Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

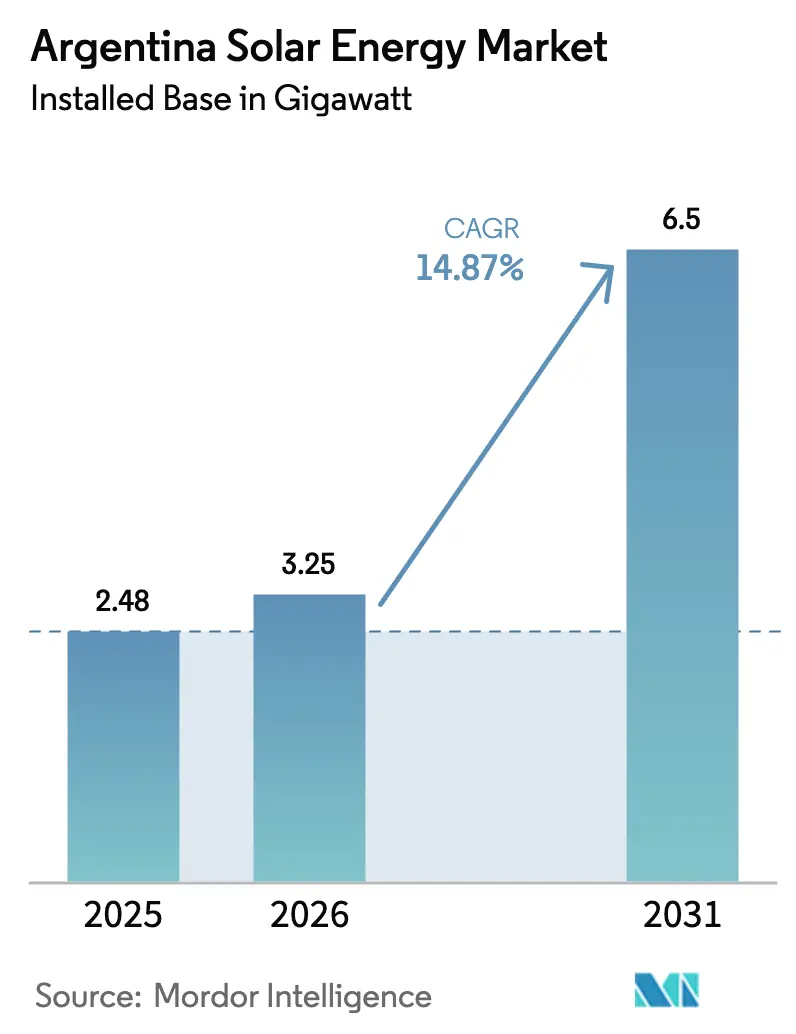

| Base Year Market Size (2025) | 2.48 gigawatt |

| Market Volume (2026) | 3.25 gigawatt |

| Market Volume (2031) | 6.5 gigawatt |

| Growth Rate (2026 - 2031) | 14.87% CAGR |

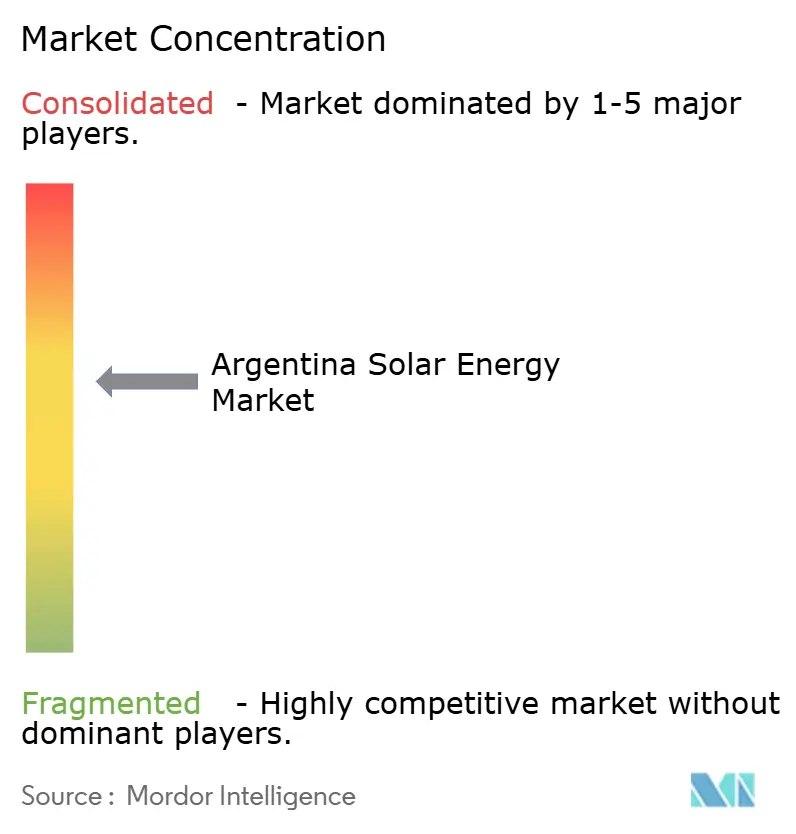

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Solar Energy Market Analysis by Mordor Intelligence

The Argentina Solar Energy Market size in terms of installed base is expected to grow from 2.48 gigawatt in 2025 to 3.25 gigawatt in 2026 and is forecast to reach 6.5 gigawatt by 2031 at 14.87% CAGR over 2026-2031.

Policy continuity under the RenovAr and MATER auctions is keeping the utility-scale pipeline bankable, while the Large Investment Incentive Regime (RIGI) approved its first solar project in 2024 and signals reliable fiscal treatment for ventures above USD 200 million. Transmission upgrades financed by CAF and the IDB will ease substation saturation in Jujuy, Salta, and Catamarca, unlocking curtailment-free capacity for the Argentine solar energy market. Long-term corporate power-purchase agreements (PPAs) signed by Telecom Argentina, Dow, and major lithium producers hedge currency risk and are accelerating commercial-and-industrial (C&I) adoption. Tracker and bifacial-module deployment continue to compress the levelized cost of energy (LCOE) and reinforce the competitiveness of photovoltaic technology within the Argentine solar energy market.

Key Report Takeaways

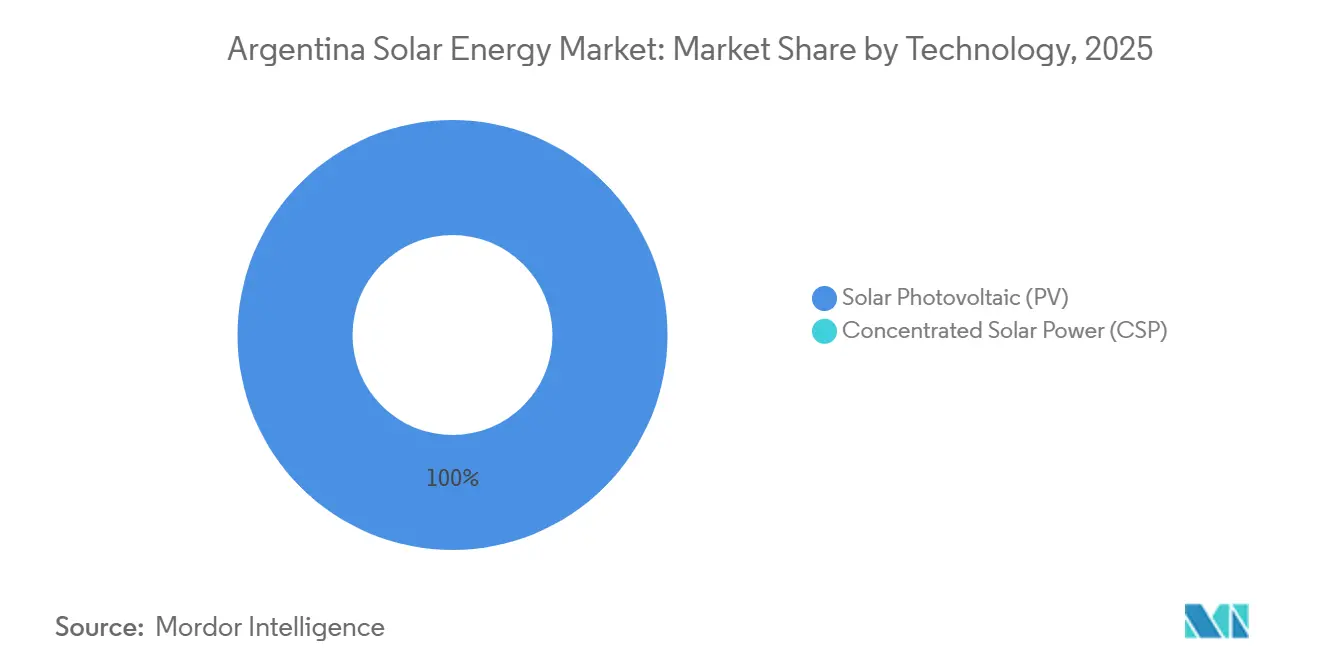

- By technology, solar photovoltaic held a 100% share of the Argentine solar energy market size in 2025 and is advancing at a 14.5% CAGR through 2031.

- By grid type, the on-grid segment led with 64.0% of the Argentine solar energy market share in 2025, while off-grid systems are projected to expand at a 17.8% CAGR to 2031.

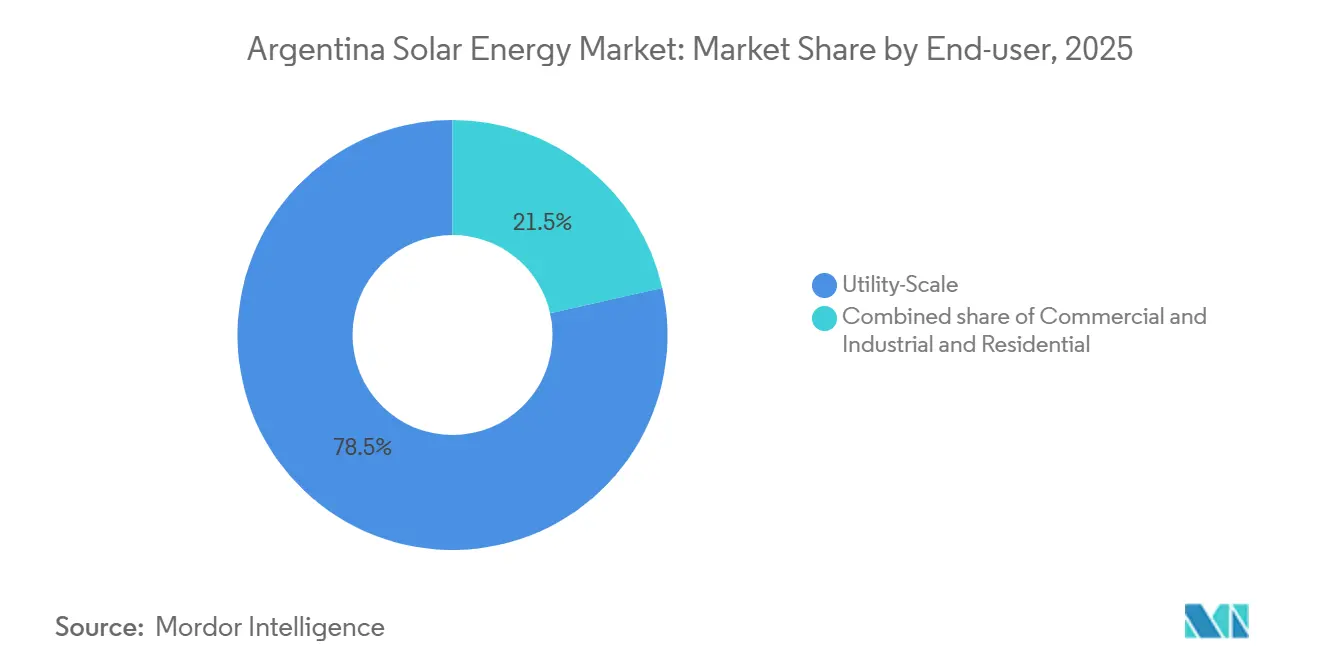

- By end-user, utility-scale plants commanded 78.5% of the Argentine solar energy market share in 2025; the C&I segment records the highest forecast growth at 19.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-energy auctions (RenovAr & MATER) continue to secure bankable PPAs | 2.8% | National, with concentration in Jujuy, Salta, San Juan, Mendoza | Long term (≥ 4 years) |

| Declining LCOE of utility-scale PV in high irradiation regions | 2.3% | Northwest (Jujuy, Salta, Catamarca) and Cuyo (San Juan, Mendoza) | Medium term (2-4 years) |

| Corporate PPA demand from mining & agro-exporters | 2.1% | Northwest lithium triangle; Buenos Aires agro-export hubs | Medium term (2-4 years) |

| Transmission-grid expansion financed by CAF & IDB | 1.9% | Northwest to Greater Buenos Aires corridor | Long term (≥ 4 years) |

| Green hydrogen roadmap spurring large hybrid PV projects | 2.5% | Coastal provinces (Buenos Aires, Río Negro, Chubut); Northwest for electrolyzer feedstock | Long term (≥ 4 years) |

| Peso-linked green-bond availability for C&I rooftop | 1.2% | Urban centers (Buenos Aires, Córdoba, Rosario, Mendoza) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

RenovAr and MATER Auctions Anchor Long-Term Pipeline Visibility

Argentina awarded more than 6.3 GW of renewables between 2016 and 2019, and 16 additional solar projects entered the Renper registry in 2025, confirming administrative continuity even without fresh auction rounds. CAMMESA reported 1.59 GW of online solar capacity by September 2024, a 25% year-on-year gain, underscoring project execution despite currency headwinds. The RIGI regime’s first solar approval, YPF Luz’s 305 MW El Quemado park, demonstrates how developers in the Argentine solar energy market can secure stable fiscal terms for multi-decade assets. Twenty-year, dollar-indexed PPAs backed by World Bank guarantees continue to de-risk utility projects and attract multilateral lending. Merchant and bilateral PPA routes are now supplementing rather than replacing auctions, creating parallel demand channels within the Argentine solar energy market.

Levelized Cost Compression Driven by Bifacial Modules and Trackers

Auction prices fell from USD 59–60/MWh in 2016 to well below USD 50/MWh on recent bids as bifacial modules and single-axis trackers spread across the Argentine solar energy market. YPF Luz’s El Quemado park installed 337,212 bifacial panels, raising energy yield by up to 15% compared with monofacial arrays. Tracker leader Trina delivered more than half of the systems deployed in 2024 and routinely offers peso-denominated contracts that shield developers from exchange-rate swings. Global module prices slipped to USD 0.08–0.10/W in 2024, partially offsetting Argentina’s 22% import tariff with solar irradiation around 2,200 kWh/m²/year in Jujuy and Salta, the Argentine solar energy market benefits from one of Latin America’s most competitive LCOEs, though financing constraints still widen the spread between wholesale supply costs and retail tariffs.

Corporate PPAs Hedge Currency and Tariff Risk

Telecom Argentina allocates roughly USD 14 million annually to three solar PPAs that cover 17.5% of its electricity needs, setting a template other corporates now emulate. Dow Argentina sources power from Atlas Renewable Energy’s 208 MW Casares park, showing how multinationals view the Argentine solar energy market as a hedge against subsidy reductions. Lithium miners Livent, Allkem, and Ganfeng sign site-specific PPAs to satisfy downstream ESG mandates and intensify demand for off-grid solar-plus-storage microgrids in the Puna plateau. Nearly all bilateral contracts are U.S.-dollar-indexed, shifting currency risk to investment-grade offtakers and improving bankability for foreign lenders. The rise of corporate PPAs, therefore, diversifies revenue streams inside the Argentine solar energy market.

Transmission Infrastructure Investment Unlocks Northwest Generation Capacity

Resolutions 715/2025 and 311/2025 mobilize multilateral loans to build 500 kV lines that will carry up to 2 GW from solar-rich Northwest provinces to the Buenos Aires load center, easing curtailment that hit plants during 2024 midday peaks.[1]Samuel Furfari, “Transmission upgrade projects gain IDB funding,” PV Tech, pv-tech.org CAF and IDB funding packages lower borrowing costs and fast-track environmental approvals, directly benefiting developers throughout the Argentine solar energy market. New grid capacity is synchronizing with Resolution 400/2025, which rewards projects that co-locate batteries by adding a firm-capacity payment on top of energy sales. Consequently, investors anticipate higher project revenues once transmission comes online around 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic volatility & FX restrictions on imported modules | -1.8% | National, with acute impact on import-dependent developers | Short term (≤ 2 years) |

| Saturation of existing substations in Northwest | -0.9% | Jujuy, Salta, Catamarca (Northwest provinces) | Medium term (2-4 years) |

| Limited local content manufacturing ecosystem | -0.7% | National, affecting supply-chain resilience | Medium term (2-4 years) |

| Community opposition in ecologically sensitive Puna plateau | -0.5% | High-altitude regions in Jujuy, Catamarca, Salta | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Macroeconomic Volatility and FX Restrictions Inflate Import Costs

Argentina’s peso lost 50% of its value in December 2023 and kept sliding through 2024, lifting the CIF cost of imported modules that already face a 22% tariff. Limited dollar availability forces developers to rely on parallel-market exchange rates or delay shipments, slowing the Argentine solar energy market.[2]Trade analyst note, “Argentina photovoltaic tariff structure,” U.S. International Trade Administration, trade.gov Reduced Chinese export rebates effective December 2024, and tighter global supply may drive further module price increases, amplifying capital-cost uncertainty.

Substation Saturation in Northwest Provinces Curtails Output

Jujuy, Salta, and Catamarca substations reached their nameplate limits during 2024 noon peaks, compelling CAMMESA to curtail solar dispatch and slash developer revenue. Although 500 kV projects are underway, lead times of three to five years postpone relief, keeping grid congestion a near-term cap on the Argentine solar energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar PV Extends Its Uncontested Lead

Solar photovoltaics contributed 100% of installed capacity in 2025, and the segment is forecast to rise at 14.5% per year through 2031, underpinning the growth of the Argentine solar energy market. Bifacial modules at El Quemado and Anchoris lifted performance ratios above 85% in 2025, illustrating how technology upgrades reinforce competitive economics.

The absence of concentrated solar power (CSP) reflects higher capex and the auction design’s lack of thermal-storage credits, steering developers toward PV-plus-battery hybrids that satisfy the new SRC Adicional category faster and at lower cost. Falling battery prices position lithium-ion storage as the preferred firming option for utility investors in the Argentine solar energy market.

By Grid Type: Off-Grid Solutions Accelerate in Mining Hubs

On-grid assets held 64.0% of capacity in 2025, yet off-grid systems are projected to climb 17.8% a year as lithium miners adopt 5-20 MW solar-diesel-battery microgrids beyond transmission reach. This dynamic diversifies the Argentina solar energy market size, reducing dependence on congested substations.

The PERMER rural electrification scheme, though modest, offers a template for community installations across Chaco and Formosa, while battery cost declines enhance the economic case for isolated agriculture and tourism lodges.

By End-User: C&I Uptake Surges on Currency-Hedged PPAs

Utility-scale plants captured 78.5% of the Argentine solar energy market share in 2025, but the C&I segment shows a 19.3% forward CAGR, fueled by telecom, chemical, and data-center PPAs that lock in stable dollar-indexed tariffs.[3]Newsroom, “Telecom Argentina inks solar PPA,” BNamericas, bnamericas.com High retail electricity prices after subsidy reductions speed paybacks for rooftop arrays in Buenos Aires and Córdoba, widening adoption among mid-sized enterprises.

Residential take-up remains low, under 10% of cumulative capacity, because long-tenor peso financing and consistent net-metering rules are still scarce across provinces, keeping households a small slice of the Argentine solar energy market.

Geography Analysis

Northwest provinces hosted about 850 MW by the end of 2025, anchored by the 312 MW Cauchari park, and continue to offer irradiation above 2,200 kWh/m²/year that underpins the Argentina solar energy market size in the region. Yet substation bottlenecks curtail output until the 500 kV corridor is completed around 2028.

Cuyo provinces accounted for roughly 565 MW, with YPF Luz, Genneia, and Atlas deploying multi-hundred-megawatt parks that enjoy shorter interconnection queues and closer proximity to Buenos Aires demand centers. The Argentine solar energy market, therefore, finds balanced growth opportunities across both the Northwest resource quality and the Cuyo grid headroom.

Buenos Aires province is emerging as a PPA-driven cluster where direct-wire arrangements minimize transmission losses and accelerate commissioning, while Patagonia’s solar role expands mainly through hybrid power for green-hydrogen export projects planned near Atlantic ports.[4]Ministry communiqué, “Green-hydrogen strategic roadmap,” Ministry of Foreign Affairs, cancilleria.gob.ar

Competitive Landscape

The Argentine solar energy market features moderately fragmented competition. Trina Solar’s tracker arm surpassed a 50% domestic share in 2024 by quoting peso-denominated contracts that buffer currency swings. Chinese module brands, Jinko, LONGi, and Canadian Solar, supply over 80% of panels despite import duties.

Genneia and YPF Luz have together commissioned more than 500 MW since 2024 and lead the developer class, while foreign IPPs such as Atlas Renewable Energy and Neoen leverage parent-company balance sheets to close dollar financing for large projects. Competitive positioning now hinges on the ability to integrate batteries and secure creditworthy C&I offtakers, a trend that will reshape value capture across the Argentine solar energy industry.

Argentina Solar Energy Industry Leaders

Genneia SA

360 Energy SA

YPF Luz

Canadian Solar Inc.

Trina Solar Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Argentine government released administrative documentation indicating progress on the proposed 20 MW Parque Solar Fotovoltaico Bandera I (Chaco), highlighting the continued expansion of Argentina’s solar energy capacity.

- January 2026: Genneia has inaugurated a 140 MW solar park in San Rafael, Mendoza. This project represents a substantial investment and is anticipated to achieve full production capacity by early 2026.

- September 2025: Aisa Group reported advancements on the Calicanto solar park (51 MW) in San Luis, which is anticipated to become operational by late 2026. This project is part of a broader USD 1.6 billion investment plan in renewable energy and other industries.

- February 2025: 360Energy Solar issued Green Bonds valued at up to USD 15 million to fund various solar projects in locations such as Colón, Arrecifes, Realicó, Palomar, and Córdoba.

Argentina Solar Energy Market Report Scope

Solar energy is heat and radiant light from the Sun that can be harnessed with technologies such as solar power (used to generate electricity) and solar thermal energy (used for applications such as water heating).

The Argentine solar energy market is segmented by technology, grid type, and end-user. By technology, the market is segmented into solar photovoltaic (PV) and concentrated solar power (CSP). By grid type, the market is segmented into on-grid and off-grid systems. By end-user, the market is segmented into utility-scale, commercial and industrial (C&I), and residential segments. For each segment, the market sizing and forecasts have been provided on the basis of installed capacity (gigawatts, GW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How fast is installed capacity expanding in the Argentina solar energy market?

Capacity rises from 3.25 GW in 2026 to 6.50 GW by 2031, implying a 14.87% CAGR.

Which segment grows quickest through 2031?

Commercial-and-industrial systems post a 19.3% CAGR as corporates lock in currency-hedged PPAs.

Where are most utility-scale solar parks located?

The Northwest and Cuyo regions host more than 1.4 GW, benefitting from irradiation above 2,200 kWh/m²/year.

What policy tools underpin long-term project bankability?

RenovAr and MATER auctions, plus RIGI fiscal incentives, supply 20-year PPAs and duty exemptions.

How big is the off-grid opportunity for mining firms?

Off-grid capacity grows 17.8% annually, with lithium operations installing 5-20 MW solar-battery microgrids.

Which suppliers dominate trackers and modules?

Trina Solar leads trackers with over 50% share, while Chinese brands provide 80%+ of shipped modules.

Page last updated on: