Market Overview

| Study Period | 2019 - 2031 |

|---|---|

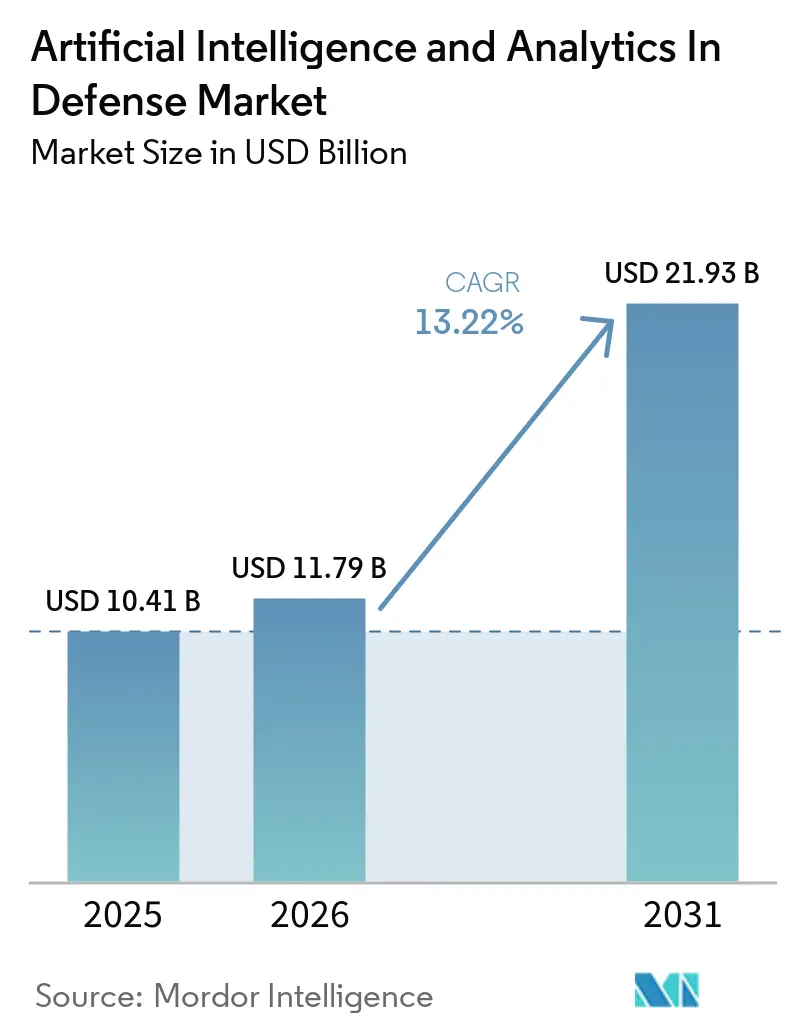

| Market Size (2026) | USD 11.79 Billion |

| Market Size (2031) | USD 21.93 Billion |

| Growth Rate (2026 - 2031) | 13.22% CAGR |

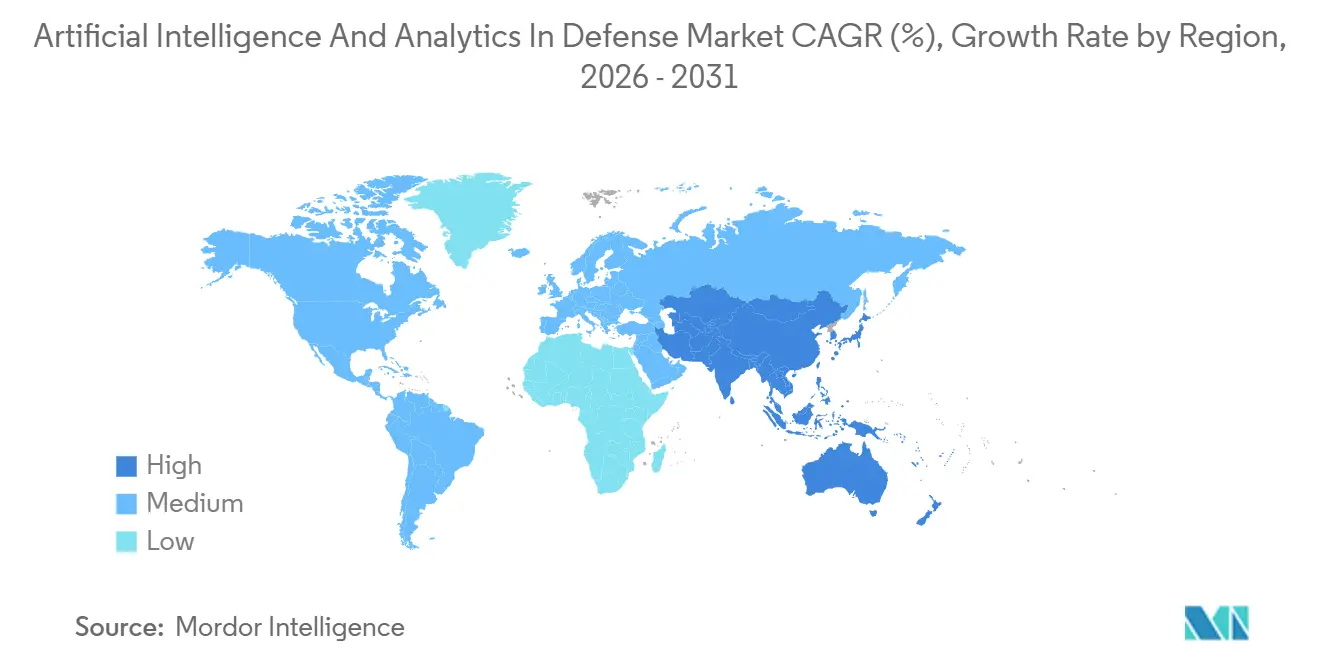

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

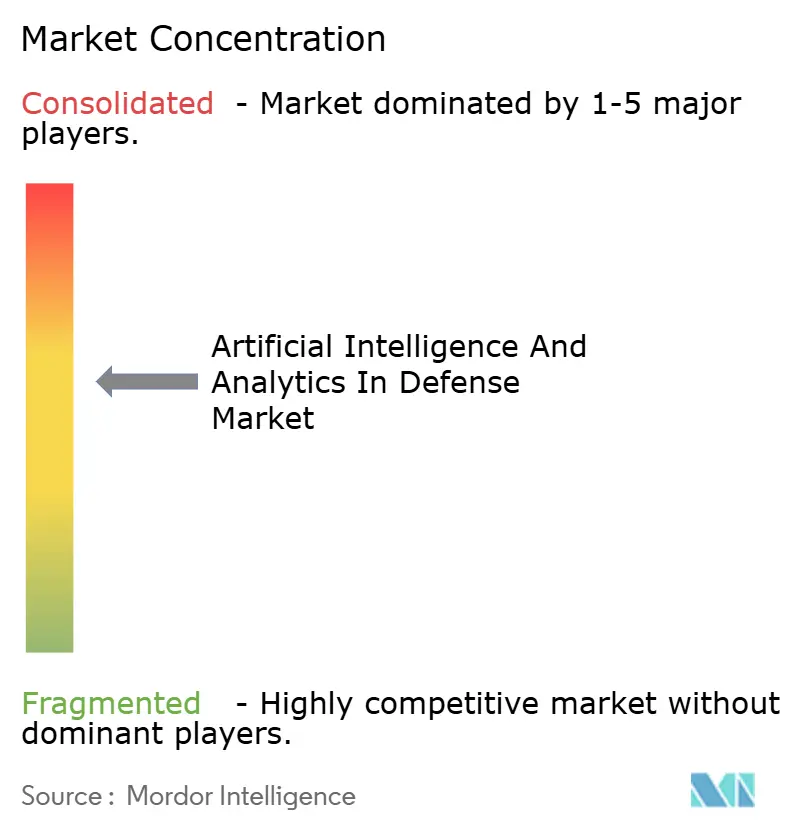

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Intelligence And Analytics In Defense Market Analysis by Mordor Intelligence

The artificial intelligence and analytics in defense market size is expected to grow from USD 10.41 billion in 2025 to USD 11.79 billion in 2026 and is forecasted to reach USD 21.93 billion by 2031 at a 13.22% CAGR during 2026-2031. Recent procurement momentum, expanding pilot-to-program transitions, and mission needs in contested theaters point to sustained adoption beyond isolated prototypes. Programs that scale data integration and autonomy at the edge are reshaping timelines and contracting patterns in ways that favor software speed and modular upgrades. Government guidance encourages automation under human oversight, which channels investment into logistics, maintenance, intelligence fusion, and training use cases that avoid sensitive debates over lethal autonomy. Record multi-year software agreements and defense-cloud deployments show buyers consolidating around platforms that can unlock classified and coalition data while meeting accreditation thresholds.

Key Report Takeaways

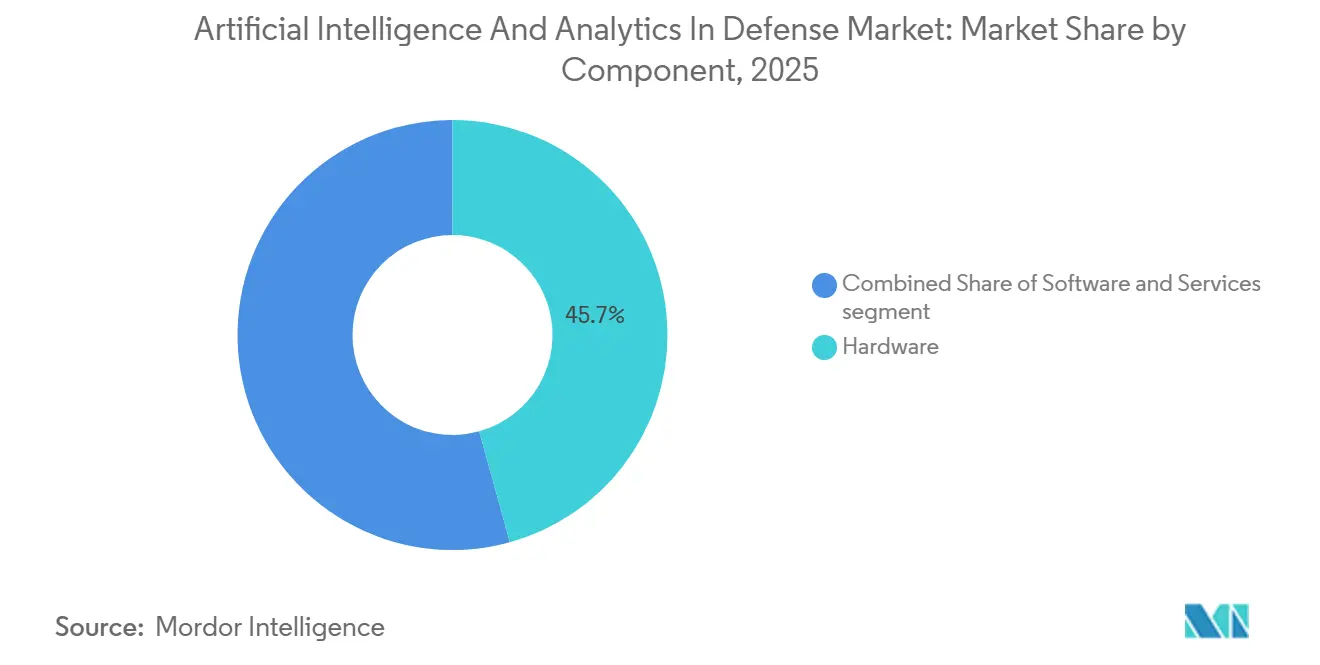

- By component, hardware accounted for 45.70% of 2025 revenue, while services are projected to grow at a CAGR of 17.10% through 2031.

- By platform, land systems captured a 43.55% market share in 2025, while airborne platforms are projected to advance at a 15.85% CAGR through 2031.

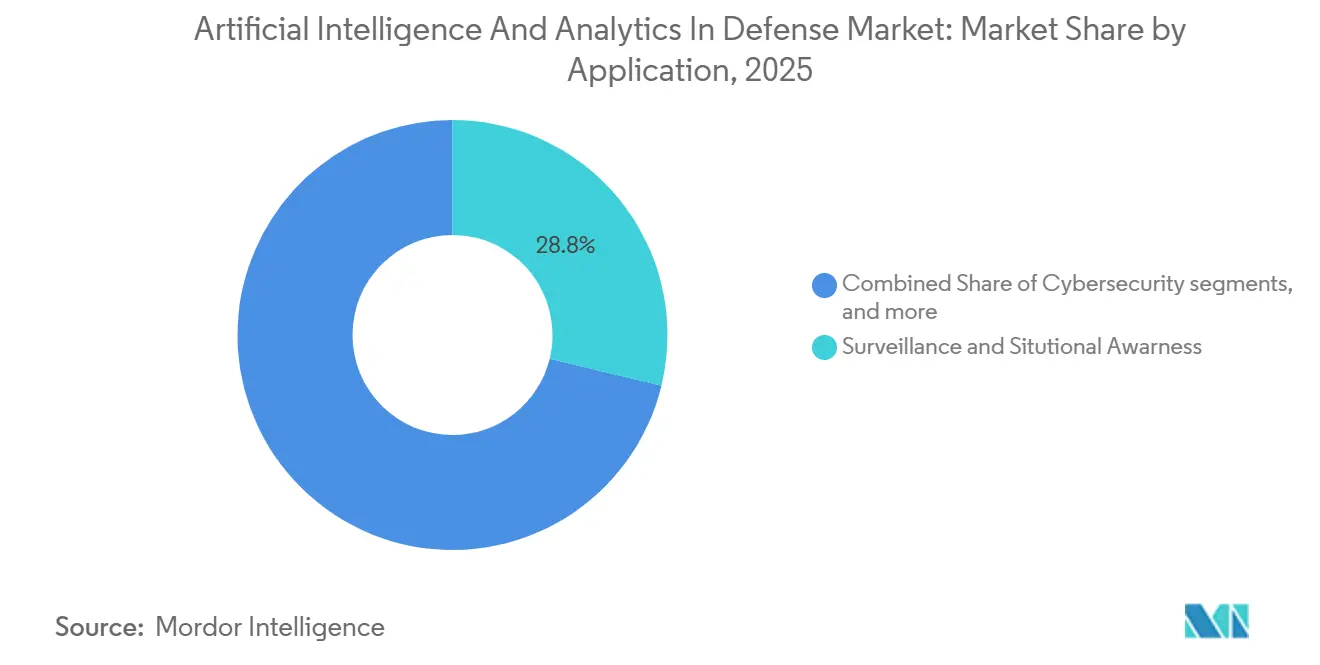

- By application, surveillance and situational awareness led with 28.80% revenue share in 2025, while the training and simulation segment is projected to expand at a 16.30% CAGR through 2031.

- By technology, artificial intelligence (AI) accounted for 64.25% of 2025 spending, while big data analytics is projected to grow at a 16.95% CAGR through 2031.

- By geography, North America held a 41.80% revenue share in 2025, while Asia-Pacific is projected to grow at a 15.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Artificial Intelligence And Analytics In Defense Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense expenditure on AI-enabled autonomous systems | +4.2% | Global, concentrated in US, China, EU | Short term (≤ 2 years) |

| Exponential growth of real-time battlefield data | +3.1% | Global, accelerated in active conflict zones | Medium term (2-4 years) |

| Government AI R&D funding initiatives | +2.8% | US, China, EU, India | Medium term (2-4 years) |

| Need for faster, data-driven decision-making | +1.9% | Global | Short term (≤ 2 years) |

| AI-based predictive maintenance for extended platform life | +1.5% | Global, emphasis on US Air Force, Navy | Long term (≥ 4 years) |

| Growth of synthetic training environments | +1.3% | US, UK, India, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Defense Expenditure on AI-Enabled Autonomous Systems

Defense buyers are converting pilots into programs with contracts that fund autonomy at scale across air, ground, and maritime domains. The US Navy’s multiyear award to Saronic for modular unmanned surface vessels signals procurement acceptance of attritable systems and validates mission demand for autonomous maritime surveillance and security roles.[1]U.S. Navy, “Navy Awards Saronic Technologies $392+ Million USV Contract,” U.S. Navy, navy.mil Software spending is expanding through enterprise-level agreements that embed data integration and AI decision support across services and classification levels, demonstrated by the US Army’s maximum-value agreement for Palantir platforms. Allied governments are standardizing on AI-enabled decision support as well, with the UK awarding a large contract for a data integration and AI platform that consolidates workflows and accelerates delivery across defense organizations. Flight test activity has also advanced autonomy maturity with collaborative combat aircraft demonstrations that validate mid-flight software handoffs and interoperability between competing control stacks, an indicator that autonomy software is approaching multi-vendor operability at a relevant scale. New solicitations for classified-ready compute clusters indicate continued investment in training and hosting advanced models within secure environments, strengthening demand for hardened edge and deployable cloud infrastructure.

Exponential Growth of Real-Time Battlefield Data

Operational video and telemetry generation has surged, with Ukraine’s war experience producing millions of hours of video used to train detection and targeting models. This data foundation enables faster classification cycles and improved accuracy rates in the field. Field demonstrations by the Indian military showed that fusing satellite, drone, and radar feeds using machine learning improved detection accuracy against concealed launchers, supporting the case for multi-sensor analytics on contested borders. Intelligence platforms that scale across services, such as Maven deployments, are helping process imagery and signals data at speeds that reallocate analyst time to higher-value tasks, aligning with the operational shift toward automated triage and human-on-the-loop review. As software-defined kill chains depend on accurate, timely data, institutions are establishing model-serving platforms and common data layers in accredited environments to shorten the collection-to-decision timelines. The combination of more sensors, better onboard compute, and secure AI pipelines now underwrites mission threads where machine-speed correlation becomes decisive in contested electromagnetic conditions.

Government AI R&D Funding Initiatives

Agencies have formalized AI as a core capability area, pairing policy guidance with programs that fund explainability, robustness, and human-machine teaming. DARPA’s AI Next Campaign spans dozens of efforts that target foundational model reliability and dynamic teaming constructs, which feed into acquisition programs looking for validated components that can transition to operations. The Department of Defense has also launched generative AI initiatives for cleared users that focus on mission planning, training content, and intelligence synthesis, under strict governance that speeds experimentation while maintaining guardrails. Parallel investments in research infrastructure, such as the National AI Research Resource pilot, expand shared compute access for defense-adjacent research communities and reduce bottlenecks for testing and benchmarking. Procurement activity for GPU clusters at high classification levels reinforces the build-out of sovereign capacity required to train and deploy models in sensitive environments. Policy guidance emphasizing automation, paired with human oversight mandates for lethal outcomes, provides a predictable lane for growth in logistics, maintenance, intelligence fusion, and training that avoids regulatory deadlock on weapons autonomy.

Need for Faster, Data-Driven Decision-Making

Commanders face compressed engagement timelines and dense sensor feeds that favor automated triage, recommendation, and tasking. Ukraine’s adoption of first-person-view drones combined with machine learning improved strike accuracy, a case study in how algorithmic targeting can yield immediate battlefield effects under high attrition. India’s Operation Sindoor demonstrated high detection accuracy by unifying multi-source intelligence in real time, reinforcing the operational payoff from data fusion and near-instantaneous classification. At the enterprise layer, the scaling of defense data platforms has shifted targeting and mission-planning workloads toward AI-enabled workflows that cut cycle times, relying on accredited clouds and common data fabric choices that centralize access and auditability. Department-level memoranda direct the use of AI to improve speed and reduce manual choke points while retaining human authority for lethal effects, codifying a balanced approach to decision support. As a result, the market is aligning product roadmaps with compressed observe-orient-decide-act cycles where rapid course-of-action generation and logistics prepositioning become standard.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront integration costs | -2.4% | Global, acute in US/EU due to CMMC, ATO processes | Short term (≤ 2 years) |

| Scarcity of defense-qualified AI talent | -1.8% | Global, especially US cleared workforce | Medium term (2-4 years) |

| Ethical and regulatory concerns over lethal autonomy | -1.1% | Global, divergent national positions | Long term (≥ 4 years) |

| Data-sovereignty limits on multi-nation model training | -0.9% | Allied coalitions and EU-US data flows | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Integration Costs

Integrating AI into legacy networks and platforms involves accreditation, cybersecurity, and interface mediation, which extend timelines and add costs. Accreditation pathways, such as the Cybersecurity Maturity Model Certification Level 2, have become table stakes for software vendors that want to handle controlled unclassified information across defense networks.[2]Palantir Technologies, “Palantir Achieves CMMC Level 2 Certification,” Palantir Investor Relations, investors.palantir.com Program offices are also working to standardize software stacks across vessels and platforms to reduce fragmentation, which can lower integration cost but requires upfront investment in typical operating environments. Department-level guidance that promotes automation while ensuring human oversight of lethal outcomes means systems must be designed with auditability and controls, which adds non-recurring engineering workload for safety and governance. The artificial intelligence and analytics in the defense market reflect this reality in services growth rates, as integrators monetize ongoing accreditation and sustainment activities aligned with evolving compliance baselines. Vendors with prior accreditations and cleared personnel enjoy a head start, but many programs still require tailored integration that cannot be reused across customers.

Scarcity of Defense-Qualified AI Talent

Scaling AI programs inside classified environments requires engineers with both machine learning expertise and the clearances to handle sensitive data. The pool of such personnel remains limited, since many candidates prefer unclassified commercial roles or lack eligibility for security vetting. Primes and established integrators have an advantage because of embedded cleared workforces and in-house accreditation pathways that accelerate onboarding. Startups can compete on algorithmic speed but face hurdles building cleared teams quickly enough to meet program ramp schedules. This talent imbalance favors partnerships that pair agile software houses with integrators who can navigate the compliance stack and staff programs at the required clearance levels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Monetize Integration Complexity

Hardware accounted for 45.70% of 2025 revenue, setting the baseline for compute, sensors, and autonomous platforms, while services posted the fastest projected growth at a 17.10% CAGR through 2031 as integration and sustainment became core value drivers. Authorities are procuring classified-ready compute clusters to support current and next-generation models, including large language and vision architectures, which reinforces demand for ruggedized servers and accelerators. At the same time, enterprise data platforms and command-and-control software continue to anchor software spending, with multi-service agreements that bring common tooling to analysis, operations planning, and intelligence workflows. These developments indicate that buyers prefer scalable platforms capable of operating across classification levels and coalitions, enabling data access and supporting modular application ecosystems instead of isolated point tools. Consequently, the artificial intelligence and analytics in defense market is balancing initial investments in computing and sensors with recurring service contracts for deployment, accreditation, and updates management.

Service expansion in the defense sector is influenced by accreditation requirements and sustainment challenges, including Authority to Operate, adherence to cybersecurity standards, and integration with existing legacy networks, which collectively contribute to recurring scope adjustments. Department policy also encourages automation in logistics and maintenance, which increases the need for model operations, data engineering, and user training across large organizations. Over the forecast, primes and IT integrators are expected to deepen partnerships with autonomy software firms to accelerate fielding and share compliance burdens, an arrangement that fits long-term sustainment contracts as AI permeates mission threads. The artificial intelligence and analytics in defense industry is also adding DevSecOps practices adapted for classified environments, which standardize delivery pipelines and speed patching without undermining security. In this context, services capture the integration premium as data volumes grow and as mission owners demand continuous model retraining that responds to adversary adaptation.

By Platform: Airborne Systems Propel Fastest Expansion

Land systems held the leading 2025 share at 43.55%, while airborne platforms recorded the highest projected growth at 15.85% CAGR through 2031 as autonomy matured in collaborative combat aircraft programs and attritable drones scaled into operational use. Demonstrations of platform-agnostic autonomy and mid-flight software handoff across different control architectures showed that software portability is improving, reducing vendor lock-in and encouraging multi-vendor fleets. Maritime autonomy is also advancing with multi-hundred-million-dollar awards for unmanned surface vessels (USVs) that emphasize modular payloads and persistent surveillance, a sign that navies are building complementary fleets of crewed and uncrewed assets. These platform trends confirm that autonomy is moving beyond isolated pilots into sustained programs where open interfaces and mission software agility are key evaluation factors.

Airborne momentum reflects operational advantages, including rapid deployment, modular payload swaps, and software updates that can be fielded without structural retrofits. Land systems remain central because of volume and mission diversity, from logistics to electronic warfare (EW) and counter-mine roles that scale across brigades. Naval programs are setting the stage for mixed-crewed architectures that exploit uncrewed endurance and risk tolerance in mine countermeasures (MCM), anti-submarine warfare (ASuW), and coastal defense. As programs move into production, the market is likely to reward suppliers that prove reliable autonomy at the edge with robust safety cases, telemetry capture, and post-mission analytics packaged for commanders and maintainers. Over the forecast, platform budgets will continue to favor software-defined capabilities, which makes sustained integration and test capacity a competitive advantage.

By Application: Training Simulation Outpaces Legacy ISR

Surveillance and situational awareness led with 28.80% of 2025 application revenue as AI-enhanced ISR compressed targeting timelines through automated detection, multi-sensor fusion, and pattern analysis across air, land, sea, and space feeds. Scaling intelligence platforms across services elevated the importance of common data layers and orchestration, prerequisites for algorithms that must operate at scale and handle coalition settings. Training and simulation is the fastest riser with a projected 16.30% CAGR, supported by the US Army’s Synthetic Training Environment and major modeling awards that modernize collective training infrastructure.

As cyber threats escalate, cyber defense use cases that pair AI-driven detection with automated response and zero-trust controls are becoming standard in new procurements. Logistics is also a priority, with supply chain assurance tools that forecast disruptions and plan resupply to protect readiness margins. Battlefield healthcare pilots extend this pattern through triage support and diagnostic tools that reduce cognitive load and route limited resources faster. The artificial intelligence and analytics in defense industry is responding with integrated app suites that connect training, operations, maintenance, and support workflows, so that insights generated in one domain feed improvements in another. Collectively, these application trends keep more forces mission-ready and help commanders operate inside compressed decision timelines.

By Technology: Big Data Analytics Gains on AI Dominance

AI was the largest technology category, accounting for 64.25% of 2025 spending, while big data analytics posted the fastest projected growth at a 16.95% CAGR, as defense organizations stood up pipelines to ingest, label, and correlate data from multiple sensors to generate actionable insights. Department initiatives have also prioritized generative AI, with cleared environments enabling mission planning, intelligence summarization, and the creation of training content under strict governance and audit controls. The artificial intelligence and analytics in defense market size for big data analytics is projected to grow at a 16.95% CAGR through 2031, driven by expanded telemetry capture, improved orchestration, and federation requirements spanning national boundaries.

Edge processing, robotics, and context-aware computing continue to advance as supporting layers that harden autonomy in contested electromagnetic environments. Flight testing across multiple platforms indicates that autonomy software is maturing toward multi-vendor operability, which raises the value of interfaces and standards that limit rework across fleets. Engineering workflows are also being accelerated by physics-informed models that compress design cycles for propulsion and airframe components, thereby improving iteration speed for new platforms.

Geography Analysis

North America held 41.80% of the market share in 2025 due to sustained procurement, enterprise software consolidation, and accredited cloud build-outs across services. Institutional guidance and accredited environments for generative AI are strengthening experimentation and deployment pathways that touch operations, training, and maintenance. Suppliers have secured multi-year awards that standardize data foundations across commands and services, shortening onboarding for new applications and reducing duplication. Maritime autonomy and common operating system initiatives are also driving US naval software standardization, which should simplify cross-platform deployments at sea. These structural choices produce a durable base for further AI investments across the region.

Asia-Pacific is projected to grow at a 15.30% CAGR through 2031, supported by official budgets that emphasize modernization and intelligentization as well as domestic investment in surveillance and border security. India’s 2026 defense budget and project pipeline include dozens of AI initiatives and significant deployments along contested borders, a sign that operational demand and industrial capability are converging. China’s official 2025 defense budget provides further context on the scale of regional modernization, which reinforces the need for autonomy and multi-sensor analytics across domains. These factors, together, point to increased regional demand for integrators that can deliver edge autonomy and secure analytics within strict sovereignty rules.

Europe is closing its capability gap through a mix of national programs and union-level initiatives, while also advancing governance frameworks that influence data sharing and AI deployment. The European Commission’s Data Act establishes data rights and sharing conditions that shape defense software architectures, especially in coalition or transatlantic settings. Several countries are seeding specialized institutions and partnerships for defense AI, including newly created or expanded agencies and cross-industry collaborations. Large national awards that standardize data platforms for defense use, including analytics and decision support, further demonstrate the region’s push for sovereign capabilities at scale.

Competitive Landscape

The artificial intelligence and analytics in defense market shows moderate consolidation, with primes scaling classified programs and non-traditional vendors expanding through large enterprise software awards. Primes and integrators are leaning into software velocity by establishing open ecosystems and acquiring simulation, modeling, and autonomy assets to accelerate delivery. BAE Systems created a dedicated digital innovation unit by combining simulation acquisitions to compete in synthetic training programs that are scaling across services and allies.[3]BAE Systems, “OneArc Digital Innovation Subsidiary Launch,” BAE Systems, baesystems.com Companies are also forming partnerships that harden autonomy and expand operator usability, such as intuitive control interfaces for uncrewed systems that reduce training time. These moves mirror buyer priorities around multi-domain operations, operator adoption, and integration speed.

Non-traditional players are winning enterprise agreements and platform-agnostic autonomy trials, giving them leverage to shape data architectures and decision support. Palantir’s expansion across US Army programs and a separate multi-year award in the United Kingdom positions it as a strategic defense data and AI layer across classification levels. Autonomy firms demonstrated cross-platform control and mid-flight software handoffs in collaborative combat aircraft trials, an indicator that agile software houses can integrate in complex flight environments. Maritime autonomy firms secured large Navy contracts that validate modular concepts and affordability goals for uncrewed fleets at sea. Digital engineering is also a battleground, with physics-informed AI cutting design cycle times and suggesting future advantages in rapid iteration and verification.

Capital flows into dual-use autonomy underscore investor confidence in near-term defense revenue and accelerated fielding schedules. Vendors are also consolidating critical compliance credentials, such as CMMC Level 2, to remove barriers to handling sensitive information and to streamline contracting below Top Secret thresholds. Standardization efforts like ShipOS point to a near-term reduction in software fragmentation across fleets, which can make integration and sustainment more efficient for both primes and newer vendors. Together, these shifts suggest measured consolidation around data platforms and autonomy stacks that meet compliance, portability, and operator-usability benchmarks.

Artificial Intelligence And Analytics In Defense Industry Leaders

Lockheed Martin Corporation

Northrop Grumman Corporation

THALES Group

BAE Systems plc

RTX Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Shield AI was selected as the mission autonomy provider for the US Air Force Collaborative Combat Aircraft (CCA) program. This decision, following a competitive evaluation, positions Shield AI’s Hivemind autonomy software as a critical component aboard Anduril’s Fury (YFQ-44A). The development reflects the growing integration of autonomous technologies in defense strategies, emphasizing the importance of innovation and partnerships in addressing operational challenges and advancing the capabilities of next-generation military systems.

- December 2025: BAE Systems launched OneArc, a defense technology entity integrating Bohemia Interactive Simulations, TerraSim, and Pitch Technologies. This strategic move consolidates expertise in synthetic training, simulation, interoperability, geospatial technologies, data analytics, and AI. By addressing the evolving threat landscape, OneArc positions BAE Systems to enhance mission readiness and operational efficiency for defense clients. The initiative underscores a broader industry trend of leveraging advanced technologies and acquisitions to strengthen capabilities in modern warfare and defense preparedness.

Global Artificial Intelligence And Analytics In Defense Market Report Scope

AI and analytics are revolutionizing the defense sector, enhancing performance and operational efficiency. Military forces worldwide are increasingly embracing AI-powered weaponry. Key technologies driving this transformation include the Internet of Things (IoT), artificial intelligence, robotics, and big data analytics.

The AI and analytics in defense market is segmented by component, platform, application, technology, and geography. By component, the market is classified into hardware, software, and services. By platform, the market is segmented into airborne, land, and naval. By application, the market is segmented into cybersecurity, battlefield healthcare, warfare platform, logistics management, training and simulation, surveillance and situational awareness, and others. By technology, the market is segmented into artificial intelligence (AI), big data analytics, and other technologies. Other technologies include the Internet of Military Things (IoMT), cybersecurity, and immersive technologies. The report also covers the market sizes and forecasts for AI and analytics in defense market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

By Component

| Hardware |

| Software |

| Services |

By Platform

| Airborne | Combat Aircraft |

| Unmanned Aerial Vehicles (UAVs) | |

| Land | Military Fighthing Vehicles |

| Unmanned Ground Vehicles (UGVs) | |

| Naval | Ships |

| Submarines | |

| Unmanned Marine Vehicles (UMVs) |

By Application

| Cybersecurity |

| Battlefield Healthcare |

| Warfare Platform |

| Logistics Management |

| Training and Simulation |

| Surveillance and Situational Awareness |

| Others |

By Technology

| Artificial Intelligence (AI) |

| Big Data Analytics |

| Other Technologies |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Platform | Airborne | Combat Aircraft | |

| Unmanned Aerial Vehicles (UAVs) | |||

| Land | Military Fighthing Vehicles | ||

| Unmanned Ground Vehicles (UGVs) | |||

| Naval | Ships | ||

| Submarines | |||

| Unmanned Marine Vehicles (UMVs) | |||

| By Application | Cybersecurity | ||

| Battlefield Healthcare | |||

| Warfare Platform | |||

| Logistics Management | |||

| Training and Simulation | |||

| Surveillance and Situational Awareness | |||

| Others | |||

| By Technology | Artificial Intelligence (AI) | ||

| Big Data Analytics | |||

| Other Technologies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and 2031 outlook for the artificial intelligence and analytics in defense market?

The artificial intelligence and analytics in defense market size reached USD 10.41 billion in 2025 and is projected to reach USD 21.93 billion by 2031 at a 13.22% CAGR during 2026-2031.

Which application is expanding the fastest through 2031?

Training and simulation is the fastest-growing application with a projected 16.30% CAGR as synthetic environments scale across services and allies.

Which platform segment leads and which is growing the fastest?

Land systems led with 43.55% in 2025, while airborne platforms are advancing at a 15.85% CAGR on the back of collaborative combat aircraft and attritable UAV programs.

Which region holds the largest share and which is accelerating fastest?

North America held 41.80% share in 2025, while Asia-Pacific is projected to post a 15.30% CAGR through 2031 as budgets and deployments scale.

What policy guardrails are shaping adoption in 2026?

The DoD’s AI-first agenda mandates human oversight for lethal decisions and encourages automation in logistics, maintenance, and intelligence, while the EU’s Data Act tightens data governance and sharing rules, affecting cross-border model training.

Page last updated on: