Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

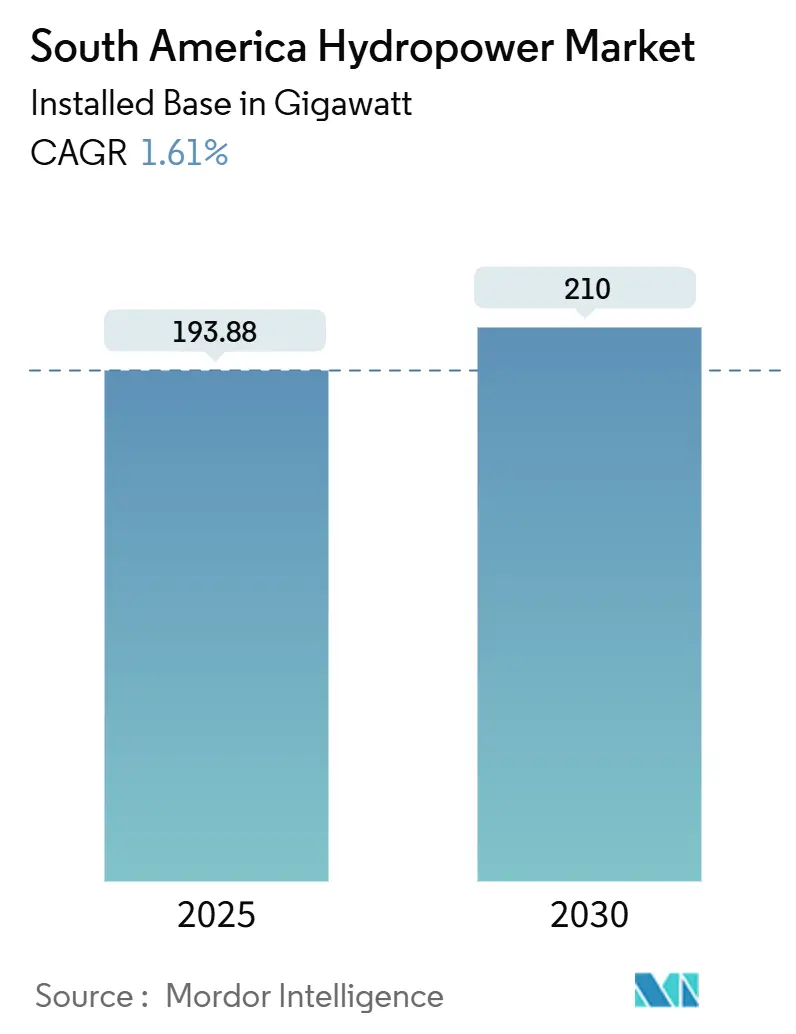

| Market Volume (2025) | 193.88 gigawatt |

| Market Volume (2030) | 210 gigawatt |

| Growth Rate (2025 - 2030) | 1.61% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Hydropower Market Analysis by Mordor Intelligence

The South America Hydropower Market size in terms of installed base is expected to grow from 193.88 gigawatt in 2025 to 210 gigawatt by 2030, at a CAGR of 1.61% during the forecast period (2025-2030).

This measured expansion reflects a regional pivot toward optimizing existing assets, tightening environmental licensing, and elevating climate-resilience standards. Hydropower continues to supply approximately 45% of Latin America’s electricity; however, operators now face volatile rainfall that has forced assets, such as Ecuador’s Coca Codo Sinclair, to curtail output for up to 14 hours a day. Policy makers respond with modernization budgets, corporate power-purchase agreements, and hybrid reservoir-plus-storage pilots that reinforce grid stability even when inflows weaken. Technology vendors are securing long-run overhaul contracts, and capital markets remain supportive of retrofit pipelines, providing a durable floor to investment despite subdued headline growth.

Key Report Takeaways

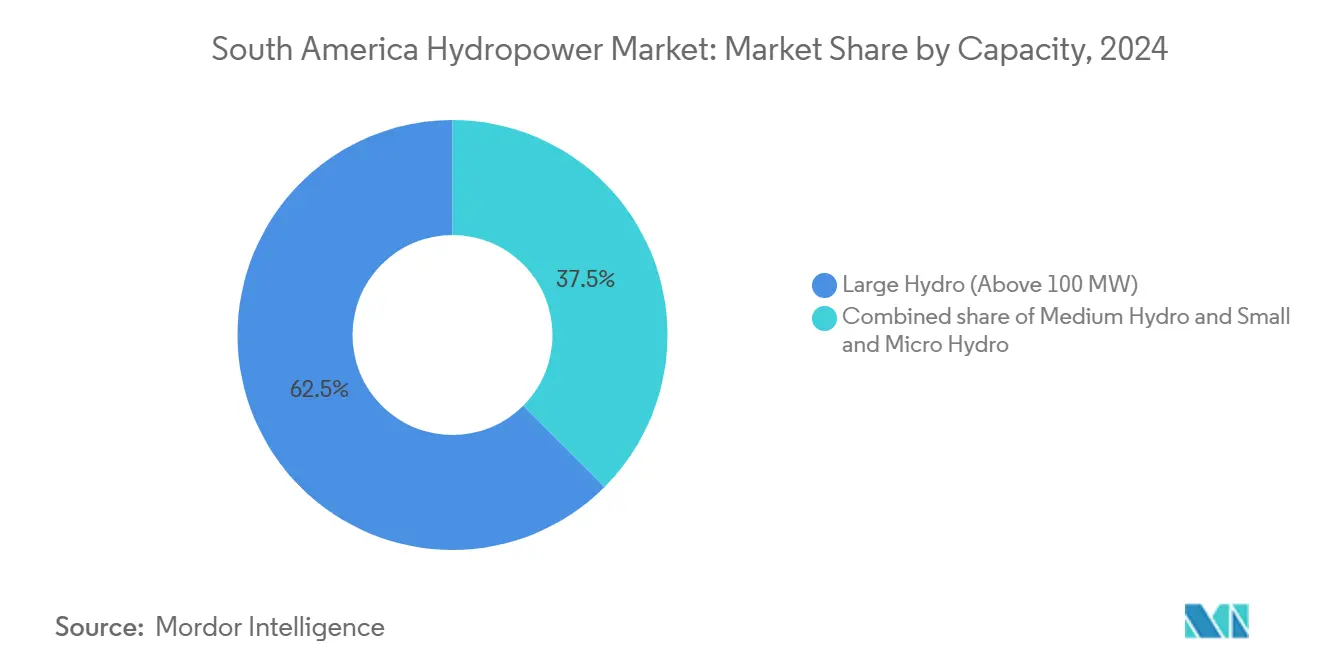

- By capacity, large hydro systems above 100 MW held 62.5% of South America's Hydropower market share in 2024, while small and micro hydro plants below 10 MW expanded fastest at a 5.7% CAGR to 2030.

- By technology, Reservoir-Based facilities captured 60.9% of the South American Hydropower market size in 2024; Pumped-Storage is forecast to grow at a 6.3% CAGR through 2030.

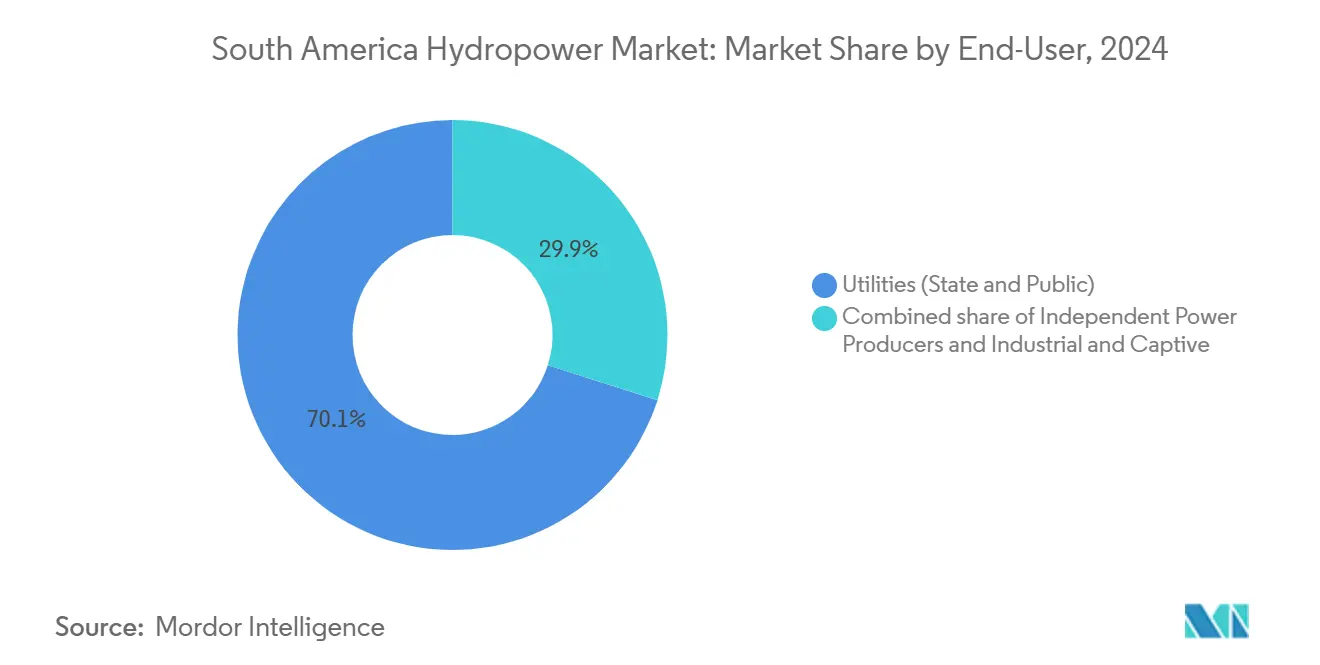

- By end-user, Utilities commanded a 70.1% share of the South American hydropower market size in 2024, whereas Independent Power Producers recorded the strongest 5.2% CAGR from 2024 to 2030.

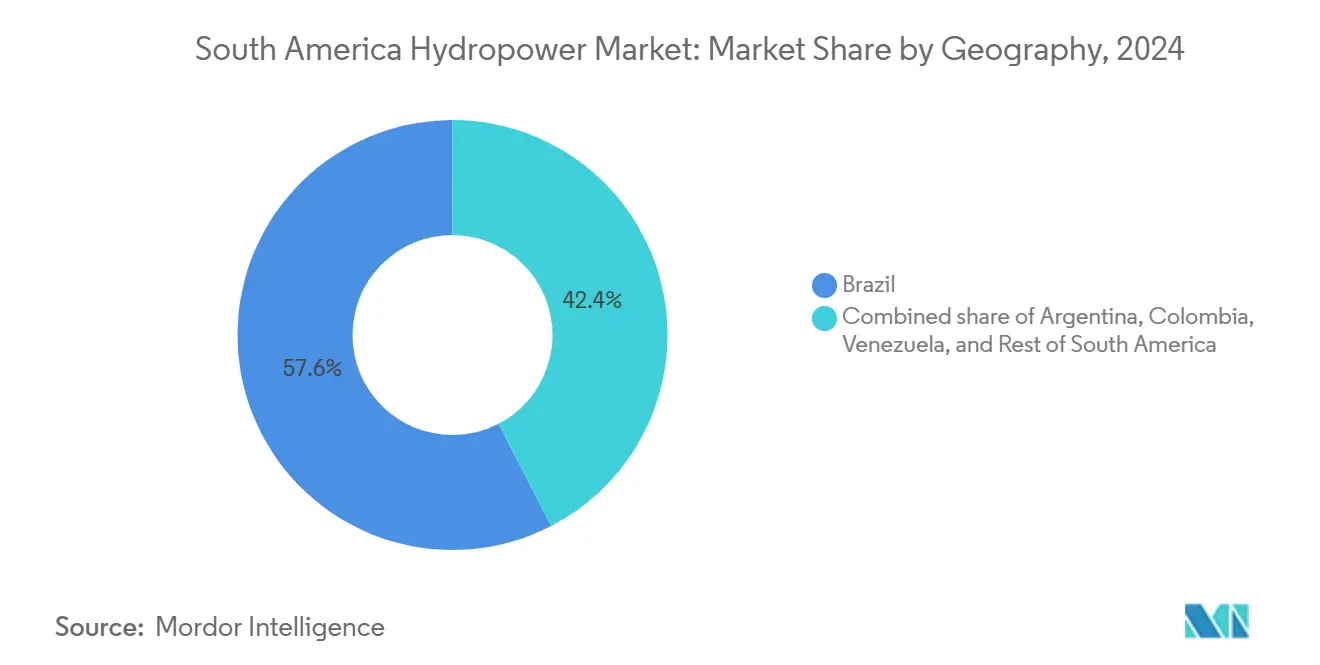

- By country, Brazil led the South American hydropower market with a 57.6% share in 2024; Colombia is projected to post the fastest growth rate of 5.5% between 2025 and 2030.

South America Hydropower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant untapped basin potential | +0.4% | Brazil, Colombia, Peru, Venezuela | Long term (≥ 4 years) |

| Regional decarbonization policies and renewable targets | +0.3% | Brazil, Colombia, Chile | Medium term (2-4 years) |

| Modernization and life-extension of aging dams | +0.5% | Brazil core; spillover to Argentina, Colombia | Short term (≤ 2 years) |

| Hybrid floating-PV retrofits on reservoirs | +0.2% | Brazil, Chile; pilots in Colombia | Medium term (2-4 years) |

| Merchant pumped-storage arbitrage projects | +0.1% | Chile, Brazil; interest in Colombia | Long term (≥ 4 years) |

| Mining and data-center corporate PPAs | +0.2% | Brazil, Chile, Peru; expansion to Colombia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Abundant Untapped Basin Potential

Brazil, Colombia, and Peru together harness less than one-third of their economic river potential, leaving material headroom for the South American hydropower market.[1]Inter-American Development Bank, “El sector hidroeléctrico en Latinoamérica,” iadb.org Brazil operates 475 certified small plants, yet still exploits only 30% of its viable hydro resource. Colombia lists 93,085 MW in theoretical capacity, but connects only a fraction of it to the grid. Updated basin mapping inside the Amazon now weighs the multi-use benefits, encouraging a phased build-out that moderates ecological impact while expanding dispatchable supply. The latent inventory, therefore, anchors long-term confidence, even though annual capacity additions remain subdued at the 1.61% CAGR headline rate for the South American Hydropower market.

Regional Decarbonisation Policies & RE Targets

Colombia’s National Development Plan aims for a 670% rise in non-hydro renewables by 2026, yet continues to rely heavily on large reservoirs as the primary balancing asset.[2]International Energy Agency, “Latin America Energy Outlook 2023,” iea.org Chile targets 80% renewable electricity by 2030 and carbon neutrality by mid-century, prompting tenders for pumped-storage projects that integrate with solar exports. Brazil’s PDE 2031 affirms the strategic weight of hydro but tightens social and biodiversity safeguards, steering investment toward upgrades rather than greenfield megaprojects. These aligned but measured policies lift investor confidence while reinforcing the considered pace embedded in the South American Hydropower market forecast.

Modernisation & Life-Extension of Ageing Dams

More than half of Brazil’s turbines entered service before the year 2000, resulting in efficiency losses of up to 10% due to cavitation and wear. Refurbishment contracts, such as GE Vernova’s nine-year São Simão overhaul, add 1,710 MW of upgraded capacity without requiring major civil works. Similar life-extension scopes across Peru and Colombia promise operating-life additions of 40-50 years at roughly half the per-kilowatt cost of a new dam. These economics underpin sustained outlays, even under capital discipline, lifting the South American hydropower market.

Hybrid Floating-PV Retrofits on Reservoirs

Covering just 3% of reservoir surfaces with floating solar can increase joint capacity factors by 10-15% while reducing water losses due to evaporation. Brazil’s Laranjeiras pilot confirms the design, enabling stored solar surplus to pump reserve water during low-flow months.[3]Vasco, Gabriel, Jones S. Silva, Fausto A. Canales, Alexandre Beluco, José de Souza, and Elton G. Rossini, "A Hydro PV Hybrid System for the Laranjeiras Dam (in Southern Brazil) Operating with Storage Capacity in the Water Reservoir," scirp.org Colombia is replicating small-scale trials, indicating a progressive rollout that aligns with mid-term grid-balancing needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E & S opposition and lengthy permitting | -0.3% | Brazil, Chile; spillover to Colombia, Peru | Medium term (2-4 years) |

| Hydrological variability and drought risk | -0.4% | Region-wide; acute in Ecuador, Chile, Brazil | Short term (≤ 2 years) |

| Water-use competition with agribusiness and navigation | -0.2% | Brazil, Argentina, Paraguay | Long term (≥ 4 years) |

| Sedimentation-driven turbine erosion | -0.1% | Andean states, Brazilian Amazon | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E&S Opposition and Lengthy Permitting

Indigenous consultation now stretches Brazilian licensing from 36 months to beyond five years, raising interest costs and triggering schedule risk. Litigation has delayed at least 2.3 GW of Chilean hydroelectric projects since 2017, citing water rights reform and local community consent.[4]Cambridge University Press, “Enforcing Citizen Participation,” cambridge.org Developers, therefore, prefer upgrades to existing concessions to sidestep greenfield approvals, restraining new capacity additions and tempering the growth rate of the South American hydropower market.

Hydrological Variability & Drought Risk

El Niño 2024-2025 reduced river inflows at Ecuador’s Coca Codo Sinclair plant, resulting in power cuts and highlighting the climate vulnerability of hydroelectricity. Low Paraná levels reduced output at the 14,000 MW Itaipu facility in 2023, and World Bank modeling warns that the frequency of multi-year droughts could double by mid-century. Adaptive reservoir management and hybridization now absorb capital once earmarked for expansion, holding the South America Hydropower market to a steady but cautious 1.61% CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Stability at the Large End, Acceleration in Small and Micro Systems

Large Hydro units above 100 MW accounted for 62.5% of the installed capacity and supplied the firm baseload that anchors the South American hydropower market size; yet, their annual growth is limited to legacy upgrades and incremental spillway efficiency gains. Small and Micro Hydroelectric Projects below 10 MW are expected to advance at a 5.7% CAGR to 2030, driven by distributed-generation tariffs, rural electrification needs, and lighter environmental footprints. Brazil’s small-plant pipeline aims for 6,500 MW by 2030, while Colombia couples Clean Development Mechanism finance with local co-ownership, improving social acceptance and locking in predictable feed-in revenue. The twin-track expansion preserves the baseline stability provided by mega-dams while injecting agile capacity at the grid edge, sustaining a balanced momentum for the South American hydropower market.

By Technology: Reservoir Dominance Meets Storage-Driven Innovation

Reservoir-based stations held 60.9% of total capacity in 2024 and remain essential for water management, flood control, and seasonal storage. Run-of-River units add low-impact energy but depend on rainfall, prompting grid planners to value pumped-storage at 6.3% CAGR as renewable penetration deepens. Chile’s coastal mounting of Espejo de Tarapacá leverages seawater topography, while Brazil studies reversible units near Rio de Janeiro load centers. Hybrid in-stream and micro-conduit devices fill irrigation channels and water supply pipes, weaving microgeneration into existing civil infrastructure. The diversified technology mix fortifies resilience and supports the broader South America Hydropower market.

By End-User: Public Ownership Persists Yet Liberalization Accelerates IPP Growth

Utilities controlled 70.1% of the capacity in 2024, reflecting national security priorities and historical public investment. However, Independent Power Producers are advancing at a 5.2% CAGR as governments relax retail tariff rules and corporations sign multi-decade renewable energy contracts. Brookfield’s 4 GW regional portfolio illustrates how global institutional capital is deployed at scale when long-term offtake certainty exists. Industrial and captive schemes remain niche but are growing in mining and agro-processing, where on-site hydroelectricity offsets volatile wholesale rates.

Geography Analysis

Brazil retained 57.6% of installed capacity in 2024 through 99,828 MW of dams spanning the Paraná, Madeira, and São Francisco basins.[5]U.S. Energy Information Administration, “Country Analysis Brief: Brazil,” eia.gov Market reforms since the 1990s have established clear paths for concession renewal and separate market operators, enabling private funding alongside state leadership. Yet deforestation in the Amazon headwaters threatens inflow stability, driving adaptation studies that blend conservation financing with energy planning.

Colombia leads the South American hydropower market in terms of fastest growth, at 5.5% CAGR, aided by clear long-term power-purchase frameworks and a 72% hydro share that supports low marginal emission factors. Brookfield manages 3,153 MW across eleven sites, backed by green-bond refinancing and digital asset monitoring. The Ituango project achieved Hydropower Sustainability Standard Silver certification in 2024, reflecting the government’s commitment to ESG benchmarks.

Argentina, Paraguay, and Chile round out the top tier. Argentina’s omnibus bill offers tax incentives for new hydroelectric projects, although macroeconomic volatility tempers near-term starts. Paraguay leverages Itaipu’s preferential tariff to fund rural electrification while renegotiating pricing formulas with Brazil. Chile balances run-of-river assets with pumped-storage to stabilize its solar-heavy grid and cover megadrought gaps, positioning itself as a test bed for merchant storage revenue. Smaller markets, including Peru, Ecuador, Bolivia, and Uruguay, pursue targeted upgrades, often linked to regional interconnectors that share reserve margins across borders.

Competitive Landscape

The South American hydropower market exhibits moderate concentration, with the top five operators accounting for just over 60% of the installed capacity. Eletrobras owns 42,559 MW and a 49.98% stake in Belo Monte’s 11,233 MW asset, underpinning its influence over dispatch even as it navigates a ‘BB-’ credit rating. Itaipu Binacional manages 14,000 MW and supplies 90% of Paraguay’s energy, making it indispensable to bilateral diplomacy and to Brazil’s reserve margin.[6]Itaipu Binacional, “Operational Statistics,” itaipu.gov.br

Brookfield Renewable operates 4 GW, split between Brazil and Colombia, with global green-bond raises exceeding USD 6 billion in 2024. ENGIE Brasil Energia acquired two mid-sized plants in March 2025, refreshing a portfolio that already integrates solar and wind with hydro to meet blended customer load.

Technology suppliers include GE Vernova, ANDRITZ, and VOITH. GE Vernova’s São Simão modernization spans nine years and upgrades 1,710 MW, embedding digital twins for predictive maintenance. ANDRITZ’s USD 892 million Mexican refurbishments underscore how Latin America’s hydro fleet attracts multi-cycle upgrade capital. Niche entrants offering floating-PV pontoons and sediment-control robotics target retrofit niches that multiply as owners extend dam lifetimes.

South America Hydropower Industry Leaders

-

Centrais Elétricas Brasileiras S.A.

-

Itaipu Binacional

-

ENGIE Brasil Energia SA

-

China Three Gorges Brasil Energia S.A.

-

Enel Américas

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ENGIE Brasil Energia acquired two hydropower plants, increasing its renewable base in Brazil’s core power pool.

- January 2025: GE Vernova won a nine-year contract with SPIC Brasil to modernize the 1,710 MW São Simão plant, enhancing turbine efficiency and digital monitoring capabilities.

- December 2024: ANDRITZ began refurbishing the Governador Parigot de Souza plant in Paraná, Brazil, replacing runners and governors to prolong asset life

- July 2024: Bitfarms secured two long-term hydro PPAs in Paraguay, channeling low-carbon power into cryptocurrency mining operations.

South America Hydropower Market Report Scope

The South America hydropower market report includes:

By Capacity

| Large Hydro (Above 100 MW) |

| Medium Hydro (10 to 100 MW) |

| Small and Micro Hydro (Below 10 MW) |

By Technology

| Reservoir-Based |

| Run-of-River |

| Pumped-Storage |

| In-Stream and Micro-conduit |

By Component (Qualitative Analysis only)

| Turbines |

| Generators |

| Control and Automation |

| Balance-of-Plant |

By End-User

| Utilities (State and Public) |

| Independent Power Producers |

| Industrial and Captive |

By Geography

| Brazil |

| Argentina |

| Colombia |

| Venezuela |

| Rest of South America |

| By Capacity | Large Hydro (Above 100 MW) |

| Medium Hydro (10 to 100 MW) | |

| Small and Micro Hydro (Below 10 MW) | |

| By Technology | Reservoir-Based |

| Run-of-River | |

| Pumped-Storage | |

| In-Stream and Micro-conduit | |

| By Component (Qualitative Analysis only) | Turbines |

| Generators | |

| Control and Automation | |

| Balance-of-Plant | |

| By End-User | Utilities (State and Public) |

| Independent Power Producers | |

| Industrial and Captive | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Venezuela | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America Hydropower market in 2025?

Installed capacity stands at 193.88 GW in 2025 and is projected to reach 210 GW by 2030 at a 1.61% CAGR.

Which country leads regional hydropower capacity?

Brazil holds 57.6% of capacity with 99,828 MW in 2024, anchored by Itaipu and Belo Monte.

What segment grows fastest through 2030?

Pumped-storage technology shows a 6.3% CAGR as grids seek flexible storage to back solar and wind.

How big is the independent power producer role?

Independent Power Producers grow at 5.2% CAGR as liberalized tariffs and corporate PPAs open market space.

What climate risks face the sector?

Drought linked to El Niño cut generation at key plants, and models predict more frequent multi-year dry spells, prompting adaptive reservoir management.

Who are the main technology suppliers for upgrades?

GE Vernova, ANDRITZ, and VOITH dominate refurbishment contracts, integrating digital twins and efficiency runners.

Page last updated on: