Artemisinin Combination Therapy Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

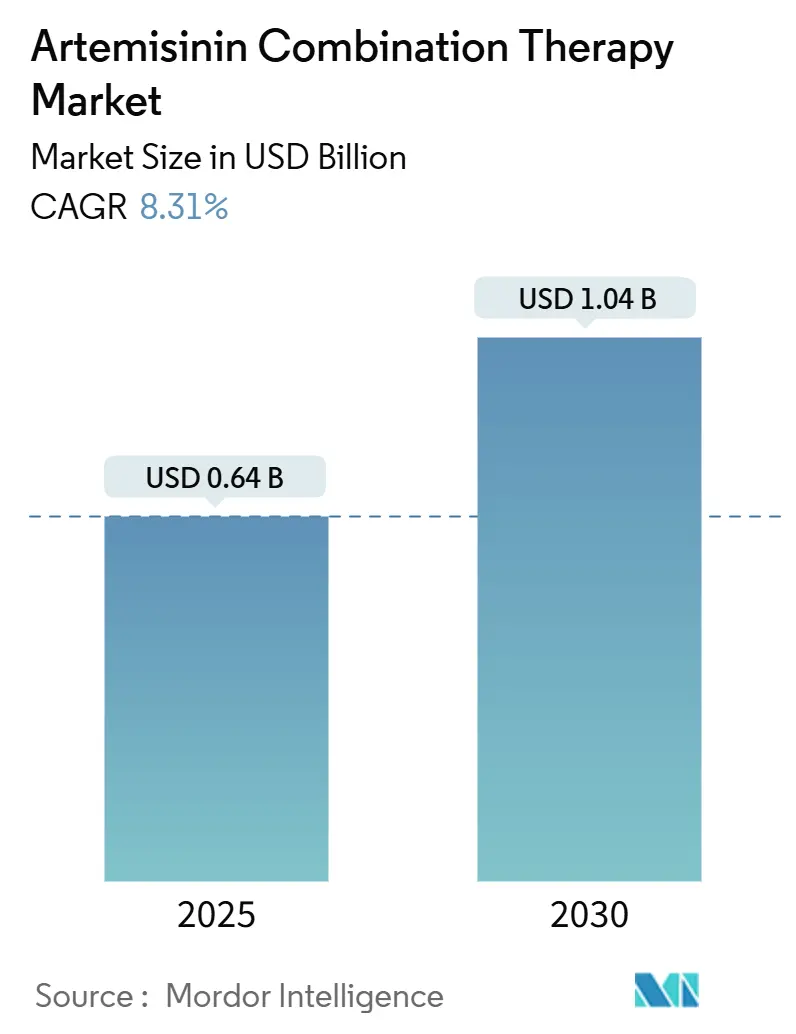

| Market Size (2025) | USD 0.64 Billion |

| Market Size (2030) | USD 1.04 Billion |

| Growth Rate (2025 - 2030) | 8.31% CAGR |

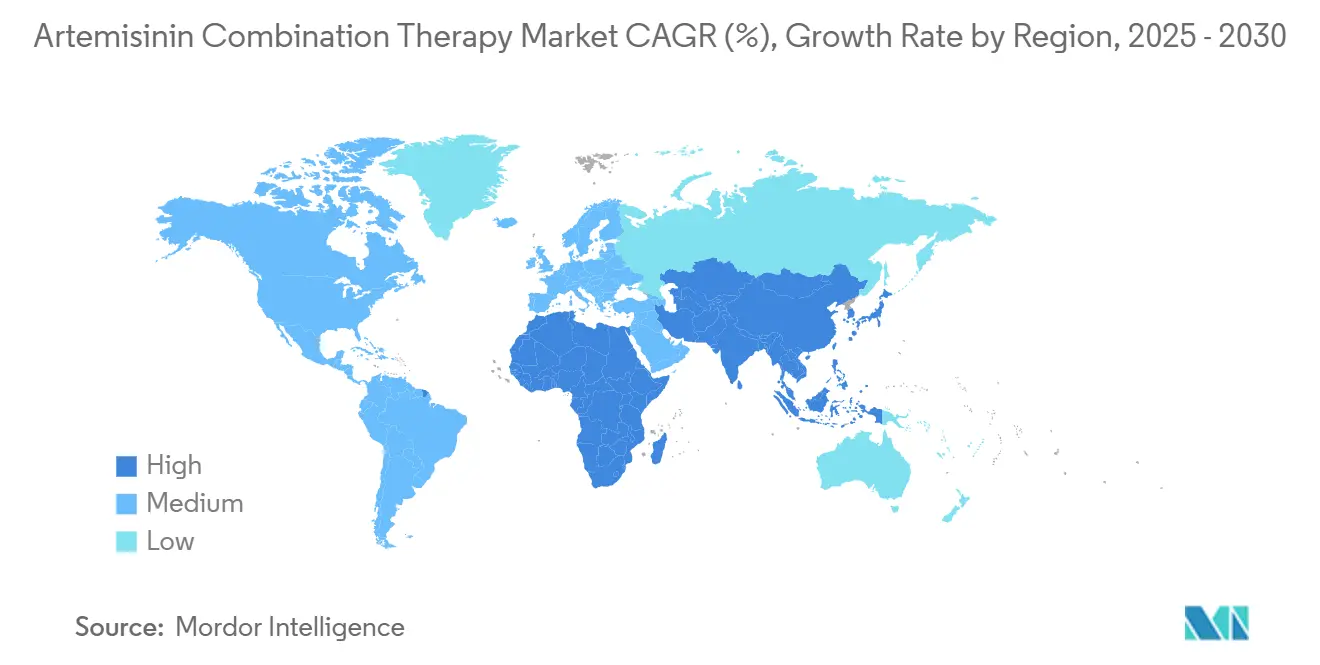

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artemisinin Combination Therapy Market Analysis by Mordor Intelligence

The Artemisinin Combination Therapy Market size is estimated at USD 0.64 billion in 2025, and is expected to reach USD 1.04 billion by 2030, at a CAGR of 8.31% during the forecast period (2025-2030).

Continued reliance on artemisinin-based regimens for uncomplicated Plasmodium falciparum malaria maintains robust baseline demand, while rising resistance in East Africa accelerates therapeutic diversification. Large-scale donor procurement, notably through the Global Fund and the U.S. President’s Malaria Initiative, sustains volumes even as aid volatility injects price uncertainty. Local manufacturing capacity is increasing across India, Nigeria, and Ethiopia, shortening lead times and lowering freight costs. Pediatric innovation, exemplified by Novartis’s Coartem Baby, opens new sub-segments, and the pipeline of triple artemisinin combinations promises differentiation in areas with K13 mutations. Together, these forces are expected to anchor an upward trajectory for the Artemisinin Combination Therapy market, despite cost headwinds in raw material supply.

Key Report Takeaways

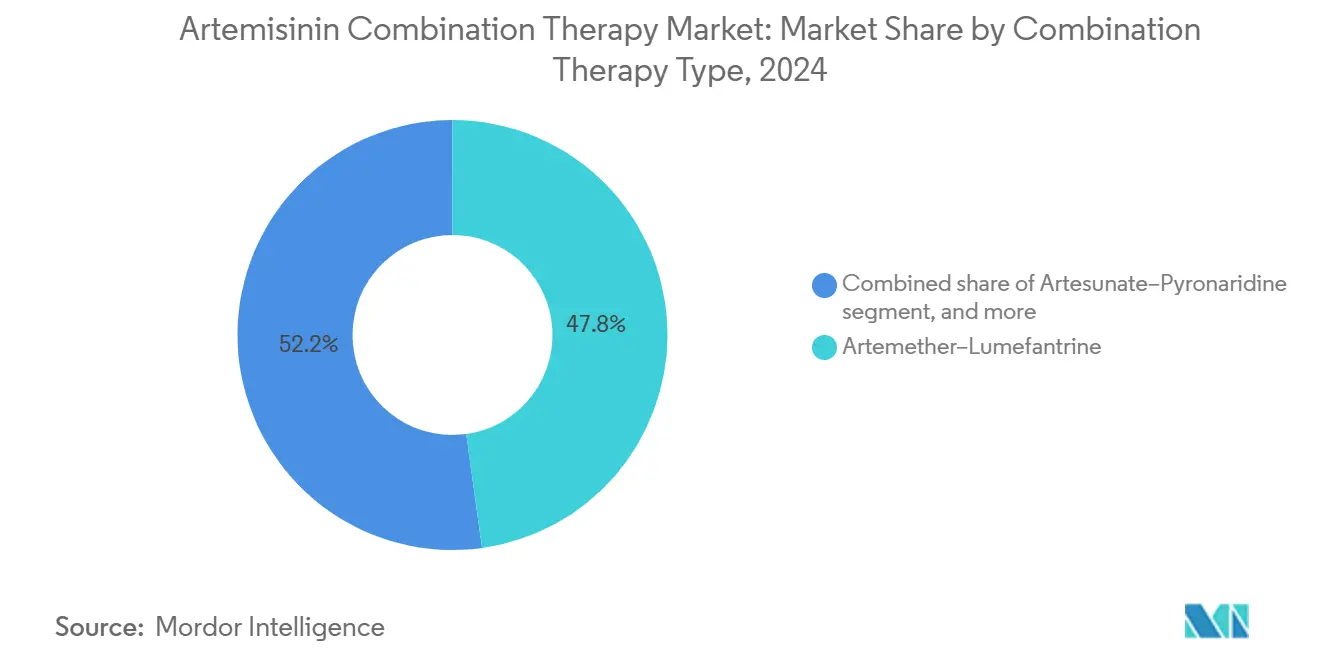

- By combination therapy, artemether-lumefantrine led with a 47.82% share of the Artemisinin Combination Therapy market in 2024; artesunate-pyronaridine is projected to expand at a 10.45% CAGR through 2030.

- By formulation, oral tablets commanded a 68.43% share of the Artemisinin Combination Therapy market size in 2024, while parenteral products are projected to advance at a 10.67% CAGR through 2030.

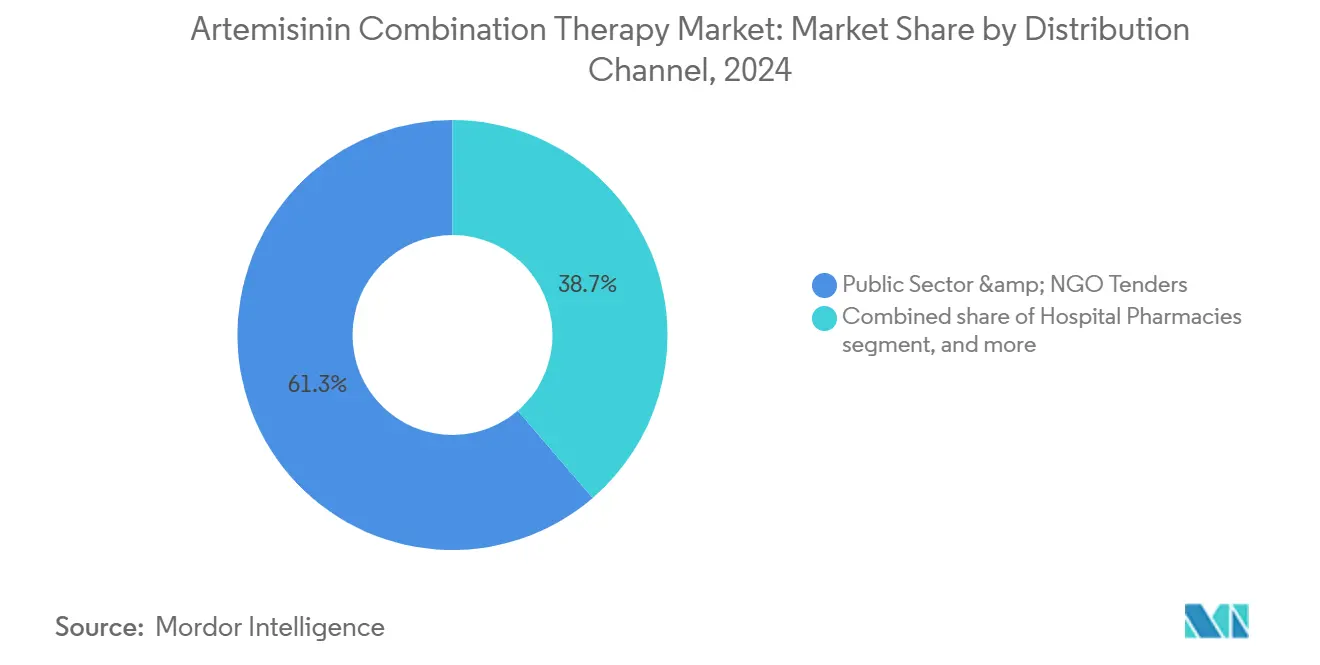

- By distribution channel, public sector tenders accounted for 61.34% of the Artemisinin Combination Therapy market in 2024; retail and online pharmacies recorded the fastest CAGR at 11.87% through 2030.

- By end-user, hospitals accounted for 55.43% of the Artemisinin Combination Therapy market in 2024, whereas community health centers are projected to grow at an 11.45% CAGR from 2024 to 2030.

- By geography, North America captured 42.43% revenue share in 2024; Asia-Pacific is forecast to deliver a 9.43% CAGR between 2025-2030.

Global Artemisinin Combination Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High malaria disease burden in endemic regions | +2.1% | Sub-Saharan Africa, Southeast Asia | Long term (≥ 4 years) |

| Large-scale government and donor procurement programs | +1.8% | Global, Africa-centric | Medium term (2-4 years) |

| Advancements in fixed-dose combination drug development | +1.4% | North America, Europe | Medium term (2-4 years) |

| Expansion of WHO prequalification and regulatory harmonization | +1.2% | Africa, Asia | Long term (≥ 4 years) |

| Scale-up of local manufacturing capacity in Africa and Asia | +0.9% | Africa, Asia-Pacific | Long term (≥ 4 years) |

| Integration of ACT with community case management & digital supply chains | +0.7% | Africa, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Malaria Disease Burden in Endemic Regions

WHO recorded 263 million clinical cases and 597,000 deaths in 2023, with 95% of fatalities in Africa. Climate-linked shifts lengthen transmission seasons, as observed in Burkina Faso and Mali where Novartis enrolled patients outside historic peaks. Children under 5 represent 76% of deaths, fuelling demand for pediatric ACTs. Endemic immunity limits symptomatic cases in adults, yet breakthrough infections still require rapid treatment, sustaining volume demand. Partial artemisinin resistance surpasses 30% prevalence in northern Uganda, compelling manufacturers to explore new partner drugs.

Large-Scale Government and Donor Procurement Programs

Public tenders distributed 217 million ACT courses in 2022, nearly all of which were in sub-Saharan Africa. April 2025 warnings of aid reductions highlight the fragility of funding, disrupting net campaigns and chemoprevention efforts. WHO-prequalified status confers a bidding advantage, nudging smaller regional suppliers toward forming joint ventures. Multiple first-line therapy policies require funders to split orders among at least three ACT regimens, thereby broadening supplier rosters and mitigating single-product risks.

Advancements In Fixed-Dose Combination Drug Development

Regulatory clearance for Coartem Baby in July 2025 satisfied dosing safety for infants under 5 kg. Triple artemisinin combinations achieved non-inferiority in Phase III studies, backed by a USD 3.3 million GHIT grant to Shanghai Fosun. Such innovations are capital-intensive but extend molecule lifespans where K13 mutations compromise efficacy.

Expansion Of WHO Prequalification and Regulatory Harmonization

Dihydroartemisinin from Guilin Pharmaceutical gained prequalification in December 2024, underscoring accelerated reviews that now target 12-month cycles. Tafenoquine’s single-dose indication for P. vivax further diversifies antimalarial portfolios.[1]Medicines for Malaria Venture, “Multiple First-Line Therapy Strategy,” mmv.orgMMV’s plan to double the number of WHO-qualified African producers by 2030 restructures supply chains toward endemic regions.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emergence of multi-drug resistance in Greater Mekong & Africa | -2.3% | Southeast Asia, East Africa | Medium term (2-4 years) |

| Volatile artemisinin raw material supply chain | -1.6% | Global | Short term (≤ 2 years) |

| Increasing competition from novel single-dose antimalarials and vaccines | -1.1% | Global | Medium term (2-4 years) |

| Proliferation of substandard and counterfeit ACTs in informal markets | -1.0% | Sub-Saharan Africa, Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Emergence Of Multi-Drug Resistance in Greater Mekong and Africa

Partial artemisinin resistance involves K13 mutations now exceeding 30% in northern Uganda and 20% in Rwanda. Clinical recurrence rates of 10.3% among children signal rising treatment failure. WHO’s multiple first-line therapy guidance raises procurement budgets because parallel stocks of at least three ACTs are required to blunt selection pressure, inflating inventory costs for ministries of health.

Volatile Artemisinin Raw Material Supply Chain

Artemisia annua yields only 0.5-0.8% artemisinin, and Chinese crop failures can quickly trigger price spikes through global supply chains. Pandemic-era freight bottlenecks resulted in localized stockouts, highlighting supply insecurity. Semisynthetic fermentation offers theoretical insulation but remains commercially subscale despite PATH-led technology transfer. Price volatility affects public tenders the most, necessitating ad-hoc budget reallocations and potentially leading to treatment lapses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Combination Therapy Type: Artemether-Lumefantrine Dominance Faces Resistance Pressure

Artemether-lumefantrine retained a 47.82% market share in the Artemisinin Combination Therapy market in 2024, buoyed by over 1 billion courses delivered since 1999. Yet rising K13 mutations curtail future reliance, pushing artesunate-pyronaridine to a 10.45% CAGR as countries pilot rotation regimens. Mozambique achieved dihydroartemisinin-piperaquine and artesunate-amodiaquine cure rates above 90% by PCR correction, legitimizing therapeutic swap-outs [2]Malaria Journal, “Efficacy of ACTs in Mozambique,” malariajournal.org. Triple combinations under evaluation may soon restructure formularies, compelling manufacturers to field multi-therapy portfolios rather than a single flagship product.

A diverse regimen pipeline reduces the risk of single-product concentration that has historically characterized the Artemisinin Combination Therapy market. Companies able to commercialize two or more WHO-endorsed combinations will capture procurement lots reserved for multi-line strategies, improving share resilience when efficacy shifts.

By Formulation: Oral Tablets Lead While Parenteral Shows Innovation Potential

Oral tablets accounted for 68.43% of the volume in 2024, thanks to community case management protocols that rely on lay health workers. The segment benefits from low manufacturing complexity and ambient-temperature stability. Pediatric demand accelerates the adoption of dispersible formats, such as Coartem Baby, illustrating the revenue unlocked when dosing aligns with weight-band precision.

Parenteral artesunate holds a smaller but vital niche for severe malaria, expanding at 10.67% CAGR as referral networks strengthen. WHO-certified plants run by Guilin, Macleods, and Ipca safeguard quality for the 2.4 mg/kg adult protocol[3]Severe Malaria Observatory, “Injectable Artesunate Dosing Guidelines,” severemalaria.org. Novartis’s investigational intravenous cipargamin aims to replace artesunate where resistance reduces clearance rates, indicating that even low-volume hospital segments can shape R&D agendas.

By Distribution Channel: Public Sector Dominance Amid Private Market Quality Concerns

Public and NGO channels accounted for 61.34% of procurement in 2024, driven by bulk Global Fund tenders that secure unit prices below USD 1. Yet donor cuts jeopardize continuity, exposing gaps that private retail chains fill. Retail and online platforms are growing at a 11.87% CAGR but exhibit a higher prevalence of counterfeit products, with WHO surveys linking non-qualified packs to clusters of treatment failures. Regulators, therefore, pilot digital verification codes, such as Nigeria’s Mobile Authentication Service, to authenticate packs at the point of sale.

By End-User: Hospital Leadership Shifts Toward Community-Centered Care

Hospitals still dispense 55.43% of ACT courses, chiefly parenteral regimens for severe malaria. Nonetheless, community health centers are expanding fastest at 11.45% CAGR as ministries roll out integrated community case management (iCCM) with digital decision support. Madagascar’s economic model estimates 3,722 DALYs averted annually through iCCM scale-up. Smartphone-enabled reporting in Mozambique’s upSCALE and Kenya’s eCHIS systems heighten adherence monitoring, positioning community channels as future volume leaders.

Geography Analysis

North America currently holds a 42.43% market share of the Artemisinin Combination Therapy market, reflecting its significant role in donor-financed global distribution. Purchases made by the U.S. President’s Malaria Initiative and Global Fund hubs in Atlanta secure multi-year framework contracts that stabilize regional demand. Advanced cold-chain logistics and stringent pharmacovigilance systems support rapid batch release, keeping stock-out risk low for both domestic travel clinics and overseas partners. The presence of R&D leaders, such as Novartis and Sanofi, attracts clinical trials that further solidify supplier relationships with procurement agencies. Nevertheless, recent indications of federal budget tightening have injected uncertainty that could reallocate some future orders toward emerging manufacturing centers in Asia.

Asia-Pacific is projected to expand its Artemisinin Combination Therapy market size at a 9.43% CAGR through 2030, the fastest pace worldwide. India’s large-scale plants operated by Cipla and Ipca combine low conversion costs with growing domestic consumption, enabling the region to compete aggressively in tenders. Governments in Myanmar, Papua New Guinea, and Cambodia are aligning their national treatment guidelines with the WHO’s multiple first-line therapy approaches, thereby widening the addressable product portfolio. As more Asian facilities secure WHO prequalification, ministries are shortening lead times and reducing currency exposure by sourcing within the region.

The Middle East & Africa continue to shoulder the heaviest disease burden, yet capture a smaller share of global spending because treatment access relies heavily on external grants. Nigeria, Tanzania, and Uganda are adopting digital package verification codes to combat falsified ACTs, a move expected to lift public confidence and stimulate legitimate retail demand. Local manufacturers in Nigeria and Ethiopia are scaling up their capacity with technical support from the Medicines for Malaria Venture, aiming to double the number of WHO-qualified African suppliers by 2030. Europe contributes primarily through donor financing and vaccine research and development (R&D) rather than direct consumption, but its stringent quality standards shape global specifications that all suppliers must meet.

Competitive Landscape

The artemisinin combination therapy market is moderately fragmented. Multinationals such as Novartis, Cipla and Sanofi secure donor tenders through WHO-qualified portfolios and pharmacovigilance capacity. July 2025 approval of Coartem Baby fortified Novartis’s pediatric franchise, while its ganaplacide-lumefantrine combination progresses in Phase III trials. Cipla leverages cost-competitive Indian plants and a WHO-listed pediatric dispersible to penetrate African tenders. Sanofi co-markets artesunate-amodiaquine, holding strong share in Francophone Africa.

Regional producers—including Nigeria’s Emzor, Ethiopia’s Addis Pharmaceutical Factory and Vietnam’s Mekophar—win local contracts where shipping lead-times trump brand prestige. Digital supply-chain integration is emerging as a differentiator; companies partnered with Kenya’s eCHIS platform obtain usage analytics that strengthen pharmacovigilance dossiers. Competitive threat also arises from vaccine developers: GSK and Bharat’s price-cut pledge for RTS,S and Oxford-Serum’s WHO-listed R21 may suppress adult treatment courses, though pediatric demand will persist given partial efficacy.

White-space opportunities center on triple combinations, infant-weight formulations and synthetic artemisinin inputs. Firms able to bundle these innovations with robust quality assurance will capture incremental Artemisinin Combination Therapy market growth despite structural donor dependence.

Artemisinin Combination Therapy Industry Leaders

Novartis AG

KPC Pharmaceuticals

Cipla Ltd.

Sanofi S.A.

Fosun Pharmaceutical (Guilin Pharmaceutical)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Novartis secured approval for Coartem Baby, the first ACT designed for neonates 2-5 kg, with roll-out across eight African nations.

- June 2025: Oxford University and Recipharm broadened vaccine manufacturing for R78C and RH5.1 candidates, bolstering clinical material supply.

- May 2025: Novartis is committed to maintaining ACT production despite potential donor cutbacks.

Global Artemisinin Combination Therapy Market Report Scope

As per the scope of the report, artemisinin is a plant derivative isolated from artemisia annua, or sweet wormwood, which is known to effectively and swiftly reduce the number of plasmodium parasites in the blood of malaria patients. The artemisinin-combination therapy (ACT) for the treatment of Plasmodium falciparum malaria

The Artemisinin Combination Therapy Market is segmented by Combination Therapy Type (Artemether-Lumefantrine, Artesunate-Amodiaquine, Artesunate-Pyronaridine, Artesunate-Sulfadoxine-Pyrimethamine, and others) and Geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Artemether-Lumefantrine |

| Artesunate-Amodiaquine |

| Artesunate-Pyronaridine |

| Artesunate-Sulfadoxine-Pyrimethamine |

| Other Combination Therapy Types |

| Oral Tablets |

| Oral Suspension (Pediatric) |

| Parenteral (IV/IM Artesunate) |

| Public Sector & NGO Tenders |

| Hospital Pharmacies |

| Retail & Online Pharmacies |

| Hospitals |

| Community Health Centres |

| Travel Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Combination Therapy Type | Artemether-Lumefantrine | |

| Artesunate-Amodiaquine | ||

| Artesunate-Pyronaridine | ||

| Artesunate-Sulfadoxine-Pyrimethamine | ||

| Other Combination Therapy Types | ||

| By Formulation | Oral Tablets | |

| Oral Suspension (Pediatric) | ||

| Parenteral (IV/IM Artesunate) | ||

| By Distribution Channel | Public Sector & NGO Tenders | |

| Hospital Pharmacies | ||

| Retail & Online Pharmacies | ||

| By End-User | Hospitals | |

| Community Health Centres | ||

| Travel Clinics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Artemisinin Combination Therapy market?

The Artemisinin Combination Therapy market size is USD 0.64 billion in 2025.

How fast is the Artemisinin Combination Therapy market expected to grow?

The market is projected to expand at an 8.31% CAGR between 2025 and 2030.

Which combination therapy holds the largest share?

Artemether-lumefantrine leads with 47.82% market share in 2024.

Why is artesunate-pyronaridine gaining popularity?

It records the highest CAGR at 10.45% due to efficacy against emerging artemisinin resistance.

How does donor funding affect market stability?

Donor procurement supplies more than 60% of global ACT volumes; aid cuts can trigger supply gaps and price volatility.

Which region is growing fastest?

Asia-Pacific is forecast to grow at a 9.43% CAGR, driven by local manufacturing and persistent malaria burden.

Page last updated on: