +0.70% | Global, research-intensive regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Screen-Time Surge

Demand is climbing because adults over 50 form a growing share of the global population and spend more time on digital devices that destabilize the tear film.[1]U.S. Food and Drug Administration, “Drug Safety Communications,” fda.gov Remote work, now embedded in corporate policy, consistently exposes eyes to low blink rates and blue-light stress. Priority FDA reviews for presbyopia drops signal regulator awareness of age-related ocular strain. Incidence data show chronic dry eye shifting from episodic to persistent, which increases repeat purchases of lubricants. These fundamentals give the artificial tears market durable volume drivers that are not tied to economic cycles.

Higher Clinical Adoption of Preservative-Free Formulations

Ophthalmologists prescribe unpreserved products more often because benzalkonium chloride toxicity worsens ocular-surface inflammation. European regulators back this shift, and packaging innovators such as Aptar have sold more than 25 million sterile squeeze dispensers that keep multi-dose bottles microbe-free. Real-world studies show fewer treatment dropouts when stinging and burning are minimized. Cost parity with preserved alternatives has arrived through better filtration and valve systems. These factors collectively lift both unit sales and average selling prices inside the artificial tears market.

Rapid OTC Switch Approvals in Key Markets

Regulators shorten review times for over-the-counter switches because active ingredients have long safety records. The FDA’s tentative nod for a brimonidine generic illustrates the trend. OTC status widens shelf space in mass retail and opens direct-to-consumer advertising, which lifts brand awareness. Volumes escalate even though unit prices fall. Earlier treatment initiation also improves clinical outcomes by preventing corneal damage, reinforcing payer support for easy access. Overall, faster switches accelerate product adoption and reinforce the artificial tears market growth trajectory.

Emerging Reimbursements for Dry-Eye Management

Large U.S. insurers now cover prescription dry-eye therapies, including intranasal varenicline and cyclosporine sprays. Coverage reduces patient out-of-pocket expense and shifts demand toward high-value formulations. Payers cite cost-effectiveness evidence showing that early control of dry eye avoids costly surgery. Reimbursement clarity incentivizes manufacturers to launch premium devices like smart droppers that monitor dose frequency. Uptake trends suggest lasting upside for the artificial tears market as coverage broadens across Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recurring Recalls Due To Microbial Contamination | -1.30% | Global, with focus on US manufacturing | Short term (≤ 2 years) |

| Margin Pressure From Generic Private-Labels | -0.90% | Global, most acute in price-sensitive markets | Medium term (2-4 years) |

| Regulatory Tightening On Preservatives | -0.70% | Europe & North America primarily | Long term (≥ 4 years) |

| Patient Over-Reliance Masking Severe DED | -0.50% | Developed markets with high OTC access | Medium term (2-4 years) |

| Supply Chain Analysis | -0.40% | Global, with regional variations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Recurring Recalls Due To Microbial Contamination

Alcon, AvKare, and others recalled millions of bottles after sterility failures that risked infection. FDA warning letters highlight inadequate aseptic controls, and corrective actions add unplanned capital costs.[2]U.S. Food and Drug Administration, “Warning Letters for Ophthalmic Products,” fda.gov Consumer trust drops after each recall and slows category growth until quality signals stabilize. Retailers respond by delisting affected brands, giving shelf space to competitors. These episodes weigh on the artificial tears market until manufacturing upgrades fully restore confidence.

Margin Pressure from Generic Private-Labels

Private-label chains cut median generic prices by 20% while branded lines raised tags 44% to offset input inflation.[3]Nature, “Advances in Biomimetic Tear Films,” nature.com Price gaps have widened beyond loyalists’ willingness to pay, moving share to store brands. Innovators now pivot toward preservative-free multi-dose and innovative packaging, where copycats face higher entry hurdles. Yet the pricing squeeze narrows gross margin and funds fewer pipeline bets, muting innovation velocity in the artificial tears market for basic formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Solutions Maintain Dominance Despite Gel Innovation

Solutions hold 46.1% share of the artificial tears market and remain the first-line option for everyday lubrication. Their familiarity, low viscosity, and broad compatibility with dosing devices keep adoption high. Gels are growing at a 7.7% CAGR since they linger longer on the cornea and deliver night-time relief. Manufacturers explore temperature-responsive gel matrices that liquefy during instillation then solidify as body heat rises. Ointments fill overnight care niches, while emulsions rebuild the lipid layer typical in meibomian gland dysfunction cases. Curcumin liposomes and super-lubricity hydrogels under study could produce next-generation solutions that mimic natural tear osmolarity.

The category also sees smart-formulation R&D designed to time-release moisture and reduce dose frequency. Producers integrate UV-blocking compounds and antioxidants to address oxidative stress from blue light. Educational campaigns help customers match viscosity to symptom severity, supporting upsell from standard drops to premium gels. As a result, product mix is shifting toward higher value packs, extending revenue per patient and improving the artificial tears market size outlook for the segment.

By Formulation: Preservative-Free Dominance Accelerates

Preservative-free lines captured 54.7% of the artificial tears market share in 2024 on clinical preference and will advance at an 8.4% CAGR to 2030. Sterile multi-dose bottles once faced cost and complexity barriers, yet new filter membranes now safeguard up to 60 days of use without microbe ingress. European regulators actively position unpreserved products as the standard of care, and U.S. guidelines increasingly echo that stance. Preserved variants persist in single-use sachets and price-driven markets but plateau as awareness of benzalkonium damage spreads.

Packaging also evolves. Santen’s Dimple Bottle uses biomass plastic to lower the carbon footprint while a valve keeps the fluid sterile. Brands test recycled polypropylene and compostable paper trays that meet eco rules without compromising barrier properties. The net result is a sharper value proposition: reduced irritation, lower infection risk, and greener containers, factors that together reinforce the artificial tears market expansion led by preservative-free technology.

By Container Type: Single-Dose Vials Surge Despite Multi-Dose Convenience

Multi-dose formats will retain a 52.3% share in 2024 as they minimize per-dose cost and fit current dosing habits. Single-dose vials, however, will record a 9.1% CAGR through 2030 because they eliminate cross-contamination and simplify dose measurement after surgery. Clinicians recommend them for immunocompromised patients and children. Waste concerns spur recycling schemes in North America and industry programs that collect empty polypropylene pods. Biodegradable polylactic acid vials are in pilot trials and may cut landfill load by 40% within five years.

Connected packaging is emerging. Sensor-enabled caps register each squeeze and send reminders to mobile apps, lifting adherence rates by up to 30% in pilot cohorts. Older users benefit from larger thumb pads and color-coded caps that distinguish day and night products. Container innovation thus addresses both safety and user experience, improving patient retention and extending lifetime value inside the artificial tears market.

By Application: Dry Eye Syndrome Dominance Faces Contact-Lens Challenge

Dry eye syndrome accounts for 62.9% of the artificial tears market size, a share driven by high disease prevalence and chronic dosing. Contact-lens moisture drops exhibit stronger momentum with a 10.1% CAGR as global lens wearers exceed 150 million. Formulations now incorporate agents that prevent protein deposition on silicone hydrogel surfaces, reducing blurred vision episodes. Post-operative lubrication holds steady with procedure volume and benefits from single-dose vial adoption that supports sterility protocols at ambulatory surgical centers.

Research into lacritin proteoforms suggests future drops may restore specific tear proteins rather than supply generic hydration. Veterinary and pediatric applications are gaining notice; regulators flagged recalls that affected both human and animal lines, underscoring cross-species supply chain links. Application diversification, therefore, spreads risk and sustains innovation momentum throughout the artificial tears market.

By Distribution Channel: Online Pharmacies Disrupt Traditional Retail

Retail pharmacies still deliver 43.7% of 2024 sales because pharmacist guidance helps first-time buyers navigate viscosity, preservatives, and application techniques. Online pharmacies post a 12.3% CAGR, propelled by home delivery, auto-refill, and tele-ophthalmology consults. Subscription boxes cut lapse rates in chronic dry eye by shipping two-month supplies two weeks before depletion. Large chains respond with click-and-collect, blending digital convenience with in-store counseling.

Regulation catches up: several U.S. states now allow e-pharmacies to package OTC artificial tears alongside video consults by licensed optometrists. Price transparency erodes brick-and-mortar margins, pressing them to curate premium niche brands. Omnichannel execution thus becomes critical to defend share and maintain the artificial tears market growth across outlets.

Geography Analysis

North America held a 35.9% revenue share in 2024, thanks to higher disposable income, broad insurance coverage, and quick FDA approvals that bring new devices to shelves first. The United States drives most demand, while Canada and Mexico trail but grow modestly on improved access to ocular care. The FDA will harmonize device quality rules with ISO 13485 in February 2026, raising compliance costs for dropping technologies and smoothing global filings.

Asia Pacific grows the fastest at a 6.9% CAGR through 2030 as urbanization increases screen exposure and awareness campaigns highlight eye health. China sees heavy e-commerce adoption, and local producers align with updated National Medical Products Administration rules that speed licensing. Japan’s aging society values high-end preservative-free drops; Santen’s reallocation of capital toward Asian assets illustrates the pull of regional demand. India adds volume through low-cost generics, though premium uptake accelerates in urban hospitals. South Korea and Australia mirror U.S. patterns with strong private insurance and early tech adoption.

Europe presents stable mid-single-digit growth amid stringent environmental policy that pushes recyclable packaging and bans certain preservatives. Germany and the United Kingdom lead clinical research tie-ins, while southern markets adopt new generics more slowly due to price controls. Cross-border e-pharmacy services gain traction under the EU Digital Services Act, broadening reach for niche brands. These regional trends combine to diversify revenue sources and cushion the artificial tears market against singular geographic shocks.

Competitive Landscape

The artificial tears market exhibits moderate fragmentation: the top five companies control roughly 55% of sales, leaving space for generics and specialty entrants. AbbVie, Alcon, and Bausch + Lomb rely on brand equity, global sales forces, and scale manufacturing. In 2024, Bausch + Lomb bought Blink eye drops from Johnson & Johnson for USD 106.5 million, adding a recognized name to its dry-eye suite. Alcon expanded laser cataract capability with its USD 356 million LENSAR purchase, creating a broader peri-operative portfolio that cross-sells lubricants.

Innovation centers on preservative-free technology, innovative adherence tools, and biomimetic ingredients. Smaller biotech firms pursue sustained-release ocular inserts that could reduce daily dosing to weekly intervals. Digital health collaborators offer AI chatbots for symptom triage and automated reordering, improving patient loyalty at minimal cost. Quality management investment escalates after recalls; companies upgrade isolators, sterile filling lines, and rapid-micro test systems to satisfy FDA scrutiny.

Competitive strategy also targets sustainability. Producers trial recyclable high-density polyethylene bottles and offset shipping emissions to appeal to environmentally conscious buyers. Private-label retailers scale quickly by exploiting strong supplier networks and aggressive shelf positioning, squeezing branded margins. As consolidation continues, scale advantages in procurement and compliance favor larger players, yet niche innovators survive by solving unmet needs like pediatric comfort drops. This balance of forces keeps the artificial tears market dynamic and innovation-driven.

Artificial Tears Industry Leaders

AbbVie

Alcon

Bausch & Lomb

Johnson & Johnson Vision

Santen Pharmaceutical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Johnson & Johnson launched TECNIS Odyssey intraocular lens across Europe, the Middle East, and Canada, achieving 93% spectacle freedom among recipients.

- March 2025: The FDA withdrew 12 generic ophthalmic approvals after manufacturers ended marketing, including Bausch & Lomb’s prednisolone drops.

- February 2025: Merck acquired EyeBio for USD 1.3 billion to expand retinal disease research.

- November 2025: Bausch + Lomb finalized the Blink acquisition and bought InflammX Therapeutics for USD 106.5 million.

Global Artificial Tears Market Report Scope

| Solutions |

| Gels |

| Ointments |

| Emulsions |

| Other Types |

| Preserved |

| Preservative-Free |

| Multi-Dose Bottles |

| Single-Dose Vials |

| Others |

| Dry Eye Syndrome |

| Allergies |

| Post-Operative Lubrication |

| Contact Lens Moisture |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies & Drug Stores |

| Online Pharmacies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | Saudi Arabia | |

| By Product Type | Solutions | ||

| Gels | |||

| Ointments | |||

| Emulsions | |||

| Other Types | |||

| By Formulation | Preserved | ||

| Preservative-Free | |||

| By Container Type | Multi-Dose Bottles | ||

| Single-Dose Vials | |||

| Others | |||

| By Application | Dry Eye Syndrome | ||

| Allergies | |||

| Post-Operative Lubrication | |||

| Contact Lens Moisture | |||

| Others | |||

| By Distribution Channel | Hospital Pharmacies | ||

| Retail Pharmacies & Drug Stores | |||

| Online Pharmacies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | Saudi Arabia | ||

Key Questions Answered in the Report

What is the current size of the artificial tears market?

The artificial tears market size reached USD 2.70 billion in 2025 and is projected to climb to USD 4.20 billion by 2030.

Which formulation leads the artificial tears market?

Preservative-free formulations held 54.7% market share in 2024 and continue to grow fastest due to lower ocular irritation.

Why are single-dose vials gaining popularity?

They eliminate contamination risk, meet post-surgical sterility standards, and are expanding at a 9.1% CAGR through 2030.

Which region shows the highest growth potential?

Asia Pacific leads in growth with a 6.9% CAGR as rising screen time and healthcare access boost demand.

How are recalls affecting the artificial tears market?

Repeated sterility recalls reduce consumer confidence and impose costly manufacturing upgrades, subtracting an estimated 1.3% from forecast CAGR.

What technological trends will shape future products?

Smart droppers that track dosing and biomimetic tear-film formulations that mimic natural tears are poised to differentiate next-generation offerings.

Page last updated on: