Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

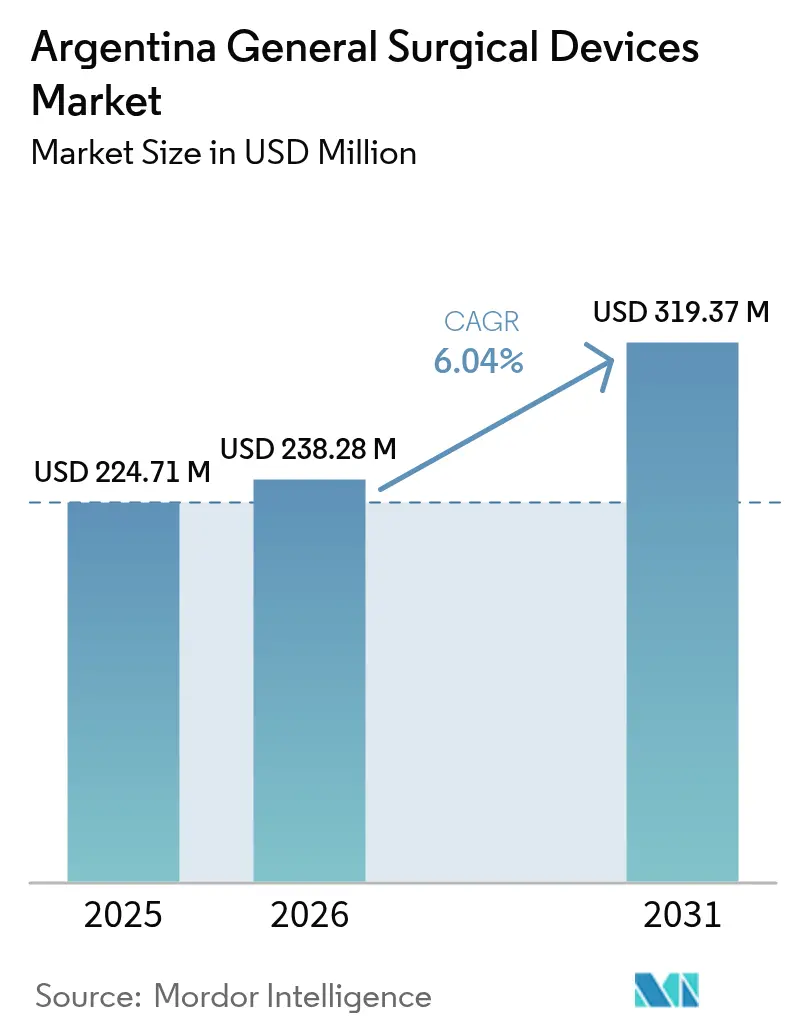

| Base Year Market Size (2025) | USD 224.71 Million |

| Market Size (2026) | USD 238.28 Million |

| Market Size (2031) | USD 319.37 Million |

| Growth Rate (2026 - 2031) | 6.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina General Surgical Devices Market Analysis by Mordor Intelligence

The Argentina General Surgical Devices Market size was valued at USD 224.71 million in 2025 and estimated to grow from USD 238.28 million in 2026 to reach USD 319.37 million by 2031, at a CAGR of 6.04% during the forecast period (2026-2031). Current expansion reflects resilient procedure volumes, faster import-payment cycles that now clear in 30–60 days, and renewed investment across metropolitan hospitals.[1]Source: U.S. Department of Commerce, “Argentina Import Payment Timeline Reduced,” trade.gov Demand is strongest where the backlog of elective surgeries converges with a nationwide pivot to minimally invasive techniques, encouraging steady procurement of laparoscopic towers, trocars, and advanced handheld instruments. Hospital groups are updating operating rooms to stay competitive in private insurance networks, while domestic production incentives offer tax advantages for basic surgical instruments. At the same time, currency swings and regulatory lead times temper purchase decisions, favoring suppliers that can guarantee reliable stocking plans and Spanish-language post-sale support. Competitive intensity remains moderate, with multinationals holding broad portfolios but ceding niche territory to regional distributors that navigate ANMAT’s documentation steps more nimbly.

Key Report Takeaways

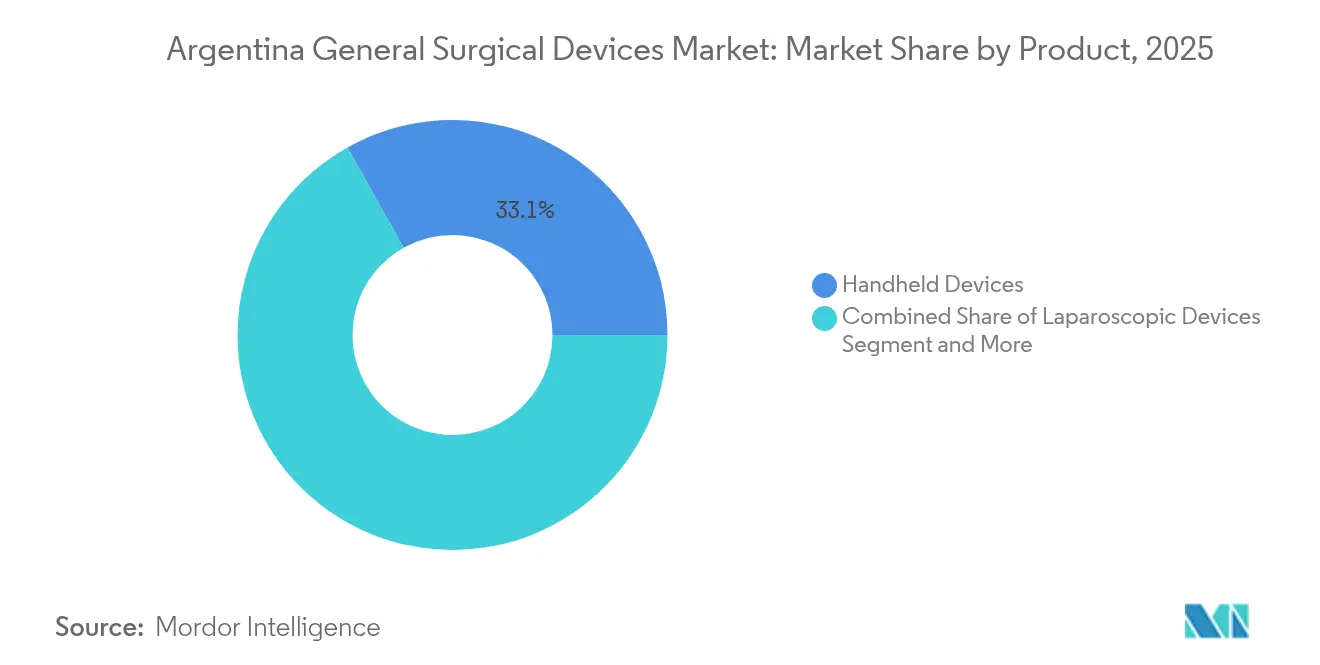

- By product type, handheld devices led with 33.12% of Argentina general surgical devices market share in 2025, whereas wound-closure devices are forecast to rise at a 6.92% CAGR to 2031.

- By procedure approach, minimally invasive surgery accounted for 70.05% share of the Argentina general surgical devices market size in 2025 and is advancing at a 7.18% CAGR through 2031.

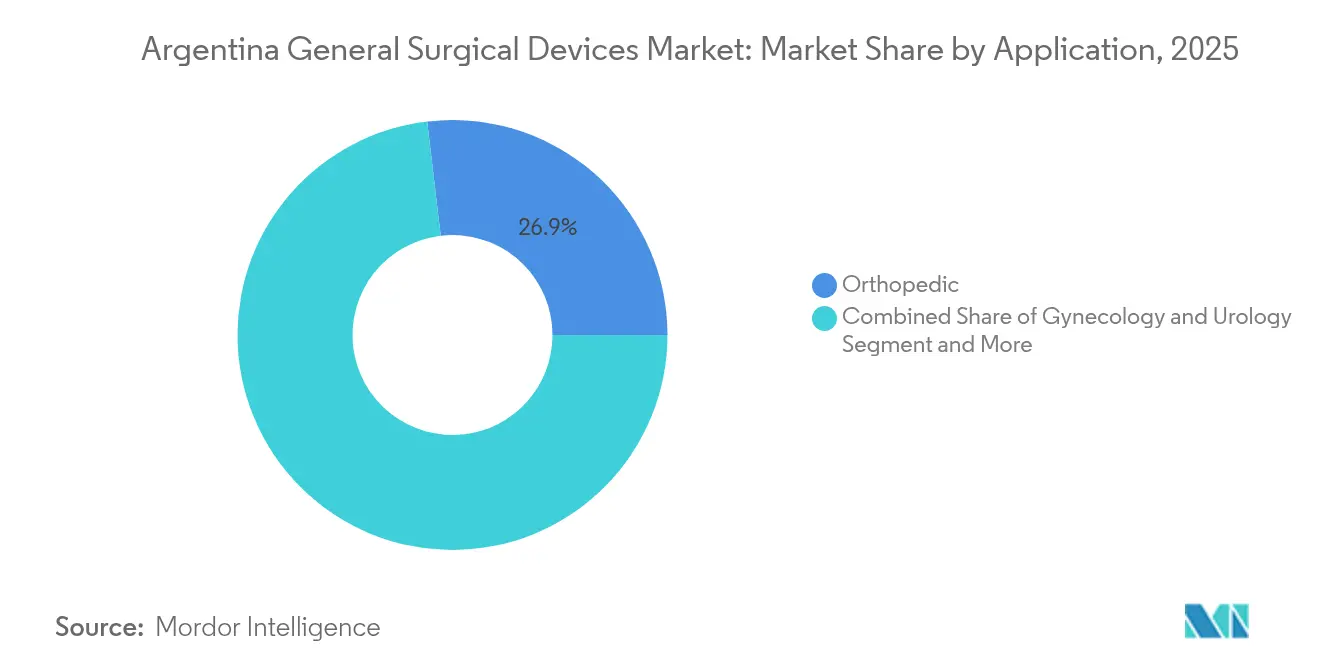

- By application, orthopedics captured 26.88% of Argentina's general surgical devices market share in 2025; gynecology and urology are projected to expand at a 7.45% CAGR to 2031.

- By end-user, hospitals held 71.60% revenue share in 2025, while ambulatory surgical centers registered the highest projected CAGR at 7.62% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina General Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand For Minimally-Invasive & Laparoscopic Surgery | +1.2% | National, with concentration in Buenos Aires, Córdoba, Santa Fe | Medium term (2-4 years) |

| Growing Incidence of Trauma & Orthopedic Injuries | +0.8% | National, with higher impact in urban centers | Long term (≥ 4 years) |

| Expanding Private Healthcare Infrastructure & Insurance Coverage | +1.0% | Buenos Aires Province, Córdoba, Mendoza | Medium term (2-4 years) |

| Post-Pandemic Elective-Surgery Backlog | +0.9% | National, with priority in metropolitan areas | Short term (≤ 2 years) |

| Domestic Production Incentives for Surgical Instruments | +0.6% | Buenos Aires Province, with spillover to Córdoba | Long term (≥ 4 years) |

| Surgeons' Shift to Reusable-Smart Handheld Devices | +0.7% | National, with early adoption in private hospitals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally Invasive & Laparoscopic Surgery

Multi-center studies in 24 Argentine hospitals confirmed that minimally invasive procedures lowered postoperative complications to 9%, compared with 11% for open surgery.[2]Source: Odetto D. et al., “Minimally invasive surgery versus laparotomy in women with high-risk endometrial cancer,” PubMed, ncbi.nlm.nih.gov Private institutions such as British Hospital Buenos Aires have added 10 dedicated theatres to amplify throughput, raising purchases of trocars and HD scopes. Early data from European use of the Hugo robotic system report median console times of 37 minutes, encouraging Argentine surgeons to explore similar platforms that shorten anesthesia cycles. Health-system administrators regard these outcomes as essential to free ward capacity during economic austerity, accelerating the Argentina general surgical devices market uptake of laparoscopic and robotic accessories. Suppliers with bundled training and dry-lab simulators gain an edge as hospitals address surgeon learning curves.

Growing Incidence of Trauma & Orthopedic Injuries

Argentina's orthopedic device market reflects broader Latin American trends, driven by aging demographics and increased musculoskeletal disorder prevalence. Zimmer Biomet earmarked USD 15.93 billion for next-generation joints and plates, signalling long-term confidence in high-growth trauma markets. Yet only three surgical robots currently serve 45 million Argentines, underlining room for advanced navigation systems that improve alignment accuracy in arthroplasty. Procurement teams in secondary cities champion handheld power tools and modular plating sets that tolerate varied OR conditions, sustaining momentum for the Argentina general surgical devices market even outside metropolitan hubs.

Expanding Private Healthcare Infrastructure & Insurance Coverage

Following the repeal of price controls, some private insurance premiums rose up to 150% in 2024. Providers now compete on technology differentiation, catalyzing bulk orders for energy-based devices and integrated OR lighting. The Buenos Aires Province strategic-investment regime offers 30-year tax holidays for projects above USD 5 million, spurring construction of ambulatory centers rich in minimally invasive capacity. Elevated capex supports the Argentina general surgical devices market as clinics shorten inpatient stays to lower insurers’ claims ratios.

Post-Pandemic Elective-Surgery Backlog

Brazilian queue-management pilots cut waiting lists from 98 days to 14 days and are informing Argentine scheduling reforms. Administrators favor instruments with robust service histories to avoid downtime during catch-up campaigns, prioritizing vendors that maintain local consignment stock. Redirected budgets toward high-throughput specialties such as cardiology and orthopedics have stabilized quarterly order flows for sternal saws, bone cements, and vascular staplers. Consequently, the Argentina general surgical devices market registers concentrated spikes that reward suppliers capable of short-lead-time fulfillment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent ANMAT Regulatory Pathway & Lengthy Registration | -0.8% | National, with administrative concentration in Buenos Aires | Long term (≥ 4 years) |

| Currency Volatility Impacting Import-Dependent Supply Chain | -1.1% | National, with higher impact on import-dependent regions | Short term (≤ 2 years) |

| Limited Reimbursement for Advanced Devices | -0.6% | National, with variations across provinces | Medium term (2-4 years) |

| Hospital Cap-Ex Freeze Amid Macro-Economic Instability | -0.9% | National, with concentration in public sector facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent ANMAT Regulatory Pathway & Lengthy Registration

Class IV devices can spend 12–15 months in approval, incurring fees up to USD 510 and compelling foreign manufacturers to appoint Argentine Authorized Representatives.[3]Source: Artixio Consulting, “Medical Device Regulations in Argentina,” artixio.com Even with EU or FDA clearance, firms must add Spanish labeling and proof of local post-market systems, delaying market entry and extending inventory-holding costs. For the Argentina general surgical devices market, this barrier means slower refresh cycles for innovative staplers, energy platforms, and navigation software.

Currency Volatility Impacting Import-Dependent Supply Chain

Roughly 80% of surgical devices are imported, exposing buyer budgets to peso swings despite recent easing of import-payment rules. The World Bank cites cyclical fiscal policy as a drain on private-sector planning confidence, limiting the horizon for long-term supply agreements. Distributors hedge through higher inventory cover, elevating storage costs and unit prices, which slows adoption of premium instrumentation in the Argentina general surgical devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Handheld Devices Remain Foundational

Handheld instruments generated 33.12% revenue in 2025, validating their position as OR staples across specialties. Hospitals favor reusable stainless-steel sets that withstand repeated sterilization, while surgeons increasingly request sensor-enabled forceps that log perfusion pressure for audit trails. Wound-closure systems are projected to post a 6.92% CAGR through 2031, reflecting the rise of barbed sutures and absorbable adhesive films that align with enhanced-recovery protocols.

Meanwhile, electrosurgical generators receive steady upgrades as facilities comply with stricter insulation-failure standards issued by international bodies. The Argentina general surgical devices market size for hand-held and closure categories is set to expand, mirroring the systems’ centrality to every OR list. Robotic and computer-assisted units still form the smallest slice, yet hospitals signal intent to triple installations by 2030, which would lift the Argentina general surgical devices market size for navigation and robotic accessories at a double-digit pace.

By Procedure Approach: Minimally Invasive is Transformative

Minimally invasive surgery (MIS) controlled 70.05% revenue in 2025 and will grow at 7.18% through 2031 as residency curricula embed laparoscopy modules. Hospitals emphasize shorter length-of-stay metrics, reinforcing the switch to small-incision techniques that rely on optical trocars, insufflators, and articulating clip appliers.

The Argentina general surgical devices market benefits from MIS’s pull-through effect on high-margin imaging towers and disposable smoke evacuation filters. Government academic hospitals in Córdoba and Santa Fe have partnered with equipment suppliers to co-share training labs, further accelerating penetration. Regional variations in minimally invasive surgery adoption reflect infrastructure disparities, with private hospitals and metropolitan centers leading implementation while rural facilities maintain traditional open surgery capabilities.

By Application: Orthopedic Volume Leads, Gynecology Accelerates

Orthopedic represented 26.88% of revenue in 2025 as fracture plates, nails, and joint prostheses support a growing elderly demographic. Elective arthroplasty is now rescheduled at near-pre-pandemic levels, intensifying demand for cement mixers and disposable pulse lavage. Gynecology and urology, although smaller in baseline volume, are forecast at a 7.45% CAGR, propelled by broader screening and outpatient hysteroscopy adoption.

Cardiology and cardiothoracic instruments see modest single-digit gains, aided by hybrid theatres that combine open and percutaneous workflows. Neurology and spine retain a niche but valuable share, with advanced microscopes and ultrasonic aspirators feeding replacement cycles. In each sub-segment, clinicians compare device wear performance against currency-inflated prices, shaping procurement decisions across the Argentina general surgical devices industry. The geographic concentration of specialized applications in metropolitan areas creates distinct market dynamics, with rural regions relying on general surgery capabilities and mobile surgical units for specialized care access.

By End-User: Hospitals Dominate but Ambulatory Centers Surge

Hospitals accounted for 71.60% sales in 2025, stocking comprehensive kits for multidisciplinary rosters. New guidelines that link reimbursement to infection-control indicators push administrators to replace aging power instruments ahead of schedule. Ambulatory surgical centers (ASCs) expand at an 7.62% CAGR, tailoring device sets to outpatient workflows. Procurement officers in ASCs prefer compact electrosurgical units and fully disposable trocar packs to streamline turnover.

Specialty clinics round out demand through focused device lists such as ENT microdebriders and ophthalmic phaco tips. As ASCs widen their procedural mix, suppliers must repurpose product education for non-hospital teams, renewing growth impetus across the Argentina general surgical devices market. The end-user landscape evolution toward distributed care delivery creates opportunities for portable, versatile surgical devices that function effectively across diverse settings while maintaining clinical performance standards.

Geography Analysis

Buenos Aires hosts nearly 40% of the population and concentrates premium private hospitals that anchor the Argentina general surgical devices market. Provincial incentives granting 30-year tax stability for healthcare projects above USD 5 million have already attracted upgrades in the north of Greater Buenos Aires. Córdoba and Santa Fe follow as secondary clusters, each anchored by teaching hospitals that pilot new laparoscopic platforms before diffusion to regional sites.

Northern provinces struggle with fewer anesthetists per capita, prompting outreach missions equipped with portable battery-operated drills and compact suction units. Patagonia’s wide geography and harsh winters test logistics, so rural ORs choose multi-application energy devices to cut stocking complexity.

Public hospitals in Mendoza rely heavily on import-payment grace periods to finalize orders, a dependency that exposes them to currency corrections. These regional contrasts drive manufacturers to craft tiered product portfolios, distributing advanced robotic consumables in urban centers while marketing durable handheld sets to remote clinics. Consequently, suppliers that adopt multi-channel distribution harness the full geographic potential of the Argentina general surgical devices market.

Regulatory Landscape

Argentina regulates general surgical devices through ANMAT (Administracion Nacional de Medicamentos, Alimentos y Tecnologia Medica), which oversees registration, vigilance, and compliance for products used in human medicine, including risk-based device classes (I to IV). Market access typically requires a local establishment habilitation and a registered local representative or importer, with digital workflows used to manage establishment and product submissions; the practical impact is most visible for import-heavy categories such as laparoscopic disposables, electrosurgical accessories, and wound-closure products.

Between 2025 and 2026, ANMAT introduced multiple measures aimed at reducing administrative friction for lower-risk categories and clarifying import conditions. Disposicion 4446/2025 (effective August 6, 2025) moved Class I and II medical product imports for registered importers away from transaction-by-transaction authorization toward online sworn-statement notifications. Disposicion 8799/2025 introduced a simplified sworn-declaration approach for habilitation of Class I and II device establishments. In 2026, Disposicion 224/2026 (effective February 2, 2026) established a formal framework for importing used and refurbished medical devices, tightening traceability and compliance expectations for secondary-market equipment entering hospitals and clinics.

Value Chain Analysis

The value chain in Argentina general surgical devices is anchored in imports (roughly 70% to 80% of supply), with multinational manufacturers supplying finished devices and consumables that move through local, ANMAT-registered importers and specialized distributors into hospitals, ambulatory surgical centers, and specialty clinics. Distribution and service capabilities are central to winning tenders and supporting recurring orders, particularly for instrument sets, electrosurgical platforms, and minimally invasive surgery accessories that require training, maintenance, and reliable replenishment.

Upstream logistics and compliance are shaped by ANMAT processes and the need for local establishment habilitation and import management, while downstream demand is concentrated in metropolitan hospital groups and expanding outpatient centers. The supply chain includes local importers and technical distributors such as Medix Medical Devices, MTG Group, Argentina Medical Products S.R.L, and TESIS SRL, which represent international brands and manage stocking, field service, and documentation. Recent ANMAT reforms, including the August 2025 import simplification for Class I and II products and the February 2026 framework for used or refurbished device imports, have shifted value-chain emphasis toward faster documentation cycles, inventory planning, and stronger post-market controls rather than repeated pre-shipment authorizations.

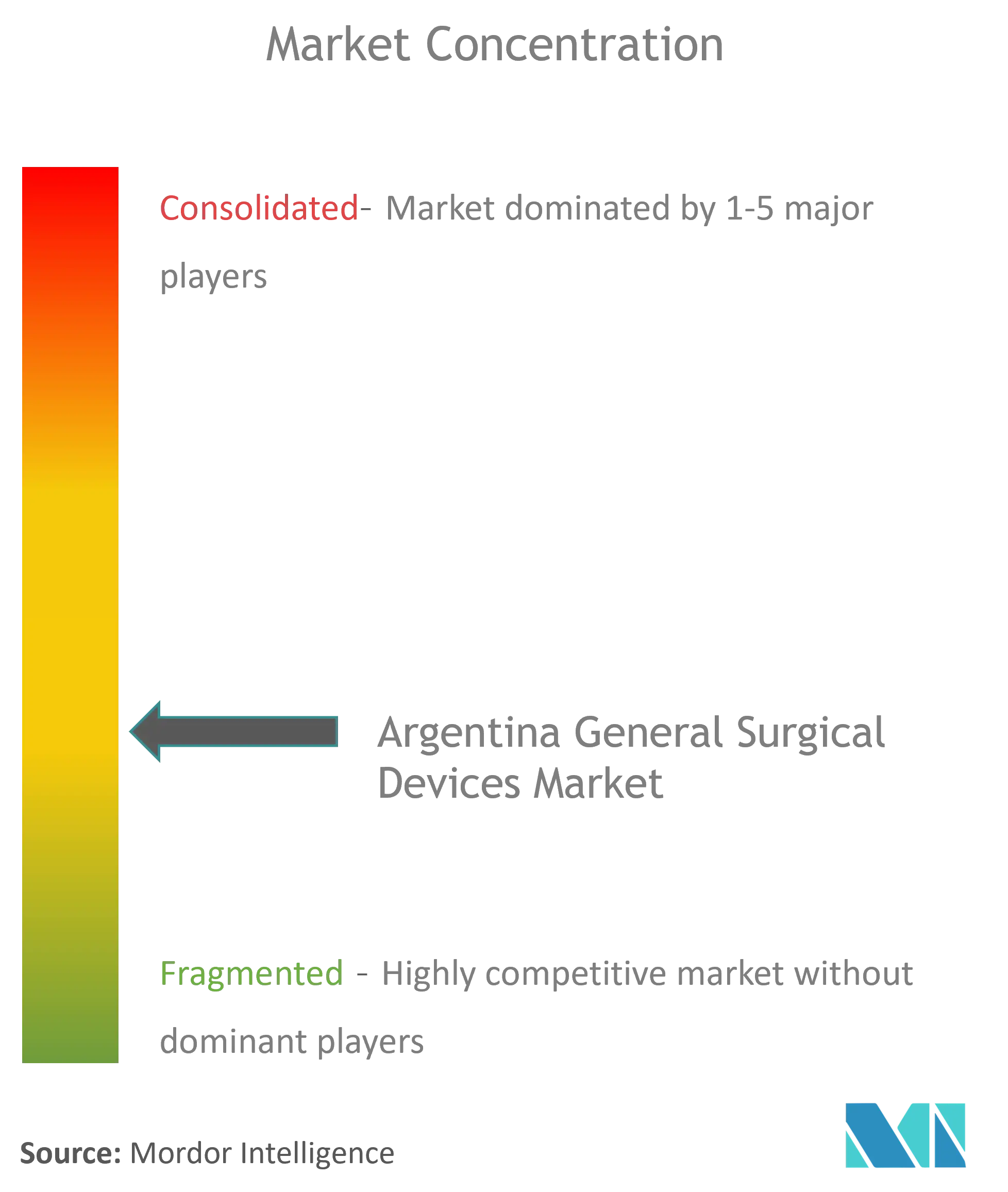

Competitive Landscape

The market is moderately fragmented, with Johnson & Johnson, Medtronic, and Stryker leveraging broad catalogs and post-sale field teams. Johnson & Johnson’s USD 1.3 billion commitment to surgical instruments, part of a wider USD 148.07 billion medtech program, enables continuous pipeline renewal. Medtronic concentrates on energy and stapling innovations, while Stryker capitalizes on a track record of targeted acquisitions that fill adjacent gaps in its trauma and power-tool lines.

Mid-tier contenders, including Karl Storz and Getinge, expand through selective M&A Karl Storz’s 2024 purchase of Asensus Surgical broadens its robotic options. Local distributors remain vital, bridging ANMAT filing nuances and servicing rural provinces. These dynamics position firms that fuse regulatory acumen with adaptive pricing to capture incremental share in the Argentina general surgical devices market.

Price competition is tempered by value-added services such as on-site instrument repair and bilingual user training. Currency hedging skills also shape vendor credibility, because delayed deliveries tied to foreign-exchange shortages can erode surgeon loyalty. Technology licensing with domestic assemblers is rising, though true local manufacturing still skews to basic forceps and retractors. Over the forecast period, strategic alliances that pair global R&D with regional brand recognition are likely to unlock the next wave of volume expansion across the Argentina general surgical devices industry.

Argentina General Surgical Devices Industry Leaders

B. Braun SE

Boston Scientific Corporation

Johnson & Johnson (Ethicon, DePuy Synthes)

Medtronic PLC

Stryker Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity centers on high-volume, low-to-mid risk surgical categories where imports dominate and administrative steps have been streamlined. With Disposicion 4446/2025 (effective August 6, 2025) replacing per-shipment import authorizations for Class I and II products with sworn-statement notifications, suppliers and distributors can prioritize consignment programs and faster replenishment cycles for laparoscopic trocars, access systems, wound-closure products, and core handheld instruments that support the countrys minimally invasive surgery mix.

A second opportunity involves expanding technology-enabled surgery beyond the largest private centers, supported by visible public-sector capability moves and a thin installed base. Public institutions such as Hospital Escuela de Agudos Dr. Ramon Madariaga (Misiones) have reported activity around advanced surgical robotics programs, which provides a reference point for broader uptake of compatible general-surgery consumables, instrument reprocessing workflows, and perioperative training packages. At the same time, ANMATs ongoing alignment work with international good regulatory practices, including IMDRF-linked essential principles and cybersecurity direction for software-reliant devices, creates room for suppliers to operationalize Spanish-language documentation, software bill of materials discipline, and post-market surveillance routines through local authorized representatives.

Recent Industry Developments

- July 2026: ANMAT advanced its 2025-2026 shift toward simplified medical device import and compliance administration, reinforcing a more digitized, trust-based approach for regulated operators. For general surgical device suppliers, the direction supports shorter administrative cycles for routine, lower-risk product flows and places more weight on local post-market and traceability discipline managed by the in-country importer.

- August 2025: ANMAT implemented Disposicion 4446/2025, replacing per-shipment import authorizations for Class I and II medical devices with an online sworn-statement notification process (commonly cited as a 48-hour notification window). This change directly affects high-volume surgical categories that are import-dependent, improving replenishment cadence for distributors servicing hospitals and ambulatory surgical centers.

- March 2024: MicroPort NeuroTech completed the first commercial implantation of its Tubridge flow diverter in Argentina. The milestone indicates continued openness among leading centers to adopt new interventional and surgical technologies, supporting broader demand for specialized procedural kits, adjunct devices, and vendor-backed clinical training.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Argentina general surgical devices market covers the value of devices used in surgical procedures across hospitals and outpatient settings in Argentina, counted at the point of sale into the healthcare system and reported in USD.

Scope exclusions: We exclude capital imaging, anesthesia and monitoring equipment, implants, and hospital room infrastructure that are not purchased as general surgical devices.

Segmentation Overview

- By Product

- Handheld Devices

- Laparoscopic Devices

- Electrosurgical Devices

- Wound-Closure Devices

- Trocars and Access Systems

- Robotic and Computer-Assisted Systems

- Other Devices

- By Procedure Approach

- Open Surgery

- Minimally Invasive Surgery

- By Application

- Gynecology and Urology

- Cardiology and Cardiothoracic

- Orthopedic

- Neurology and Spine

- Other Applications

- By End-user

- Hospitals

- Ambulatory Surgical Centres

- Specialty Clinics

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with defining what is treated as a general surgical device and how it is used through Argentina's hospital and outpatient pathways. We focused on import dependency and pricing volatility, since both can distort simple comparisons across years. We used public sources such as Argentina customs trade statistics, Ministry of Health publications, ANMAT regulatory notices, World Bank macro series, and peer reviewed clinical and health economics journals to map procedure volumes and procurement patterns.

We then checked company filings, investor presentations, distributor catalogs, association websites, and reputable press coverage to understand shifts in product mix, including growth in minimally invasive procedures and energy device adoption. In parallel, paid subscriptions for company financials and news, plus an import export shipment level database, were used selectively to validate supplier presence, pricing direction, and the timing of demand swings. The desk sources listed here are illustrative only, and many other sources were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary interviews and surveys were used to test device scope, typical selling prices, and channel markups that are not consistently visible in public data. We spoke with a balanced mix of manufacturers, importers, distributors, hospital procurement teams, surgeons, and clinic administrators across major Argentine demand centers, then used follow up calls when desk signals and field inputs did not align.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | |

| Mid tier: 46% | Functional/Unit leaders: 31% | |

| Smaller Players: 16% | Managers: 57% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up flow that stays practical for Argentina. First, the top-down side rebuilt the demand pool from surgical procedure volumes by setting, procedure mix shifts (open versus minimally invasive), and per procedure device utilization assumptions, which were then converted into value using typical price bands observed in tenders and distributor quotations.

To keep the totals realistic, selective bottom-up checks were added through supplier and channel roll ups for a sampled basket, including handheld instruments, laparoscopic access devices (trocars), electrosurgical units and accessories, and wound closure products. Where coverage gaps appeared, we filled them using proxy ratios from comparable institutions and then adjusted them after expert review so that outliers did not inflate the national total.

Forecasts were produced using scenario analysis supported by a simple multivariate regression view of key drivers, including expected surgery volumes, hospital budget cycles, exchange rate pressure on imported devices, replacement cycles for powered and energy devices, and adoption pace for minimally invasive approaches. Assumptions were finalized only after they matched the direction and magnitude shared by interviewees who actively price and procure these products.

Data Validation & Update Cycle

Model outputs were cross checked against independent signals such as import trends for relevant HS codes, public procurement activity patterns, and hospital utilization commentary to confirm that growth did not outrun observable demand. Large variances were investigated, and if the cause could not be explained through a clear market change, the assumptions were revisited and respondents were re contacted.

Before sign off, the work goes through multiple analyst reviews that focus on logic checks, unit consistency, and year on year reasonableness by device group. Reports are refreshed annually, and interim updates are made when major regulatory changes, currency shocks, or procurement disruptions materially shift pricing or volumes. Right before delivery, we do a final pass to ensure the latest public indicators are reflected.

Mordor Intelligence's Argentina General Surgical Devices Market Estimate Compared With Other Published Estimates

Published market sizes for Argentina general surgical devices can differ even when the titles look similar, because the counted products, the year chosen, and the way prices are normalized are rarely the same. We have found the biggest drivers to be scope creep into broader medical devices, differences in how imported product pricing is converted into USD, and whether procedure volumes are used to sanity check revenue totals.

Some external estimates expand the scope into a wider surgery equipment pool and also apply forward prices to a near term year, which pushes the number up quickly. Mordor Intelligence counts only general surgical devices (such as handheld, laparoscopic, electrosurgical, wound closure, and access devices) and keeps the base year anchored to 2025 pricing and utilization checks before forecasting forward.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 224.71 M (2025) | |

| Industry Publisher A | USD 482.50 M (2026) | Uses a later year and a broader inclusion set that appears to mix general surgical devices with adjacent operating room and minimally invasive equipment, and then applies higher assumed average selling prices without clear procedure based cross checks. |

| Regional Research House B | USD 410.00 M (2025) | Often aggregates wider medical device revenue linked to surgery and assumes an average growth uplift for imports, which can overstate value when currency conversion timing and distributor margins are not normalized for Argentina. |

The spread across published figures is mainly explained by what gets counted as a surgical device set, plus the year and FX timing used to express pricing in USD. By tying the market to procedure driven demand and then confirming value with targeted supplier and channel checks, the estimate stays traceable to clear inputs that can be repeated and updated.

Key Questions Answered in the Report

What is the current value of the Argentina general surgical devices market?

It stands at USD 238.28 million in 2026 and is projected to reach USD 319.37 million by 2031.

Which product category leads the Argentina general surgical devices market?

Handheld devices hold the largest share at 33.12% in 2025, driven by their universal use across specialties.

How dominant is minimally invasive surgery in Argentina?

Minimally invasive procedures represent 70.05% of the market and are growing at a 7.18% CAGR through 2031.

Which end-user segment is expanding fastest?

Ambulatory surgical centers post the quickest growth, with an 7.62% CAGR expected to 2031.

What are the main hurdles for foreign device manufacturers?

Extended ANMAT approval timelines of up to 15 months and currency volatility that complicates import financing.

Page last updated on: