Artificial Intelligence (AI) In MRI Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

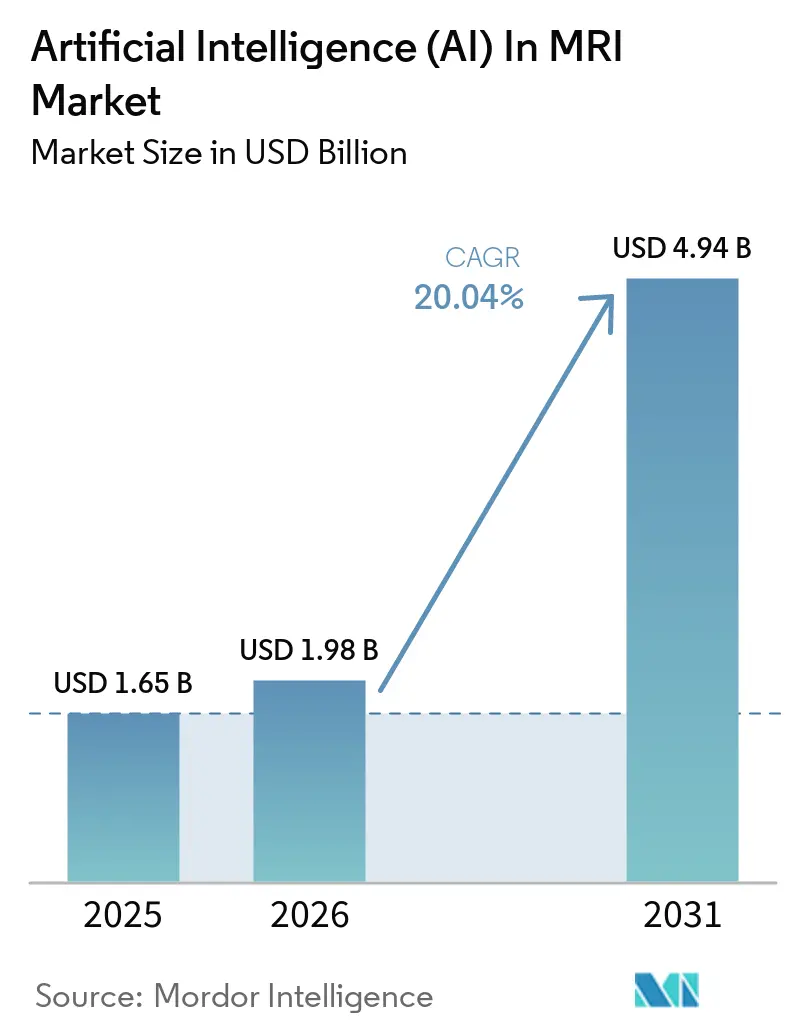

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 4.94 Billion |

| Growth Rate (2026 - 2031) | 20.04% CAGR |

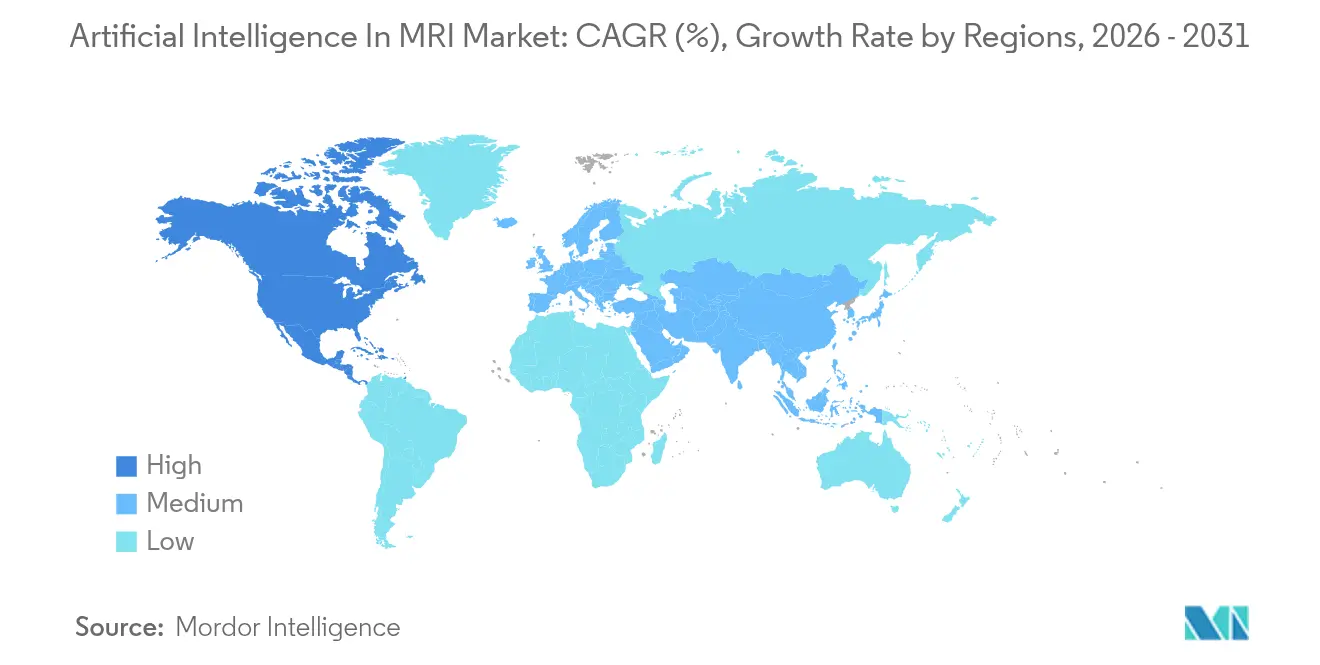

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Intelligence (AI) In MRI Market Analysis by Mordor Intelligence

The Artificial Intelligence (AI) in MRI Market size is expected to grow from USD 1.65 billion in 2025 to USD 1.98 billion in 2026 and is forecast to reach USD 4.94 billion by 2031 at 20.04% CAGR over 2026-2031. Growth is propelled by clearer reimbursement pathways, cloud PACS migration, and vendor-neutral marketplaces that allow algorithms to run on any scanner. Enterprise buyers view AI as a core workflow tool rather than an experimental add-on, a perception strengthened by FDA clearances that now exceed 1,000 imaging algorithms, 80% of which relate to MRI. Portable low-field MRI combined with edge AI is extending advanced imaging into rural settings, while multi-omics integration positions MRI as a data hub for precision medicine. Competitive intensity is moderate as imaging multinationals form partnerships with AI specialists to protect installed bases, even as pure-play vendors innovate in niches such as pediatric and ultra-high-field imaging. Cyber-security costs and data-ownership fragmentation remain restraining factors, but advances in federated learning and homomorphic encryption are steadily mitigating these concerns.

Key Report Takeaways

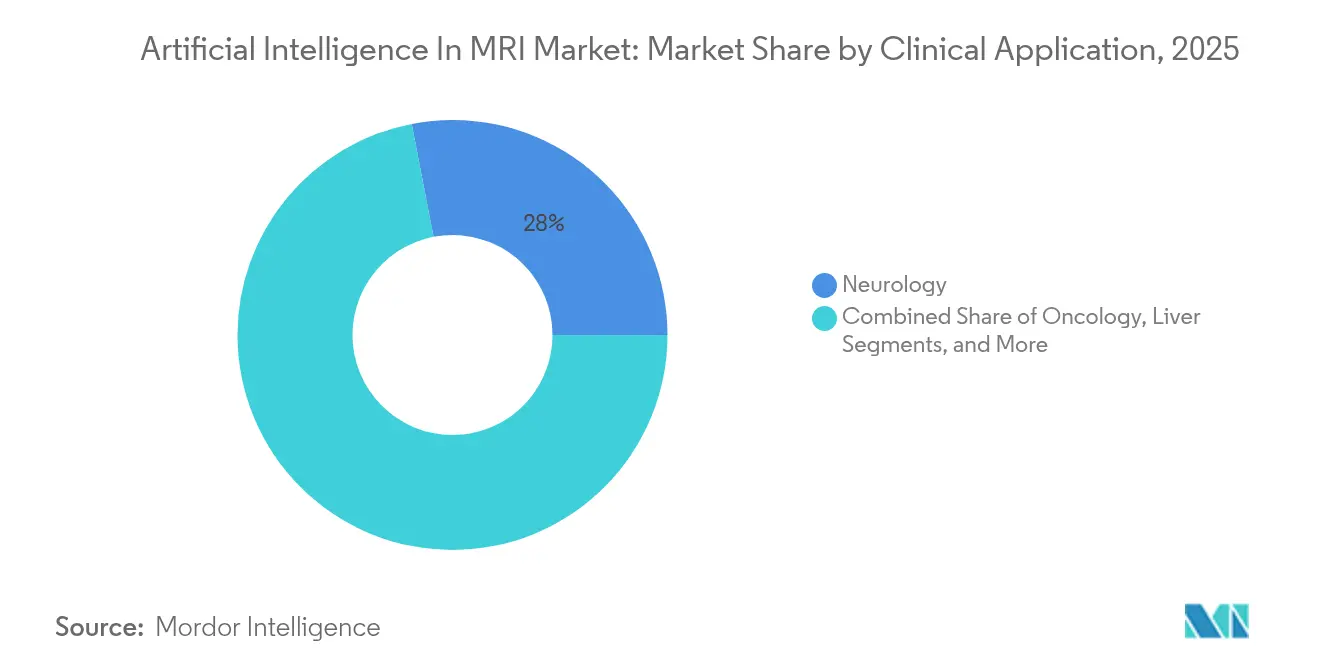

- By clinical application, neurology led with 28.04% of the Artificial Intelligence (AI) in MRI market share in 2025, whereas oncology is projected to expand at a 21.05% CAGR through 2031.

- By solution, software captured 64.12% of the Artificial Intelligence (AI) in MRI market share in 2025, while services are advancing at a 20.31% CAGR to 2031.

- By technology, deep learning held 32.35% of the Artificial Intelligence (AI) in MRI market size in 2025; natural language processing is forecast to grow at 20.86% CAGR to 2031.

- By deployment type, cloud models accounted for 60.55% share of the Artificial Intelligence (AI) in MRI market size in 2025, and hybrid models are growing at 22.02% CAGR.

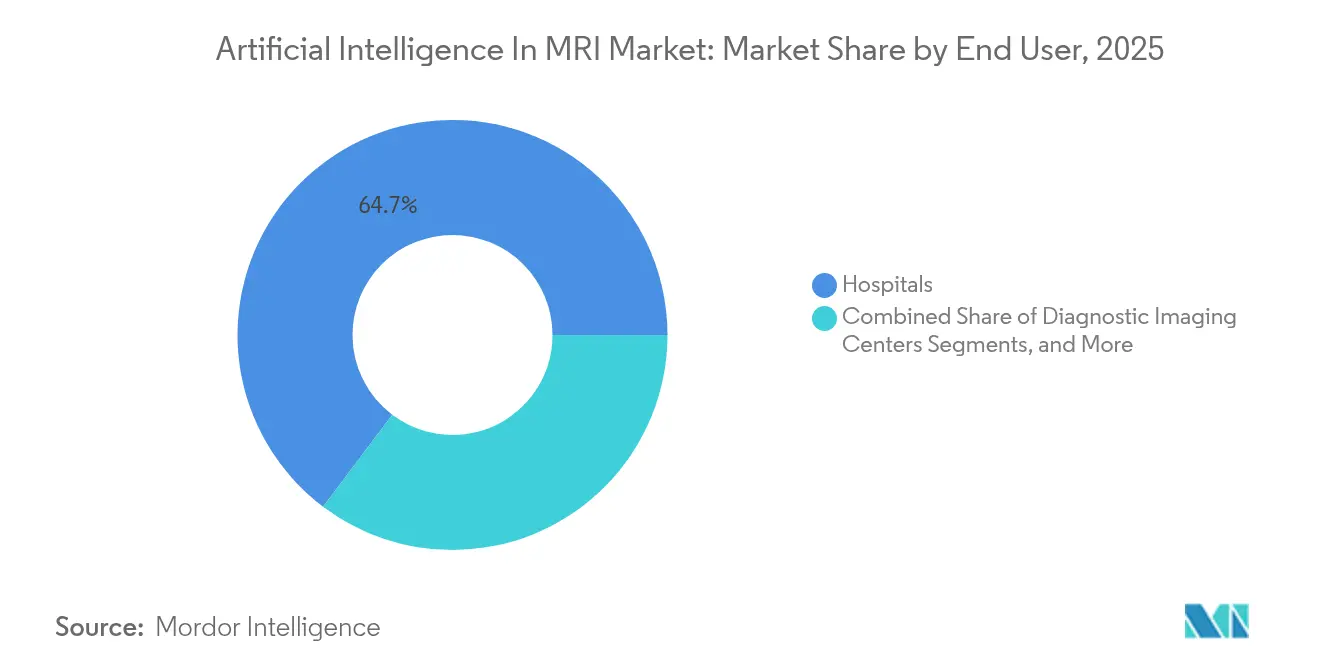

- By end user, hospitals controlled 64.72% share of the Artificial Intelligence (AI) in MRI market size in 2025, but diagnostic imaging centers post the highest 20.8% CAGR through 2031.

- By geography, North America commanded 45.28% of the Artificial Intelligence (AI) in MRI market share in 2025; Asia-Pacific is expanding at 21.43% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Artificial Intelligence (AI) In MRI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement shift to new-technology add-on payments | +3.2% | North America & EU | Medium term (2-4 years) |

| Multi-omics datasets integration | +2.8% | Global research hubs | Long term (≥ 4 years) |

| Portable low-field MRI adoption | +2.1% | APAC core, MEA spill-over | Medium term (2-4 years) |

| Vendor-neutral AI marketplaces | +1.9% | Global | Short term (≤ 2 years) |

| Enterprise cloud PACS migration | +2.4% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| National cancer-screening AI programs | +1.8% | EU & APAC, selective North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Shift to New-Technology Add-On Payments

Medicare’s expansion of new-technology add-on payments (NTAP) to cover FDA-cleared AI MRI tools turns AI from a discretionary spend into a reimbursable service [1]Centers for Medicare & Medicaid Services, “CMS Official Website,” Centers for Medicare & Medicaid Services, cms.gov. Systems now recoup algorithm costs per scan, creating predictable revenue that accelerates enterprise rollouts. Private insurers typically mirror Medicare within 12-18 months, widening the payment pool. Vendors meeting NTAP criteria report faster sales cycles and higher renewal rates. The policy shift especially benefits algorithms that boost diagnostic accuracy, such as stroke triage tools now documenting 21% higher lesion-detection rates.

Multi-Omics Integration Drives Precision Medicine Convergence

AI platforms that fuse MRI radiomics with genomic and proteomic data reach 86.05% accuracy in schizophrenia classification and outperform imaging-only models in therapy response prediction [2]Cornell University, “arXiv e-Print Archive,” arXiv, arxiv.org. Oncology centers deploy such solutions to personalize regimens, reducing trial-and-error prescribing. Data governance frameworks and standardized vocabularies are essential to manage cross-modal inputs, enlarging demand for AI middleware. Research consortia in the United States, Japan, and Germany are pooling de-identified multi-omics datasets to refine predictive models. As protocols mature, multi-omics AI is expected to migrate from flagship hospitals to community imaging networks.

Advances in Low-Field Portable MRI Expand Access

Portable 0.064 Tesla scanners equipped with edge GPUs now perform bedside brain imaging in 15 minutes at one-third the cost of conventional systems. AI-based noise-reduction and super-resolution algorithms close the image-quality gap, unlocking use in emergency rooms and rural clinics. Governments in India and Indonesia are subsidizing low-field units to improve stroke and trauma care. Vendors report a 38% rise in purchase orders tied to disaster-response kits. The portability trend also cultivates new datasets that improve algorithm robustness across field strengths.

Vendor-Neutral Marketplaces Accelerate Algorithm Adoption

Imaging departments increasingly source algorithms from vendor-neutral stores that integrate via DICOM Supplement 219 AI Results profiles. Hospitals select best-in-class tools regardless of scanner brand, reducing lock-in and stimulating algorithm competition. Marketplace usage has tripled since 2023 among mid-size U.S. health systems. Subscription or pay-per-scan pricing lowers entry barriers for smaller sites. Interoperability standards limit integration effort to an average of four IT staff-days per algorithm, half the pre-marketplace norm.

Enterprise-Wide Cloud PACS Migration

Cloud PACS adoption cuts local hardware refresh expenditure by 30% while providing the elasticity needed for on-demand AI inference. Real-time algorithm updates arrive without software patch downtime, and cross-site reading pools improve radiologist productivity by 18%. Vendors bundle cybersecurity services to manage HIPAA and GDPR requirements. Early adopters in the United States report 25% fewer workflow interruptions compared with on-premise AI pipelines. The model’s scalability attracts networks with dozens of imaging sites that previously ran siloed archives.

National Screening Programs Standardize AI

European breast and prostate screening programs now require AI audit trails and quality metrics, creating large validation datasets that feed continuous algorithm improvement [3]European Society of Radiology, “European Radiology Journal,” European Radiology, european-radiology.org. Asia-Pacific governments pilot liver-cancer MRI screening using AI lesion classification to address hepatitis prevalence. Standardized performance thresholds accelerate cross-border algorithm approvals. Public datasets produced by these programs help vendors reduce development time by up to six months, lowering R&D costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented image-data ownership | -2.1% | Global, acute in North America | Medium term (2-4 years) |

| Shortage of annotated 7-Tesla datasets | -1.3% | Research centers worldwide | Long term (≥ 4 years) |

| Cyber-security and PHI-compliance costs | -1.8% | Global, stringent in EU & North America | Short term (≤ 2 years) |

| Opaque model explainability | -1.6% | Global, EU regulatory focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Image-Data Ownership Impedes Algorithm Generalizability

Medical images remain locked in individual health-system silos, limiting access to diverse datasets needed for robust AI training [4]National Center for Biotechnology Information, “PubMed Central Homepage,” National Institutes of Health, ncbi.nlm.nih.gov. Rare-disease models suffer most due to low case volumes. Recent hospital mergers exacerbate silo size without improving sharing. Federated learning can train across sites without moving data, but high compute demands and network latency slow adoption. Industry associations are drafting interoperability charters, yet legal hurdles around secondary data use persist.

Shortage of Annotated 7-Tesla Datasets

Ultra-high-field MRI provides exceptional spatial resolution but is installed mainly at research centers that lack clinical volumes. As of 2025 fewer than 140 scanners worldwide collect annotated patient studies suitable for AI. Vendors cannot justify full-scale commercial models without data, delaying algorithms for epilepsy, micro-vascular pathology, and ultra-fine cartilage assessment. Research grants now include dedicated annotation budgets, but dataset maturity remains a multi-year task.

Cyber-Security and PHI-Compliance Costs

Cloud AI pipelines must satisfy HIPAA, GDPR, and regional privacy rules that add encryption, audit, and access-control overheads. Compliance spending can reach USD 0.12 per image, pressuring margins for high-volume teleradiology firms. Ransomware events at U.S. hospitals in 2024 heightened caution, prolonging procurement approvals. Vendors respond with zero-trust architectures and AES-256 encryption, yet liability insurance premiums continue to rise.

Opaque Model Explainability Risks Clinical Liability

Black-box deep learning systems expose hospitals to malpractice claims when clinicians cannot justify AI recommendations. EU regulators now require post-market surveillance of interpretability metrics. Radiologists prefer saliency-map or counterfactual-explanation features, but implementation is uneven. This restraint slows purchase decisions, particularly in high-risk indications like cardiac ischemia where false negatives carry serious consequences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Clinical Application: Neurology Dominance with Oncology Momentum

Neurology held 28.04% of the AI in MRI market in 2025 due to mature algorithms for stroke, multiple-sclerosis lesion load, and neurodegenerative disease tracking. Oncology’s 21.05% CAGR is poised to narrow the gap as radiogenomic models boost therapy stratification accuracy. Cardiovascular tools automate ejection-fraction measurement with ±3% variance. Musculoskeletal imaging uses AI to grade cartilage degeneration, while prostate algorithms achieve 97.9% sensitivity for clinically significant cancer. The AI in MRI market size for oncology is projected to climb to USD 1.32 billion by 2031 at the segment level, underscoring growth potential.

Neurology vendors focus on acute-stroke triage and longitudinal brain-atrophy quantification, both reimbursed under NTAP. Oncology developers integrate MRI with next-generation sequencing to guide immunotherapy choices. Cardiovascular AI sees broader use as myocardial-perfusion protocols gain insurer coverage. Musculoskeletal models find buyers among sports-medicine clinics seeking point-of-injury decisions. Prostate imaging benefits from active-surveillance programs that favor non-invasive monitoring. Fetal and neonatal applications remain nascent but attract grants targeted at reducing infant morbidity.

By Solution: Software Supremacy with Service Upswing

Software captured 64.12% AI in MRI market share in 2025, reflecting straightforward deployment via PACS plugins and thin-client viewers. AI in MRI market size for services is growing fastest, supported by 20.31% CAGR tied to implementation consulting and algorithm recalibration. Hardware contributes smaller revenue but is critical to edge inference. Super-resolution reconstructions run on GPUs embedded in scanners, aiding sub-second latency.

Hospitals increasingly sign multi-year managed-service contracts that bundle algorithm updates, uptime guarantees, and on-call clinical scientists. Service providers monitor model drift and retrain quarterly using local data. Hardware makers roll out accelerator cards optimized for mixed-precision compute to cut power consumption by 35%. The interplay of software, hardware, and services creates recurring revenue streams that stabilize vendor cash flows.

By Technology: Deep Learning Leads, NLP Accelerates

Deep learning accounted for 32.35% of the AI in MRI market size in 2025 through convolutional and transformer-based networks that segment tissue and quantify lesions. NLP posts 20.86% CAGR as radiology departments automate report generation and mine unstructured text for follow-up compliance. Classical machine-learning retains value in small-dataset settings, while computer vision pipelines provide image normalization and artifact suppression.

Speech recognition integrated with NLP allows real-time dictation feedback that flags inconsistencies. Federated learning gains traction in multi-site research, using secure aggregation to train joint models without copying data. Vendors blend techniques, embedding NLP outputs into image-based networks to create holistic patient profiles.

By Deployment Type: Cloud Scale with Hybrid Agility

Cloud models held 60.55% share of the AI in MRI market size in 2025 and cut total cost of ownership for multi-site networks by 28%. Hybrid configurations grow at 22.02% CAGR as institutions keep PHI on-premise while tapping cloud GPUs for heavy training jobs. Edge devices support low-latency inference in trauma bays.

Regions with stringent data-sovereignty laws, such as Germany and Saudi Arabia, adopt hybrid stacks that encrypt data locally and transmit feature maps only. Cloud vendors court hospitals with HITRUST and ISO 27001 certifications. On-premise holds niche appeal for sites with limited bandwidth or military security protocols.

By MRI System Architecture: Closed-Bore Dominance, Portable Surge

Closed-bore systems held dominant (60.88%) due to homogenous fields and robust AI training datasets. Open systems serve bariatric and interventional cases, while portable scanners witness the fastest unit growth. AI boosts portable image clarity through physics-informed reconstruction, enabling bedside stroke triage.

Healthcare NGOs deploy mobile vans with AI-enhanced portable MRI to conflict zones and disaster areas. Closed-bore vendors add ambient-experience features to counter patient claustrophobia, using AI to predict motion and adaptive sequence selection. Interventional suites integrate open MRI with robotic guidance powered by real-time segmentation.

By MRI Field Strength: Mid-Field Stability, Ultra-High Innovation

Mid-field 1.5 T systems anchor routine imaging and thus AI algorithm volume. High-field 3 T scanners gain share in neuro-oncology where contrast-to-noise gains improve detection. Low-field portable units leverage AI to lift SNR to diagnostic levels, extending access. Ultra-high 7 T remains research-focused; limited data constrains commercial AI offerings.

Interest in adaptive field-strength models that harmonize images across scanners is rising. Vendors explore synthetic 3 T image generation from 1.5 T inputs, reducing repeat scans. The Iseult 11.7 T project advances ultra-high-field research, creating opportunities for micro-structure AI studies.

By End User: Hospital Scale with Imaging-Center Growth

Hospitals command 64.72% market share, leveraging bundled AI in MRI licenses negotiated during fleet upgrades. Diagnostic imaging centers show 20.8% CAGR because smaller governance boards shorten decision cycles. Specialty clinics deploy task-specific models, such as cartilage-measurement tools in orthopedic practices. Academic institutes remain algorithm incubators, publishing validation studies that drive commercial uptake.

Imaging-center chains market AI-accelerated exams as premium services, enhancing patient acquisition. Hospital networks integrate AI outputs into EMRs to trigger care pathways that reduce readmissions. Ambulatory surgical centers pilot intra-operative MRI guidance powered by real-time segmentation.

By Business Model: Subscription Upswing

Perpetual licenses still represent the largest revenue slice, yet AI-as-a-Service subscriptions post double-digit growth as buyers favor OPEX. Pay-per-scan plans appeal to small centers with unpredictable volume. Vendors guarantee 99.5% algorithm uptime and deliver quarterly performance dashboards.

Framework contracts bundle multiple algorithms under flat monthly fees, aligning costs with utilization patterns. Outcome-based pricing pilots tie payments to reduced readmission rates or shorter scan times. Standardized APIs ease switching costs, emphasizing vendor performance over lock-in.

Geography Analysis

North America led the AI in MRI market with 45.28% share in 2025, supported by more than 1,000 FDA-cleared imaging algorithms and favorable NTAP reimbursement. Venture capital funding surpassed USD 1.2 billion for MRI-focused AI start-ups between 2023 and 2025, enabling rapid clinical pilots. Large networks such as Sutter Health deployed cloud AI across 27 hospitals, cutting brain MRI read times by 22%. Academic alliances in Canada leverage national compute grids for federated learning, advancing cross-province stroke models.

Asia-Pacific registers the fastest 21.43% CAGR, driven by public-sector investment and large patient datasets. China’s regulator approved 59 AI devices through Class III pathways by mid-2024, demonstrating high trust in local AI vendors. Japan funds AI to offset radiologist shortages tied to an aging workforce. South Korea’s 5G backbone underpins cloud-first deployments that stream raw k-space data for off-site reconstruction. Australia pilots portable AI-MRI units in remote Indigenous communities.

Europe maintains steady growth aided by the EU AI Act, which classifies medical-device AI as high-risk and mandates quality management systems. Germany’s national radiology society publishes AI scorecards for algorithm transparency, boosting clinician confidence. The United Kingdom’s NHS AI Lab sponsors trials that integrate MRI AI outputs directly into care-pathway dashboards. Middle East health ministries invest in AI to reduce outbound medical tourism, while Chile and Brazil use public–private partnerships to upgrade imaging fleets.

Competitive Landscape

Competitive intensity is moderate, led by Siemens Healthineers, Philips, and GE HealthCare, which collectively manage more than 60% of MRI scanner installations worldwide. Siemens adopted NVIDIA’s MONAI Deploy framework to expedite third-party algorithm certification in its OpenRecon environment. Philips collaborates with NVIDIA to co-develop a foundational MRI model that reduces scan times by 25%. GE HealthCare secured multi-year deals with St. Luke’s University Health Network worth USD 30 million for AI-enabled MRI suites that cut exam slots from 45 to 10 minutes.

Pure-play vendors target niche workflows. AIRS Medical’s SwiftMR reconstruction gains CE Mark and deploys across 11 EU countries. Cerebriu’s Smart Protocols engine automates sequence planning, saving three minutes per study. Mediaire reports 24% market penetration in Germany for its brain volumetry tool, offering cloud or on-premise variants. Start-ups like DeepSpin apply generative topology optimization for compact MRI hardware, promising 50% cost cuts.

Competitive strategy centers on ecosystem building rather than price. Multinationals open algorithm stores to attract developer communities. Patent filings climb, with Siemens holding 450 active AI imaging patents, Philips 395, and GE HealthCare 370. Partnerships with academic centers secure training datasets under compliant data-use agreements. Cyber-security certifications and explainability toolkits become differentiators during tenders.

Artificial Intelligence (AI) In MRI Industry Leaders

Koninklijke Philips N.V.

Siemens Healthineers AG

IBM Corporation

Microsoft Corp (Nuance Communications Inc.)

Perimeter Medical Imaging AI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Aiatella raised €2 million to scale its multi-modal vascular-measurement platform spanning MRI, CT, and ultrasound.

- May 2025: Philips partnered with NVIDIA to build an AI foundational model that lowers MRI scan times and automates zero-click planning.

- April 2025: St. Luke’s University Health Network invested over USD 30 million in GE HealthCare AI-enabled MRI technology with Intelligent Radiation Therapy features.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the artificial intelligence in MRI market as the worldwide revenue generated from software, model-as-a-service platforms, and AI-enabled workflow tools that enhance image acquisition, reconstruction, triage, or quantitative analysis exclusively on magnetic resonance images used in human clinical care.

Scope exclusions include solutions applied to CT, X-ray, ultrasound, research-only MRI, and any hardware revenue, which are outside this assessment.

Segmentation Overview

- By Clinical Application (Value, USD)

- Musculoskeletal

- Oncology

- Liver

- Cardiovascular

- Neurology

- Prostate

- Fetal & Neonatal

- Other Applications

- By Solution

- Software

- Services

- Hardware (Edge GPUs & Accelerators)

- By Technology

- Deep Learning

- Machine Learning (non-deep)

- Computer Vision

- Natural Language Processing

- Speech Recognition

- Federated Learning

- Other Emerging AI Technologies

- By Deployment Type

- On-premise

- Cloud-based

- Hybrid

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Specialty Clinics

- Ambulatory Surgical Centers

- Research & Academic Institutes

- By MRI Field Strength

- Low-field (<1.5 T)

- Mid-field (1.5 T)

- High-field (3 T)

- Ultra-High-field (7 T +)

- By MRI System Architecture

- Closed Bore

- Open MRI

- Portable / Point-of-Care MRI

- By Business Model

- License / Perpetual

- Subscription (SaaS)

- Pay-per-scan

- AI-as-a-Service

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed radiologists, PACS administrators, AI start-ups, and large-hospital procurement leads across North America, Europe, and Asia-Pacific. Dialogs clarified average selling prices, cloud adoption hurdles, and real-world scan-time gains, allowing us to reconcile desk findings and finetune growth drivers.

Desk Research

Our team screens open datasets such as FDA 510(k) AI device clearances, OECD health-expenditure series, Eurostat diagnostic-imaging procedure volumes, and WHO cancer registries, then layers insights from radiology trade bodies like RSNA and the European Society of Radiology. Company 10-Ks and investor decks provide penetration benchmarks, while D&B Hoovers and Dow Jones Factiva supply private-market revenue ranges. Patent-family trends from Questel help gauge algorithm maturity across sequences. The sources listed here are illustrative, not exhaustive.

Market-Sizing & Forecasting

We begin with a top-down reconstruction of the install base of MRI scanners and annual scan volumes by region, apply verified AI-penetration rates from interviews, and multiply by blended software ASPs to derive 2025 revenue. Supplier roll-ups and sampled contract checks act as a bottom-up cross-check, and any variance beyond ±8 % triggers re-work. Key model inputs include scanner density per million population, median scan minutes saved through AI, reimbursement codes that reward AI-assisted studies, venture funding inflows, and algorithm approval counts. A multivariate regression on these drivers underpins the 2025-2030 forecast, while scenario analysis captures regulatory or reimbursement shocks.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, senior-analyst peer check, and research-manager sign-off. Models refresh annually; interim events such as landmark FDA clearances prompt quick revisions so clients receive the latest view.

Why Mordor's Artificial Intelligence In MRI Baseline Earns Unmatched Trust

Published market values often diverge because firms pick different inclusion rules, currency years, or refresh speeds.

Key gap drivers in this field stem from whether pure-play algorithm revenue is isolated, how multi-modality suites are split, and the depth of clinical-procedure mapping. Mordor's study captures only MRI-specific AI software and service income and updates every twelve months, whereas others mingle hardware or broader imaging AI and extend older price decks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.65 B | Mordor Intelligence | MRI-only AI software & services, scan-volume anchored |

| USD 6.17 B | Regional Consultancy A | Bundles AI modules sold with MRI hardware and service contracts |

| USD 7.12 B | Industry Association B | Aggregates all imaging AI modalities, extrapolates from venture funding without scan-volume filters |

In summary, because we align market scope tightly with clinical MRI usage, validate every assumption through practitioner interviews, and triangulate volumes with procedure statistics, Mordor's baseline offers decision-makers a balanced and reproducible yardstick that sits between over-stated total-imaging figures and hardware-weighted estimates.

Key Questions Answered in the Report

How big is the Artificial Intelligence (AI) in MRI Market?

The Artificial Intelligence (AI) in MRI Market size is expected to reach USD 1.98 billion in 2026 and grow at a CAGR of 20.04% to reach USD 4.94 billion by 2031.

Which region leads the Artificial Intelligence (AI) in MRI market?

North America holds 45.28% of global revenue in 2025, supported by clear FDA pathways and NTAP reimbursement.

Who are the key players in Artificial Intelligence In MRI Market?

Koninklijke Philips N.V., Siemens Healthineers AG, IBM Corporation, Microsoft Corp (Nuance Communications Inc.) and Perimeter Medical Imaging AI are the major companies operating in the Artificial Intelligence In MRI Market.

Which is the fastest growing region in Artificial Intelligence In MRI Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Page last updated on: