Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.51 Billion |

| Market Size (2026) | USD 1.54 Billion |

| Market Size (2031) | USD 1.73 Billion |

| Growth Rate (2026 - 2031) | 2.26% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Armenia Freight And Logistics Market Analysis by Mordor Intelligence

The Armenia freight and logistics market size is expected to grow from USD 1.51 billion in 2025 to USD 1.54 billion in 2026 and is forecast to reach USD 1.73 billion by 2031 at 2.26% CAGR over 2026-2031. Measured growth is anchored in corridor‐focused public spending, a policy mix that aligns Eurasian Economic Union obligations with the Comprehensive and Enhanced Partnership Agreement (CEPA), and the country’s ambition to monetize its location between the Black Sea and the Persian Gulf. Rising transit volumes, particularly Russian cargo moving through the Georgia-Armenia axis, balance headwinds such as import-heavy trade flows, an aging truck fleet, and closed borders with Turkey and Azerbaijan that channel 85% of shipments through Georgian ports. Investments in the North-South Road Corridor, including EUR 236 million (USD 260.45 million) for the Sisian-Kajaran stretch, are shortening domestic haulage times and lifting service reliability. Meanwhile, a USD 37 million dry-port project in Shirak Province aims to process 4.7 million tons of cargo in its first year, signaling the state's intent to build an inland gateway for multimodal flows.

Key Report Takeaways

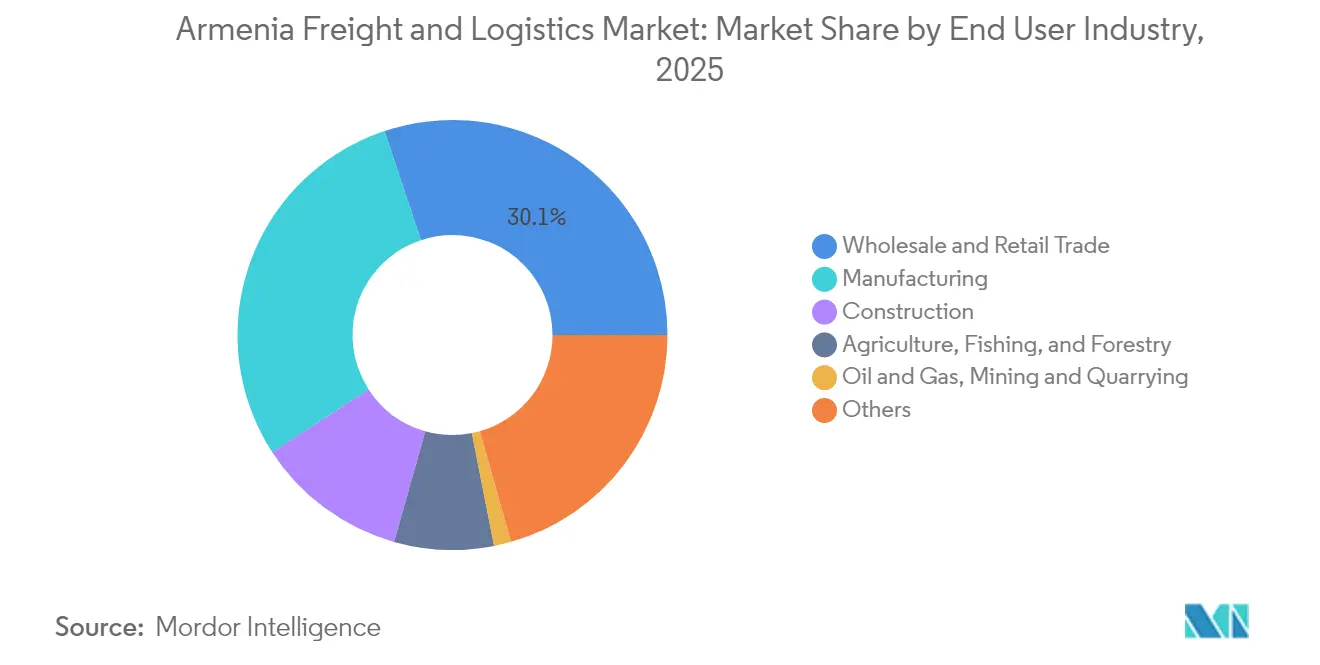

- By end user industry, wholesale and retail trade captured 30.12% revenue share in 2025, whereas manufacturing is poised to register the quickest 2.39% CAGR in the Armenia freight and logistics market size between 2026-2031.

- By logistics function, freight transport held 46.68% of the Armenia freight and logistics market share in 2025, while courier, express, and parcel (CEP) services are projected to log the fastest 2.61% CAGR between 2026-2031.

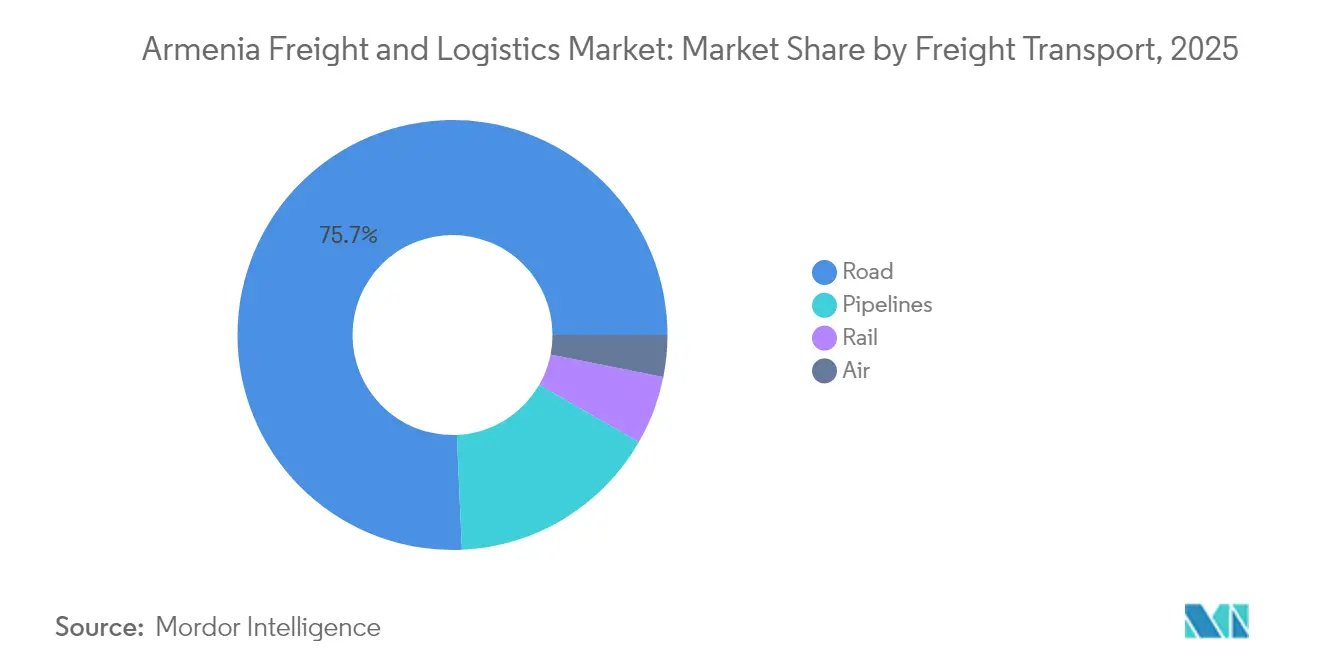

- By freight transport mode, road freight held a 75.70% revenue share in 2025; air freight is forecast to expand at the highest 2.50% CAGR between 2026-2031.

- By CEP, domestic deliveries commanded 76.34% of 2025 revenue, while international CEP is expected to advance at a 2.79% CAGR between 2026-2031.

- By warehousing and storage, non-temperature controlled held 81.55% share in 2025; temperature controlled storage is anticipated to grow at a 2.24% CAGR between 2026-2031.

- By freight forwarding mode, air freight forwarding dominated with 77.20% 2025 revenue share and is also projected to be the fastest-growing at a 2.81% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Armenia Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| North-South road corridor investment by government has unlocked transit potential | +0.5% | National | Long term (≥ 4 years) |

| Mining-sector capex surge creating oversize/project-cargo opportunities | +0.4% | Syunik and Lori provinces | Medium term (2-4 years) |

| Russian cargo, once diverted by war, now reroutes through Georgia-Armenia corridor | +0.3% | Border crossings with Georgia | Short term (≤ 2 years) |

| Returnees and the diaspora drive SME exports of high-value processed foods | +0.2% | Export-oriented regions | Medium term (2-4 years) |

| EU-Armenia CEPA standards raising demand for certified 3PL services | +0.2% | National | Medium term (2-4 years) |

| Digital trade facilitation platforms streamlining cross-border documentation | +0.1% | National, with focus on border crossings and customs zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mining-Sector Capex Surge Creating Oversize/Project-Cargo Opportunities

Metal mining generated 39.3% of export receipts and 5.4% of state revenue in 2024, with Zangezur Copper-Molybdenum Combine leading output[1]EITI Armenia, “Mining sector revenue contribution report 2024,” eiti.org . New exploration, such as Sagamar LLC’s 5,000 ha Chknagh-Armanis license, drives a flow of equipment consignments weighing hundreds of tons, forcing shippers to deploy multi-axle trailers and escort services. Specialized heavy-haul demand is emerging as a niche where operators with engineering know-how can capture high margins despite the broader industry’s fragmented fleet profile.

Russian Cargo, Once Diverted by War, Now Reroutes Through Georgia-Armenia Corridor

Transit volumes on the Middle Corridor climbed from 1.1 million tons in 2022 to 2 million tons in 2023[2]Caspian Policy Center, “Middle Corridor trade doubles amid war,” caspianpolicy.org . Container traffic expanded 33% over the same span, underscoring Armenia’s role as a buffer route between Russian suppliers and Gulf buyers. Operators gain volume but also shoulder geopolitical risk, as any flare-up in regional relations can quickly redirect flows elsewhere.

North-South Road Corridor Investment by Government has Unlocked Transit Potential

The Kajaran-Agarak leg broke ground in early 2024 and features 17 bridges, two tunnels, and five hubs built to European specifications. By tying Iran’s border to Georgia’s ports, the highway slices door-to-door transit times between Mumbai and Moscow from six weeks to three. Completed segments already register faster customs clearance and smoother axle weight enforcement, raising confidence among foreign forwarders.

Returnees and the Diaspora Drive SME Exports of High-Value Processed Foods

Programs such as iGorts channel diaspora skills and capital into agro-processing ventures that require cold chains and traceability. SMEs selling organic preserves and ready-to-eat specialties rely on temperature-controlled consignments and direct-to-consumer parcel flows targeting Armenian expatriate communities across North America and the EU.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land-locked geography and closed borders with Turkiye/Azerbaijan elevate transit times | -0.6% | National | Long term (≥ 4 years) |

| Import-heavy trade imbalances lead to high empty-backhaul ratios in Armenia | -0.3% | Return journeys from ports | Medium term (2-4 years) |

| Fragmented truck fleet (≥70 % pre-Euro 3) keeps operating costs high | -0.2% | National | Medium term (2-4 years) |

| Rigid EAEU customs procedures slowing digital freight documentation roll-out | -0.1% | Cross-border trade | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Land-Locked Geography and Closed Borders with Turkey/Azerbaijan Elevate Transit Times

Container rates from Far-East ports to Black Sea gateways stand at USD 4,100 per 40-ft box, a premium that filters into domestic retail prices. Dependence on a single Georgian corridor lengthens Europe-bound hauls by 2-3 days versus a hypothetical open Turkish frontier, while the shuttered Azerbaijan border blocks cost-effective Caspian crossings.

Import-Heavy Trade Imbalances Lead to High Empty-Backhaul Ratios in Armenia

Imports reached USD 16.80 billion against exports of USD 13.02 billion in 2024, pushing empty-backhaul rates beyond 40% on European lanes. Carriers recoup losses by raising outbound rates, a cycle that dents the price competitiveness of Armenian exporters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Wholesale Trade Leads Diversified Demand

Wholesale and retail trade retained a 30.12% revenue share in 2025 as Armenian distributors absorbed diverted Russian throughput, especially fast-moving consumer goods pivoted from Baltic ports. The Armenia freight and logistics market size derived from this vertical climbed to USD 0.46 billion in the base year, feeding continuous demand for palletized storage and groupage services. Retailers reward 3PLs that deliver 99.5% on-time warehouse receipts, nudging providers to adopt radio-frequency identification for case-level accuracy.

Manufacturing registers the fastest 2.39% CAGR between 2026-2031, aided by diaspora equity in processed foods and electronics sub-assemblies. Plant operators must satisfy CEPA traceability standards, stimulating certified third-party logistics contracts for temperature control, hazardous material handling, and bonded warehousing. Over the forecast horizon, processed food lines targeting the EU could push cold-chain lane utilization above 70%, unlocking scale economies despite Armenia’s relatively modest domestic demand.

By Logistics Function: Freight Transport Dominates Multi-Modal Operations

Freight Transport commanded 46.68% of the Armenia freight and logistics market share in 2025. Road freight transport contributed 75.70% of that value, leveraging 377 km of rebuilt Lori Province roads financed with USD 223 million between 2018-2023. Forwarders note that the modality’s flexibility offsets terrain constraints, yet the prevalence of pre-EURO 3 rigs drags average fleet age above 18 years. Rail retains a sub-8% tonnage slice, but niche minerals and bulk cereal flows keep the mode operationally relevant. Air freight’s 0.26% of load picked (tons) share belies its role in high-value electronics and pharmaceuticals, segments willing to pay USD 1.41 per ton-km versus USD 0.12 on road.

Courier, express, and parcel (CEP) services sit at the inflection of e-commerce and diaspora gifting. CEP services are expected to grow at 2.61% CAGR between 2026-2031, underpinned by same-day delivery coverage in Yerevan, Gyumri, and Vanadzor. Automated sorters and micro-fulfillment hubs shrink last-mile costs, while blockchain-anchored smart contracts reduce cash-on-delivery disputes. As international CEP accelerates, carriers are co-loading outbound parcels with high-yield air cargo to smooth space. Government incentives on customs pre-clearance for sub-USD 200 parcels further compress delivery windows to North American destinations.

By Courier, Express, and Parcel Destination: Domestic Growth Outpaces International

Domestic CEP deliveries are sustaining 76.34% market share in the segment in 2025. The e-commerce gross merchandise value (GMV) grew to USD 766.42 million in 2025 and will approach USD 1.08 billion by 2029, sharpening demand for same-day routing algorithms.

International CEP, while smaller, is on a 2.79% CAGR (2026-2031) trajectory as diaspora-linked gifting surges during religious and national holidays. Carriers mitigate Armenia’s landlocked limitations by consolidating Yerevan uplift into 3 weekly Narita-Tbilisi freighters, then trucking to Armenian delivery nodes within 12 hours.

By Warehousing and Storage Temperature Control: Non-Controlled Dominates Operations

Non-Temperature Controlled facilities represented 81.55% of the warehousing and storage segment during 2025 in the Armenia freight and logistics market. Unit economics are attractive, operating cost per m² averages USD 3.20 monthly, half the chilled-storage equivalent.

Yet, temperature-controlled is expected to expand at a 2.24% CAGR (2026-2031), catalyzed by EU-standard food lines and vaccine-grade pharma requiring +2°C to +8°C regimes. The Syunik Customs and Logistics Centre’s EUR 12 million (USD 13.24 million) financing includes modular cold stores sized for 12,000 pallet places, a pivotal benchmark for provincial infrastructure.

By Freight Transport Mode: Road Infrastructure Drives Modal Choice

Road freight undertakings accounted for 75.70% of the Armenia freight transport segment in 2025, moving high freight volumes over a 7,700 km network. The network’s interstate share sits at 1,400 km, with tolling studies under review to finance maintenance without inflating shipper costs. Planned truck weighing stations aim to cut overloading damage, a chronic issue that lifts per-kilometer depreciation.

Air freight, though a 0.26% sliver on load picked (tons), is slated for a 2.50% CAGR (2026-2031), propelled by Zvartnots International Airport’s 60-city connectivity and terminal expansion that lifts annual cargo capacity toward 40,000 tons. Consignments range from pharmaceuticals to IT components, lines where transit time beats price elasticity. Rail stabilizes at around 7.93% of the load picked (tons) share as Georgia-Black Sea bottlenecks limit competitive throughput. Should the discussed Armenia-Iran railway proceed, mineral exporters forecast a modal pivot that halves the distance to Persian Gulf ports.

By Freight Forwarding Mode: Air Services Command Premium Positioning

Air freight forwarding earned 77.20% of forwarding revenues in 2025, buoyed by electronics, precision machinery, and active pharmaceutical ingredients that tolerate freight rates above USD 7.50 per kg.

Air freight forwarding remained the fastest growing sub-segment as well, growing at a 2.81% CAGR between 2026-2031. Freight forwarders leverage the Digital Trade Corridor’s customs-pre-lodgment to shave documentation cycles to under four hours. Multimodal specialists focus on project cargo, orchestrating break-bulk deliveries of 120-ton mine crushers through Poti port, then onto hydraulic dollies across the mountainous Kapan road.

Geography Analysis

Armenia’s 257.6 km of roads per 1,000 km² yields functional domestic reach, yet only the Georgian and Iranian borders are open to trucks year-round, funneling 85% of external trade through Georgian ports. Modernization of the Friendship Bridge doubled axle capacity and provided an alternate passage when Georgian customs intensified checks on Russia-bound loads in 2024. The Armenia freight and logistics market, therefore, balances proximity advantages with political sensitivity, a duality visible every time a policy change in Tbilisi cascades into Yerevan rate sheets.

The North-South Road Corridor’s EUR 236 million (USD 260.45 million) Sisian-Kajaran tranche features gradient cuts and 1.5 km tunnels to secure year-round road availability, lowering accident risk, and freeing oversized carriers from seasonal daylight restrictions. The southern link to Iran’s Norduz crossing is increasingly strategic as discussions on an India-Iran-Armenia multimodal chain progress, potentially shortening Mumbai-Moscow voyages by three weeks.

Shirak Province’s dry port anchors a government plan to create 2,000 direct jobs and an ecosystem of customs brokers, insurers, and 3PLs. Once operational, the site aims to process 4.7 million tons annually. The facility’s rail spur links to the Gyumri-Vanadzor trunk line, offering an inland clearance option that circumvents Yerevan congestion.

Competitive Landscape

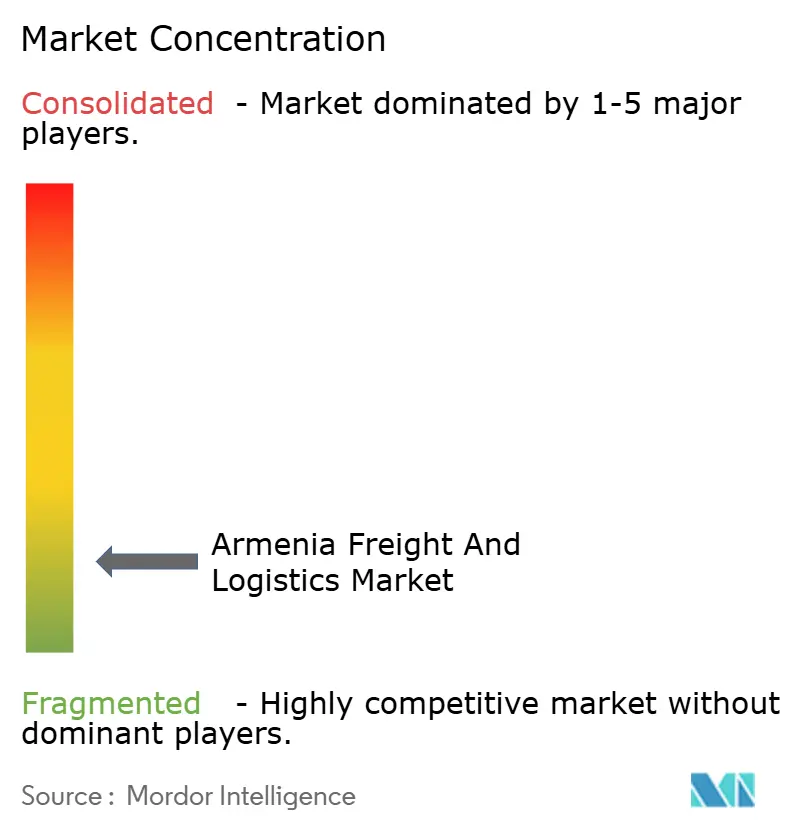

The Armenia freight and logistics market is highly fragmented, although DSV’s EUR 14.3 billion (USD 15.78 billion) acquisition of DB Schenker in April 2025 forged the largest global forwarder, able to pair Central European consolidation hubs with Armenia’s thin but rising volumes. The merged entity targets DKK 9 billion (USD 1.33 billion) in cost synergies by 2028, including uniform IT and shared procurement.

Local SMEs retain sub-regional edge through bilingual dispatchers and familiarity with mountainous lanes. However, requirements for ISO 22000 food-safety certification and TAPA-FSR Grade-A warehousing favor capital-rich international firms. Technology is the battleground: Gebrüder Weiss adopted a carrier-identity blockchain that neutralizes double-brokering, reducing fraud risk on Armenian inbound contracts.

White-space opportunities lie in cold chain, mining project cargo, and diasporic e-commerce fulfillment. CEVA’s USD 440 million purchase of Borusan Tedarik widens its Turkish footprint and may channel capacity toward Armenia once the Turkish border reopens. MSC’s standalone East/West network, operational from February 2025, reshapes feeder schedules into Batumi, influencing truck departure windows for Armenian shippers.

Armenia Freight And Logistics Industry Leaders

UNITRANS, Ltd.

DHL Group

Mira Trans

CMA CGM Group (Including CEVA Logistics)

The MSC Group (Including Mediterranean Shipping Company)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: CEVA Logistics agreed to acquire 100% of Borusan Tedarik for USD 440 million, adding 570,000 m² of warehousing that could reroute regional flows into Armenia.

- February 2025: MSC launched its standalone East/West network after the 2M dissolution, creating new feeder calls at Batumi that impact Armenian routings.

- June 2024: Gebrüder Weiss deployed the Carrier Identity™ platform to tighten truck-freight security across Caucasus lanes.

- May 2024: Publicis Sapient acquired Spinnaker SCA to bolster end-to-end supply-chain advisory services.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Armenia freight and logistics market as all revenue that firms earn inside the country from moving, storing, and value-adding to goods. This includes road, rail, air, pipeline, and multimodal freight transport together with freight forwarding, contract warehousing, courier-express-parcel services, customs brokerage, and ancillary logistics management. According to Mordor Intelligence, the market therefore captures the full commercial chain from pick-up to final hand-off, whatever the commodity or shipment size.

Scope exclusion: Passenger transport, fleet operations run purely in-house by manufacturers or retailers, and charges raised outside Armenian territory are not counted.

Segmentation Overview

- End User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining and Quarrying

- Wholesale and Retail Trade

- Others

- Logistics Function

- Courier, Express, and Parcel (CEP)

- By Destination Type

- Domestic

- International

- By Destination Type

- Freight Forwarding

- By Mode of Transport

- Air

- Others

- By Mode of Transport

- Freight Transport

- By Mode of Transport

- Air

- Pipelines

- Rail

- Road

- By Mode of Transport

- Warehousing and Storage

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Temperature Control

- Other Services

- Courier, Express, and Parcel (CEP)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview fleet owners, freight forwarders, warehouse operators, customs officers, and e-commerce shippers across Yerevan, Lori, and Syunik. These dialogues check rate movements, asset-turn ratios, and corridor bottlenecks, and they allow us to triangulate assumptions on average haul length, load factors, and contract pricing that public sources seldom reveal.

Desk Research

We gather foundational statistics from publicly accessible tier-1 sources such as the Statistical Committee of Armenia's freight volume tables, Eurasian Economic Union trade bulletins, UN Comtrade shipment codes, World Bank Logistics Performance Index indicators, and International Civil Aviation Organization cargo dashboards. Company filings, central-bank exchange records, and reputable press releases enrich trend lines, while paid databases, D&B Hoovers for operator financials and Dow Jones Factiva for deal flow, help validate firm-level benchmarks. Numerous additional secondary references supported gap-filling; the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down construct links national freight-ton-kilometers and import-export flows to an addressable revenue pool, which is then cross-checked through sampled average selling price times volume roll-ups from leading carriers and warehouse operators. Key variables like corridor spending on the North-South Road, fleet age mix (Euro 3 or older share), cross-border transit tonnage from Russia via Georgia, e-commerce parcel volumes, diesel price swings, and drayage turnaround times drive both the 2025 baseline and scenario testing. Forecasts through 2030 apply multivariate regression reinforced by ARIMA trend smoothing, with coefficients vetted by industry respondents; any opaque datapoint is replaced by a conservative proxy derived from three-point moving averages.

Data Validation & Update Cycle

Outputs pass automated variance checks against historical series and peer ratios, followed by a two-step analyst review. Material anomalies trigger re-contact of key informants. The model refreshes every twelve months, yet interim updates are issued when policy shifts or macro shocks alter freight demand.

Why Our Armenia Freight And Logistics Baseline Commands Reliability

Published estimates often diverge; definitions, input breadth, currency treatments, and refresh timing vary, so numbers seldom align.

Key gap drivers include whether warehousing and CEP are folded in, if transit earnings outside Armenia are added, and the vintage of exchange rates and GDP deflators applied before inflation adjustment. Mordor's disciplined scope, yearly refresh, and dual-path validation minimize such skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.51 B (2025) | Mordor Intelligence | - |

| USD 0.85 B (2024) | Regional Consultancy A | Omits warehousing and CEP; keeps 2022 exchange rate fixed |

| USD 2.14 B (2024) | Global Consultancy B | Adds foreign transit fees and passenger baggage handling revenue |

| USD 1.20 B (2025) | Trade Journal C | Uses tonnage x tariff proxy without invoice validation |

These contrasts show why decision-makers favor Mordor's balanced, transparent baseline: every figure ties back to clearly documented variables, repeatable steps, and a refresh cadence that keeps the view current.

Key Questions Answered in the Report

What is the current value of the Armenia freight and logistics market?

The Armenia freight and logistics market size stands at USD 1.54 billion in 2026 and is forecast to reach USD 1.73 billion by 2031.

Which logistics function generates the highest revenue?

Freight Transport is the largest logistics function, accounting for 46.68% of 2025 market revenue, with road freight transport making up three-quarters of that segment.

Which end-user industry is growing fastest?

Manufacturing leads growth at a 2.39% CAGR between 2026-2031 due to diaspora investment and CEPA-driven quality standards.

How does Armenia’s geography affect logistics costs?

Landlocked status and closed Turkish and Azerbaijani borders force 85% of cargo through Georgia, inflating haulage costs and lengthening transit times by up to three days.

What infrastructure project will most influence future transit flows?

The North-South Road Corridor, especially the Sisian-Kajaran and Kajaran-Agarak sections, is expected to cut domestic transit times and link Iranian and Georgian gateways, positioning Armenia as a viable segment of the International North-South Transport Corridor.

Which segment of warehousing and storage is expanding fastest?

Temperature Controlled storage is growing at a 2.24% CAGR (2026-2031), driven by higher-value food and pharmaceutical exports that require cold-chain integrity.

Page last updated on: