Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

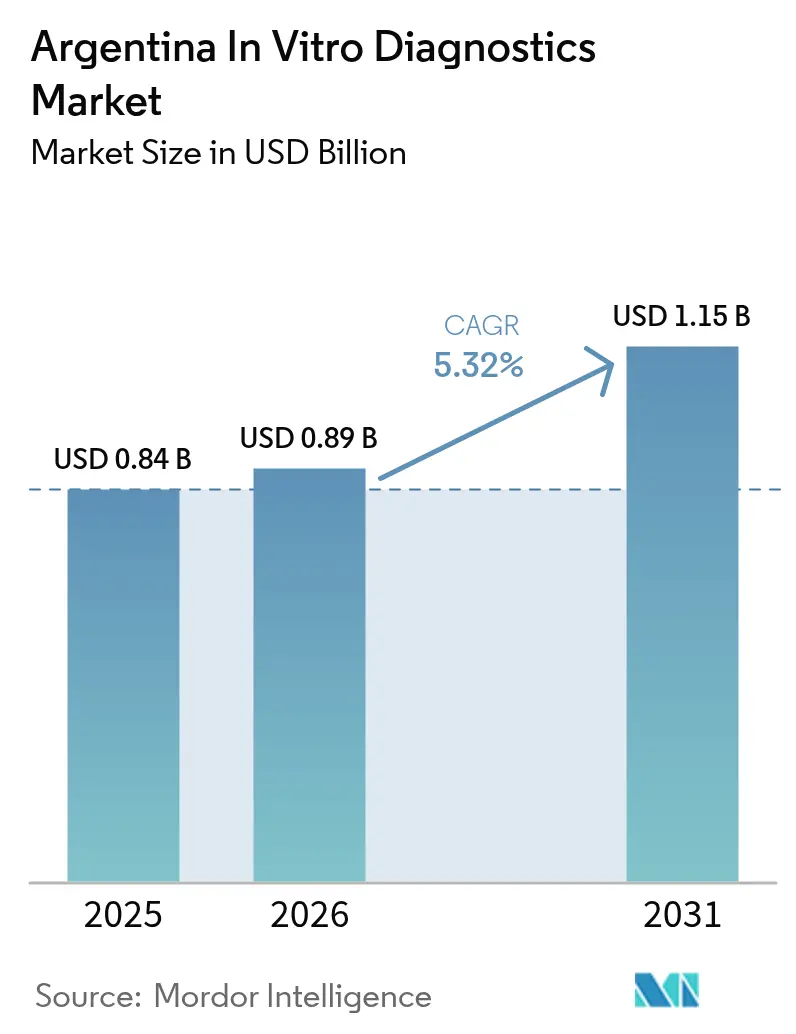

| Base Year Market Size (2025) | USD 0.84 Billion |

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.15 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

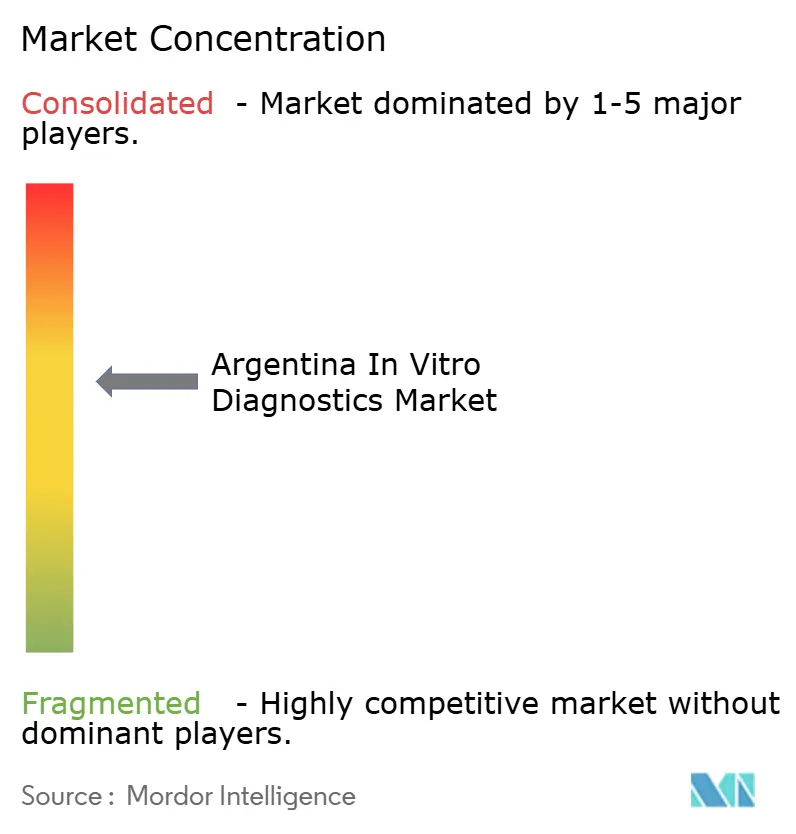

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina In Vitro Diagnostics Market Analysis by Mordor Intelligence

Argentina in vitro diagnostics market size in 2026 is estimated at USD 0.89 billion, growing from 2025 value of USD 0.84 billion with 2031 projections showing USD 1.15 billion, growing at 5.32% CAGR over 2026-2031. Rising chronic disease prevalence, wider private insurance uptake and public-sector lab upgrades are the primary engines of growth. Currency volatility, however, continues to raise the landed cost of imported analyzers and consumables, prompting hospitals to explore locally made reagents. Precision-medicine programs are stimulating demand for molecular assays, while mandatory e-prescriptions effective January 2025 link test data directly to clinical workflows. Opportunities also stem from point-of-care platforms that extend diagnostics into remote provinces.

Key Report Takeaways

- By test type, Clinical Chemistry led with 27.62% of Argentina in vitro diagnostics market share in 2025, while Molecular Diagnostics is projected to grow at a 8.92% CAGR through 2031.

- By product category, Reagents & Consumables accounted for 66.45% share of the Argentina in vitro diagnostics market size in 2025; Software & Services is anticipated to expand at a 10.42% CAGR to 2031.

- By technology, ELISA/CLIA methods held 36.55% Argentina in vitro diagnostics market share in 2025, whereas NGS Panels are forecast to rise at an 11.23% CAGR over the same period.

- By end user, Diagnostic Reference Laboratories commanded 50.35% share of the Argentina in vitro diagnostics market size in 2025; Point-of-Care settings exhibit the fastest growth at 9.86% CAGR to 2031.

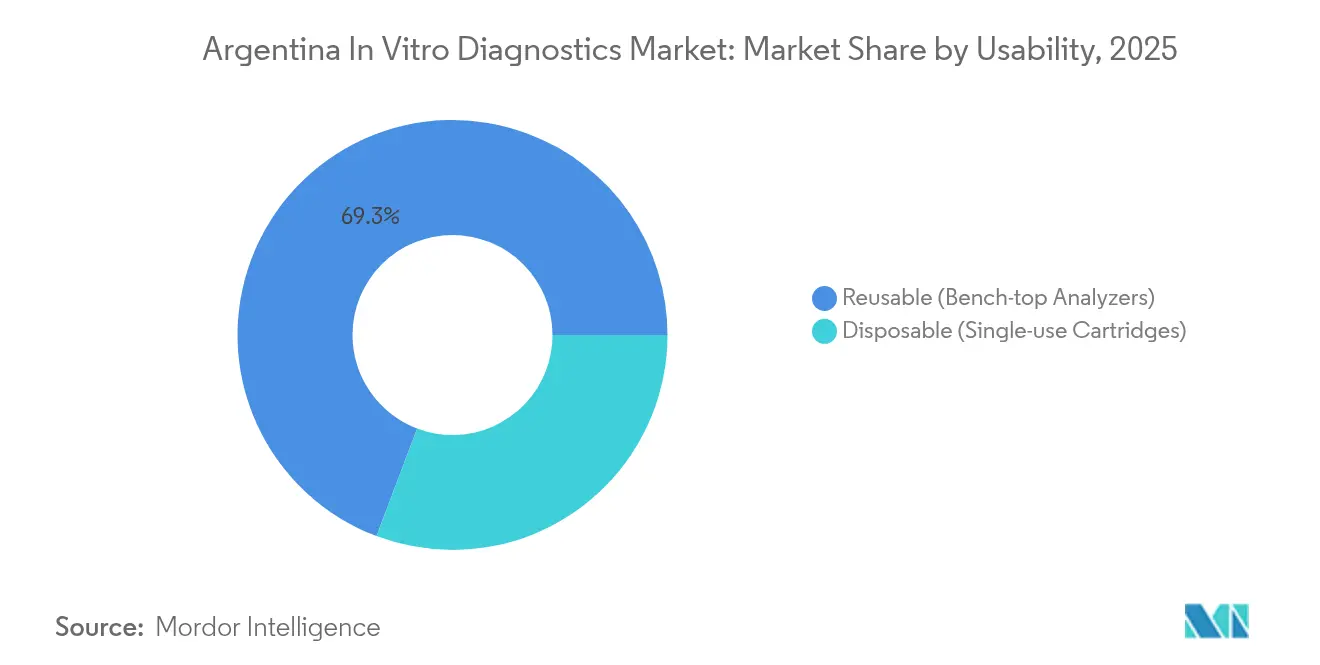

- By usability, Reusable Analyzers led with 69.25% of Argentina in vitro diagnostics market share in 2025; Disposable Cartridges are projected to expand at a 10.08% CAGR through 2031.

- By application, Infectious Diseases accounted for 32.60% share of the Argentina in vitro diagnostics market size in 2025, while Oncology/Cancer Biomarkers are advancing at a 9.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina In Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Burden of chronic & infectious diseases | +1.8% | Buenos Aires, Córdoba, Mendoza | Long term (≥ 4 years) |

| Government modernization of public laboratories & reimbursement | +1.2% | Urban centers | Medium term (2-4 years) |

| Expansion of private health insurance | +0.9% | Buenos Aires Metropolitan Area | Medium term (2-4 years) |

| Local reagent manufacturing initiatives | +0.7% | Industrial hubs nationwide | Long term (≥ 4 years) |

| Shift toward point-of-care testing in underserved provinces | +0.5% | Northwestern & northeastern provinces | Short term (≤ 2 years) |

| Post-COVID Acceleration of Molecular & Immunoassay Platform Adoption | +0.8% | National, with concentration in major cities and teaching hospitals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Burden of Chronic & Infectious Diseases Boosting Diagnostic Demand

Non-communicable diseases account for 78% of Argentina’s disease burden, and cardiovascular ailments alone cause 30% of annual deaths[1]Thomas Gaziano, “Project Details – NIH RePORTER,” National Institutes of Health, nih.gov. High mortality from chronic kidney disease, with an age-standardized rate of 9.2 per 100,000, underscores the need for earlier testing. Hospitals are therefore investing in biomarker and molecular panels that shorten therapeutic decision times. Expanded HIV and STI screening programs further lift reagent volumes. Together these factors underpin steady unit growth across the Argentina in vitro diagnostics market.

Government Modernization of Public Laboratories & Test Reimbursement

The National Digital Health Strategy promotes interoperable lab information systems, while Programa Sumar ties provincial funding to performance indicators[2]Transform Health Coalition, “Country-Specific Fact Sheet: Argentina,” transformhealthcoalition.org. SENASA’s expanded laboratory network improves nationwide sample logistics. These actions stimulate procurement of analyzers compatible with electronic prescription workflows, accelerating data-driven diagnostics in the Argentina in vitro diagnostics market.

Expansion of Private Health Insurance

Private insurers now cover a widening range of preventive screens, creating a discerning customer base keen on high-specificity molecular tests. Regulatory price caps linked to a “health cost index” push payers toward value-based purchasing, favoring platforms with demonstrable clinical impact. Uptake is strongest in Buenos Aires, where higher household incomes support premium policies that reimburse next-generation sequencing.

Shift Toward Point-of-Care Testing in Underserved Provinces

mHealth-enabled POCT initiatives improve cardiovascular screening adherence in Jujuy, Misiones and Salta provinces through the PRIMECare trial. Portable lateral-flow assays allow same-visit treatment decisions where central labs are distant. This decentralization accelerates result turnaround and elevates test volumes for manufacturers with rugged cartridge platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility elevating import costs | -1.5% | Nationwide | Medium term (2-4 years) |

| Fragmented provincial procurement hindering volume-based pricing | -0.8% | Smaller provinces | Long term (≥ 4 years) |

| Shortage of Skilled Laboratory Workforce Outside Major Urban Centers | -0.6% | Rural provinces and secondary cities | Long term (≥ 4 years) |

| Extended ANMAT Approval Cycles Delaying Market Entry | -0.7% | National, with heightened impact on innovative technologies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility Elevating Import Costs for Instruments & Consumables

Multiple exchange rates and capital controls lift the peso cost of imported analyzers, forcing providers to delay upgrades. Even as the federal budget posted a primary surplus in 2024, recurrent devaluation inflated reagent invoices by double digits[3]OECD, “OECD Economic Outlook 2024 Issue 2: Argentina,” oecd.org. Vendors often denominate quotes in USD, adding hedging surcharges that compress hospital margins and slow high-end segment adoption inside the Argentina in vitro diagnostics market.

Fragmented Provincial Procurement Hindering Volume-based Pricing

Argentina’s 24 provinces run independent tender cycles that prevent pooled purchasing power. Studies in Mendoza show 19.7% of adults reporting unmet care needs attributable to administrative inefficiencies. Smaller jurisdictions thus pay higher unit prices for assays, widening access gaps between urban centers and remote districts. Limited batch sizes also deter suppliers from holding local inventory, elongating lead times.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Gaining Speed

Clinical Chemistry generated 27.62% of Argentina in vitro diagnostics market share in 2025 on the back of high-volume lipid, renal and liver panels used for chronic disease monitoring. Routine deployment across public and private labs ensures predictable reagent pull-through. Yet reimbursement ceilings cap price escalation, prompting vendors to focus on reagent stability to protect margins. Immunodiagnostics maintains traction in HIV and hepatitis screening, where algorithmic confirmatory testing drives repeat orders.

Molecular Diagnostics is forecast to post a 8.92% CAGR, the swiftest within the Argentina in vitro diagnostics market. COVID era capacity remains in place, repurposed toward oncogenic mutation detection and multi-pathogen respiratory panels. Laboratories in Buenos Aires and Córdoba are validating liquid biopsy workflows despite staffing gaps that slow nationwide rollout. The segment’s rise signals a long-term tilt toward precision medicine, though test affordability remains a hurdle away from major metros.

By Product: Software & Services Accelerating Connectivity

Reagents & Consumables delivered 66.45% of Argentina in vitro diagnostics market size in 2025 due to the consumable nature of chemistry, immunoassay and PCR workflows. Currency swings have made single-source contracts desirable, pushing health systems to cultivate local suppliers. The emergent domestic reagent consortium, backed by academic know-how, is shortening lead times and stabilizing kit pricing for provincial hospitals.

Software & Services is projected to grow 10.42% per year as e-prescription mandates drive adoption of lab information systems. Middleware that consolidates analyzer outputs into clinical records elevates data integrity and meets audit requirements. Vendors offering turnkey integration with hospital EMR suites enjoy an early-mover edge in the Argentina in vitro diagnostics market, particularly where cloud connectivity is feasible.

By Technology: NGS Panels Driving Genomic Profiling

ELISA/CLIA procedures still accounted for 36.55% of revenue in 2025, owing to versatility in hormone, autoimmune and pathogen testing. Advances such as magnetic-bead separation and nanostructured surfaces have raised assay sensitivity, extending platform relevance. Real-time PCR retains dominance in viral load monitoring given its lower capital threshold versus sequencing.

NGS Panels are set to register an 11.23% CAGR and will expand Argentina in vitro diagnostics market size through broader oncology panels reimbursed by private insurers. Laboratories are piloting hereditary cancer panels that consolidate multiple genes into one run, reducing per-sample cost. However, skill shortages outside Buenos Aires hinder uniform adoption, and reimbursement codes are still evolving.

By Usability: Disposable Cartridges Extending Reach

Reusable analyzers comprised 69.25% of 2025 instrument placements, leveraging throughput economies in central labs. Their upgrade cycle, typically seven to 10 years, shields suppliers from short-term shocks. Preventive maintenance packages are bundled to keep uptime above 95%, a contractual metric demanded by tertiary hospitals.

Disposable cartridge systems are forecast to grow 10.08% annually, supported by public-health projects delivering rapid tests at primary-care posts. Cardiovascular and renal panels packaged into sealed microfluidic chips simplify training, vital in regions lacking specialist technologists. Field studies with hantavirus antibody strips further demonstrate cartridge versatility.

By Application: Oncology Biomarkers Outpacing Growth

Infectious disease assays held 32.60% revenue in 2025 as Argentina sustained HIV, dengue and Chagas surveillance programs. Ministries procure combined ELISA and rapid tests to widen screening breadth, reinforcing steady reagent demand. Diabetes testing adds a sizable share, mirrored by escalating type 2 prevalence among adults.

Oncology biomarkers are projected to expand at a 9.05% CAGR, the fastest within the Argentina in vitro diagnostics industry. Precision-oncology clinics order comprehensive genomic profiles to tailor targeted therapies, with private payers reimbursing companion diagnostics. Public coverage remains limited, pushing manufacturers to craft tiered panel offerings to suit diverse budgets.

By End User: Point-of-Care Settings Gathering Momentum

Diagnostic reference laboratories captured 50.35% of Argentina in vitro diagnostics market size during 2025 principally through consolidated sample volumes and specialized test menus. Their long-term agreements with managed-care organizations guarantee reagent throughput, though staff attrition in secondary cities threatens turnaround-time targets.

Point-of-care environments are poised for 9.86% CAGR growth as handheld analyzers reach pharmacies, ambulatory clinics and mobile units. The PRIMECare intervention couples Bluetooth-enabled cholesterol meters with teleconsults, illustrating how integrated workflows can raise screening adherence in remote towns.

Geography Analysis

Buenos Aires Metropolitan Area accounted for roughly 39.45% of national test volumes thanks to high insurance coverage and a dense network of tertiary hospitals. Reference labs here run 24/7 sequencing hubs, making the region the early adopter of NGS oncology panels despite elevated import costs. Provincial governments depend on capital-city logistics corridors that expedite reagent distribution.

Central provinces of Córdoba, Santa Fe and Mendoza form the second cluster of demand. Regional nephrology clinics rely heavily on chemistry and immunoassay panels to monitor chronic kidney disease, an area with a 9.2 per 100,000 mortality footprint. Digital-health pilots using cloud LIS platforms demonstrate how the Argentina in vitro diagnostics market can address distance barriers between secondary cities and rural catchments.

Northwestern and northeastern provinces remain under-served. Limited centrifuge infrastructure and shortages of laboratory technologists constrain routine testing capacity. Pilot programs distribute portable lateral-flow kits for dengue and leptospirosis, bridging gaps until fixed labs are upgraded. Conditional transfers under Programa Sumar incentivize these provinces to expand basic chemistry services, yet procurement fragmentation keeps analyzer prices elevated.

Regulatory Landscape

In Argentina, in vitro diagnostics (IVDs) are regulated by ANMAT (Administracion Nacional de Medicamentos, Alimentos y Tecnologia Medica) under the Ministry of Health, with core medical device/IVD regulatory frameworks anchored in Disposicion ANMAT 2674/1999 and subsequent updates such as Disposicion 7425/2013 that references MERCOSUR technical requirements. Market access typically requires local establishment authorization for manufacturers and importers, evidence of Good Manufacturing Practices (BPF), and a local Authorized Representative for foreign manufacturers to submit and maintain regulatory compliance.

ANMAT has expanded electronic processes for submissions and lifecycle management, with HELENA used as the official electronic registration channel for IVD products (notably in lower-risk groups) and related medical devices, while THEMIS supports simplified declarations for low-risk medical device establishments. Registrations are time-bound (commonly five years) and require renewal or revalidation, which makes regulatory planning and local regulatory operations a practical differentiator, particularly for imported analyzers and higher-complexity assays where market participants cite approval cycles as a constraint.

Competitive Landscape

The Argentina in vitro diagnostics market is moderately concentrated. Multinationals such as Abbott, Roche and Siemens Healthineers command the bulk of high-end instrument placements, leveraging nationwide distributor footprints and service depots. Their strategy centers on reagent-rental contracts that preserve long-term customer lock-in despite peso volatility.

Local biotechnology firms are scaling reagent production, with 340 companies active by 2023 and revenues of USD 3.75 billion. Partnerships between public labs and private developers accelerate tech-transfer of ELISA kits for endemic diseases. BD’s decision to spin off its Biosciences and Diagnostic Solutions business marks a global move toward more focused portfolios, hinting at potential distribution realignments in Argentina.

Competitive advantage is tilting toward integrated ecosystems that link analyzers, middleware and decision-support modules. Vendors embedding regulatory reporting templates for ANMAT’s updated import fee structure position themselves as compliance partners rather than mere suppliers, an increasingly important distinction amid evolving trade rules.

Argentina In Vitro Diagnostics Industry Leaders

Danaher Corporation

Bio-Rad Laboratories Inc.

BioMérieux

F. Hoffmann-La Roche Ltd.

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities in Argentina are closely tied to two visible shifts in market infrastructure: digital health integration and improvements in regulatory throughput. The mandatory e-prescription environment effective January 2025 and the National Digital Health Strategy create whitespace for middleware, LIS connectivity, and cybersecurity-aware data pathways that connect analyzers, reference labs, and providers. This reinforcement supports faster growth in the Software and Services layer within IVD procurement. On the supply side, the push toward local reagent manufacturing, including formal collaboration networks supporting domestic reagent production, creates room for locally produced, high-rotation kits in clinical chemistry and immunoassay workflows, where import-cost volatility pressures hospital budgets.

A second opportunity cluster focuses on expanding test menus beyond major metros using point-of-care platforms and reducing training burdens in underserved provinces (northwest and northeast). This builds on programs and pilots that deploy portable tests and mHealth-enabled screening workflows, such as the PRIMECare-linked approach cited for remote provinces. Regulatory modernization also improves commercialization cadence: ANMATs use of digital submission workflows (HELENA) and simplified pathways for lower-risk device groups create a clearer lane for manufacturers to broaden portfolios in routine IVD categories. At the same time, the smaller pool of higher-risk IVD registrations highlights whitespace for firms prepared to carry the heavier technical dossier and clinical evidence burden for molecular assays and oncology-linked companion diagnostics.

Recent Industry Developments

- June 2026: ANMAT activity indicators referenced publicly highlighted high-volume processing of medical device registration procedures year-to-date, reflecting a more industrialized submission and review workflow supported by digital systems such as HELENA. Higher regulatory throughput reduces the operational risk around launch timing for routine IVD categories and can accelerate catalog expansion by distributors and local representatives.

- March 2025: Argentinas biotech sector reported 340 companies generating USD 3.75 billion in product revenue, including molecular diagnostic kits and ELISA assays. The scale of the local biotech base strengthens the vendor ecosystem for locally produced reagents and supports hospital strategies that diversify supply away from fully imported consumables during currency swings.

- April 2024: ANMAT updated import fee schedules for medical products, including IVDs, introducing a progressive structure aligned with technological complexity. The change directly affected the cost-to-import for higher-complexity instruments and assays, reinforcing procurement interest in local reagents and in contracting models that bundle service, consumables, and regulatory administration.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the value of in vitro diagnostic testing in Argentina, including clinical tests performed on human samples using reagents and consumables, analyzers, and supporting software and related services across care settings.

Scope exclusions: Veterinary diagnostics and research-use-only assays that are not used for clinical decision-making are not counted.

Segmentation Overview

- By Test Type

- Clinical Chemistry

- Immunodiagnostics

- Molecular Diagnostics

- Hematology

- Coagulation & Hemostasis

- Microbiology

- Point-of-Care Lateral Flow

- Other Test Types

- By Product

- Instruments / Analyzers

- Reagents & Consumables

- Software & Services

- By Technology

- ELISA / CLIA

- Real-time PCR & Isothermal NAAT

- NGS Panels

- Microarrays & Lab-on-Chip

- Lateral-Flow Immunoassay

- Flow Cytometry

- By Usability

- Disposable (Single-use Cartridges)

- Reusable (Bench-top Analyzers)

- By Application

- Infectious Diseases

- Diabetes

- Cancer / Oncology Biomarkers

- Cardiology

- Autoimmune & Inflammatory Disorders

- Nephrology

- Blood Screening & Transfusion Safety

- Other Applications

- By End User

- Diagnostic Reference Laboratories

- Hospitals & Clinics

- Point-of-Care Settings (Polyclinics, Ambulances)

- Home & Self-Testing Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the core demand and supply picture for Argentina diagnostics before modeling started, so the inputs are tied to measurable health and trade signals. Public sources such as the World Health Organization, PAHO, the World Bank, Argentina Ministry of Health publications, and peer-reviewed laboratory medicine journals were reviewed to understand testing needs, disease burden, and system capacity.

We also used sources such as customs and trade statistics for IVD-related imports, association and regulator releases where available, plus company filings and investor presentations to sense-check product mix and pricing movement. In areas where public reporting is thin, we selectively used paid subscriptions for company financials and intelligence, along with a shipment-level import-export database, to fill gaps on supplier presence and landed-cost direction. The desk sources referenced here are illustrative only, and other public and secondary sources were also used to support data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what is purchased and used in Argentina, then aligning it with realistic pricing and utilization behavior. Interviews covered importers and distributors, lab managers, hospital procurement teams, and practicing clinicians, with the sample balanced across major urban demand centers and smaller provinces, so the model does not overfit to one buyer type.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 15% | |

| Mid tier: 49% | Functional/Unit leaders: 36% | |

| Smaller Players: 17% | Managers: 49% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build that connects Argentina testing activity to spend per test, then adjusts for the split between public and private settings and for import reliance. The total is corroborated with selective bottom-up checks, mainly using sampled supplier and distributor revenue ranges, reagent pull-through channel checks, and an ASP times volume build for a few high-share test areas.

Key inputs used in the model include expected testing intensity for chronic and infectious conditions, the share of tests moving to point-of-care, analyzer installed-base replacement patterns, reagent-to-instrument spend ratios, and the effect of currency movement on imported kits and consumables. Where bottom-up signals are missing for smaller provinces or niche techniques, we use proxy ratios from similar lab profiles and then re-check them through expert feedback.

For forecasting, scenario analysis is used to reflect different paths for FX stability, public procurement timing, and private lab expansion, and a base case is selected using consensus ranges from interviews. Output growth is also sanity-checked against healthcare utilization direction and expected technology mix shifts in immunoassay and molecular testing.

Data Validation & Update Cycle

Results are validated through triangulation across demand signals, trade indicators, and interview feedback, and then checked for variance at each step so unrealistic jumps are caught early. If the model implies a sudden change in pricing, test intensity, or product mix, the assumption is re-opened, supporting sources are re-read, and experts are re-contacted when needed.

Before sign-off, another analyst reviews the logic, unit conversions, and currency treatment, followed by a final pass to confirm definitions were applied consistently. Reports are refreshed annually, with interim updates when major events materially change pricing, access, or test volumes, so clients receive an updated view close to delivery.

Mordor Intelligence's Vitro Diagnostics Argentina Market Size Compared With Other Published Estimates

It is normal to see different market size numbers for Argentina IVD, since teams do not always count the same items, and they often use different base years and pricing assumptions. The largest gaps usually come from what is included as IVD spending, how imports are translated into local currency values, and whether services and software are treated as part of the market.

Some published figures lean toward a narrower medical-device view that mainly tracks kits and instruments. In Mordor Intelligence's estimate, IVD-related software and services supporting clinical testing are included, while veterinary plus research-use-only assays are kept out. This changes the final total even before forecasting assumptions are applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.84 B (2025) | |

| Global Consultancy A | USD 0.35 B (2023) | Uses an earlier base year and a narrower revenue scope that emphasizes reagent and instrument sales, with limited uplift for software or service components and less explicit currency timing for import-heavy categories. |

| Industry Research Publisher B | USD 0.36 B (2023) | Applies a lower growth path and a smaller counted demand pool, which can happen when point-of-care uptake and private lab expansion are not fully reflected, and when price updates lag inflation and FX effects. |

Overall, the spread across published numbers can be traced back to year choice, scope inclusion, and how pricing is refreshed in a volatile currency environment. By keeping the model tied to clear testing drivers and practical cross-checks on pricing and channel flow, the estimate stays explainable and repeatable for planning use cases.

Key Questions Answered in the Report

What is the current value of the Argentina in vitro diagnostics market?

The market is valued at USD 0.89 billion in 2026 and is expected to reach USD 1.15 billion by 2031.

Which test type is growing the fastest?

Molecular Diagnostics is projected to record a 8.92% CAGR through 2031 as oncology and infectious-disease uses expand.

How is government policy influencing laboratory demand?

Programmes such as the National Digital Health Strategy and Programa Sumar are driving lab modernization and reimbursement, boosting demand for interoperable analyzers and reagents.

Why is local reagent production important?

Domestic manufacturing reduces currency-related import cost spikes and improves supply security, strengthening market resilience.

Which regions show the greatest unmet diagnostic need?

Northwestern and northeastern provinces face limited lab capacity and benefit most from point-of-care testing initiatives.

What technology is advancing precision medicine in Argentina?

Next-generation sequencing panels are rapidly gaining ground, enabling comprehensive genomic profiling for targeted cancer therapy decisions.

Page last updated on: