Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

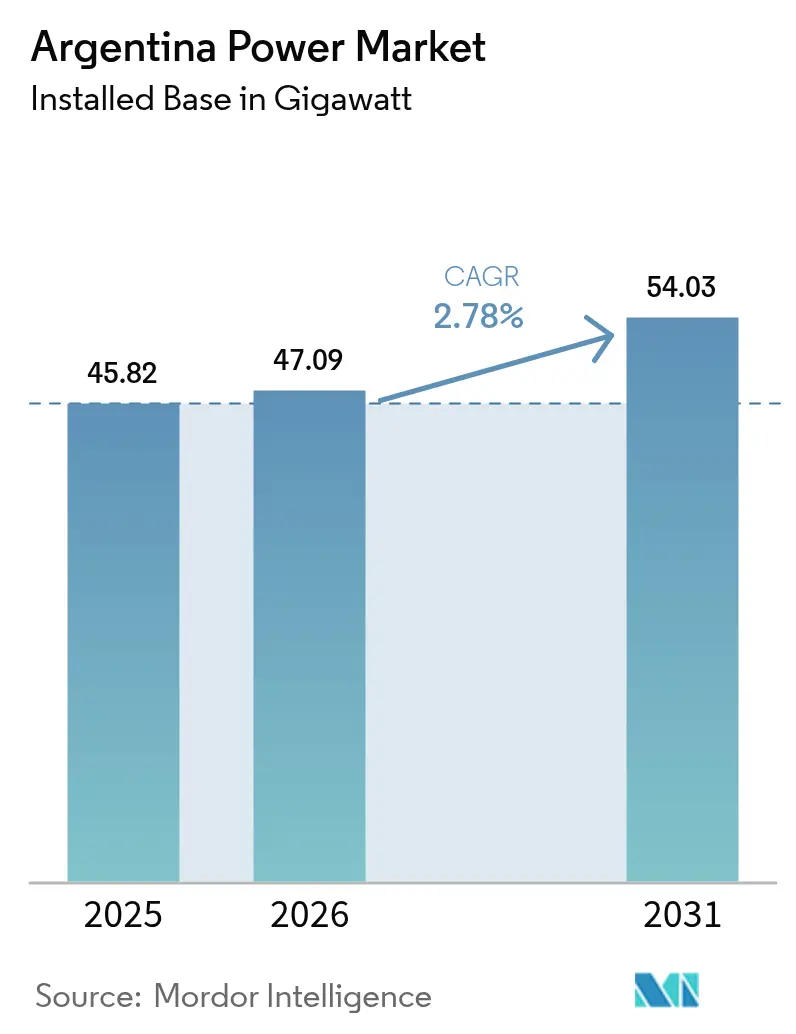

| Base Year Market Size (2025) | 45.82 gigawatt |

| Market Volume (2026) | 47.09 gigawatt |

| Market Volume (2031) | 54.03 gigawatt |

| Growth Rate (2026 - 2031) | 2.78% CAGR |

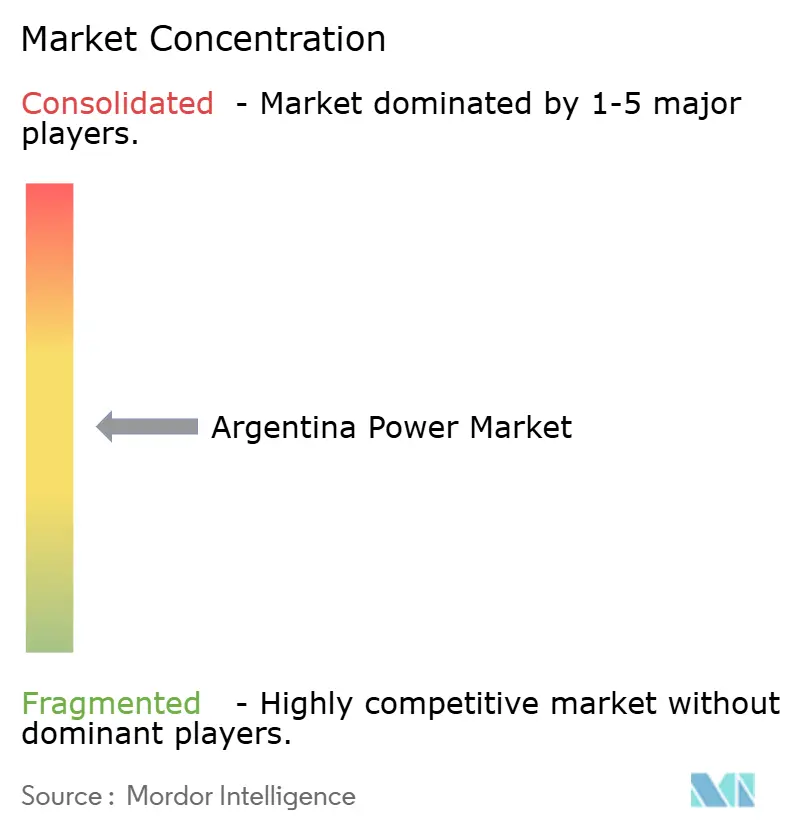

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Power Market Analysis by Mordor Intelligence

Argentina Power Market size in 2026 is estimated at 47.09 gigawatt, growing from 2025 value of 45.82 gigawatt with 2031 projections showing 54.03 gigawatt, growing at 2.78% CAGR over 2026-2031.

Argentina Power Market expansion is unfolding as President Javier Milei’s tariff reforms shift electricity pricing away from heavy subsidies, while abundant Vaca Muerta gas supplies, a 20% clean energy mandate for 2025, and USD 12 billion in multilateral grid-modernisation support converge to reshape investment flows. A sustained inflow of foreign capital, stricter local-content rules under the third Renovar auction, and growing corporate demand from mining and agro-industrial customers are accelerating renewable additions even as gas-fired plants remain the mainstay of baseload supply. Rising industrial activity in Buenos Aires and the lithium triangle lifts overall demand, yet hydropower drought risks, currency volatility, and transmission congestion still temper the outlook. Private developers are therefore pairing renewables with storage and distributed generation to manage curtailment risk and grid stress while investors pursue acquisition opportunities in a sector moving toward gradual consolidation.

Key Report Takeaways

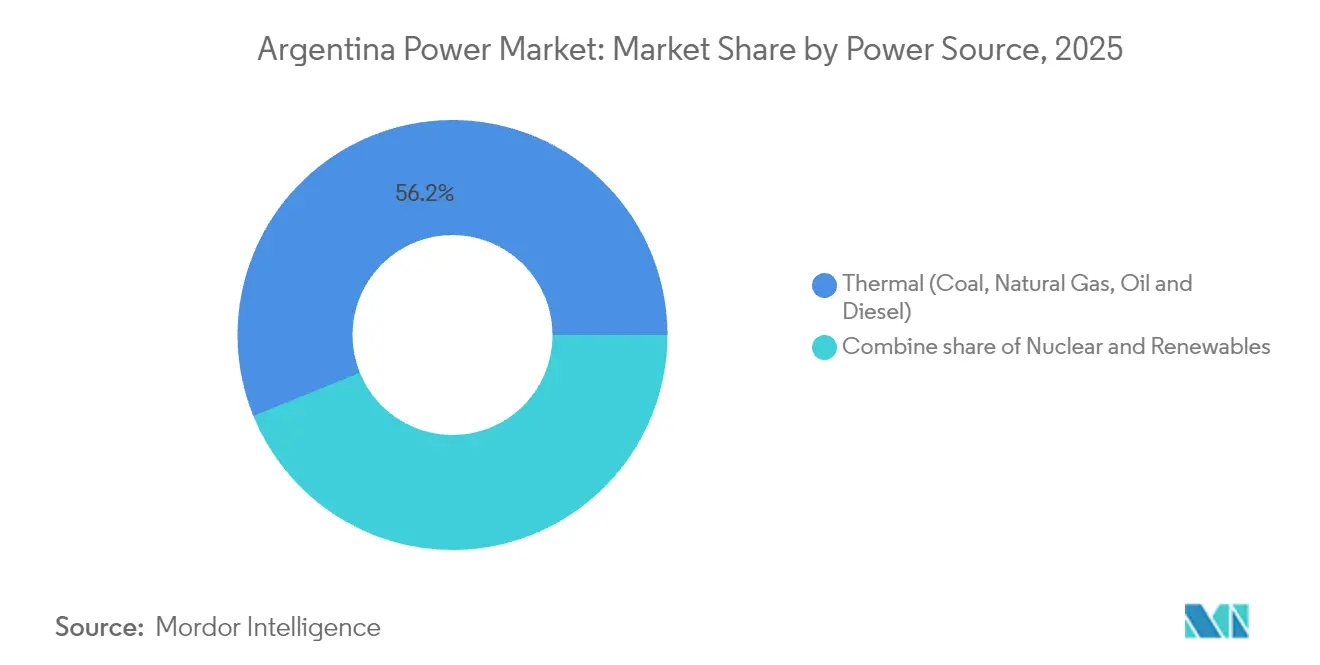

- By power source, thermal held 56.15% of the Argentine power market share in 2025; nuclear is forecast to expand at 10.4% CAGR through 2031.

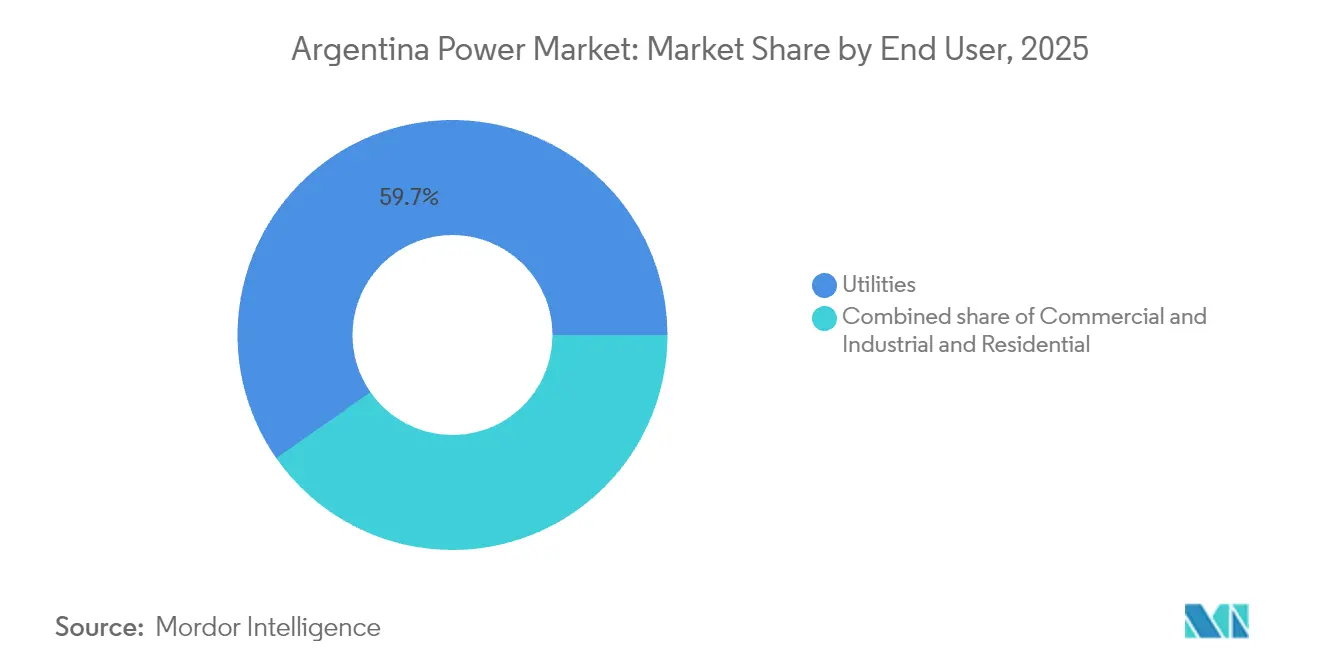

- By end-user type, the utilities segment accounted for 59.70% of the Argentine power market size in 2025, while the commercial and industrial segment is projected to advance at a 5.3% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Renovar auctions accelerating renewables | 0.80% | National, concentrated in Patagonia, Jujuy, Salta | Medium term (2-4 years) |

| Low-cost gas from Vaca Muerta basin improving plant load factors | 0.60% | National, strongest in Buenos Aires and Neuquén | Short term (≤ 2 years) |

| Multilateral-funded grid modernization projects | 0.40% | Priority corridors: Patagonia-Buenos Aires, Cuyo-Litoral | Long term (≥ 4 years) |

| Industrial rebound lifting electricity demand | 0.50% | Greater Buenos Aires, Córdoba, Santa Fe | Short term (≤ 2 years) |

| Behind-the-meter solar uptake in agro-industrial estates | 0.30% | Pampas, Mendoza, Tucumán | Medium term (2-4 years) |

| Mining-sector corporate PPAs in the Lithium Triangle | 0.40% | Jujuy, Salta, Catamarca | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government “Renovar” Auctions Accelerating Renewables

The third Renovar round targets 400 MW and continues a shift toward competitive tenders that delivered sub-USD 50/MWh solar tariffs.(1)Renewables Now, “Argentina Launches Renovar 3.0 Auction,” renewablesnow.comRecent 373 MW additions in 2024 and a projected 700 MW in 2025 underscore steady progress. Enhanced local-content rules, grid-integration protocols, and the RIGI incentive regime have already unlocked USD 11.8 billion in private bids. Genneia’s 90 MW solar plant and a USD 240 million wind investment illustrate the growing scale of domestic commitments, though success hinges on transmission upgrades backed by the World Bank’s USD 12 billion support package.

Low-Cost Gas from Vaca Muerta Basin Improving Plant Load Factors

Record production of 400,000 bpd in Q3 2024 and a 1 million bpd target for 2030 reposition Vaca Muerta as a cornerstone of Argentina's power market economics. The USD 2.5 billion Vaca Muerta Sur pipeline channels gas to demand hubs, reducing costly LNG imports and lifting thermal capacity factors. YPF's partnership with Eni on floating LNG ensures flexible volumes that can pivot to domestic generators during peak demand.(2)Offshore Magazine, “YPF and Eni Advance Argentina LNG,” offshore-mag.com Natural-gas output averaged 5 Bcf/d in September 2024, with Vaca Muerta contributing more than 70%.

Multilateral-Funded Grid Modernisation Projects

A USD 12 billion World Bank package and IFC’s USD 5.5 billion private-sector window target transmission, storage, and smart-grid upgrades. Central Puerto’s USD 600 million line to north-west mining sites demonstrates how concessional finance aligns with renewable growth and industrial demand. The 2024-2050 transmission plan prioritises high-voltage links and storage integration, directly addressing the curtailment challenges that have constrained Patagonia wind projects.

Industrial Rebound Lifting Electricity Demand

Manufacturing output recovered in 2024 as access to foreign currency improved, raising power demand in Buenos Aires, Córdoba, and Santa Fe. Lithium producers such as Ganfeng’s Mariana project in Salta installed a dedicated 28 MW plant to power an annual 20,000-ton lithium carbonate output. Petrochemical and steel players benefit from cheaper gas feedstocks, while corporate PPAs anchor long-term renewable offtake. Tariff normalisation, however, saw Buenos Aires rates rise 268% in 2024, prompting efficiency upgrades and on-site generation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic volatility and currency risk | -0.50% | Import-dependent projects nationwide | Short term (≤ 2 years) |

| Transmission congestion curtailing renewables | -0.40% | Patagonia-Buenos Aires, Cuyo-Litoral | Medium term (2-4 years) |

| Paraná-basin drought reducing hydro output | -0.30% | Litoral provinces, binational Yacyretá | Short term (≤ 2 years) |

| Community opposition to large Patagonia hydro projects | -0.20% | Santa Cruz province | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Macroeconomic Volatility & Currency Risk

The peso’s 50% December 2023 devaluation raised financing costs and squeezed project cash flows. A USD 2 billion payment backlog at system operator CAMMESA tightens liquidity, even with revised 60-day settlement terms. RIGI offers 30-year tax stability for projects above USD 200 million, yet import restrictions and exchange-rate gaps still push equipment costs 30% higher year on year. World Bank credit lines partly buffer currency risk, but developers remain exposed to further peso losses.

Transmission Congestion Curtailing Renewables

Patagonia wind farms and northern solar arrays often out-generate local demand, forcing curtailment when export capacity is full. The March 2025 heatwave left 620,000 Buenos Aires customers without power and highlighted grid fragility. Resolution 906/2023 creates a framework for battery energy storage to smooth dispatch, while the 2024-2050 plan schedules high-voltage links that would move surplus renewables to load centres.(3)Mercopress, “Heatwave Triggers Buenos Aires Blackout,” mercopress.com Implementation lags, however, keep curtailment a medium-term restraint.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Gas Anchors Today, Nuclear Bets on Tomorrow

Thermal assets dominated at 56.15% of installed capacity in 2025, confirming gas as the linchpin of present-day supply. This slice equates to 25.73 GW within the Argentina power market size, underpinned by Vaca Muerta feedstock that has displaced LNG imports. Nuclear contributes less than 4% now, yet is poised for a 10.4% CAGR, the fastest pace among all sources, driven by the 32 MW CAREM25 small modular reactor scheduled for 2027 and Chinese-backed life extensions at Atucha I and Embalse. Renewables are accelerating, yet the 15% curtailment of Patagonian wind in 2024 underscores integration hurdles.

Vaca Muerta economics continue to sustain combined-cycle repowerings, including Pampa Energía’s USD 350 million Genelba expansion slated for 2026. Solar capacity in Jujuy rose by 300 MW to serve lithium extraction, while hydro output dropped sharply amid drought, revealing the weather-dependency of legacy assets. The segmentation shows a dual narrative: thermal plants are being optimized for abundant domestic gas, whereas capital for long-life decarbonization is split between baseload nuclear and faster-to-build but grid-constrained renewables.

By End User: Utilities Still Rule, C&I Redraws Boundaries

Utilities retained a 59.70% footprint in the 2025 Argentina power market, equal to 27.35 GW of the Argentina power market size under CAMMESA’s centralized dispatch model. However, the C&I segment is forecast to grow 5.3% annually to 2031, riding on lithium-sector PPAs and agro-industrial solar that sidestep tariff risk. Mining companies alone signed offtake deals for 320 MW of clean capacity in 2024, insulating operations from peso volatility.

Subsidy rollbacks lifted residential tariffs by 300% in nominal terms during 2024, causing payment arrears and highlighting inequitable exposure to cost recovery. Developers favor creditworthy miners and exporters, leaving households to bear rising grid charges, a regulatory gap that could deepen social fissures. The Argentine power market demands updated cross-subsidy frameworks to balance self-generation benefits against communal system costs.

Geography Analysis

Regional dynamics strongly influence the Argentine power market. Buenos Aires and the surrounding provinces dominate consumption yet rely on distant resource hubs for supply. The March 2025 blackout, which affected 620,000 customers, underlined the need for stronger high-voltage links. Upgrading transmission will help move wind and solar from Patagonia and the north into this main load centre, reducing curtailment and improving resilience.

Patagonia hosts the country’s best wind regime, with capacity factors above 50%. Projects such as Verano Energy’s 200 MW solar array demonstrate rising solar interest as panel costs fall. Transmission, however, remains a bottleneck until the planned extra-high-voltage corridor is complete. The Argentina power market size for renewable projects in Patagonia is forecast to reach 9.65 GW by 2031, though timely grid expansion will determine actual realisation rates.

Northern provinces, Salta, Jujuy, and Catamarca, form the lithium triangle. Mining expansion translates into rapid power-demand growth. Ganfeng’s Mariana plant requires 28 MW of captive capacity, and Rio Tinto’s USD 2.5 billion project will need a similar supply once operational. Solar irradiation levels support competitive photovoltaic projects, while new transmission lines extend grid reach to remote sites. Hydropower potential, concentrated in the northeast, faces climate-driven variability, with the IEA projecting 15%-28% output declines by the end of the century.

Competitive Landscape

The Argentine power market features moderate fragmentation. The top four companies hold about 33% of installed capacity, creating room for new entrants and acquisitions. Foreign investors announced USD 8.9 billion across 99 deals in 2024, and energy accounted for 70% of the transaction value. Pampa Energía balances participation in the Vaca Muerta Sur pipeline with renewable additions, committing USD 1.5 billion to unconventional gas that feeds domestic generators.

Genneia leads private renewable deployment, commissioning 90 MW of solar and investing USD 240 million in wind. AES Argentina is expanding the Vientos Bonaerenses complex by 102.4 MW. Central Puerto leverages a USD 600 million IFC facility to build transmission that unlocks new demand nodes. Technology adoption focuses on battery storage and advanced controls required by Resolution 906/2023, aligning with domestic lithium availability.

Strategic alliances grow in importance. YPF and Eni are progressing toward an LNG final investment decision that would monetise surplus Vaca Muerta gas, while Wärtsilä secured a three-year operations agreement for a lithium-mine power plant in Salta. Distributed generation and corporate PPAs give industrial users direct procurement options, and mining firms increasingly develop captive systems, adding competitive pressure on traditional utilities.

Argentina Power Industry Leaders

Pampa Energia SA

AES Argentina Generación SA

YPF Luz

Enel SpA

Edenor SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: YPF and Eni have formalized agreements for an Argentina LNG project targeting a 12 million tons per annum (Mtpa) capacity, utilizing floating liquefied natural gas (FLNG) units. This project, named Argentina LNG (ARGLNG), aims to develop the Vaca Muerta shale gas resources for international markets.

- May 2025: Argentina has approved Rio Tinto's $2.5 billion lithium project under the RIGI (Large Investment Incentive Regime) framework. This is the first mining project to be approved under the RIGI program. The project, known as the Rincon lithium project, is located in Salta province.

- April 2025: The World Bank Group (WBG) has announced a USD 12 billion support package for Argentina, focused on reforms to attract private investment and boost job creation. As part of this, the International Finance Corporation (IFC) will invest up to USD 5.5 billion, including USD 2 billion within the first year, to support private sector development, with a specific focus on energy.

- March 2025: Genneia has inaugurated a 90 MW solar plant, Parque Solar Malargüe I, in Mendoza, Argentina, marking a significant step towards a cleaner energy transition and increased renewable energy capacity in the region.

Argentina Power Market Report Scope

Power is generated through various primary sources, including coal, hydro, solar, and thermal. In utilities, it's a step before its delivery to its end users. The process is then followed by Transmission and distribution. Under this, the power generated is distributed via high-voltage lines (transmission lines) and low-voltage lines (distribution lines) according to the end user's requirements.

The Argentina power market is segmented by Power Source (Thermal (Coal, Natural Gas, Oil and Diesel), Nuclear, Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal)), by End User (Utilities, Commercial and Industrial, Residential), by T&D Voltage Level (High-Voltage Transmission (Above 230 kV), Sub-Transmission (69 to 161 kV), Medium-Voltage Distribution (13.2 to 34.5 kV), Low-Voltage Distribution (Up to 1 kV)). Only qualitative analysis is provided for power transmission and distribution (T&D). For each segment, the market sizing and forecasts are based on installed capacity, except for power transmission and distribution (T&D), for which only qualitative analysis will be provided.

By Power Source

| Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) |

By End User

| Utilities |

| Commercial and Industrial |

| Residential |

By T&D Voltage Level (Qualitative Analysis only)

| High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) |

| Medium-Voltage Distribution (13.2 to 34.5 kV) |

| Low-Voltage Distribution (Up to 1 kV) |

| By Power Source | Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear | |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) | |

| By End User | Utilities |

| Commercial and Industrial | |

| Residential | |

| By T&D Voltage Level (Qualitative Analysis only) | High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) | |

| Medium-Voltage Distribution (13.2 to 34.5 kV) | |

| Low-Voltage Distribution (Up to 1 kV) |

Key Questions Answered in the Report

What is the forecast installed capacity for Argentina in 2031?

Installed capacity is expected to reach 54.03 GW by 2031, implying a 2.78% CAGR from the 2026 base.

Which segment is growing fastest within generation sources?

Nuclear is projected to expand at a 10.4% CAGR, the quickest growth rate among all generation types.

How large is the share of thermal generation today?

Thermal generation accounts for 56.15% of installed capacity, making it the dominant source in 2025.

Why are corporate PPAs significant in Argentina?

They give miners and industrial users tariff certainty and bypass peso volatility, accelerating dedicated renewable projects.

What is causing renewable curtailment in Patagonia?

A constrained 500-kV corridor limits transfers to Buenos Aires, curtailing about 15% of wind output until new lines arrive in 2027.

How is currency risk affecting new projects?

Peso depreciation and inflation inflate financing costs and have triggered force-majeure claims on several wind equipment contracts.

Page last updated on: